The Impact of Carbon Emission Trading Policy on Enterprise ESG Performance: Evidence from China

Abstract

:1. Introduction

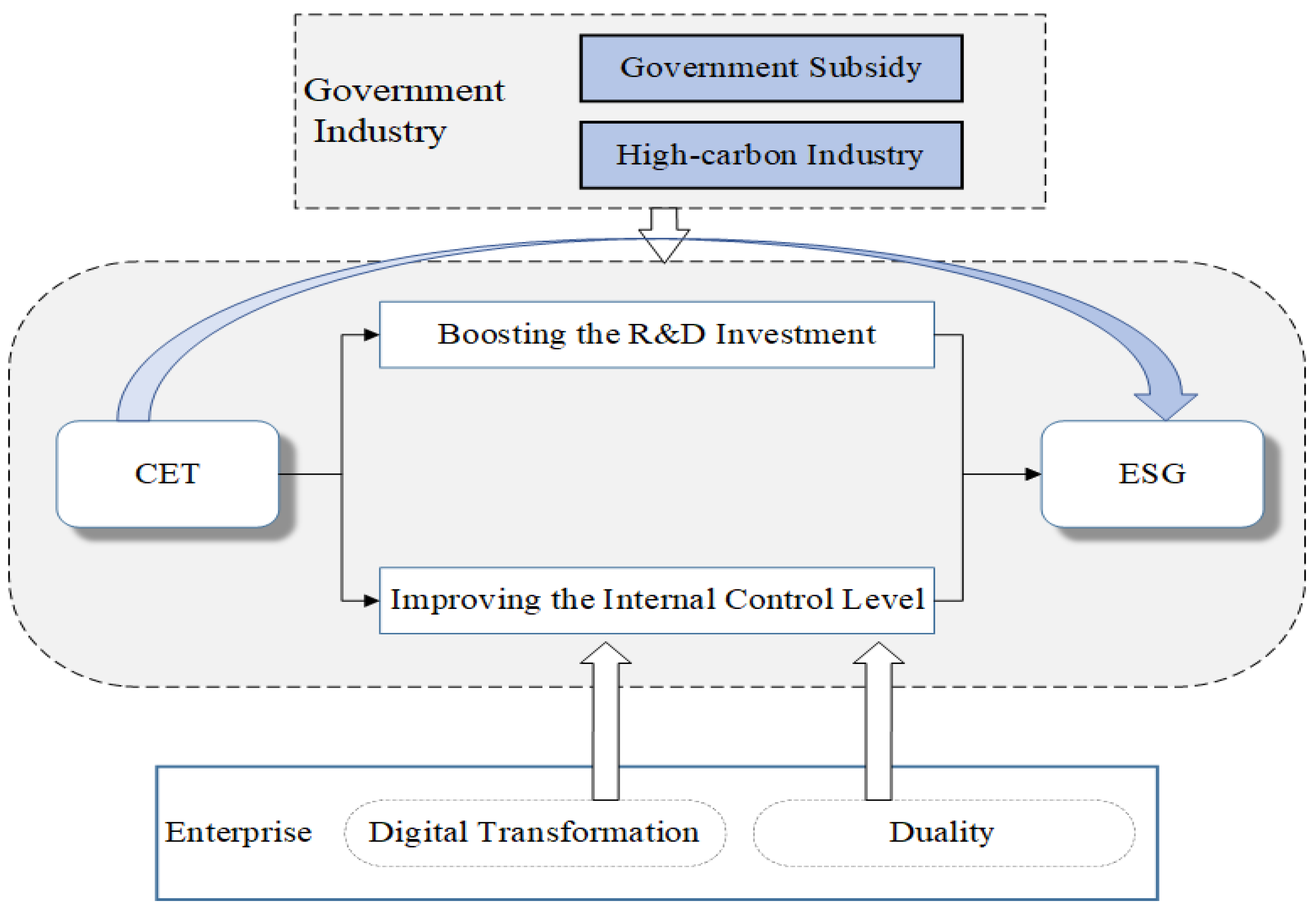

2. Related Research and Hypothesis Development

2.1. The Carbon Emission Trading Policy and Enterprise ESG Performance

2.2. The Mechanism of Corporate R&D Investment

2.3. The Mechanism of Corporate Internal Control Levels

3. Research Design

3.1. Sample and Data

3.2. Variable Definitions

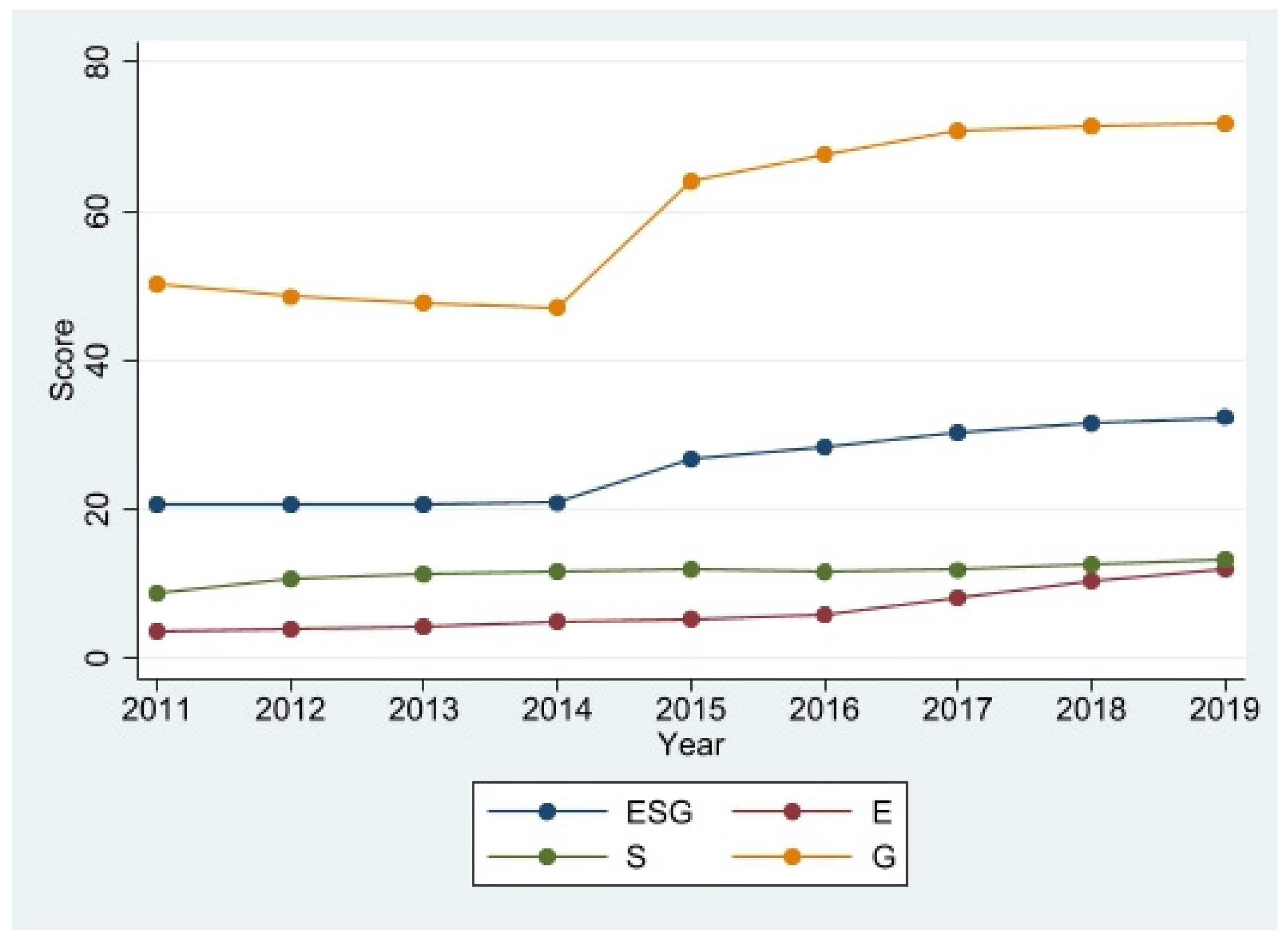

3.2.1. Dependent Variables: ESG Score (ESG)

3.2.2. Independent Variables: Implementation of Carbon Trading Policy Treat_Post (Treat*Post)

3.2.3. Control Variables

3.3. Model Design

3.4. Descriptive Statistics

3.5. Single-Factor Analysis

4. Empirical Results

4.1. Baseline Results

4.2. Robustness Analysis

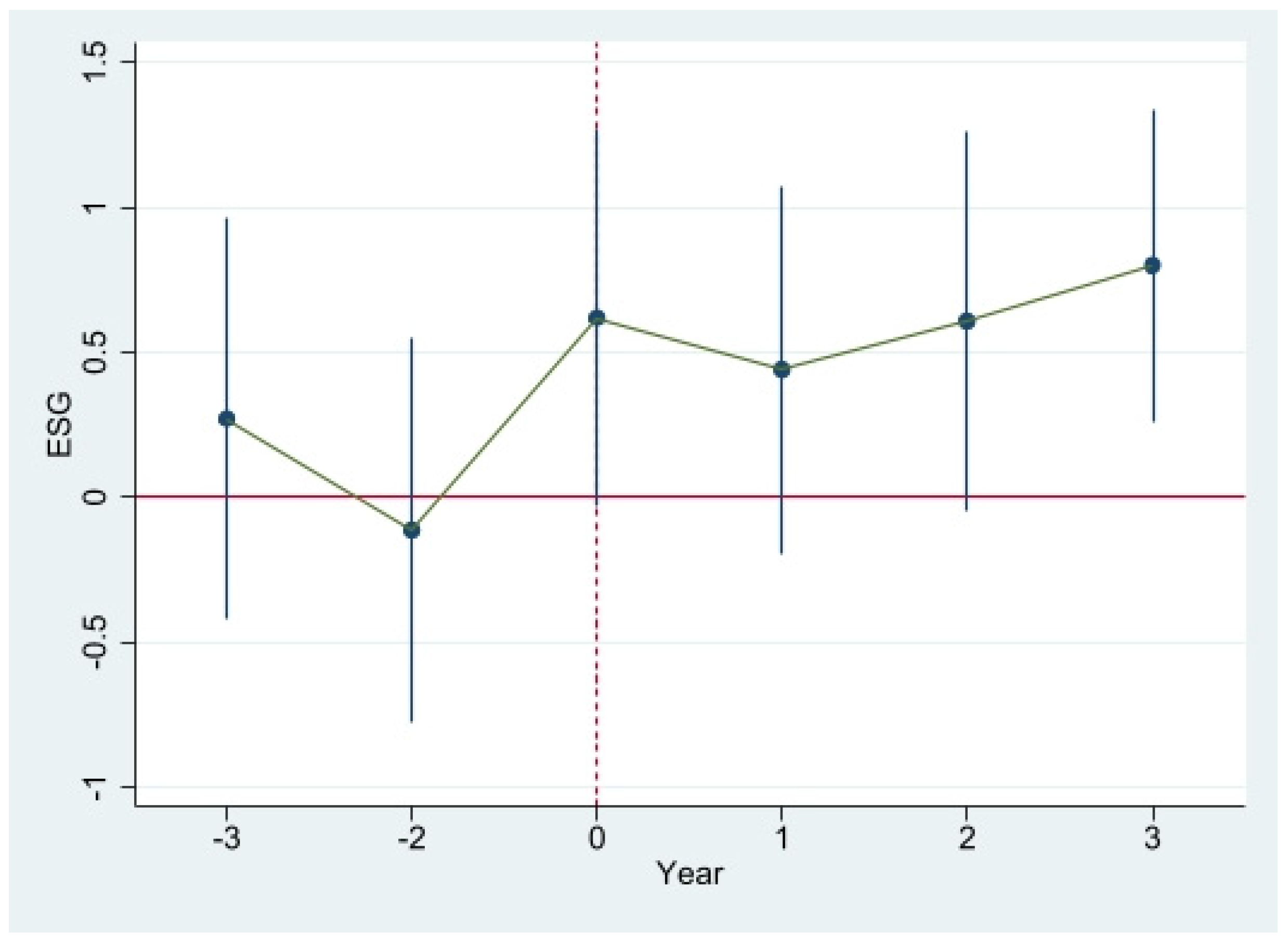

4.2.1. Parallel Trend Test

4.2.2. Exclude Other Policies

4.2.3. Replace Fixed Effect

4.2.4. Heckman Two-Stage Model

4.2.5. Replace the Explained Variables

4.2.6. Subsample Test

4.2.7. PSM-DID

4.2.8. Multi-Period DID

5. Mechanism Analysis

5.1. R&D Investment

5.2. Internal Control Level

6. Heterogeneity Analysis

6.1. Industry

6.2. Duality

6.3. Digital Transformation

6.4. Government Subsidy

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Pillar (Weight) | Subject (Weight) |

|---|---|

| Environmental (33%) | Ecological and Biodiversity Impacts (4.79%) |

| Supply Chain (4.79%) | |

| Water (4.79%) | |

| Air Quality (4.78%) | |

| Materials and Waste (4.74%) | |

| Energy (4.73%) | |

| Climate Change (4.70%) | |

| Social (33%) | Health and Safety (5.58%) |

| Ethics and Compliance (5.57%) | |

| Human Capital (5.55%) | |

| Supply Chain (5.54%) | |

| Community and Customers (5.53%) | |

| Diversity (5.49%) | |

| Governance (33%) | Independence (4.18%) |

| Nominations and Governance Oversight (4.18%) | |

| Sustainability Governance (4.18%) | |

| Tenure (4.18%) | |

| Audit Risk and Oversight (4.17%) | |

| Diversity (4.17%) | |

| Board Composition (4.16%) | |

| Compensation (4.16%) |

References

- Tang, L.; Wu, J.; Yu, L.; Bao, Q. Carbon emissions trading scheme exploration in China: A multi-agent-based model. Energy Policy 2015, 81, 152–169. [Google Scholar] [CrossRef]

- Zhang, Y.-J.; Sun, Y.-F.; Huang, J. Energy efficiency, carbon emission performance, and technology gaps: Evidence from CDM project investment. Energy Policy 2018, 115, 119–130. [Google Scholar] [CrossRef]

- Liu, L.; Chen, C.; Zhao, Y.; Zhao, E. China’s carbon-emissions trading: Overview, challenges and future. Renew. Sustain. Energy Rev. 2015, 49, 254–266. [Google Scholar] [CrossRef]

- Medina, V.; Pardo, Á.; Pascual, R. The timeline of trading frictions in the European carbon market. Energy Econ. 2014, 42, 378–394. [Google Scholar] [CrossRef]

- Wei, Y.; Gong, P.; Zhang, J.; Wang, L. Exploring public opinions on climate change policy in “Big Data Era”—A case study of the European Union Emission Trading System (EU-ETS) based on Twitter. Energy Policy 2021, 158, 112559. [Google Scholar] [CrossRef]

- Lu, Y.; Gao, Y.; Zhang, Y.; Wang, J. Can the green finance policy force the green transformation of high-polluting enterprises? A quasi-natural experiment based on “Green Credit Guidelines”. Energy Econ. 2022, 114, 106265. [Google Scholar] [CrossRef]

- Zhao, X.-G.; Wu, L.; Li, A. Research on the efficiency of carbon trading market in China. Renew. Sustain. Energy Rev. 2017, 79, 1–8. [Google Scholar] [CrossRef]

- Mai, T.-K.; Foley, A.M.; McAleer, M.; Chang, C.-L. Impact of COVID-19 on returns-volatility spillovers in national and regional carbon markets in China. Renew. Sustain. Energy Rev. 2022, 169, 112861. [Google Scholar] [CrossRef]

- Wang, H.; Chen, Z.; Wu, X.; Nie, X. Can a carbon trading system promote the transformation of a low-carbon economy under the framework of the porter hypothesis?—Empirical analysis based on the PSM-DID method. Energy Policy 2019, 129, 930–938. [Google Scholar] [CrossRef]

- Xu, S.; Pan, W.; Wen, D. Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China. Sustainability 2023, 15, 6333. [Google Scholar] [CrossRef]

- Chen, Y.; Xu, Z.; Zhang, Z.; Ye, W.; Yang, Y.; Gong, Z. Does the carbon emission trading scheme boost corporate environmental and financial performance in China? J. Clean. Prod. 2022, 368, 133151. [Google Scholar] [CrossRef]

- Liu, J.-Y.; Zhang, Y.-J. Has carbon emissions trading system promoted non-fossil energy development in China? Appl. Energy 2021, 302, 117613. [Google Scholar] [CrossRef]

- Bu, T.; Du, W.; Tang, C.; Liu, Y.; Wang, X.; Wang, Y.; Tang, D. Market-oriented environmental regulations, employment adjustment and transfer path: Quasi-experimental evidence from China’s carbon emissions trading pilot. J. Clean. Prod. 2022, 369, 133292. [Google Scholar] [CrossRef]

- Yu, P.; Hao, R.; Cai, Z.; Sun, Y.; Zhang, X. Does emission trading system achieve the win-win of carbon emission reduction and financial performance improvement?—Evidence from Chinese A-share listed firms in industrial sector. J. Clean. Prod. 2022, 333, 130121. [Google Scholar] [CrossRef]

- Liu, M.; Zhou, C.; Lu, F.; Hu, X. Impact of the implementation of carbon emission trading on corporate financial performance: Evidence from listed companies in China. PLoS ONE 2021, 16, e0253460. [Google Scholar] [CrossRef]

- Liu, J.; Mao, W.; Qiao, X. Dynamic and asymmetric effects between carbon emission trading, financial uncertainties, and Chinese industry stocks: Evidence from quantile-on-quantile and causality-in-quantiles analysis. N. Am. J. Econ. Financ. 2023, 65, 101883. [Google Scholar] [CrossRef]

- Teixidó, J.; Verde, S.F.; Nicolli, F. The impact of the EU Emissions Trading System on low-carbon technological change: The empirical evidence. Ecol. Econ. 2019, 164, 106347. [Google Scholar] [CrossRef]

- Zhang, W.; Li, G.; Guo, F. Does carbon emissions trading promote green technology innovation in China? Appl. Energy 2022, 315, 119012. [Google Scholar] [CrossRef]

- Zhou, F.; Wang, X. The carbon emissions trading scheme and green technology innovation in China: A new structural economics perspective. Econ. Anal. Policy 2022, 74, 365–381. [Google Scholar] [CrossRef]

- Chen, Z.; Hu, L.; He, X.; Liu, Z.; Chen, D.; Wang, W. Green Financial Reform and Corporate ESG Performance in China: Empirical Evidence from the Green Financial Reform and Innovation Pilot Zone. Int. J. Environ. Res. Public Health 2022, 19, 14981. [Google Scholar] [CrossRef]

- Chen, S.; Han, X.; Zhang, Z.; Zhao, X. ESG investment in China: Doing well by doing good. Pac.-Basin Financ. J. 2023, 77, 101907. [Google Scholar] [CrossRef]

- Liu, M.; Luo, X.; Lu, W.-Z. Public perceptions of environmental, social, and governance (ESG) based on social media data: Evidence from China. J. Clean. Prod. 2023, 387, 135840. [Google Scholar] [CrossRef]

- Tan, Y.; Zhu, Z. The effect of ESG rating events on corporate green innovation in China: The mediating role of financial constraints and managers’ environmental awareness. Technol. Soc. 2022, 68, 101906. [Google Scholar] [CrossRef]

- Naeem, N.; Cankaya, S.; Bildik, R. Does ESG performance affect the financial performance of environmentally sensitive industries? A comparison between emerging and developed markets. Borsa Istanb. Rev. 2022, 22, S128–S140. [Google Scholar] [CrossRef]

- Zeng, L.; Jiang, X. ESG and Corporate Performance: Evidence from Agriculture and Forestry Listed Companies. Sustainability 2023, 15, 6723. [Google Scholar] [CrossRef]

- Sun, X.; Zhou, C.; Gan, Z. Green Finance Policy and ESG Performance: Evidence from Chinese Manufacturing Firms. Sustainability 2023, 15, 6781. [Google Scholar] [CrossRef]

- Zhang, D. Does green finance really inhibit extreme hypocritical ESG risk? A greenwashing perspective exploration. Energy Econ. 2023, 121, 106688. [Google Scholar] [CrossRef]

- Zhou, S.; Rashid, M.H.U.; Mohd. Zobair, S.A.; Sobhani, F.A.; Siddik, A.B. Does ESG Impact Firms’ Sustainability Performance? The Mediating Effect of Innovation Performance. Sustainability 2023, 15, 5586. [Google Scholar] [CrossRef]

- Jang, G.-Y.; Kang, H.-G.; Kim, W. Corporate executives’ incentives and ESG performance. Financ. Res. Lett. 2022, 49, 103187. [Google Scholar] [CrossRef]

- Shu, H.; Tan, W. Does carbon control policy risk affect corporate ESG performance? Econ. Model. 2023, 120, 106148. [Google Scholar] [CrossRef]

- Luo, L.; Tang, Q. The real effects of ESG reporting and GRI standards on carbon mitigation: International evidence. In Business Strategy and the Environment; John Wiley & Sons: Hoboken, NJ, USA, 2022. [Google Scholar] [CrossRef]

- Tang, J.; Wang, X.; Liu, Q. The spillover effect of customers’ ESG to suppliers. Pac.-Basin Financ. J. 2023, 78, 101947. [Google Scholar] [CrossRef]

- Baratta, A.; Cimino, A.; Longo, F.; Solina, V.; Verteramo, S. The Impact of ESG Practices in Industry with a Focus on Carbon Emissions: Insights and Future Perspectives. Sustainability 2023, 15, 6685. [Google Scholar] [CrossRef]

- Xu, H.; Wu, Y. The China Trade Shock and the ESG Performances of US firms. arXiv 2022, arXiv:2201.12402. [Google Scholar] [CrossRef]

- Yao, R.; Fei, Y.; Wang, Z.; Yao, X.; Yang, S. The Impact of China’s ETS on Corporate Green Governance Based on the Perspective of Corporate ESG Performance. Int. J. Environ. Res. Public Health 2023, 20, 2292. [Google Scholar] [CrossRef]

- Zhao, X.; Tao, W.; Ma, X.; Wang, C.; Mentel, G. Exploring the role of environmental regulation on energy security: Contextual findings for sustainable development in Chinese provinces. Gondwana Res. 2023, 116, 113–124. [Google Scholar] [CrossRef]

- Liu, M.; Li, Y. Environmental regulation and green innovation: Evidence from China’s carbon emissions trading policy. Financ. Res. Lett. 2022, 48, 103051. [Google Scholar] [CrossRef]

- Huang, H.; Yi, M. Impacts and mechanisms of heterogeneous environmental regulations on carbon emissions: An empirical research based on DID method. Environ. Impact Assess. Rev. 2023, 99, 107039. [Google Scholar] [CrossRef]

- Hu, J.; Pan, X.; Huang, Q. Quantity or quality? The impacts of environmental regulation on firms’ innovation–Quasi-natural experiment based on China’s carbon emissions trading pilot. Technol. Forecast. Soc. Chang. 2020, 158, 120122. [Google Scholar] [CrossRef]

- Lu, W.; Wu, H.; Yang, S.; Tu, Y.P. Effect of environmental regulation policy synergy on carbon emissions in China under consideration of the mediating role of industrial structure. J. Environ. Manag. 2022, 322, 116053. [Google Scholar] [CrossRef]

- Huang, X.; Tian, P. How does heterogeneous environmental regulation affect net carbon emissions: Spatial and threshold analysis for China. J. Environ. Manag. 2023, 330, 117161. [Google Scholar] [CrossRef]

- Xie, L.; Zhou, Z.; Hui, S. Does environmental regulation improve the structure of power generation technology? Evidence from China’s pilot policy on the carbon emissions trading market(CETM). Technol. Forecast. Soc. Chang. 2022, 176, 121428. [Google Scholar] [CrossRef]

- Ning, B.; Zhang, X.; Liu, X.; Yang, C.; Li, G.; Ma, Q. Allocation of carbon quotas with local differential privacy. Appl. Energy 2022, 326, 119974. [Google Scholar] [CrossRef]

- Zhou, X.; Niu, A.; Lin, C. Optimizing carbon emission forecast for modelling China’s 2030 provincial carbon emission quota allocation. J. Environ. Manag. 2023, 325, 116523. [Google Scholar] [CrossRef] [PubMed]

- Liu, Y.; Liu, S.; Shao, X.; He, Y. Policy spillover effect and action mechanism for environmental rights trading on green innovation: Evidence from China’s carbon emissions trading policy. Renew. Sustain. Energy Rev. 2022, 153, 111779. [Google Scholar] [CrossRef]

- Gu, G.; Zheng, H.; Tong, L.; Dai, Y. Does carbon financial market as an environmental regulation policy tool promote regional energy conservation and emission reduction? Empirical evidence from China. Energy Policy 2022, 163, 112826. [Google Scholar] [CrossRef]

- Jia, Z. What kind of enterprises and residents bear more responsibilities in carbon trading? A step-by-step analysis based on the CGE model. Environ. Impact Assess. Rev. 2023, 98, 106950. [Google Scholar] [CrossRef]

- Niyommaneerat, W.; Suwanteep, K.; Chavalparit, O. Sustainability indicators to achieve a circular economy: A case study of renewable energy and plastic waste recycling corporate social responsibility (CSR) projects in Thailand. J. Clean. Prod. 2023, 391, 136203. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Pinnuck, M.; Richardson, G.D. The Valuation Relevance of Greenhouse Gas Emissions under the European Union Carbon Emissions Trading Scheme. Eur. Account. Rev. 2014, 24, 551–580. [Google Scholar] [CrossRef]

- Yu, X.; Shi, J.; Wan, K.; Chang, T. Carbon trading market policies and corporate environmental performance in China. J. Clean. Prod. 2022, 371, 133683. [Google Scholar] [CrossRef]

- Chen, Y.P.V.; Zhuo, Z.; Huang, Z.; Li, W. Environmental regulation and ESG of SMEs in China: Porter hypothesis re-tested. Sci. Total Environ. 2022, 850, 157967. [Google Scholar] [CrossRef]

- Ni, X.; Jin, Q.; Huang, K. Environmental regulation and the cost of debt: Evidence from the carbon emission trading system pilot in China. Financ. Res. Lett. 2022, 49, 103134. [Google Scholar] [CrossRef]

- Bai, X.; Han, J.; Ma, Y.; Zhang, W. ESG performance, institutional investors’ preference and financing constraints: Empirical evidence from China. Borsa Istanb. Rev. 2022, 22, S157–S168. [Google Scholar] [CrossRef]

- Alam, M.S.; Atif, M.; Chien-Chi, C.; Soytaş, U. Does corporate R&D investment affect firm environmental performance? Evidence from G-6 countries. Energy Econ. 2019, 78, 401–411. [Google Scholar] [CrossRef]

- Hung, K.-P.; Chou, C. The impact of open innovation on firm performance: The moderating effects of internal R&D and environmental turbulence. Technovation 2013, 33, 368–380. [Google Scholar] [CrossRef]

- Zhong, Q.; Han, L.; Jin, J. Do green credit guidelines impact on heavily polluting firms in rent-seeking? Financ. Res. Lett. 2022, 47, 102747. [Google Scholar] [CrossRef]

- He, M.; Zhu, X.; Li, H. How does carbon emissions trading scheme affect steel enterprises’ pollution control performance? A quasi natural experiment from China. Sci. Total Environ. 2023, 858, 159871. [Google Scholar] [CrossRef]

- Huang, P.; Jiao, Y.; Li, S. Impact of internal control quality on the information content of social responsibility reports: A study based on text similarity—Evidence from China. Int. J. Account. Inf. Syst. 2022, 45, 100558. [Google Scholar] [CrossRef]

- Guo, Y.; Guo, Y.; Lai Lan Mo, P.; Zhang, X. Partner-Level internal control opinion shopping and its economic consequences: Evidence from “SOX 404” in an emerging market. J. Account. Public Policy 2023, 2023, 107056. [Google Scholar] [CrossRef]

- Le, H.Q.; Vu, T.P.L.; Do, V.P.A.; Do, A.D. The enduring effect of formalization on firm-level corruption in Vietnam: The mediating role of internal control. Int. Rev. Econ. Financ. 2022, 82, 364–373. [Google Scholar] [CrossRef]

- Yang, L.; Qin, H.; Gan, Q.; Su, J. Internal Control Quality, Enterprise Environmental Protection Investment and Finance Performance: An Empirical Study of China’s A-Share Heavy Pollution Industry. Int. J. Environ. Res. Public Health 2020, 17, 6082. [Google Scholar] [CrossRef]

- Chen, Z.; Xie, G. ESG disclosure and financial performance: Moderating role of ESG investors. Int. Rev. Financ. Anal. 2022, 83, 102291. [Google Scholar] [CrossRef]

- Liu, M.; Shan, Y.; Li, Y. Study on the effect of carbon trading regulation on green innovation and heterogeneity analysis from China. Energy Policy 2022, 171, 113290. [Google Scholar] [CrossRef]

- Chen, Y.; Li, T.; Zeng, Q.; Zhu, B. Effect of ESG performance on the cost of equity capital: Evidence from China. Int. Rev. Econ. Financ. 2023, 83, 348–364. [Google Scholar] [CrossRef]

- Chen, W.; Zhang, L.; Shi, L.; Shao, Y.; Zhou, K. Carbon emissions trading system and investment efficiency: Evidence from China. J. Clean. Prod. 2022, 358, 131782. [Google Scholar] [CrossRef]

- Zhang, H.; Feng, C.; Zhou, X. Going carbon-neutral in China: Does the low-carbon city pilot policy improve carbon emission efficiency? Sustain. Prod. Consum. 2022, 33, 312–329. [Google Scholar] [CrossRef]

- Kostka, G.; Goron, C. From targets to inspections: The issue of fairness in China’s environmental policy implementation. Environ. Politics 2020, 30, 513–537. [Google Scholar] [CrossRef]

- Weng, Z.; Liu, T.; Wu, Y.; Cheng, C. Air quality improvement effect and future contributions of carbon trading pilot programs in China. Energy Policy 2022, 170, 113264. [Google Scholar] [CrossRef]

- Cheng, S.; Fan, W.; Meng, F.; Chen, J.; Liang, S.; Song, M.; Liu, G.; Casazza, M. Potential Role of Fiscal Decentralization on Interprovincial Differences in CO2 Emissions in China. Environ. Sci. Technol. 2021, 55, 813–822. [Google Scholar] [CrossRef]

- Cheng, S.; Wang, P.; Chen, B.; Fan, W. Decoupling and decomposition analysis of CO2 emissions from government spending in China. Energy 2022, 243, 122741. [Google Scholar] [CrossRef]

- Deng, X.; Li, W.; Ren, X. More sustainable, more productive: Evidence from ESG ratings and total factor productivity among listed Chinese firms. Financ. Res. Lett. 2023, 51, 103439. [Google Scholar] [CrossRef]

- He, F.; Du, H.; Yu, B. Corporate ESG performance and manager misconduct: Evidence from China. Int. Rev. Financ. Anal. 2022, 82, 102201. [Google Scholar] [CrossRef]

- He, X.; Jing, Q.-L. The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation. Sustainability 2022, 14, 14946. [Google Scholar] [CrossRef]

- Li, S.; Liu, Q.; Lu, L.; Zheng, K. Green policy and corporate social responsibility: Empirical analysis of the Green Credit Guidelines in China. J. Asian Econ. 2022, 82, 101531. [Google Scholar] [CrossRef]

- Lian, Y.; Ye, T.; Zhang, Y.; Zhang, L. How does corporate ESG performance affect bond credit spreads: Empirical evidence from China. Int. Rev. Econ. Financ. 2023, 85, 352–371. [Google Scholar] [CrossRef]

- Gu, L.; Zhang, H. Stakeholder-oriented corporate investment: A catering perspective. Financ. Res. Lett. 2022, 48, 102863. [Google Scholar] [CrossRef]

- Bissoondoyal-Bheenick, E.; Brooks, R.; Do, H.X. ESG and firm performance: The role of size and media channels. Econ. Model. 2023, 121, 106203. [Google Scholar] [CrossRef]

- Han, G.; Chen, T.; Liu, T. Digital Transformation and Enterprise Capacity Utilization: Empirical Findings from Chinese Manufacturing Enterprises. J. Financ. Econ. 2022, 48, 154–168. [Google Scholar] [CrossRef]

- Tang, M.; Cheng, S.; Guo, W.; Ma, W.; Hu, F. Effects of Carbon Emission Trading on Companies’ Market Value: Evidence from Listed Companies in China. Atmosphere 2022, 13, 240. [Google Scholar] [CrossRef]

- Khan, M.A. ESG disclosure and Firm performance: A bibliometric and meta analysis. Res. Int. Bus. Financ. 2022, 61, 101668. [Google Scholar] [CrossRef]

- Wang, B.Y.; Duan, M.; Liu, G. Does the power gap between a chairman and CEO matter? Evidence from corporate debt financing in China. Pac.-Basin Financ. J. 2021, 65, 101495. [Google Scholar] [CrossRef]

- Zhao, C.Y.; Wang, W.C.; Li, X.S. How Does Digital Transformation Affect the Total Factor Productivity of Enterprises? Financ. Trade Econ. 2021, 42, 114–129. [Google Scholar] [CrossRef]

- Shang, Y.; Raza, S.A.; Huo, Z.; Shahzad, U.; Zhao, X. Does enterprise digital transformation contribute to the carbon emission reduction? Micro-level evidence from China. Int. Rev. Econ. Financ. 2023, 86, 1–13. [Google Scholar] [CrossRef]

- Xu, R.; Shen, Y.; Liu, M.; Li, L.; Xia, X.; Luo, K. Can government subsidies improve innovation performance? Evidence from Chinese listed companies. Econ. Model. 2023, 120, 106151. [Google Scholar] [CrossRef]

- Zhang, D.; Kong, Q. Credit policy, uncertainty, and firm R&D investment: A quasi-natural experiment based on the Green Credit Guidelines. Pac.-Basin Financ. J. 2022, 73, 101751. [Google Scholar] [CrossRef]

| Variable | Definitions |

|---|---|

| ESG | Bloomberg ESG score data |

| Treat | In the case of enterprises that are located in carbon trading pilot areas, the value is 1; otherwise, it is 0 |

| Post | In case the year is 2014 or later, the value is 1; otherwise, it is 0 |

| Treat_Post | The cross-product of Treat and Post |

| Lev | Total assets divided by total liabilities |

| Rib | The ratio of independent directors to the size of the board |

| Roa | The ratio of net profit to total assets |

| Grow | The current period’s operating income minus the previous period’s operating income divided by the previous period’s operating income |

| Ppe | Fixed assets divided by total assets |

| Cash | The ratio of net cash flow from operations to total assets |

| Top1 | The percentage of shares held by the largest shareholder |

| Size | The natural logarithm of total enterprise assets |

| Turnover | The ratio of operating income to total assets |

| Variable | N | Mean | sd | Min | p25 | p50 | p75 | Max |

|---|---|---|---|---|---|---|---|---|

| ESG | 8145 | 26.20 | 7.956 | 6.198 | 20.30 | 25.95 | 30.01 | 65.04 |

| Treat | 8145 | 0.404 | 0.491 | 0 | 0 | 0 | 1 | 1 |

| Post | 8145 | 0.715 | 0.451 | 0 | 0 | 1 | 1 | 1 |

| Lev | 8145 | 0.478 | 0.200 | 0.0500 | 0.324 | 0.490 | 0.633 | 0.894 |

| Rib | 8145 | 37.51 | 5.480 | 33.33 | 33.33 | 36.36 | 41.67 | 57.14 |

| Roa | 8145 | 0.0460 | 0.0570 | −0.252 | 0.0170 | 0.0390 | 0.0740 | 0.194 |

| Grow | 8145 | 0.360 | 0.943 | −0.701 | −0.0310 | 0.123 | 0.398 | 6.766 |

| Ppe | 8145 | 0.234 | 0.179 | 0.00200 | 0.0900 | 0.190 | 0.341 | 0.696 |

| Cash | 8145 | 0.0570 | 0.0690 | −0.162 | 0.0160 | 0.0550 | 0.0990 | 0.243 |

| Top1 | 8145 | 38.36 | 15.90 | 8.770 | 25.67 | 37.26 | 50.19 | 75.10 |

| Size | 8145 | 23.10 | 1.288 | 19.74 | 22.18 | 23.00 | 23.90 | 26.18 |

| Turnover | 8145 | 0.647 | 0.444 | 0.0750 | 0.347 | 0.543 | 0.812 | 2.525 |

| (1) Treat = 0 | (2) Treat = 1 | (1)–(2) | ||||

|---|---|---|---|---|---|---|

| Variables | N1 | Mean1 | N2 | Mean2 | MeanDiff | t-Value |

| ESG | 4851 | 25.48 | 3294 | 27.26 | −1.783 | −9.986 *** |

| Lev | 4851 | 0.474 | 3294 | 0.485 | −0.0110 | −2.534 ** |

| Rib | 4851 | 37.13 | 3294 | 38.06 | −0.934 | −7.577 *** |

| Roa | 4851 | 0.0450 | 3294 | 0.0470 | −0.00200 | −1.677 * |

| Grow | 4851 | 0.321 | 3294 | 0.418 | −0.0970 | −4.553 *** |

| Ppe | 4851 | 0.253 | 3294 | 0.205 | 0.0480 | 11.898 *** |

| Cash | 4851 | 0.0590 | 3294 | 0.0540 | 0.00500 | 3.032 *** |

| Top1 | 4851 | 37.45 | 3294 | 39.69 | −2.234 | −6.237 *** |

| Size | 4851 | 22.98 | 3294 | 23.28 | −0.306 | −10.595 *** |

| Turnover | 4851 | 0.648 | 3294 | 0.644 | 0.00400 | 0.406 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variables | ESG | ESG | ESG | ESG | ESG | ESG |

| Treat_Post | 0.638 *** | 0.615 *** | 1.928 *** | 1.362 *** | 0.662 *** | 0.629 *** |

| (3.580) | (3.435) | (11.538) | (8.798) | (3.697) | (3.495) | |

| Lev | −1.779 *** | −3.733 *** | −1.791 *** | |||

| (−3.157) | (−7.992) | (−3.159) | ||||

| Rib | 0.029 ** | 0.029 ** | 0.030 ** | |||

| (2.391) | (2.507) | (2.396) | ||||

| Roa | 2.983 ** | −3.208 ** | 2.975 ** | |||

| (2.550) | (−2.182) | (2.537) | ||||

| Grow | −0.015 | −0.063 | −0.023 | |||

| (−0.259) | (−0.847) | (−0.393) | ||||

| Ppe | 0.239 | 0.467 | 0.097 | |||

| (0.357) | (0.996) | (0.143) | ||||

| Cash | 0.175 | 4.227 *** | 0.073 | |||

| (0.213) | (3.790) | (0.088) | ||||

| Top1 | 0.017 ** | −0.008 ** | 0.020 ** | |||

| (2.216) | (−1.976) | (2.514) | ||||

| Size | 0.518 *** | 2.312 *** | 0.531 *** | |||

| (3.969) | (35.349) | (4.011) | ||||

| Turnover | −0.328 | 1.157 *** | −0.359 | |||

| (−1.298) | (6.876) | (−1.408) | ||||

| Constant | 25.974 *** | 13.117 *** | 25.636 *** | −27.517 *** | 25.967 *** | 12.786 *** |

| (406.664) | (4.337) | (308.003) | (−19.427) | (405.593) | (4.166) | |

| Observations | 8046 | 8046 | 8144 | 8144 | 8046 | 8046 |

| R-squared | 0.844 | 0.845 | 0.412 | 0.510 | 0.844 | 0.846 |

| Firm FE | YES | YES | NO | NO | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Industry FE | NO | NO | YES | YES | YES | YES |

| (1) | (2) | ||

|---|---|---|---|

| Variables | ESG | Variables | ESG |

| Pre_3 | 0.272 | ||

| (0.771) | |||

| Pre_2 | −0.114 | ||

| (−0.334) | |||

| Current | 0.620 * | ||

| (1.858) | |||

| Post_1 | 0.439 | ||

| (1.354) | |||

| Post_2 | 0.608 * | ||

| (1.828) | |||

| Post_3 | 0.802 *** | ||

| (2.919) | |||

| Treat_Post | 0.632 *** | ||

| (3.514) | |||

| Lev | −1.820 *** | Lev | −1.751 *** |

| (−3.206) | (−3.085) | ||

| Rib | 0.030 ** | Rib | 0.029 ** |

| (2.392) | (2.383) | ||

| Roa | 3.078 *** | Roa | 2.948 ** |

| (2.620) | (2.514) | ||

| Grow | −0.022 | Grow | −0.023 |

| (−0.374) | (−0.403) | ||

| Ppe | 0.110 | Ppe | 0.079 |

| (0.162) | (0.117) | ||

| Cash | 0.056 | Cash | 0.064 |

| (0.068) | (0.078) | ||

| Top1 | 0.534 *** | Top1 | 0.020 ** |

| (4.033) | (2.495) | ||

| Size | 0.020 ** | Size | 0.537 *** |

| (2.556) | (4.056) | ||

| Turnover | −0.335 | Turnover | −0.355 |

| (−1.313) | (−1.393) | ||

| Inspection | 0.047 | ||

| (0.296) | |||

| Pilot | −0.296 | ||

| (−1.594) | |||

| Constant | 12.669 *** | Constant | 12.664 *** |

| (4.125) | (4.125) | ||

| Observations | 8046 | Observations | 8046 |

| R-squared | 0.846 | R−squared | 0.846 |

| Firm FE | YES | Firm FE | YES |

| Year FE | YES | Year FE | YES |

| Industry FE | YES | Industry FE | YES |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variables | ESG | ESG | ESG |

| Treat_Post | 0.688 *** | 0.600 *** | 2.506 * |

| (3.735) | (3.303) | (1.751) | |

| Lev | −2.323 *** | −1.675 *** | −1.967 *** |

| (−4.041) | (−2.910) | (−3.344) | |

| Rib | 0.022 * | 0.032 ** | 0.041 *** |

| (1.803) | (2.554) | (3.233) | |

| Roa | 2.340 ** | 3.128 *** | 3.390 *** |

| (1.963) | (2.662) | (2.830) | |

| Grow | −0.038 | −0.020 | −0.044 |

| (−0.662) | (−0.351) | (−0.752) | |

| Ppe | −0.125 | 0.065 | 0.306 |

| (−0.183) | (0.096) | (0.441) | |

| Cash | 0.157 | −0.076 | 0.114 |

| (0.188) | (−0.092) | (0.136) | |

| Top1 | 0.019 ** | 0.020 *** | 0.024 *** |

| (2.399) | (2.584) | (3.002) | |

| Size | 0.650 *** | 0.525 *** | 0.581 *** |

| (4.837) | (3.907) | (4.234) | |

| Turnover | −0.279 | −0.343 | −0.240 |

| (−1.090) | (−1.343) | (−0.918) | |

| Constant | 22.768 *** | 23.218 *** | 20.662 *** |

| (5.733) | (4.400) | (3.872) | |

| Observations | 8145 | 8145 | 8145 |

| R-squared | 0.854 | 0.848 | 0.855 |

| Firm FE | YES | YES | YES |

| Year FE | YES | YES | YES |

| Industry FE | YES | YES | YES |

| Region FE | NO | YES | YES |

| Year-Industry FE | YES | NO | NO |

| Year-Region FE | NO | NO | YES |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | ESG | ESG | ESG | ESG | ESG |

| Treat_Post | 0.590 *** | 0.041 * | 0.655 ** | 0.555 *** | 0.555 *** |

| (3.273) | (1.829) | (2.068) | (3.029) | (3.071) | |

| Lev | −8.058 *** | −0.495 *** | −3.181 *** | −1.843 *** | −2.204 *** |

| (−3.855) | (−8.286) | (−2.957) | (−3.172) | (−3.434) | |

| Rib | 0.293 *** | −0.002 | −0.039 * | 0.030 ** | 0.014 |

| (3.428) | (−1.382) | (−1.828) | (2.397) | (0.993) | |

| Roa | −0.292 | 0.800 *** | 0.443 | 3.901 *** | 0.898 |

| (−0.186) | (6.491) | (0.202) | (3.229) | (0.598) | |

| Grow | 0.327 *** | −0.016 ** | 0.031 | 0.000 | 0.027 |

| (2.592) | (−2.548) | (0.302) | (0.005) | (0.436) | |

| Ppe | −19.506 *** | 0.091 | −1.325 | 0.036 | 0.065 |

| (−3.081) | (1.191) | (−1.088) | (0.052) | (0.085) | |

| Cash | −2.824 ** | −0.234 ** | 1.247 | 0.428 | 0.410 |

| (−2.271) | (−2.470) | (0.835) | (0.503) | (0.452) | |

| Top1 | 0.097 *** | 0.002 *** | −0.006 | 0.017 ** | 0.025 *** |

| (3.727) | (2.624) | (−0.378) | (2.105) | (2.744) | |

| Size | 3.124 *** | 0.171 *** | 1.537 *** | 0.543 *** | 0.237 |

| (3.705) | (11.397) | (5.203) | (4.010) | (1.492) | |

| Turnover | −0.362 | 0.025 | 0.024 | −0.531 ** | −0.343 |

| (−1.421) | (0.870) | (0.050) | (−2.016) | (−1.155) | |

| IMR | 26.910 *** | ||||

| (3.114) | |||||

| Constant | −78.283 *** | 2.885 *** | 7.337 | 12.729 *** | 18.231 *** |

| (−2.662) | (8.528) | (1.074) | (4.054) | (4.966) | |

| Observations | 8046 | 20,846 | 5776 | 7649 | 5966 |

| R-squared | 0.846 | 0.690 | 0.850 | 0.848 | 0.843 |

| Firm FE | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES | YES |

| (1) 1:4 Nearest Neighbor Matching | (2) Kernel Matching | (3) Multi-Period DID | |

|---|---|---|---|

| Variables | ESG | ESG | ESG |

| Treat_Post | 0.575 *** | 0.621 *** | 0.319 * |

| (3.056) | (3.449) | (1.735) | |

| Lev | −1.651 *** | −1.837 *** | −1.710 *** |

| (−2.758) | (−3.226) | (−3.017) | |

| Rib | 0.025 * | 0.030 ** | 0.030 ** |

| (1.936) | (2.437) | (2.447) | |

| Roa | 3.921 *** | 2.938 ** | 3.009 ** |

| (3.136) | (2.505) | (2.564) | |

| Grow | −0.041 | −0.023 | −0.026 |

| (−0.685) | (−0.393) | (−0.451) | |

| Ppe | −0.081 | 0.051 | −0.001 |

| (−0.113) | (0.075) | (−0.002) | |

| Cash | 0.099 | 0.073 | 0.019 |

| (0.114) | (0.088) | (0.023) | |

| Top1 | 0.020 ** | 0.020 *** | 0.019 ** |

| (2.435) | (2.606) | (2.457) | |

| Size | 0.499 *** | 0.533 *** | 0.543 *** |

| (3.541) | (4.024) | (4.103) | |

| Turnover | −0.414 | −0.355 | −0.372 |

| (−1.536) | (−1.395) | (−1.460) | |

| Constant | 13.632 *** | 12.728 *** | 12.551 *** |

| (4.172) | (4.147) | (4.087) | |

| Observations | 7330 | 8042 | 8046 |

| R-squared | 0.848 | 0.846 | 0.845 |

| Firm FE | YES | YES | YES |

| Year FE | YES | YES | YES |

| Industry FE | YES | YES | YES |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | R&D | ESG | ICQ | ESG |

| Treat_Post | 1.197 *** | 0.038 *** | ||

| (6.152) | (4.312) | |||

| R&D | 0.094 *** | |||

| (8.434) | ||||

| ICQ | 1.031 *** | |||

| (4.191) | ||||

| Lev | −0.248 | −1.733 *** | −0.039 | −1.649 *** |

| (−0.406) | (−3.071) | (−1.410) | (−2.912) | |

| Rib | −0.028 ** | 0.034 *** | 0.001 ** | 0.029 ** |

| (−2.081) | (2.739) | (2.205) | (2.347) | |

| Roa | 2.407 * | 2.879 ** | 0.036 | 3.051 *** |

| (1.902) | (2.464) | (0.619) | (2.604) | |

| Grow | −0.010 | −0.021 | −0.001 | −0.028 |

| (−0.162) | (−0.368) | (−0.244) | (−0.481) | |

| Ppe | 1.196 | −0.053 | 0.017 | −0.045 |

| (1.635) | (−0.078) | (0.524) | (−0.067) | |

| Cash | 0.427 | −0.007 | −0.001 | −0.010 |

| (0.480) | (−0.009) | (−0.029) | (−0.012) | |

| Top1 | −0.024 *** | 0.021 *** | −0.000 | 0.019 ** |

| (−2.807) | (2.690) | (−1.063) | (2.495) | |

| Size | 1.479 *** | 0.411 *** | 0.002 | 0.553 *** |

| (10.362) | (3.102) | (0.378) | (4.191) | |

| Turnover | 0.175 | −0.417 | −0.037 *** | −0.330 |

| (0.635) | (−1.641) | (−2.938) | (−1.297) | |

| Constant | −29.981 *** | 15.307 *** | 3.525 *** | 8.719 *** |

| (−9.060) | (4.983) | (23.447) | (2.739) | |

| Observations | 8033 | 8033 | 8046 | 8046 |

| R-squared | 0.814 | 0.847 | 0.448 | 0.846 |

| Firm FE | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Bdiff | Industry | Duality | Digital Transformation | Government Subsidy |

| Treat_Post | 1.474 *** | 1.162 *** | −0.941 *** | −1.113 *** |

| Lev | 3.997 *** | −0.977 ** | 1.918 *** | 0.619 |

| Rib | −0.066 *** | −0.049 *** | 0.022 * | −0.022 |

| Roa | 2.176 *** | −1.178 ** | −2.731 ** | −2.425 * |

| Grow | 0.040 | 0.218 *** | 0.039 | 0.088 |

| Ppe | −0.916 ** | 3.170 *** | 1.034 | 1.214 |

| Cash | 1.489 *** | 0.578 | −2.994 *** | −1.873 *** |

| Top1 | 0.035 *** | −0.000 | −0.020 ** | −0.011 |

| Size | −1.132 *** | −0.731 *** | 0.308 * | 0.139 |

| Turnover | −1.602 *** | 0.271 ** | 0.032 | 1.113 *** |

| Industry | Duality | Digital Transformation | Government Subsidy | |||||

|---|---|---|---|---|---|---|---|---|

| (1) Ind = 1 | (2) Ind = 0 | (3) Dual = 1 | (4) Dual = 0 | (5) Low Samples | (6) High Samples | (7) Low Samples | (8) High Samples | |

| Variables | ESG | ESG | ESG | ESG | ESG | ESG | ESG | ESG |

| Treat_Post | −0.493 | 0.981 *** | −0.688 | 0.914 *** | 0.193 | 1.135 *** | −0.144 | 0.969 *** |

| (−1.063) | (5.042) | (−1.359) | (4.559) | (0.793) | (3.500) | (−0.586) | (3.411) | |

| Lev | −4.685 *** | −0.688 | −0.509 | −1.486 ** | −0.844 | −2.762 *** | −1.540 ** | −2.159 ** |

| (−3.141) | (−1.105) | (−0.336) | (−2.282) | (−1.051) | (−2.987) | (−2.102) | (−2.133) | |

| Rib | 0.079 *** | 0.013 | 0.065 * | 0.015 | 0.038 ** | 0.015 | 0.014 | 0.036 * |

| (2.849) | (0.934) | (1.808) | (1.088) | (2.046) | (0.846) | (0.811) | (1.846) | |

| Roa | 0.023 | 2.199 * | 4.409 * | 3.232 ** | 1.700 | 4.432 *** | 1.138 | 3.563 * |

| (0.008) | (1.716) | (1.699) | (2.295) | (0.987) | (2.645) | (0.754) | (1.694) | |

| Grow | −0.062 | −0.022 | −0.247 | −0.030 | 0.013 | −0.026 | 0.022 | −0.066 |

| (−0.318) | (−0.368) | (−1.472) | (−0.466) | (0.187) | (−0.249) | (0.332) | (−0.552) | |

| Ppe | 0.748 | −0.168 | −2.350 | 0.820 | −0.105 | −1.138 | −0.029 | −1.244 |

| (0.551) | (−0.201) | (−1.258) | (1.082) | (−0.117) | (−0.911) | (−0.033) | (−1.028) | |

| Cash | −1.187 | 0.302 | −0.586 | −0.007 | −0.997 | 1.996 | −0.458 | 1.415 |

| (−0.536) | (0.345) | (−0.301) | (−0.008) | (−0.927) | (1.555) | (−0.456) | (0.957) | |

| Top1 | −0.005 | 0.030 *** | 0.014 | 0.014 | 0.005 | 0.025 ** | 0.028 ** | 0.038 *** |

| (−0.281) | (3.403) | (0.575) | (1.589) | (0.451) | (2.091) | (2.449) | (2.893) | |

| Size | 1.652 *** | 0.520 *** | 1.280 *** | 0.549 *** | 0.804 *** | 0.496 ** | 0.644 *** | 0.505 ** |

| (4.073) | (3.621) | (3.351) | (3.533) | (3.763) | (2.338) | (3.547) | (2.049) | |

| Turnover | 0.778 | −0.824 *** | −0.472 | −0.201 | −0.329 | −0.361 | 0.122 | −0.991 ** |

| (1.306) | (−2.861) | (−0.674) | (−0.681) | (−0.855) | (−0.934) | (0.346) | (−2.364) | |

| Constant | −12.179 | 12.735 *** | −5.343 | 12.595 *** | 4.731 | 16.020 *** | 9.371 ** | 14.089 ** |

| (−1.303) | (3.803) | (−0.601) | (3.500) | (0.965) | (3.252) | (2.283) | (2.387) | |

| Observations | 1673 | 6350 | 1451 | 6327 | 3911 | 3908 | 3858 | 3859 |

| R-squared | 0.843 | 0.850 | 0.852 | 0.853 | 0.844 | 0.877 | 0.846 | 0.868 |

| Firm FE | YES | YES | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES | YES | YES | YES | YES |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Y.; Zhang, Y.; Sun, Z. The Impact of Carbon Emission Trading Policy on Enterprise ESG Performance: Evidence from China. Sustainability 2023, 15, 8279. https://doi.org/10.3390/su15108279

Zhang Y, Zhang Y, Sun Z. The Impact of Carbon Emission Trading Policy on Enterprise ESG Performance: Evidence from China. Sustainability. 2023; 15(10):8279. https://doi.org/10.3390/su15108279

Chicago/Turabian StyleZhang, Yadu, Yiteng Zhang, and Zuoren Sun. 2023. "The Impact of Carbon Emission Trading Policy on Enterprise ESG Performance: Evidence from China" Sustainability 15, no. 10: 8279. https://doi.org/10.3390/su15108279

APA StyleZhang, Y., Zhang, Y., & Sun, Z. (2023). The Impact of Carbon Emission Trading Policy on Enterprise ESG Performance: Evidence from China. Sustainability, 15(10), 8279. https://doi.org/10.3390/su15108279