1. Introduction

Creative and cultural activities, more recently encompassed in the Orange economy, have been the subject of great interest in recent decades. They have been attributed great potential as engines of economic growth and sustainable development, a role that has been encouraged by various international organizations. There has been much commentary on the important capacity of the creative and cultural sector to generate sustainable growth from the triple economic, social, and environmental perspective. Accepting this premise, there is a commitment to the creative and the cultural economy that is manifested in the proposal and the implementation of various economic policy measures. However, despite the wide acceptance of the growth capacity of creative and cultural activities, there is a lack of empirical evidence to support this claim. The objective of this paper is to contribute to alleviating the lack of empirical results/evidence. The widespread acceptance of the capacity of creative and cultural activities to generate growth and employment has driven the design and the implementation of economic policies to stimulate and to support these activities in several economies. This study provides empirical evidence not only for the sector as a whole but also for the different activities that compose it, information that can be very useful for policy design. Thus, the questions we propose to answer are the following: Is the Orange sector capable of generating sustained growth over time at a higher rate than other economic sectors? Furthermore, does it make sense to speak of the Orange economy as a sector or, on the contrary, is it a grouping of activities with little relation?

The paper begins with a literature review on sector delimitation and its contribution to growth and to sustainability and then gives way to the empirical study carried out. It considers Orange economy companies in two Spanish regions: the Valencian Community and the Galician Community—both coastal regions, one on the Mediterranean and the other on the Atlantic. For information selection, the SABI® database, “Sistema Anual de Balances Ibéricos” (Annual System of Iberian Balance Sheets) has been used; and, the companies that, according to the National Classification of Economic Activities (CNAE-2009), belong to the sectors included in the creative and cultural sector have been considered. The data collected are part of the information related to the annual accounts that companies must submit to the Mercantile Registry. The sample consists of 8191 companies, for the analytical period from 2000 to 2019. The activities included in the Orange sector are diverse, so it seems appropriate, in addition to the overall sector analysis to delve into the characteristics and companies’ results according to the different types of included activity branches. The study shows a picture of the Orange sector structure based on the classification of activities. The companies are grouped according to their CNAE in three large subgroups: creative manufacturing, cultural industries, and creative sectors. The various subgroups are, in turn, made up of groups of activities called branches, which are grouped according to their affinity.

The analyses carried out show that revenues, the number of companies, and the results of the Orange sector have grown proportionally more than the economy as a whole, so our results support the claim that the Orange economy is the driving force behind growth. Furthermore, if we consider the types of activities that comprise the sector and its dynamism, they have been greater than the economy as a whole, except in some cases. In terms of profitability, the results obtained from the data analysis allow us to affirm that the Orange sector as a whole presents good sustained profitability over time, as well as showing greater resilience than other sectors in the face of the crisis unleashed in 2008. Finally, it is necessary to point out that a complete assessment of the sustainability of the Orange sector requires addressing the social and the environmental pillars.

The remainder of the paper is structured as follows: first, a theoretical framework is presented; second, the employed methods are presented; third, the qualitative study is presented; and finally, some discussions and future works are provided.

4. Results

To answer Hypothesis 1, the variables operating income, total assets, shareholders’ equity, income before taxes, economic profitability, and financial profitability were analyzed for each year (2000–2019). In order to reduce the variables, a factor analysis was performed. The result of the correlation matrix yielded a value of 0.508 for the Kaiser Mayer Olkin test with a significance of (

p < 0.001). The variance explained by the three factors is 75.865% (see

Table A2).

The first factor of the factorial analysis, which can be identified as company size, includes the variables of shareholders’ equity, assets, and operating income. These three variables explain 39.12% of the variance. The second factor is formed by the result variables, which shows that it has no clear relationship with the previous variables, and it represents 18.975%. The third factor is composed of profitability variables, both economic and financial, which indicates that their behavior is different and they are not related to the same intensity with the other variables (see

Table A3).

Once the factors have been identified, the correlations between the most selected variables of each factor are analyzed: for factor 1 (size), the most representative variable is considered to be operating income; for factor 2, earnings, only this variable is included since it is a single variable; and, for factor 3, profitability, specifically financial profitability is considered since it better represents the concept of profitability as it is an indicator of the relationship between the company’s revenues and invested equity.

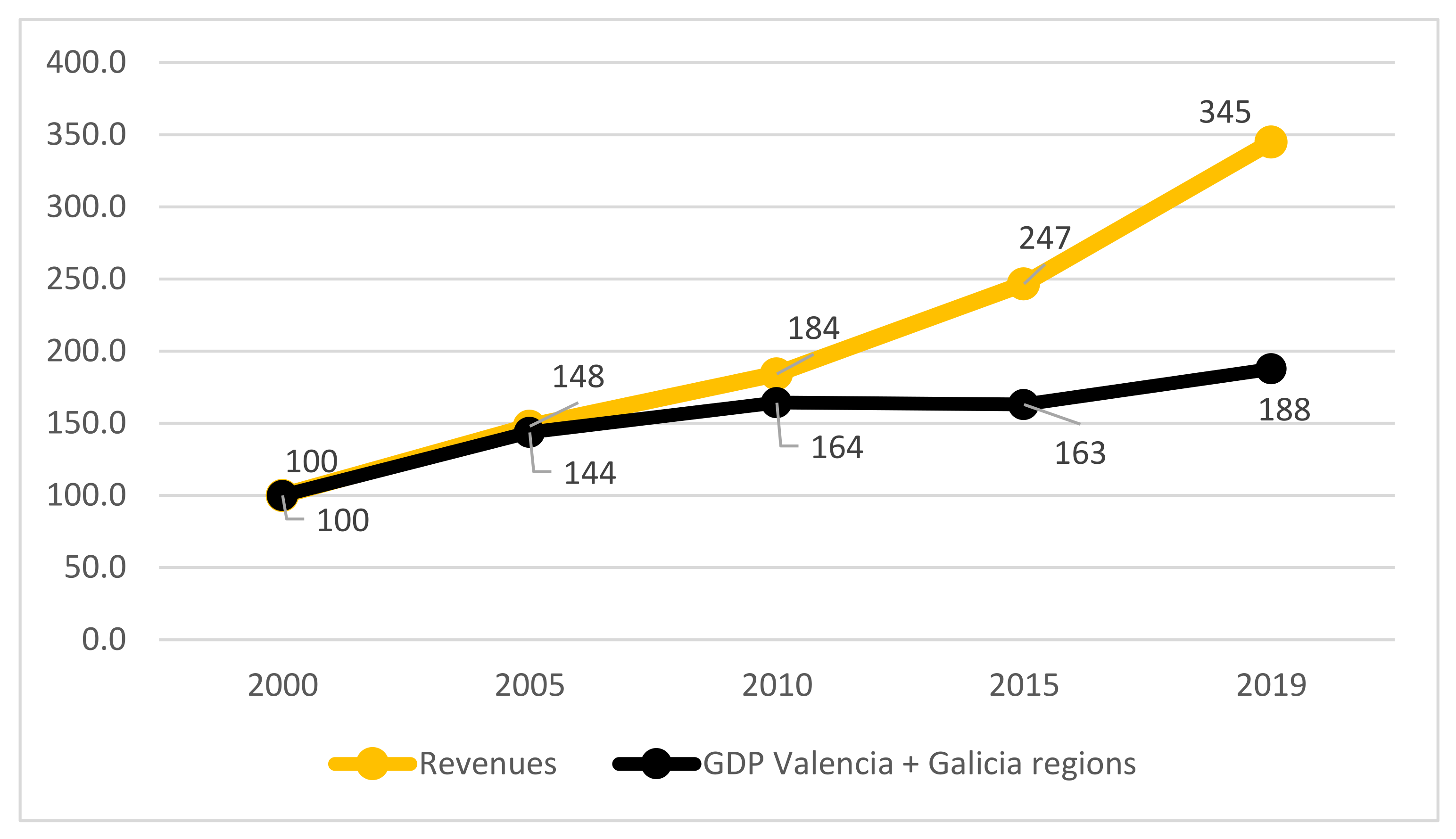

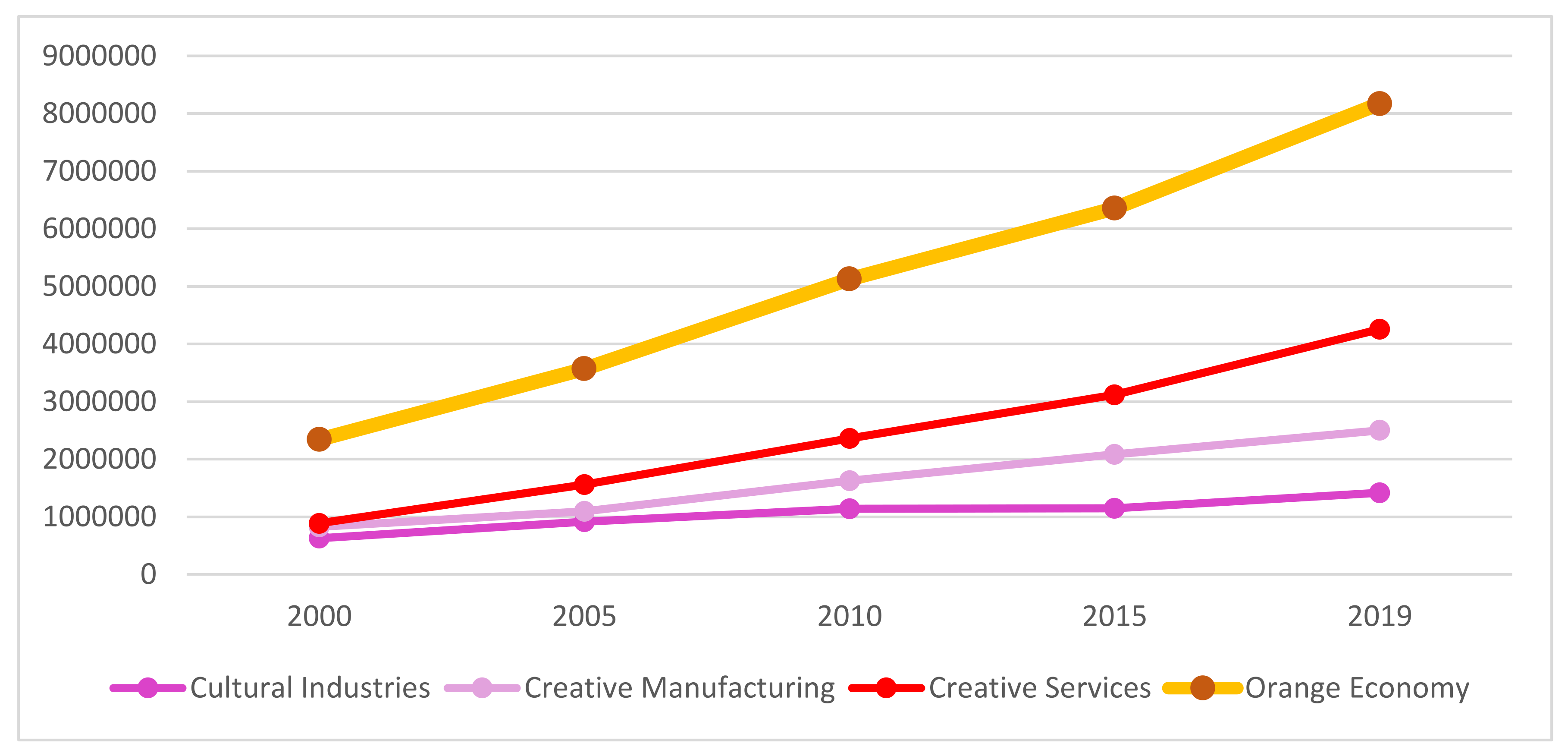

The Orange sector’s revenue growth has been much higher than the economy’s GDP. The Orange economy has experienced a significant increase for the period analyzed (2000–2019), more than triple the value at the beginning of the period. Thus, there was an increase of 344.9% in the sector’s revenue at current prices compared to a GDP growth of 87.6% in both regions (see

Figure 2 and

Table A4.). In terms of proportion, GDP revenues from the Orange economic sector reached 4.8% of GDP in 2019 compared to 2.6% in 2000. Another relevant figure is the turnover in Spain, which has increased by 22.1% in the period 2015–2019; an interval in which the Orange economy has risen by 39.9%. Growth occurred in all subgroups, with the creative services subgroup experiencing the largest increase in percentage terms (693.6%).

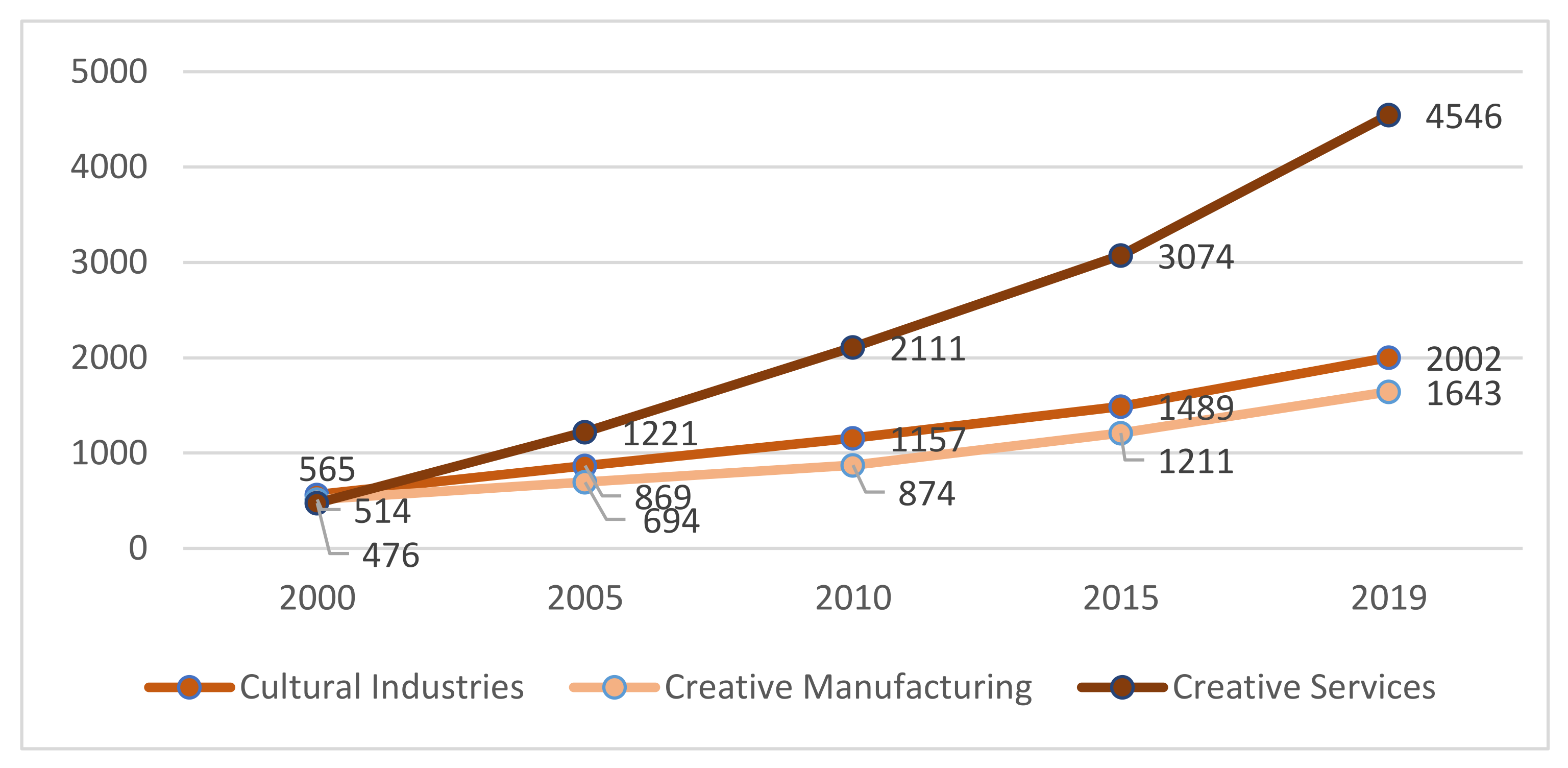

Another notable aspect is the increase in revenue and the number of companies in a period that has coincided with one of the biggest crises in the Spanish economy (spanning 2008 to 2014, when after several years of decline the annual GDP growth rate reached 1.4%.), which reveals the attractiveness of the Orange economy and its resilience, (

Figure 3 and

Table A5).

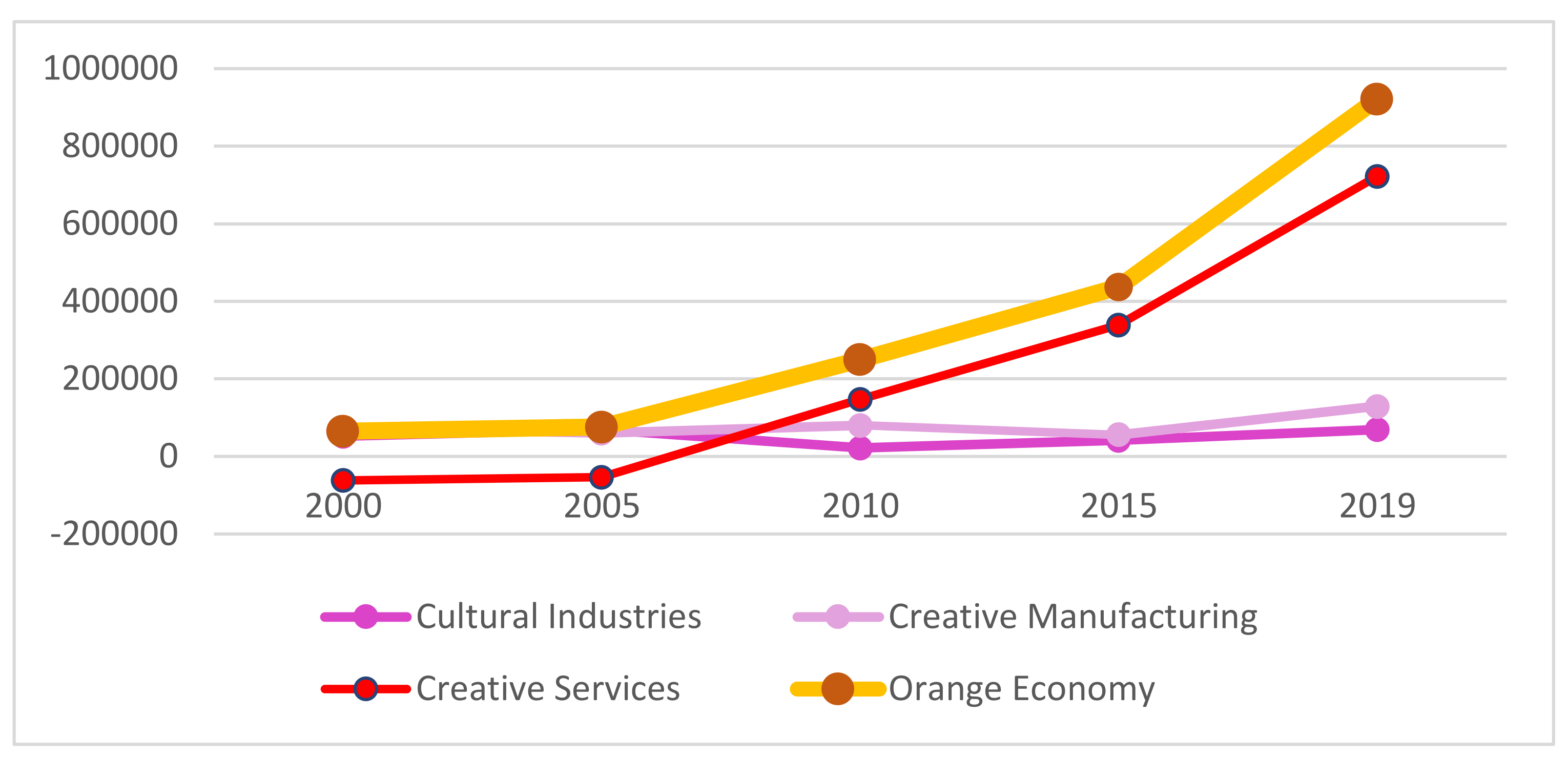

In terms of earnings before taxes (EBT) in current terms, the Orange economic sector has increased across 19 years more than 13 times their initial value (1316.2%), from €65,083 thousands in 2000 to €921,709 thousands in 2009 (see

Table A6), a fact that evidences the good economic health of the sector. The EBTs of the Orange economy have been beneficial for society. Companies that obtain good profitability pay higher corporate taxes. If we consider that the tax rate is 25%, based on the data, the estimated collection of the State Agency of Tax Administration (AEAT) for corporations in 2019 will amount to €230,427.3 thousand. As for VAT, with a general tax rate of 21%, the VAT charged is estimated at €293,456 thousand.

In the analysis of the sector’s growth, it was considered appropriate to study the evolution of the correlations between the selected variables, measured by the Spearman coefficient (

Table A7). For this purpose, the years 2005 (before the crisis), 2010 (during the crisis period), and 2019 (before the crisis caused by the COVID-19 pandemic) were considered. In the case of the correlation between revenues and earnings, the index is similar over time, although it decreases during the crisis period. As for the variable earnings and financial profitability, the index shows a moderate and unequal relationship over time, with a very weak relationship in the crisis period. In the case of financial profitability, measured by the ratio between earnings and shareholders’ equity, the low correlation between earnings and profitability can only be explained by a low relationship between earnings and shareholders’ equity. The decrease in the correlation between earnings and profitability in 2010 compared to 2005 is explained by a much larger drop in earnings than in shareholders’ equity. The higher ratio in 2019 is explained by a higher growth in earnings than in shareholders’ equity. Although the profitability of the sector is related to the following hypothesis, it has been considered appropriate to include it in this section, since the objective is to analyze its relationship with the variable revenues and earnings. The correlations between the different blocks of the Orange economy have also been analyzed (see

Table A8).

It can be concluded that the first of the hypotheses is fulfilled, since the high growth of the Orange economy has been proven, with rates—even in periods of crisis—much higher than those of the Spanish economy as a whole.

Hypothesis 2. Profitability has been analyzed on the basis of the two traditional ratios: economic profitability and financial profitability. Economic profitability is determined from the ratio of earnings before taxes to total assets. Financial profitability is determined from the ratio of earnings before taxes to equity.

We understand that an activity will be economically sustainable when it is durable over time. For this, it is not enough for the level of income to increase or to be maintained in real terms. In addition, the earnings must be positive, although not necessarily during each of the years considered. The two ratios mentioned, economic and financial profitability, are also indicators of sustainability. The maintenance of an activity over time and, therefore, its capacity to generate employment in a sustainable manner in a free-market context requires that the capital invested in this activity achieves an attractive return on capital. If returns are positive and higher than in other sectors, capital flows into the activity, increasing income and employment.

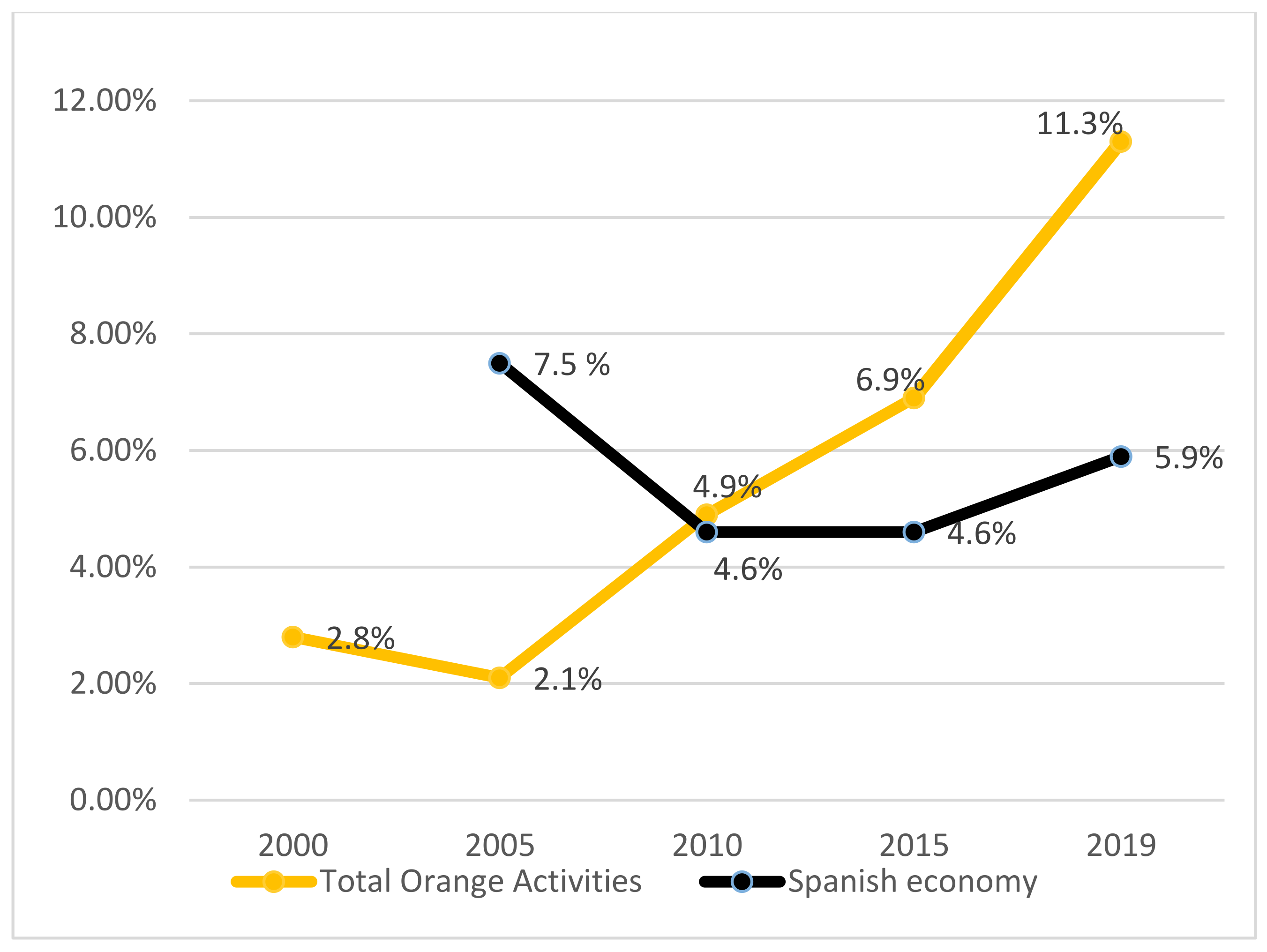

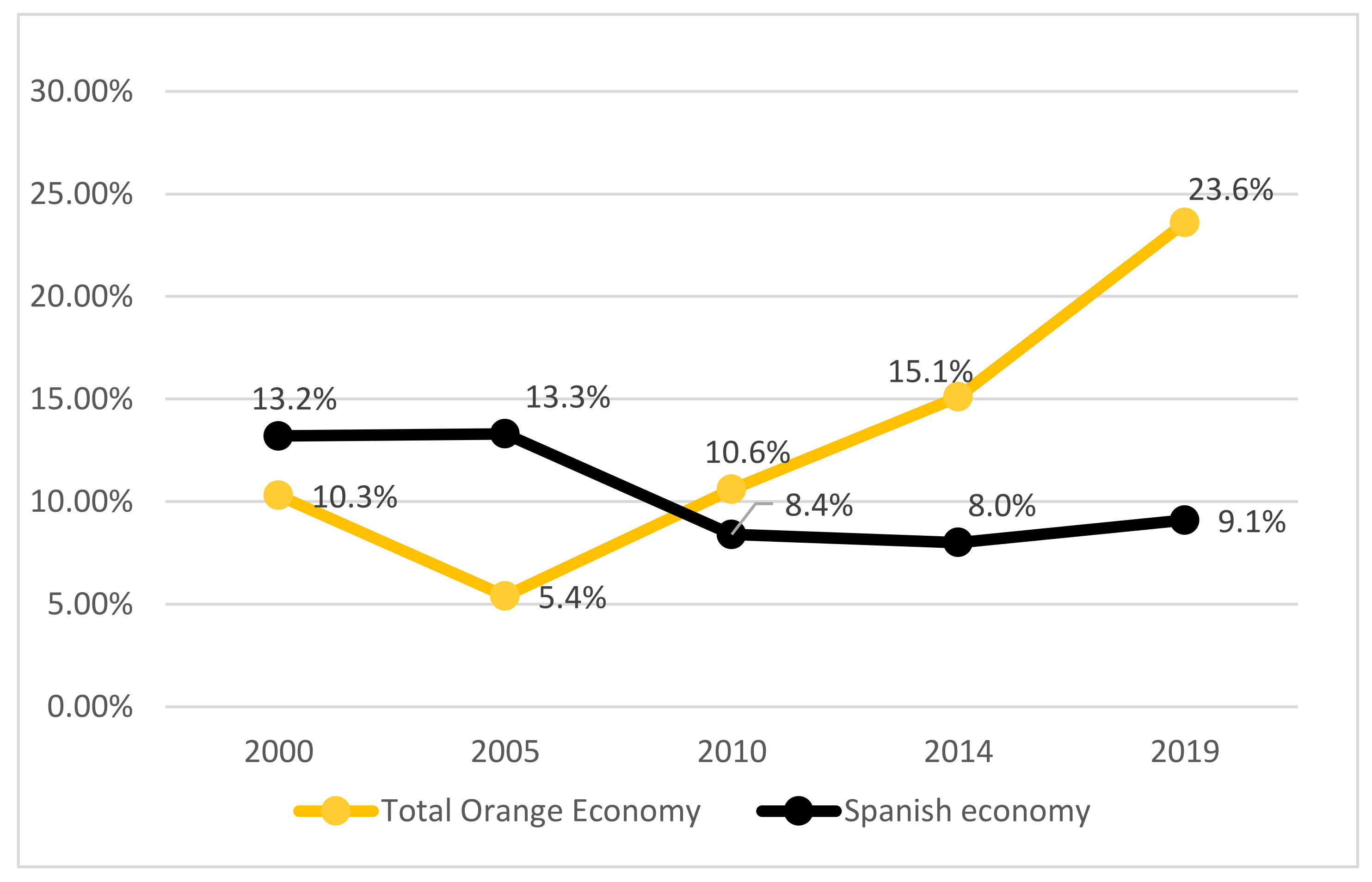

A key indicator of economic sustainability is economic profitability over time, which is shown in

Figure 4 and

Table A9. The first conclusion that can be drawn is that the economic profitability of the Orange economic sector is higher than the general company’s profitability in Spain. In fact, there is an increase in the differences in each year of the 2000–2019 period, up to 11.3% compared to the 5.9% on average for the country.

If we look at the evolution of economic profitability, we can see that before the crisis, the profitability of the Orange sector was lower than that of the Spanish economy as a whole, but this behavior has changed since the crisis, as the economic profitability ratio of the Orange sector is much higher than that of the Spanish economy as a whole.

Financial profitability, in terms of evolution, shows a behavior similar to that of economic profitability. Before the crisis, the ratio was lower than that of the economy as a whole, and then it reversed. In this case, as in the case of economic profitability, which measures the proportion that EBT represents of the company’s level of equity; if we analyze the equity, it can be seen in

Figure 5 and

Table A10 that during the period 2000–2019 it multiplied more than 5 times, which again demonstrates the strength of the sector.

It can be concluded that the second hypothesis is fulfilled by demonstrating that since 2010 the economic and financial profitability of the Orange economy has substantially exceeded that obtained by the Spanish economy.

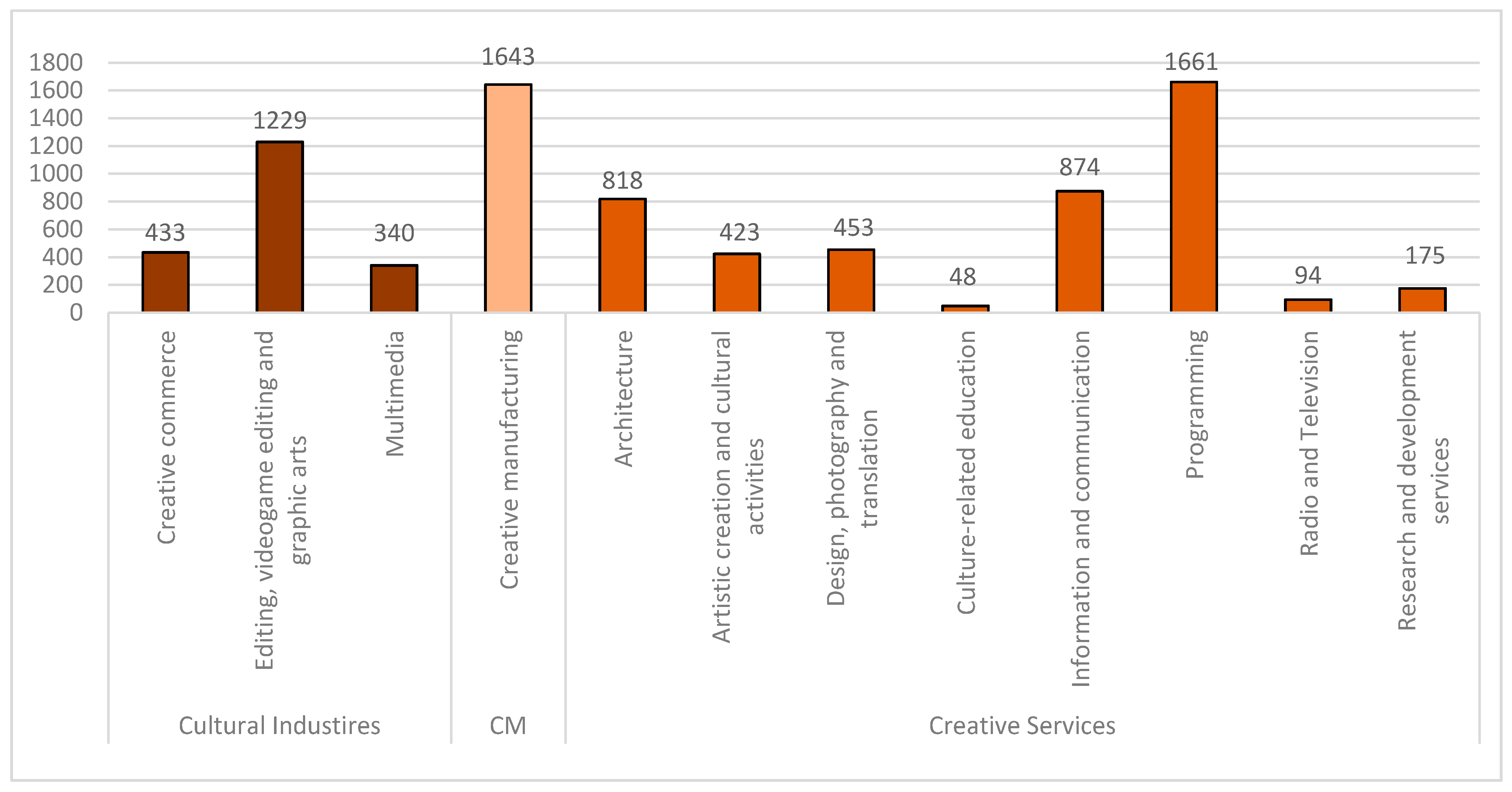

Hypothesis 3. It is noteworthy that for the period 2000–2019, operating revenues of the different subgroups and branches of the Orange economy have grown above the GDP growth at current prices, in all cases except for radio and television, which have suffered a decrease. The subgroup with the highest growth rate is creative services (693.6%). At the branch level, design, photography, and translation (3082.6%); artistic creation and cultural activities (1222.2%); and research and development services (1017.6%) stand out. Another noteworthy block is programming, which with a growth rate of 924.7%, ranks second in terms of turnover (see

Table A4). The increase in revenue from the Orange economy is related to the sharp increase in companies from 1550 organizations in 2000 to 8191 in 2019. This represents an increase of 426.8% (

Table A5), a general increase in all subgroups and all branches. This is evidence of the sector’s strength. There is an almost 100% correlation between turnover and the number of companies generated in all branches. In fact, the number of companies also grows in the branches with the highest turnover, such as creative manufacturing (319.6%), programming (1019%), and multimedia (772.7%). In addition, the spectacular growth of companies in education (2400%), architecture (1363.3%) and artistic creation (1321.9%) activity branches is noteworthy, which shows the absence of barriers to entry, except in the radio and television branch, where corporations have a greater presence (27.4%) and a negative correlation has been observed between turnover and company creation.

Table A11 shows the significance level of revenue by activity branches, obtained after applying a unifactorial variance analysis and Levene’s test for the most representative activity branches of the Orange economy. Levene’s test allows determining whether or not equal variances were assumed in the distribution of the compared data. The earnings show that the creative manufacturing branch has generated the most revenue in a very significant way sig < 0.001 (***) when compared to the other branches, except when compared to design and photography, which is the second with the highest average revenue.

If we talk about earnings in 2019, in this branch, the average earnings per company are 8.63 higher than the earnings per company for the sector as a whole. In the research services activity branch, the figure is also very high but somewhat lower, 7.56 times. Once again, the radio and television activity branch stands out in a negative sense, with losses amounting to 9.2 times the sectoral average. It should be taken into account that these activities are either public entities with the objective of providing a social service or they receive subsidies from the public sector. The case in culture-related education, with only 1.9% of the sectoral average, its average revenue amounted to 19% in 2019. (See

Table A6)

An earnings comparison with revenue shows that the design, photography, and translation activity branch—in fourth place of the sector’s revenue (8.2%)—accounts for 47.8% of the sector’s total earnings. On the other hand, for the manufacturing activity branch, the behavior is reversed, with 45% of operating revenues and 14.5% of EBT. Programming, on the other hand, with 14.3% compared to an initial 10.2%, shows a similar proportion. Also noteworthy are the research services activity branch, with 16.1% of the earnings, and information and communication, which reached 12.6%.

If we analyze the earnings evolution, the high growth obtained by the design and photography activity branch is striking, which has gone from a value of €608 thousand in 2000 to €440,448 thousand in 2019. The initial value is multiplied by a little more than 724 times in 2019. In addition, the dynamism of the programming activity branch should also be noted, with earnings increasing from €5160 thousands in 2000 to €93,817 thousands in 2019, (

Figure 6 and

Table A6). Activities such as those carried out by the information and communication and research services activity branches, despite not being the most important in terms of revenue, have improved significantly, with growth rates of 1175% and 27,032.4%, respectively.

In terms of total assets, the analyses reveal that the branch requiring the most assets is creative manufacturing, reaching 30.6% of total assets in 2019. Other activities with high proportions are those related to: artistic creation (13.7% of the total) and programming (12.7% of the total). On the contrary, the education for culture activity branch requires few assets in relation to the sector average, which is not contradictory with having been the area with the highest growth in assets during the period 2000–2019, achieving a growth rate of 3900%. Design and photography again expresses its dynamism, with a 2715% growth in assets during this period. In similar terms, programming (1464.8%) and research services (1668.6%) activity branches show a similar growth in assets, with an increase of 249.2% in 19 years, which is indicative of an increase in investment in this sector (

Figure 7 and,

Table A12).

Additionally outstanding is the performance of the research and development services activity branch, with 22.9% of economic profitability, double the sector average and four times the national average. Its average earnings before tax has increased by 2070.6%, and that it has gone from profits of €546 thousand in 2000 to €148,143 thousand in 2019—the good performance of this branch is evident. However, its revenue over the total of the sector accounts for 2.8%, which places it in seventh place in this section. Information and communication also deserves a mention in this section, since with 18.7% profitability it is the third most profitable branch. Moreover, its growth in earnings before taxes has increased by 1175.5% over the last 19 years. On a negative note, it is worth mentioning the poor economic profitability of radio and television, as it is a low-yield sector with a need for high assets. The case of artistic creation is similar, with a low profitability of 0.7%, as it has an increase in assets that is much higher than EBT. Finally, it is worth noting that the education related to culture activity branch, without requiring many assets, has a return clearly below the average for the sector (

Table A9).

The application of unifactorial variance method and Levene’s test make it possible to obtain the degree of significance in this section. Thus,

Table A13 shows that the creative manufacturing activity branch has the highest level of assets in a significant way, but this is to the detriment of its economic profitability since this ratio does not show any significance with respect to the other blocks. The profitability of the design and photography activity branch is significant but only compared to editing, videogame editing, and graphic arts (third in terms of revenue). Moreover, even though it is the most profitable, it is not statistically significantly more profitable than the other activities. The comparison of economic profitability between the other branches does not allow us to conclude that the returns are statistically significant. Another noteworthy fact is that of the creative manufacturing and editing, videogame editing, and graphic arts, which occupy first and third place in turnover, respectively, and despite having financial profitability below the sector average, they have been higher than the Spanish average.

To determine the significance of financial profitability, it is necessary to apply variances with Levene’s test. In general terms, manufacturing repeats as the activity branch with the highest equity, and it is significant with respect to programming and to editing, videogame editing, and graphic arts (

Table A14). In any case, it is not as significant as total assets. There are not statistically relevant differences in financial profitability; not even the design, photography, and translation branch, which had significant comparisons in its favor, shows its best financial ratios in statistical significance.

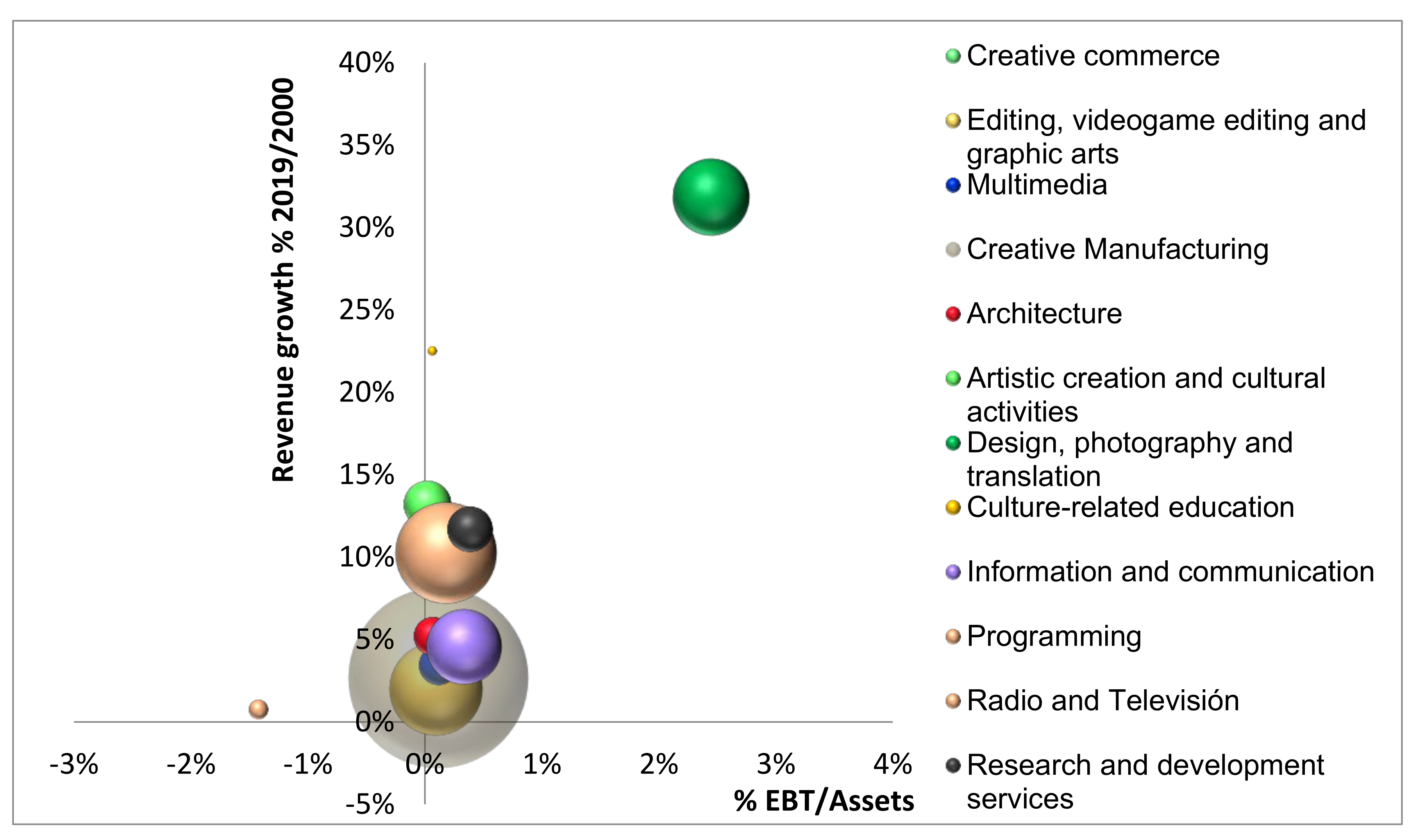

Figure 8 visually shows the importance or weight that each of the activity branches has in the Orange economy as a whole, measured in 2019 revenues (size of the figure), together with the dynamism shown in the period 2000–2019; comparing turnover levels (vertical) and % financial profitability (horizontal), it can be said:

It can be seen that the star sector of economic sustainability is the design, photography, and translation activity branch, with the highest growth in revenue, the highest financial profitability, and ranking fourth in terms of revenue.

The branch with the greatest current weight is creative manufacturing, which represents an average turnover for the period 2000–2019 of almost 50% of the sector’s total turnover. It has experienced a growth of 166.6% in that period, above the regional GDP (INE, 2021), which grew by 87.6%. Its financial profitability was 11.8% in 2019, above the national average (9.1%).

Few activities in Spain can boast a growth pattern of 924.7%, have the third highest financial profitability (18.4%), and hold the second place for revenue in the Orange economy (14.3%), such is the case of the programming branch activity.

A fourth branch with an outstanding position, but lower than the previous three, is research services. Its high profitability (38.5%) is the second highest in the sector. Moreover, its growth was 1071.6% during the period under study. On the other hand, its level of turnover is not very significant, representing only 2.8% of the Orange economy.

Finally, it is worth highlighting information and communication activity, since it ranks third in terms of financial profitability (38.5%). Although its growth (354.8%) was lower than that of other more dynamic blocks, it was higher than the average for the sector and for GDP. This block accounts for 7.9% of the sector’s total and therefore occupies a well-deserved fourth position.

It can be concluded that the third hypothesis is fulfilled, since it has been shown that there are differences in the variables’ evolution in the different blocks and branches of activity during the period analyzed. However, the ANOVA shows that the differences are not significant, so their inclusion in the same sector can be considered (see

Table A13 and

Table A14).

5. Discussion and Conclusions

The Orange economy, which encompasses the creative industries and the cultural sector, has been the subject of growing interest in the last two decades. Since the beginning of the 21st century, the potential of cultural and creative activities to generate sustainable growth has been increasingly recognized [

5,

7,

12,

15,

16,

18,

27], showing greater resilience than the rest of the economy during the 2008 crisis [

11,

44] and higher growth after the crisis [

13]. Many countries have opted for the implementation of policies to promote cultural and creative industries because of their capacity to generate employment [

14]. Although consideration of the potential of the Orange economy as an engine of sustainable growth is quite widespread, empirically proven results are lacking [

14,

38]. This paper contributes to alleviating the lack of empirical studies, focused on the role of the Orange economy in two Spanish regions, with the aim of providing knowledge about the possibilities of this sector as a driver of the economy and assessing its economic sustainability.

On the other hand, as it is a sector formed by activities that differ significantly in their characteristics, it is not enough with a global vision and it is necessary to delve into the different activities that conform it [

17]. This study provides specific knowledge of the different activities and valuable information for the design and the implementation of economic policy measures.

From the analyses conducted, it can be concluded that the Orange economy, inclusive of the creative industries, has behaved as a dynamic and economically sustainable sector. After the crisis, Orange economic growth, in relative terms, has been higher than in the economy as a whole and the same can be said of the economic and the financial profitability rates.

The analyses carried out allow us to conclude that Hypothesis 1 is fulfilled. The Orange economy is growing faster than the economy as a whole and it is an engine of growth. Starting with the operating revenue in the Orange sector, at the beginning of the period, in 2000 it represented 2.6% of GDP; and, at the end of the period, in 2019, this share rose to 4.8%. The results support the assertion of an increase in the share of the creative economy in the GDP of developed countries [

40]. For the two regions considered together, the Valencian and the Galician regions, the growth rate of the Orange sector’s operating revenue for the period (2000–2019) amounts to 244.94%, while the GDP growth reaches 87.6%. Therefore, the Orange sector’s revenue growth rate is much higher than that of nominal GDP. The results of the study conducted are in line with those that point to the significant revenue generating capacity of creative industries and the cultural sector [

7,

14,

39]. The growth is significant not only in revenues, since the number of enterprises is also increasing to a large extent. In 2000, in the regions of Valencia and Galicia, it amounted to 1555, and by the end of the period in 2019 the figure reached 8191 companies, an increase of 426.8%. As for the evolution of earning before taxes, if we compare the year 2000 with 2019, the variation rate is 1316.20%. The increase in earnings has been slightly more than 13 times the initial value, growing above the economy’s average. Good growth rates are positive for society; generating greater capital income means greater tax collection, which has an impact on governments’ budgetary capacity and, therefore, greater capacity to provide public goods and services. The results obtained support the affirmation of the Orange economy as an engine of economic growth [

7,

14,

17,

18,

31,

32].

Another aspect of interest is the sector’s resilience, i.e., its ability to cope with or recover from adverse situations such as the 2008 crisis. As to the question, are cultural and creative activities resilient? The data from the study indicate that during the 2008 crisis there was an increase in revenue and in the number of companies. These results are consistent with other studies. The results support the resilience of Orange activities [

11,

41]. Other cases, such as the study conducted for the United States, indicate that the cultural economy did not experience decline during the recession [

44].

The study shows that, on average, companies in the Orange sector, have achieved higher levels of profitability when compared to the levels achieved by the economy as a whole, since the 2008 crisis. The higher profitability achieved since the crisis are evident in that the Orange economy is a resilient sector. Thus, the analyses carried out confirm Hypothesis 2.

The activities included in the Orange economy are very varied. It is not enough to have a global picture of the sector’s evolution, but it is necessary to delve deeper into the impact of the different activities on growth. The analyses carried out support the third hypothesis: it can be affirmed that there are differences in growth rates as well as in profitability levels, if we consider the different activities of the Orange sector, both by block and by branch of activity. For the period 2000–2019, the operating revenues of the different subsectors and activity branches of the Orange economy have grown above GDP growth, in all cases except for radio and television which suffered a decrease. The subsector with the highest growth rate is creative services (793.6%). At the activity branch level, design, photography, and translation (3182.6%); artistic creation and cultural activities (1222.2%); research and development services (1117.6%); and programming (1024.7%) stand out. If we analyze the center of the sector, the star activity is design, photography, and cultural activities, with the highest sales growth rate, the highest financial profitability, and a fourth position in terms of revenue. Contrary to the positive evolution of the design activity sector, creative manufacturing, which is the subsector with the highest weight, almost 50% of the turnover, is one of the least dynamic in terms of growth rates. In the case of programming activity, the growth is 924.7%, it has the third highest financial profitability (18.4%), and it represents the second place in revenue (14.3%).

In relation to the work limitations and future research lines, it should be noted that our analysis has an important limitation, we do not consider in the study those companies that due to their status as sole proprietors are not required to file accounts in the Mercantile Register and, therefore, do not appear in the SABI

® database. This limitation is especially important in some activities as they involve numerous self-employed people [

37]. Furthermore, we must delve deeper into the other two pillars of sustainability, the social pillar and the environmental pillar [

45]. Once the sector’s capacity to generate income, employment, and positive earnings is known, we must assess the sector’s contribution to social sustainability by answering questions such as jobs generated, quality, salaries, and income distribution. To what extent does the Orange economy generate quality jobs? What is the distribution of income like? We should not stop at merely assessing growth. It is necessary to go further and study the impact on the welfare of the population.

Of course, assessing sustainability requires a response to aspects related to environmental impact. It has often been considered that creative sectors and Cultural industries are not polluting, but there are many activities included in this term and it does not seem to be possible to generalize. There is a lack of empirical evidence in this regard.

Beyond the study scope of sustainable economic, social, and environmental development, another aspect to be taken into account is to extend the study territory to include large and medium-sized cities, since creative activities are mainly concentrated in cities and it seems that the city’s size matters. As future research lines, it is proposed to extend the present investigation to other autonomous communities, as well as to carry out comparative studies with other countries.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}