_Li.png)

Partisan Conflict, National Security Policy Uncertainty and Tourism

, , , ,

, , , ,

Abstract

:1. Introduction

2. Literature Review

2.1. Impact of Partisan Conflict on Tourism

2.2. Impact of National Security Threats on Tourism

2.3. Relationship between Partisan Conflict and National Security Policy Uncertainty

2.4. Analysis of Different Tourism Performance

2.5. TVP-VAR Based Connectedness Measures

3. Methodology and Data

3.1. A Mixed-Method of DY Framework with TVP-VAR Model

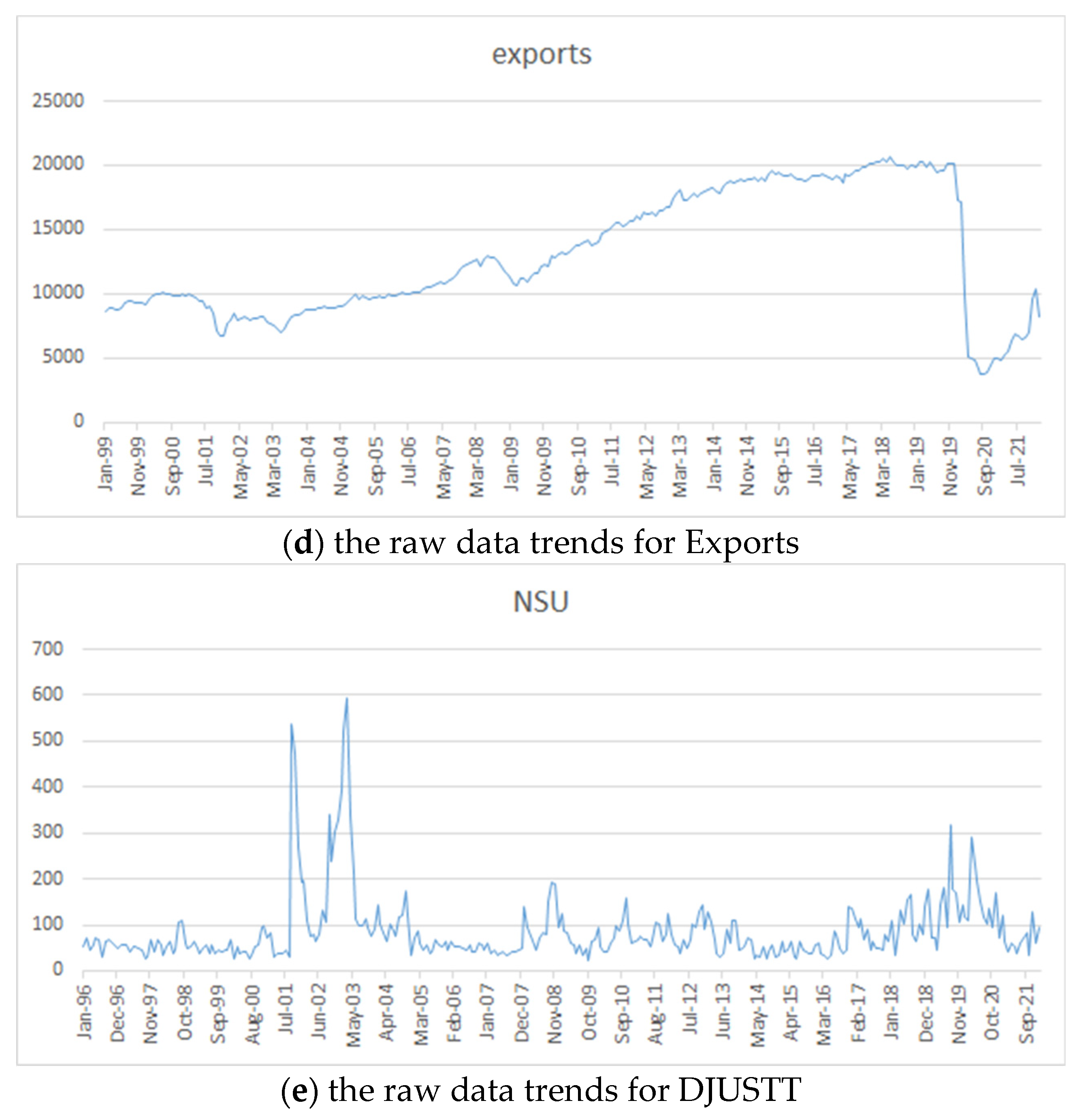

3.2. Data

4. Empirical Results

4.1. Static Analysis

4.1.1. Total Connectedness

4.1.2. Net Pairwise Connectedness

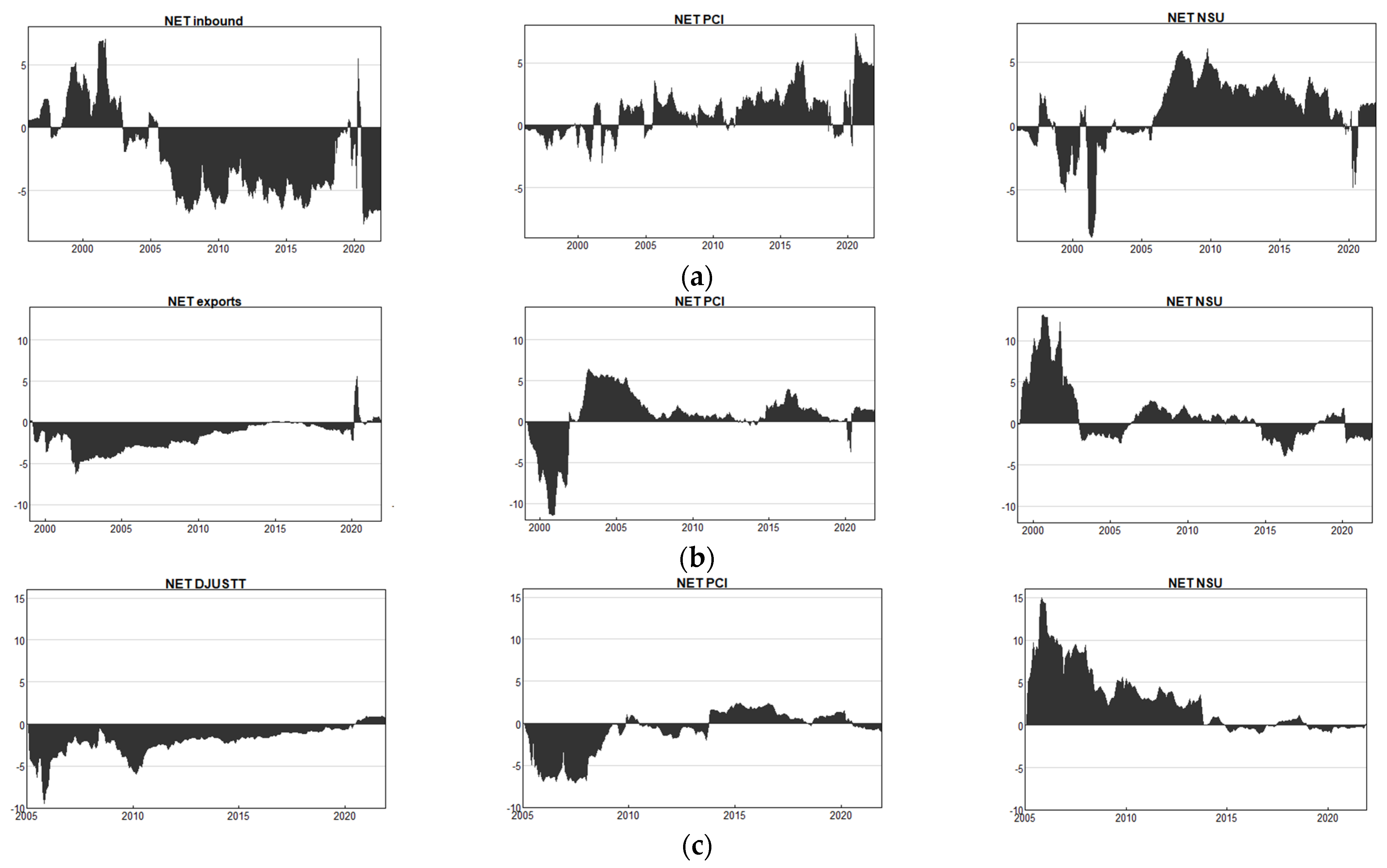

4.2. Dynamic Analysis

4.2.1. Total Spillovers

4.2.2. Net Spillovers and Pairwise Spillovers

4.3. Further Discussion

4.4. Robustness Check

5. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bunghez, C.L. The importance of tourism to a destination’s economy. J. East. Eur. Res. Bus. Econ. 2016, 2016, 143495. [Google Scholar] [CrossRef]

- Balli, F.; Shahzad, S.J.H.; Uddin, G.S. A tale of two shocks: What do we learn from the impacts of economic policy uncertainties on tourism? Tour. Manag. 2018, 68, 470–475. [Google Scholar] [CrossRef]

- Guenichi, H.; Khalfaoui, H.; Chouaibi, N. The impact of own-Country, USA and China’s economic policy uncertainty on stock market returns: Evidence from war, epidemic and financial crisis periods. Int. J. Sustain. Econ. 2021, 13, 126–149. [Google Scholar] [CrossRef]

- Huifu, N. Have Cross-Category Spillovers of Economic Policy Uncertainty Changed during the US–China Trade War? J. Asian Econ. 2021, 74, 101312. [Google Scholar]

- Farmaki, A.; Altinay, L.; Botterill, D.; Hilke, S. Politics and sustainable tourism: The case of Cyprus. Tour. Manag. 2015, 47, 178–190. [Google Scholar] [CrossRef]

- Akadiri, S.S.; Eluwole, K.K.; Akadiri, A.C.; Avci, T. Does causality between geopolitical risk, tourism and economic growth matter? Evidence from Turkey. J. Hosp. Tour. Manag. 2020, 43, 273–277. [Google Scholar] [CrossRef]

- Demiralay, S. Political uncertainty and the us tourism index returns. Ann. Tour. Res. 2020, 84, 102875. [Google Scholar] [CrossRef]

- Mehmood, S.; Ahmad, Z.; Khan, A.A. Dynamic relationships between tourist arrivals, immigrants, and crimes in the United States. Tour. Manag. 2016, 54, 383–392. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Das, D.; Dutta, A. Geopolitical risk, economic policy uncertainty and tourist arrivals: Evidence from a developing country. Tour. Manag. 2019, 75, 323–327. [Google Scholar] [CrossRef]

- Seabra, C.; Reis, P.; Abrantes, J.L. The influence of terrorism in tourism arrivals: A longitudinal approach in a Mediterranean country. Ann. Tour. Res. 2020, 80, 102811. [Google Scholar] [CrossRef]

- Rosselló, J.; Becken, S.; Santana-Gallego, M. The effects of natural disasters on international tourism: A global analysis. Tour. Manag. 2020, 79, 104080. [Google Scholar] [CrossRef] [PubMed]

- Cheng, C.H.J.; Hankins, W.B.; Chiu, C.-W.J. Does US partisan conflict matter for the Euro area? Econ. Lett. 2016, 138, 64–67. [Google Scholar] [CrossRef]

- Jeong, G.-H.; Quirk, P.J. Division at the water’s edge: The polarization of foreign policy. Am. Politics Res. 2019, 47, 58–87. [Google Scholar] [CrossRef]

- Carter, D.P.; May, P.J. Making sense of the US COVID-19 pandemic response: A policy regime perspective. Adm. Theory Prax. 2020, 42, 265–277. [Google Scholar]

- Lee, F.E. How party polarization affects governance. Annu. Rev. Political Sci. 2015, 18, 261–282. [Google Scholar] [CrossRef]

- Raunio, T.; Wagner, W. Towards parliamentarisation of foreign and security policy? West Eur. Politics 2017, 40, 1–19. [Google Scholar] [CrossRef]

- Apergis, E.; Apergis, N. Can the COVID-19 pandemic and oil prices drive the US Partisan Conflict Index. Energy Res. Lett. 2020, 1, 13144. [Google Scholar] [CrossRef]

- Ma, T.; Hong, T.; Zhang, H. Tourism spatial spillover effects and urban economic growth. J. Bus. Res. 2015, 68, 74–80. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, H.; Gao, W.; Yang, C. Spillover effects from news to travel and leisure stocks during the COVID-19 pandemic: Evidence from the time and frequency domains. Tour. Econ. 2021, 13548166211058497. [Google Scholar] [CrossRef]

- Bassil, C. The effect of terrorism on tourism demand in the Middle East. Peace Econ. Peace Sci. Public Policy 2014, 20, 669–684. [Google Scholar] [CrossRef]

- Abdelsalam, O.; Aysan, A.F.; Cepni, O.; Disli, M. The spillover effects of the COVID-19 pandemic: Which subsectors of tourism have been affected more? Tour. Econ. 2021, 13548166211053670. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Gabauer, D. Refined measures of dynamic connectedness based on time-Varying parameter vector autoregressions. J. Risk Financ. Manag. 2020, 13, 84. [Google Scholar] [CrossRef] [Green Version]

- Koop, G.; Korobilis, D. A new index of financial conditions. Eur. Econ. Rev. 2014, 71, 101–116. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Macroeconomic Volatility and Stock Market Volatility, Worldwide; National Bureau of Economic Research: Cambridge, MA, USA, 2008. [Google Scholar]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yılmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econom. 2014, 182, 119–134. [Google Scholar] [CrossRef]

- Officials, E. Multilevel Partisan Conflict and Drug Violence in Mexico. In Inside Countries: Subnational Research in Comparative Politics; Cambridge University Press: Cambridge, UK, 2019; Volume 181. [Google Scholar]

- Rother, B.; Pierre, G.; Lombardo, D.; Herrala, R.; Toffano, P.; Roos, E.; Auclair, G.; Manasseh, K. The Economic Impact of Conflicts and the Refugee Crisis in the Middle East and North Africa; International Monetary Fund: Washington, DC, USA, 2016. [Google Scholar]

- Azzimonti, M. Partisan conflict and private investment. J. Monet. Econ. 2018, 93, 114–131. [Google Scholar] [CrossRef]

- Apergis, N.; Hayat, T.; Saeed, T. US partisan conflict uncertainty and oil prices. Energy Policy 2021, 150, 112118. [Google Scholar] [CrossRef]

- Balcilar, M.; Akadiri, S.S.; Gupta, R.; Miller, S.M. Partisan conflict and income inequality in the United States: A nonparametric causality-In-Quantiles approach. Soc. Indic. Res. 2019, 142, 65–82. [Google Scholar] [CrossRef]

- Iversen, T. Contested Economic Institutions: The Politics of Macroeconomics and Wage Bargaining in Advanced Democracies; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Milner, H.V.; Judkins, B. Partisanship, trade policy, and globalization: Is there a left–Right divide on trade policy? Int. Stud. Q. 2004, 48, 95–119. [Google Scholar] [CrossRef]

- Azzimonti, M. Partisan conflict, news, and investors’ expectations. J. Money Credit. Bank. 2021, 53, 971–1003. [Google Scholar] [CrossRef]

- Seetaram, N. Immigration and international inbound tourism: Empirical evidence from Australia. Tour. Manag. 2012, 33, 1535–1543. [Google Scholar] [CrossRef]

- Karabulut, G.; Bilgin, M.H.; Demir, E.; Doker, A.C. How pandemics affect tourism: International evidence. Ann. Tour. Res. 2020, 84, 102991. [Google Scholar] [CrossRef]

- Azzimonti, M.; Talbert, M. Polarized business cycles. J. Monet. Econ. 2014, 67, 47–61. [Google Scholar] [CrossRef]

- Harb, G.; Bassil, C. Terrorism and inbound tourism: Does immigration have a moderating effect? Tour. Econ. 2020, 26, 500–518. [Google Scholar] [CrossRef]

- Zheng, C.; Li, Z.; Wu, J. Tourism Firms’ Vulnerability to Risk: The Role of Organizational Slack in Performance and Failure. J. Travel Res. 2022, 61, 990–1005. [Google Scholar] [CrossRef]

- Pastor, L.; Veronesi, P. Uncertainty about government policy and stock prices. J. Financ. 2012, 67, 1219–1264. [Google Scholar] [CrossRef]

- Gupta, R.; Pierdzioch, C.; Selmi, R.; Wohar, M.E. Does partisan conflict predict a reduction in US stock market (realized) volatility? Evidence from a quantile-On-Quantile regression model. N. Am. J. Econ. Financ. 2018, 43, 87–96. [Google Scholar] [CrossRef]

- Cheng, C.H.J.; Chiu, C.-W.J.; Hankins, W.B.; Stone, A.-L. Partisan conflict, policy uncertainty and aggregate corporate cash holdings. J. Macroecon. 2018, 58, 78–90. [Google Scholar] [CrossRef]

- Huang, D.; Liyao, W. Partisan Conflict and Stock Price; Research Collection Lee Kong Chian School of Business: Singapore, 2018. [Google Scholar]

- Cai, Y.; Wu, Y. Time-Varied causality between US partisan conflict shock and crude oil return. Energy Econ. 2019, 84, 104512. [Google Scholar] [CrossRef]

- Jiang, Y.; Ren, Y.S.; Ma, C.Q.; Liu, J.L.; Sharp, B. Does the price of strategic commodities respond to US partisan conflict? Resour. Policy 2020, 66, 101617. [Google Scholar] [CrossRef]

- Mangold, P. National Security and International Relations (Routledge Revivals); Routledge: London, UK, 2013. [Google Scholar]

- Sayigh, Y. Confronting the 1990s: Security in the developing countries: Introduction. Adelphi Pap. 1990, 30, 3–7. [Google Scholar] [CrossRef]

- Jawabreh, O. Management of Tourism Crisis in the Middle East. In Public Sector Crisis Management; IntechOpen: London, UK, 2020. [Google Scholar]

- Chisadza, C.; Clance, M.; Gupta, R.; Wanke, P. Uncertainty and tourism in Africa. Tour. Econ. 2022, 28, 964–978. [Google Scholar] [CrossRef]

- Edo, A.; Ragot, L.; Rapoport, H.; Sardoschau, S.; Steinmayr, A. The Effects of Immigration in Developed Countries: Insights from Recent Economic Research; EconPol Policy Report; IFO Institute: Munich, Germany, 2018. [Google Scholar]

- Lee, C.C.; Olasehinde-Williams, G.; Akadiri, S.S. Geopolitical risk and tourism: Evidence from dynamic heterogeneous panel models. Int. J. Tour. Res. 2021, 23, 26–38. [Google Scholar] [CrossRef]

- Sass, E. The impact of eastern Ukrainian armed conflict on tourism in Ukraine. Geo J. Tour. Geosites 2020, 30, 880–888. [Google Scholar] [CrossRef]

- Cró, S.; Martins, A.M. Structural breaks in international tourism demand: Are they caused by crises or disasters? Tour. Manag. 2017, 63, 3–9. [Google Scholar] [CrossRef]

- Hall, C.M. Climate change and its impacts on coastal tourism: Regional assessments, gaps and issues. In Global Climate Change and Coastal Tourism: Recognizing Problems, Managing Solutions and Future Expectations; CABI Publisher: Wallingford, UK, 2018; pp. 27–48. [Google Scholar]

- Ryu, K.; Bordelon, B.M.; Pearlman, D.M. Destination-Image recovery process and visit intentions: Lessons learned from Hurricane Katrina. J. Hosp. Mark. Manag. 2013, 22, 183–203. [Google Scholar] [CrossRef]

- Perles-Ribes, J.F.; Ramón-Rodríguez, A.B.; Sevilla-Jiménez, M.; Moreno-Izquierdo, L. Unemployment effects of economic crises on hotel and residential tourism destinations: The case of Spain. Tour. Manag. 2016, 54, 356–368. [Google Scholar] [CrossRef]

- Neumayer, E.; Plümper, T. Spatial spill-Overs from terrorism on tourism: Western victims in Islamic destination countries. Public Choice 2016, 169, 195–206. [Google Scholar] [CrossRef]

- Fourie, J.; Rosselló-Nadal, J.; Santana-Gallego, M. Fatal attraction: How security threats hurt tourism. J. Travel Res. 2020, 59, 209–219. [Google Scholar] [CrossRef]

- Jin, X.C.; Qu, M.; Bao, J. Impact of crisis events on Chinese outbound tourist flow: A framework for post-Events growth. Tour. Manag. 2019, 74, 334–344. [Google Scholar] [CrossRef]

- Yang, Y.; Zhang, H.; Chen, X. Coronavirus pandemic and tourism: Dynamic stochastic general equilibrium modeling of infectious disease outbreak. Ann. Tour. Res. 2020, 83, 102913. [Google Scholar] [CrossRef]

- Sio-Chong, U.; So, Y.-C. The impacts of financial and non-Financial crises on tourism: Evidence from Macao and Hong Kong. Tour. Manag. Perspect. 2020, 33, 100628. [Google Scholar]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Mandel, D.R.; Irwin, D. Uncertainty, intelligence, and national security decisionmaking. Int. J. Intell. Count. 2021, 34, 558–582. [Google Scholar] [CrossRef]

- Trejo, G.; Ley, S. Federalism, drugs, and violence. Why intergovernmental partisan conflict stimulated inter-Cartel violence in Mexico. Política Y Gob. 2016, 23, 11–56. [Google Scholar]

- Kriner, D.L.; Shen, F.X. Conscription, inequality, and partisan support for war. J. Confl. Resolut. 2016, 60, 1419–1445. [Google Scholar] [CrossRef]

- Burbach, D.T. Partisan dimensions of confidence in the US military, 1973–2016. Armed Forces Soc. 2019, 45, 211–233. [Google Scholar] [CrossRef]

- Wadhia, S.S. Is immigration law national security law. Emory LJ 2016, 66, 669. [Google Scholar]

- Holman, M.R.; Merolla, J.L.; Zechmeister, E.J. Terrorist threat, male stereotypes, and candidate evaluations. Political Res. Q. 2016, 69, 134–147. [Google Scholar] [CrossRef]

- Ghalia, T.; Fidrmuc, J.; Samargandi, N.; Sohag, K. Institutional quality, political risk and tourism. Tour. Manag. Perspect. 2019, 32, 100576. [Google Scholar] [CrossRef]

- Lanouar, C.; Goaied, M. Tourism, terrorism and political violence in Tunisia: Evidence from Markov-Switching models. Tour. Manag. 2019, 70, 404–418. [Google Scholar] [CrossRef]

- Petit, S.; Seetaram, N. Measuring the effect of revealed cultural preferences on tourism exports. J. Travel Res. 2019, 58, 1262–1273. [Google Scholar] [CrossRef]

- Hailemariam, A.; Ivanovski, K. The effect of economic policy uncertainty on US tourism net exports. Tour. Econ. 2021, 13548166211025334. [Google Scholar] [CrossRef]

- Saha, S.; Yap, G. The moderation effects of political instability and terrorism on tourism development: A cross-Country panel analysis. J. Travel Res. 2014, 53, 509–521. [Google Scholar] [CrossRef]

- Zopiatis, A.; Savva, C.; Lambertides, N.; McAleer, M. Tourism stocks in times of crisis: An econometric investigation of unexpected nonmacroeconomic factors. J. Travel Res. 2019, 58, 459–479. [Google Scholar] [CrossRef]

- Bashir, H.A.; Kumar, D. Investor attention, uncertainty and travel & leisure stock returns amid the COVID-19 pandemic. Curr. Issues Tour. 2022, 25, 28–33. [Google Scholar]

- Chen, M.-H. The response of hotel performance to international tourism development and crisis events. Int. J. Hosp. Manag. 2011, 30, 200–212. [Google Scholar] [CrossRef]

- Demir, E.; Ersan, O. Economic policy uncertainty and cash holdings: Evidence from BRIC countries. Emerg. Mark. Rev. 2017, 33, 189–200. [Google Scholar] [CrossRef]

- Hadi, D.M.; Irani, F.; Gökmenoğlu, K.K. External determinants of the stock price performance of tourism, travel, and leisure firms: Evidence from the United States. Int. J. Hosp. Tour. Adm. 2020, 23, 679–695. [Google Scholar] [CrossRef]

- Lee, C.-C.; Chen, M.-P. Do country risks matter for tourism development? International evidence. J. Travel Res. 2021, 60, 1445–1468. [Google Scholar] [CrossRef]

- Lee, C.-C.; Chen, M.-P.; Peng, Y.-T. Tourism development and happiness: International evidence. Tour. Econ. 2021, 27, 1101–1136. [Google Scholar] [CrossRef]

- Yarovaya, L.; Brzeszczyński, J.; Lau, C.K.M. Intra-And inter-Regional return and volatility spillovers across emerging and developed markets: Evidence from stock indices and stock index futures. Int. Rev. Financ. Anal. 2016, 43, 96–114. [Google Scholar] [CrossRef]

- Wang, G.J.; Xie, C.; Jiang, Z.Q.; Stanley, H.E. Who are the net senders and recipients of volatility spillovers in China’s financial markets? Financ. Res. Lett. 2016, 18, 255–262. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Trans-Atlantic equity volatility connectedness: US and European financial institutions, 2004–2014. J. Financ. Econom. 2015, 14, 81–127. [Google Scholar]

- Dragouni, M.; Filis, G.; Gavriilidis, K.; Santamaria, D. Sentiment, mood and outbound tourism demand. Ann. Tour. Res. 2016, 60, 80–96. [Google Scholar] [CrossRef]

- Baruník, J.; Kočenda, E.; Vácha, L. Asymmetric connectedness on the US stock market: Bad and good volatility spillovers. J. Financ. Mark. 2016, 27, 55–78. [Google Scholar] [CrossRef]

- Gamba-Santamaría, S.; Gómez-González, J.E.; Melo-Velandia, L.F.; Hurtado-Guarín, J.L. Stock market volatility spillovers: Evidence for Latin America. Financ. Res. Lett. 2017, 20, 207–216. [Google Scholar] [CrossRef] [Green Version]

- Demirer, M.; Diebold, F.X.; Liu, L.; Yılmaz, K. Estimating global bank network connectedness. J. Appl. Econom. 2018, 33, 1–15. [Google Scholar] [CrossRef]

- Antonakakis, N.; Gabauer, D. Refined Measures of Dynamic Connectedness Based on TVP-VAR; Munich Personal RePEc Archive: Munich, Germany, 2017. [Google Scholar]

- Korobilis, D.; Yilmaz, K. Measuring Dynamic Connectedness with Large Bayesian VAR Models. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3099725 (accessed on 18 July 2022).

- Antonakakis, N.; Gabauer, D.; Gupta, R.; Plakandaras, V. Dynamic connectedness of uncertainty across developed economies: A time-Varying approach. Econ. Lett. 2018, 166, 63–75. [Google Scholar] [CrossRef]

- Gabauer, D.; Gupta, R. On the transmission mechanism of country-Specific and international economic uncertainty spillovers: Evidence from a TVP-VAR connectedness decomposition approach. Econ. Lett. 2018, 171, 63–71. [Google Scholar] [CrossRef]

- Zhang, Y.; Hamori, S. Do news sentiment and the economic uncertainty caused by public health events impact macroeconomic indicators? Evidence from a TVP-VAR decomposition approach. Q. Rev. Econ. Financ. 2021, 82, 145–162. [Google Scholar] [CrossRef]

- Balcilar, M.; Gabauer, D.; Umar, Z. Crude Oil futures contracts and commodity markets: New evidence from a TVP-VAR extended joint connectedness approach. Resour. Policy 2021, 73, 102219. [Google Scholar] [CrossRef]

- Azzimonti, M. Partisan Conflict. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2457406 (accessed on 18 July 2022).

- Lucas, R.E. Why doesn’t capital flow from rich to poor countries? Am. Econ. Rev. 1990, 80, 92–96. [Google Scholar]

- Bastiaens, I. The politics of foreign direct investment in authoritarian regimes. Int. Interact. 2016, 42, 140–171. [Google Scholar] [CrossRef]

- Owen, E. The political power of organized labor and the politics of foreign direct investment in developed democracies. Comp. Political Stud. 2015, 48, 1746–1780. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Mean | Max | Min | Std. Dev. | Kurt | Skew | ADF | PP |

|---|---|---|---|---|---|---|---|---|

| PCI | 4.687 | 5.603 | 4.081 | 0.326 | 2.745 | 0.149 | −4.553 a | −3.963 a |

| NSU | 4.247 | 6.386 | 3.255 | 0.591 | 4.092 | 0.942 | −7.376 a | −7.341 a |

| Inbound | 15.214 | 15.946 | 13.170 | 0.519 | 10.627 | −2.205 | −3.792 a | −3.911 a |

| Exports | −0.001 | 0.310 | −0.158 | 0.064 | 64.405 | −5.972 | −10.076 a | −10.102 a |

| DJUSTT | 0.010 | 0.318 | −0.237 | 0.093 | 5.189 | −0.328 | −13.571 a | −13.656 a |

| Panel A | Inbound | PCI | NSU | FROM |

|---|---|---|---|---|

| Inbound | 69.8 | 19.5 | 10.7 | 30.2 |

| PCI | 17.6 | 79.1 | 3.3 | 20.9 |

| NSU | 5.9 | 4.7 | 89.4 | 10.6 |

| TO | 23.5 | 24.2 | 14.0 | 61.8 |

| NET directional connectedness | −6.7 | 3.4 | 3.4 | 20.6 |

| Panel B | Exports | PCI | NSU | FROM |

| Exports | 84.7 | 5.8 | 9.5 | 15.3 |

| PCI | 4.8 | 91.1 | 4.1 | 8.9 |

| NSU | 5.6 | 5.2 | 89.3 | 10.7 |

| TO | 10.3 | 10.9 | 13.6 | 34.9 |

| NET directional connectedness | −4.9 | 2.0 | 2.9 | 11.6 |

| Panel C | DJUSTT | PCI | NSU | FROM |

| DJUSTT | 89.6 | 2.2 | 8.2 | 10.4 |

| PCI | 0.7 | 91.3 | 8.0 | 8.7 |

| NSU | 3.9 | 3.9 | 92.2 | 7.8 |

| TO | 4.6 | 6.1 | 16.2 | 26.9 |

| NET directional connectedness | −5.8 | −2.6 | 8.4 | 9.0 |

| Panel A | Inbound | PCI | NSP_EMV | FROM |

|---|---|---|---|---|

| Inbound | 62.9 | 25.6 | 11.5 | 37.1 |

| PCI | 9.1 | 88.6 | 2.4 | 11.4 |

| NSP_EMV | 2.9 | 9.7 | 87.3 | 12.7 |

| TO | 12.0 | 35.4 | 13.8 | 61.2 |

| NET directional connectedness | −25.1 | 23.9 | 1.2 | 20.4 |

| Panel B | Exports | PCI | NSP_EMV | FROM |

| Exports | 78.9 | 4.0 | 17.2 | 21.1 |

| PCI | 1.8 | 95.3 | 2.9 | 4.7 |

| NSP_EMV | 9.1 | 10.2 | 80.7 | 19.3 |

| TO | 10.9 | 14.2 | 20.0 | 45.1 |

| NET directional connectedness | −10.2 | 9.5 | 0.7 | 15.0 |

| Panel C | DJUSTT | PCI | NSP_EMV | FROM |

| DJUSTT | 84.4 | 3.0 | 12.7 | 15.6 |

| PCI | 0.2 | 98.5 | 1.3 | 1.5 |

| NSP_EMV | 7.3 | 4.8 | 87.8 | 1.2 |

| TO | 7.6 | 7.8 | 14.0 | 29.3 |

| NET directional connectedness | −8.1 | 6.3 | 1.8 | 9.8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, R.; Zhang, H.; Fan, Q.; Gao, W.; Luo, X.; Yang, S. Partisan Conflict, National Security Policy Uncertainty and Tourism. Sustainability 2022, 14, 10858. https://doi.org/10.3390/su141710858

Zhang R, Zhang H, Fan Q, Gao W, Luo X, Yang S. Partisan Conflict, National Security Policy Uncertainty and Tourism. Sustainability. 2022; 14(17):10858. https://doi.org/10.3390/su141710858

Chicago/Turabian StyleZhang, Rufei, Haizhen Zhang, Qingzhu Fan, Wang Gao, Xue Luo, and Shixiong Yang. 2022. "Partisan Conflict, National Security Policy Uncertainty and Tourism" Sustainability 14, no. 17: 10858. https://doi.org/10.3390/su141710858

APA StyleZhang, R., Zhang, H., Fan, Q., Gao, W., Luo, X., & Yang, S. (2022). Partisan Conflict, National Security Policy Uncertainty and Tourism. Sustainability, 14(17), 10858. https://doi.org/10.3390/su141710858