Agricultural Grain Markets in the COVID-19 Crisis, Insights from a GVAR Model

Abstract

:1. Introduction

2. Recent Literature on Agricultural Markets and the COVID-19 Pandemic

3. Generalized Impulse Response Functions to COVID-19

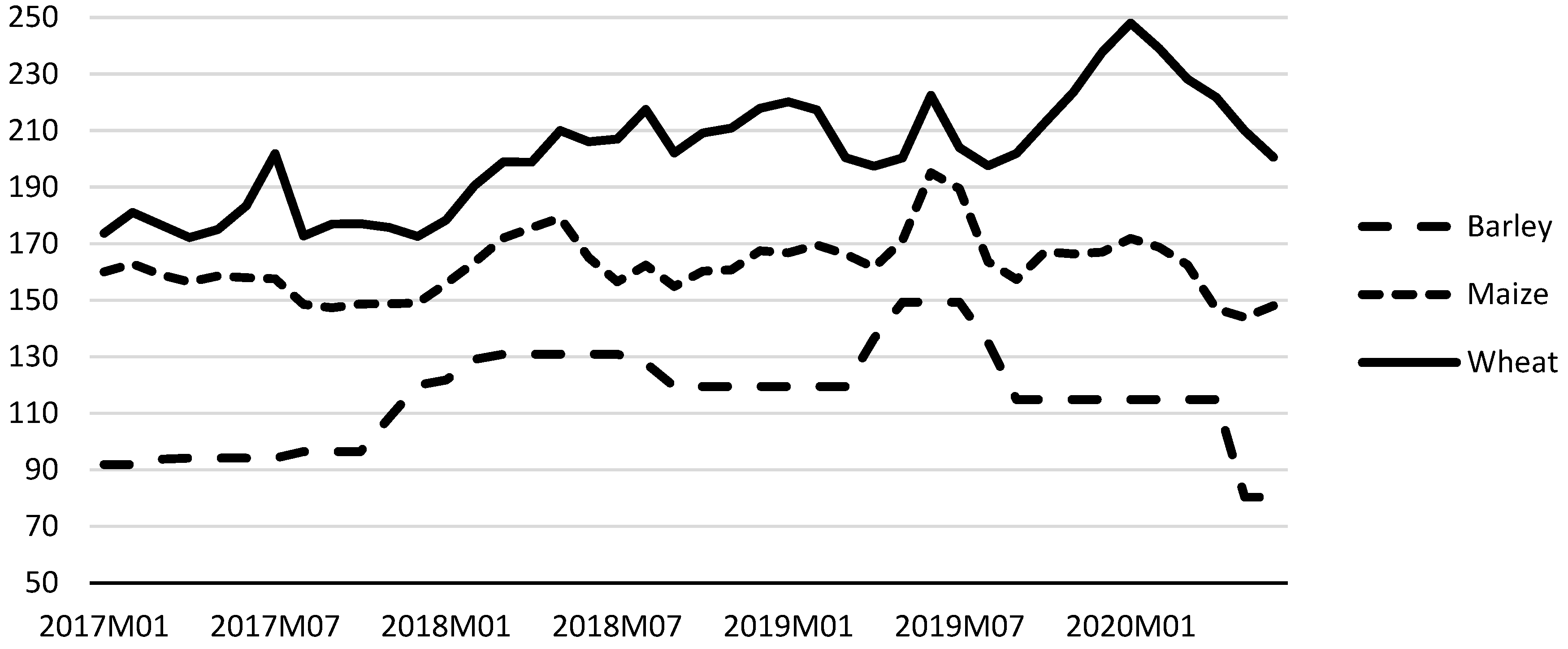

3.1. A Global VAR Model for the Feed Market

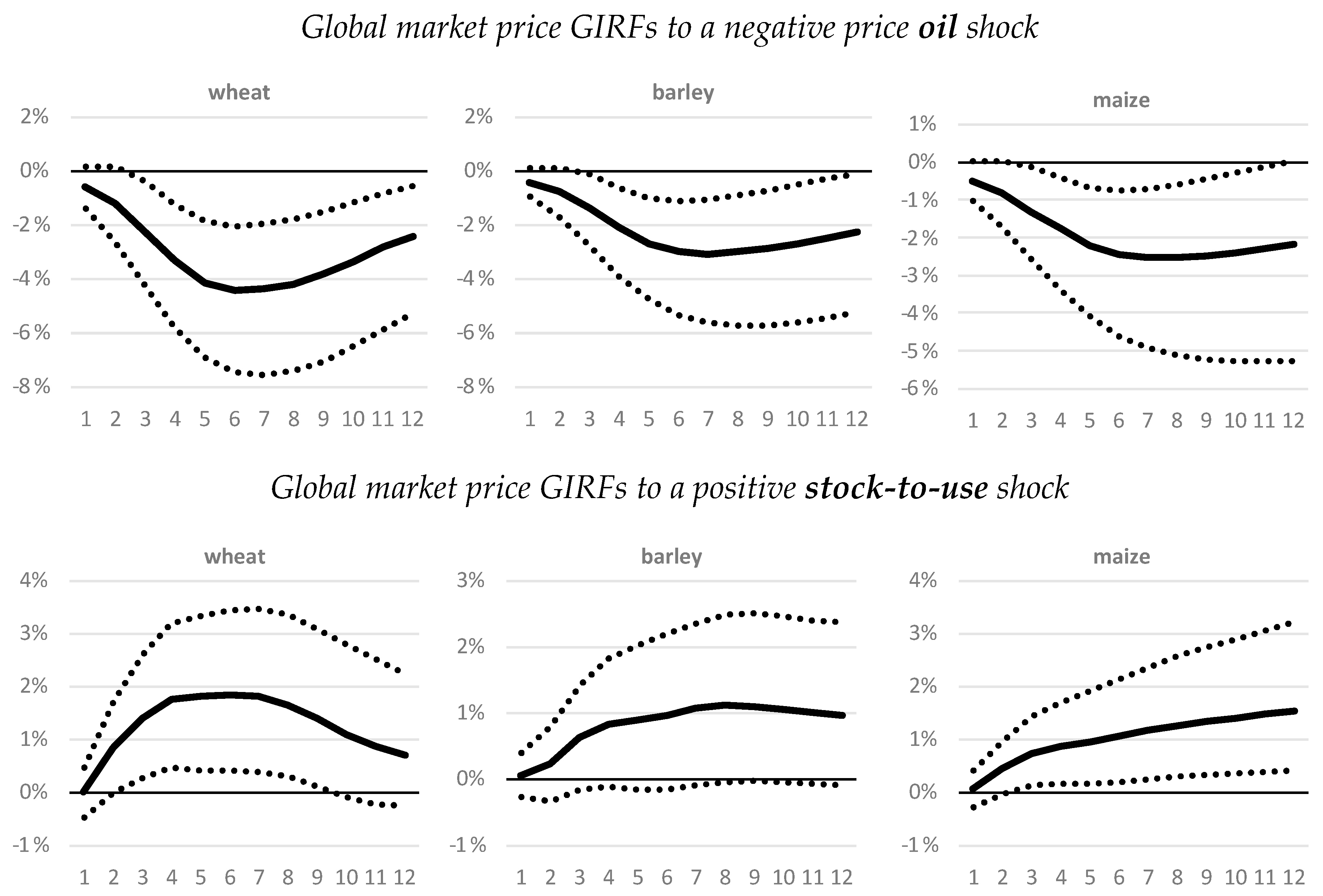

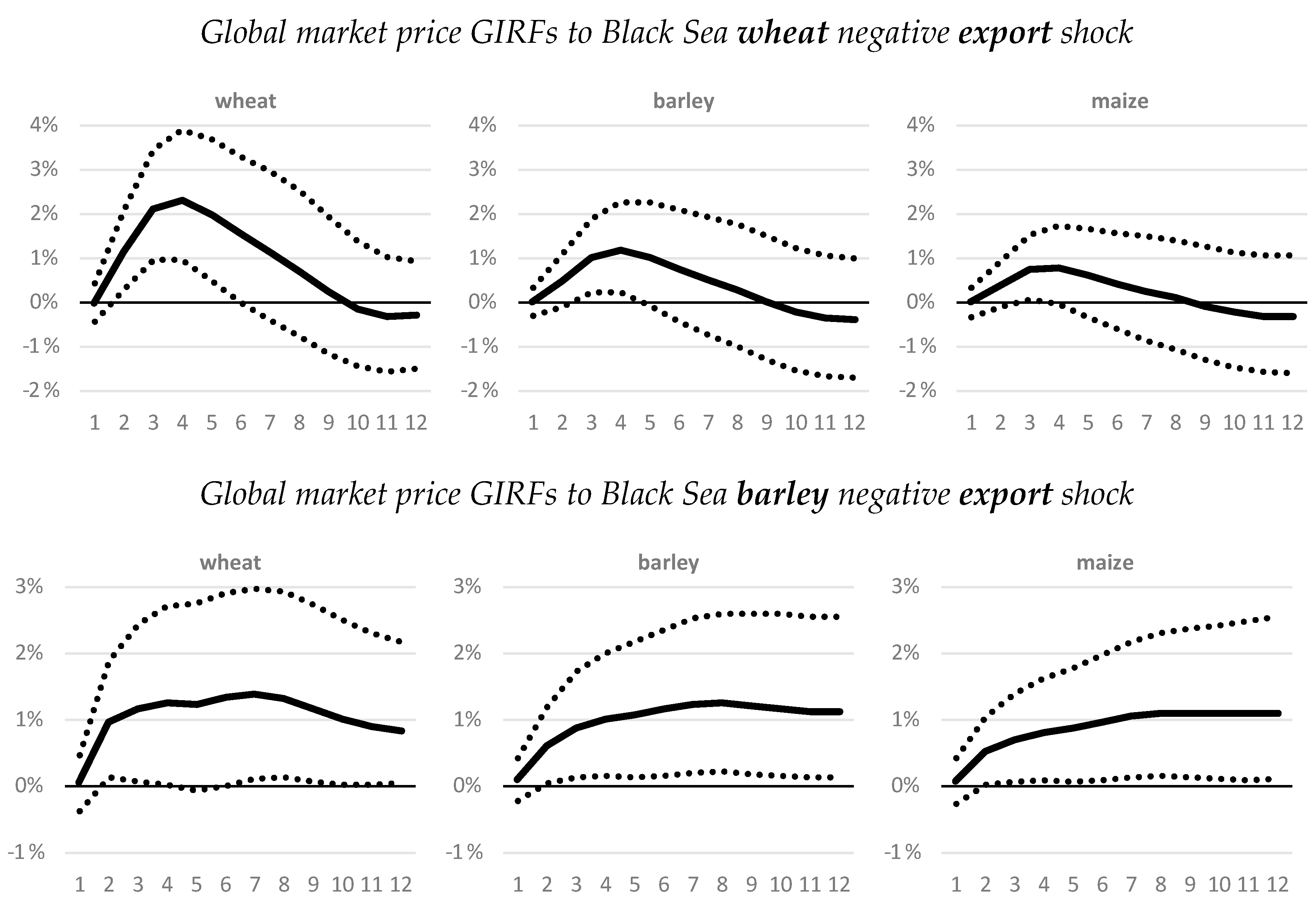

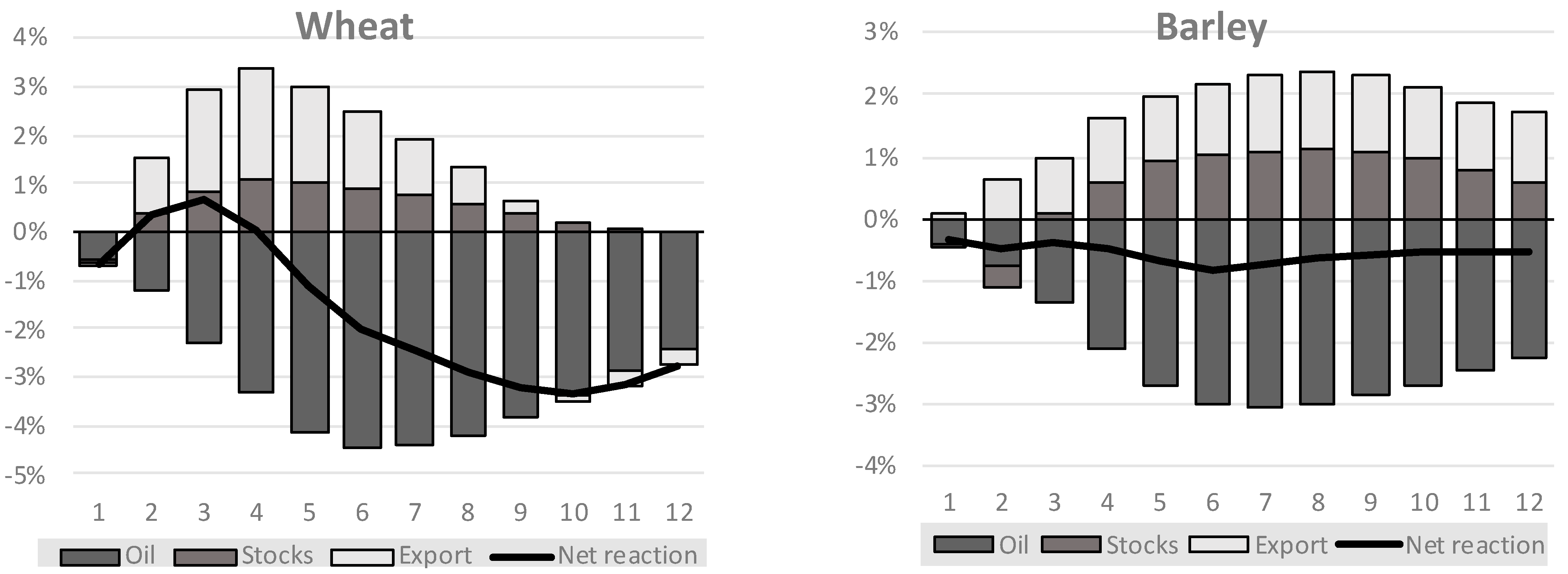

3.2. Results Discussion

- a one standard error negative global shock to oil price, which is equivalent to an oil price reduction of −4.4%;

- a one standard error negative shock to stock-to-use ratios, a shock affecting stocks in all countries, which is equivalent to an average reduction between −0.2% to −6.6% (−2.9% on average), depending on the commodity and country;

- a one standard error negative shock to exports in Black Sea countries, which is equivalent to −3.8% exports reduction for wheat and −4.2% for barley.

- Oil price shocks generate the strongest price responses (compared to stocks and exports);

- The oil shock takes more time to fully affect prices than the stock-to-use ratio shocks;

- A one standard error reduction of exports has a stronger impact on prices than a similar shock to stocks;

- All things equal and in case they happen simultaneously, the price increasing effect of the reduction of stocks are compensated by the impact of lower oil prices, for up to 12 months;

- Maize prices exhibit a lower sensitivity than wheat prices, but the effect of a stock-to-use reduction does not dissipate over time (hysteresis).

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- IMF. International Monetary Fund. World Economic Outlook Update. In World Economic Outlook; IMF: Washington, DC, USA, 2020. [Google Scholar]

- Maliszewska, M.; Mattoo, A.; van der Mensbrugghe, M.D. The Potential Impact of COVID-19 on GDP and Trade. SSRN Electron. J. 2020, 3573211. [Google Scholar]

- Aday, S.; Aday, M.S. Impacts of COVID-19 on Food Supply Chain. Food Qual. Saf. 2020, 4, 167–180. [Google Scholar] [CrossRef]

- Chenarides, L.; Manfredo, M.; Richards, T.J. COVID-19 and Food Supply Chains. Appl. Econ. Perspect. Policy 2021, 43, 270–279. [Google Scholar] [CrossRef]

- Laborde, D.; Martin, W.; Swinnen, J.; Vos, R. COVID-19 and Risks to Global Food Security. Science 2020, 39, 500–502. [Google Scholar] [CrossRef] [PubMed]

- Barichello, R. The COVID-19 pandemic: Anticipating its effects on Canada’s agricultural trade. Can. J. Agric. Econ. 2020, 68, 219–224. [Google Scholar] [CrossRef]

- Deaton, B.J.; Deaton, B.J. Food security and Canada’s agricultural system challenged by COVID-19. Can. J. Agric. Econ. 2020, 68, 143–149. [Google Scholar] [CrossRef]

- World Bank. The Commodity Markets Outlook, April 2020 Edition; World Bank: Washington, DC, USA, 2020; Available online: https://www.worldbank.org/en/research/commodity-markets (accessed on 1 June 2020).

- Kerr, W.A. The COVID-19 pandemic and agriculture: Short- and long-run implications for international trade relations. Can. J. Agric. Econ. 2020, 68, 225–229. [Google Scholar] [CrossRef]

- Glauber, J.; Laborde, D.; Martin, W.; Vos, R. COVID-19: Trade Restrictions Are Worst Possible Response to Safeguard Food Security; IFPRI Blog post, March 27; International Food Policy Research Institute: Washington, DC, USA, 2022. [Google Scholar]

- Morton, J. On the susceptibility and vulnerability of agricultural value chains to COVID-19. World Dev. 2020, 136, 105132. [Google Scholar] [CrossRef]

- FAO. Migrant Workers and the COVID-19 Pandemic; FAO: Rome, Italy, 2020; Available online: https://www.fao.org/3/ca8559en/CA8559EN.pdf (accessed on 15 January 2020).

- Baffes, J.; Oymak, I.C. Food Commodity Prices: Prospects and Risks Post-Coronavirus, World Bank Blogs. June 2020. Available online: https://blogs.worldbank.org/opendata/food-commodity-prices-prospects-and-risks-post-coronavirus (accessed on 1 July 2020).

- Dees, S.; di Mauro, F.; Pesaran, M.H.; Smith, L.V. Exploring the international linkages of the euro area: A global VAR analysis. J. Appl. Econom. 2007, 22, 1–38. [Google Scholar] [CrossRef]

- Gutierrez, L.; Piras, F.; Roggero, P.P. A Global VectorAutoregression model for the analysis of the wheat export prices. Am. J. Agric. Econ. 2015, 97, 1494–1511. [Google Scholar] [CrossRef]

- Espitia, A.; Rocha, N.; Ruta, M. COVID-19 and Food Protectionism: The Impact of the Pandemic and Export Restrictions on World Food Markets; World Bank, Policy Research Working Paper 9253; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Laborde, D.; Martin, W.; Vos, R. Poverty and Food Insecurity could Grow Dramatically as COVID-19 Spreads; International Food Policy Research Institute: Washington, DC, USA, 2020. [Google Scholar]

- Torero Cullen, M. Coronavirus, Food Supply Chains under Strain: What to Do? Food and Agriculture Organization: Rome, Italy, 2020. [Google Scholar]

- WHO. Director-General’s Opening Remarks at the Media Briefing on COVID-19; WHO: Geneva, Switzerland, 2020.

- ITC. Global Map of COVID-19 Temporary Trade Measures; ITC: Washington, DC, USA, 2020. Available online: https://www.macmap.org/covid19 (accessed on 10 February 2020).

- FAO. Food and Agriculture Policy Decision Analysis (FAPDA): Policy Database; FAO: Rome, Italy, 2020; Available online: https://www.fao.org/in-action/fapda/fapda-home/en/ (accessed on 10 January 2020).

- Headey, D.; Fan, S. Reflections of the Global Food Crisis; IFPRI Monograph: Washington, DC, USA, 2010. [Google Scholar]

- Martin, W.; Anderson, K. Export Restrictions and Price Insulation during Commodity Price Booms. Am. J. Agric. Econ. 2012, 94, 422–427. [Google Scholar] [CrossRef]

- Giordani, P.; Rocha, N.; Ruta, M. Food prices and the multiplier effect of trade policy. J. Int. Econ. 2016, 101, 102–122. [Google Scholar] [CrossRef]

- USDA. Production, Supply, and Distribution (PSD) Database; USDA: Washington, DC, USA, 2020. Available online: https://apps.fas.usda.gov/psdonline/app/index.html#/app/downloads (accessed on 5 February 2020).

- Schmidhuber, J.; Pound, J.; Qiao, B. COVID-19: Channels of Transmission to Food and Agriculture; Food and Agriculture Organization: Rome, Italy, 2020. [Google Scholar]

- Pesaran, M.H.; Schuermann, T.; Weiner, S.M. Modeling regional interdependencies using a global error-correcting macroeconometric model. J. Bus. Econ. Stat. 2004, 22, 129–162. [Google Scholar] [CrossRef]

- Gutierrez, L. Impacts of El Niño-Southern Oscillation on the wheat market: A global dynamic analysis. PLoS ONE 2017, 12, e0179086. [Google Scholar] [CrossRef] [PubMed]

- Pierre, G.; Kaminski, J. Cross-country maize market linkages in Africa: Integration and price transmission across local and global mark. Agric. Econ. 2019, 50, 79–90. [Google Scholar] [CrossRef]

- Beckman, J.; Borchers, A.; Jones, C.A. Agriculture’s Supply and Demand for Energy and Energy Products; USDA-ERS: Kansas, MI, USA, 2013.

- Myers, R.J.; Johnson, S.; Helmar, M.; Harry, B.H. Long-run and Short-run Co-Movements in Energy Prices and the Prices of Agricultural Feedstocks for Biofuel. Am. J. Agric. Econ. 2014, 96, 991–1008. [Google Scholar] [CrossRef]

- Lundberg, C.; Skolrud, T.; Adrangi, B.; Chatrath, A. Oil Pass Through to Agricultural Commodities. Am. J. Agric. Econ. 2021, 103, 721–742. [Google Scholar] [CrossRef]

- Smith, L.V.; Galesi, A. GVAR Toolbox 2.0 (2014). Available online: https://sites.google.com/site/gvarmodelling/gvar-toolbox (accessed on 11 January 2020).

- IGC. World Grain Statistics; International Grains Council: London, UK, 2016. [Google Scholar]

- FAO. Food Policy Monitoring and Analysis (FPMA) Tool; FAO: Rome, Italy, 2020; Available online: https://fpma.apps.fao.org/giews/food-prices/tool/public/#/home (accessed on 15 January 2020).

- EU 2020. DG AGRI Crop Market Observatory. Available online: https://ec.europa.eu/info/food-farming-fisheries/farming/facts-and-figures/markets/overviews/market-observatories/crops_en (accessed on 1 February 2020).

- OECD. Consumer Price Index Database; OECD: Paris, France, 2020; Available online: https://stats.oecd.org/Index.aspx?DataSetCode=PRICES_CPI (accessed on 20 January 2020).

- IMF. International Monetary Fund database, International Financial Statistics; IMF: Washington, DC, USA, 2020; Available online: https://data.imf.org/ (accessed on 2 March 2020).

- UN. UN Comtrade Database; UN: New York, NY, USA, 2020; Available online: https://comtrade.un.org/data/ (accessed on 10 January 2020).

- Lütkepohl, H. New Introduction to Multiple Time Series; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Baumeister, C.; Kilian, L. Do oil prices increases cause higher food prices? Econ. Policy 2014, 29, 691–747. [Google Scholar] [CrossRef]

- Bobenrieth, E.; Wright, B.; Zeng, D. Stock-to-use ratios and prices as indicators of vulnerability to spikes in global cereal markets. Agric. Econ. 2013, 44, 43–52. [Google Scholar] [CrossRef]

- Hochman, G.; Rajagopal, D.; Timilsina, G.; Zilberman, D. Quantifying the causes of the global food commodity price crisis. Biomass Bioenergy 2014, 68, 106–114. [Google Scholar] [CrossRef]

- Tadesse, G.; Algieri, B.; Kalkuhl, M.; von Braun, J.J. Drivers and triggers of international food price spikes and volatility. Food Policy 2014, 47, 117–128. [Google Scholar] [CrossRef]

- IFPRI. Food Export Restrictions during the COVID-19 Crisis; IFPRI: Washington, DC, USA, 2020; Available online: https://public.tableau.com/profile/laborde6680#!/vizhome/ExportRestrictionsTracker/FoodExportRestrictionsTracker (accessed on 8 February 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Production | Consumption | Exports | Ending Stocks | |

|---|---|---|---|---|

| Wheat | ||||

| Avg. 2017–2019 | 749, 486 | 745, 841 | 181, 621 | 269, 166 |

| June 2020 | 773, 434 | 753, 185 | 187, 491 | 314, 840 |

| Percentage change | 3.20 | 0.98 | 3.23 | 16.97 |

| Maize | ||||

| Avg. 2017–2019 | 1, 068, 754 | 1, 093, 282 | 157, 952 | 269, 166 |

| June 2020 | 1, 188, 476 | 1, 163, 510 | 182, 888 | 337, 873 |

| Percentage change | 11.20 | 6.42 | 15.79 | 25.53 |

| Barley | ||||

| Avg. 2017–2019 | 144, 851 | 146, 507 | 27, 067 | 19, 256 |

| June 2020 | 155, 259 | 154, 114 | 25, 288 | 22, 920 |

| Percentage change | 7.19 | 5.19 | −6.57 | 19.03 |

| ARG | AUS | BRA | CAN | EU | RUK | USA | ||

|---|---|---|---|---|---|---|---|---|

| Domestic variables | Wheat Price | 1 | 1 | 1 | 1 | 1 | 1 | |

| Maize Price | 1 | 1 | 1 | 1 | 1 | |||

| Barley Price | 1 | 1 | 1 | 1 | 1 | |||

| CPI | 1 | 1 | 1 | 1 | 1 | 1 | ||

| Exchange Rate | 1 | 1 | 1 | 1 | 1 | |||

| Wheat stock-to-use | 1 | 1 | 1 | 1 | 1 | 1 | ||

| Maize stock-to-use | 1 | 1 | 1 | 1 | 1 | |||

| Barley stock-to-use | 1 | 1 | 1 | 1 | 1 | |||

| Wheat exports | 1 | 1 | 1 | 1 | 1 | 1 | ||

| Maize exports | 1 | 1 | 1 | 1 | 1 | |||

| Barley exports | 1 | 1 | 1 | 1 | 1 | |||

| Foreign variables | Wheat Price | 1 | 1 | 1 | 1 | 1 | 1 | |

| Maize Price | 1 | 1 | 1 | 1 | 1 | |||

| Barley Price | 1 | 1 | 1 | 1 | 1 | |||

| Global var. | Oil | 1 | 1 | 1 | 1 | 1 | 1 | 2 |

| Wheat | ARG | AUS | BRA | CAN | EU | RUK | USA |

|---|---|---|---|---|---|---|---|

| ARG | 0% | 8% | 6% | 7% | 7% | 7% | 8% |

| AUS | 25% | 0% | 24% | 29% | 27% | 29% | 30% |

| BRA | 1% | 1% | 0% | 1% | 1% | 1% | 1% |

| CAN | 19% | 23% | 18% | 0% | 20% | 22% | 22% |

| EU | 13% | 16% | 13% | 15% | 0% | 15% | 16% |

| RUK | 20% | 24% | 19% | 22% | 21% | 0% | 23% |

| USA | 22% | 27% | 20% | 25% | 23% | 25% | 0% |

| Maize | ARG | AUS | BRA | CAN | EU | RUK | USA |

| ARG | 0% | 19% | 24% | 19% | 20% | 20% | 36% |

| AUS | 0% | 0% | 0% | 0% | 0% | 0% | 0% |

| BRA | 27% | 22% | 0% | 22% | 23% | 23% | 42% |

| CAN | 3% | 2% | 3% | 0% | 3% | 3% | 5% |

| EU | 5% | 4% | 5% | 4% | 0% | 4% | 8% |

| RUK | 6% | 4% | 6% | 5% | 5% | 0% | 9% |

| USA | 60% | 49% | 62% | 50% | 50% | 51% | 0% |

| Barley | ARG | AUS | BRA | CAN | EU | RUK | USA |

| ARG | 0% | 18% | 10% | 11% | 12% | 12% | 10% |

| AUS | 47% | 0% | 42% | 48% | 51% | 51% | 43% |

| BRA | 0% | 0% | 0% | 0% | 0% | 0% | 0% |

| CAN | 13% | 20% | 11% | 0% | 14% | 14% | 12% |

| EU | 19% | 30% | 17% | 19% | 0% | 21% | 17% |

| RUK | 19% | 30% | 17% | 20% | 21% | 0% | 18% |

| USA | 2% | 3% | 2% | 2% | 2% | 2% | 0% |

| Model Settings | Contemporaneous Coefficients | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| p | q | Cointegrating Relations | Wheat Coeff. | S.E. | Maize Coeff. | S.E. | Barley Coeff. | S.E. | |

| ARGENTINA | 2 | 1 | 1 | 0.515 | 0.085 | 0.934 | 0.088 | ||

| AUSTRALIA | 3 | 2 | 2 | 1.123 | 0.164 | 0.517 | 0.156 | ||

| BRAZIL | 3 | 1 | 2 | 0.735 | 0.096 | ||||

| CANADA | 1 | 1 | 2 | 0.877 | 0.196 | −0.104 | 0.058 | 0.047 | 0.117 |

| EU | 1 | 1 | 4 | 0.708 | 0.105 | 0.450 | 0.149 | 0.633 | 0.120 |

| BLACKSEA | 2 | 2 | 2 | 0.456 | 0.092 | 0.577 | 0.104 | ||

| USA | 1 | 2 | 1 | 0.866 | 0.097 | 0.729 | 0.099 | −0.126 | 0.138 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gutierrez, L.; Pierre, G.; Sabbagh, M. Agricultural Grain Markets in the COVID-19 Crisis, Insights from a GVAR Model. Sustainability 2022, 14, 9855. https://doi.org/10.3390/su14169855

Gutierrez L, Pierre G, Sabbagh M. Agricultural Grain Markets in the COVID-19 Crisis, Insights from a GVAR Model. Sustainability. 2022; 14(16):9855. https://doi.org/10.3390/su14169855

Chicago/Turabian StyleGutierrez, Luciano, Guillaume Pierre, and Maria Sabbagh. 2022. "Agricultural Grain Markets in the COVID-19 Crisis, Insights from a GVAR Model" Sustainability 14, no. 16: 9855. https://doi.org/10.3390/su14169855

APA StyleGutierrez, L., Pierre, G., & Sabbagh, M. (2022). Agricultural Grain Markets in the COVID-19 Crisis, Insights from a GVAR Model. Sustainability, 14(16), 9855. https://doi.org/10.3390/su14169855