A Systematic Literature Review on Ownership and Corporate Social Responsibility in Family Firms

Abstract

:1. Introduction

2. Materials and Methods

3. Literature Review

3.1. Family Firm

3.2. CSR

3.3. Ownership

4. Main Effect of Ownership on CSR

4.1. Ownership Promoting CSR

4.2. Ownership Reducing CSR

4.3. U-Shaped Relationship between Ownership and CSR

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No | Author/year | Ownership | CSR | Theories |

|---|---|---|---|---|

| The positive relationship between ownership and CSR | ||||

| 1 | Li, 2012 [114] Chen and Wen, 2017 [115] Li, 2019 [116] Madden et al., 2020 [18] Ryuand Chae, 2021 [117] | Family ownership/ ownership proportion | CSR | Socioemotional selectivity theoryLong-term development perspective |

| 2 | Zhou, 2011 [77] Isabel-Maria et al., 2021 [118] | Family ownership | Insider responsibilities (investors, employees) External liability (creditors, partners, consumers) | Stakeholder theory SEW theory |

| 3 | Zeng, 2020 [21] | Family ownership Second largest shareholder | CSR engagement | Agency theory SEW theory |

| 4 | Aguilar and Luis, 2019 [119] | Family ownership | CSR practice (environment, social) | / |

| 5 | Syed and Butt, 2017 [85] Habbash, 2017 [66] | Government ownership Family ownership | CSR disclosure practices | Legitimacy theory Agency theory |

| 6 | Liu et al., 2017 [95] | Family ownership | CSR performance | SEW theory |

| 7 | Li et al., 2020 [81] | Family control | Green governance | Agency theory SEW theory |

| 8 | Bammens and Hünermund, 2020 [17] | Family ownership/ ownership proportion | Introduction of innovation ecology | Institutional theory Mixed game logic theory |

| 9 | Rubino and Napoli, 2020 [80] | Family ownership | Environmental performance | SEW theory |

| 10 | Maria Federica and Mirella, 2018 [120] | Family ownership | CSR instrumental, moral, and relational motivation | SEW theory |

| 11 | Chen & Chen, 2014 [12] Dou et al., 2014 [82] Ye et al., 2019 [83] | Family ownership proportion | Charitable donation | Stakeholder theory SEW theory Legitimacy theory |

| 12 | Christensen-Salem et al., 2021 [78] Wu and Zhang, 2019 [84] | Family ownership/ ownership proportion | Employees perceived organizational care/ employee responsibility | SEW theory Stakeholder theory |

| 13 | Cruz et al., 2014 [13] Zhu, 2021 [86] | Family ownership/ ownership proportion | External stakeholder-related CSR | Stakeholder theory SEW theory |

| 14 | Bingham et al., 2011 [16] | Family ownership/ ownership proportion | CSR performance activities Special stakeholder-related CSR | Stakeholder theory |

| 15 | Block and Wagner, 2014 [20] | Family ownership Founder ownership | CSR concern | SEW theory |

| 16 | Giovanna and De Massis, 2015 [121] | Family ownership | Different CSR reports Different CSR themes | Institutional theory |

| 17 | Xu et al., 2018 [63] | Family ownership/ ownership proportion | Philanthropy and environment governance-related CSR behavior | SEW theory Social responsibility pyramid theory |

| 18 | Kim and Lee, 2018 [99] | Family ownership | CSR performance | Agency theory |

| 19 | Sahasranamam et al., 2019 [19] | Business group ownership Family ownership | Community-related CSR | Agency theory Sociological perspectives of institutions |

| 20 | Andrea et al., 2021 [122] | Family ownership | CSR practice | SEW theory |

| 21 | Fehre and Weber, 2019 [96] | Founder ownership; family foundation ownership | Management CSR concern | SEW theory |

| 22 | Shu and Chiang, 2020 [67] | External large shareholders Institutional investor | CSR participation | Agency theory |

| 23 | Jian and Dai, 2019 [97] | Ownership Balance ratio | Social responsibility information-disclosure quality | / |

| The negative relationship between ownership and CSR | ||||

| 1 | LaBelle et al., 2015 [113] EI Ghoul et al., 2016 [110] | Family ownership | CSR performance | Agency theory SEW theory |

| 2 | Nekhili et al., 2017 [123] | Family ownership | CSR information report | Stakeholder theory |

| 3 | Chen and Cheng, 2020 [124] | Family ownership | CSR assurance | Agency theory |

| 4 | Rees and Rodionova, 2014 [101] | Family ownership | ESG: environment, social, governance | Agency theory |

| 5 | Block and Wagner., 2014 [20] | Family ownership/ founder ownership | CSR concern | SEW theory |

| 6 | McGuire et al., 2012 [125] | Family ownership | Poor CSR performance | Resource dependence theory Stakeholder theory |

| 7 | Zhou and Zhao, 2017 [103] Zhou et al., 2020 [102] | Family ownership/ ownership proportion | Environment responsibility practice/ environmental disclosure | Agency theory SEW theory |

| 8 | Stavrou et al., 2007 [76] Block, 2010 [75] Kim et al., 2019 [74] | Family ownership/ ownership proportion | Layoff tendency; deep layoffs | Place-based view |

| 9 | Cruz et al., 2014 [13] Zhu, 2021 [86] | Family ownership/ ownership proportion | Internal stakeholder-related CSR | Stakeholder theory SEW theory |

| 10 | Bingham et al., 2010 [16] | Family ownership/ ownership proportion | CSR social initiative CSR social concern | Stakeholder theory |

| 11 | Block and Wagner, 2014 [20] | Family ownership founder ownership | Community-related CSR CSR concern | Organizational and family identity view SEW theory |

| 12 | Giovanna and De Massis, 2015 [121] | Family ownership | CSR standards | Institutional theory |

| 13 | Xu et al., 2018 [63] | Family ownership/ ownership proportion | Philanthropy and environment governance-related CSR willingness | SEW theory Social responsibility pyramid theory |

| 14 | Kim and Lee, 2018 [99] | Family ownership | Corporate governance | Agency theory |

| 15 | Jian and Dai, 2019 [97] | Ownership concentration | Equity balance level Management shareholding ratio | / |

| 16 | Wu and Zhang, 2019 [84] | Family ownership/ ownership proportion | Charitable donation | Stakeholder SEW theory |

| 17 | Ye et al., 2019 [83] | Family ownership/ ownership proportion | Internal employee welfare | Stakeholder theory SEW theory Legitimacy theory |

| 18 | Andrea et al., 2021 [122] | Family ownership | CSR communication | SEW theory |

| 19 | Shu and Chiang, 2020 [67] | Internal large shareholders including directors | CSR motivation | Agency theory |

| 20 | Dick et al., 2021 [126] | Founder-controlled family firms | CSR participation | Social emotional endowment perspective |

| 21 | Atkinson and Galaskiewicz, 1988 [111] | Shares owned by CEO or single individuals | Charity | Agency theory |

| Other relationships between ownership and CSR | ||||

| 1 | Terlaak et al., 2018 [112] | The degree of family ownership | U-shaped relationship—the tendency of environmental performance disclosure | SEW theory |

| 2 | Labelle, et al., 2015 [113] | Family ownership | Curvilinear relationship Corporate social performance | Agency theory SEW theory |

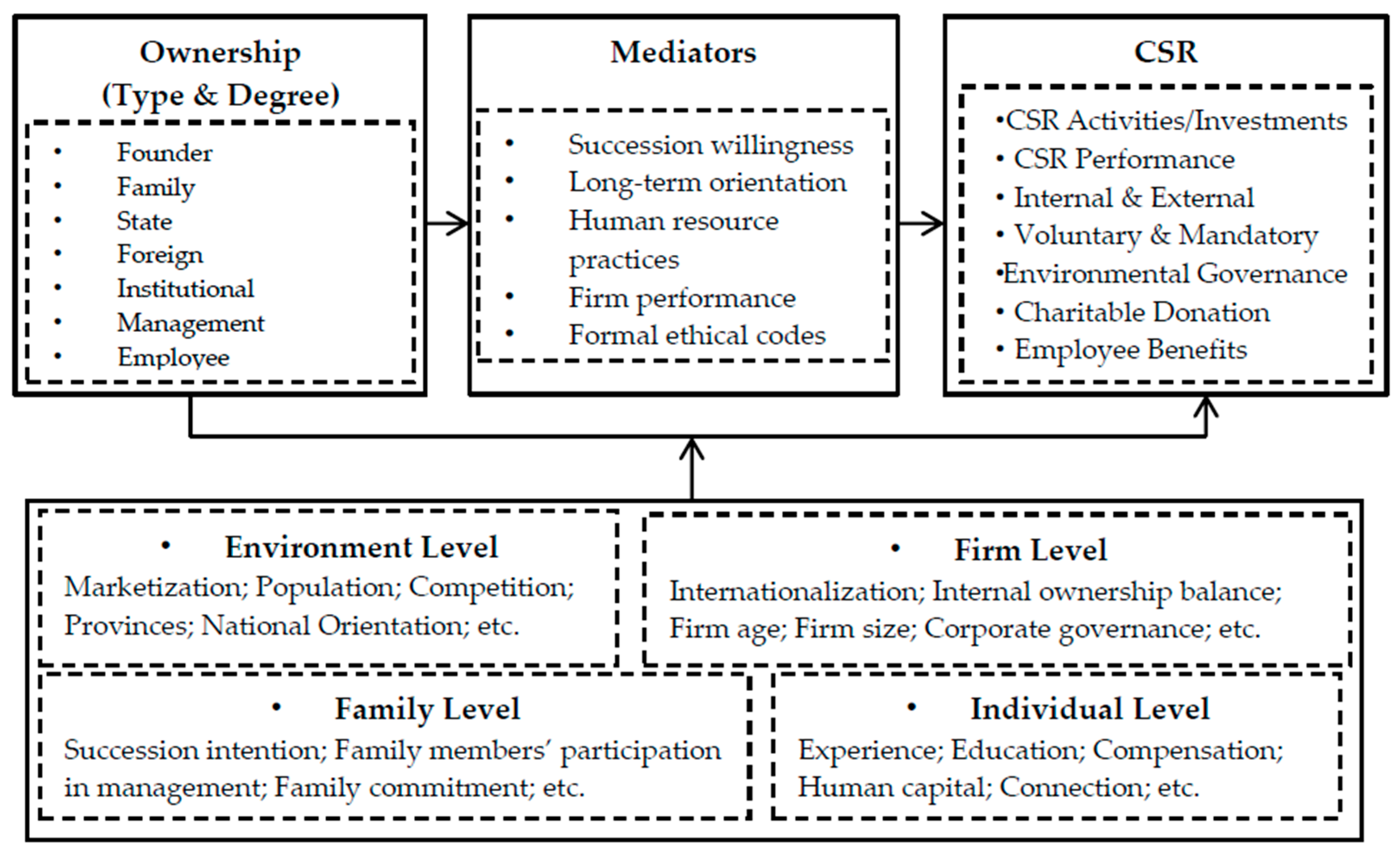

5. Mediators for the Relationship between Ownership and CSR

| Family level |

|

| Firm level | |

| Family firm level |

6. Contingent Factors for the Relationship between Family Firm Ownership and CSR

| Environment level | |

| Firm level | |

| Family Level |

|

| Individual level |

|

| Others |

|

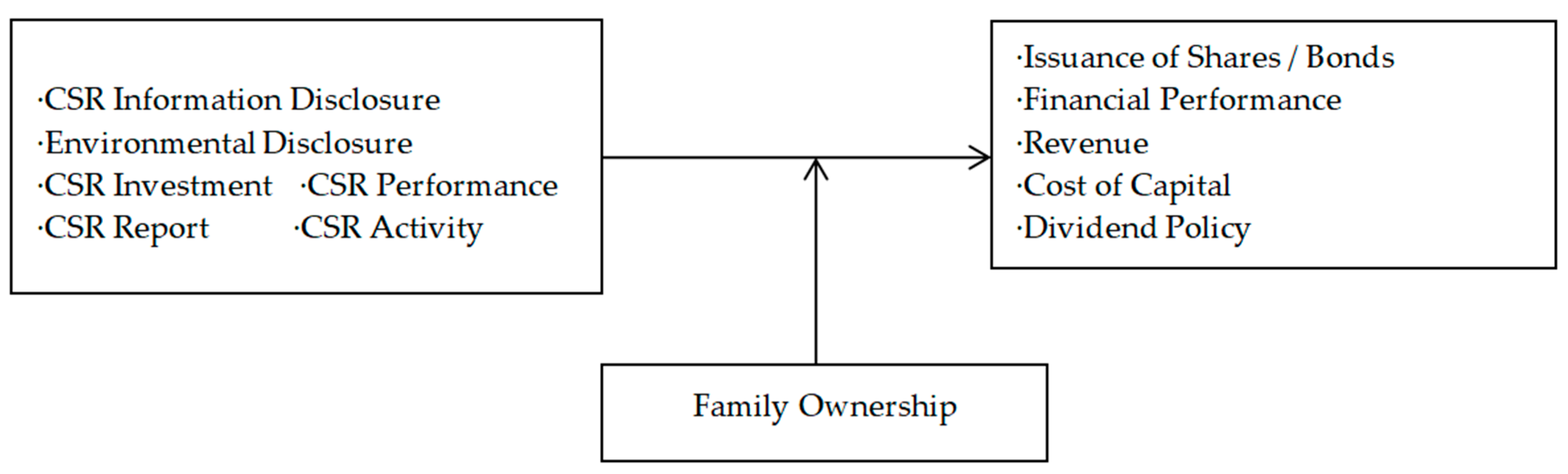

7. Family Ownership as a Moderator

7.1. Family Ownership as Moderator for the Relationship between Antecedents and CSR

7.2. Family Ownership as Moderator for the Relationship between CSR and Outcomes

8. Discussion and Conclusions

8.1. Analysis of Theories Adopted in Past Research

8.2. Analysis of Methods Adopted in Past Research

8.3. Practical Implications

8.4. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Dahlsrud, A. How corporate social responsibility is defined: An analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Montiel, I. Corporate Social Responsibility and Corporate Sustainability: Separate Pasts, Common Futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef] [Green Version]

- Uhlaner, L.M.; Berent-Braun, M.M.; Jeurissen, R.J.M.; de Wit, G. Beyond Size: Predicting Engagement in Environmental Management Practices of Dutch SMEs. J. Bus. Ethics 2012, 109, 411–429. [Google Scholar] [CrossRef]

- Faller, C.M.; Knyphausen-Aufseß, D.Z. Does Equity Ownership Matter for Corporate Social Responsibility? A Literature Review of Theories and Recent Empirical Findings. J. Bus. Ethics 2018, 150, 15–40. [Google Scholar] [CrossRef]

- Du, S.; Vieira, E.T., Jr. Striving for Legitimacy Through Corporate Social Responsibility: Insights from Oil Companies. J. Bus. Ethics 2012, 110, 413–427. [Google Scholar] [CrossRef]

- Panwar, R.; Paul, K.; Nybakk, E.; Hansen, E.; Thompson, D. The Legitimacy of CSR Actions of Publicly Traded Companies Versus Family-Owned Companies. J. Bus. Ethics 2013, 125, 481–496. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Sharma, S. Managerial Interpretations and Organizational Context as Predictors of Corporate Choice of Environmental Strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar]

- Mariani, M.M.; Al-Sultan, K.; De Massis, A. Corporate social responsibility in family firms: A systematic literature review. J. Small Bus. Manag. 2021, 1–55. [Google Scholar] [CrossRef]

- Kelly, L.M.; Athanassiou, N.; Crittenden, W.F. Founder Centrality and Strategic Behavior in the Family-Owned Firm. Entrep. Theory Pract. 2000, 25, 27–42. [Google Scholar] [CrossRef]

- Dou, J.; Su, E.; Wang, S. When Does Family Ownership Promote Proactive Environmental Strategy? The Role of the Firm’s Long-Term Orientation. J. Bus. Ethics 2017, 158, 81–95. [Google Scholar] [CrossRef]

- Ling, C.; Huali, C. The Clan Involvement, the Socio-emotional Wealth and the Corporate Charitable Contributions: A Case Study Based on the Survey of the Private Enterprises All over China. Manag. World 2014, 8, 90–101+188. [Google Scholar]

- Cruz, C.; Martin, L.-K.; Lucía, G.-G.; Pascual, B. Are Family Firms Really More Socially Responsible? Entrep. Theory Pract. 2014, 38, 1295–1316. [Google Scholar] [CrossRef] [Green Version]

- Le Breton-Miller, I.; Miller, D. Family firms and practices of sustainability: A contingency view. J. Fam. Bus. Strat. 2016, 7, 26–33. [Google Scholar] [CrossRef]

- Morck, R.; Yeung, B. Family Control and the Rent–Seeking Society. Entrep. Theory Pract. 2004, 28, 391–409. [Google Scholar] [CrossRef] [Green Version]

- Bingham, J.B.; Dyer, W.G.; Smith, I.; Adams, G.L. A Stakeholder Identity Orientation Approach to Corporate Social Performance in Family Firms. J. Bus. Ethics 2010, 99, 565–585. [Google Scholar] [CrossRef]

- Bammens, Y.; Hünermund, P. Nonfinancial considerations in eco-innovation decisions: The role of family ownership and reputation concerns. J. Prod. Innov. Manag. 2020, 37, 431–453. [Google Scholar] [CrossRef]

- Madden, L.; McMillan, A.; Harris, O. Drivers of selectivity in family firms: Understanding the impact of age and ownership on CSR. J. Fam. Bus. Strat. 2020, 11, 100335. [Google Scholar] [CrossRef]

- Sahasranamam, S.; Arya, B.; Sud, M. Ownership structure and corporate social responsibility in an emerging market. Asia Pac. J. Manag. 2019, 37, 1165–1192. [Google Scholar] [CrossRef] [Green Version]

- Block, J.; Wagner, M. Ownership versus management effects on corporate social responsibility concerns in large family and founder firms. J. Fam. Bus. Strat. 2014, 5, 339–346. [Google Scholar] [CrossRef]

- Zeng, T. Corporate social responsibility (CSR) in Canadian family firms. Soc. Responsib. J. 2020. [Google Scholar] [CrossRef]

- Short, J. The Art of Writing a Review Article. J. Manag. 2009, 35, 1312–1317. [Google Scholar] [CrossRef]

- Newman, A.; Martin Obschonka, J.M.; Gemma, G.C. Entrepreneurial Passion: A Review, Synthesis, and Agenda for Future Research. Appl. Psychol. 2021, 70, 816–860. [Google Scholar] [CrossRef] [Green Version]

- Ramos-Hidalgo, E.; Orta-Pérez, M.; Agustí, M.A. Ethics and Social Responsibility in Family Firms. Research Domain and Future Research Trends from a Bibliometric Perspective. Sustainability 2021, 13, 14009. [Google Scholar] [CrossRef]

- Liñán, F.; Alain, F. A Systematic Literature Review on Entrepreneurial Intentions. Int. Entrep. Manag. J. 2015, 11, 907–933. [Google Scholar] [CrossRef]

- Mariani, M.M.; Borghi, M. Industry 4.0: A bibliometric review of its managerial intellectual structure and potential evolution in the service industries. Technol. Forecast. Soc. Chang. 2019, 149, 119752. [Google Scholar] [CrossRef]

- Zupic, I.; Čater, T. Bibliometric methods in management and organization. Organ. Res. Methods 2015, 18, 429–472. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The journal coverage of Web of Science and Scopus: A comparative analysis. Scientometrics 2016, 106, 213–228. [Google Scholar] [CrossRef]

- Vieira, E.S.; Gomes, J. A Comparison of Scopus and Web of Science for a Typical University. Scientometrics 2009, 81, 587–600. [Google Scholar] [CrossRef]

- CNKI. “CNKI Introduction”. Available online: https://oversea.cnki.net/index/Support/en/Introduction.html (accessed on 16 May 2022).

- Mingers, J.; Yang, L. Evaluating journal quality: A review of journal citation indicators and ranking in business and management. Eur. J. Oper. Res. 2017, 257, 323–337. [Google Scholar] [CrossRef]

- Hoepner, A.G.F.; Unerman, J. Explicit and Implicit Subject Bias in the ABS Journal Quality Guide. Account. Educ. 2012, 21, 3–15. [Google Scholar] [CrossRef]

- Hussain, S. Journal List Fetishism and the ‘sign of 4’ in the ABS Guide: A Question of Trust? Organization 2015, 22, 119–138. [Google Scholar] [CrossRef] [Green Version]

- Morris, H.; Harvey, C.; Kelly, A. Journal rankings and the ABS Journal Quality Guide. Manag. Decis. 2009, 47, 1441–1451. [Google Scholar] [CrossRef] [Green Version]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2009, 84, 523–538. [Google Scholar] [CrossRef] [Green Version]

- König, A.; Nadine, K.; Albrecht, E. The family innovator’s dilemma: How family influence affects the adoption of discontinuous technologies by incumbent firms. Acad. Manag. Rev. 2013, 38, 418–441. [Google Scholar] [CrossRef] [Green Version]

- Duran, P.; Kammerlander, N.; Van Essen, M.; Zellweger, T. Doing more with less: Innovation input and output in family firms. Acad. Manag. J. 2016, 59, 1224–1264. [Google Scholar] [CrossRef] [Green Version]

- Peng, M.W.; Jiang, Y. Institutions Behind Family Ownership and Control in Large Firms. J. Manag. Stud. 2010, 47, 253–273. [Google Scholar] [CrossRef]

- Miller, D.; Le Breton-Miller, I.; Lester, R.H.; Cannella, A.A. Are Family Firms Really Superior Performers? J. Corp. Financ. 2007, 5, 829–858. [Google Scholar] [CrossRef]

- Gomez–Mejia, L.R.; Campbell, J.T.; Martin, G.; Hoskisson, R.E.; Makri, M.; Sirmon, D.G. Socioemotional Wealth as a Mixed Gamble: Revisiting Family Firm R&D Investments with the Behavioral Agency Model. Entrep. Theory Pract. 2014, 38, 1351–1374. [Google Scholar] [CrossRef]

- Villalonga, B.; Amit, R. How Do Family Ownership, Control and Management Affect Firm Value? J. Financ. Econ. 2006, 80, 385–417. [Google Scholar] [CrossRef] [Green Version]

- Llach, J.; Nordqvist, M. Innovation in family and non-family businesses: A resource perspective. Int. J. Entrep. Ventur. 2010, 2, 381. [Google Scholar] [CrossRef]

- Chua, J.H.; Chrisman, J.J.; Sharma, P. Defining the Family Business by Behavior. Entrep. Theory Pract. 1999, 23, 19–39. [Google Scholar] [CrossRef]

- Chrisman, J.J.; Chua, J.H.; Sharma, P. Trends and Directions in the Development of a Strategic Management Theory of the Family Firm. Entrep. Theory Pract. 2005, 29, 555–575. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Martynov, A. The Effect of Ownership Structure on Corporate Social Responsibility: Empirical Evidence from Korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Jia, M.; Zhang, Z. Managerial Ownership and Corporate Social Performance: Evidence from Privately Owned Chinese Firms’ Response to the Sichuan Earthquake. Corp. Soc. Responsib. Environ. Manag. 2012, 20, 257–274. [Google Scholar] [CrossRef]

- Su, R.; Chunping, L.; Weili, T. The heterogeneous effects of CSR dimensions on financial performance—A new approach for csr measurement. J. Bus. Econ. Manag. 2020, 21, 987–1009. [Google Scholar] [CrossRef]

- Cavaco, S.; Crifo, P. CSR and Financial Performance: Complementarity between Environmental, Social and Business Behaviours. Appl. Econ. 2014, 46, 3323–3338. [Google Scholar] [CrossRef]

- Girerd-Potin, I.; Jimenez-Garcès, S.; Louvet, P. Which Dimensions of Social Responsibility Concern Financial Investors? J. Bus. Ethics 2014, 121, 559–576. [Google Scholar] [CrossRef] [Green Version]

- Inoue, Y.; Lee, S. Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries. Tour. Manag. 2011, 32, 790–804. [Google Scholar] [CrossRef]

- Wang, Z.; Reimsbach, D.; Braam, G. Political Embeddedness and the Diffusion of Corporate Social Responsibility Prac-tices in China: A Trade-off between Financial and CSR Performance? J. Clean. Prod. 2018, 198, 1185–1197. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate Social Performance and Organizational Attractiveness to Prospective Employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Clarkson, M.B.E. A Stakeholder Framework for Analyzing and Evaluating Corporate Social Performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Peloza, J.; Papania, L. The Missing Link between Corporate Social Responsibility and Financial Performance: Stakeholder Salience and Identification. Corp. Reput. Rev. 2008, 11, 169–181. [Google Scholar] [CrossRef]

- Contini, M.; Annunziata, E.; Rizzi, F.; Frey, M. Exploring the influence of Corporate Social Responsibility (CSR) domains on consumers’ loyalty: An experiment in BRICS countries. J. Clean. Prod. 2019, 247, 119158. [Google Scholar] [CrossRef]

- Flammer, C.; Hong, B.; Minor, D. Corporate governance and the rise of integrating corporate social responsibility criteria in executive compensation: Effectiveness and implications for firm outcomes. Strat. Manag. J. 2019, 40, 1097–1122. [Google Scholar] [CrossRef]

- Hur, W.-M.; Moon, T.-W.; Choi, W.-H. When are internal and external corporate social responsibility initiatives amplified? Employee engagement in corporate social responsibility initiatives on prosocial and proactive behaviors. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 849–858. [Google Scholar] [CrossRef]

- Skudiene, V.; Auruskeviciene, V. The contribution of corporate social responsibility to internal employee motivation. Balt. J. Manag. 2012, 7, 49–67. [Google Scholar] [CrossRef]

- Al-Shammari, M.; Rasheed, A.; Al-Shammari, H.A. CEO Narcissism and Corporate Social Responsibility: Does CEO Narcissism Affect CSR Focus? J. Bus. Res. 2019, 104, 106–117. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A.; Rayton, B. The contribution of corporate social responsibility to organizational commitment. Int. J. Hum. Resour. Manag. 2007, 18, 1701–1719. [Google Scholar] [CrossRef] [Green Version]

- Carroll, A.B. Managing ethically with global stakeholders: A present and future challenge. Acad. Manag. Perspect. 2004, 18, 114–120. [Google Scholar] [CrossRef]

- Xu, J.; Li, S.; Zhang, D. Family Involvement, Institutional Environment and Corporate Voluntary Social Responsibility: Study Based on the Tenth Survey of the Private Enterprises All over China. Bus. Manag. J. 2018, 40, 37–53. [Google Scholar]

- Lee, M.-D.P. Does Ownership Form Matter for Corporate Social Responsibility? A Longitudinal Comparison of Environmental Performance between Public, Private, and Joint-venture Firms. Bus. Soc. Rev. 2009, 114, 435–456. [Google Scholar] [CrossRef]

- Tetrault Sirsly, C.-A.; Sujit, S. Strategies for Sustainability Initiatives: Why Ownership Matters. Corp. Gov. 2013, 13, 541–550. [Google Scholar] [CrossRef]

- Habbash, M. Corporate Governance and Corporate Social Responsibility Disclosure: Evidence from Saudi Arabia. Int. J. Corp. Strategy Soc. Responsib. 2017, 1, 161–178. [Google Scholar]

- Shu, P.-G.; Chiang, S.-J. The impact of corporate governance on corporate social performance: Cases from listed firms in Taiwan. Pac. Basin Financ. J. 2020, 61, 101332. [Google Scholar] [CrossRef]

- Grougiou, V.; Dedoulis, E.; Leventis, S. Corporate Social Responsibility Reporting and Organizational Stigma: The Case of “Sin” Industries. J. Bus. Res. 2016, 69, 905–914. [Google Scholar] [CrossRef]

- Venkataraman, I.; Lulseged, A. Does Family Status Impact US Firms’ Sustainability Reporting? Sustain. Account. Manag. Policy J. 2013, 4, 163–189. [Google Scholar]

- Jo, H.; Harjoto, M.A. Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Panicker, V.S. Ownership and corporate social responsibility in Indian firms. Soc. Responsib. J. 2017, 13, 714–727. [Google Scholar] [CrossRef]

- Pascual, B.; Cruz, C.; Gomez-Mejia, L.R.; Larraza-Kintana, M. Socioemotional Wealth and Corporate Responses to Institutional Pressures: Do Family-Controlled Firms Pollute Less? Adm. Sci. Q. 2010, 55, 82–113. [Google Scholar]

- Baumann-Pauly, D.; Wickert, C.; Spence, L.J.; Scherer, A.G. Organizing Corporate Social Responsibility in Small and Large Firms: Size Matters. J. Bus. Ethics 2013, 115, 693–705. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.; Haider, Z.A.; Wu, Z.; Dou, J. Corporate Social Performance of Family Firms: A Place-Based Perspective in the Context of Layoffs. J. Bus. Ethics 2019, 167, 235–252. [Google Scholar] [CrossRef]

- Block, J. Family Management, Family Ownership, and Downsizing: Evidence from S&P 500 Firms. Fam. Bus. Rev. 2010, 23, 109–130. [Google Scholar]

- Stavrou, E.; Kassinis, G.; Filotheou, A. Downsizing and Stakeholder Orientation among the Fortune 500: Does Family Ownership Matter? J. Bus. Ethics 2007, 72, 149–162. [Google Scholar] [CrossRef]

- Zhou, L. Family Involvement and Corporate Social Responsibility: Manufacturing Evidence from China Economic Management. J. Chin. Sociol. 2011, 33, 45–53. [Google Scholar]

- Christensen-Salem, A.; Mesquita, L.F.; Hashimoto, M.; Hom, P.W.; Gomez-Mejia, L.R. Family firms are indeed better places to work than non-family firms! Socioemotional wealth and employees’ perceived organizational caring. J. Fam. Bus. Strat. 2021, 12, 100412. [Google Scholar] [CrossRef]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L.R. Socioemotional Wealth in Family Firms. Fam. Bus. Rev. 2012, 25, 258–279. [Google Scholar] [CrossRef]

- Rubino, F.; Napoli, F. What Impact Does Corporate Governance Have on Corporate Environmental Performances. An Empirical Study of Italian Listed Firms. Sustainability 2020, 12, 5742. [Google Scholar] [CrossRef]

- Li, X.; Li, W.; Zhang, Y. Family Control, Political Connection, and Corporate Green Governance. Sustainability 2020, 12, 7068. [Google Scholar] [CrossRef]

- Dou, J.; Zhang, Z.; Su, E. Does Family Involvement Make Firms Donate More? Empirical Evidence From Chinese Private Firms. Fam. Bus. Rev. 2014, 27, 259–274. [Google Scholar] [CrossRef] [Green Version]

- Ye, Y.; Li, K.; Hu, G. The Selective Participation in Corporate Social Responsibility in Family Enterprises. J. Beijing Inst. Technol. 2019, 21, 76–85. [Google Scholar]

- Wu, F.; Zhang, Y. Family Involvement, Non-Market Strategies and Corporate Performance: From the Multi-Dimensional Per-spective of Social Emotional Wealth. Contemp. Financ. Econ. 2019, 3, 81–93. [Google Scholar]

- Syed, M.A.; Butt, S.A. Financial and non-financial determinants of corporate social responsibility: Empirical evidence from Pakistan. Soc. Responsib. J. 2017, 13, 780–797. [Google Scholar] [CrossRef]

- Zhu, B. The self-centered philanthropist: Family involvement and corporate social responsibility in private enterprises. J. Chin. Sociol. 2021, 8, 21. [Google Scholar] [CrossRef]

- Yan, Y.; Li, K. Impact of Family Involvement on Internal and External Corporate Social Responsibilities: Evidence from Chinese Publicly Listed Firms. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 352–365. [Google Scholar]

- Zhu, H.; Ye, Q.; Li, X. Social Emotional Wealth Theory and its Breakthrough in Family Firms Research. Foreign Econ. Manag. 2012, 34, 56–62. [Google Scholar]

- Godfrey, P.C. The Relationship Between Corporate Philanthropy And Shareholder Wealth: A Risk Management Perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef] [Green Version]

- Gibb, D.W., Jr.; Whetten, D.A. Family Firms and Social Responsibility: Preliminary Evidence from the S&P 500. Entrep. Theory Pract. 2006, 30, 785–802. [Google Scholar]

- Miller, D.; Le Breton-Miller, I. Managing for the Long Run: Lessons in Competitive Advantage from Great Family Businesses; Harvard Business Press: Boston, MA, USA, 2005. [Google Scholar]

- Lloyd, S. Variants of Agency Contracts in Family-financed Ventures as a Continuum of Familial Altruistic and Market Rational-ities. J. Bus. Ventur. 2003, 18, 597–618. [Google Scholar]

- Vazquez, P. Family Business Ethics: At the Crossroads of Business Ethics and Family Business. J. Bus. Ethics 2016, 150, 691–709. [Google Scholar] [CrossRef]

- de la Cruz Déniz Déniz, M.; Suárez, M.K.C. Corporate Social Responsibility and Family Business in Spain. J. Bus. Ethics 2005, 56, 27–41. [Google Scholar] [CrossRef]

- Liu, M.; Shi, Y.; Wilson, C.; Zhenyu Wu, Z. Does Family Involvement Explain Why Corporate Social Responsibility Affects Earnings Management? J. Bus. Res. 2017, 75, 8–16. [Google Scholar] [CrossRef]

- Fehre, K.; Weber, F. Why some are more equal: Family firm heterogeneity and the effect on management’s attention to CSR. Bus. Ethics A Eur. Rev. 2018, 28, 321–334. [Google Scholar] [CrossRef]

- Jian, R.; Dai, C. Research on the Impact of Ownership Structure Characteristics on the Quality of Social Responsibility Information Disclosure: Based on the Data Analysis of Family Listed Companies in China. Sci. Decis. Mak. 2019, 4, 41–57. [Google Scholar]

- Malik, M. Value-Enhancing Capabilities of CSR: A Brief Review of Contemporary Literature. J. Bus. Ethics 2014, 127, 419–438. [Google Scholar] [CrossRef]

- Kim, A.; Lee, Y. Family firms and corporate social performance: Evidence from Korean firms. Asia Pac. Bus. Rev. 2018, 24, 693–713. [Google Scholar] [CrossRef]

- Desender, K.; Epure, M. The Pressure behind Corporate Social Performance: Ownership and Institutional Configurations. Glob. Strategy J. 2021, 11, 210–244. [Google Scholar] [CrossRef]

- Rees, W.; Rodionova, T. The Influence of Family Ownership on Corporate Social Responsibility: An International Analysis of Publicly Listed Companies. Corp. Gov. Int. Rev. 2014, 23, 184–202. [Google Scholar] [CrossRef]

- Zhou, Z.; Lai, Y.; Yi, X.; Zeng, H. Can Controlling Family Involvement Promote Enterprises to Fulfill Environmental Responsibilities? Based on the Evidence of A-share Listed Companies in China. J. Nanjing Audit. Univ. 2020, 17, 37–46. [Google Scholar]

- Zhou, W.; Zhao, J. Family Involvement, International Operation and Corporate Environmental Responsibility. Jilin Univ. J. Soc. Sci. Ed. 2017, 57, 84–94+205. [Google Scholar]

- Anderson, R.C.; Reeb, D.M. Founding-Family Ownership and Firm Performance: Evidence from the S&P 500. J. Financ. 2003, 58, 1301–1328. [Google Scholar] [CrossRef]

- Andres, C. Large shareholders and firm performance—An empirical examination of founding-family ownership. J. Corp. Financ. 2008, 14, 431–445. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate Social Responsibility as a Conflict Between Shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Rees, W.; Rodionova, T. What type of controlling investors impact on which elements of corporate social responsibility? J. Sustain. Financ. Invest. 2013, 3, 238–263. [Google Scholar] [CrossRef]

- Bertrand, M.; Mehta, P.; Mullainathan, S. Ferreting Out Tunneling: An Application to Indian Business Groups. Q. J. Econ. 2000, 117, 121–148. [Google Scholar] [CrossRef]

- DeAngelo, H.; DeAngelo, L. Controlling stockholders and the disciplinary role of corporate payout policy: A study of the Times Mirror Company. J. Financ. Econ. 2000, 56, 153–207. [Google Scholar] [CrossRef]

- EI Ghoul, S.; Guedhami, O.; Wang, H.; Kwok, C.C.Y. Family Control and Corporate Social Responsibility. J. Bank. Financ. 2016, 73, 131–146. [Google Scholar] [CrossRef]

- Atkinson, L.; Galaskiewicz, J. Stock Ownership and Company Contributions to Charity. Adm. Sci. Q. 1988, 33, 82. [Google Scholar] [CrossRef]

- Terlaak, A.; Kim, S.; Roh, T. Not Good, Not Bad: The Effect of Family Control on Environmental Performance Disclosure by Business Group Firms. J. Bus. Ethics 2018, 153, 977–996. [Google Scholar] [CrossRef]

- Labelle, R.; Hafsi, T.; Francoeur, C.; Ben Amar, W. Family Firms’ Corporate Social Performance: A Calculated Quest for Socioemotional Wealth. J. Bus. Ethics 2015, 148, 511–525. [Google Scholar] [CrossRef]

- Li, X. Empirical study on family involvement, and agricultural enterprises corporate social responsibility. Guangdong Agri-Cult. Sci. 2012, 39, 233–236. [Google Scholar]

- Chen, J.; Wen, Z. Family Control, Executive Incentive and Corporate Social Responsibility: An Empirical Study Based on Chinese Listed Companies. J. Nanjing Audit. Univ. 2017, 14, 66–74. [Google Scholar]

- Li, Y. Family Involvement, Executive Compensation and Corporate Social Responsibility. Commun. Financ. Account. 2019, 24, 67–70. [Google Scholar]

- Ryu, H.; Chae, S.-J. Family Firms, Chaebol Affiliations, and Corporate Social Responsibility. Sustainability 2021, 13, 3016. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Martín-Moreno, J.; Khan, S.A.; Hussain, N. Socio-emotional Wealth and Corporate Responses to Environmental Hostility: Are Family Firms More Stakeholder Oriented? Bus. Strategy Environ. 2021, 30, 1003–1018. [Google Scholar] [CrossRef]

- Aguilar, E.; Luis, J. Corporate Social Responsibility Practices Developed by Mexican Family and Non-family Business-es. J. Fam. Bus. Manag. 2019, 9, 40–53. [Google Scholar] [CrossRef]

- Izzo, M.F.; Ciaburri, M. Why Do They Do That? Motives and Dimensions of Family Firms’ CSR Engagement. Soc. Responsib. J. 2018, 14, 633–650. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-family Firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Venturelli, A.; Principale, S.; Ligorio, L.; Cosma, S. Walking the Talk in Family Firms. An Empirical Investigation of CSR Communication and Practices. Corp. Soc.-Responsib. Environ. Manag. 2021, 28, 497–510. [Google Scholar] [CrossRef]

- Nekhili, M.; Nagati, H.; Chtioui, T.; Rebolledo, C. Corporate social responsibility disclosure and market value: Family versus nonfamily firms. J. Bus. Res. 2017, 77, 41–52. [Google Scholar] [CrossRef]

- Chen, Y.-L.; Cheng, H.-Y. Public family businesses and corporate social responsibility assurance: The role of mimetic pressures. J. Account. Public Policy 2020, 39, 106734. [Google Scholar] [CrossRef]

- McGuire, J.; Dow, S.; Ibrahim, B. All in the family? Social performance and corporate governance in the family firm. J. Bus. Res. 2012, 65, 1643–1650. [Google Scholar] [CrossRef]

- Dick, M.; Wagner, E.; Pernsteiner, H. Founder-Controlled Family Firms, Overconfidence, and Corporate Social Re-sponsibility Engagement: Evidence from Survey Data. Fam. Bus. Rev. 2021, 34, 71–92. [Google Scholar] [CrossRef]

- Lumpkin, G.T.; Brigham, K.H. Long–Term Orientation and Intertemporal Choice in Family Firms. Entrep. Theory Pract. 2011, 35, 1149–1169. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a Theory of Stakeholder Identification and Salience: Defining the Principle of Who and What Really Counts. Acad. Manag. Rev. 1997, 22, 853. [Google Scholar] [CrossRef]

- Sharma, P. An Overview of the Field of Family Business Studies: Current Status and Directions for the Future. Fam. Bus. Rev. 2004, 17, 1–36. [Google Scholar] [CrossRef]

- Deephouse, D.L.; Jaskiewicz, P. Do Family Firms Have Better Reputations Than Non-Family Firms? An Integration of Socioemotional Wealth and Social Identity Theories. J. Manag. Stud. 2013, 50, 337–360. [Google Scholar] [CrossRef]

- Kalm, M.; Gomez-Mejia, L.R. Socioemotional wealth preservation in family firms. Rev. Adm. 2016, 51, 409–411. [Google Scholar] [CrossRef] [Green Version]

- Dal Maso, L.; Basco, R.; Bassetti, T.; Lattanzi, N. Family Ownership and Environmental Performance: The Mediation Effect of Human Resource Practices. Bus. Strategy Environ. 2020, 29, 1548–1562. [Google Scholar] [CrossRef]

- Cuadrado-Ballesteros, B.; Rodríguez-Ariza, L.; García-Sánchez, I.-M.; Martínez-Ferrero, J. The mediating effect of ethical codes on the link between family firms and their social performance. Long Range Plan. 2017, 50, 756–765. [Google Scholar] [CrossRef]

- Li, M.; Shi, X. Empirical Research on Relational Contractual governance, Corporate Financial Performance and Corporate Social Responsibility of Family Businesses: A Pragmatic Study on Family Businesses from A Shares. J. Xi’an Univ. Financ. Econ. 2014, 27, 62–66. [Google Scholar]

- Cennamo, C.; Berrone, P.; Cruz, C.; Gomez–Mejia, L.R. Socioemotional Wealth and Proactive Stakeholder Engagement: Why Family–Controlled Firms Care More about their Stakeholders. Entrep. Theory Pract. 2012, 36, 1153–1173. [Google Scholar] [CrossRef]

- Yu, B.; Zeng, S.; Chen, H.; Meng, X.; Chiming, T. Doing More and Doing Better Are Two Different Entities: Different Patterns of Family Control and Environmental Performance. Bus. Strategy Environ. 2021, 30, 1–20. [Google Scholar] [CrossRef]

- Gavana, G.; Gottardo, P.; Moisello, A.M. Sustainability Reporting in Family Firms: A Panel Data Analysis. Sustainability 2017, 9, 38. [Google Scholar] [CrossRef] [Green Version]

- Xu, E.; Zheng, P. Corporate Social Responsibility in International Operation. Soft Sci. 2006, 20, 53–57. [Google Scholar]

- Graafland, J. Family business ownership and cleaner production: Moderation by company size and family management. J. Clean. Prod. 2020, 255, 120120. [Google Scholar] [CrossRef]

- Abeysekera, A.P.; Fernando, C.S. Corporate social responsibility versus corporate shareholder responsibility: A family firm perspective. J. Corp. Financ. 2018, 61, 101370. [Google Scholar] [CrossRef]

- Cui, V.; Shujun, D.; Liu, M.; Wu, Z. Revisiting the Effect of Family Involvement on Corporate Social Responsi-bility: A Behavioral Agency Perspective. J. Bus. Ethics 2016, 152, 291–309. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Profumo, G.; Tutore, I. Board gender diversity and corporate environmental performance: The moderating role of family and dual-class majority ownership structures. Bus. Strat. Environ. 2019, 29, 1127–1144. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Rodríguez-Ariza, L.; García-Sánchez, I.-M. Corporate Social Responsibility as an Entrenchment Strategy, with a Focus on the Implications of Family Ownership. J. Clean. Prod. 2016, 135, 760–770. [Google Scholar] [CrossRef]

- Ge, J.; Micelotta, E. When Does the Family Matter? Institutional Pressures and Corporate Philanthropy in China. Organ. Stud. 2019, 40, 833–857. [Google Scholar] [CrossRef]

- Mazzelli, A.; Kotlar, J.; De Massis, A. Blending In While Standing Out: Selective Conformity and New Product Introduction in Family Firms. Entrep. Theory Pract. 2018, 42, 206–230. [Google Scholar] [CrossRef]

- Yang, Z.; Ma, G.; Chen, J. Entrepreneurs’ Comprehensive Status, Family Involvement and Corporate Social Responsibility –Micro Evidence from the Survey of Private Enterprises in China. Econ. Perspect. 2021, 8, 101–115. [Google Scholar]

- Li, S.; Hou, M.; Wang, D. Management Overconfidence and Corporate Social Responsibility. Chin. Rev. Fianncial Stud. 2015, 7, 58–69+124. [Google Scholar]

- Rodríguez-Ariza, L.; Cuadrado-Ballesteros, B.; Martínez-Ferrero, J.; García-Sánchez, I.-M. The role of female directors in promoting CSR practices: An international comparison between family and non-family businesses. Bus. Ethics A Eur. Rev. 2017, 26, 162–174. [Google Scholar] [CrossRef]

- Jing, C.; Zhang, Z.; Jia, M. How CEO Narcissism Affects Corporate Social Responsibility Choice? Asia Pac. J. Manag. 2019, 38, 897–924. [Google Scholar]

- Zhou, L. The impact of Guanxi Network on Social Responsibility of Family Firms: Evidence from Manufacturing Family Firms in Zhejiang and Chongqing. Stat. Inf. Forum 2014, 29, 91–97. [Google Scholar]

- Hajawiyah, A.; Adhariani, D.; Djakman, C. The Sequential Effect of CSR and COE: Family Ownership Moderation. Soc. Responsib. J. 2019, 15, 939–954. [Google Scholar] [CrossRef]

- Singal, M. Corporate Social Responsibility in the Hospitality and Tourism Industry: Do Family Control and Financial Condition Matter? Int. J. Hosp. Manag. 2014, 36, 81–89. [Google Scholar] [CrossRef]

- Gavana, G.; Gottardo, P.; Moisello, A.M. Do Customers Value CSR Disclosure? Evidence from Italian Family and Non-Family Firms. Sustainability 2018, 10, 1642. [Google Scholar] [CrossRef] [Green Version]

- Du, S.; Bhattacharya, C.; Sen, S. Maximizing Business Returns to Corporate Social Responsibility (CSR): The Role of CSR Communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Shepherd, D.A.; Haynie, J.M. Family business, identity Conflict, and an Expedited Entrepreneurial Process: A Process of Resolving Identity Conflict. Entrep. Theory Pract. 2009, 6, 1245–1264. [Google Scholar] [CrossRef]

- Reay, T. Family–Business Meta–Identity, Institutional Pressures, and Ability to Respond to Entrepreneurial Opportunities. Entrep. Theory Pract. 2009, 33, 1265–1270. [Google Scholar] [CrossRef]

- Randolph, R.V.; Memili, E.; Koç, B.; Young, S.L.; Yildirim-Öktem, Ö.; Sönmez, S. Innovativeness and Cor-porate Social Responsibility in Hospitality and Tourism Family Firms: The Role of Family Firm Psychological Capital. Int. J. Hosp. Manag. 2022, 101, 103128. [Google Scholar] [CrossRef]

- Diaz-Moriana, V.; Clinton, E.; Kammerlander, N.; Lumpkin, G.T.; Craig, J. Innovation Motives in Family Firms: A Transgenerational View. Entrep. Theory Pract. 2018, 44, 256–287. [Google Scholar] [CrossRef] [Green Version]

- Luthans, F.; Avolio, B.J.; Avey, J.B.; Norman, S.M. Positive psychological capital: Measurement and relationship with performance and satisfaction. Pers. Psychol. 2007, 60, 541–572. [Google Scholar] [CrossRef] [Green Version]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Su, S.; Zhu, F.; Zhou, H. A Systematic Literature Review on Ownership and Corporate Social Responsibility in Family Firms. Sustainability 2022, 14, 7817. https://doi.org/10.3390/su14137817

Su S, Zhu F, Zhou H. A Systematic Literature Review on Ownership and Corporate Social Responsibility in Family Firms. Sustainability. 2022; 14(13):7817. https://doi.org/10.3390/su14137817

Chicago/Turabian StyleSu, Saier, Fei Zhu, and Haibo Zhou. 2022. "A Systematic Literature Review on Ownership and Corporate Social Responsibility in Family Firms" Sustainability 14, no. 13: 7817. https://doi.org/10.3390/su14137817

APA StyleSu, S., Zhu, F., & Zhou, H. (2022). A Systematic Literature Review on Ownership and Corporate Social Responsibility in Family Firms. Sustainability, 14(13), 7817. https://doi.org/10.3390/su14137817