Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises

Abstract

:1. Introduction

2. Policy Background and Literature Review

2.1. Policy Background

2.2. Literature Review

3. Research Design

3.1. Hypotheses

3.1.1. Green Finance and Green Enterprises’ Technological Innovation

3.1.2. Green Finance and Green Enterprises’ Financial Performance

3.1.3. The Heterogeneous Effect of Digital Financial Development

3.1.4. The Heterogeneous Effect of Green Development

3.1.5. The Heterogeneous Effect of Marketization Level

3.2. Data

3.3. Model

4. Results and Discussions

4.1. Descriptive Statistics

4.2. The DID Regression Results

4.3. Robustness Test

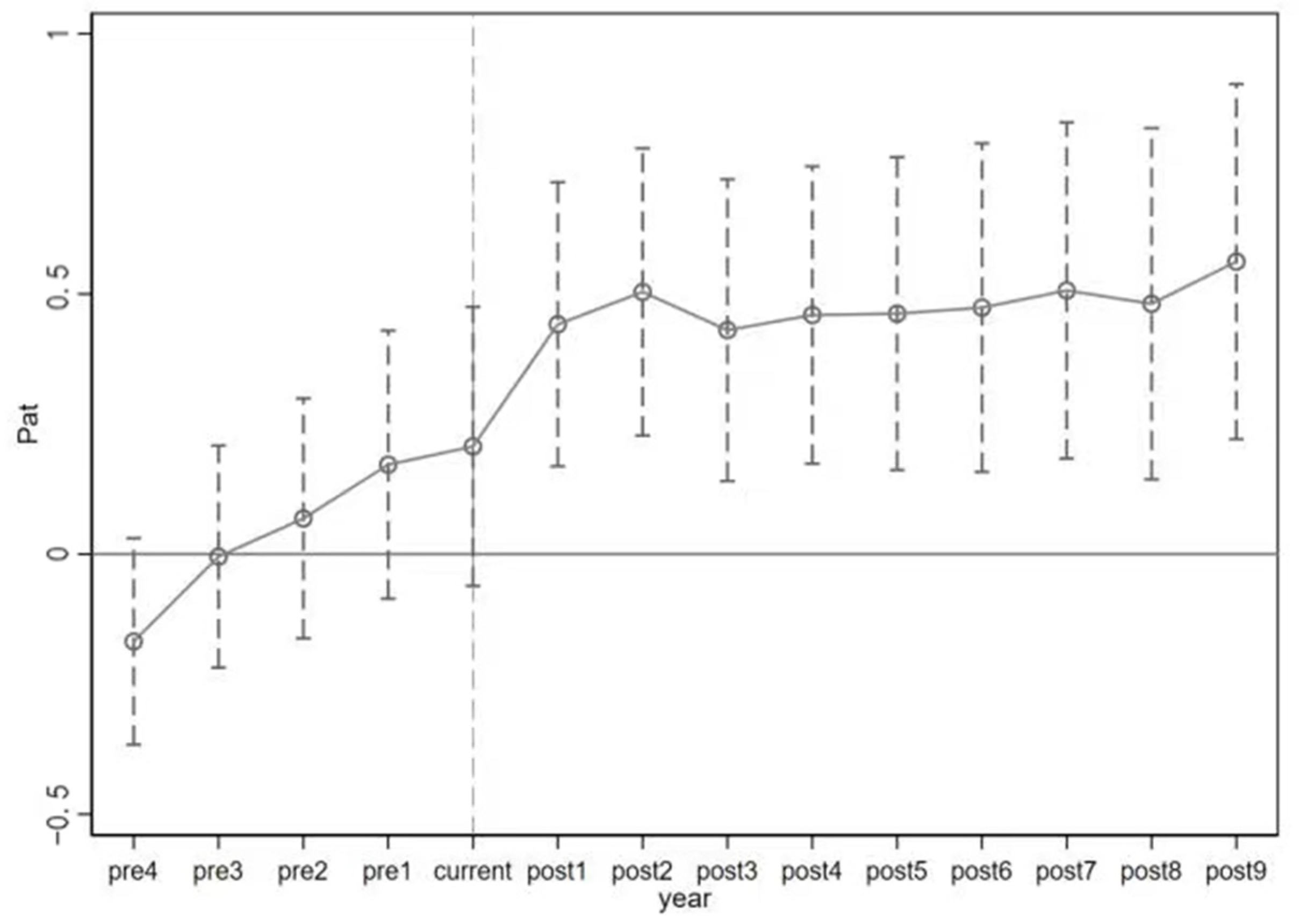

4.3.1. Parallel Trend Test

4.3.2. Change the Sample

4.3.3. Alternative Proxies for Technological Innovation

4.3.4. Alternative Proxies for Financial Performance

4.4. Heterogeneity Analysis

4.4.1. The Heterogeneity of Digital Financial Level

4.4.2. The Heterogeneity of Green Development Level

4.4.3. The Heterogeneity of Marketization Level

5. Conclusions

5.1. Theoretical Implications

- (1)

- The impact of the Green Credit Guidelines on the technological innovation of green enterprises has been verified using the DID model, which supports the incentive effect proposed by Hypothesis 1. Green credit can adjust the investment and financing activities of enterprises through its role in resource allocation, and this incentive effect can be achieved through two channels. On the one hand, financial institutions restrict the issuance of new loans to high-polluting industries through credit terms, and increase the loan interest rate to enterprises in these industries, thus effectively curbing new investment in high-polluting enterprises and forcing these enterprises to carry out green innovation. On the other hand, financial institutions increase credit support for green companies and green projects, such as clean and environmental protection, promote investment and financing activities in green and clean industries, and guide green industries to attract more production factors for green development.

- (2)

- The financial performance of green enterprises has been significantly improved after the implementation of the Green Credit Guidelines, which is supportive for Hypothesis 2. Green credit encourages enterprises to increase investment in research and development, significantly alleviates the lack of investment for technological innovation, and forms a positive incentive for innovation activities. Through innovative technologies, companies make up for the additional costs caused by financing constraints, improve production efficiency, enhance corporate competitiveness, and ultimately bring about improved operating conditions and good financial performance. Moreover, the green credit policy guides the flow of funds from polluting industries to green industries by implementing differentiated interest rates for enterprises with different industrial structures. The effect of this policy is to promote the technological innovation of green and environmentally friendly enterprises such as high-tech industries and knowledge service industries, and bring about good financial performance of green enterprises.

- (3)

- Heterogeneity analysis is carried out from three aspects: the level of digital finance, the level of green development, and the level of marketization. We found that after the implementation of the “Green Credit Guidelines” policy, green companies in areas with high levels of digital finance have significantly improved their technological innovation and financial performance, while green companies in areas with low levels of digital finance have not been significantly affected by green credit policies. These findings support Hypothesis 3(a) but contradict Hypothesis 3(b). Green enterprises in areas with high levels of green development have significantly improved their technological innovation and financial performance. Conversely, green enterprises in areas with low levels of green development were not significantly affected by the policy. These findings are in favor of Hypothesis 4(a), but not in favor of Hypothesis 4(b). Green credit policies can significantly promote the innovation and financial performance of green enterprises in regions with a high degree of marketization, but have no significant impact on green enterprises in regions with a low degree of marketization. This conclusion is supportive for Hypothesis 5(a), but disapproval for Hypothesis 5(b).

5.2. Policy Implications

- (1)

- The government should bear the responsibility of enhancing the environmental protection awareness of all sectors of society, so that the whole society can establish the concept of green development and raise the concept of green development to a strategic level. The government should actively guide financial institutions to integrate the concept of green development into their own culture, system, and operation process, continuously improve the green credit system, and develop green finance in the long term. The government should actively encourage enterprises to carry out green transformation, establish the concept of sustainable development, and infiltrate the concept of green development into the entire production process of enterprises. The government should guide consumers to pay attention to environmental and ecological issues, improve their awareness of environmental protection, build a correct consumption outlook, and integrate green consumption into their consumption habits.

- (2)

- The relevant mechanism of financial institutions needs to be improved. First, a complete and efficient approval mechanism needs to be improved. According to the environmental performance and risk assessment of the enterprise, the enterprise is classified, and different approval channels are established to improve the efficiency of credit approval. Second, the approval of corporate loan motives needs to be strengthened to ensure the innovation quality of green enterprises from the source, and to realize the rational allocation and utilization of resources. Third, dynamic management of credit funds is implemented, and operational procedures and evaluation indicators are improved. In addition, differentiated management should be formed, and individualized credit management should be implemented for different enterprises and different stages of the same enterprise to improve the degree of adaptation of policies. Fourth, innovation is realized in green financial products, systems, and services. In response to the problems of green enterprises’ asset-light operation and lack of collateral, we have innovated new financing guarantee models such as carbon asset pledge financing and income right pledge loans. Fifth, the use of credit funds is closely monitored, and the withdrawal mechanism of credit funds is improved. When an investment project is found to deviate from the initial goal, it should communicate with the debtor in a timely manner, and give a warning if necessary. If the warning is invalid, the loan can be terminated according to the withdrawal mechanism.

- (3)

- Enterprises should seize opportunities to achieve high-level development. Enterprises should strengthen green governance, improve managers’ enthusiasm for green decision-making through incentive mechanisms, and promote green transformation of enterprises. In addition, the management has a lot of room to operate on environmental protection-related expenses. The management and control mechanism of the enterprise should be strengthened to prevent the management from misappropriating green credit funds and making inefficient environmental protection investments, so that the green credit funds can be used reasonably and efficiently.

5.3. Ideas for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1.000 | ||||||||||||||

| 2 | 0.263 *** | 1.000 | |||||||||||||

| 3 | 0.210 *** | 0.535 *** | 1.000 | ||||||||||||

| 4 | 0.177 *** | 0.690 *** | 0.000 | 1.000 | |||||||||||

| 5 | 0.387 *** | 0.441 *** | 0.352 *** | 0.355 *** | 1.000 | ||||||||||

| 6 | 0.129 *** | 0.331 *** | 0.538 *** | 0.092 *** | 0.387 *** | 1.000 | |||||||||

| 7 | 0.097 *** | −0.096 *** | −0.157 *** | −0.005 | −0.009 | −0.067 *** | 1.000 | ||||||||

| 8 | −0.026 ** | −0.111 *** | −0.064 *** | −0.132 *** | −0.259 *** | −0.167 *** | −0.120 *** | 1.000 | |||||||

| 9 | −0.004 | 0.005 | −0.034 *** | 0.009 | −0.040 *** | 0.019 | −0.027 ** | −0.094 *** | 1.000 | ||||||

| 10 | 0.033 *** | −0.016 | −0.015 | −0.018 | 0.099 *** | −0.040 *** | 0.017 | 0.007 | −0.020 | 1.000 | |||||

| 11 | −0.071 *** | −0.102 *** | −0.050 *** | −0.099 *** | −0.319 *** | −0.045 *** | −0.007 | 0.118 *** | 0.359 *** | 0.036 *** | 1.000 | ||||

| 12 | −0.023 * | −0.010 | −0.083 *** | 0.042 *** | −0.003 | −0.066 *** | 0.073 *** | −0.020 | 0.013 | −0.014 | 0.025 * | 1.000 | |||

| 13 | −0.185 *** | −0.054 *** | −0.072 *** | −0.028 ** | 0.069 *** | −0.014 | 0.006 | −0.220 *** | 0.010 | 0.100 *** | −0.108 *** | −0.062 *** | 1.000 | ||

| 14 | −0.050 *** | 0.013 | −0.141 *** | 0.111 *** | 0.116 *** | −0.214 *** | 0.082 *** | −0.002 | 0.039 *** | 0.067 *** | −0.059 *** | 0.036 *** | 0.047 *** | 1.000 | |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | ||||||||||||||

| 2 | 0.0110 | 1 | |||||||||||||

| 3 | −0.028 ** | 0.535 *** | 1 | ||||||||||||

| 4 | 0.00300 | 0.690 *** | 0 | 1 | |||||||||||

| 5 | 0.061 *** | 0.441 *** | 0.352 *** | 0.355 *** | 1 | ||||||||||

| 6 | −0.090 *** | 0.331 *** | 0.538 *** | 0.092 *** | 0.387 *** | 1 | |||||||||

| 7 | −0.0120 | −0.096 *** | −0.157 *** | −0.00500 | −0.00900 | −0.067 *** | 1 | ||||||||

| 8 | 0.160 *** | −0.111 *** | −0.064 *** | −0.132 *** | −0.259 *** | −0.167 *** | −0.120 *** | 1 | |||||||

| 9 | −0.339 *** | 0.00500 | −0.034 *** | 0.00900 | −0.040 *** | 0.0190 | −0.027 ** | −0.094 *** | 1 | ||||||

| 10 | 0.090 *** | −0.0160 | −0.0150 | −0.0180 | 0.099 *** | −0.040 *** | 0.0170 | 0.00700 | −0.0200 | 1 | |||||

| 11 | 0.088 *** | −0.102 *** | −0.050 *** | −0.099 *** | −0.319 *** | −0.045 *** | −0.00700 | 0.118 *** | 0.359 *** | 0.036 *** | 1 | ||||

| 12 | 0.127 *** | −0.0100 | −0.083 *** | 0.042 *** | −0.00300 | −0.066 *** | 0.073 *** | −0.0200 | 0.0130 | −0.0140 | 0.025 * | 1 | |||

| 13 | −0.029 ** | −0.054 *** | −0.072 *** | −0.028 ** | 0.069 *** | −0.0140 | 0.00600 | −0.220 *** | 0.0100 | 0.100 *** | −0.108 *** | −0.062 *** | 1 | ||

| 14 | 0.100 *** | 0.0130 | −0.141 *** | 0.111 *** | 0.116 *** | −0.214 *** | 0.082 *** | −0.00200 | 0.039 *** | 0.067 *** | −0.059 *** | 0.036 *** | 0.047 *** | 1 | |

Appendix B

| Variables | VIF | 1/VIF | |

|---|---|---|---|

| Panel A: model (1) | |||

| 1 | 4.56 | 0.219326 | |

| 2 | 2.72 | 0.368207 | |

| 3 | 3.52 | 0.284166 | |

| 4 | 1.70 | 0.588064 | |

| 5 | 1.61 | 0.622769 | |

| 6 | 1.05 | 0.955054 | |

| 7 | 1.22 | 0.818591 | |

| 8 | 1.27 | 0.789663 | |

| 9 | 1.06 | 0.946906 | |

| 10 | 1.45 | 0.691883 | |

| 11 | 1.02 | 0.975746 | |

| 12 | 1.10 | 0.905238 | |

| 13 | 1.12 | 0.896668 | |

| Panel B: model (2) | |||

| 1 | 4.56 | 0.219317 | |

| 2 | 2.75 | 0.363422 | |

| 3 | 3.53 | 0.282945 | |

| 4 | 1.76 | 0.566969 | |

| 5 | 1.61 | 0.620853 | |

| 6 | 1.05 | 0.955222 | |

| 7 | 1.60 | 0.624740 | |

| 8 | 1.68 | 0.596258 | |

| 9 | 1.06 | 0.946333 | |

| 10 | 1.19 | 0.839444 | |

| 11 | 1.03 | 0.975275 | |

| 12 | 1.11 | 0.898220 | |

| 13 | 1.12 | 0.889633 | |

References

- Acemoglu, D.; Akcigit, U.; Hanley, D.; Kerr, W.R. Transition to clean technology. J. Political Econ. 2016, 124, 52–104. [Google Scholar] [CrossRef] [Green Version]

- Hong, M.; Li, Z.; Drakeford, B. Do the green credit guidelines affect corporate green technology innovation? Empirical research from China. Int. J. Environ. Res. Public Health 2021, 18, 1682. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Li, M. Credit policy and its heterogeneous effects on green innovations. J. Financ. Stab. 2022, 58, 100961. [Google Scholar] [CrossRef]

- Andersen, D.C. Do credit constraints favor dirty production? Theory and plant-level evidence. J. Environ. Econ. Manag. 2017, 84, 189–208. [Google Scholar] [CrossRef]

- Yu, C.H.; Wu, X.; Zhang, D.; Chen, S.; Zhao, J. Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy 2021, 153, 112255. [Google Scholar] [CrossRef]

- Shi, J.; Yu, C.; Wang, T. Does green financial policy affect debt-financing cost of heavy-polluting enterprises? An empirical evidence based on Chinese pilot zones for green finance reform and innovations. Technol. Forecast. Soc. Chang. 2022, 179, 121678. [Google Scholar] [CrossRef]

- Liu, X.; Wang, E.; Cai, D. Green credit policy, property rights and debt financing: Quasi-natural experimental evidence from China. Financ. Res. Lett. 2019, 29, 129–135. [Google Scholar] [CrossRef]

- Li, W.; Zheng, M.; Zhang, Y.; Cui, G. Green governance structure, ownership characteristics, and corporate financing constraints. J. Clean. Prod. 2020, 260, 121008. [Google Scholar] [CrossRef]

- Chai, S.L.; Zhang, K.; Wei, W.; Ma, W.; Abedin, M.Z. The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. J. Clean. Prod. 2022, 363, 132458. [Google Scholar] [CrossRef]

- Lv, C.; Bian, B.; Lee, C.C.; He, Z. Regional gap and the trend of green finance development in China. Energy Econ. 2021, 102, 105476. [Google Scholar] [CrossRef]

- Hu, G.; Wang, X.; Wang, Y. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Lee, C.C.; Lee, C.C. How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 2022, 107, 105863. [Google Scholar] [CrossRef]

- Ngo, Q.T.; Tran, H.A.; Tran, H.T.T. The impact of green finance and Covid-19 on economic development: Capital formation and educational expenditure of ASEAN economies. China Financ. Rev. Int. 2022, 12, 261–279. [Google Scholar] [CrossRef]

- Liu, C.; Xiong, M. Green finance reform and corporate innovation: Evidence from China. Financ. Res. Lett. 2022, 48, 102993. [Google Scholar] [CrossRef]

- Xu, X.; Li, J. Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. J. Clean. Prod. 2020, 264, 121574. [Google Scholar] [CrossRef]

- Wen, H.; Lee, C.C.; Zhou, F. Green credit policy, credit allocation efficiency, and upgrade of energy-intensive enterprises. Energy Econ. 2021, 94, 105099. [Google Scholar] [CrossRef]

- Zhang, K.; Li, Y.; Qi, Y.; Shao, S. Can green credit policy improve environmental quality? Evidence from China. J. Environ. Manag. 2021, 298, 113445. [Google Scholar] [CrossRef]

- Huang, Y.; Chen, C.; Lei, L.; Zhang, Y. Impacts of green finance on green innovation: A spatial and nonlinear perspective. J. Clean. Prod. 2022, 365, 132548. [Google Scholar] [CrossRef]

- Tian, C.; Li, X.; Xiao, L.; Zhu, B. Exploring the impact of green credit policy on green transformation of heavy polluting industries. J. Clean. Prod. 2022, 335, 130257. [Google Scholar] [CrossRef]

- Kang, H.; Jung, S.; Lee, H. The impact of Green Credit Policy on manufacturers’ efforts to reduce suppliers’ pollution. J. Clean. Prod. 2020, 248, 119271. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef] [PubMed]

- Nenavath, S. Impact of fintech and green finance on environmental quality protection in India: By applying the semi-parametric difference-in-differences (SDID). Renew. Energy 2022, 193, 913–919. [Google Scholar] [CrossRef]

- Wu, S.; Wu, L.; Zhao, X. Impact of the green credit policy on external financing, economic growth and energy consumption of the manufacturing industry. Chin. J. Popul. Resour. Environ. 2022, 20, 59–68. [Google Scholar] [CrossRef]

- Chang, K.; Zeng, Y.; Wang, H.; Wu, X. The effects of credit policy and financial constraints on tangible and research development investment: Firm-level evidence from China’s renewable energy industry. Energy Policy 2019, 130, 438–447. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, Y.; Wang, H.; Ouyang, X.; Xie, Y. Can green credit policy promote low-carbon technology innovation? J. Clean. Prod. 2022, 359, 132061. [Google Scholar] [CrossRef]

- Zhang, D.; Kong, Q. Credit policy, uncertainty, and firm R&D investment: A quasi-natural experiment based on the Green Credit Guidelines. Pac.-Basin Financ. J. 2022, 73, 101751. [Google Scholar]

- Yao, S.; Pan, Y.; Sensoy, A.; Uddin, G.S.; Cheng, F. Green credit policy and firm performance: What we learn from China. Energy Econ. 2021, 101, 105415. [Google Scholar] [CrossRef]

- Richardson, S. Over-investment of free cash flow. Rev. Account. Stud. 2006, 11, 159–189. [Google Scholar] [CrossRef]

- Atanassov, J. Arm’s Length Financing and Innovation: Evidence from Publicly Traded Firms. Manag. Sci. 2016, 62, 128–155. [Google Scholar] [CrossRef]

- Chiu, Y.B.; Lee, C.C. Effects of financial development on energy consumption: The role of country risks. Energy Econ. 2020, 90, 104833. [Google Scholar] [CrossRef]

- Demertzis, M.; Merler, S.; Wolff, G.B. Capital Markets Union and the Fintech Opportunity. J. Financ. Regul. 2018, 4, 157–165. [Google Scholar] [CrossRef]

- Chen, S.Q.; Zhang, H. Does digital finance promote manufacturing servitization: Micro evidence from China. Int. Rev. Econ. Financ. 2021, 76, 856–869. [Google Scholar] [CrossRef]

- Tang, X.; Ding, S.; Gao, X.; Zhao, T. Can digital finance help increase the value of strategic emerging enterprises? Sustain. Cities Soc. 2022, 81, 103829. [Google Scholar] [CrossRef]

- Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving Environmental Goals? A Preliminary Assessment of ‘Green Fintech’ and ‘Sustainable Digital Finance’. Eur. Co. Financ. Law Rev. 2022, 19, 128–174. [Google Scholar] [CrossRef]

- Zhang, M.; Liu, Y. Influence of digital finance and green technology innovation on China’s carbon emission efficiency: Empirical analysis based on spatial metrology. Sci. Total Environ. 2022, 838, 156463. [Google Scholar] [CrossRef]

- Kong, Q.X.; Li, R.R.; Peng, D.; Wong, Z. High-technology development zones and innovation in knowledge-intensive service firms: Evidence from Chinese a-share listed firms. Int. Rev. Financ. Anal. 2021, 78, 101883. [Google Scholar] [CrossRef]

- Tan, X.; Yan, Y.; Dong, Y. Peer effect in green credit induced green innovation: An empirical study from China’s Green Credit Guidelines. Resour. Policy 2022, 76, 102619. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, C.; Luo, S. Resource Allocation Effect of Green Credit Policy: Based on DID Model. Mathematics 2021, 9, 159. [Google Scholar] [CrossRef]

- Jacobson, L.S.; LaLonde, R.J.; Sullivan, D.G. Earnings losses of displaced workers. Am. Econ. Rev. 1993, 83, 685–709. [Google Scholar]

- Bertrand, M.; Duflo, E.; Mullainathan, S. How much should we trust differences-in-differences estimates? Q. J. Econ. 2004, 119, 249–275. [Google Scholar] [CrossRef] [Green Version]

- Wang, X.; Liu, S.; Tao, Z.; Cao, Q. The impact of industrial policy and its combinations on the innovation quality of wind power enterprises: A study from the perspective of financing modes. Renew. Energy 2022, 188, 945–956. [Google Scholar] [CrossRef]

- Cao, S.; Nie, L.; Sun, H.; Sun, W.; Taghizadeh-Hesary, F. Digital finance, green technological innovation and energy-environmental performance: Evidence from China’s regional economies. J. Clean. Prod. 2021, 327, 129458. [Google Scholar] [CrossRef]

- Feng, S.; Zhang, R.; Li, G. Environmental decentralization, digital finance and green technology innovation. Struct. Chang. Econ. Dyn. 2022, 61, 70–83. [Google Scholar] [CrossRef]

- Wu, Y.; Huang, S. The effects of digital finance and financial constraint on financial performance: Firm-level evidence from China’s new energy enterprises. Energy Econ. 2022, 112, 106158. [Google Scholar] [CrossRef]

- Li, R.; Chen, Y. The influence of a green credit policy on the transformation and upgrading of heavily polluting enterprises: A diversification perspective. Econ. Anal. Policy 2022, 74, 539–552. [Google Scholar] [CrossRef]

| Category | Variable Names | Variable Definitions |

|---|---|---|

| Explained variable | ) | The natural logarithm of (total number of patent applications for the year + 1) |

| ) | Total operating profit divided by operating income | |

| Explanatory variable | The multiplication term of policy and enterprise | |

| Post = 1 (after 2012), otherwise Post = 0 | ||

| Treat = 1 (green enterprise), otherwise Treat = 0 | ||

| Control variable | ) | Natural logarithm of total assets |

| ) | Natural logarithm of years since business started | |

| ) | The total operating income of the enterprise for the year divided by the average total assets | |

| ) | Current assets divided by current liabilities | |

| ) | Total liabilities divided by total assets | |

| ) | Natural logarithm of net cash flow from operating activities | |

| ) | Market capitalization divided by (total assets—net intangible assets—net goodwill) | |

| (Operating income in period t minus operating income in period t − 1) divided by operating income in period t − 1 | ||

| ) | Net fixed assets divided by total asset balance | |

| Shareholding ratio of the largest shareholder |

| Variable | Mean | Std. Dev. | Minimum | Maximum |

|---|---|---|---|---|

| 2.470 | 1.797 | 0.000 | 9.572 | |

| 0.077 | 0.220 | −6.282 | 1.738 | |

| 22.330 | 1.460 | 16.160 | 28.270 | |

| 2.699 | 0.512 | −2.485 | 3.718 | |

| 0.681 | 0.428 | 0.001 | 5.837 | |

| 2.033 | 2.133 | −5.132 | 48.470 | |

| 0.499 | 1.590 | −0.195 | 96.960 | |

| 0.053 | 0.209 | −11.060 | 0.558 | |

| 2.183 | 1.764 | 0.715 | 69.240 | |

| 0.193 | 0.542 | −0.957 | 16.340 | |

| 0.235 | 0.157 | 0.000 | 0.954 | |

| 34.580 | 14.950 | 3.620 | 95.100 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| 0.439 *** | 0.043 ** | 0.364 *** | 0.021 * | |

| (4.62) | (2.13) | (3.69) | (1.96) | |

| 0.240 *** | 0.064 *** | |||

| (3.48) | (3.69) | |||

| −0.240 | −0.049 ** | |||

| (−1.02) | (−2.28) | |||

| 0.079 | 0.039 ** | |||

| (0.70) | (2.01) | |||

| 0.006 | −0.002 | |||

| (0.54) | (−0.44) | |||

| 0.010 | −0.524 *** | |||

| (1.12) | (−3.54) | |||

| −0.081 | 0.019 | |||

| (−1.08) | (0.60) | |||

| −0.013 | 0.016 *** | |||

| (−0.64) | (4.81) | |||

| −0.049 * | 0.050 *** | |||

| (−1.66) | (6.32) | |||

| −0.191 | −0.063 | |||

| (−0.61) | (−0.94) | |||

| −0.005 | 0.001 *** | |||

| (−1.43) | (2.70) | |||

| Constant | 1.459 *** | 0.115 *** | −2.830 * | −1.028 *** |

| (26.62) | (20.34) | (−1.92) | (−3.20) | |

| Firm-FE | YES | YES | YES | YES |

| Year-FE | YES | YES | YES | YES |

| Observations | 6345 | 6296 | 5893 | 5886 |

| F | 27.99 | 5.821 | 27.95 | 13.08 |

| R-squared | 0.204 | 0.009 | 0.191 | 0.196 |

| Variables | (1) | (2) |

|---|---|---|

| 0.360 *** | 0.020 * | |

| (3.82) | (1.89) | |

| 0.220 *** | 0.064 *** | |

| (3.00) | (3.47) | |

| −0.099 | −0.067 *** | |

| (−0.44) | (−2.86) | |

| 0.030 | 0.036 * | |

| (0.27) | (1.86) | |

| 0.008 | −0.002 | |

| (0.91) | (−0.56) | |

| 0.019 ** | −0.501 *** | |

| (2.00) | (−3.17) | |

| −0.109 * | −0.001 | |

| (−1.82) | (−0.03) | |

| −0.029 | 0.014 *** | |

| (−1.37) | (3.59) | |

| −0.047 * | 0.046 *** | |

| (−1.70) | (5.24) | |

| −0.150 | −0.048 | |

| (−0.52) | (−0.66) | |

| −0.007 * | 0.001 ** | |

| (−1.92) | (1.98) | |

| Constant | −2.591 * | −0.986 *** |

| (−1.69) | (−2.85) | |

| Firm-FE | YES | YES |

| Year-FE | YES | YES |

| Observations | 5051 | 5045 |

| F | 28.39 | 11.51 |

| R-squared | 0.206 | 0.187 |

| Variables | (1) | (2) |

|---|---|---|

| 0.647 * | 0.011 * | |

| (1.94) | (1.91) | |

| −0.142 | 0.005 | |

| (−0.66) | (1.06) | |

| −0.679 | −0.015 | |

| (−0.94) | (−1.07) | |

| −1.418 *** | 0.052 *** | |

| (−4.87) | (3.95) | |

| −0.100 ** | 0.002 ** | |

| (−2.06) | (2.44) | |

| −1.028 | −0.035 *** | |

| (−1.03) | (−27.76) | |

| −1.756 ** | −0.541 *** | |

| (−2.09) | (−4.77) | |

| −0.143 *** | 0.009 *** | |

| (−2.59) | (3.74) | |

| −0.337 *** | 0.018 *** | |

| (−3.41) | (4.31) | |

| −0.457 | −0.059 ** | |

| (−0.33) | (−2.33) | |

| −0.008 | 0.001 *** | |

| (−0.82) | (2.86) | |

| Constant | 8.048 ** | −0.063 |

| (2.13) | (−0.61) | |

| Firm-FE | YES | YES |

| Year-FE | YES | YES |

| Observations | 4669 | 5893 |

| F | 13.55 | 174.0 |

| R-squared | 0.178 | 0.654 |

| Heterogeneity | High Degree of Digital Financial Index | Low Degree of Digital Financial Index | ||

|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (4) |

| 0.392 *** | 0.033 ** | 0.261 | −0.004 | |

| (3.63) | (2.57) | (1.21) | (−0.24) | |

| 0.224 *** | 0.074 *** | 0.274 ** | 0.033 *** | |

| (2.81) | (3.46) | (2.14) | (3.61) | |

| −0.100 | −0.041 * | −0.906 | −0.096 | |

| (−0.39) | (−1.77) | (−1.53) | (−1.54) | |

| 0.049 | 0.038 | 0.168 | 0.034 | |

| (0.32) | (1.56) | (1.23) | (1.23) | |

| 0.009 | −0.005 | −0.025 | 0.008 * | |

| (0.79) | (−1.11) | (−0.82) | (1.75) | |

| −0.081 | −0.610 *** | 0.011 | −0.287 *** | |

| (−0.52) | (−3.49) | (0.67) | (−3.19) | |

| −0.047 | 0.013 | −0.650 | 0.348 *** | |

| (−0.56) | (0.97) | (−1.53) | (3.73) | |

| −0.012 | 0.017 *** | −0.008 | 0.009 *** | |

| (−0.48) | (4.95) | (−0.25) | (2.74) | |

| −0.043 | 0.045 *** | −0.081 * | 0.058 *** | |

| (−1.10) | (5.64) | (−1.71) | (3.50) | |

| −0.116 | −0.130 * | −0.366 | 0.070 | |

| (−0.28) | (−1.77) | (−0.82) | (0.55) | |

| −0.008 * | 0.001 ** | 0.001 | 0.001 | |

| (−1.91) | (2.36) | (0.09) | (1.54) | |

| Constant | −2.538 | −1.210 *** | −2.541 | −0.431 ** |

| (−1.52) | (−2.99) | (−0.85) | (−2.21) | |

| Firm-FE | YES | YES | YES | YES |

| Year-FE | YES | YES | YES | YES |

| Observations | 4284 | 4281 | 1609 | 1605 |

| F | 11.43 | 11.56 | 76.02 | 10.97 |

| R-squared | 0.181 | 0.244 | 0.226 | 0.139 |

| Heterogeneity | High Degree of Green Development Index | Low Degree of Green Development Index | ||

|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (4) |

| 0.517 *** | 0.024 * | 0.129 | 0.008 | |

| (4.76) | (1.86) | (0.72) | (0.50) | |

| 0.207 ** | 0.076 *** | 0.306 *** | 0.039 *** | |

| (2.57) | (3.18) | (2.68) | (4.38) | |

| −0.042 | −0.051 ** | −0.829 | −0.023 | |

| (−0.16) | (−2.25) | (−1.51) | (−0.50) | |

| 0.074 | 0.055 ** | 0.091 | 0.008 | |

| (0.53) | (2.30) | (0.53) | (0.31) | |

| 0.005 | −0.002 | −0.006 | 0.002 | |

| (0.37) | (−0.59) | (−0.25) | (0.69) | |

| −0.199 | −0.542 *** | 0.007 | −0.442 *** | |

| (−1.41) | (−2.95) | (0.44) | (−6.34) | |

| −0.002 | 0.003 | −0.744 * | 0.392 *** | |

| (−0.03) | (0.22) | (−1.69) | (4.38) | |

| −0.022 | 0.019 *** | 0.009 | 0.009 *** | |

| (−0.93) | (3.87) | (0.29) | (2.88) | |

| −0.037 | 0.049 *** | −0.081 * | 0.051 *** | |

| (−0.84) | (5.61) | (−1.83) | (3.57) | |

| 0.258 | −0.142 | −0.706 | 0.013 | |

| (0.76) | (−1.64) | (−1.32) | (0.13) | |

| −0.008 ** | 0.001 ** | −0.002 | 0.001 * | |

| (−2.11) | (2.29) | (−0.24) | (1.71) | |

| Constant | −2.222 | −1.265 *** | −3.226 | −0.618 *** |

| (−1.27) | (−2.80) | (−1.31) | (−3.39) | |

| Firm-FE | YES | YES | YES | YES |

| Year-FE | YES | YES | YES | YES |

| Observations | 3934 | 3931 | 1959 | 1955 |

| F | 11.64 | 9.717 | 115.4 | 14.03 |

| R-squared | 0.190 | 0.236 | 0.210 | 0.149 |

| Heterogeneity | High Degree of Marketization | Low Degree of Marketization | ||

|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (4) |

| 0.403 *** | 0.034 *** | 0.122 | −0.034 | |

| (3.89) | (2.74) | (0.44) | (−1.48) | |

| 0.215 *** | 0.071 *** | 0.371 * | 0.012 | |

| (3.04) | (3.84) | (1.96) | (0.96) | |

| −0.164 | −0.046 ** | −0.939 | −0.051 | |

| (−0.66) | (−2.04) | (−1.18) | (−0.89) | |

| 0.042 | 0.042 * | 0.310 | 0.032 | |

| (0.33) | (1.87) | (1.25) | (1.44) | |

| 0.010 | −0.004 | −0.051 | 0.011 * | |

| (0.94) | (−1.05) | (−1.30) | (1.73) | |

| 0.007 | −0.602 *** | −0.163 | −0.236 *** | |

| (0.70) | (−3.75) | (−0.50) | (−3.39) | |

| −0.076 | 0.022 | −0.443 | 0.280 *** | |

| (−0.98) | (1.01) | (−0.92) | (3.99) | |

| −0.009 | 0.015 *** | −0.018 | 0.009 * | |

| (−0.41) | (4.92) | (−0.44) | (1.81) | |

| −0.047 | 0.047 *** | −0.065 | 0.055 *** | |

| (−1.40) | (5.84) | (−0.95) | (3.58) | |

| −0.154 | −0.053 | −0.255 | −0.156 *** | |

| (−0.44) | (−0.71) | (−0.42) | (−2.74) | |

| −0.006 | 0.001 *** | −0.001 | 0.000 | |

| (−1.43) | (2.75) | (−0.06) | (0.16) | |

| Constant | −2.372 | −1.151 *** | −4.487 | −0.017 |

| (−1.57) | (−3.37) | (−0.98) | (−0.05) | |

| Firm-FE | YES | YES | YES | YES |

| Year-FE | YES | YES | YES | YES |

| Observations | 4960 | 4953 | 933 | 933 |

| F | 32.17 | 10.60 | 4.133 | 17.00 |

| R-squared | 0.188 | 0.204 | 0.220 | 0.310 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Du, M.; Zhang, R.; Chai, S.; Li, Q.; Sun, R.; Chu, W. Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises. Sustainability 2022, 14, 9287. https://doi.org/10.3390/su14159287

Du M, Zhang R, Chai S, Li Q, Sun R, Chu W. Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises. Sustainability. 2022; 14(15):9287. https://doi.org/10.3390/su14159287

Chicago/Turabian StyleDu, Mo, Ruirui Zhang, Shanglei Chai, Qiang Li, Ruixuan Sun, and Wenjun Chu. 2022. "Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises" Sustainability 14, no. 15: 9287. https://doi.org/10.3390/su14159287

APA StyleDu, M., Zhang, R., Chai, S., Li, Q., Sun, R., & Chu, W. (2022). Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises. Sustainability, 14(15), 9287. https://doi.org/10.3390/su14159287