4.1. Sample Selection and Data Sources

According to the classification standard of heavy pollution industries, this classification is used as the standard in the sample selection process. First, based on the 16 types of industries included in the heavy polluting industries mentioned above, and referring to the industry classification results of listed companies by China Securities Regulatory Commission in 2017, it screened out listed companies that meet the classification standards for heavy pollution industries; next, the paper intercepted the 2014–2017 panel data of listed companies that met the criteria.

After screening, it was found that the number of listed companies that met the above requirements increased year by year from 2014 to 2020, from 33 in 2014 to 59 in 2020. In order to consider the completeness and comparability of the sample data, this paper finally selects 33 listed companies in heavy pollution industries as the research sample, with a total of 132 observations during the period from 2014 to 2020.

4.3. Descriptive Statistical Analysis

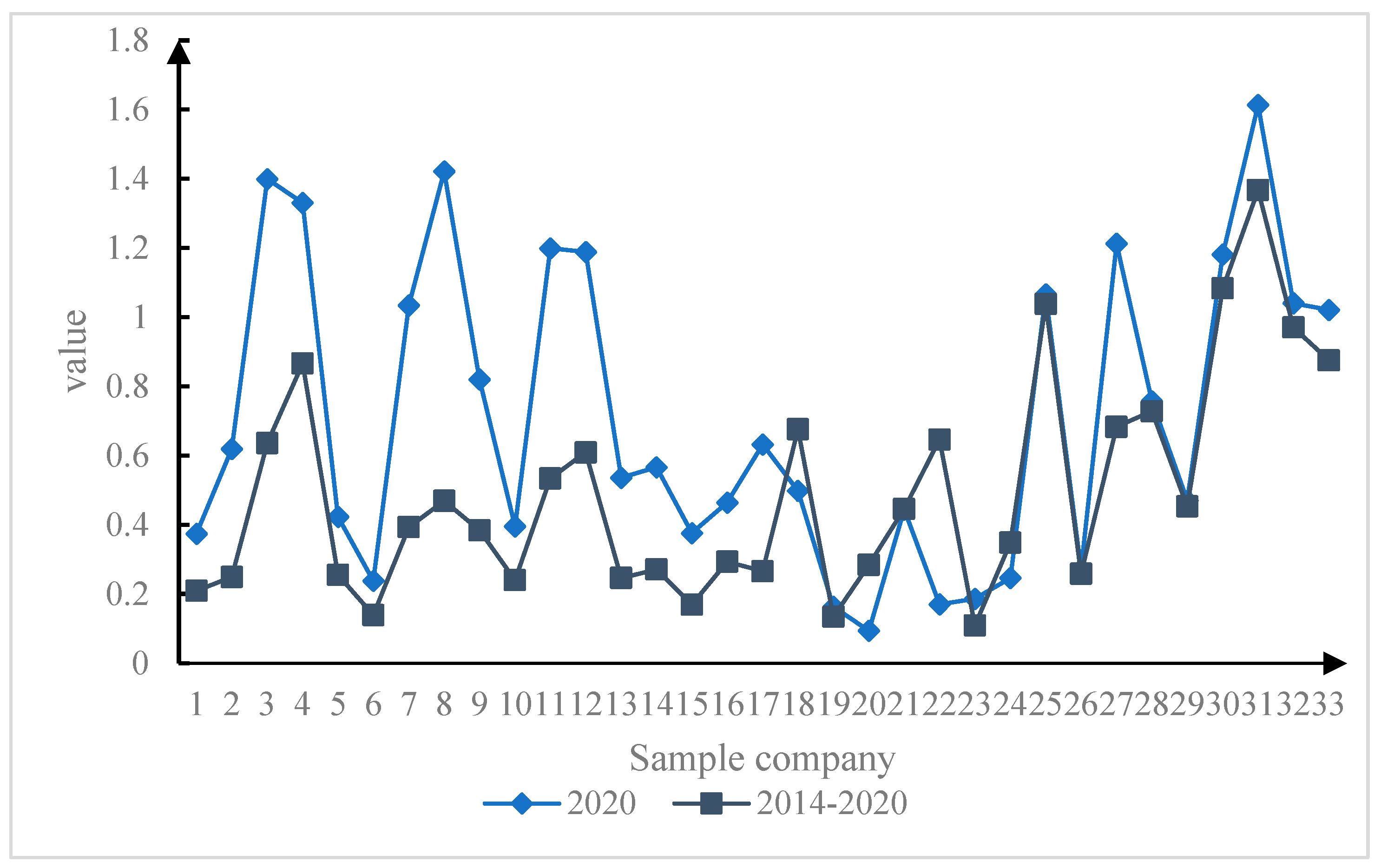

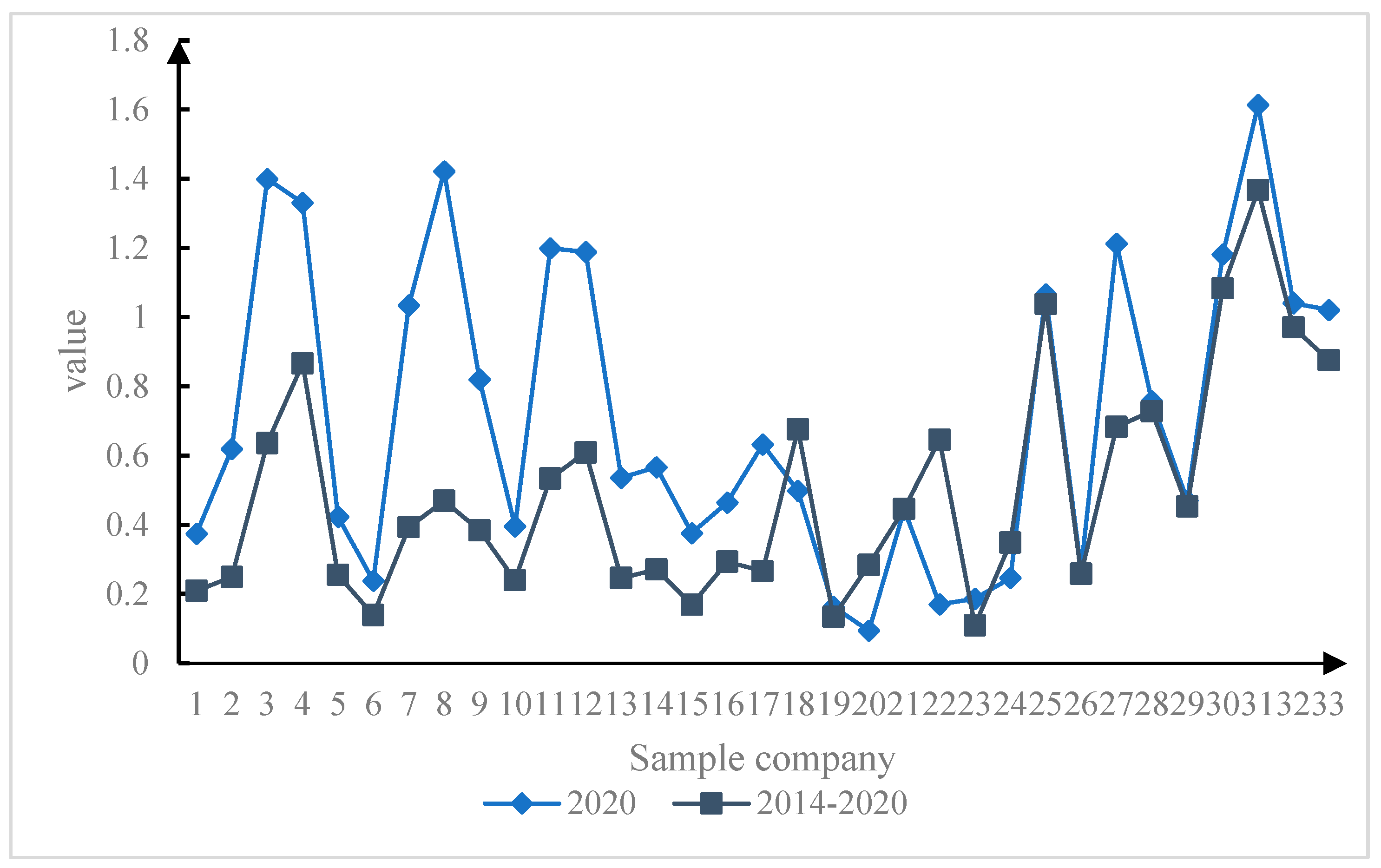

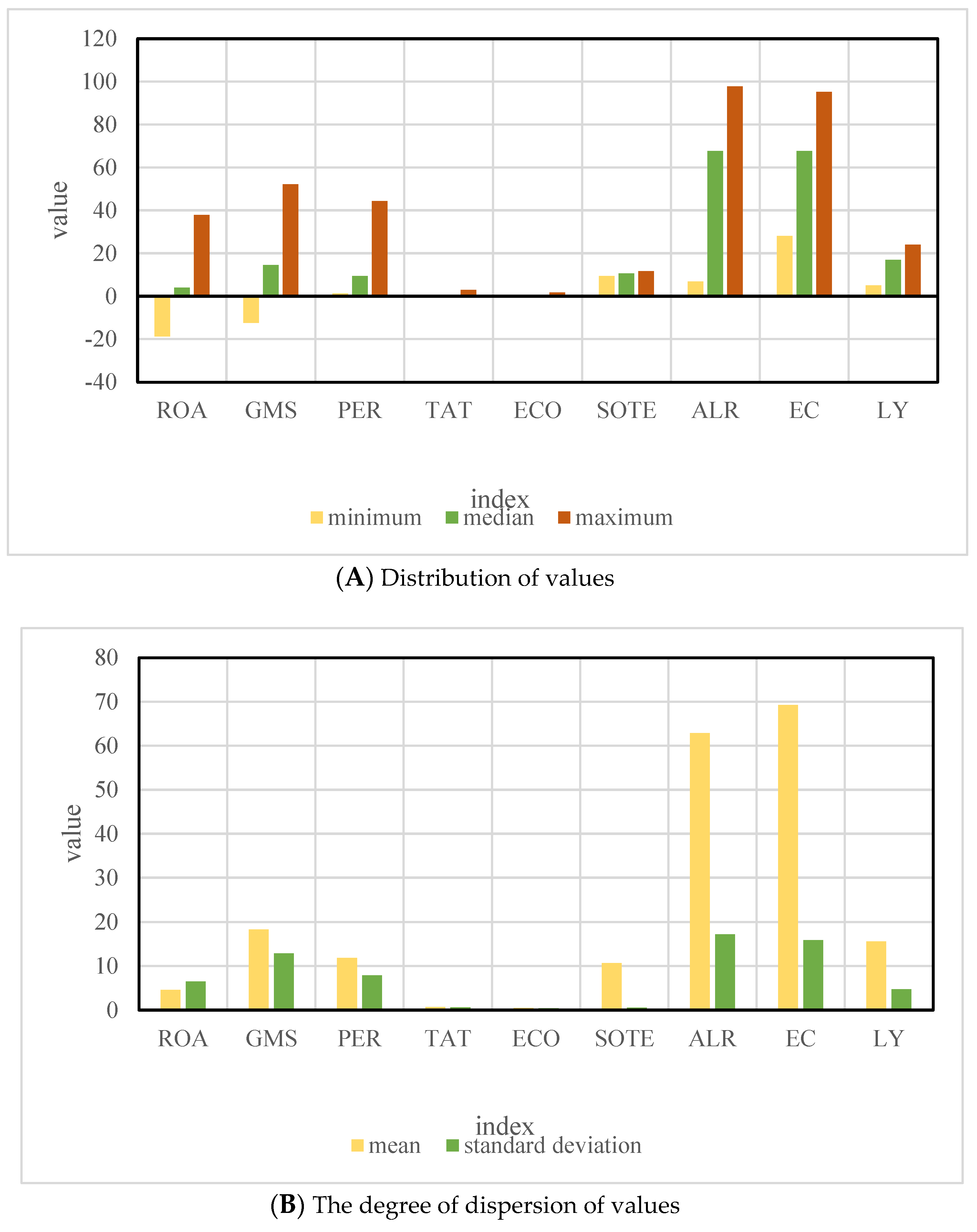

According to the specific values of return on assets (ROA), gross margin of sales (GMS), period expense rate (PER), total asset turnover (TAT) of listed companies in heavy pollution industries from 2014 to 2020 in the appendix, and the size of the enterprise (SOTE), asset-liability ratio (ALR), equity concentration (EC), and listing years (LY), and perform descriptive statistics to obtain the descriptive statistics of related variables in

Figure 6.

Figure 6A shows the minimum value, median and maximum value of each index in 7 years, and

Figure 6B shows the mean value and standard deviation of each index in 7 years. The approximate distribution of values can be known by comparing the median to the mean. The following are the specific analysis results:

(1) The average return on assets (ROA) and gross margin of sales (GMS) of each company are 4.580% and 18.354%, respectively, indicating that the average return on sample companies is positive. (2) The median of the period expense rate (PER) of the sample enterprises is less than the mean (9.43011.903). That is, half of the enterprises’ period expense rates are lower than the mean, indicating that the sample enterprises’ period expense management and control efficiency is high. (3) The average value of the total asset turnover (TAT) of the sample companies is greater than the median (0.7340.519). That is, the total asset turnover of half of the sample companies is less than the average value, indicating that the turnover speed of more than half of the sample companies is relatively slow and the operating capacity is weak. (4) The median of the eco-efficiency (ECO) of the sample enterprises is less than the mean value of eco-efficiency (0.3820.489), indicating that the eco-efficiency of most enterprises does not reach the average level. In addition, there is a big difference between the minimum value of 0.012 and the maximum value of 1.712 for the eco-efficiency of the sample enterprises, indicating that the eco-efficiency levels of the sample enterprises are uneven. (5) The minimum and maximum logarithm of total assets (SOTE) are 9.425 and 11.757, respectively. The mean and standard deviation are 10.693 and 0.539, respectively, indicating that there is little difference in the scale of sample enterprises. The median (67.3%) of the asset-liability ratio (ALR) of the sample enterprises is greater than the mean value of the asset-liability ratio (62.875%), indicating that at least half of the sample enterprises have an asset-liability ratio greater than 62.875%. The average shareholding ratio of the top ten shareholders is 69.254% [

33].

4.4. Correlation Analysis

It can be seen from

Table 5 that the Pearson correlation coefficient of return on assets (ROA) and eco-efficiency (ECO) is 0.374, the significance level is 0.000, and there is a significant positive correlation at the 0.1% level. The Pearson correlation coefficient of gross margin of sales (GMS) and eco-efficiency (ECO) is 0.344, the significance level is 0.000, and there is a significant positive correlation at the 0.1% level. The Pearson correlation coefficient between period expense rate (PER) and eco-efficiency (ECO) is −0.007, the significance level is 0.940, and the correlation is weak. The Pearson correlation coefficient of total asset turnover (TAT) and eco-efficiency (ECO) was 0.270, the significance level was 0.002, and there was a significant positive correlation at the 1% level. The above results show that under the Pearson correlation test, the ecological efficiency is significantly positively correlated with the return on assets, gross margin of sales, and total asset turnover, and has a weak negative correlation with the period expense rate.

The Pearson correlation coefficient reflects the correlation between any two variables. The addition of a control variable may affect the relationship between the dependent variable and the independent variable. Therefore, the company size, asset-liability ratio, equity concentration and listing years are added as control variables to study the correlation between ecological efficiency and financial performance.

Comparing

Table 4 with

Table 6, it can be found that return on assets (ROA), gross margin of sales (GMS), and total asset turnover (TAT) have all passed the significance test. It can be seen from

Table 6 that ECO and ROA are significantly positively correlated (

p < 0.01), which preliminarily shows that the improvement of ecological efficiency has a promoting effect on the financial performance indicator ROA. There was a significant positive correlation between ECO and GMS (

p < 0.01), a significant positive correlation between ECO and TAT (

p < 0.01), and a negative correlation between ECO and PER, but it was not significant. It shows that the improvement of ecological efficiency can promote the improvement of enterprise financial performance index ROA by affecting the gross margin of sales of sales and total asset turnover rate. It can also promote the improvement of enterprise financial performance index ROA by affecting the period expense rate, but the effect is not obvious.

4.5. Panel Data Regression Analysis

According to the article, four panel data models of the impact of environmental economic transformation on ecological efficiency were constructed to test the direction and extent of the impact of environmental economic transformation on ecological efficiency. It was originally assumed

, that is, the intercept term of all individuals is the same. When the obtained

p value is 0.0000, the null hypothesis is strongly rejected. The fixed effect model is selected, otherwise, the random effect model is selected. From the Hausman test results in

Table 7, it can be found that the

p-value obtained by model (3-3) and model (3-5) is 0.0000, rejecting the null hypothesis and choosing the fixed effect model, while model (3-2) and model (3-4) choose a random effects model.

In order to study the direction and extent of the impact of ecological efficiency on financial performance of listed companies in heavily polluting industries, according to the model constructed in this paper, Stata12.0 software is used to perform regression analysis on relevant variables and data. The regression results of the four panel data models are as follows:

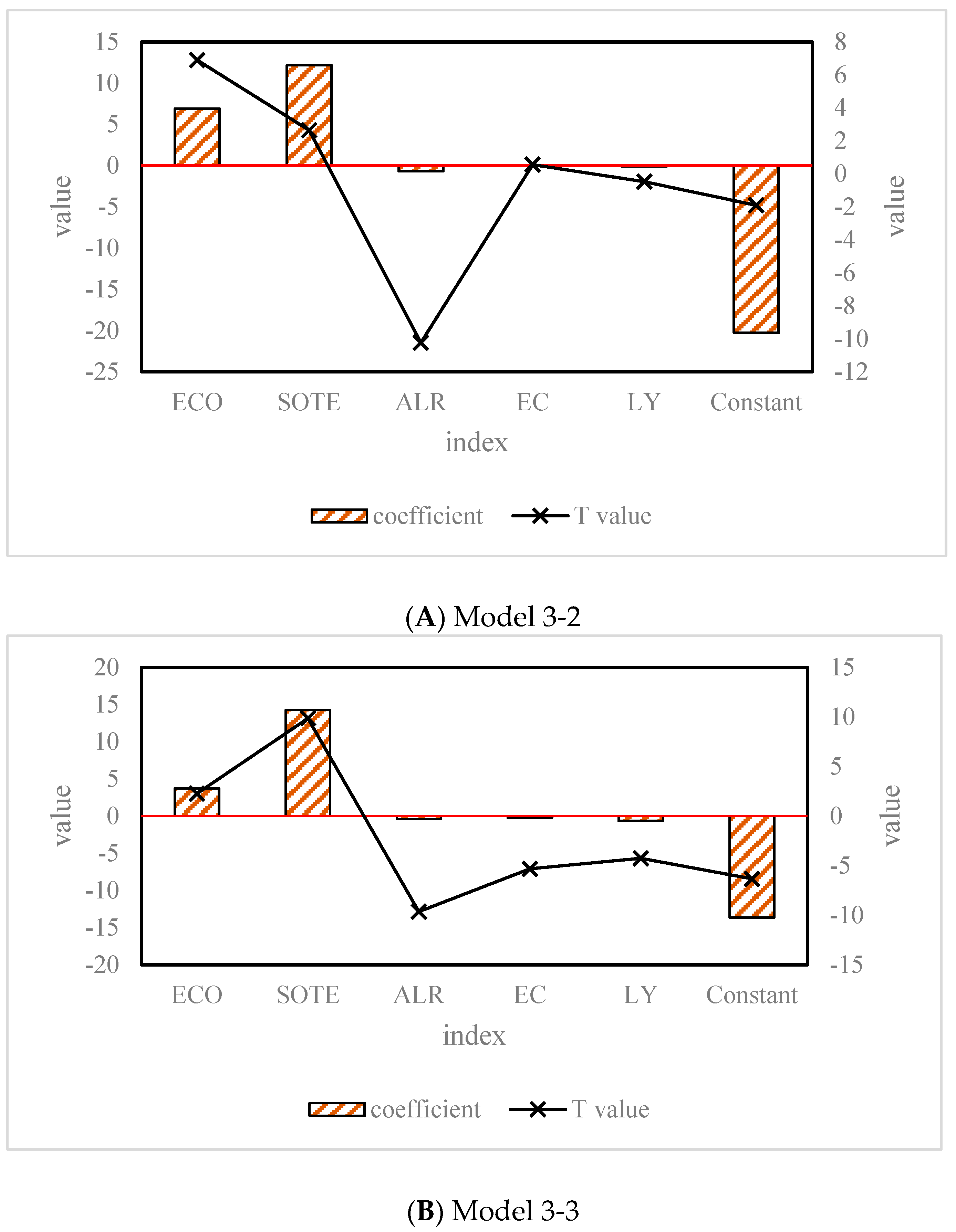

(1) Influence of return on assets and gross margin of sales on ecological efficiency

In this paper, Stata12.0. software is used to perform regression analysis on panel data model 3-2 and model 3-3 to explore the impact of ecological efficiency on asset returns. The analysis results are shown in

Figure 7.

It can be seen from

Figure 7A that ECO and return on assets (ROA) are significantly positively correlated (

p < 0.01), indicating that the improvement of ecological efficiency helps to improve the efficiency of asset use, that is, the improvement of ecological efficiency can help to improve the investment efficiency of listed companies, and the hypothesis

is verified. At the same time, it can also be found that the regression coefficient of enterprise size is 12.162 (

p < 0.01), indicating that enterprise size as a control variable has a significant positive correlation with the return on assets. The regression coefficient of the asset-liability ratio is −0.683 (

p < 0.01), indicating that the asset-liability ratio as a control variable is significantly negatively correlated with the return on assets. The concentration of ownership, listing years and the return on assets are not correlated.

It can be seen from

Figure 7B that ECO is significantly positively correlated with gross margin of sales (GMS) (

p < 0.05), indicating that the higher the eco-efficiency, the greater the company’s gross margin of sales, which verifies Hypothesis 1. At the same time, it can also be found that the regression coefficient of enterprise scale is 14.5858 (

p < 0.01), indicating that enterprise scale as a control variable has a significant positive correlation with gross margin of sales. The regression coefficients of the asset-liability ratio, equity concentration, and listing years are −0.413 (

p < 0.01), −0.285 (

p < 0.01), and −0.637 (

p < 0.01), respectively. This indicates that the asset-liability ratio, equity concentration and listing years as control variables are significantly negatively correlated with gross margin of sales.

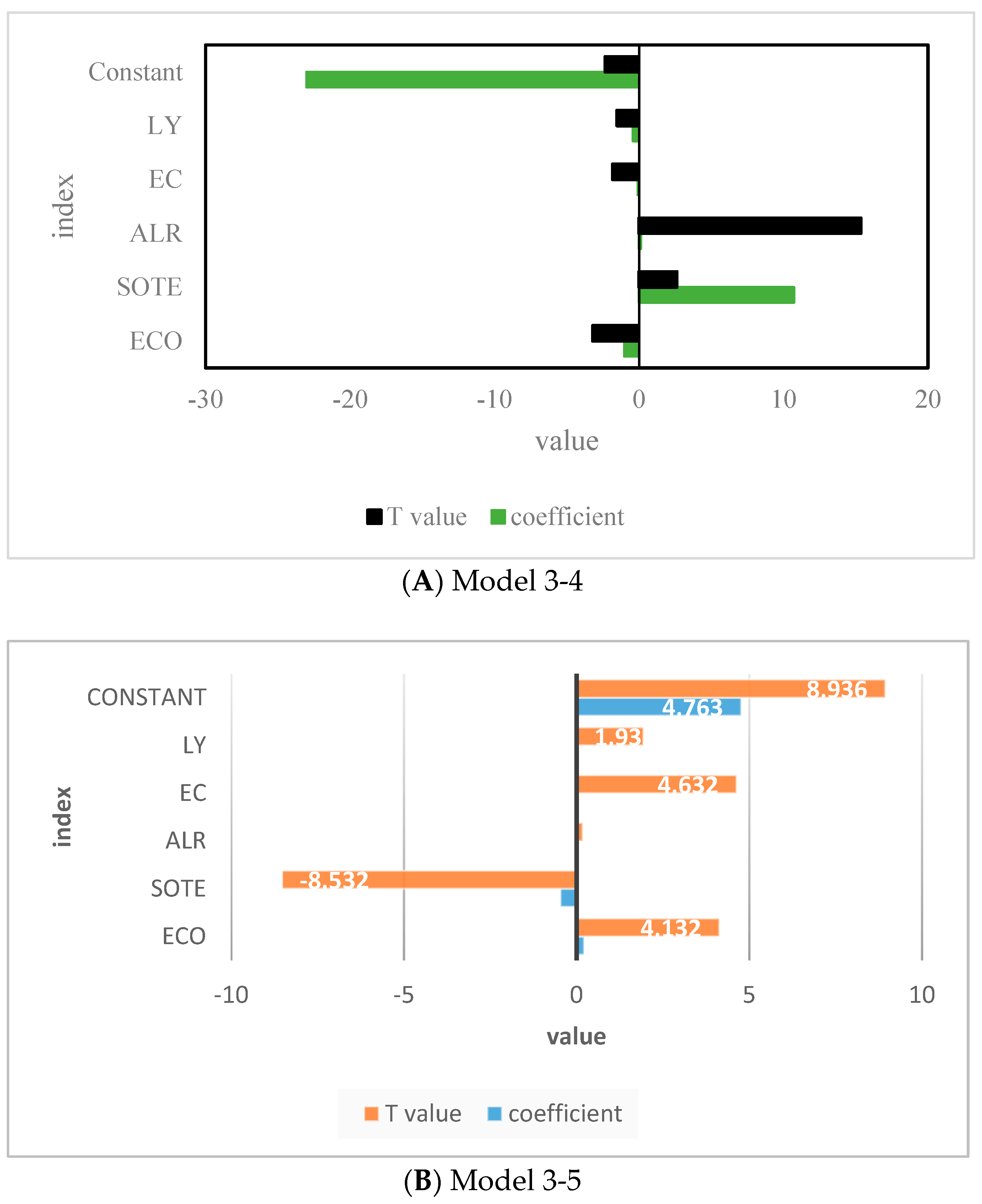

(2) Periodic expense rate and its influence on total asset turnover rate on ecological efficiency

In this paper, Stata12.0. software is used to conduct regression analysis on panel data model 3-4 and model 3-5 to explore the impact of period expense rate and total asset turnover rate on ecological efficiency. The analysis results are shown in

Figure 8.

It can be seen from

Figure 8A that ECO is significantly negatively correlated with the period expense ratio (PER) (

p < 0.05), indicating that the improvement of eco-efficiency can help reduce the current period expense of the enterprise, which verifies Hypothesis

. At the same time, it can also be found that the regression coefficients of enterprise scale and asset-liability ratio are 10.7839 (

p < 0.10) and 0.1364 (

p < 0.01), respectively. This indicates that the scale of enterprises and the asset-liability ratio as control variables are significantly positively correlated with the period expense rate. The equity concentration, listing years, and the period expense rate are not correlated.

It can be seen from

Figure 8B that ECO is significantly positively correlated with the total asset turnover (TAT) (

p < 0.01), indicating that the improvement of ecological efficiency helps the turnover of assets. The improvement of ecological efficiency can help improve the utilization efficiency of listed companies’ assets, which verifies the hypothesis

. At the same time, it can also be found that the regression coefficient of enterprise size is −0.4650 (

p < 0.01), indicating that enterprise size as a control variable is significantly negatively correlated with total asset turnover. The asset turnover rate is not related to the total asset turnover. The regression coefficients of equity concentration and listing years are 0.0084 (

p < 0.01) and 0.0115 (

p < 0.05), respectively, indicating that the equity concentration and listing years as control variables are significantly positively correlated with the total asset turnover.

According to the four panel data models of the impact of environmental and economic transformation on ecological efficiency constructed in the article, and combining the four indicators of ROA, GMS, PER, and TAT, the comprehensive coefficient of the environmental, and economic transformation indicators calculated by the software is 1.325 (p < 0.001). The experimental results are helpful for listed companies in the heavily polluted industry to actively explore ways to improve ecological efficiency.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}