Business Students Expectations of Brazilian Corporate Governance: Insights for a Sustainable Path in an Emerging Business Environment

Abstract

:1. Introduction

2. Corporate Governance for Business Students and Sustainability

3. Contextualization of the Lava Jato Investigation and Hypothesis Development

Hypothesis Development

4. Methodology

4.1. Constructs and Variables

4.2. Proposed Structural Equation Modeling

4.3. Confirmatory Factor Analysis and Latent Variables

4.4. This Study’s Main Delimitation

5. Results

SEM

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| 1—Totally Disagree | 2—Disagree | 3—Neither Agree nor Disagree | 4—Agree | 5—Totally Agree |

|---|

- Self-declared Knowledge of Corporate Governance (SKCG)

- 4.1.

- I believe that I understand the concepts of governance.

- 4.2.

- I believe corporate governance is/will be important to companies’ businesses.

- 4.3.

- I believe understanding corporate governance concepts will help in my career.

- Board of Directors (BD)

- 5.1

- The Board of Directors should participate in strategic planning.

- 5.2

- The Board of Directors is responsible for ensuring the management system’s effectiveness.

- 5.3

- Members of the Board of Directors should have experience in relevant industries.

- 5.4

- The board of directors should have experience in finance or related areas.

- 5.5

- The board of directors should be independent in decision-making.

- 5.6

- The board of directors should understand the operational environment.

- 5.7

- The board of directors should understand organizational processes.

- 5.8

- Members of the Board of Directors should exchange critical information and comments.

- 5.9

- The board of directors should monitor the progress of the council resolutions.

- Risk Management (RM)

- 6.1

- Organizations should align their risk management plan with corporate strategy.

- 6.2

- Organizations should identify key risk indicators at the corporate level.

- 6.3

- Organizations should cascade (pass along) key risk indicators to relevant departments.

- 6.4

- Organizations should target risk management policy.

- 6.5

- Organizations should monitor the results of risk management.

- 6.6

- Organizations should specify the chief executive responsible for risk management.

- 6.7

- Organizations should integrate the risk management system throughout the organization.

- Internal Control (IC)

- 7.1

- Organizations should communicate clearly-specified segregation of duties and authorization.

- 7.2

- I understand the concept of internal control.

- 7.3

- Organizations should develop internal control manuals for all departments.

- 7.4

- Control activities should be realized in all departments.

- 7.5

- Organizations should emphasize risk-based control.

- Internal Audit (IA)

- 8.1

- Internal auditors should provide recommendations to improve internal control.

- 8.2

- Organizations should align the audit program with corporate strategy.

- 8.3

- Organizations should emphasize risk-based audits.

- 8.4

- Organizations should have adequate numbers of qualified internal auditors.

- 8.5

- It is important to have several diverse skills of the auditors.

- Human Resources Strategic Management (HRSM)

- 9.1

- Organizations should align human resource strategy with corporate strategy.

- 9.2

- Organizations should formulate human resources strategy to improve employee productivity.

- 9.3

- Organizations should formulate human resources strategies to improve employee satisfaction.

- 9.4

- Organizations should align their human resources plan with their strategic business plan.

- 9.5

- Organizations should align employees’ key performance indicators with departments and organizational key performance indicators.

- 9.6

- Organizations should implement performance-based compensation.

- 9.7

- Organizations should have career development plans for all hierarchical levels.

- 9.8

- Organizations should use modern tools for human resource management.

- 9.9

- Organizations should use tools to assess employee satisfaction.

- 9.10

- Organizations should have experience in strategic human resource management practices.

- 9.11

- Organizational departments should collaborate in human resources management.

- 9.12

- Organizational departments should collaborate in the design of training and development programs.

- Information Technology (IT)

- 10.1

- Organizations should align the main information technology plan with corporate strategy.

- 10.2

- Organizations should allocate investment to information technology based on strategic results.

- 10.3

- Organizations should provide an executive information system.

- 10.4

- Organizations should provide information technology to support risk management.

- 10.5

- Organizations should provide information technology to support internal control and audit.

- 10.6

- Organizations should provide information technology to support human resource management.

- 10.7

- Departments should collaborate in developing information technology applications.

- 10.8

- Departments should collaborate in the capacity of the information technology team.

- 10.9

- Organizations should collaborate in the capacity of the information technology team.

- 10.10

- Organizations should provide an adequate number of information technology training programs.

- Corporate Governance Expectations After Lava Jato (CGECW)

- 11.1

- I understand the extent of the moral and ethical crisis that the ‘Lava-Jato’ operation evidenced in the Brazilian private sector

- 11.2

- There will be a positive impact on corporate governance practices.

- 11.3

- There will be a reduction in the political appointment for members of the boards of directors.

- 11.4

- There will be a higher number of independent directors.

- 11.5

- Management systems are prepared for future cases of corruption.

- 11.6

- There will be more appointments of more qualified/experienced.

- 11.7

- There will be greater concern about reputational risk on the part of companies.

- 11.8

- There will be an expansion of the scope of risk control for other types of risk (e.g., legal, reputational, and political risk).

- 11.9

- Internal controls will be incremented to detect irregularities.

- 11.10

- There will be increased awareness that meeting improved governance practices to ensure long-term sustainability.

- 11.11

- There will be greater diligence in meeting compliance activities by companies.

- 11.12

- There will be more effective adoption of compliance instruments, not only to meet corporate governance manuals.

- 11.13

- Directors and officers will be more subject to the control of corporate governance instruments (e.g., audit system, controllership, rules, and statutes).

- 11.14

- Directors and officers shall be further repressed about anticompetitive, unfair and illegal conduct.

- 11.15

- Directors and officers will be less able to override the effects of internal controls under the illegal activities practiced.

- 11.16

- There will be increased transparency to mitigate other cases of corruption.

- 11.17

- There will be less manipulation of accounting to conceal corruption schemes.

- 11.18

- The internal audit will better identify and alert possible illegal activities.

- 11.19

- The external audit will better identify and alert possible illicit activities.

- 11.20

- There will be a greater possibility for company employees to report possible ethical deviations independently.

- 11.21

- Compliance mechanisms will be more robust and more transparent.

- 11.22

- Creditors and investors will demand better anti-corruption prevention mechanisms.

- 11.23

- The market will penalize companies that have governance practices that are not effective.

- 11.24

- There will be further training for employees to clarify doubts about specific misconduct from the point of view of corporate governance.

- 11.25

- Corporate governance is a more effective mechanism for self-regulation of enterprises than state regulation.

References

- Jensen, M.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs, and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Berle, A.; Means, G. The Modern Corporation and Private Property; Macmillian: New York, NY, USA, 1932. [Google Scholar]

- Jacoby, S. Corporate Governance and Society. Challenge 2005, 48, 69–87. [Google Scholar] [CrossRef]

- Jacobs, M. How Business Schools have failed business. Wall Str. J. 2009, 24, A13. [Google Scholar]

- Rezaee, Z.; Szendi, J.; Elmore, J.; Zhang, R. Corporate governance and ethics education: Viewpoints from accounting academicians and practitioners. Adv. Account. Educ. 2012, 13, 127–158. [Google Scholar]

- Rezaee, Z.; Zhang, R.; Saadullah, S. Corporate governance education: An analysis of existing syllabi. IUP J. Gov. Public Policy 2011, 6, 62–91. [Google Scholar]

- Zuckweiler, K.M.; Rosacker, K.M.; Hayes, S.K. Business students’ perceptions of corporate governance best practices. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 361–376. [Google Scholar] [CrossRef]

- Denis, D.K.; McConnell, J.J. International corporate governance. J. Financ. Quant. Anal. 2003, 38, 1–36. [Google Scholar] [CrossRef]

- Khongmalai, O.; Tang, J.C.S.; Siengthai, S. Empirical evidence of corporate governance in Thai state-owned enterprises. Corp. Gov. Int. J. Bus. Soc. 2010, 10, 617–634. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. A survey of corporate governance. J. Financ. 1997, 52, 737–783. [Google Scholar] [CrossRef]

- Tysiac, K. Corporate governance best practices 10 years after SOX. J. Account. 2012, 214, 24–26. [Google Scholar]

- Ricart, J.E.; Rey, C. Purpose in Corporate Governance: The Path towards a More Sustainable World. Sustainability 2022, 14, 4384. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Financ. 2021, 66, 101889. [Google Scholar] [CrossRef]

- Lagasio, V.; Cucari, N. Corporate governance and environmental social governance disclosure: A meta-analytical review. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 701–711. [Google Scholar] [CrossRef]

- Pedersen, L.H.; Fitzgibbons, S.; Pomorski, L. Responsible investing: The ESG-efficient frontier. J. Financ. Econ. 2021, 142, 572–597. [Google Scholar] [CrossRef]

- Arjoon, S. Corporate Governance: An Ethical Perspective. J. Bus. Ethics 2005, 61, 343–352. [Google Scholar] [CrossRef]

- Felo, A.J. Corporate Governance and Business Ethics. Studies in Economic Ethics and Philosophy. In Corporate Governance and Business Ethics; Brink, A., Ed.; Springer: Dordrecht, The Netherland, 2011; Volume 39. [Google Scholar] [CrossRef]

- Cadbury, A. Report of the Committee on the Financial Aspects of Corporate Governance; Gee & Co. Ltd.: London, UK, 1992.

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Naciti, V.; Cesaroni, F.; Pulejo, L. Corporate governance and sustainability: A review of the existing literature. J. Manag. Gov. 2022, 26, 55–74. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Huidrom, R.; Kose, M.A.; Ohsonrge, F. How Important is Spillover from Major Emerging Markets? Policy Research Working Paper 8093; World Bank Group: Washington, DC, USA, 2017. [Google Scholar]

- Al-Rahmi, A.M.; Al-Rahmi, W.M.; Alturki, U.; Aldraiweesh, A.; Almutairy, S.; Al-Adwan, A.S. Exploring the Factors Affecting Mobile Learning for Sustainability in Higher Education. Sustainability 2021, 13, 7893. [Google Scholar] [CrossRef]

- Baglama, B.; Evcimen, E.; Altinay, F.; Sharma, R.C.; Tlili, A.; Altinay, Z.; Dagli, G.; Jemni, M.; Shadiev, R.; Yucesoy, Y.; et al. Analysis of Digital Leadership in School Management and Accessibility of Animation-Designed Game-Based Learning for Sustainability of Education for Children with Special Needs. Sustainability 2022, 14, 7730. [Google Scholar] [CrossRef]

- Holdsworth, S.; Thomas, I. Competencies or capabilities in the Australian higher education landscape and its implications for the development and delivery of sustainability education. High. Educ. Res. Dev. 2021, 40, 1466–1481. [Google Scholar] [CrossRef]

- Boetto, H.; Bell, K. Environmental sustainability in social work education: An online initiative to encourage global citizenship. Int. Soc. Work 2015, 58, 448–462. [Google Scholar] [CrossRef] [Green Version]

- Hamid, S.; Ijab, M.T.; Sulaiman, H.; Md Anwar, R.; Norman, A.A. Social media for environmental sustainability awareness in higher education. Int. J. Sustain. High. Educ. 2017, 18, 474–491. [Google Scholar] [CrossRef] [Green Version]

- Jacobi, P.R.; de Toledo, R.F.; Grandisoli, E. Education, sustainability and social learning. Braz. J. Sci. Technol. 2016, 3, 3. [Google Scholar] [CrossRef]

- Friedland, J.; Jain, T. Reframing the Purpose of Business Education: Crowding-in a Culture of Moral Self-Awareness. J. Manag. Inq. 2022, 31, 15–29. [Google Scholar] [CrossRef]

- Becht, M.; Bolton, P.; Roell, A. Corporate Governance and Control. ECGI—Finance Working Paper n. 2002. Available online: https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=343461 (accessed on 14 July 2022).

- Silveira, A.D.M. Governança Corporativa no Brasil e no Mundo—Teoria e Prática; Elsevier: São Paulo, Brazil, 2010. [Google Scholar]

- Coffee, C.J. Gatekeepers: The role of the professions in corporate governance. In Clarendon Lectures in Management Studies; Oxford University Press: Oxford, UK, 2006; pp. 1–400. [Google Scholar]

- Department of the Treasury. Discussion Outline for Consideration by the Advisory Committee on the Auditing Profession (30 October); Federal Register: Washington, DC, USA, 2007; Volume 72.

- AACSB International. Presentation by John, J. Fernandes on Corporate governance: Essentials for the future manager. In Proceedings of the International Conference and Annual Meeting, San Francisco, CA, USA, 2005. [Google Scholar]

- Sherman, P.; Hansen, J. The new corporate social responsibility: A call for sustainability in business education. Int. J. Environ. Sustain. Dev. 2009, 9, 241–254. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. Corporate Social Responsibility. J. Bus. Ethics 2004, 54, 323–337. [Google Scholar] [CrossRef] [Green Version]

- Nicholson, C.Y.; DeMoss, M. Teaching Ethics and Social Responsibility: An Evaluation of Undergraduate Business Education at the Discipline Level. J. Educ. Bus. 2010, 84, 213–218. [Google Scholar] [CrossRef]

- Popescu, D.I.; Ceptureanu, S.I.; Alexandru, A.A.; Ceptureanu, E.G. Relationships between Knowledge Absorptive Capacity, Innovation Performance and Information Technology. Case study: The Romanian Creative Industries SMEs. Stud. Inform. Control 2019, 28, 463–476. [Google Scholar] [CrossRef]

- BBC News. Brazil Corruption Scandals: All You Need to Know. 2017. Available online: http://www.bbc.com/news/world-latin-america-35810578 (accessed on 17 July 2022).

- Folha de São Paulo. Entenda a Operação Lava Jato, da Polícia Federal. 2014. Available online: http://www1.folha.uol.com.br/poder/2014/11/1548049-entenda-a-operacao-lava-jato-da-policia-federal.shtml (accessed on 14 July 2022).

- El País. Cronologia da Lava Jato. 2017. Available online: https://brasil.elpais.com/brasil/2017/04/12/politica/1492018492_100094.html (accessed on 14 July 2022).

- Watts, J. Operation ‘Lava-Jato’: Is This the Biggest Corruption Scandal in History? 2017. Available online: https://www.theguardian.com/world/2017/jun/01/brazil-operation-’Lava-Jato’-is-this-the-biggest-corruption-scandal-in-history (accessed on 22 February 2018).

- Claessens, S.; Yurtoglu, B. Corporate Governance in Emerging Markets: A Survey. Emerg. Mark. Rev. 2013, 15, 1–33. [Google Scholar] [CrossRef]

- Rubino, M.; Vitolla, F. Corporate governance and the information system: How a framework for IT governance supports ERM. Corp. Gov. Int. J. Eff. Board Perform. 2014, 14, 320–338. [Google Scholar] [CrossRef]

- Raghupathi, W. Corporate governance of IT: A framework for development. Commun. ACM 2007, 50, 94–99. [Google Scholar] [CrossRef]

- Klamm, B.K.; Kobelsky, K.W.; Watson, M.W. Determinants of the Persistence of Internal Control Weaknesses. Account. Horiz. 2012, 26, 307–333. [Google Scholar] [CrossRef]

- Ege, M.S. Does Internal Audit Function Quality Deter Management Misconduct? Account. Rev. 2015, 90, 495–527. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R.; Canella, A.A., Jr. Corporate governance: Decades of dialogue and data. Acad. Manag. Rev. 2003, 28, 371–382. [Google Scholar] [CrossRef] [Green Version]

- Krishnan, J. Audit committee quality and internal control: An empirical analysis. Account. Rev. 2005, 80, 649–675. [Google Scholar] [CrossRef]

- Adams, R.; Hermalin, B.E.; Weisbach, M.S. The Role of Boards of Directors in Corporate Governance: A Conceptual Framework and Survey; Working Paper 14486; National Bureau of Economic Research: Cambridge, MA, USA, 2010. [Google Scholar]

- Carver, J. The promise of governance theory: Beyond codes and best practices. Corp. Gov. Int. Rev. 2007, 15, 1030–1037. [Google Scholar] [CrossRef]

- Knechel, W.R.; Willekens, M. The role of risk management and governance indetermining audit demand. J. Bus. Financ. Account. 2006, 33, 1344–1367. [Google Scholar] [CrossRef]

- Bhimani, A. Risk management, corporate governance and management accounting: Emerging interdependencies. Manag. Account. Res. 2009, 20, 2–5. [Google Scholar] [CrossRef]

- Vaughan, E.J.; Vaughan, T.M. Fundamentals of Risk and Insurance, 11th ed.; John Wiley & Sons, Inc.: Chichester, UK, 2014. [Google Scholar]

- Martin, G.; Gollan, P.J. Corporate governance and strategic human resources management in the UK financial services sector: The case of the RBS. Int. J. Hum. Resour. Manag. 2012, 23, 3295–3314. [Google Scholar] [CrossRef] [Green Version]

- Tenenhaus, M.; Amato, S.; Esposito Vinzi, V. A Global Goodness-of-Fit Index for PLS Structural Equation Modeling. In Proceedings of the XLII SIS Scientific Meeting, CLEUP, Padova, Italy, 9–11 June 2004; pp. 739e–742e. [Google Scholar]

- Dijkstra, T.K. Latent variables and indices: Herman world’s basic design and partial least squares. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer Handbooks of Computational Statistics Series; Springer: Berlin/Heidelberg, Germany; Dordrechtthe, The Netherlands; London, UK; New York, NY, USA, 2010; Volume II, pp. 23–46. [Google Scholar]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Thousand Oaks: Sage, CA, USA, 2017. [Google Scholar]

- Wold, H. Soft modeling: Systems under indirect observation: Causality, structure, prediction. In The Basic Design and Some Extensions; Joreskog, K.G., Wold, H., Eds.; North-Holland: Amsterdam, The Netherlands, 1982; Part II; pp. 1–54. [Google Scholar]

- Garver, N.S.; Mentzer, J.T. Logistics research methods: Employing structural equation modeling to test for construct validity. J. Bus. Logist. 1999, 20, 33–57. [Google Scholar]

- Vieira, K.M.; Milach, F.T.; Huppes, D. Equações estruturais aplicadas à satisfação dos alunos: Um estudo no curso de ciências contábeis daUniversidade Federal de Santa Maria. Rev. Contab. Finanças 2008, 19, 65–76. [Google Scholar] [CrossRef] [Green Version]

- Thompson, B. Reading and understanding more multivariate statistics. In Ten Commandments of Structural Equation Modeling; Grimm, L.G., Yarnold, P.R., Eds.; American Psychological Association: Washington, DC, USA, 2006; pp. 261–284. [Google Scholar]

- Santos, D.B.; Mendes-Da-Silva, W.; Flores, E.; Norvilitis, J. Predictors of credit card use and perceived financial well-being in female college students: A Brazil-United States comparative study. Int. J. Consum. Stud. 2016, 40, 133–142. [Google Scholar] [CrossRef]

- Anderson, J.C.; Gerbing, D.W. Structural equation modeling in practice: A review and recommended two-step approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Hu, L.T.; Bentler, P.M. Cutoff Criteria for Fit Indexes in Covariance Structure Analysis: Conventional Criteria Versus New Alternatives. Struct. Equ. Modeling Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M.; Diamantopoulos, A.; Straub, D.W.; Ketchen, D.J.; Hair, J.F.; Hult, G.T.M.; Calantone, R.J. Common Beliefs and Reality about Partial Least Squares: Comments on Rönkkö & Evermann (2013). Organ. Res. Methods 2014, 17, 182–209. [Google Scholar]

- Bentler, P.M.; Bonett, D.G. Significance tests and goodness of fit in the analysis of covariance structures. Psychol. Bull. 1980, 88, 588–606. [Google Scholar] [CrossRef]

- Lohmöller, J.-B. Latent Variable Path Modeling with Partial Least Squares; Physica: Heidelberg, Germany, 1989. [Google Scholar]

| Dates | Events |

|---|---|

| 17 March 2014 | The police arrested 17 people, including Paulo Roberto Costa, Director of Refining and Supply at Petrobras. |

| 14 November 2014 | Federal police launch a new phase of the investigation, involving searches of large suppliers such as Camargo Correa, OAS, Odebrecht, and seven other companies. |

| 6 March 2015 | The Federal Supreme Court authorizes the investigation of 12 senators and 22 representatives for corruption. |

| 19 June 2015 | The powerful businessman Marcelo Odebrecht is arrested. He is later sentenced to 19 years and 4 months in prison. |

| 3 August 2015 | José Dirceu, the Chief of Staff of ex-President Luiz Inácio Lula da Silva, is detained. The following year, he receives two prison sentences, one for 23 years and 3 months and the other for 11 years. |

| 25 November 2015 | Labor Party (PT) Senator Delcídio do Amaral is detained for obstructing the investigation. Amaral decides to confess and implicates President Dilma Rousseff and ex-President Lula in the scheme. |

| 10 March 2016 | Lula is indicted in São Paulo for money laundering and concealment of assets. |

| 22 March 2016 | Investigators find a system of “professional” corruption in Odebrecht based on the payment of bribes. |

| 12 May 2016 | Rousseff is impeached for manipulating public accounts and economic indicators in a separate case. Vice President Michel Temer takes office as Acting President. |

| 23 May 2016 | Romero Jucá has to leave the Ministry of Planning hours after Folha de São Paulo publishes a recording in which he suggests to contain the Lava Jato investigation. |

| 15 June 2016 | Temer is implicated in the plot by Sérgio Machado, the ex-President of Transpetro, a Petrobras subsidiary. |

| 31 August 2016 | Dilma is convicted by the Senate. Temer becomes president. |

| 26 September 2016 | The police arrest Antonio Palocci, ex-Finance Minister and Chief of Staff of Rousseff. |

| 19 October 2016 | Former Representative Eduardo Cunha, who was instrumental in Rousseff’s impeachment, is arrested for corruption. At the end of March 2017, he is sentenced to 15 years and 4 months in prison for corruption. |

| 19 January 2017 | Judge Teori Zavascki, in charge of the Lava Jato investigation, dies in a small plane crash. |

| 30 January 2017 | Eike Batista, who was the richest man in Brazil, is arrested as the Petrobras case unfolds. |

| 16 February 2017 | Prosecutors from 11 countries announce that they will investigate Odebrecht’s crimes in coordination with Brazil. |

| 14 March 2017 | Attorney General Rodrigo Janot calls for the opening of 83 investigations against politicians with legislative immunity based on the confessions of former Odebrecht executives. |

| 11 April 2017 | The Federal Supreme Court agrees to open investigations into eight ministers of President Temer’s administration. The case also includes 29 senators, at least 40 representatives, and 3 governors. |

| Major/Professional Experience | without | ≤1 Year | <1 ≤ 3 Years | <3 ≤ 5 Years | >5 Years | Total |

|---|---|---|---|---|---|---|

| # Accounting Students | 4 | 10 | 36 | 8 | 20 | 78 |

| % Accounting Students | 5% | 13% | 46% | 10% | 26% | 100% |

| # Actuarial Students | 6 | 10 | 6 | 2 | 10 | 34 |

| % Actuarial Students | 18% | 29% | 18% | 6% | 29% | 100% |

| # Business Students | 5 | 20 | 34 | 11 | 35 | 105 |

| % Business Students | 5% | 19% | 32% | 10% | 33% | 100% |

| # Economics Students | 3 | 24 | 29 | 31 | 24 | 111 |

| % Economics Students | 3% | 22% | 26% | 28% | 22% | 100% |

| # Total | 10 | 20 | 42 | 10 | 30 | 328 |

| % Total | 3% | 6% | 13% | 3% | 9% | 100% |

| Constructs | Definition | # of Indicators | Literature References |

|---|---|---|---|

| BD | Higher scores indicate greater expectations in terms of the role of the Board of Directors as a corporate governance tool | 9 | [7,9] |

| HRM | Higher scores indicate greater expectations about the role of strategic human resources management as a corporate governance tool | 12 | |

| IAs | Higher scores indicate greater expectations about the role of internal audits as a corporate governance tool | 5 | |

| ICs | Higher scores indicate greater expectations about the role of internal controls as a corporate governance tool | 5 | |

| IT | Higher scores indicate greater expectations about the role of information technology as a corporate governance tool | 10 | |

| RM | Higher scores indicate greater expectations about the role of risk management as a corporate governance tool | 7 | |

| SKCG | Higher scores indicate greater self-declared knowledge about corporate governance and its role in successful companies | 3 | |

| CGECW | Higher scores indicate greater expectations about Brazilian corporate governance after the Lava Jato investigation | 25 | Developed for this study |

| Index | Questions |

|---|---|

| BD | Board of Directors |

| Q5.1 | The Board of Directors should participate in strategic planning. |

| Q5.3 | Members of the Board of Directors should have experience in relevant industries. |

| Q5.8 | Members of the Board of Directors should exchange critical information and comments. |

| CGELJ | Corporate Governance Expectations After Lava Jato |

| Q11.6 | There will be more indications of more qualified/experienced advisors. |

| Q11.15 | Directors and officers will be less able to override the effects of internal controls regarding illegal practices. |

| Q11.18 | Internal audits will be better able to identify and warn of possible illegal practices. |

| HRM | Strategic Human Resources Management |

| Q9.1 | Organizations should align human resources with corporate strategy. |

| Q9.4 | Organizations should align their personnel with their strategic business plan. |

| Q9.5 | Organizations should align key employee performance indicators with departmental and organizational key performance indicators. |

| IA | Internal Audits |

| Q8.1 | Internal auditors should provide recommendations to improve internal controls. |

| Q8.3 | Organizations should emphasize risk-based audits. |

| Q8.4 | Organizations should have adequate numbers of qualified internal auditors. |

| IC | Internal Controls |

| Q7.1 | Organizations should communicate clearly-specified segregation of duties and authority. |

| Q7.4 | Control activities should be realized in all departments. |

| Q7.5 | Organizations should emphasize risk-based controls. |

| IT | Information Technology |

| Q10.4 | Organizations should provide information technology to support risk management. |

| Q10.5 | Organizations should provide information technology to support internal controls and audits. |

| Q10.7 | Departments should collaborate in developing information technology applications. |

| RM | Risk Management |

| Q6.1 | Organizations should align their risk management plan with corporate strategy. |

| Q6.2 | Organizations should identify key risk indicators at the corporate level. |

| Q6.3 | Organizations should pass along key risk indicators to relevant departments. |

| SKCG | Self-declared Knowledge of Corporate Governance |

| Q11.1 * | I understand the extent of the moral and ethical crisis that the Lava Jato investigation has revealed in the Brazilian private sector |

| Q4.2 | I believe corporate governance is important to business. |

| Q4.3 | I believe that understanding corporate governance concepts will help me in my career. |

| Latent Variables | AVE | CA | CR |

|---|---|---|---|

| BD | 0.687 | 0.707 | 0.728 |

| CGECW | 0.638 | 0.720 | 0.840 |

| HRM | 0.657 | 0.739 | 0.851 |

| IAs | 0.505 | 0.672 | 0.821 |

| ICs | 0.608 | 0.691 | 0.739 |

| IT | 0.611 | 0.758 | 0.859 |

| RM | 0.629 | 0.675 | 0.728 |

| SKCG | 0.540 | 0.710 | 0.798 |

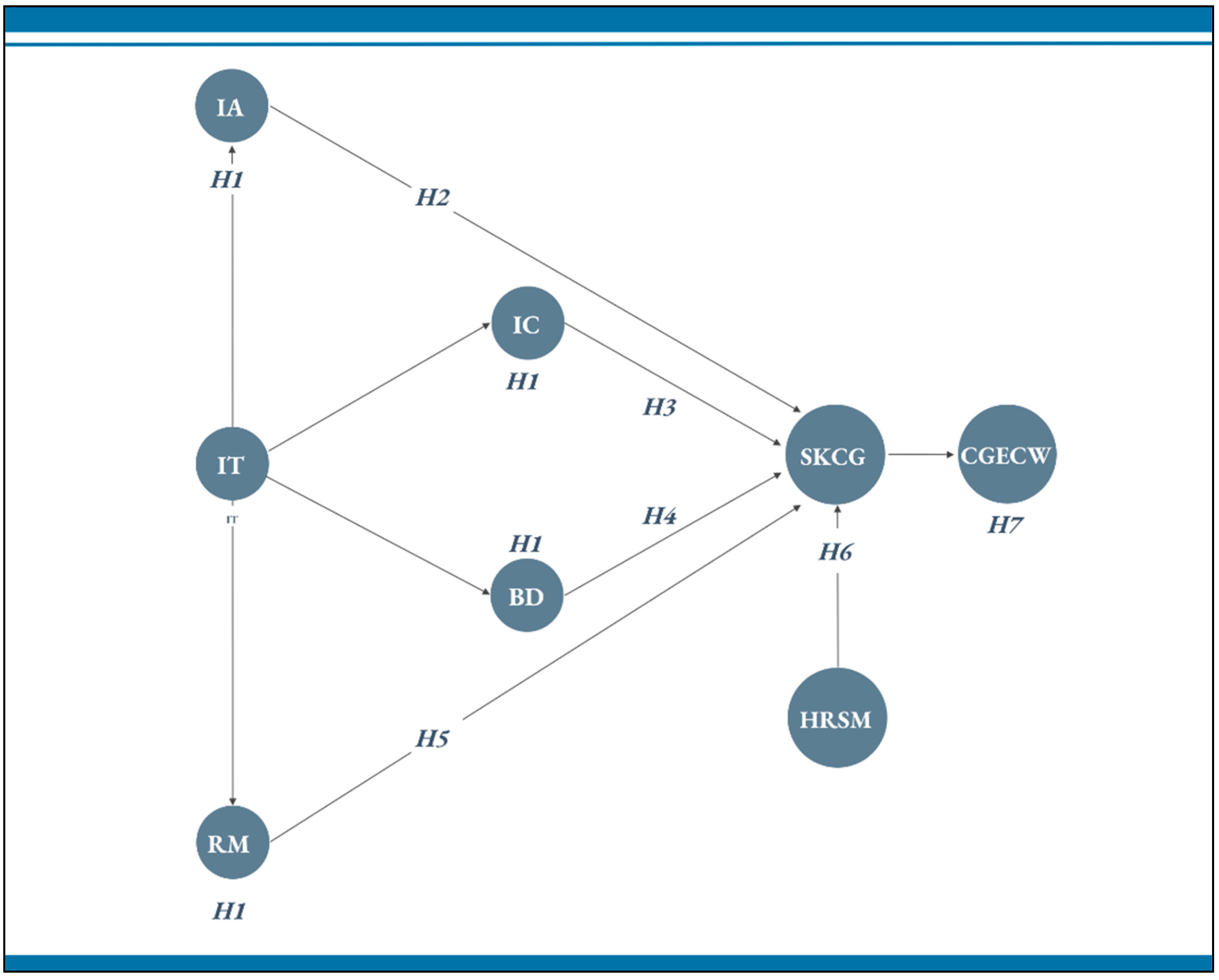

| Path Modeling | Hypotheses | Expected Sign | Parameters | Standard Deviation |

|---|---|---|---|---|

| IT -> BD | H1 | + | 0.545 *** | 0.084 |

| IT -> IAs | H1 | + | 0.504 *** | 0.088 |

| IT -> ICs | H1 | + | 0.402 *** | 0.087 |

| IT -> RM | H1 | + | 0.580 *** | 0.077 |

| IAs -> SKCG | H2 | − | −0.335 ** | 0.139 |

| ICs -> SKCG | H3 | + | 0.040 | 0.113 |

| BD -> SKCG | H4 | − | −0.021 | 0.131 |

| RM -> SKCG | H5 | + | 0.388 *** | 0.155 |

| HRM -> SKCG | H6 | + | 0.405 *** | 0.132 |

| SKCG -> CGECW | H7 | − | −0.301 *** | 0.106 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Flores, E.; De Paula, D.A.; Sampaio, J.d.O. Business Students Expectations of Brazilian Corporate Governance: Insights for a Sustainable Path in an Emerging Business Environment. Sustainability 2022, 14, 8817. https://doi.org/10.3390/su14148817

Flores E, De Paula DA, Sampaio JdO. Business Students Expectations of Brazilian Corporate Governance: Insights for a Sustainable Path in an Emerging Business Environment. Sustainability. 2022; 14(14):8817. https://doi.org/10.3390/su14148817

Chicago/Turabian StyleFlores, Eduardo, Douglas Augusto De Paula, and Joelson de Oliveira Sampaio. 2022. "Business Students Expectations of Brazilian Corporate Governance: Insights for a Sustainable Path in an Emerging Business Environment" Sustainability 14, no. 14: 8817. https://doi.org/10.3390/su14148817

APA StyleFlores, E., De Paula, D. A., & Sampaio, J. d. O. (2022). Business Students Expectations of Brazilian Corporate Governance: Insights for a Sustainable Path in an Emerging Business Environment. Sustainability, 14(14), 8817. https://doi.org/10.3390/su14148817