Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude

,

,  , and

, and

Abstract

1. Introduction

2. Literature Review

2.1. Fintech Services

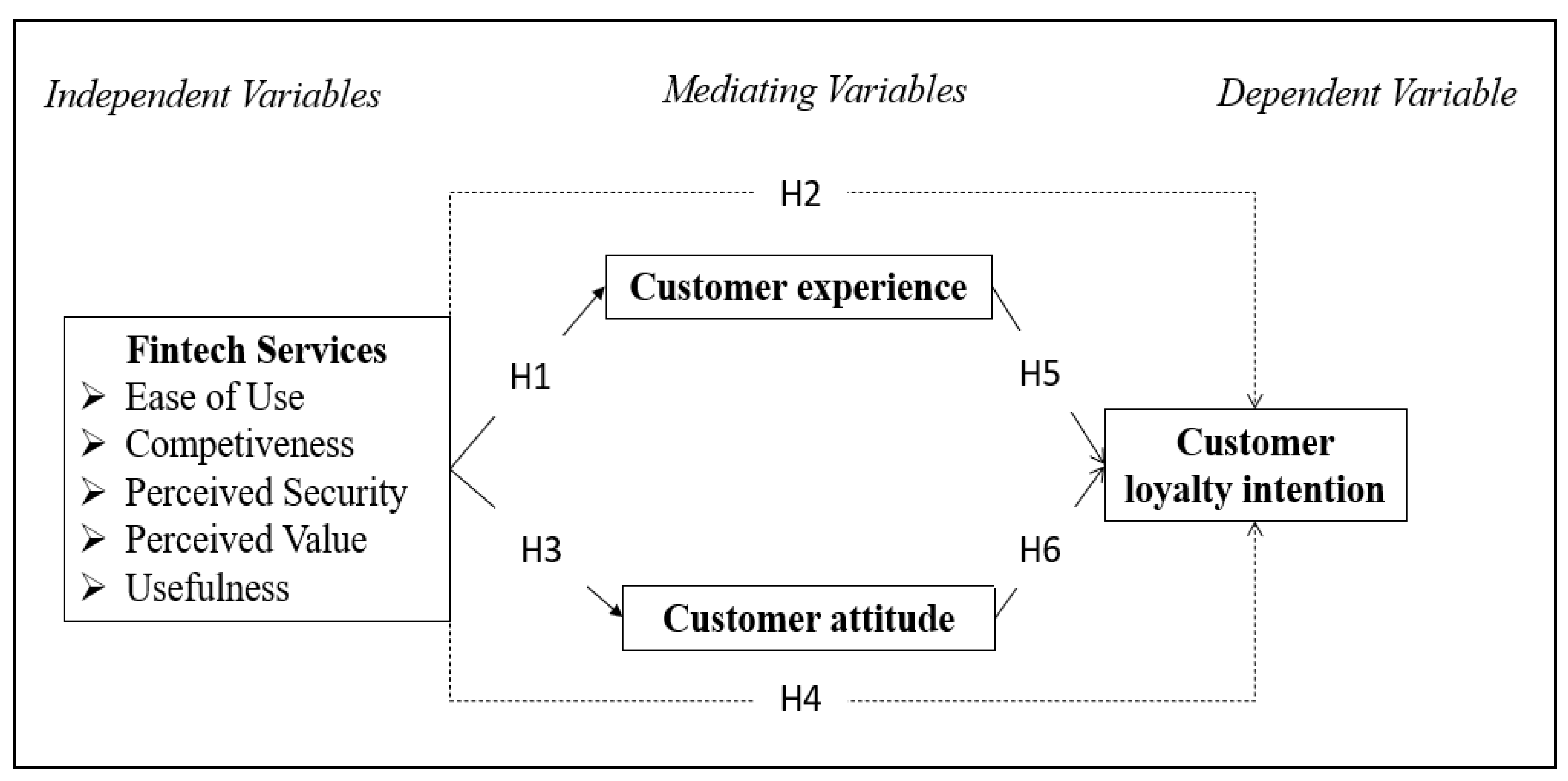

2.2. Theoretical Framework and Hypothesis Development

2.2.1. Technology Acceptance Model (TAM)

2.2.2. Fintech Services and Customer Experiences

2.2.3. Fintech Services and Customer Attitudes

2.2.4. Customer Experience and Customer Loyalty Intentions

2.2.5. Customer Attitude and Customer Loyalty Intention

3. Methods

3.1. Sample and Population

3.2. Measurement of Constructs

3.3. Data Collection Procedure

3.4. Demographic Profile

4. Analysis and Findings

4.1. Analyzing Tools

4.2. Measurement Model

4.3. Structural Model

4.4. Fit Indices

5. Discussion

6. Conclusions

6.1. Theoretical Implications

6.2. Managerial Implications

6.3. Research Limitations and Future Scope

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Mention, A.L. The Future of Fintech. Res. Technol. Manag. 2019, 62, 59–63. [Google Scholar] [CrossRef]

- Jin, C.C.; Seong, L.C.; Khin, A.A. Factors Affecting the Consumer Acceptance towards Fintech Products and Services in Malaysia. Int. J. Asian Soc. Sci. 2019, 9, 59–65. [Google Scholar] [CrossRef]

- Temelkov, Z. Financial technology companies as a positive disruptor for the hospitality industry. Sci. Refereed Online J. Impact Factor 2019, 54, 72–77. Available online: http://eprints.ugd.edu.mk/21561/ (accessed on 9 November 2022).

- Zhang, B.Z.; Baeck, P.; Ziegler, T.; Bone, J.; Garvey, K. Pushing Boundaries: The 2015 UK Alternative Finance Industry Report. 2016. Available online: https://ssrn.com/abstract=3621312 (accessed on 25 August 2022).

- Grèzes, V.; Emery, L.; Schegg, R.; Perruchoud, A. Crowdfunded tourism activities: Study on the direct impact of Swiss crowdfunding platforms on the tourism industry. In Proceedings of the Conference: Travel & Tourism Research Association, Innsbruck, Austria, 22–24 April 2015; pp. 1–10. [Google Scholar]

- Pollari, I.; Ruddenklau, A. Pulse of Fintech H2 2019. In Global Trends; KPMG International: Amstelveen, The Netherlands, 2020; p. 9. [Google Scholar]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Bolton, R.N.; McColl-Kennedy, J.R.; Cheung, L.; Gallan, A.; Orsingher, C.; Witell, L.; Zaki, M. Customer experience challenges: Bringing together digital, physical and social realms. J. Serv. Manag. 2018, 29, 776–808. [Google Scholar] [CrossRef]

- Cetin, G. Experience vs. quality: Predicting satisfaction and loyalty in services. Serv. Ind. J. 2020, 40, 1167–1182. [Google Scholar] [CrossRef]

- Lemon, K.N.; Verhoef, P.C. Understanding customer experience throughout the customer journey. J. Mark. 2016, 80, 69–96. [Google Scholar] [CrossRef]

- Alam, M.M.D.; Karim, R.A.; Habiba, W. The relationship between CRM and customer loyalty: The moderating role of customer trust. Int. J. Bank Mark. 2021, 39, 1248–1272. [Google Scholar] [CrossRef]

- Al Karim, R.; Habiba, W. How CRM Components Impact Customer Loyalty: A Case from Bangladesh Banking Industry. J. Manag. Inf. 2020, 7, 43–61. [Google Scholar] [CrossRef]

- Khanam, M.J.J. Regulatory Challenges and Social Opportunities of Financial Inclusion through Fintech in Developing Countries with Reference to Bangladesh. September 2020. Available online: https://ritsumei.repo.nii.ac.jp/?action=repository_action_common_download&item_id=13918&item_no=1&attribute_id=20&file_no=1 (accessed on 29 August 2022).

- Rahman, B.; Ahmed, O.; Shakil, S. Fintech in Bangladesh: Ecosystem, Opportunities and Challenges. Int. J. Bus. Technopreneurship 2021, 11, 73–90. [Google Scholar]

- Rashid, H. Prospects of Digital Financial Services in Bangladesh in the Context of Fourth Industrial Revolution. Asian J. Soc. Sci. Leg. Stud. 2020, 2, 88–95. [Google Scholar]

- Ahmed, N.; Rony, R.J.; Khan, S.S.; Ahmed, M.S.; Sinha, A.; Saha, A.; Amir, S.; Abeer, I.A.; Sarcar, S. Resilience During COVID Pandemic: Role of Fintech in the Perspective of Bangladesh. 2022. Available online: https://ssrn.com/abstract=4009497 (accessed on 22 September 2022).

- Eickhoff, M.; Muntermann, J.; Weinrich, T. What do Fintechs actually do? A Taxonomy of Fintech Business Models. In Proceedings of the International Conference on Information Systems—Transforming Society with Digital Innovation, ICIS 2017, Seoul, Republic of Korea, 10–13 December 2017. [Google Scholar]

- Stulz, R.M. Fintech, BigTech, and the Future of Banks. J. Appl. Corp. Financ. 2019, 31, 86–97. [Google Scholar] [CrossRef]

- Kim, Y.; Park, Y.J.; Choi, J.; Yeon, J. An empirical study on the adoption of “Fintech” service: Focused on mobile payment services. Adv. Sci. Technol. Lett. 2015, 114, 136–140. [Google Scholar]

- Wang, M.; Chang, Y. Technology leadership, brand equity, and customer loyalty towards fintech service providers in China. In Proceedings of the Twenty-Fourth Americas Conference on Information Systems, New Orleans, LA, USA, 16–18 August 2018. [Google Scholar]

- Oshodin, O.; Molla, A.; Karanasios, S.; Ong, C.E. Is Fin tech a disruption or a new eco-system? An exploratory investigation of banks response to fintech in Australia. In Proceedings of the 28th Australasian Conference on Information Systems, Sydney, Australia, 3–6 December 2017. [Google Scholar]

- Gulamhuseinwala, I.; Bull, T.; Lewis, S. FinTech is gaining traction and young, high-income users are the early adopters. J. Financ. Perspect. 2015, 3, 16–23. [Google Scholar]

- Barbu, C.M.; Florea, D.L.; Dabija, D.C.; Barbu, M.C.R. Customer experience in fintech. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1415–1433. [Google Scholar] [CrossRef]

- Moore, G.C.; Benbasat, I. Fintech Adoption: A Critical Appraisal of the Strategies of Paytm in India. IUP J. Manag. Res. 2020, 19, 7–17. [Google Scholar]

- Haqqi, F.R.; Suzianti, A. Exploring Risk and Benefit Factors Affecting User Adoption Intention of Fintech in Indonesia. In Proceedings of the 3rd Asia Pacific Conference on Research in Industrial and Systems Engineering, Depok, Indonesia, 16–17 June 2020; pp. 13–18. [Google Scholar]

- Ryu, H.S. What makes users willing or hesitant to use Fintech? The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Nawayseh, M.K. Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of Fintech applications? J. Open Innov. Technol. Mark. Complex. 2020, 6, 153. [Google Scholar] [CrossRef]

- Baber, H. Impact of Fintech on customer retention in Islamic banks of Malaysia. Int. J. Bus. Syst. Res. 2020, 14, 217–227. [Google Scholar] [CrossRef]

- Alkhazaleh, A.M.K.; Haddad, H. How does the Fintech services delivery affect customer satisfaction: A scenario of Jordanian banking sector. Strateg. Chang. 2021, 30, 405–413. [Google Scholar] [CrossRef]

- Huei, C.T.; Cheng, L.S.; Seong, L.C.; Khin, A.A.; Leh Bin, R.L. Preliminary study on consumer attitude towards Fintech products and services in malaysia. Int. J. Eng. Technol. (UAE) 2018, 7, 166–169. [Google Scholar] [CrossRef]

- Morgan, P.J.; Trinh, L.Q. Fintech and Financial Literacy in the Lao PDR. 2019. Available online: https://ssrn.com/abstract=3398235 (accessed on 8 October 2022).

- Doan, T.T.T. The Effect of Perceived Risk and Technology Self-Efficacy on Online Learning Intention: An Empirical Study in Vietnam. J. Asian Financ. Econ. Bus. 2021, 8, 385–393. [Google Scholar]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User acceptance of computer technology. J. Manag. Sci. 1989, 35, 982–1003. [Google Scholar]

- Setiawan, B.; Nugraha, D.P.; Irawan, A.; Nathan, R.J. User Innovativeness and Fintech Adoption in Indonesia. J. Open Innov. Technol. Mark. Complex. 2021, 7, 188. [Google Scholar] [CrossRef]

- Arulraj, D.J.; Annamalai, T.R. Firms’ Financing Choices and Firm Productivity: Evidence from an Emerging Economy. Int. J. Glob. Bus. Compet. 2020, 15, 35–48. [Google Scholar] [CrossRef]

- Dwivedi, P.; Ibrahim, J.; Rajeev, A. Role of Fintech Adoption for Competitiveness and Performance of the Bank: A Study of Banking Industry in UAE. Int. J. Glob. Bus. Compet. 2021, 16, 130–138. [Google Scholar] [CrossRef]

- Momaya, K.S. The Past and the Future of Competitiveness Research: A Review in an Emerging Context of Innovation and EMNEs. Int. J. Glob. Bus. Compet. 2019, 14, 1–10. [Google Scholar] [CrossRef]

- Wang, Y.; Xiuping, S.; Zhang, Q. Can fintech improve the efficiency of commercial banks? —An analysis based on big data. Res. Int. Bus. Financ. 2020, 55, 101338. [Google Scholar] [CrossRef]

- Momaya, K.S.; Pandey, P.; Vallaturu, V.K.; Sonar, R.M.; Bodduri, A.K.S. Fintech platforms, and competitiveness: Exploring role of MoT as a differentiator for firms of Indian origin (FIOs). In Proceedings of the 29th International Conference on Management of Technology, Cairo, Egypt, 13 September 2020. [Google Scholar]

- Cajetan, I.M.; Patrick, O.E. Digital Banking, Customer Experience and Bank Financial Performance: UK Customers’ Perceptions. Eletronic Libr. 2018, 34, 1–5. [Google Scholar]

- Garg, R.; Rahman, Z.; Qureshi, M.N. Measuring customer experience in banks: Scale development and validation. J. Model. Manag. 2014, 9, 87–117. [Google Scholar] [CrossRef]

- Shiau, W.-L.; Yuan, Y.; Pu, X.; Ray, S.; Chen, C.C. Understanding fintech continuance: Perspectives from self-efficacy and ECT-IS theories. Ind. Manag. Data Syst. 2020, 120, 1659–1689. [Google Scholar] [CrossRef]

- Lee, E.-Y.; Lee, S.-B.; Jeon, Y.J.J. Factors influencing the behavioral intention to use food delivery apps. Soc. Behav. Pers. Int. J. 2017, 45, 1461–1473. [Google Scholar] [CrossRef]

- Najib, M.; Fahma, F. Investigating the Adoption of Digital Payment System through an Extended Technology Acceptance Model: An Insight from the Indonesian Small and Medium Enterprises. Int. J. Adv. Sci. Eng. Inf. Technol. 2020, 10, 1702. [Google Scholar] [CrossRef]

- Najib, M.; Ermawati, W.; Fahma, F.; Endri, E.; Suhartanto, D. FinTech in the Small Food Business and Its Relation with Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 88. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef]

- Chuang, L.-M.; Liu, C.-C.; Kao, H.-K. International Journal of Management and Administrative Sciences (IJMAS) The Adoption of Fintech Service: TAM perspective. Int. J. Manag. Adm. Sci. 2016, 3, 1–15. [Google Scholar]

- Ventre, I.; Kolbe, D. The Impact of Perceived Usefulness of Online Reviews, Trust and Perceived Risk on Online Purchase Intention in Emerging Markets: A Mexican Perspective. J. Int. Consum. Mark. 2020, 32, 287–299. [Google Scholar] [CrossRef]

- Suzianti, A.; Haqqi, F.R.; Fathia, S.N. Strategic recommendations for financial technology service development: A comprehensive risk-benefit IPA-Kano analysis. J. Model. Manag. 2021, 17, 1481–1503. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319. [Google Scholar] [CrossRef]

- Sciarelli, M.; Prisco, A.; Gheith, M.H.; Muto, V. Factors affecting the adoption of blockchain technology in innovative Italian companies: An extended TAM approach. J. Strategy Manag. 2021, 15, 495–507. [Google Scholar] [CrossRef]

- Le, M.T.H. Examining factors that boost intention and loyalty to use Fintech post-COVID-19 lockdown as a new normal behavior. Heliyon 2021, 7, e07821. [Google Scholar] [CrossRef] [PubMed]

- Yang, H.; Song, H.; Cheung, C.; Guan, J. How to enhance hotel guests’ acceptance and experience of smart hotel technology: An examination of visiting intentions. Int. J. Hosp. Manag. 2021, 97, 103000. [Google Scholar] [CrossRef]

- Huang, Y.C.; Chang, L.L.; Yu, C.P.; Chen, J. Examining an extended technology acceptance model with experience construct on hotel consumers’ adoption of mobile applications. J. Hosp. Mark. Manag. 2019, 28, 957–980. [Google Scholar] [CrossRef]

- Hasni, M.J.S.; Farah, M.F.; Adeel, I. The technology acceptance model revisited: Empirical evidence from the tourism industry in Pakistan. J. Tour. Futures, 2021; ahead-of-print. [Google Scholar]

- Singh, S.; Srivastava, P. Social media for outbound leisure travel: A framework based on technology acceptance model (TAM). J. Tour. Futures 2019, 5, 43–61. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.-H.; Loh, X.-M.; Hew, J.-J.; Ooi, K.-B. The disruptive mobile wallet in the hospitality industry: An extended mobile technology acceptance model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef] [PubMed]

- Bae, S.Y.; Han, J.H. Considering cultural consonance in trustworthiness of online hotel reviews among generation Y for sustainable tourism: An extended TAM model. Sustainability 2020, 12, 2942. [Google Scholar] [CrossRef]

- Jung, J.; Park, E.; Moon, J.; Lee, W.S. Exploration of sharing accommodation platform airbnb using an extended technology acceptance model. Sustainability 2021, 13, 1185. [Google Scholar] [CrossRef]

- Molinillo, S.; Navarro-García, A.; Anaya-Sánchez, R.; Japutra, A. The impact of affective and cognitive app experiences on loyalty towards retailers. J. Retail. Consum. Serv. 2020, 54, 101948. [Google Scholar] [CrossRef]

- Karim, R.A.; Islam, M.W. Assessing customer demand and customer satisfaction through social and environmental practices in the hotel sector of Bangladesh. GeoJournal Tour. Geosites 2020, 30, 843–851. [Google Scholar] [CrossRef]

- Van Thiel, D.; Van Raaij, F. Explaining customer experience of digital financial advice. Economics 2017, 5, 69–84. [Google Scholar]

- Moliner-Tena, M.A.; Monferrer-Tirado, D.; Estrada-Guillén, M. Customer engagement, non-transactional behaviors and experience in services: A study in the bank sector. Int. J. Bank Mark. 2019, 37, 730–754. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Lemon, K.N.; Parasuraman, A.; Roggeveen, A.; Tsiros, M.; Schlesinger, L.A. Customer experience creation: Determinants, dynamics and management strategies. J. Retail. 2009, 85, 31–41. [Google Scholar] [CrossRef]

- Rose, S.; Clark, M.; Samouel, P.; Hair, N. Online customer experience in e-retailing: An empirical model of antecedents and outcomes. J. Retail. 2012, 88, 308–322. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Service-dominant logic: Continuing the evolution. J. Acad. Mark. Sci. 2008, 36, 1–10. [Google Scholar] [CrossRef]

- Brakus, J.J.; Schmitt, B.H.; Zarantonello, L. Brand Experience: What is It? How is it Measured? Does it Affect Loyalty? J. Mark. 2009, 73, 52–68. [Google Scholar] [CrossRef]

- De Keyser, A.; Lemon, K.N.; Klaus, P.; Keiningham, T.L. A framework for understanding and managing the customer experience. Mark. Sci. Inst. Work. Pap. Ser. 2015, 85, 15–121. [Google Scholar]

- Homburg, C.; Jozić, D.; Kuehnl, C. Customer experience management: Toward implementing an evolving marketing concept. J. Acad. Mark. Sci. 2017, 45, 377–401. [Google Scholar] [CrossRef]

- Turlais, V. Business Scenario Planning for Declining Industry. J. Bus. Manag. 2016, 11, 14. [Google Scholar]

- Ajzen, I. The Theory of Planned Behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Khan, I.; Fatma, M.; Kumar, V.; Amoroso, S. Do experience and engagement matter to millennial consumers? Mark. Intell. Plan. 2021, 39, 329–341. [Google Scholar] [CrossRef]

- Becker, L.; Jaakkola, E. Customer experience: Fundamental premises and implications for research. J. Acad. Mark. Sci. 2020, 48, 630–648. [Google Scholar] [CrossRef]

- Bleier, A.; Harmeling, C.M.; Palmatier, R.W. Creating Effective Online Customer Experiences. J. Mark. 2018, 83, 98–119. [Google Scholar] [CrossRef]

- KPMG. The Truth About Customer Loyalty. 2019. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2019/11/customer-loyalty-report.pdf (accessed on 8 October 2022).

- Fornell, C. A National Customer Satisfaction Barometer: The Swedish Experience. J. Mark. 1992, 56, 6–21. [Google Scholar] [CrossRef]

- Jenneboer, L.; Herrando, C.; Constantinides, E. The Impact of Chatbots on Customer Loyalty: A Systematic Literature Review. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 212–229. [Google Scholar] [CrossRef]

- Brandtzaeg, P.B.; Følstad, A. Why People Use Chatbots. In Internet Science; INSCI 2017; Springer: Cham, Switzerland, 2017; pp. 377–392. [Google Scholar]

- Herrmann, A.; Xia, L.; Monroe, K.B.; Huber, F. The influence of price fairness on customer satisfaction: An empirical test in the context of automobile purchases. J. Prod. Brand Manag. 2007, 16, 49–58. [Google Scholar] [CrossRef]

- Krejcie, R.; Morgan, S. Sample size determination. Bus. Res. Methods 1970, 4, 34–36. [Google Scholar]

- Floyd, F.J.; Widaman, K.F. Factor analysis in the development and refinement of clinical assessment instruments. Psychol. Assess. 1995, 7, 286–299. [Google Scholar] [CrossRef]

- Rabiul, M.K.; Shamsudin, F.M.; Yean, T.F.; Patwary, A.K. Linking leadership styles to communication competency and work engagement: Evidence from the hotel industry. J. Hosp. Tour. Insights 2022, in press. [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Malhotra, A. ES-QUAL: A multiple-item scale for assessing electronic service quality. J. Serv. Res. 2005, 7, 213–233. [Google Scholar] [CrossRef]

- Ringle, C.M.; Sarstedt, M.; Straub, D.W. Editor’s comments: A critical look at the use of PLS-SEM in “MIS Quarterly”. MIS Q. 2012, 36, iii–xiv. [Google Scholar] [CrossRef]

- Lowry, P.B.; Gaskin, J. Partial least squares (PLS) structural equation modeling (SEM) for building and testing behavioral causal theory: When to choose it and how to use it. IEEE Trans. Prof. Commun. 2014, 57, 123–146. [Google Scholar] [CrossRef]

- Chin, W.W. How to Write Up and Report Pls Analyses; Springer: London, UK, 2010. [Google Scholar]

- Hair, J.F.; Howard, M.C.; Nitzl, C. Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. J. Bus. Res. 2020, 109, 101–110. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Nitzl, C.; Roldán Salgueiro, J.L.; Cepeda-Carrión, G. Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Ind. Manag. Data Syst. 2016, 116, 1849–1864. [Google Scholar] [CrossRef]

- Hoe, L.C.; Mansori, S. The Effects of Product Quality on Customer Satisfaction and Loyalty: Evidence from Malaysian Engineering Industry. Int. J. Ind. Mark. 2018, 3, 20. [Google Scholar] [CrossRef]

- Keiningham, T.; Ball, J.; Benoit, S.; Bruce, H.L.; Buoye, A.; Dzenkovska, J.; Nasr, L.; Ou, Y.C.; Zaki, M. The interplay of customer experience and commitment. J. Serv. Mark. 2017, 9, 1–72. [Google Scholar] [CrossRef]

- Kranzbühler, A.M.; Kleijnen, M.H.; Morgan, R.E.; Teerling, M. The multilevel nature of customer experience research: An integrative review and research agenda. Int. J. Manag. Rev. 2018, 20, 433–456. [Google Scholar] [CrossRef]

{kind=link}

| Author(s) | Variables | Findings |

|---|---|---|

| Yang et al. [54] | Perceived ease of use; perceived usefulness; technology readiness; technology amenities; visiting intentions | (1) Perceived ease of use and perceived usefulness are correlated with technology amenities but not with technology readiness. (2) Technology readiness affects intentions to visit smart hotels, but technology amenities do not. |

| Huang et al. [55] | Perceived ease of use; perceived usefulness; consumers’ experiences; behavioral intention | (1) Perceived ease of use and perceived usefulness have positive impacts on hotel consumers’ experiences of mobile apps, (2) Perceived usefulness and user experience influence hotel apps acceptance by customers. |

| Hasni et al. [56] | Perceived ease of use; perceived usefulness; behavioural intention | The findings reveal that the perceived usefulness and perceived ease of use of a social-media platform positively impact the behavioral intention |

| Singh and Srivastava [57] | Perceived usefulness; perceived ease of use; perceived trust; social capital. | TAM model validated though perceived usefulness and perceived ease of use as determinants of SM usage. |

| Lew et al. [58] | Technology self-efficacy; perceived critical mass, usefulness, ease of use, mobile self-efficacy, perceived enjoyment; behavioral intention | Mobile ease of use, usefulness, self-efficacy, and perceived enjoyment are positively correlated to behavioral intention |

| Bae and Han [59] | Cultural consonance; perceived ease of use; Perceived usefulness; attitude towards websites; intention to use the website | (1) An agreed-upon cultural model of trustworthiness of online hotel reviews exists among sample members. (2) Cultural consonance of trustworthiness and perceived ease of use and attitude towards websites were correlated. |

| Jung et al. [60] | Network externalities; trust; interactivity; ease of use; usefulness; intention to repurchase. | (1) Network externalities are essential to account for trust and interactivity; interactivity is an influential element to both ease of use and usefulness. |

| Demographic | Categories | Frequency | Percent |

|---|---|---|---|

| Gender | Male | 192 | 52.6 |

| Female | 173 | 47.4 | |

| Age Group | 21–30 Years | 165 | 45.2 |

| 31–40 Years | 111 | 30.4 | |

| 41–50 Years | 43 | 11.8 | |

| Above 50 Years | 46 | 12.6 | |

| Marital Status | Single | 187 | 51.23 |

| Married | 145 | 39.73 | |

| Separated/divorced | 33 | 9.04 | |

| Education | HSC/Diploma | 63 | 17.3 |

| Graduation | 159 | 43.6 | |

| Post-graduation | 87 | 23.8 | |

| Others | 56 | 15.3 | |

| Profession | Self-employed | 65 | 17.8 |

| Service Holder | 82 | 22.5 | |

| Student | 151 | 41.4 | |

| Others | 67 | 18.4 |

| Fintech Based Services [α = 0.940, CR = 0.947, AVE = 0.528] | FL |

|---|---|

| EOU1: It is easy to use Fintech services. | 0.693 |

| EOU2: I think the operation interface of Fintech is friendly and understandable | 0.651 |

| EOU3: It is easy to have device to use Fintech services | 0.747 |

| COM1: Fintech services reduce the expense of financial transactions and services. | 0.725 |

| COM2: Fintech services help to improve the services quality. | 0.666 |

| COM3: Fintech services save my time. | 0.809 |

| COM4: Fintech services increase flexibility. | 0.765 |

| PRS1: I feel Fintech services are a secure system. | 0.715 |

| PRS2: Providing information while using Fintech services feels secure to me. | 0.661 |

| PRS3: I am not worried about data/information security while using Fintech services. | 0.766 |

| PRV1: I can save my money using Fintech services. | 0.617 |

| PRV2: For the given price, I rate Fintech services as a good offer. | 0.707 |

| PRV3: I consider Fintech services to be a good purchase. | 0.773 |

| USE1: Fintech services have the ability to meet my need. | 0.774 |

| USE2: I can save a lot of time using Fintech services. | 0.752 |

| USE3: Fintech services increase my efficiency. | 0.778 |

| Customer experience [α = 0.891, CR = 0.916, AVE = 0.646] | |

| CEX1: Information attained from Fintech based service is useful. | 0.726 |

| CEX2: Information gained from Fintech based service brings interesting ideas to mind. | 0.872 |

| CEX3: I learned a lot from using Fintech based service. | 0.749 |

| CEX4: I feel optimistic using Fintech based service. | 0.825 |

| CEX5: I feel good using Fintech based service. | 0.777 |

| CEX6: I feel enthusiastic using Fintech based service. | 0.862 |

| Customer Attitude [α = 0.892, CR = 0.933, AVE = 0.822] | |

| CAT1: In my opinion using Fintech based service is a worthy idea. | 0.908 |

| CAT2: I believe using Fintech based service provides pleasant experience. | 0.919 |

| CAT 3: I am inquisitive towards Fintech based service. | 0.893 |

| Customer Loyalty Intentions [α = 0.867, CR = 0.919, AVE = 0.790] | |

| CLI1: I will share positive things regarding Fintech based service to other individuals. | 0.885 |

| CLI2: I will definitely recommend Fintech based service to other individuals. | 0.906 |

| CLI3: I will definitely continue using Fintech based service. | 0.875 |

| ATU | CE | CLI | FS | |

|---|---|---|---|---|

| ATU | ||||

| CE | 0.819 | |||

| CLI | 0.816 | 0.698 | ||

| FS | 0.757 | 0.681 | 0.740 |

| Hypothesis Path | Beta | t-Values | p-Values | Decision | VIF (<3.0) | |

|---|---|---|---|---|---|---|

| Direct Hypotheses | ||||||

| H1 | Fintech services → customer experience | 0.669 | 26.237 | 0.000 | Supported | 2.805 |

| H3 | Fintech services → customer attitude | 0.711 | 27.005 | 0.000 | Supported | 2.508 |

| H5 | Customer experience → customer loyalty intention | 0.134 | 2.632 | 0.004 | Supported | 2.207 |

| H6 | Customer attitude → customer loyalty intention | 0.392 | 5.466 | 0.000 | Supported | |

| Mediation Hypotheses | ||||||

| H2 | Fintech services→ customer experience → customer loyalty intention | 0.089 | 2.608 | 0.005 | Supported | |

| H4 | Fintech services→ customer attitude→ customer loyalty intention | 0.279 | 5.317 | 0.000 | Supported |

| Construct | R Square (R2) | Effects Size (f2) | Predictive Relevance (Q2) |

|---|---|---|---|

| Customer attitude | 0.506 (M) | 1.022 (L) | 0.412 |

| Customer experience | 0.447 (M) | 0.808 (L) | 0.259 |

| Customer-loyalty intension | 0.587 (M) | 0.111(S) | 0.459 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karim, R.A.; Sobhani, F.A.; Rabiul, M.K.; Lepee, N.J.; Kabir, M.R.; Chowdhury, M.A.M. Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude. Sustainability 2022, 14, 16481. https://doi.org/10.3390/su142416481

Karim RA, Sobhani FA, Rabiul MK, Lepee NJ, Kabir MR, Chowdhury MAM. Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude. Sustainability. 2022; 14(24):16481. https://doi.org/10.3390/su142416481

Chicago/Turabian StyleKarim, Rashed Al, Farid Ahammad Sobhani, Md Karim Rabiul, Nusrat Jahan Lepee, Mohammad Rokibul Kabir, and Mohammad Abdul Matin Chowdhury. 2022. "Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude" Sustainability 14, no. 24: 16481. https://doi.org/10.3390/su142416481

APA StyleKarim, R. A., Sobhani, F. A., Rabiul, M. K., Lepee, N. J., Kabir, M. R., & Chowdhury, M. A. M. (2022). Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude. Sustainability, 14(24), 16481. https://doi.org/10.3390/su142416481