Does Infrastructure Development Contribute to EU Countries’ Economic Growth?

Abstract

:1. Introduction

2. Theoretical Background

3. Methodology

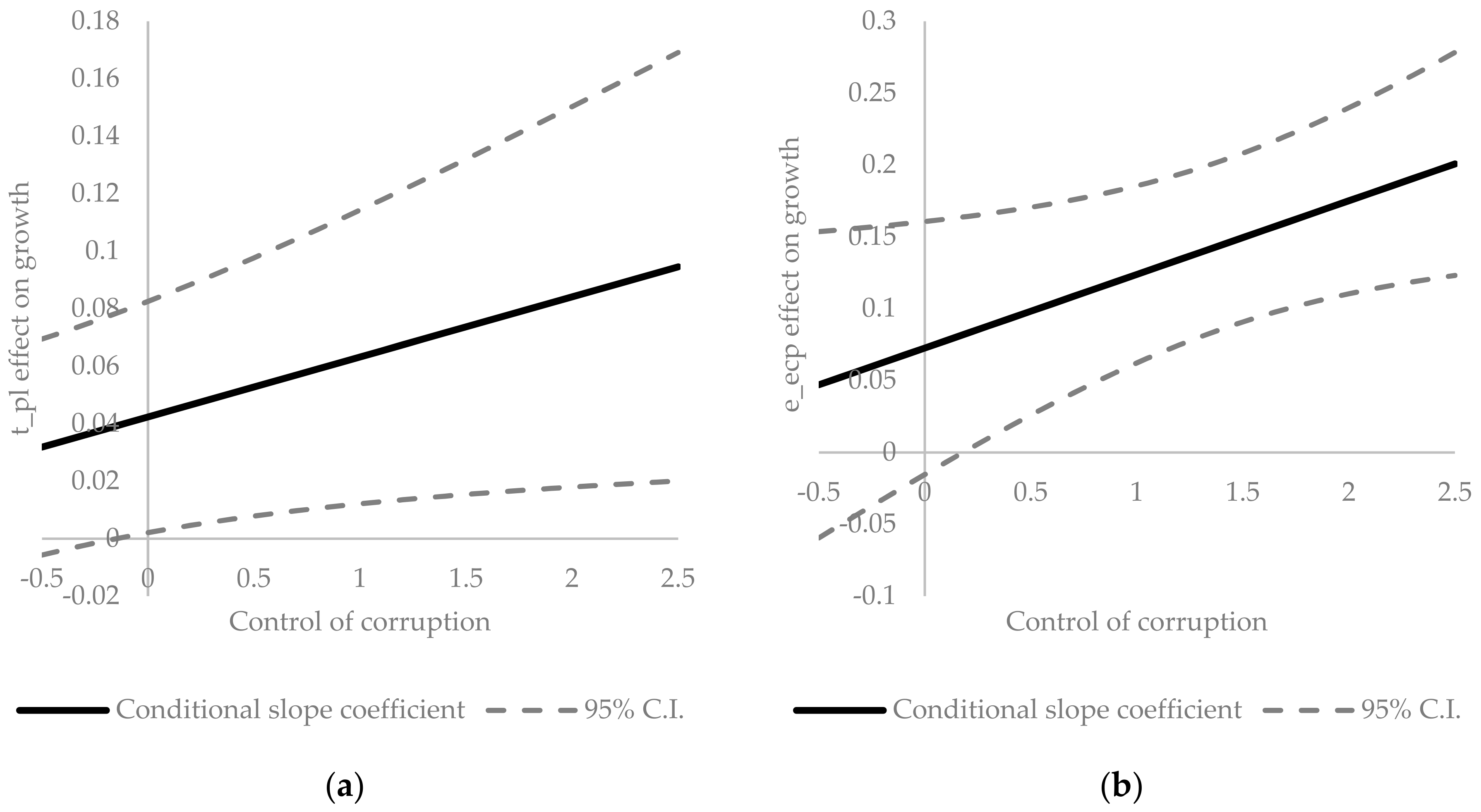

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Research by | Covered Period | Units and Level | Methods Applied | Infrastructure Variable | Outcome Variable | Main Results |

|---|---|---|---|---|---|---|

| Transport infrastructure impact | ||||||

| Boopen [1] | 1980–2000 | 38 Sub-Saharan African countries | Pooled OLS **, FE **, RE ** | Length of paved road in kilometres | GDP per capita based on PPP | Positive, significant. |

| Zhang [6] | 1993–2004 | China 29 provinces | FE **, RE ** with spatial matrix | Local TI capital stock | GDP | Positive, significant. |

| Hong et al. [7] | 1998–2007 | 31 Chinese provinces | FE **, RE **, OLS ** | Land transport index, Air transport index, Water transport index | GDP per capita | Strong positive, significant impact of land transport. Positive significant of water transport after the investments exceeds a threshold level. Weak impact of airway transport. |

| Crescenzi & Rodríguez-Pose [32] | 1990–2004 | EU-15, NUTS1 and NUTS2 | Two-way FE ** and GMM **-diff regressions | Kilometres of motorways (per land area, per thousand inhabitants, per million Euro of GDP) | GDP per capita | Positive, small, and middle significant. Depends on socio-economic conditions, innovation capacity and capacity to attract migrants. |

| Yu et al. [8] | 1978–2008 | China provinces (3 clusters according to GDP) | Linear regression, Granger causality test | Transport investment | GDP | At national level: unidirectional Granger causality from economic growth to transport infrastructure; At the regional level: bidirectional causality in the eastern region, and unidirectional causality from economic growth to transport infrastructure in central and western regions. |

| Pradhan & Badgchi [12] | 1970–2010 | India | Granger causality test, VECM ** | Length of road and rail in kilometres | GDP | Bidirectional causality between road transportation and economic growth. Unidirectional causality from rail transportation to economic growth. |

| Carruthers [27] | 20 years (not specified) | EU27 (4 scenario) | Cost-benefit, elasticity analysis | TI investments | GDP per capita, trade balance as % of GDP | Positive impact both on economic growth and trade balance. |

| Farhadi [33] | 1870–2009 | 18 OECD countries | FE **, FGLS **, GMM ** | Capital stock of transportation provided by the government as a share of GDP | Labour productivity (LP), TFP | Positive, significant, but not substantial impact on LP and TFP. |

| Luz et al. [30] | 2010–2014 | 10 countries | Linear regression | LPI* as transport infrastructure index | GDP, GDP per capita | Insignificant on GPD; positive, significant on GDP per capita. |

| Meersman & Nazemzadeh [28] | 1979–2013 | Belgium | LA-VAR ** | The total length of the road and rail network | GDP per capita | Positive, significant. |

| Maparu & Mazumder [14] | 1990–2011 | India | VAR **, VECM ** | 9 indicators: Total Transport Expenditure, Railway Density, Total Road Density, etc. | GDP per capita, urbanisation | Positive, significant in long run. Unidirectional causality from economic development to transport infrastructure in most of the cases. |

| Cigu et al. [29] | 2000–2014 | EU-28 countries | Pooled OLS **, RE **, FE ** | The index of transport infrastructure status | GDP per capita based on PPP | Positive, significant even after institutional and other factors are controlled for. |

| Lenz et al. [31] | 1995–2016 | CEE* Member States | Pooled OLS **, FE **, RE ** | Length of total railways (km), length of total road network (km) | GDP | Positive, significant, except negative impact of railway infrastructure. |

| Saidi et al. [4] | 2000–2016 | MENA* countries (3 subgroups) | GMM ** | Kilometres of roads per capita | GDP per capita | Positive, significant in all regions. |

| Kyriacou et al. [34] | 1996–2010 | 34 countries | DEA **, Regression analysis | TI investment | TI index | Positive, significant. Depends on government quality. |

| Batool & Goldmann [16] | 1973–2014 | Pakistan | VAC **, VAR ** models | The length of the paved road and rails network, public and private capital stock in transport | GDP, GDP per capita | Positive, significant in long-run. |

| Elburz & Cubukcu [17] | 2004–2014 | Turkey 26 NUTS 2 regions | OLS **, SDM ** | Roads and motorway infrastructure length (km) per capita | Regional GDP per capita | Positive, significant. |

| Muvawala et al. [18] | 1983–2018 | Uganda | ARDL ** model | Expenditure on Transport Infrastructure | GDP Growth Rate | Positive significant in long run, but negative significant in short run |

| Wang et al. [11] | 2000–2017 | China’s 30 provincial-level regions | Threshold panel model | Industrial agglomeration index, highway density (length of highway route relative to physical space) | Energy consumption/GDP; TFEE* | Positive, significant only when a certain threshold is exceeded. |

| Wang et al. [22] | 2007–2016 | 42 BRI countries divide in to 5 regions | SA ** tests, SLM **, SEM **, SDM ** | The railway network density, the road network density | GDP per capita | Positive, significant at the national level. Negative, significant at regional level in East Asia-Central Asia. Positive, significant at regional level in Central and Eastern Europe. |

| ICT infrastructre impact | ||||||

| Madden & Savage [35] | 1990–1995 | 27 CEE * | OLS ** | Share of telecommunications investment in GDP | Real GDP per capita growth rate | Positive, significant. |

| Pohjola [36] | 1980–1995 | 39 countries | Regression | Ratio of spending on IT to nominal GDP | GDP per working age population in PPP | Positive, strong, and significant in the smaller sample of the developed (OECD) countries. |

| Datta & Agarwal [37] | 1980–1992 | 22 OECD | Dynamic FE ** | Access lines per 100 inhabitants | Real GDP per capita growth rate | Positive, significant after controlling for a number of other factors. |

| Sridhar, K. S. & Sridhar, V. [23] | 1990–2001 | 63 countries | 3SLS ** | Telephones per 100 inhabitants, total Telecom penetration, telephone revenue per user, investments, etc. | Real GDP, Real GDP per capita | Positive, significant. |

| Donou-Adonsou et al. [3] | 1993–2012 | All Sub-Saharan Africa countries | FE **, 2SLS **, IV-GMM ** | Internet usage andMobile phone subscriptions | GDP per capita growth rate | Positive, significant. |

| Pradhan et al. [68] | 2001–2012 | G-20 countries | VECM **, Granger causality test | Broadband users and Internet users in percentage of total population | GDP per capita | Positive, significant. Granger causality relationship among per capita economic growth, ICT infrastructure and other factors. |

| Toader et al. [38] | 2000–2017 | EU-28 | GMM **, OLS ** | Fixed-broadband subscriptions per 100 inhabitants, the percentage of households with a broadband Internet connection, percentage of individuals using the Internet; mobile cellular subscriptions (per 100 people) | GDP per capita in market prices | Positive, significant. |

| Haftu [5] | 2006–2015 | 40 Sub-Saharan Africa (SSA) countries | Two-step system GMM ** | The percentage of individuals using the Internet, cellular telephone subscription per 100 inhabitants | GDP per capita | Mobile phone penetration has positive significant impact on growth; Internet has not contributed to the per capita GDP. |

| Untari, Priyarsono & Noviani [19] | 2011–2016 | Indonesia provinces | TSLS ** | Cellular telephones, Internet accessibility, number of BTS, and government ICT expenditure | Regional GDP, Gini coefficient | Physical infrastructure indicators have a positive, significant impact on economic growth. Government spending on ICTs do not significantly impact economic growth and income inequality. |

| Maneejuk & Yamaka [24] | 1995–2017 | 5 developed and 5 developing countries | TKR ** model, PKR ** model | Fixed-Telephone Subscriptions (FTS), Mobile Cellular Subscriptions (MCS), Fixed-Broadband Subscriptions (FBS), Percentage of Individuals using the Internet (PUI) | Real GDP per capita in PPP* | (i) FTS, MCS have significant non-linear impact on economic growth in developing and developed countries (TKR model); (ii) FTS, MCS and FBS have positive direct impact on growth in developed countries (PKR model); (iii) FTS, MCS have a non-linear impact on growth in developing countries. |

| Nair, Pradhan & Arvin [39] | 1961–2018 | 36 OECD countries | VECM ** | Composite index of ICT | Real GDP per capita | Positive, significant in the long-run and in the short run. |

| Kallal, Haddaji & Ftiti [20] | 1997–2015 | Tunisia, sectoral level | ARDL ** | ICT diffusion index (ICTD) | Real value-added | Significant, positive long-term effect and negative short-term effect. |

| Energy infrastructure impact | ||||||

| Lin & Chiu [9] | 2016–2020 | 30 regional/ provincial level in China | Leontief I-O model | Amount of investment in the energy industry | regional GDP | The energy infrastructure investment increased the final demand of other related manufacturing sectors, whose services were required for the completion of infrastructure construction. |

| Yang et al. [10] | 2000–2014 | China 29 provinces | GMM ** | Effective Cost Index (ECI), power grid infrastructure (PGI) investments | Real GDP per capita | (i) ECI impact the regional economic growth negatively; (ii) PGI investment generate higher marginal benefits for the less developed inland areas than the developed coastal areas. |

| Mixed (severel types) infrastructure impact | ||||||

| Calderón & Servén [69] | 1960–2000 | Macro, 121 countries | GMM ** | The Aggregate Index of Infrastructure Stocks, The Aggregate Index of Infrastructure Quality. Covers transport, ICT, and energy infrastructure. | GDP per capita, Gini Coefficient | Positive, significant impact of infrastructure on economic growth in long-run. Robust negative, significant impact of infrastructure quantity and quality on income inequality. |

| Canning & Pedroni [52] | 1950–1992 | 67 countries | ADF ** test, Granger causality test | Paved roads per capita, Electricity generating capacity per capita, Telephones per capita. | GDP per capita | Positive, significant in the vast majority of cases in long run. Results vary across individual countries. In some countries infrastructure is under-supplied and over-supplied in others. |

| Kumo [2] | 1960–2009 | South Africa, country level | VAR ** model, Granger causality tests | Government infrastructure investment and GDP ratio | GDP | Strong bidirectional Granger causality between economic infrastructure investment and GDP growth. |

| Awan & Anum [15] | 1971–2013 | Pakistan, country level | ARDL ** | Infrastructure Development Index. Covers transport, ICT, and energy infrastructure. | GDP | Positive, significant. |

| European Commission [25] | 1950–2012 | Macro, EU-28 | Full Modified OLS ** and Dynamic OLS ** estimations, FE ** | Infrastructure provision per capita (kilometres of roads and railway lines; megawatt of electrical capacity (electricity) per million people | GDP per capita | Positive, significant. |

| Palei [26] | 2012 | 124 countries | Regression analysis | Infrastructure index | Global competitiveness index | Positive, significant. |

| Mitra et al. [13] | 1994–2010 | Indian manufacturing sector (8 industries) | Fully modified OLS **, panelcointegration and System GMM ** | An aggregate infrastructure index (covers transport, ICT, and energy infrastructure). ICT infrastructure index | TFP* and technical efficiency (TE) | Positive, significant. Stronger impact in industries which are more exposed to foreign competition (Textile, Transport Equipment, Chemicals, Metal & Metal Products). |

| Apurv & Uzma [70] | 1980–2017 | BRICS Countries | OLS **, FE **, RE** | Electric power Consumption (kWh per capita), Fixed telephone subscriptions, Raillines (total route, km), Agricultural irrigated land | GDP | Panel data results: (i) positive, significant impact of energy infrastructure on economic growth; (ii) negative, significant impact telecommunication infrastructure on economic growth. |

| Arif et al. [21] | 2006–2016 | 19 Asian countries, 16 manufacturing industries | Fully modified OLS ** | Telecom, road, and power infrastructure | TFP* | Positive, significant. Road infrastructure is more important for low technology-intensive industries, whereas power infrastructure is crucial for high technology-intensive industries. |

Appendix B

| (24) | (25) | (26) | (27) | (28) | (29) | (30) | (31) | (32) | (33) | (34) | (35) | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Core Infrastructure (INFR) | ICT infrastructure | Fixed telephone | ln(ict_ft) | γ | 0.0009 | |||||||||||

| (0.0046) | ||||||||||||||||

| Fixed broadband | ln(ict_fb) | 0.0034 | ||||||||||||||

| (0.0029) | ||||||||||||||||

| Mobile cellular | ln(ict_mc) | 0.0260 * | ||||||||||||||

| (0.0151) | ||||||||||||||||

| Water and sanitation | Sanitation facilities | ln(ws_sf) | 0.0425 | |||||||||||||

| (0.0561) | ||||||||||||||||

| Drinking water facilities | ln(ws_dwf) | 0.0083 | ||||||||||||||

| (0.0335) | ||||||||||||||||

| Transport infrastructure | Railways | ln(t_rw) | 0.0027 | |||||||||||||

| (0.0149) | ||||||||||||||||

| Roads | ln(t_r) | 0.0019 | ||||||||||||||

| (0.0073) | ||||||||||||||||

| Inland waterways | ln(t_ww) | 0.0052 | ||||||||||||||

| (0.0171) | ||||||||||||||||

| Pipelines | ln(t_pl) | 0.0237 *** | ||||||||||||||

| (0.0050) | ||||||||||||||||

| Air transport | ln(t_ap) | 0.0116 | ||||||||||||||

| (0.0074) | ||||||||||||||||

| Energy | Electricity | ln(e_epc) | 0.0145 ** | |||||||||||||

| (0.0072) | ||||||||||||||||

| Institutions (Control of corruption) | inst_cc | c1 | 0.0122 * | 0.0120 ** | 0.0104 * | 0.0130 ** | 0.0122 ** | 0.0109 ** | 0.0104 | 0.0126 ** | 0.0120 | 0.0205 *** | 0.0184 *** | 0.0151 *** | ||

| (0.0060) | (0.0060) | (0.0055) | (0.0055) | (0.0060) | (0.0055) | (0.0094) | (0.0061) | (0.0092) | (0.0055) | (0.0051) | (0.0058) | |||||

| Population growth | Δln(pop) | c2 | −0.9613 | −0.9570 | −1.0570 * | −0.9655 | −0.9665 | −0.8976 | −1.0780 | −1.0570 | −0.1386 | −0.0847 | −1.0420 * | −1.0910 * | ||

| (0.5851) | (0.5857) | (0.6124) | (0.5879) | (0.5921) | (0.5902) | (0.7675) | (0.7102) | (0.2284) | (0.2528) | (0.6275) | (0.6325) | |||||

| Population density | ln(dens) | c3 | 0.0598 | 0.0601 | 0.0599 | 0.0648 | 0.0604 | 0.0651 | 0.0436 | 0.0261 | −0.1598 *** | −0.0608 | −0.0008 | 0.0308 | ||

| (0.0832) | (0.0837) | (0.0835) | (0.0845) | (0.0836) | (0.0856) | (0.0924) | (0.0812) | (0.0398) | (0.0436) | (0.0749) | (0.0848) | |||||

| Urbanisation level | ln(urb) | c4 | 0.0250 | 0.0237 | 0.0019 | 0.0317 | 0.0118 | 0.0503 | 0.1071 | −0.0067 | −0.1299 | −0.0266 | −0.0007 | 0.0248 | ||

| (0.0746) | (0.0730) | (0.0756) | (0.0738) | (0.0688) | (0.0720 | (0.1016) | (0.0812) | (0.0758) | (0.0916) | (0.0659) | (0.0732) | |||||

| Growth of the labour force | Δln(lf) | c5 | 0.1963 *** | 0.1959 *** | 0.1952 *** | 0.1926 *** | 0.2003 *** | 0.1930 *** | 0.1772 ** | 0.1938 *** | 0.09386 ** | 0.1265 *** | 0.1816 ** | 0.1686 *** | ||

| (0.0531) | (0.0523) | (0.0538) | (0.0546) | (0.0560) | (0.0543) | (0.0715) | (0.0608) | (0.0382) | (0.0463) | (0.0735) | (0.0557) | |||||

| Gross capital formation | gcf | c6 | 0.0042 ** | 0.0042 ** | 0.0034 * | 0.0043 ** | 0.0042 ** | 0.0042 ** | 0.0049 | 0.0030 * | 0.0018 | 0.0000 | 0.0038 ** | 0.0035 | ||

| (0.0019) | (0.0019) | (0.0018) | (0.0020) | (0.0019) | (0.0019) | (0.0031) | (0.0018) | (0.0026) | (0.0024) | (0.0019) | (0.0023) | |||||

| Squared Gross capital formation | gcf2 | c7 | −0.0001 *** | −0.0001 *** | −0.0000 ** | −0.0001 *** | −0.0001 *** | −0.0001 *** | −0.0001 ** | −0.0000 ** | −0.0000 | −0.0000 | −0.0001 *** | −0.0000 ** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Openness to trade | ln(opn) | c8 | 0.0597 *** | 0.0597 *** | 0.0525 *** | 0.0599 *** | 0.0589 *** | 0.0584 *** | 0.0630 *** | 0.0594 *** | 0.0616 *** | 0.0693 *** | 0.0517 *** | 0.0517 *** | ||

| (0.0164) | (0.0164) | (0.0153) | (0.0165) | (0.0157) | (0.0176) | (0.0183) | (0.0156) | (0.0178) | (0.0204) | (0.0167) | (0.0187) | |||||

| Foreign direct investment | fdi | c9 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | 0.0000 | −0.0000 ** | −0.0000 | −0.0003 *** | −0.0000 | −0.0000 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Government size | ln(gov) | c10 | −0.0235 * | −0.0234 ** | −0.0270 ** | −0.0247 ** | −0.0248 * | −0.0251 ** | −0.0288 | −0.0134 | −0.0083 | 0.0016 | −0.0225 | −0.0173 | ||

| (0.0120) | (0.0118) | (0.0109) | (0.0122) | (0.0139) | (0.0117) | (0.0203) | (0.0160) | (0.0178) | (0.0159) | (0.0136) | (0.0124) | |||||

| Research and development | ln(r&d) | c11 | −0.0029 | −0.0031 | −0.0052 | −0.0015 | −0.0037 | −0.0013 | −0.0160 * | −0.0033 | −0.0051 | −0.0144 | −0.0019 | −0.0098 | ||

| (0.0119) | (0.0120) | (0.0118) | (0.0123) | (0.0130) | (0.0130) | (0.0081) | (0.0111) | (0.0094) | (0.0107) | (0.0132) | (0.0079) | |||||

| Inflation | Δln(cpi) | c12 | 0.0076 | 0.0087 | −0.0137 | 0.0130 | 0.0138 | −0.0149 | 0.0143 | −0.0186 | −0.0644 | −0.0230 | 0.0464 | −0.0055 | ||

| (0.0436) | (0.0445) | (0.0462) | (0.0413) | (0.0534) | (0.0488) | (0.0457) | (0.0391) | (0.0454) | (0.0392) | (0.0761) | (0.0489) | |||||

| Human capital | ln(hc) | c13 | 0.0076 | 0.0075 | 0.0126 | 0.0077 | 0.0068 | 0.0043 | 0.0042 | 0.0071 | 0.0060 | 0.0090 | 0.0080 | 0.0027 | ||

| (0.0096) | (0.0097) | (0.0101) | (0.0095) | (0.0109) | (0.0087) | (0.0133) | (0.0113) | (0.0113) | (0.0079) | (0.0102) | (0.0097) | |||||

| GDP per capita | ln(Y) | β | −0.1267 *** | −0.1267 *** | −0.1187 *** | −0.1325 *** | −0.1279 *** | −0.1313 *** | −0.1166 *** | −0.1469 *** | −0.1889 *** | −0.1570 *** | −0.1222 *** | −0.1363 *** | ||

| (0.0292) | (0.0293) | (0.0323) | (0.0329) | (0.0272) | (0.0302) | (0.0348) | (0.0247) | (0.0214) | (0.0167) | (0.0326) | (0.0349) | |||||

| Intercept | α | 0.6846 | 0.6846 | 0.6867 | 0.7745 | 0.6528 | 0.7309 | 0.4192 | 0.4118 | 1.1510 | 2.9360 | 1.6920 *** | 1.1710 | |||

| (0.9196) | (0.9196) | (0.9181) | (0.9107) | (0.9284) | (0.8402) | (1.018) | (1.095) | (0.8505) | (0.5449) | (0.5360) | (0.7877) | |||||

| Number of observations | 342 | 342 | 339 | 342 | 342 | 332 | 237 | 294 | 201 | 166 | 320 | 312 | ||||

| Within R2 | 0.7854 | 0.7854 | 0.7869 | 0.7861 | 0.7857 | 0.7904 | 0.8004 | 0.8204 | 0.8708 | 0.8683 | 0.7734 | 0.7884 | ||||

| Pesaran CD test for cross-sectional dependence (1) [p-value] | [0.213] | [0.1969] | [0.2122] | [0.211] | [0.2154] | [0.1967] | [0.1998] | [0.2004] | [0.1884] | [0.222] | [0.2212] | [0.1734] | ||||

| Test for differing group intercepts (2) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wald joint test on time dummies (3) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Hausman test (4) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wooldridge test (5) [p-value] | [0.1717] | [0.1532] | [0.1593] | [0.1667] | [0.1573] | [0.1673] | [0.1625] | [0.1756] | [0.1414] | [0.198] | [0.1779] | [0.1538] | ||||

| (36) | (37) | (38) | (39) | (40) | (41) | (42) | (43) | (44) | (45) | (46) | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Core Infrastructure (INFR) | ICT infrastructure | Fixed telephone | ln(ict_ft) | γ | 0.0109 | ||||||||||

| (0.0138) | |||||||||||||||

| ln(ict_ft)× inst_cc | φ | 0.0065 | |||||||||||||

| (0.0070) | |||||||||||||||

| Fixed broadband | ln(ict_fb) | γ | 0.0034 | ||||||||||||

| (0.0029) | |||||||||||||||

| ln(ict_fb)× inst_cc | φ | 0.0004 | |||||||||||||

| (0.0015) | |||||||||||||||

| Mobile cellular | ln(ict_mc) | γ | 0.02256 *** | ||||||||||||

| (0.0040) | |||||||||||||||

| ln(ict_mc)× inst_cc | φ | 0.0087 | |||||||||||||

| (0.0059) | |||||||||||||||

| Water and sanitation | Sanitation facilities | ln(ws_sf) | γ | 0.0028 | |||||||||||

| (0.0360) | |||||||||||||||

| ln(ws_sf)× inst_cc | φ | 0.0243 | |||||||||||||

| (0.0617) | |||||||||||||||

| Drinking water facilities | ln(ws_dwf) | γ | 0.0495 | ||||||||||||

| (0.0667) | |||||||||||||||

| ln(ws_dwf)× inst_cc | φ | 0.0135 | |||||||||||||

| (0.0984) | |||||||||||||||

| Transport infrastructure | Railways | ln(t_rw) | γ | 0.0164 | |||||||||||

| (0.0304) | |||||||||||||||

| ln(t_rw)× inst_cc | φ | 0.0096 | |||||||||||||

| (0.0182) | |||||||||||||||

| Roads | ln(t_r) | γ | 0.0018 | ||||||||||||

| (0.0088) | |||||||||||||||

| ln(t_r)× inst_cc | φ | 0.0002 | |||||||||||||

| (0.0094) | |||||||||||||||

| Inland waterways | ln(t_ww) | γ | 0.0117 | ||||||||||||

| (0.0154) | |||||||||||||||

| ln(t_ww)× inst_cc | φ | 0.0012 | |||||||||||||

| (0.0073) | |||||||||||||||

| Pipelines | ln(t_pl) | γ | 0.0154 ** | ||||||||||||

| (0.0064) | |||||||||||||||

| ln(t_pl)× inst_cc | φ | 0.0192 ** | |||||||||||||

| (0.0074) | |||||||||||||||

| Air transport | ln(t_ap) | γ | 0.0059 | ||||||||||||

| (0.0095) | |||||||||||||||

| ln(t_ap)× inst_cc | φ | 0.0090 | |||||||||||||

| (0.0093) | |||||||||||||||

| Energy | Electricity | ln(e_epc) | γ | 0.0423 *** | |||||||||||

| (0.0114) | |||||||||||||||

| ln(e_epc)× inst_cc | φ | 0.0335 *** | |||||||||||||

| (0.0114) | |||||||||||||||

| Institutions (Control of corruption) | inst_cc | c1 | 0.0354 | 0.0091 | 0.0074 | −0.0997 | 0.0722 | 0.0510 | 0.0114 | 0.0516 *** | 0.0404 *** | 0.0877 | 0.1067 *** | ||

| (0.0270) | (0.0071) | (0.0337) | (0.2802) | (0.4475) | (0.0812) | (0.0649) | (0.0166) | (0.0146) | (0.0705) | (0.0334) | |||||

| Population growth | Δln(pop) | c2 | −0.9488 | −1.0530 * | −0.9655 | −0.9132 | −0.8908 | −1.076 | −1.0570 | −0.0743 | −0.1499 | −0.9161 * | −0.8158 | ||

| (0.5802) | (0.6105) | (0.5911) | (0.5874) | (0.6150) | (0.7778) | (0.7048) | (0.2087) | (0.2597) | (0.5365) | (0.5364) | |||||

| Population density | ln(dens) | c3 | 0.0616 | 0.0571 | 0.0644 | 0.0575 | 0.0664 | 0.0553 | 0.0261 | −0.1542 *** | −0.0550 | −0.0065 | 0.0451 | ||

| (0.0838) | (0.0804) | (0.0861) | (0.0866) | (0.0823) | (0.0888) | (0.0818) | (0.0346) | (0.0417) | (0.0721) | (0.0830) | |||||

| Urbanisation level | ln(urb) | c4 | 0.0144 | 0.0008 | 0.0331 | 0.0413 | 0.0515 | 0.1317 | −0.0068 | −0.1850 ** | −0.0658 | 0.0169 | 0.0450 | ||

| (0.0744) | (0.0741) | (0.0718) | (0.0689) | (0.0688) | (0.1163) | (0.0838) | (0.0779) | (0.0921) | (0.0723) | (0.0801) | |||||

| Growth of the labour force | Δln(lf) | c5 | 0.1910 *** | 0.1963 *** | 0.1929 *** | 0.1942 *** | 0.1924 *** | 0.1790 ** | 0.1940 *** | 0.1055 ** | 0.1285 *** | 0.1831 ** | 0.1713 *** | ||

| (0.0499) | (0.0549) | (0.0543) | (0.0564) | (0.0545) | (0.0738) | (0.0583) | (0.0375) | (0.0477) | (0.0740) | (0.0523) | |||||

| Gross capital formation | gcf | c6 | 0.0042 ** | 0.0033 * | 0.0043 ** | 0.0039 * | 0.0042 ** | 0.0045 | 0.0030 * | 0.0017 | −0.0005 | 0.0044 ** | 0.0027 | ||

| (0.0019) | (0.0018) | (0.0020) | (0.0019) | (0.0017) | (0.0029) | (0.0018) | (0.0024) | (0.0024) | (0.0020) | (0.0018) | |||||

| Squared Gross capital formation | gcf2 | c7 | −0.0001 *** | −0.0000 *** | −0.0001 *** | −0.0001 ** | −0.0001 *** | −0.0001 * | −0.0000 ** | −0.0000 | −0.0000 | −0.0001 *** | −0.0000 ** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Openness to trade | ln(opn) | c8 | 0.0620 *** | 0.0523 *** | 0.0601 *** | 0.0588 *** | 0.0583 *** | 0.0667 *** | 0.0594 *** | 0.0651 *** | 0.0719 *** | 0.0502 *** | 0.0457 ** | ||

| (0.0165) | (0.0151) | (0.0159) | (0.0164) | (0.0179) | (0.0168) | (0.0152) | (0.0187) | (0.0205) | (0.0161) | (0.0171) | |||||

| Foreign direct investment | fdi | c9 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | 0.0000 | −0.0000 *** | −0.0000 | −0.0003 *** | −0.0000 | −0.0000 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Government size | ln(gov) | c10 | −0.0244 * | −0.0268 ** | −0.0244 * | −0.0246 * | −0.0248 * | −0.0278 | −0.0134 | −0.0072 | 0.0011 | −0.0188 | −0.0247 * | ||

| (0.0119) | (0.0110) | (0.0126) | (0.0140) | (0.0131) | (0.0223) | (0.0163) | (0.0182) | (0.0162) | (0.0133) | (0.0127) | |||||

| Research and development | ln(r&d) | c11 | −0.0018 | −0.0053 | −0.0015 | −0.0011 | −0.0013 | −0.0181 * | −0.0033 | −0.0055 | −0.0156 | −0.0015 | −0.0181 ** | ||

| (0.0121) | (0.0119) | (0.0122) | (0.0133) | (0.0130) | (0.0091) | (0.0118) | (0.0092) | (0.0106) | (0.0131) | (0.0078) | |||||

| Inflation | Δln(cpi) | c12 | 0.0139 | −0.0163 | 0.0097 | −0.0119 | −0.0130 | 0.0102 | −0.0188 | −0.0671 | −0.0389 | 0.0609 | 0.0061 | ||

| (0.0463) | (0.0438) | (0.0473) | (0.0601) | (0.0499) | (0.0409) | (0.0424) | (0.0459) | (0.0443) | (0.0806) | (0.0479) | |||||

| Human capital | ln(hc) | c13 | 0.0098 | 0.0128 | 0.0081 | 0.0035 | 0.0042 | 0.0038 | 0.0071 | 0.0063 | 0.0062 | 0.0059 | 0.0091 | ||

| (0.0104) | (0.0101) | (0.0103) | (0.0110) | (0.0088) | (0.0133) | (0.0120) | (0.0112) | (0.0081) | (0.0109) | (0.0100) | |||||

| GDP per capita | ln(Y) | β | −0.1246 *** | −0.1180 *** | −0.1317 *** | −0.1274 *** | −0.1319 *** | −0.1139 *** | −0.1469 *** | −0.1889 *** | −0.1573 *** | −0.1227 *** | −0.1617 *** | ||

| (0.0304) | (0.0326) | (0.0315) | (0.0285) | (0.0327) | (0.0349) | (0.0247) | (0.0194) | (0.0185) | (0.0322) | (0.0308) | |||||

| Intercept | α | 0.6379 | 0.6379 | 0.7850 | 0.6380 | 0.6340 | 0.3817 | 0.1719 | 1.1520 | 3.1240 *** | 1.8500 *** | 1.1290 | |||

| (0.9413) | (0.9413) | (0.8958) | (0.8968) | (0.8677) | (0.9015) | (1.1740) | (0.8632) | (0.4747) | (0.5711) | (0.8060) | |||||

| Number of observations | 342 | 339 | 342 | 332 | 332 | 237 | 294 | 201 | 166 | 320 | 312 | ||||

| Within R2 | 0.7866 | 0.7869 | 0.7861 | 0.7896 | 0.7905 | 0.8017 | 0.8204 | 0.8772 | 0.8707 | 0.7770 | 0.8043 | ||||

| Pesaran CD test for cross-sectional dependence (1) [p-value] | [0.1916] | [0.1748] | [0.2423] | [0.1981] | [0.2106] | [0.1955] | [0.2109] | [0.2252] | [0.1825] | [0.192] | [0.1976] | ||||

| Test for differing group intercepts (2) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wald joint test on time dummies (3) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Hausman test (4) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wooldridge test (5) [p-value] | [0.1705] | [0.1523] | [0.1963] | [0.1578] | [0.1783] | [0.1552] | [0.1536] | [0.1986] | [0.1532] | [0.1357] | [0.1491] | ||||

| (47) | (48) | (49) | (50) | (51) | (52) | (53) | (54) | (55) | (56) | (57) | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Core Infrastructure (INFR) | ICT infrastructure | Fixed telephone | ln(ict_ft) | γ | 0.0325 | ||||||||||

| (0.0333) | |||||||||||||||

| ln(ict_ft)× inst_rq | φ | 0.0188 | |||||||||||||

| (0.0198) | |||||||||||||||

| Fixed broadband | ln(ict_fb) | γ | 0.0025 | ||||||||||||

| (0.0034) | |||||||||||||||

| ln(ict_fb)× inst_rq | φ | 0.0021 | |||||||||||||

| (0.0027) | |||||||||||||||

| Mobile cellular | ln(ict_mc) | γ | 0.3764 ** | ||||||||||||

| (0.1577) | |||||||||||||||

| ln(ict_mc)× inst_rq | φ | 0.3308 * | |||||||||||||

| (0.1755) | |||||||||||||||

| Water and sanitation | Sanitation facilities | ln(ws_sf) | γ | 0.0608 | |||||||||||

| (0.0481) | |||||||||||||||

| ln(ws_sf)× inst_rq | φ | 0.0289 | |||||||||||||

| (0.0223) | |||||||||||||||

| Drinking water facilities | ln(ws_dwf) | γ | 0.0106 | ||||||||||||

| (0.0136) | |||||||||||||||

| ln(ws_dwf)× inst_rq | φ | 0.0129 | |||||||||||||

| (0.0111) | |||||||||||||||

| Transport | Railways | ln(t_rw) | γ | 0.0378 | |||||||||||

| (0.0304) | |||||||||||||||

| ln(t_rw)× inst_rq | φ | 0.0186 | |||||||||||||

| (0.0183) | |||||||||||||||

| Roads | ln(t_r) | γ | 0.0259 | ||||||||||||

| (0.0240) | |||||||||||||||

| ln(t_r)× inst_rq | φ | 0.0133 | |||||||||||||

| (0.0102) | |||||||||||||||

| Inland waterways | ln(t_ww) | γ | 0.0361 | ||||||||||||

| (0.0445) | |||||||||||||||

| ln(t_ww)× inst_rq | φ | 0.0089 | |||||||||||||

| (0.0242) | |||||||||||||||

| Pipelines | ln(t_pl) | γ | 0.0541 *** | ||||||||||||

| (0.0131) | |||||||||||||||

| ln(t_pl)× inst_rq | φ | 0.0283 ** | |||||||||||||

| (0.0111) | |||||||||||||||

| Air transport | ln(t_ap) | γ | 0.0034 | ||||||||||||

| (0.0133) | |||||||||||||||

| ln(t_ap)× inst_rq | φ | 0.0024 | |||||||||||||

| (0.0119) | |||||||||||||||

| Energy | Electricity | ln(e_epc) | γ | 0.1426 *** | |||||||||||

| (0.0349) | |||||||||||||||

| ln(e_epc)× inst_rq | φ | 0.1057 *** | |||||||||||||

| (0.0314) | |||||||||||||||

| Institutions (Regulatory Quality) | inst_rq | c1 | 0.0465 | 0.0242 *** | 0.0432 | 0.4437 *** | 1.696 ** | 0.0950 | 0.1096 | 0.0216 | 0.0579 ** | 0.0410 | 0.0937 | ||

| (0.0714) | (0.0078) | (0.0549) | (0.1355) | (0.7200) | (0.0757) | (0.0720) | (0.0577) | (0.0233) | (0.0919) | (0.0662) | |||||

| Population growth | Δln(pop) | c2 | −1.4100 * | −1.4700 * | −1.3860 * | −1.2210 * | −1.2810 * | −1.8640 ** | −1.6230 ** | −1.2210 ** | −0.4674 | −1.2530 | −1.600 ** | ||

| (0.6998) | (0.7174) | (0.6923) | (0.6253) | (0.6691) | (0.7228) | (0.8077) | (0.4958) | (0.3981) | (0.7398) | (0.6899) | |||||

| Population density | ln(dens) | c3 | 0.1142 | 0.1275 | 0.1355 | 0.0768 | 0.1164 * | 0.0946 | 0.0824 | −0.1094 | −0.0822 | 0.1431 | 0.0723 | ||

| (0.0798) | (0.0823) | (0.0862) | (0.0730) | (0.0702) | (0.0843) | (0.0746) | (0.1002) | (0.1001) | (0.0858) | (0.0802) | |||||

| Urbanisation level | ln(urb) | c4 | 0.0222 | −0.0267 | 0.0298 | 0.0028 | 0.0433 | −0.0163 | −0.0491 | −0.2801 ** | −0.4700 ** | 0.01387 | 0.0199 | ||

| (0.0886) | (0.0921) | (0.0990) | (0.0848) | (0.0816) | (0.1673) | (0.1070) | (0.1072) | (0.2060) | (0.1007) | (0.0979) | |||||

| Growth of the labour force | Δln(lf) | c5 | 0.2154 ** | 0.1985 ** | 0.2101 ** | 0.2044 ** | 0.2058 ** | 0.1997 * | 0.2362 ** | 0.0720 | 0.0295 | 0.3143 *** | 0.2302 *** | ||

| (0.0859) | (0.0906) | (0.0794) | (0.0928) | (0.0921) | (0.1154) | (0.0931) | (0.0753) | (0.1058) | (0.1116) | (0.0866) | |||||

| Gross capital formation | gcf | c6 | 0.0064 ** | 0.0059 * | 0.0069 ** | 0.0060 ** | 0.0056 * | 0.0080 * | 0.0051 | 0.0030 | −0.0017 | 0.0065 * | 0.0071 ** | ||

| (0.0030) | (0.0032) | (0.0033) | (0.0028) | (0.0030) | (0.0039) | (0.0032) | (0.0047) | (0.0036) | (0.0035) | (0.0032) | |||||

| Squared Gross capital formation | gcf2 | c7 | −0.0001 ** | −0.0001 ** | −0.0001 ** | −0.0001 ** | −0.0001 ** | −0.0002 ** | −0.0001 * | −0.0000 | 0.0000 | −0.0001 ** | −0.0002 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Openness to trade | ln(opn) | c8 | 0.1117 *** | 0.1121 *** | 0.1144 *** | 0.1138 *** | 0.1159 *** | 0.1136 *** | 0.1185 *** | 0.1374 *** | 0.1342 *** | 0.1097 *** | 0.0709 *** | ||

| (0.0221) | (0.0249) | (0.0222) | (0.0222) | (0.0246) | (0.0226) | (0.0260) | (0.0361) | (0.0315) | (0.0266) | (0.0243) | |||||

| Foreign direct investment | fdi | c9 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | 0.0002 | −0.0000 | 0.0000 | −0.0002 | −0.0000 | −0.0000 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0002) | (0.0000) | (0.0000) | |||||

| Government size | ln(gov) | c10 | −0.0659 ** | −0.0724 *** | −0.0712 ** | −0.0584 | −0.0681 ** | −0.0885 ** | −0.0667 * | −0.0362 | −0.0193 | −0.0711 ** | −0.0778 ** | ||

| (0.0309) | (0.0259) | (0.0284) | (0.0359) | (0.0335) | (0.0367) | (0.0365) | (0.0225) | (0.0148) | (0.0326) | (0.0312) | |||||

| Research and development | ln(r&d) | c11 | 0.0020 | 0.0022 | 0.0054 | −0.0009 | 0.0013 | −0.0153 | 0.0006 | −0.0232 | −0.0381 * | 0.0087 | −0.0024 | ||

| (0.0161) | (0.0137) | (0.0140) | (0.0153) | (0.0150) | (0.0149) | (0.0155) | (0.0161) | (0.0187) | (0.0173) | (0.0124) | |||||

| Inflation | Δln(cpi) | c12 | −0.1965 *** | −0.1745 *** | −0.1985 ** | −0.2848 *** | −0.2940 *** | −0.1689 ** | −0.1641 ** | −0.2563 *** | −0.2982 ** | −0.3186 ** | −0.1251 | ||

| (0.0641) | (0.0609) | (0.0738) | (0.0648) | (0.0613) | (0.0757) | (0.0695) | (0.0756) | (0.1073) | (0.1151) | (0.0923) | |||||

| Human capital | ln(hc) | c13 | −0.0018 | 0.0023 | 0.0020 | 0.0046 | −0.0019 | −0.0046 | −0.0039 | 0.0008 | 0.0025 | −0.0070 | 0.0064 | ||

| (0.0120) | (0.0115) | (0.0119) | (0.0118) | (0.0102) | (0.0149) | (0.0143) | (0.0151) | (0.0130) | (0.0122) | (0.0108) | |||||

| GDP per capita | ln(Y) | β | −0.1617 *** | −0.1491 *** | −0.1726 *** | −0.1568 *** | −0.1565 *** | −0.1615 *** | −0.1860 *** | −0.2333 *** | −0.2018 *** | −0.1729 *** | −0.2007 *** | ||

| (0.0386) | (0.0412) | (0.0414) | (0.0353) | (0.0396) | (0.0329) | (0.0304) | (0.0341) | (0.0382) | (0.0470) | (0.0450) | |||||

| Intercept | α | 0.7758 | 0.7758 | 0.7087 | 0.5536 | 1.4570 | 2.0170 * | 0.9702 | 1.1970 | 3.7890 *** | 4.0650 *** | 0.6466 | |||

| (0.9979) | (0.9979) | (0.9711) | (1.0330) | (0.9200) | (1.0960) | (1.2040) | (0.8823) | (1.0380) | (1.3680) | (1.1140) | |||||

| Number of observations | 342 | 339 | 342 | 342 | 332 | 237 | 294 | 201 | 166 | 320 | 312 | ||||

| Within R2 | 0.7537 | 0.7535 | 0.7561 | 0.7631 | 0.7669 | 0.7824 | 0.7790 | 0.8305 | 0.8221 | 0.7473 | 0.7515 | ||||

| Pesaran CD test for cross-sectional dependence (1) [p-value] | [0.2007] | [0.1978] | [0.2127] | [0.213] | [0.2149] | [0.1992] | [0.205] | [0.2017] | [0.2275] | [0.2236] | [0.2188] | ||||

| Test for differing group intercepts (2) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wald joint test on time dummies (3) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Hausman test (4) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wooldridge test (5) [p-value] | [0.1545] | [0.1546] | [0.1674] | [0.1493] | [0.159] | [0.1434] | [0.1646] | [0.1668] | [0.1595] | [0.1625] | [0.1607] | ||||

References

- Boopen, S. Transport Infrastructure and Economic Growth: Evidence from Africa Using Dynamic Panel Estimates. Empir. Econ. Lett. 2006, 5, 37–52. [Google Scholar]

- Kumo, W.L. Infrastructure Investment and Economic Growth in South Africa: A Granger Causality Analysis; Working Paper Series No. 160; African Development Bank: Tunis, Tunisia, 2012. [Google Scholar]

- Donou-Adonsou, F.; Lim, S.; Mathey, S.A. Technological Progress and Economic Growth in Sub-Saharan Africa: Evidence from Telecommunications Infrastructure. Int. Adv. Econ. Res. 2016, 22, 65–75. [Google Scholar] [CrossRef]

- Saidi, M.; Shahbaz, M.; Akhtar, P. The long-run relationships between transport energy consumption, transport infra-structure, and economic growth in MENA countries. Transp. Res. Part A 2018, 111, 78–95. [Google Scholar]

- Haftu, G.G. Information communications technology and economic growth in Sub-Saharan Africa: A panel data approach. Telecomm. Policy 2019, 43, 88–99. [Google Scholar] [CrossRef]

- Zhang, X. Transport infrastructure, spatial spillover and economic growth: Evidence from China. Front. Econ. China 2008, 3, 585–597. [Google Scholar] [CrossRef]

- Hong, J.; Chu, Z.; Wang, Q. Transport infrastructure and regional economic growth: Evidence from China. Transportation 2011, 38, 737–752. [Google Scholar] [CrossRef]

- Yu, N.; De Jong, M.; Storm, S.; Mi, J. Transport Infrastructure, Spatial Clusters and Regional Economic Growth in China. Transp. Rev. 2012, 32, 3–28. [Google Scholar] [CrossRef]

- Lin, T.-Y.; Chiu, S.-H. Sustainable Performance of Low-Carbon Energy Infrastructure Investment on Regional Develop-ment: Evidence from China. Sustainability 2018, 10, 4657. [Google Scholar] [CrossRef] [Green Version]

- Yang, F.; Zhang, S.; Sun, C. Energy infrastructure investment and regional inequality: Evidence from China’s power grid. Sci. Total Environ. 2020, 749, 142384. [Google Scholar] [CrossRef]

- Wang, N.; Zhu, Y.; Yang, T. The impact of transportation infrastructure and industrial agglomeration on energy efficiency: Evidence from China’s industrial sectors. J. Clean. Prod. 2020, 244, 118708. [Google Scholar] [CrossRef]

- Pradhan, R.P.; Bagchi, T.P. Effects of transport infrastructure on economic growth in India: The VECM approach. Res. Transp. Econ. 2013, 38, 139–148. [Google Scholar] [CrossRef]

- Mitra, A.; Sharma, C.; Véganzonès-Varoudakis, M.-A. Infrastructure, information & communication technology and firms’ productive performance of the Indian manufacturing. J. Policy Model. 2016, 38, 353–371. [Google Scholar]

- Maparu, T.S.; Mazumder, T.N. Transport infrastructure, economic development and urbanisation in India (1990–2011): Is there any causal relationship? Transp. Res. Part A 2017, 100, 319–336. [Google Scholar]

- Awan, A.G.; Anum, V. Impact of Infrastructure Development on Economic growth: A Case study of Pakistan. Int. J. Dev. Econ. 2014, 2, 1–15. [Google Scholar]

- Batool, I.; Goldman, K. The role of public and private transport infrastructure capital in Economic growth. Evidence from Pakistan. Res. Transp.Econ. 2020, 88, 100886. [Google Scholar] [CrossRef]

- Elburz, Z.; Cubukcu, K.M. Spatial effects of transport infrastructure on regional growth: The case of Turkey. Spat. Inf. Res. 2021, 29, 19–30. [Google Scholar] [CrossRef]

- Muvawala, J.; Sebukeera, H.; Ssebulime, K. Socio-economic impacts of transport infrastructure investment in Uganda: In-sight from frontloading expenditure on Uganda’s urban roads and highways. Res. Transp.Econ. 2020, 88, 100971. [Google Scholar] [CrossRef]

- Untari, R.; Priyarson, D.S.; Novianti, T. Impact of Information and Communication Technology (ICT) Infrastructure on Economic Growth and Income Inequality in Indonesia. Int. J. Sci. Res. Sci. Eng. Technol. 2019, 6, 109–116. [Google Scholar] [CrossRef]

- Kallal, R.; Haddaji, A.; Ftiti, Z. ICT diffusion and economic growth: Evidence from the sectorial analysis of a periphery country. Technol. Forecast. Soc. Change 2021, 162, 120403. [Google Scholar] [CrossRef]

- Arif, U.; Javid, M.; Khan, F.N. Productivity impact of infrastructure development in Asia. Econ. Syst. 2020, 45, 1–12. [Google Scholar] [CrossRef]

- Wang, C.; Lim, M.K.; Zhang, X.; Zhao, L.; Lee, P.T.-W. Railway and road infrastructure in the Belt and Road Initiative countries: Estimating the impact of transport infrastructure on economic growth. Transp. Res. Part A 2020, 134, 288–307. [Google Scholar] [CrossRef]

- Sridhar, K.S.; Sridhar, V. Telecommunications infrastructure and economic growth: Evidence from developing countries. Appl. Econ. Int. Dev. 2007, 7, 37–61. [Google Scholar]

- Maneejuk, P.; Yamaka, W. An analysis of the impacts of telecommunications technology and innovation on economic growth. Telecomm. Policy 2020, 44, 102038. [Google Scholar] [CrossRef]

- European Commission; European Economy. Infrastructure in the EU: Developments and Impact on Growth; Occasional Papers 203; European Comission: Brussels, Belgium, 2014. [Google Scholar]

- Palei, T. Assessing The Impact of Infrastructure on Economic Growth and Global Competitiveness. Procedia Econ. Financ. 2015, 23, 168–175. [Google Scholar] [CrossRef] [Green Version]

- Carruthers, R. Transport Infrastructure. In Economic and Social Development of the Southern and Eastern Mediterranean Countries; Ayadi, R., Dabrowski, M., De Wulf, L., Eds.; Springer: Cham, Switzerland, 2015. [Google Scholar]

- Meersman, H.; Nazemzadeh, M. The contribution of transport infrastructure to economic activity: The case of Belgium. Case Stud. Transp. Policy 2017, 5, 316–324. [Google Scholar] [CrossRef]

- Cigu, E.; Agheorghiesei, D.T.; Gavriluta (Vatamanu), A.F.; Toader, E. Transport Infrastructure Development, Public Performance and Long-Run Economic Growth: A Case Study for the Eu-28 Countries. Sustainability 2019, 11, 67. [Google Scholar] [CrossRef] [Green Version]

- Luz, J.; Reis, J.; Leite, F.A.; Araújo, K.; Moritz, G. Effects of Transport Infrastructure in the Economic Development. In Proceedings of the IFIP In-ternational Conference on Advances in Production Management Systems (APMS), Iguassu Falls, Brazil, 3–7 September 2016; Springer: New York, NY, USA, 2016; Volume 488, pp. 633–640. [Google Scholar]

- Lenz, N.V.; Skender, H.P.; Adelajda Mirković, P.A. The macroeconomic effects of transport infrastructure on economic growth: The case of Central and Eastern, E.U. member states. Econ. Res. Ekon Istraz. 2018, 31, 1953–1964. [Google Scholar] [CrossRef]

- Crescenzi, R.; Rodríguez-Pose, A. Infrastructure and regional growth in the European Union. Pap. Reg. Sci. 2012, 91, 487–513. [Google Scholar] [CrossRef]

- Farhadi, M. Transport infrastructure and long-run economic growth in OECD countries. Transp. Res. Part A 2015, 74, 73–90. [Google Scholar] [CrossRef]

- Kyriacou, A.P.; Muinelo-Gallo, L.; Roca-Sagalé. The efficiency of transport infrastructure investment and the role of government quality: An empirical analysis. Transp. Policy 2019, 74, 93–102. [Google Scholar] [CrossRef]

- Madden, G.; Savage, S.J. CEE telecommunications investment and economic Growth. Inf. Econ. Policy 1998, 10, 173–195. [Google Scholar] [CrossRef] [Green Version]

- Pohjola, M. Information Technology and Economic Growth: A Cross-Country Analysis; WIDER Working Papers No. 173; The United Nations University & World Institute for Development Economic Research; UNU Wider: Helsinki, Finland, 2020. [Google Scholar]

- Datta, A.; Agarwal, S. Telecommunications and economic growth: A panel data approach. Appl. Econ. 2004, 36, 1649–1654. [Google Scholar] [CrossRef]

- Toader, E.; Firtescu, B.N.; Roman, A.; Anton, S.G. Impact of Information and Communication Technology Infrastructure on Economic Growth: An Empirical Assessment for the EU Countries. Sustainability 2018, 10, 3750. [Google Scholar] [CrossRef] [Green Version]

- Nair, M.; Pradhan, R.P.; Arvin, M.B. Endogenous dynamics between R&D, ICT and economic growth: Empirical evidence from the OECD countries. Technol. Soc. 2020, 62, 101315. [Google Scholar] [CrossRef]

- Stupak, J.M. Economic Impact of Infrastructure Investment. Congr. Res. Serv. 2018, 7-5700, 1–16. [Google Scholar] [CrossRef]

- Rietveld, P.; Bruinsma, F. Is Transport Infrastructure Effective? Transport Infrastructure and Accessibility: Impact on the Space Economy; Springer: Berlin/Heidelberg, Germany, 1998. [Google Scholar] [CrossRef]

- Azevedo, I.M.L. Consumer End-Use Energy Efficiency and Rebound Effects. Annu. Rev. Environ. Resour. 2014, 39, 393–418. [Google Scholar] [CrossRef] [Green Version]

- Sanctuary, M.; Hakan, T.; Laurence, H. Making Water a Part of Economic Development: The Economic Benefits of Improved Water Management and Services. SIWI Report. 2005. Available online: https://www.who.int/water_sanitation_health/waterandmacroecon.pdf (accessed on 15 December 2021).

- Wang, J.; Zuoa, W.; Rhode-Barbarigosb, L.; Lua, X.; Wangc, J.; Lin, Y. Literature review on modeling and simulation of energy infrastructures from a resilience perspective. Reliab. Eng. Syst. Saf. 2019, 183, 360–373. [Google Scholar] [CrossRef]

- Brambor, T.; Clark, W.; Golder, M. Understanding Interaction Models: Improving Empirical Analyses. Polit. Anal. 2006, 14, 63–82. [Google Scholar] [CrossRef] [Green Version]

- Panizza, U.; Presbitero, A.F. Public debt and economic growth: Is there a causal effect? J. Macroecon. 2014, 41, 21–41. [Google Scholar] [CrossRef] [Green Version]

- Newey, W.K.; West, K.D. Hypothesis testing with efficient method of moments estimation. Int. Econ. Rev. 1987, 28, 777–787. [Google Scholar] [CrossRef]

- Abreu, M.; De Groot, R.J. A meta-analysis of β-convergence: The legendary 2%. J. Econ. Surv 2005, 19, 389–420. [Google Scholar] [CrossRef]

- Welsh Government. Code of Best Practice on Mobile Phone Network Development for Wales; Welsh Government: Cardiff, UK, 2021. [Google Scholar]

- Girard, J.; Gruber, H. Telecommunication Network Development and Investment in The European Union; European In-vestment Bank: Luxembourg, 1996; Available online: https://www.eib.org/en/publications/telecommunications-network-development (accessed on 17 March 2022).

- European Commission. Europe’s Digital Decade: Commission Sets the Course towards a Digital Empowered Europe by 2030. Europe’s Digital Compass; European Commission: Brusells, Belgium, 2021; Available online: https://ec.europa.eu/commission/presscorner/detail/en/IP_21_983 (accessed on 17 March 2022).

- World Economic Forum. The Impact of 5G: Creating New Value across Industries and Society; PWC Global: Geneva, Switzerland, 2020. [Google Scholar]

- WaterAid. The Financial Landscape of Water and Sanitation: Opportunities to Improve WASH ODA From The European Union, France, Germany and Spain; Coalition-EAU: London, UK, 2021; Available online: https://www.coalition-eau.org/wp-content/uploads/eu-report-march-2021-a4-en-final.pdf (accessed on 17 March 2022).

- European Commission. Cohesion Funds and European Regional Development Funds Investing in Water Services. Member States Allocate Different amount to Water Investment; European Commission: Brussels, Belgium, 2020; Available online: https://cohesiondata.ec.europa.eu/stories/s/In-profile-EU-investments-in-clean-water/4p6c-nzcb/#cohesion-fund-and-european-regional-development-fund-investing-in-water-services (accessed on 17 March 2022).

- EurEau. Europe’s Water in Figures. An Overview of The European Drinking Water and Waste Water Sector; The European Federation of National Association of Water Services: Brusells, Belgium, 2017; Available online: https://www.eureau.org/resources/publications/1460-eureau-data-report-2017-1/file (accessed on 17 March 2022).

- EurEau. In The Governance of Water Services in Europe; The European Federation of National Association of Water Services: Brusells, Belgium, 2020; Available online: https://www.eureau.org/resources/publications/5268-the-governance-of-water-services-in-europe-2020-edition-2/file (accessed on 17 March 2022).

- European Commission. Blending in the Water and Aanitation Sector; Tools and Methods Series Reference Document No 21; European Commission: Brusells, Belgium, 2015. [Google Scholar]

- Water Europe. Technology & Innovation. In The Value of Water. Multiple Waters for Multiple Purposes and Users. Towards a Future-Proof Model for a European Water-Smart Society; Water Europe Technology and Innovation: Brusells, Belgium, 2020; Available online: https://watereurope.eu/wp-content/uploads/2020/04/WE-Water-Vision-english_online.pdf (accessed on 20 March 2022).

- OECD. The Roundtable on Financing Water. Discussion Highlights; OECD Water: Paris, France, 2020; Available online: https://www.oecd.org/water/6th-Roundtable-on-Financing-Water-in-Europe-Summary-and-Highlights.pdf (accessed on 20 March 2022).

- Rail Baltica. 10 Benefits from the Rail Baltica Project Implementation. Available online: https://www.railbaltica.org/benefits/ (accessed on 30 January 2022).

- Hazenberg, R.; Bajwa-Patel, M. A Review of The Impact of Waterway Restoration; University of Northampton: Northampton, UK, 2014; Available online: https://canalrivertrust.org.uk/media/library/6337.pdf (accessed on 30 January 2022).

- Chen, A.; Li, Y.; Nie, T.; Liu, R. Does Transport Infrastructure Inequality Matter for Economic Growth? Evidence from China. Land 2021, 10, 874. [Google Scholar] [CrossRef]

- Canning, D.; Pedroni, P. The Effects of Infrastructure on Long Run Economic Growth (Working Papers 2004-04) Department of Economics; Williams College: Williamstown, MA, USA, 2004. [Google Scholar]

- European Commission. The European Union–What It Is And What It Does; European Union: Brussels, Belgium, 2021. Available online: https://op.europa.eu/webpub/com/eu-what-it-is/en/#chapter2_16 (accessed on 20 March 2022).

- European Commission. REPowerEU: Joint Eropean Action For More Affordable, Secure And Sustainable Energy; European Commission: Strasbourg, France, 2022; Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_22_1511 (accessed on 22 March 2022).

- Pandey, V. Energy Infrastructure for Sustainable Development. In Affordable and Clean Energy; Filho, W.L., Azul, A.M., Brandli, L., Salvia, A.L., Wall, T., Eds.; Springer: Cham, Switzerland, 2020; pp. 1–13. [Google Scholar]

- Fruhmann, C.; Tuerk, A. Renewable Energu Support Policies in Europe. Climate Policy Info HUB. Available online: https://climatepolicyinfohub.eu/renewable-energy-support-policies-europe.html#:~:text=The%20overall%20European%20Union%20(EU,change%20legislation%20of%20the%20EU (accessed on 22 March 2022).

- Pradhan, R.P.; Mallik, G.; Bagchi, T.P. Information communication technology (ICT) infrastructure and economic growth: A causality evinced by cross-country panel data. IIMB Manag. Rev. 2018, 30, 91–103. [Google Scholar] [CrossRef]

- Calderón, C.; Servén, L. The Effects of Infrastructure development on Growth and Income Distribution; Working Papers No. 270; Central Bank of Chile: Warshington, DC, USA, 2004. [Google Scholar]

- Apurv, R.; Uzma, S.H. The impact of infrastructure investment and development on economic growth on BRICS. Indian Growth Dev. Rev. 2020, 14, 122–147. [Google Scholar] [CrossRef]

| Type of Infrastructure | Impact Transmission Channels |

|---|---|

| Transport | TI development → increase connectivity → enchase market accessibility → increase business activity → increase flow of resources → stimulate innovations → economic growth [11] |

| TI development → reduction generalised transport cost → increase productivity (added value) → economic growth [41] | |

| Information and communication (ICTI) | ICTI development → production ICT goods and services → economic growth [5,38] |

| ICT infrastructure development → usage ICT goods and services in other sectors → efficiency and productivity growth → economic growth [5,38] | |

| ICT infrastructure development → facilitates knowledge acceptability and creation → human capital growth → economic growth [5,20] | |

| Energy (EI) | EI development → reduction of energy resources transfers cost → efficiency and productivity growth → economic growth [10] |

| EI development → reduction of energy prices → increase consumption or diversion of freed-up monetary resources to consumption of other products or savings → increase production → economic growth [10] | |

| EI development → energy losses reduction → reduction energy prices → saving generation → investments → economic growth [42] | |

| Water and sanitation (W&SI) | W&SI development → reduce the illness → improve human capital → increase labour productivity → economic growth [26,43] |

| Notation | Variable | Average | Min. | Max. | S. D. |

|---|---|---|---|---|---|

| Y | GDP per capita (constant 2010 US$) | 3.22 × 104 | 3.98 × 103 | 1.12 × 105 | 2.11 × 104 |

| pop | Population, total | 1.79 × 107 | 3.90 × 105 | 8.31 × 107 | 2.27 × 107 |

| dens | Population density (people per sq. km of land area) | 174 | 17 | 1.51 × 103 | 242 |

| urb | Urban population (% of total population) | 72.2 | 50.8 | 98.0 | 12.5 |

| lf | Labour force, total | 8.61 × 106 | 1.56 × 105 | 4.39 × 107 | 1.10 × 107 |

| gcf | Gross capital formation (% of GDP) | 22.9 | 11.9 | 46.0 | 4.56 |

| opn | Trade (% of GDP) | 117 | 45.4 | 408 | 64.9 |

| fdi | Foreign direct investment, net inflows (% of GDP) | 11.8 | −58.3 | 449 | 38.2 |

| gov | Total general government expenditure (% of GDP) | 44.7 | 24.5 | 64.8 | 6.55 |

| r&d_r | Researchers in R&D (per million people) | 2.90 × 103 | 321 | 8.00 × 103 | 1.62 × 103 |

| cpi | Consumer price index (2010 = 100) | 96.8 | 32 | 124 | 13.5 |

| hc | Tertiary educational attainment age group 30–34 (%) | 33.5 | 7.4 | 58.8 | 11.8 |

| inst_cc | Control of Corruption: Estimate | 1.03 | −0.491 | 2.47 | 0.792 |

| inst_rq | Regulatory Quality: Estimate | 1.20 | −0.109 | 2.10 | 0.443 |

| INFR—core infrastructure | |||||

| ict—ICT infrastructure | |||||

| ict_ft | Fixed telephone subscriptions (per 100 people) | 39.8 | 4.86 | 72.1 | 13.9 |

| ict_fb | Fixed broadband subscriptions (per 100 people) | 21.1 | 0.0119 | 46.0 | 12.6 |

| ict_mc | Mobile cellular subscriptions (per 100 people) | 107. | 9.23 | 172. | 29.6 |

| ws—water and sanitation infrastructure | |||||

| ws_sf | Share of the population with access to safely managed sanitation facilities (%) | 81.8 | 24.7 | 99.7 | 14.6 |

| ws_dwf | Share of the population with access to safely managed drinking water facilities (%) | 95.6 | 67.2 | 100. | 5.68 |

| t—transport infrastructure | |||||

| t_rw | Railway tracks (kilometres per 1000 sq. km of land area) | 88.9 | 21.2 | 258. | 60.9 |

| t_r | Roads (kilometres per 1000 sq. km of land area) | 1.48 × 103 | 112. | 9.68 × 103 | 1.52 × 103 |

| t_ww | Navigable inland waterways (kilometres per 1000 sq. km of land area) | 18.2 | 3.58 | 187. | 33.7 |

| t_pl | Pipelines operated (kilometres per 1000 sq. km of land area) | 10.7 | 0.411 | 24.5 | 5.56 |

| t_ap | Air passenger transport (passengers on board per 1000 inhabitants) | 2.77 × 103 | 80.0 | 1.45 × 104 | 2.17 × 103 |

| e—energy infrastructure | |||||

| e_epc | Electricity production capacities (megawatts per one mil. of GDP) | 0.0678 | 0.000 | 0.363 | 0.0469 |

| Type of Infrastructure and Variable | Notation | Coefficient | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Core Infrastructure (INFR) | ICT | Fixed telephone | ln(ict_ft) | γ | 0.0081 | |||||||||||

| (0.0085) | ||||||||||||||||

| Fixed broadband | ln(ict_fb) | 0.0033 | ||||||||||||||

| (0.0032) | ||||||||||||||||

| Mobile cellular | ln(ict_mc) | 0.0241 * | ||||||||||||||

| (0.0126) | ||||||||||||||||

| Water and sanitation | Sanitation facilities | ln(ws_sf) | 0.0328 | |||||||||||||

| (0.0347) | ||||||||||||||||

| Drinking water facilities | ln(ws_dwf) | 0.0736 | ||||||||||||||

| (0.0808) | ||||||||||||||||

| Transport | Railways | ln(t_rw) | 0.0085 | |||||||||||||

| (0.0178) | ||||||||||||||||

| Roads | ln(t_r) | 0.0122 | ||||||||||||||

| (0.0097) | ||||||||||||||||

| Inland waterways | ln(t_ww) | 0.0221 | ||||||||||||||

| (0.0320) | ||||||||||||||||

| Pipelines | ln(t_pl) | 0.0450 *** | ||||||||||||||

| (0.0118) | ||||||||||||||||

| Air transport | ln(t_ap) | 0.0030 | ||||||||||||||

| (0.0084) | ||||||||||||||||

| Energy | Electricity | ln(e_epc) | 0.0256 * | |||||||||||||

| (0.0136) | ||||||||||||||||

| Institutions (Control of corruption) | inst_cc | c1 | 0.0201 ** | 0.0211 *** | 0.0181 *** | 0.0237 ** | 0.0198 ** | 0.0174 ** | 0.0141 | 0.0192 ** | 0.0187 | 0.0280 *** | 0.0256 *** | 0.0186 ** | ||

| (0.0079) | (0.0076) | (0.0063) | (0.0091) | (0.0077) | (0.0073) | (0.0135) | (0.0085) | (0.0109) | (0.0068) | (0.0088) | (0.0079) | |||||

| Population growth | Δln(pop) | c2 | −1.4120 ** | −1.4510 ** | −1.4830 ** | −1.4290 ** | −1.3910 * | −1.3170 * | −1.7700 ** | −1.5790 * | −1.1610 ** | −0.4482 | −1.3010 * | −1.6700 ** | ||

| (0.6659) | (0.6590) | (0.6987) | (0.6714) | (0.7078) | (0.6726) | (0.6937) | (0.8153) | (0.4939) | (0.3559) | (0.7579) | (0.7426) | |||||

| Population density | ln(dens) | c3 | 0.0931 | 0.0911 | 0.0938 | 0.1133 | 0.0908 | 0.1075 | 0.0894 | 0.0549 | −0.1125 | −0.0965 | 0.1000 | 0.0513 | ||

| (0.0835) | (0.0835) | (0.0822) | (0.0903) | (0.0866) | (0.0833) | (0.0949) | (0.0787) | (0.0969) | (0.0863) | (0.0907) | (0.0881) | |||||

| Urbanisation level | ln(urb) | c4 | −0.0349 | −0.0228 | −0.0525 | −0.0078 | 0.0175 | −0.0028 | −0.0364 | −0.0771 | −0.3074 ** | −0.3036 * | −0.0370 | −0.0149 | ||

| (0.0920) | (0.0898) | (0.0904) | (0.1011) | (0.0913) | (0.0895) | (0.1522) | (0.1078) | (0.1066) | (0.1468) | (0.0998) | (0.0974) | |||||

| Growth of the labour force | Δln(lf) | c5 | 0.2155 ** | 0.2190 ** | 0.2139 ** | 0.2004 ** | 0.1995 ** | 0.2092 ** | 0.1854 * | 0.2402 ** | 0.0588 | 0.0320 | 0.3034 *** | 0.2264 ** | ||

| (0.0874) | (0.0887) | (0.0878) | (0.0851) | (0.0954) | (0.0952) | (0.1090) | (0.0953) | (0.0739) | (0.1041) | (0.1077) | (0.0923) | |||||

| Gross capital formation | gcf | c6 | 0.0074 ** | 0.0072 ** | 0.0066 ** | 0.0079 ** | 0.0075 ** | 0.0075 ** | 0.0090 ** | 0.0061 * | 0.0026 | −0.0004 | 0.0072 ** | 0.0080 ** | ||

| (0.0030) | (0.0030) | (0.0032) | (0.0031) | (0.0030) | (0.0031) | (0.0045) | (0.0031) | (0.0044) | (0.0039) | (0.0031) | (0.0035) | |||||

| Squared Gross capital formation | gcf2 | c7 | −0.0002 ** | −0.0001 ** | −0.0001 ** | −0.0002 *** | −0.0002 *** | −0.0002 ** | −0.0002 ** | −0.0001 ** | −0.0000 | 0.0000 | −0.0001 ** | −0.0002 ** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Openness to trade | ln(opn) | c8 | 0.1081 *** | 0.1081 *** | 0.1039 *** | 0.1088 *** | 0.1113 *** | 0.1103 *** | 0.1023 *** | 0.1073 *** | 0.1344 *** | 0.1279 *** | 0.1042 *** | 0.0744 *** | ||

| (0.0226) | (0.0224) | (0.0237) | (0.0216) | (0.0227) | (0.0247) | (0.0228) | (0.0261) | (0.0358) | (0.0322) | (0.0255) | (0.0239) | |||||

| Foreign direct investment | fdi | c9 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | 0.0000 | −0.0000 * | 0.0000 | −0.0000 | −0.0000 | −0.0000 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Government size | ln(gov) | c10 | −0.0712 ** | −0.0726 ** | −0.0738 *** | −0.0760 ** | −0.0664 ** | −0.0728 ** | −0.0861 ** | −0.0621 * | −0.0331 | −0.0143 | −0.0711 * | −0.0681 ** | ||

| (0.0290) | (0.0288) | (0.0282) | (0.0288) | (0.0330) | (0.0304) | (0.0359) | (0.0353) | (0.0243) | (0.0151) | (0.0348) | (0.0301) | |||||

| Research and development | ln(r&d) | c11 | 0.0036 | 0.0050 | 0.0018 | 0.0093 | 0.0065 | 0.0058 | −0.0166 | 0.0005 | −0.0155 | −0.0233 | 0.0093 | −0.0009 | ||

| (0.0141) | (0.0142) | (0.0139) | (0.0139) | (0.0143) | (0.0153) | (0.0104) | (0.0144) | (0.0160) | (0.0158) | (0.0154) | (0.0110) | |||||

| Inflation | Δln(cpi) | c12 | −0.1759 ** | −0.1857 *** | −0.1961 *** | −0.1541 ** | −0.2005 ** | −0.2049 *** | −0.1637 ** | −0.1970 *** | −0.2496 *** | −0.2057 * | −0.3107 *** | −0.1668 ** | ||

| (0.0659) | (0.0642) | (0.0700) | (0.0659) | (0.0785) | (0.0683) | (0.0789) | (0.0630) | (0.0769) | (0.0983) | (0.1095) | (0.0722) | |||||

| Human capital | ln(hc) | c13 | −0.0030 | −0.0020 | 0.0008 | −0.0025 | 0.0001 | −0.0072 | −0.0060 | −0.0054 | −0.0026 | 0.0014 | −0.0072 | 0.0017 | ||

| (0.0113) | (0.0118) | (0.0116) | (0.0108) | (0.0123) | (0.0096) | (0.0141) | (0.0138) | (0.0145) | (0.0127) | (0.0113) | (0.0110) | |||||

| GDP per capita | ln(Y) | β | −0.1666 *** | −0.1670 *** | −0.1573 *** | −0.1901 *** | −0.1621 *** | −0.1740 *** | −0.1600 *** | −0.1894 *** | −0.2479 *** | −0.2249 *** | −0.1810 *** | −0.1961 *** | ||

| (0.0366) | (0.0369) | (0.0408) | (0.0430) | (0.0364) | (0.040) | (0.0387) | (0.0306) | (0.0334) | (0.0362) | (0.0455) | (0.0463) | |||||

| Intercept | α | 1.0750 | 1.0750 | 1.0560 | 1.1070 | 0.9464 | 0.8922 | 0.6053 | 1.2400 | 1.5990 * | 3.9730 *** | 3.5350 *** | 1.2100 | |||

| (0.9767) | (0.9767) | (0.9741) | (0.9666) | (1.0520) | (0.9700) | (1.0760) | (1.2400) | (0.9108) | (0.9519) | (1.0690) | (1.0540) | |||||

| Number of observations | 342 | 342 | 339 | 342 | 342 | 332 | 237 | 294 | 201 | 166 | 320 | 312 | ||||

| Within R2 | 0.7538 | 0.7546 | 0.7537 | 0.7591 | 0.7560 | 0.7580 | 0.7797 | 0.7782 | 0.8343 | 0.8233 | 0.7504 | 0.7503 | ||||

| Pesaran CD test for cross-sectional dependence (1) [p-value] | [0.1979] | [0.2113] | [0.1999] | [0.2192] | [0.1919] | [0.2052] | [0.1864] | [0.2208] | [0.2142] | [0.2172] | [0.2207] | [0.1806] | ||||

| Test for differing group intercepts (2) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wald joint test on time dummies (3) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Hausman test (4) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wooldridge test (5) [p-value] | [0.1438] | [0.154] | [0.1731] | [0.196] | [0.1472] | [0.1761] | [0.1432] | [0.1631] | [0.1509] | [0.1766] | [0.1824] | [0.1447] | ||||

| Type of Infrastructure and Variable | Notation | Coefficient | (13) | (14) | (15) | (16) | (17) | (18) | (19) | (20) | (21) | (22) | (23) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Core Infrastructure (INFR) | ICT | Fixed telephone | ln(ict_ft) | γ | 0.0044 | ||||||||||

| (0.0219) | |||||||||||||||

| ln(ict_ft)× inst_cc | φ | 0.0024 | |||||||||||||

| (0.0010) | |||||||||||||||

| Fixed broadband | ln(ict_fb) | γ | 0.0033 | ||||||||||||

| (0.0033) | |||||||||||||||

| ln(ict_fb)× inst_cc | φ | 0.0024 | |||||||||||||

| (0.0020) | |||||||||||||||

| Mobile cellular | ln(ict_mc) | γ | 0.0239 * | ||||||||||||

| (0.0121) | |||||||||||||||

| ln(ict_mc)× inst_cc | φ | 0.0089 | |||||||||||||

| (0.0088) | |||||||||||||||

| Water and sanitation | Sanitation facilities | ln(ws_sf) | γ | 0.0520 | |||||||||||

| (0.0400) | |||||||||||||||

| ln(ws_sf)× inst_cc | φ | 0.1093 * | |||||||||||||

| (0.0584) | |||||||||||||||

| Drinking water facilities | ln(ws_dwf) | γ | 0.1052 | ||||||||||||

| (0.0821) | |||||||||||||||

| ln(ws_dwf)× inst_cc | φ | 0.0609 | |||||||||||||

| (0.1106) | |||||||||||||||

| Transport | Railways | ln(t_rw) | γ | 0.0146 | |||||||||||

| (0.0409) | |||||||||||||||

| ln(t_rw)× inst_cc | φ | 0.0042 | |||||||||||||

| (0.0245) | |||||||||||||||

| Roads | ln(t_r) | γ | 0.0016 | ||||||||||||

| (0.0131) | |||||||||||||||

| ln(t_r)× inst_cc | φ | 0.0202 | |||||||||||||

| (0.0133) | |||||||||||||||

| Inland waterways | ln(t_ww) | γ | 0.0186 | ||||||||||||

| (0.0323) | |||||||||||||||

| ln(t_ww)× inst_cc | φ | 0.0103 | |||||||||||||

| (0.0116) | |||||||||||||||

| Pipelines | ln(t_pl) | γ | 0.0423 *** | ||||||||||||

| (0.0100) | |||||||||||||||

| ln(t_pl)× inst_cc | φ | 0.0209 *** | |||||||||||||

| (0.0074) | |||||||||||||||

| Air transport | ln(t_ap) | γ | 0.0042 | ||||||||||||

| (0.0082) | |||||||||||||||

| ln(t_ap)× inst_cc | φ | 0.0119 | |||||||||||||

| (0.0109) | |||||||||||||||

| Energy | Electricity | ln(e_epc) | γ | 0.0727 *** | |||||||||||

| (0.0238) | |||||||||||||||

| ln(e_epc)× inst_cc | φ | 0.0512 *** | |||||||||||||

| (0.0154) | |||||||||||||||

| Institutions (Control of corruption) | inst_cc | c1 | 0.0296 | 0.0260 *** | −0.0193 | −0.4808 * | 0.2950 | 0.0319 | −0.1203 | 0.0399 | 0.0760 *** | 0.1167 | 0.1587 *** | ||

| (0.0383) | (0.0090) | (0.0383) | (0.2647) | (0.5051) | (0.1088) | (0.0909) | (0.0262) | (0.0205) | (0.0813) | (0.0449) | |||||

| Population growth | Δln(pop) | c2 | −1.448 ** | −1.507 ** | −1.428 ** | −1.349 * | −1.286 * | −1.769 ** | −1.611 * | −1.127 ** | −0.6057 | −1.134 * | −1.249 * | ||

| (0.6570) | (0.6981) | (0.6856) | (0.7045) | (0.7061) | (0.7017) | (0.8437) | (0.4959) | (0.3821) | (0.6227) | (0.6235) | |||||

| Population density | ln(dens) | c3 | 0.09164 | 0.1106 | 0.1097 | 0.0871 | 0.1131 | 0.0945 | 0.0520 | −0.1095 | −0.0824 | 0.0927 | 0.0731 | ||

| (0.0836) | (0.0888) | (0.0921) | (0.0882) | (0.0783) | (0.0934) | (0.0799) | (0.0945) | (0.0804) | (0.0876) | (0.0802) | |||||

| Urbanisation level | ln(urb) | c4 | −0.0262 | −0.0462 | 0.0026 | 0.0704 | 0.0025 | −0.0256 | −0.0946 | −0.3369*** | −0.3984*** | −0.0139 | 0.0160 | ||

| (0.0875) | (0.0934) | (0.0984) | (0.0958) | (0.0831) | (0.1696) | (0.1096) | (0.1270) | (0.1439) | (0.1079) | (0.0894) | |||||

| Growth of the labour force | Δln(lf) | c5 | 0.2172 ** | 0.2070 ** | 0.2027 ** | 0.1910 * | 0.2063 ** | 0.1862 | 0.2583 *** | 0.0651 | 0.0367 | 0.3054 *** | 0.2306 ** | ||

| (0.0863) | (0.0877) | (0.0835) | (0.0999) | (0.0979) | (0.1091) | (0.0939) | (0.0750) | (0.1070) | (0.1054) | (0.0891) | |||||

| Gross capital formation | gcf | c6 | 0.0072 ** | 0.0068 ** | 0.0075 ** | 0.0070 ** | 0.0077 ** | 0.0089 * | 0.0061 * | 0.0025 | −0.0017 | 0.0079 ** | 0.0069 ** | ||

| (0.0030) | (0.0032) | (0.0033) | (0.0031) | (0.0029) | (0.0045) | (0.0031) | (0.0043) | (0.0038) | (0.0033) | (0.0029) | |||||

| Squared Gross capital formation | gcf2 | c7 | −0.0001 *** | −0.0001 ** | −0.0002 ** | −0.0001 ** | −0.0002 *** | −0.0002 ** | −0.0001 ** | −0.0000 | 0.0000 | −0.0002 ** | −0.0002 ** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |||||

| Openness to trade | ln(opn) | c8 | 0.1089 *** | 0.1050 *** | 0.1108 *** | 0.1148 *** | 0.1095 *** | 0.1039 *** | 0.1109 *** | 0.1363 *** | 0.1343 *** | 0.1022 *** | 0.0653 *** | ||

| (0.0218) | (0.0242) | (0.0213) | (0.0248) | (0.0246) | (0.0233) | (0.0235) | (0.0353) | (0.0339) | (0.0259) | (0.0225) | |||||

| Foreign direct investment | fdi | c9 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | −0.0000 | 0.0002 | −0.0000 ** | 0.0000 | −0.0000 * | −0.0000 | −0.0000 *** | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0001) | (0.0000) | (0.0000) | (0.0001) | (0.0000) | (0.0000) | |||||

| Government size | ln(gov) | c10 | −0.0730 ** | −0.0748 *** | −0.0735 ** | −0.0683 ** | −0.0711 ** | −0.0857 ** | −0.0601 | −0.0325 | −0.0155 | −0.0663 ** | −0.0795 ** | ||

| (0.0292) | (0.0267) | (0.0307) | (0.0336) | (0.0320) | (0.0379) | (0.0369) | (0.0238) | (0.0140) | (0.0315) | (0.0294) | |||||

| Research and development | ln(r&d) | c11 | 0.0055 | 0.0020 | 0.0093 | 0.0100 | 0.0059 | −0.0175 | 0.0056 | −0.0157 | −0.0260 * | 0.0097 | −0.0136 | ||

| (0.0149) | (0.0138) | (0.0136) | (0.0141) | (0.0154) | (0.0120) | (0.0151) | (0.0157 | (0.0157) | (0.0156) | (0.0111) | |||||

| Inflation | Δln(cpi) | c12 | −0.1838 *** | −0.1806 ** | −0.1791 ** | −0.2560 *** | −0.1962 *** | −0.1656 ** | −0.2159 *** | −0.2511 *** | −0.2439 ** | −0.2916 ** | −0.1491 ** | ||

| (0.0657) | (0.0690) | (0.0678) | (0.0835) | (0.0689) | (0.0750) | (0.0688) | (0.0771) | (0.0970) | (0.1149) | (0.0700) | |||||

| Human capital | ln(hc) | c13 | −0.0011 | −0.0004 | 0.0003 | −0.0013 | −0.0079 | −0.0062 | −0.0017 | −0.0025 | −0.0054 | −0.0100 | 0.0115 | ||

| (0.0111) | (0.0115) | (0.0117) | (0.0112) | (0.0095) | (0.0142) | (0.0145) | (0.0147) | (0.0121) | (0.0125) | (0.0117) | |||||

| GDP per capita | ln(Y) | β | −0.1662 *** | −0.1615 *** | −0.1841 *** | −0.1617 *** | −0.1767 *** | −0.1588 *** | −0.1894 *** | −0.2478 *** | −0.2255 *** | −0.1816 *** | −0.2351 *** | ||

| (0.0382) | (0.0418) | (0.0423) | (0.0380) | (0.0439) | (0.0409) | (0.0306) | (0.0321) | (0.0378) | (0.0479) | (0.0493) | |||||

| Intercept | α | 1.038 | 1.0380 | 1.0440 | 0.8350 | 0.7365 | 0.4353 | 1.1350 | 1.6750 * | 4.0730 *** | 3.9180 *** | 1.1540 | |||

| (0.9949) | (0.9949) | (1.0080) | (1.0250) | (1.0210) | (0.8675) | (1.4500) | (0.9121) | (0.9921) | (1.0560) | (1.0690) | |||||

| Number of observations | 342 | 339 | 342 | 332 | 332 | 237 | 294 | 201 | 166 | 320 | 312 | ||||

| Within R2 | 0.7547 | 0.7547 | 0.7605 | 0.7606 | 0.7585 | 0.7799 | 0.7824 | 0.8352 | 0.8302 | 0.7533 | 0.7694 | ||||

| Pesaran CD test for cross-sectional Dependence (1) [p-value] | [0.1902] | [0.1979] | [0.2159] | [0.1881] | [0.2129] | [0.18] | [0.1939] | [0.2375] | [0.1863] | [0.2105] | [0.2169] | ||||

| Test for differing group intercepts (2) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wald joint test on time dummies (3) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Hausman test (4) [p-value] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | [<0.001] | ||||

| Wooldridge test (5) [p-value] | [0.1662] | [0.1635] | [0.1824] | [0.1685] | [0.1738] | [0.1275] | [0.1436] | [0.1937] | [0.1371] | [0.1618] | [0.193] | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Maciulyte-Sniukiene, A.; Butkus, M. Does Infrastructure Development Contribute to EU Countries’ Economic Growth? Sustainability 2022, 14, 5610. https://doi.org/10.3390/su14095610

Maciulyte-Sniukiene A, Butkus M. Does Infrastructure Development Contribute to EU Countries’ Economic Growth? Sustainability. 2022; 14(9):5610. https://doi.org/10.3390/su14095610

Chicago/Turabian StyleMaciulyte-Sniukiene, Alma, and Mindaugas Butkus. 2022. "Does Infrastructure Development Contribute to EU Countries’ Economic Growth?" Sustainability 14, no. 9: 5610. https://doi.org/10.3390/su14095610

APA StyleMaciulyte-Sniukiene, A., & Butkus, M. (2022). Does Infrastructure Development Contribute to EU Countries’ Economic Growth? Sustainability, 14(9), 5610. https://doi.org/10.3390/su14095610