Does Business Group’s Conscious of Social Responsibility Enhance its Investment Efficiency? Evidence from ESG Disclosure of China’s Listed Companies

Abstract

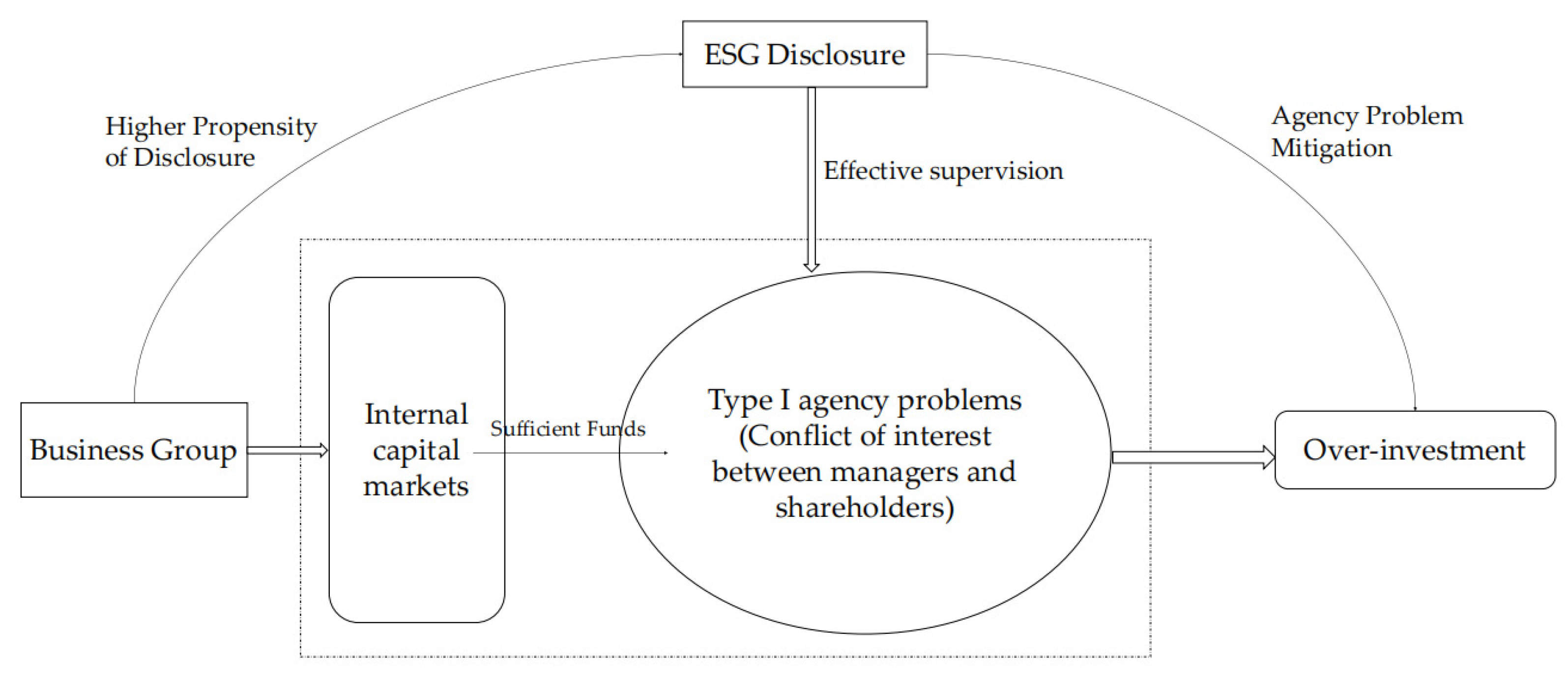

:1. Introduction

2. Hypothesis Developments

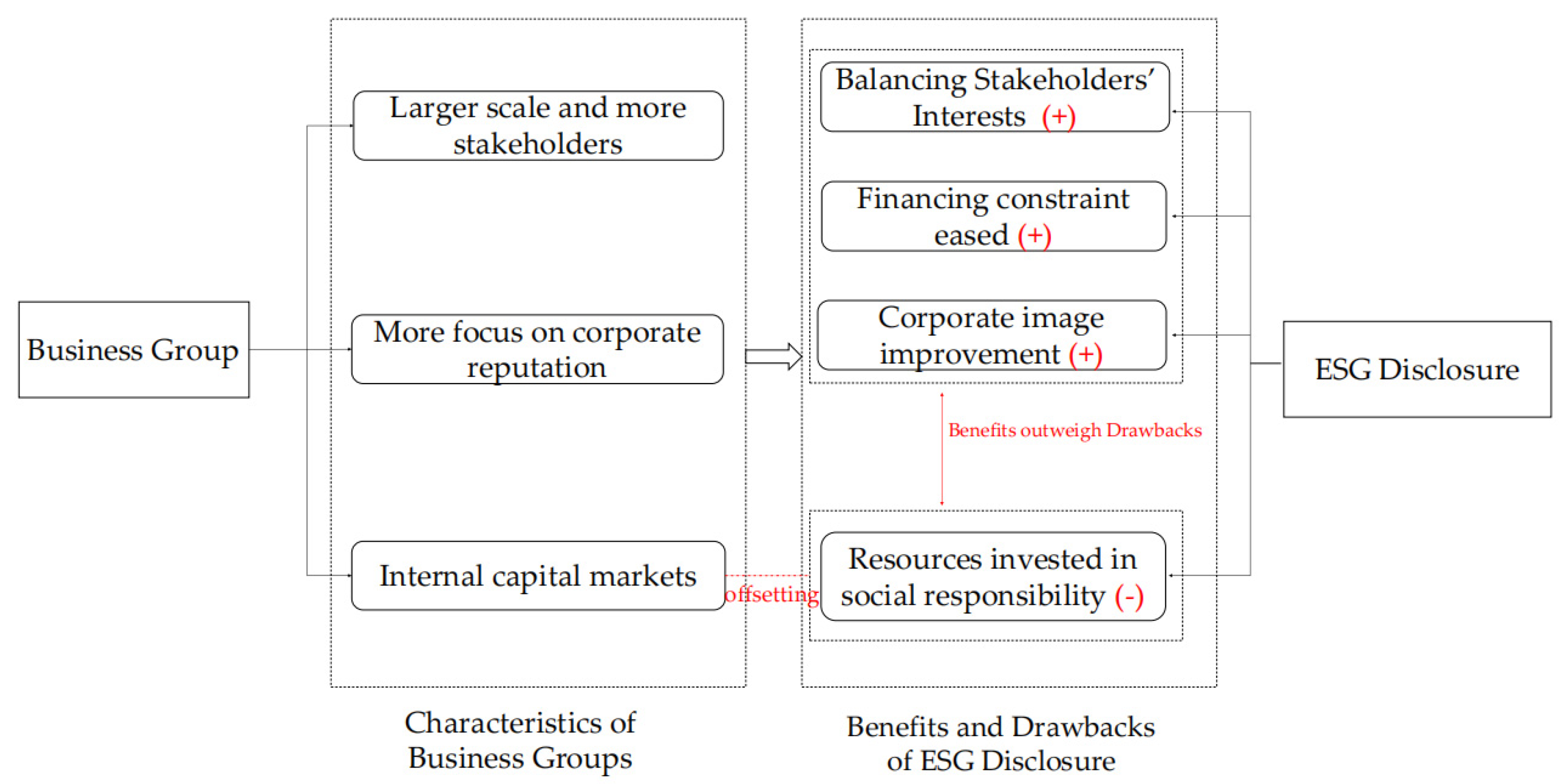

2.1. Business Group and ESG Disclosure

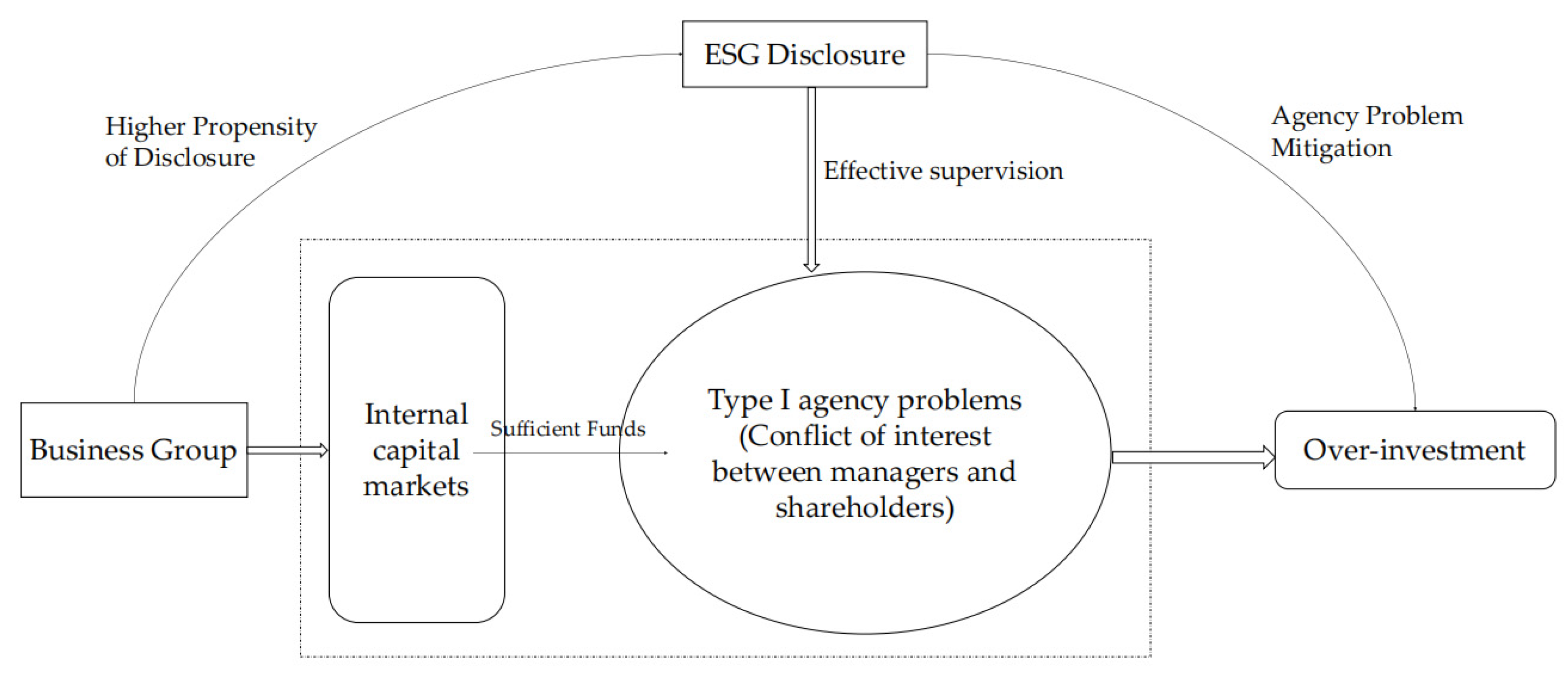

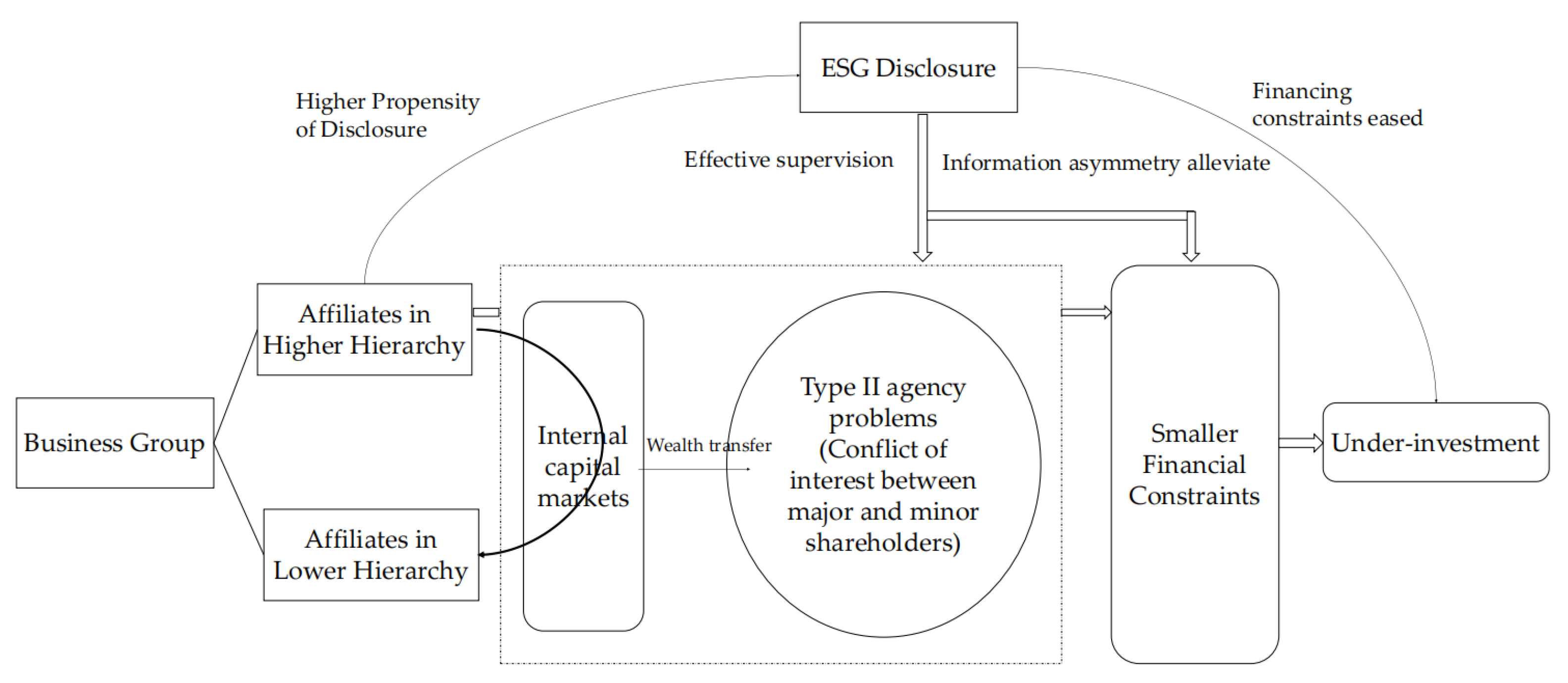

2.2. Business Group, ESG Disclosure and Investment Efficiency

3. Data and Method

3.1. Sample Selection and Data Source

3.2. Variable Definitions

3.2.1. Investment Efficiency

3.2.2. ESG Disclosure

3.2.3. Business Group

3.2.4. Pyramid Hierarchy

3.2.5. Control Variables

3.3. Method

4. Results

4.1. Descriptive Statistics

4.2. Propensity of Business Groups on ESG Disclosure

4.3. Different Propensity of Pyramid Member Firms on ESG Disclosure

4.4. The Moderating Effect of ESG Disclosure on the Investment Efficiency

4.4.1. Business Group and Investment Efficiency

4.4.2. Pyramid Levels and Investment Efficiency

4.4.3. The Effect of ESG Disclosure on Group-Affiliated Firm’s Investment Efficiency

4.4.4. Pyramid Levels, ESG Disclosure and Investment Efficiency

4.5. Mechanism Testing

4.5.1. Mitigating Effects of ESG Disclosures on Agency Problems

4.5.2. Mitigating Effects of ESG Disclosures on Financial Constrains

5. Conclusions and Policy Implications

5.1. Conclusions

5.2. Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Shakil, M.H. Environmental, social and governance performance and financial risk: Moderating role of ESG controversies and board gender diversity. Resour. Policy 2021, 72, 102144. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Zhang, F.; Qin, X.; Liu, L. The interaction effect between ESG and green innovation and its impact on firm value from the perspective of information disclosure. Sustainability 2020, 12, 1866. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, P.; Nguyen, A. The effect of corporate social responsibility on firm risk. Soc. Responsib. J. 2015, 11, 324–339. [Google Scholar] [CrossRef]

- Zhao, C.; Guo, Y.; Yuan, J.; Wu, D.; Zhou, Y.; Kang, J. ESG and corporate financial performance: Empirical evidence from China’s listed power generation companies. Sustainability 2018, 10, 2607. [Google Scholar] [CrossRef] [Green Version]

- Dimson, E.; Karakas, O.; Li, X. Active ownership. Rev. Financ. Stud. 2015, 28, 3225–3268. [Google Scholar] [CrossRef] [Green Version]

- Fatemi, A.; Glaum, M.; Kaiser, S. ESG performance and firm value: The moderating role of disclosure. Glob. Financ. J. 2018, 38, 45–64. [Google Scholar] [CrossRef]

- Fatemi, A.M.; Fooladi, I.J.; Tehranian, H. Valuation effects of corporate social responsibility. J. Bank. Financ. 2015, 59, 182–192. [Google Scholar] [CrossRef]

- Malik, M. Value-enhancing capabilities of CSR: A brief review of contemporary literature. J. Bus. Ethics 2015, 127, 419–438. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating shared value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef] [Green Version]

- Chen, S.; Zheng, S.; Song, T.; Wu, D. Government intervention and investment efficiency: Evidence from China. J. Corp. Financ. 2011, 17, 259–271. [Google Scholar] [CrossRef]

- Stein, J.C. Agency, information and corporate investment. Handb. Econ. Financ. 2003, 1, 111–165. [Google Scholar]

- Lueg, K.; Krastev, B.; Lueg, R. Bidirectional effects between organizational sustainability disclosure and risk. J. Clean. Prod. 2019, 229, 268–277. [Google Scholar] [CrossRef]

- Jia, Y.; Gao, X.; Julian, S. Do firms use corporate social responsibility to insure against stock price risk? Evidence from a natural experiment. Strat. Manag. J. 2020, 41, 290–307. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Zhong, M.; Gao, L. Does corporate social responsibility disclosure improve firm investment efficiency? Evidence from China. Rev. Financ. Stud. 2017, 16, 348–365. [Google Scholar]

- Lin, Y.E.; Li, Y.W.; Cheng, T.Y.; Lam, K. Corporate social responsibility and investment efficiency: Does business strategy matter? Int. Rev. Econ. Financ. 2021, 73, 101585. [Google Scholar] [CrossRef]

- Anwar, R.; Malik, J.A. When does corporate social responsibility disclosure affect investment efficiency? A new answer to an old question. SAGE Open 2020, 10, 21582440209. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. New York Times Magazine, 13 September 1970; 32–33. [Google Scholar]

- Sen, S.; Bhattacharya, C.B.; Korschun, D. The role of corporate social responsibility in strengthening multiple stakeholder relationships: A field experiment. J. Acad. Mark. Sci. 2006, 34, 158–166. [Google Scholar] [CrossRef]

- Huang, X.; Jiang, X.; Liu, W.; Chen, Q. Business group-affiliation and corporate social responsibility: Evidence from listed companies in China. Sustainability 2021, 13, 2110. [Google Scholar] [CrossRef]

- Choi, Y.K.; Han, S.H.; Kwon, Y. CSR activities and internal capital markets: Evidence from Korean business groups. Pac. Basin Financ. J. 2019, 55, 283–298. [Google Scholar] [CrossRef]

- Zeng, T. Corporate social responsibility (CSR) in Canadian family firms. Soc. Resp. J. 2021, 17, 703–718. [Google Scholar] [CrossRef]

- He, J.; Mao, X.; Rui, O.M.; Zha, X. Business groups in China. J. Corp. Financ. 2013, 22, 166–192. [Google Scholar] [CrossRef] [Green Version]

- Yiu, D.; Bruton, G.D.; Lu, Y. Understanding business group performance in an emerging economy: Acquiring resources and capabilities in order to prosper. J. Manag. Stud. 2005, 42, 183–206. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. The emergence of corporate pyramids in China. 2005. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=686582 (accessed on 14 April 2022).

- Johnson, S.; La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A. Tunneling. Am. Econ. Rev. 2000, 90, 22–27. [Google Scholar] [CrossRef]

- Kim, E.H.; Lyon, T.P. Greenwash vs. brownwash: Exaggeration and undue modesty in corporate sustainability disclosure. Organ. Sci. 2015, 26, 705–723. [Google Scholar] [CrossRef]

- Khanna, T.; Palepu, K. Is group affiliation profitable in emerging markets? An analysis of diversified Indian business groups. J. Financ. 2000, 55, 867–891. [Google Scholar] [CrossRef]

- Aguilera-Caracuel, J.; Guerrero-Villegas, J.; García-Sánchez, E. Reputation of multinational companies: Corporate social responsibility and internationalization. Eur. J. Manag. Bus. Econ. 2017, 26, 329–346. [Google Scholar] [CrossRef]

- Fatemi, A.M.; Fooladi, I.J. Sustainable finance: A new paradigm. Glob. Financ. J. 2013, 24, 101–113. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Almeida, H.V.; Wolfenzon, D. A theory of pyramidal ownership and family business groups. J. Financ. 2006, 61, 2637–2680. [Google Scholar] [CrossRef] [Green Version]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef] [Green Version]

- Sroufe, R.; Gopalakrishna-Remani, V. Management, social sustainability, reputation, and financial performance relationships: An empirical examination of US firms. Organ. Environ. 2019, 32, 331–362. [Google Scholar] [CrossRef] [Green Version]

- Eng, L.L.; Mak, Y.T. Corporate governance and voluntary disclosure. J. Account. Public Policy 2003, 22, 325–345. [Google Scholar] [CrossRef]

- Khan, A.; Muttakin, M.B.; Siddiqui, J. Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. J. Bus. Ethics 2013, 114, 207–223. [Google Scholar] [CrossRef]

- Ullmann, A.A. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance of US firms. Acad. Manag. Rev. 1985, 10, 540–557. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 1995, 20, 404–437. [Google Scholar] [CrossRef]

- Baek, J.S.; Kang, J.K.; Lee, I. Business groups and tunneling: Evidence from private securities offerings by Korean chaebols. J. Financ. 2006, 61, 2415–2449. [Google Scholar] [CrossRef] [Green Version]

- Bertrand, M.; Mehta, P.; Mullainathan, S. Ferreting out tunneling: An application to Indian business groups. Q. J. Econ. 2002, 117, 121–148. [Google Scholar] [CrossRef]

- Gonenc, H.; Hermes, N. Propping: Evidence from new share issues of Turkish business group firms. J. Multinatl. Financ. Manag. 2008, 18, 261–275. [Google Scholar] [CrossRef]

- Ying, Q.; Wang, L. Propping by controlling shareholders, wealth transfer and firm performance: Evidence from Chinese listed companies. China J. Account. Res. 2013, 6, 133–147. [Google Scholar] [CrossRef] [Green Version]

- Morck, R.; Yeung, B. Agency problems in large family business groups. Entrep. Theory Pract. 2003, 27, 367–382. [Google Scholar] [CrossRef]

- Claessens, S.; Djankov, S.; Lang, L.H. The separation of ownership and control in East Asian corporations. J. Financ. Econ. 2000, 58, 81–112. [Google Scholar] [CrossRef]

- Zhong, H. Government intervention, insider control and corporate investment. Manag. World 2010, 7, 98–108. [Google Scholar]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A. Corporate ownership around the world. J. Financ. 1999, 54, 471–517. [Google Scholar] [CrossRef]

- Cheung, Y.; Rau, P.R.; Stouraitis, A. Tunneling, propping, and expropriation: Evidence from connected party transactions in Honk Kong. J. Financ. Econ. 2006, 82, 343–386. [Google Scholar] [CrossRef] [Green Version]

- Allman, E.; Won, J. The Effect of ESG Disclosure on Corporate Investment Efficiency. Available online: https://ssrn.com/abstract=3816592 (accessed on 28 November 2021).

- Roychowdhury, S.; Shroff, N.; Verdi, R.S. The effects of financial reporting and disclosure on corporate investment: A review. J. Account. Econ. 2019, 68, 101246. [Google Scholar] [CrossRef]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Matsusaka, J.G.; Nanda, V. Internal capital markets and corporate refocusing. J. Financ. Intermed. 2002, 11, 176–211. [Google Scholar] [CrossRef]

- Biddle, G.C.; Hilary, G.; Verdi, R.S. How does financial reporting quality relate to investment efficiency? J. Account. Econ. 2009, 48, 112–131. [Google Scholar] [CrossRef]

- Branco, M.; Rodrigues, L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. Organizational Structure as a Decentralization Device: Evidence from Corporate Pyramids. 2007. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=963430. (accessed on 14 April 2022).

- Cuadrado-Ballesteros, B.; Garcia-Sanchez, I.M.; Martinez Ferrero, J. How are corporate disclosures related to the cost of capital? The fundamental role of information asymmetry. Manag. Decis. 2016, 54, 1669–1701. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, social and governance performance and stock price volatility: A moderating role of firm size. J. Public. Aff. 2020, e2574. [Google Scholar] [CrossRef]

- Richardson, S. Over-investment of free cash flow. Rev. Acc. Stud. 2006, 11, 159–189. [Google Scholar] [CrossRef]

- Khanna, T.; Yafeh, Y. Business groups in emerging markets: Paragons or parasites? J. Econ. Lit. 2007, 45, 331–372. [Google Scholar] [CrossRef] [Green Version]

- Leff, N.H. Industrial organization and entrepreneurship in the developing countries: The economic groups. Econ. Dev. Cult. Change 1978, 26, 661–675. [Google Scholar] [CrossRef]

- Kim, J.B.; Li, Y.; Zhang, L. CFOs versus CEOs: Equity incentives and crashes. J. Finan. Econ. 2011, 101, 713–730. [Google Scholar] [CrossRef]

- Rajan, R.G.; Zingales, L. Financial dependence and growth. Am. Econ. Rev. 1998, 88, 559–586. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | N | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Absinv | 4774 | 0.0353 | 0.0479 | 0.0004 | 0.3127 |

| Underinv | 2755 | 0.0245 | 0.0239 | 0.0004 | 0.2271 |

| Overinv | 2019 | 0.0500 | 0.0654 | 0.0004 | 0.3127 |

| ESG | 5540 | 20.6766 | 6.0986 | 7.4400 | 61.7200 |

| E_dis | 4552 | 10.4477 | 6..8351 | 0.7800 | 60.4200 |

| S_dis | 5521 | 23.3889 | 8.8968 | 3.5100 | 73.6842 |

| G_dis | 5540 | 45.6670 | 5.5252 | 14.2900 | 81.2621 |

| Group | 5540 | 0.3991 | 0.4898 | 0 | 1 |

| Layer | 5540 | 2.8287 | 0.3778 | 1 | 11 |

| ROA | 5540 | 0.4827 | 0.5370 | −0.1240 | 0.2192 |

| Size | 5540 | 10.0318 | 0.5193 | 8.9223 | 11.4777 |

| Tang | 5540 | 0.2272 | 0.1790 | 0.0019 | 0.7396 |

| OCF | 5540 | 0.0583 | 0.0693 | −0.1288 | 0.2555 |

| Lev | 5540 | 0.4823 | 0.1989 | 0.0750 | 0.8783 |

| Top1 | 5540 | 0.3823 | 0.1620 | 0.0848 | 0.7802 |

| Indep | 5540 | 0.3743 | 0.0537 | 0.3333 | 0.5714 |

| TobinQ | 5540 | 1.9712 | 1.2475 | 0.8546 | 7.6868 |

| Age | 5540 | 12.7246 | 6.3256 | 0 | 25 |

| Soe | 5540 | 0.6119 | 0.4874 | 0 | 1 |

| Variables | ESG (1) | E_dis (2) | S_dis (3) | G_dis (4) |

|---|---|---|---|---|

| Group | 0.6321 *** (3.77) | 0.4339 ** (2.06) | 0.9005 *** (3.52) | −0.3088 * (−1.94) |

| Constant | −23.9501 *** (−11.45) | −33.6442 *** (−12.64) | −27.0331 *** (−8.46) | 20.9494 *** (10.57) |

| Controls | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes |

| N | 5540 | 4552 | 5521 | 5540 |

| R2 | 0.2436 | 0.1933 | 0.1730 | 0.1715 |

| Variables | ESG (1) | E_dis (2) | S_dis (3) | G_dis (4) |

|---|---|---|---|---|

| Group | 0.3469 * (1.75) | 0.5206 ** (2.12) | 0.5837 * (1.93) | −0.5351 *** (−2.85) |

| Layer | 0.1634 (0.83) | 1.6534 *** (6.18) | 0.0387 (0.13) | 0.3421 * (1.83) |

| Group*Layer | 0.8275 *** (2.64) | −0.4775 (−1.19) | 0.9245 * (1.93) | 0.6483 ** (2.18) |

| Constant | −23.6442 *** (−11.28) | −33.6671 *** (−12.70) | −26.6488 *** (−8.32) | 21.1247 *** (10.64) |

| Controls | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes |

| N | 5540 | 4552 | 5521 | 5540 |

| R2 | 0.2460 | 0.2029 | 0.1741 | 0.1748 |

| Variables | Absinv (1) | Underinv (2) | Overinv (3) |

|---|---|---|---|

| Group | 0.0111 *** (7.03) | 0.0014 (1.26) | 0.0060 * (1.79) |

| Constant | 0.0057 (0.29) | −0.0085 (−0.66) | 0.1101 ** (2.54) |

| Controls | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| N | 4774 | 2755 | 2019 |

| R2 | 0.0839 | 0.0946 | 0.1502 |

| Variables | Absinv (1) | Underinv (2) | Overinv (3) |

|---|---|---|---|

| Group | 0.0086 *** (4.71) | −0.0004 (−0.34) | 0.0058 (1.32) |

| Layer | 0.0006 (0.29) | −0.0041 *** (−2.91) | −0.0013 (−0.30) |

| Group*Layer | 0.0071 ** (2.41) | 0.0105 *** (4.24) | 0.0005 (0.08) |

| Constant | 0.0097 (0.49) | −0.0047 (−0.37) | 0.1101** (2.53) |

| Controls | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| N | 4774 | 2755 | 2019 |

| R2 | 0.0864 | 0.1008 | 0.1502 |

| Variables | Absinv (1) | Underinv (2) | Overinv (3) |

|---|---|---|---|

| ESG | 0.0327 *** (1.02) | −0.0001 (−0.59) | 0.0001 (0.39) |

| Group | 0.0327 *** (6.30) | 0.0072 * (1.90) | 0.0251 ** (2.42) |

| Group*ESG | −0.0010 *** (−4.35) | −0.0003 (−1.55) | −0.0009 * (−1.93) |

| Constant | −0.0158 (−0.78) | −0.0150 (−1.14) | 0.0828 * (1.84) |

| Controls | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| N | 4774 | 2755 | 2019 |

| R2 | 0.0885 | 0.0964 | 0.1526 |

| Variables | Absinv (1) | Underinv (2) | Overinv (3) |

|---|---|---|---|

| ESG | −0.0001 (−0.35) | −0.0003 *** (−2.69) | 0.0005 (1.02) |

| Group | 0.0251 *** (3.92) | −0.0001 (−0.03) | 0.0283 * (1.89) |

| Layer | −0.0119 * (−1.82) | −0.0221 *** (−5.03) | 0.0132 (0.90) |

| ESG*Group | −0.0008 *** (−2.64) | 0.0000 (0.04) | −0.0011 (−1.58) |

| ESG*Layer | 0.0006 ** (2.02) | 0.0009 *** (4.34) | −0.0007 (−1.03) |

| Group*Layer | 0.0239 ** (2.30) | 0.0350 *** (3.79) | −0.0059 (−0.29) |

| ESG*Group*Layer | −0.0008 * (−1.69) | −0.0012 *** (−2.98) | 0.0004 (0.41) |

| Constant | −0.0090 (−0.44) | −0.0092 (−0.71) | 0.0769 * (1.69) |

| Year | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes |

| N | 4774 | 2755 | 2019 |

| R2 | 0.0923 | 0.1095 | 0.1532 |

| Variables | Absinv | Underinv | Overinv | |||

|---|---|---|---|---|---|---|

| Analyst = 0 | Analyst = 1 | Analyst = 0 | Analyst = 1 | Analyst = 0 | Analyst = 1 | |

| ESG | 0.0002 (0.56) | 0.0000 (0.25) | −0.0003 ** (−2.00) | 0.0001 (0.86) | 0.0006 (0.91) | −0.0003 (−0.70) |

| Group | 0.0434 *** (5.82) | 0.0012 (0.15) | 0.0037 (0.67) | 0.0082 (1.50) | 0.0405 *** (2.72) | −0.0168 (−0.86) |

| ESG*Group | −0.0013 *** (−3.85) | −0.0000 (−0.14) | −0.0001 (−0.41) | −0.0003 (−1.40) | −0.0016 ** (−2.34) | 0.0009 (1.10) |

| Constant | −0.0340 (−1.07) | 0.0105 (0.39) | 0.0006 (0.03) | −0.0106 (−0.59) | 0.0581 (0.99) | 0.1020 (1.29) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 2683 | 2091 | 1332 | 1423 | 1351 | 668 |

| R2 | 0.1210 | 0.0855 | 0.1434 | 0.1201 | 0.1664 | 0.2002 |

| Variables | Absinv | Underinv | Overinv | |||

|---|---|---|---|---|---|---|

| EFD = 0 | EFD = 1 | EFD = 0 | EFD = 1 | EFD = 0 | EFD = 1 | |

| ESG | −0.0002 (−0.52) | 0.0000 (0.02) | −0.0002 (−1.20) | −0.0004 ** (−2.24) | 0.0002 (0.32) | 0.0008 (1.04) |

| Group | 0.0365 *** (3.71) | 0.0150 * (1.79) | 0.0083 (1.39) | −0.0058 (−0.98) | 0.0333 (1.63) | 0.0259 (1.15) |

| Layer | −0.0123 (−1.26) | −0.0131 (−1.51) | −0.0153 *** (−2.62) | −0.0308 *** (−4.44) | 0.0041 (0.19) | 0.0183 (0.85) |

| ESG*Group | −0.0011 ** (−2.48) | −0.0005 (−1.29) | −0.0004 (−1.34) | 0.0002 (0.93) | −0.0012 (−1.23) | −0.0011 (−1.08) |

| ESG*Layer | 0.0006 (1.27) | 0.0007 * (1.70) | 0.0006* (1.94) | 0.0014 *** (4.23) | −0.0003 (−0.33) | −0.0009 (−0.89) |

| Group*Layer | 0.0147 (0.96) | 0.0342 ** (2.45) | 0.0230 (1.45) | 0.0462 *** (3.70) | −0.0079 (−0.28) | 0.0032 (0.10) |

| ESG*Group*Layer | −0.0004 (−0.62) | −0.0012 * (−1.91) | −0.0006 (−0.89) | −0.0018 *** (−3.29) | 0.0004 (0.30) | 0.0000 (0.01) |

| Constant | −0.0314 (−0.96) | 0.0138 (0.53) | −0.0334* (−1.67) | 0.0090 (0.50) | 0.0928 (1.45) | 0.0982 (1.41) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 2488 | 2286 | 1294 | 1461 | 1194 | 825 |

| R2 | 0.1186 | 0.0932 | 0.1369 | 0.1263 | 0.1781 | 0.1781 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hai, M.; Fang, Z.; Li, Z. Does Business Group’s Conscious of Social Responsibility Enhance its Investment Efficiency? Evidence from ESG Disclosure of China’s Listed Companies. Sustainability 2022, 14, 4817. https://doi.org/10.3390/su14084817

Hai M, Fang Z, Li Z. Does Business Group’s Conscious of Social Responsibility Enhance its Investment Efficiency? Evidence from ESG Disclosure of China’s Listed Companies. Sustainability. 2022; 14(8):4817. https://doi.org/10.3390/su14084817

Chicago/Turabian StyleHai, Mengdie, Ziwei Fang, and Zhaohua Li. 2022. "Does Business Group’s Conscious of Social Responsibility Enhance its Investment Efficiency? Evidence from ESG Disclosure of China’s Listed Companies" Sustainability 14, no. 8: 4817. https://doi.org/10.3390/su14084817

APA StyleHai, M., Fang, Z., & Li, Z. (2022). Does Business Group’s Conscious of Social Responsibility Enhance its Investment Efficiency? Evidence from ESG Disclosure of China’s Listed Companies. Sustainability, 14(8), 4817. https://doi.org/10.3390/su14084817