Improving the Material and Financial Circularity of the Plastic Packaging Value Chain in The Netherlands: Challenges, Opportunities, and Implications

Abstract

:1. Introduction

- What are the most feasible and efficient policies that would create a more circular plastic packaging value chain in The Netherlands?

- What are the effects of these policies on the business models of key industry stakeholders and the material and financial circularity of the Dutch plastic packaging value chain?

2. Literature Review

2.1. Global Plastic Packaging Industry

2.2. Plastic Packaging Industry in The Netherlands

2.2.1. Current Situation

2.2.2. Institutional Structure, General Political Regulations and Targets

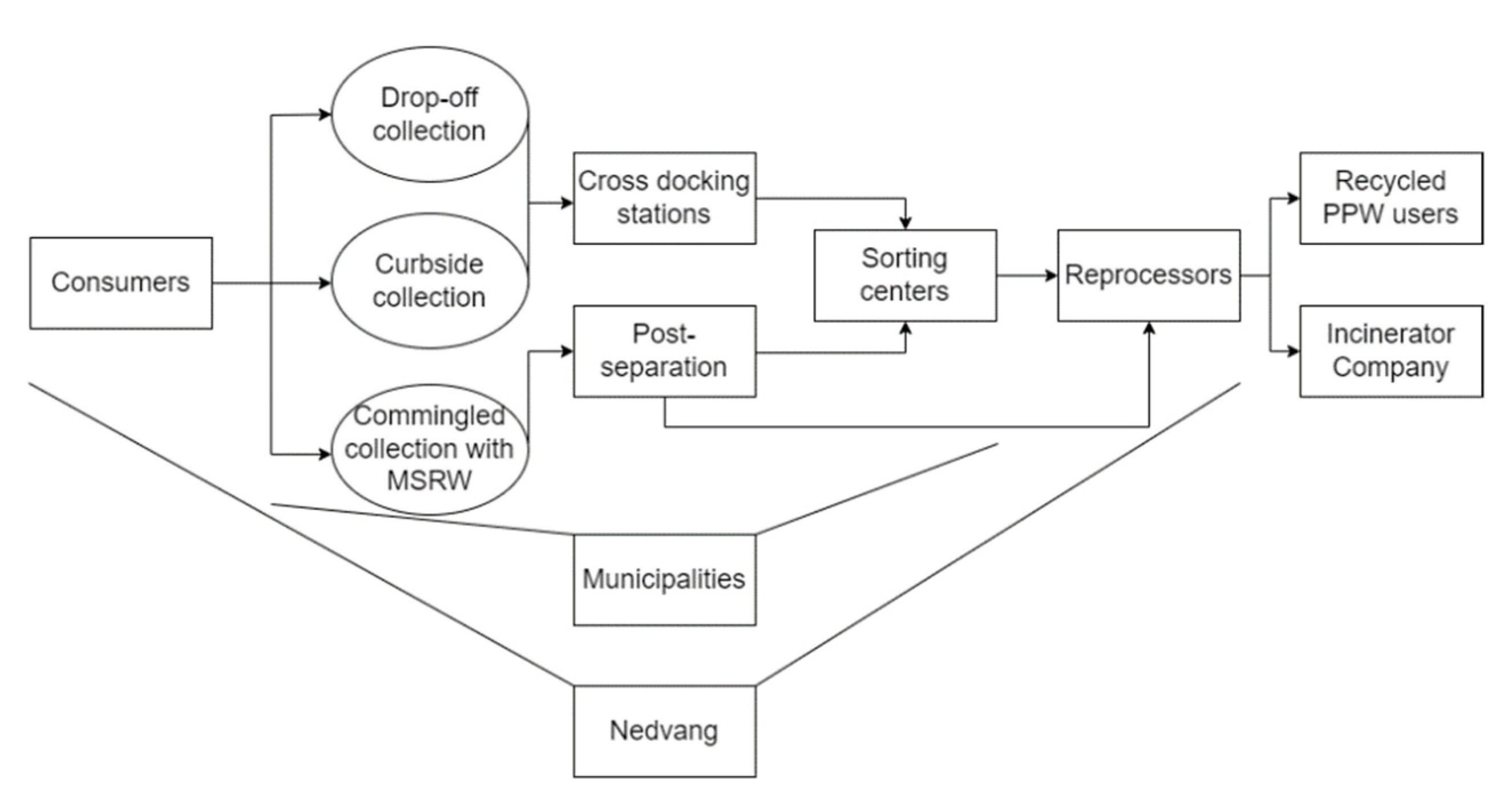

2.2.3. The Organization of PPW Treatment in The Netherlands

- Household waste: Plastic packaging from households is separated in two ways—source separation and post-separation. With the former, consumers separate plastics from other household waste themselves; in the latter, sorting centers use waste processors to separate plastics from the other types of waste using infrared and film-grabber techniques [43]. While post-separation facilities can collect more material than source separation, the difference between the amounts of produced milled goods and agglomerates that each system produces are small [40,44]. Household waste contains several types of plastic and is sorted into three pure polymeric fractions (i.e., PET bottles, PE and PP), two product types (i.e., PET trays and films) and one mixed plastics fraction [6].

- Industrial waste: This type of waste can either be sorted or left unsorted before being sent to recycling facilities. Plastic waste from businesses is usually a mono-stream, which is a waste stream of just one type of plastic.

- Deposit return scheme: By means of the aforementioned deposit return scheme, Dutch citizens are incentivized to recycle PET bottles (greater than 50 cl) for which there is a deposit obligation. In 2021, small PET bottles were also added to this system [45]. The deposit return scheme is treated and registered as post-industrial packaging waste [44]. A ‘return packaging′ body, Stichting Retourverpakking Nederland (SRN), is responsible for the majority of producers, importers and supermarkets returning, sorting, and processing these plastic bottles. Nedvang reviews data received from the SRN and performs trend analyses. Two supermarkets have their own system for returnable bottles.

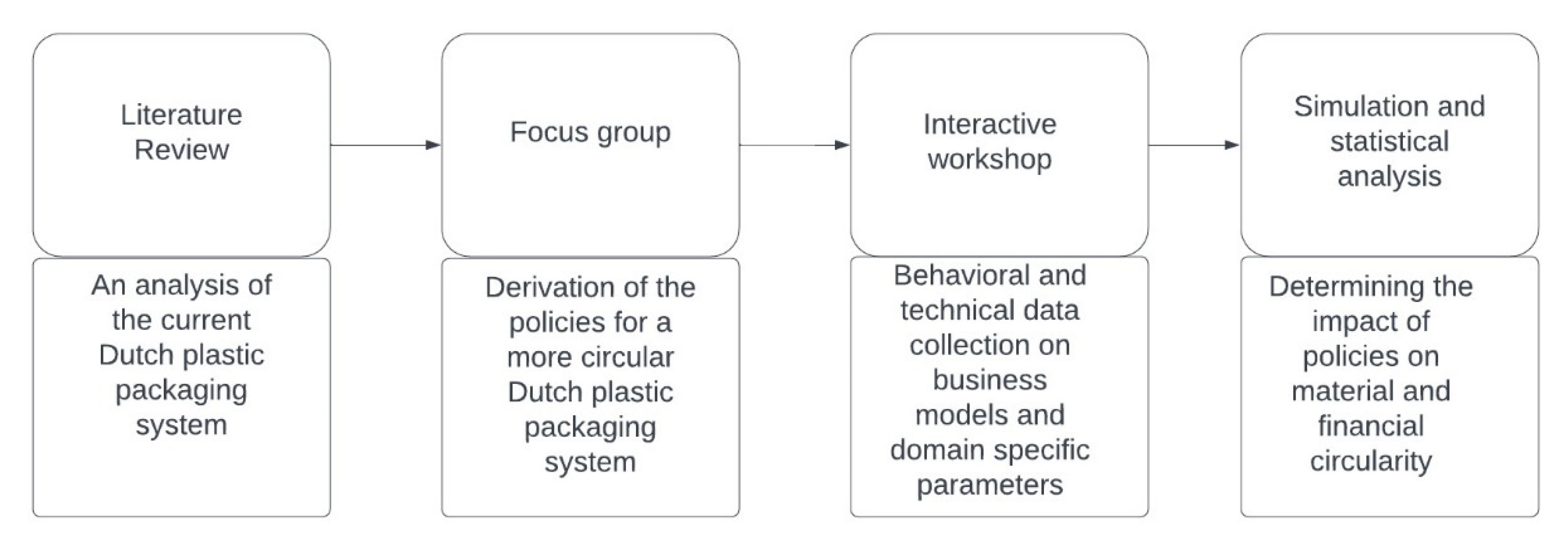

3. Data Collection and Research Method

3.1. Data Collection Phase I

- Policy 1: Quadrupling the incineration fee;

- Policy 2: Establishing a center of excellence that specifically supports SMEs in their research and development (R&D) efforts, the development of technical expertise (e.g., common labelling and chemical marking aligned with standardised separation and sorting systems), and access to state-of-the-art facilities for plastic packaging treatment;

- Policy 3: The amount producers and importers of plastic packaged goods pay in waste management tax to Afvalfonds Verpakkingen is halved for recycled plastic packaging and doubled for non-recycled plastic packaging.

3.2. Data Collection Phase II

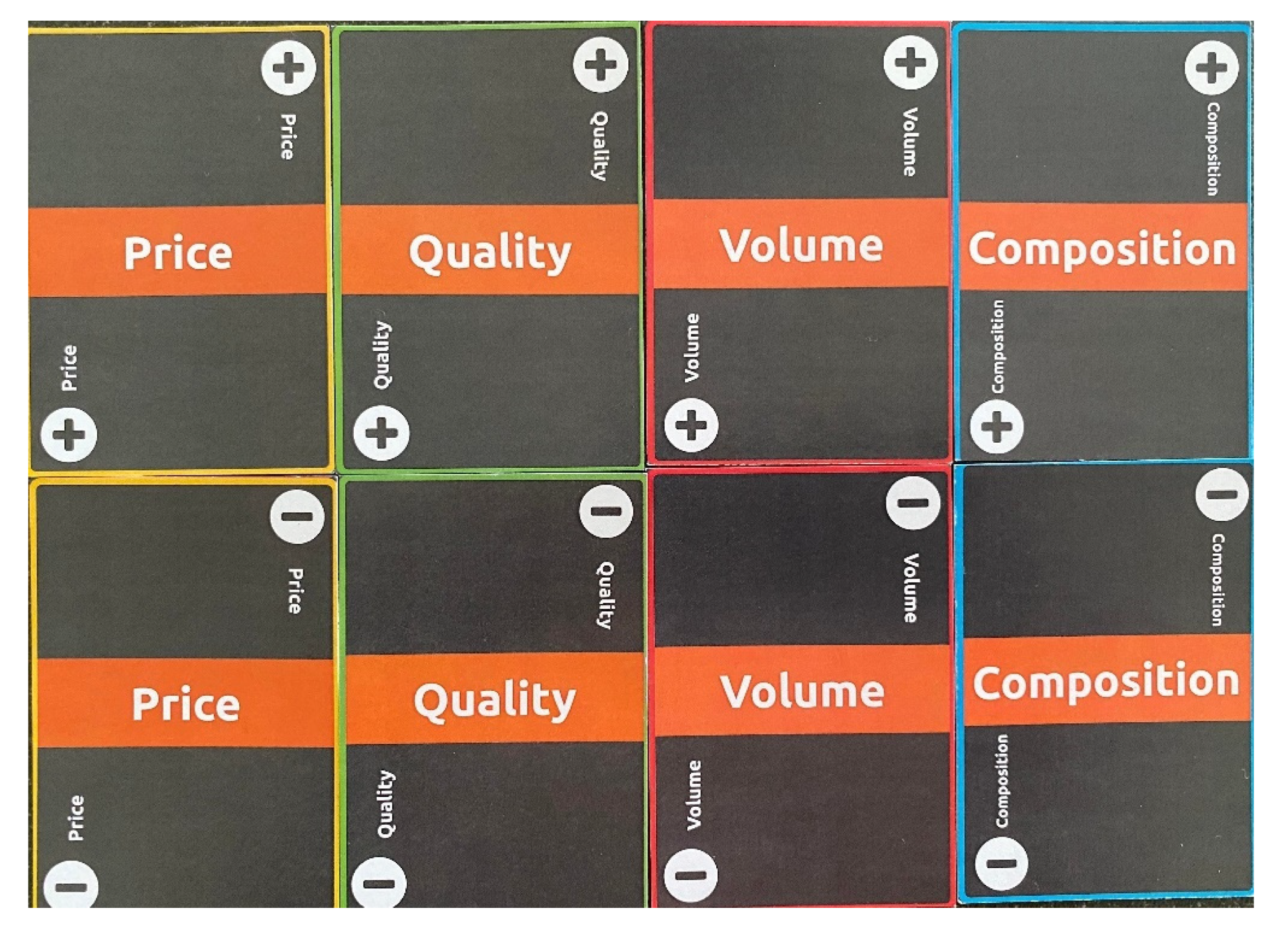

- Game board: A visual representation of the plastic packaging value chain, showing material and monetary flows between the stakeholders and the position and role of the stakeholders within the system;

- Business model and flow cards: Participants were given sets of business model and flow cards which they used to indicate the expected impact of a specific policy on their business models and the quality, composition, volume, and price of their input and output flow. The business model cards represented the nine building blocks of a business model canvas [50], with an extra card for the sustainability effect of each introduced policy. The participants used the flow cards to communicate an increase or decrease in the above-mentioned impact areas (quality, composition, etc.). The business model and flow cards used can be seen in Figure 2 and Figure 3, respectively, below:

3.3. The Computer Simulation and Statistical Analyses

4. Results

4.1. The Effects of Policy 1 on the Business Models

4.2. The Effects of Policy 1 on Material and Financial Circularity

4.3. The Effects of Policy 2 on the Business Models

4.4. The Effects of Policy 2 on Material and Financial Circularity

4.5. The Effects of Policy 3 on the Business Models

4.6. The Effects of Policy 3 on Material and Financial Circularity

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Status Quo Business Models

- The Plastic Packaging Producer

- The Brand Owner

- The Waste Collector

- The Post-Separator

- The Waste Sorting Company

- The Recycling Company

- The Incinerator Company

References

- Guglielmi, G. In the Next 30 Years, We’ll Make Four Times More Plastic Waste than We Ever Have. 2017. Available online: https://www.science.org/content/article/next-30-years-we-ll-make-four-times-more-plastic-waste-we-ever-have (accessed on 26 March 2022).

- Bressanelli, G.; Adrodegari, F.; Pigosso, D.C.A.; Parida, V. Towards the Smart Circular Economy Paradigm: A Definition, Conceptualization, and Research Agenda. Sustainability 2022, 14, 4960. [Google Scholar] [CrossRef]

- Al-Salem, S.M.; Lettieri, P.; Baeyens, J. The Valorization of Plastic Solid Waste (PSW) by Primary to Quaternary Routes: From Re-Use to Energy and Chemicals. Prog. Energy Combust. Sci. 2010, 36, 103–129. [Google Scholar] [CrossRef]

- Calisto Friant, M.; Lakerveld, D.; Vermeulen, W.J.V.; Salomone, R. Transition to a Sustainable Circular Plastics Economy in The Netherlands: Discourse and Policy Analysis. Sustainability 2021, 14, 190. [Google Scholar] [CrossRef]

- Ragaert, K.; Delva, L.; Van Geem, K. Mechanical and Chemical Recycling of Solid Plastic Waste. Waste Manag. 2017, 69, 24–58. [Google Scholar] [CrossRef]

- Picuno, C.; Van Eygen, E.; Brouwer, M.T.; Kuchta, K.; Thoden van Velzen, E.U. Factors Shaping the Recycling Systems for Plastic Packaging Waste—A Comparison between Austria, Germany and The Netherlands. Sustainability 2021, 13, 6772. [Google Scholar] [CrossRef]

- Vollmer, I.; Jenks, M.J.F.; Roelands, M.C.P.; White, R.J.; Harmelen, T.; Wild, P.; Laan, G.P.; Meirer, F.; Keurentjes, J.T.F.; Weckhuysen, B.M. Beyond Mechanical Recycling: Giving New Life to Plastic Waste. Angew. Chem. Int. Ed. 2020, 59, 15402–15423. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Eze, W.U.; Umunakwe, R.; Obasi, H.C.; Ugbaja, M.I.; Uche, C.C.; Madufor, I.C. Plastics Waste Management: A Review of Pyrolysis Technology. Clean Technol. Recycl. 2021, 1, 50–69. [Google Scholar] [CrossRef]

- Gradus, R. Postcollection Separation of Plastic Recycling and Design-For-Recycling as Solutions to Low Cost-Effectiveness and Plastic Debris. Sustainability 2020, 12, 8415. [Google Scholar] [CrossRef]

- Moad, G.; Solomon, D.H. The Critical Importance of Adopting Whole-of-Life Strategies for Polymers and Plastics. Sustainability 2021, 13, 8218. [Google Scholar] [CrossRef]

- Bucknall, D.G. Plastics as a Materials System in a Circular Economy. Philos. Trans. R. Soc. A 2020, 378, 20190268. [Google Scholar] [CrossRef]

- Mah, A. Future-Proofing Capitalism: The Paradox of the Circular Economy for Plastics. Global Environ. Polit. 2021, 21, 121–142. [Google Scholar] [CrossRef]

- Polymer Comply Europe. The Usage of Recycled Plastic Materials by Plastic Converters in Europe. (2nd ed.). 2019. Available online: https://www.ahpi.gr/wp-content/uploads/2019/01/PCE-Report-2nd-EuPC-Survey-on-the-Use-of-rPM-by-European-Plastics-Converters-v.1_compressed.pdf (accessed on 23 March 2022).

- Eriksen, M.K.; Christiansen, J.D.; Daugaard, A.E.; Astrup, T.F. Closing the Loop for PET, PE and PP Waste from Households: Influence of Material Properties and Product Design for Plastic Recycling. Waste Manag. 2019, 96, 75–85. [Google Scholar] [CrossRef] [PubMed]

- Brouwer, M.; Picuno, C.; Thoden van Velzen, E.U.; Kuchta, K.; De Meester, S.; Ragaert, K. The Impact of Collection Portfolio Expansion on Key Performance Indicators of the Dutch Recycling System for Post-Consumer Plastic Packaging Waste, a Comparison between 2014 and 2017. Waste Manag. 2019, 100, 112–121. [Google Scholar] [CrossRef] [PubMed]

- Thoden van Velzen, E.U.; Brouwer, M.T.; Feil, A. Collection Behaviour of Lightweight Packaging Waste by Individual Households and Implications for the Analysis of Collection Schemes. Waste Manag. 2019, 89, 284–293. [Google Scholar] [CrossRef]

- Hahladakis, J.N.; Iacovidou, E. Closing the Loop on Plastic Packaging Materials: What Is Quality and How Does It Affect Their Circularity? Sci. Total Environ. 2018, 630, 1394–1400. [Google Scholar] [CrossRef] [PubMed]

- Brouwer, M.T.; Thoden van Velzen, E.U.; Ragaert, K.; ten Klooster, R. Technical Limits in Circularity for Plastic Packages. Sustainability 2020, 12, 10021. [Google Scholar] [CrossRef]

- Verrips, A.; Hoogendoorn, S.; Jansema-Hoekstra, K.; Romijn, G. The Circular Economy of Plastics in the Netherlands. In Environmental Sustainability and Education for Waste Management, Education for Sustainability; So, W.W.M., Chow, C.F., Lee, J.C.K., Eds.; Springer: Singapore, 2019; pp. 43–56. ISBN 9789811391729. [Google Scholar]

- World Economic Forum; Ellen MacArthur Foundation; McKinsey & Company. The New Plastics Economy: Rethinking the Future of Plastics. 2016. Available online: https://emf.thirdlight.com/link/faarmdpz93ds-5vmvdf/@/preview/1?o (accessed on 23 March 2022).

- Rabobank Industry Analysis. Unpacking the Dutch Plastics Packaging Industry. Available online: https://silo.tips/download/unpacking-the-dutch-plastics-packaging-industry (accessed on 23 March 2022).

- Grand View Research Plastic Packaging Market Size, Share & Trends Analysis Report by Product (Flexible, Rigid), by Technology (Extrusion, Thermoforming), by Application (Food & Beverages, Pharmaceuticals), and Segment Forecasts, 2021–2028. Available online: https://www.grandviewresearch.com/industry-analysis/plastic-packaging-market# (accessed on 23 March 2022).

- OECD. Improving Plastics Management: Trends, policy responses, and the role of international co-operation and trade. OECD Environ. Policy Pap. 2018, 12, 20. [Google Scholar] [CrossRef]

- Geyer, R.; Jambeck, J.R.; Law, K.L. Production, Use, and Fate of All Plastics Ever Made. Sci. Adv. 2017, 3, e1700782. [Google Scholar] [CrossRef] [Green Version]

- Su, Y.; Duan, H.; Wang, Z.; Song, G.; Kang, P.; Chen, D. Characterizing the Environmental Impact of Packaging Materials for Express Delivery via Life Cycle Assessment. J. Clean. Prod. 2020, 274, 122961. [Google Scholar] [CrossRef]

- Arunan, I.; Crawford, R.H. Greenhouse Gas Emissions Associated with Food Packaging for Online Food Delivery Services in Australia. Resour. Conserv. Recycl. 2021, 168, 105299. [Google Scholar] [CrossRef]

- Klein Lankhorst, H. Sustainable Packaging, the Dutch Way. Available online: https://vdocument.in/sustainable-packaging-the-dutch-way-sustainable-packaging-the-dutch-way-hester.html (accessed on 23 March 2022).

- Afvalfonds Verpakkingen. Monitoring Verpakkingen: Resultaten Inzameling en Recycling. 2018. Available online: https://afvalfondsverpakkingen.nl/a/i/Monitoring-Verpakkingen-Resultaten-inzameling-en-recycling-2018.pdf (accessed on 23 March 2022).

- KIDV; Natuur & Milieu; CE Delft. Factcheck Plastic Recycling. Available online: https://kidv.nl/media/publicaties/factcheck-plastic-recycling-in-nederland-deft.pdf?1.2.4 (accessed on 23 March 2022).

- Bishop, G.; Styles, D.; Lens, P.N.L. Recycling of European Plastic Is a Pathway for Plastic Debris in the Ocean. Environ. Int. 2020, 142, 105893. [Google Scholar] [CrossRef] [PubMed]

- Brooks, A.L.; Wang, S.; Jambeck, J.R. The Chinese Import Ban and Its Impact on Global Plastic Waste Trade. Sci. Adv. 2018, 4, eaat0131. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bergsma, G.; Bijleveld, M. LCA: Recycling of Plastic Packaging Waste from Households. Available online: https://cedelft.eu/publications/lca-recycling-of-household-plastic-packaging-waste/ (accessed on 23 March 2022).

- Gradus, R.; van Koppen, R.; Dijkgraaf, E.; Nillesen, P.A. Cost-Effectiveness Analysis for Incineration or Recycling of Dutch Household Plastics. (TI 2016-039/VI Tinbergen Institute Discussion Paper). 2016. Available online: https://papers.tinbergen.nl/16039.pdf (accessed on 23 March 2022).

- Bellacosa, L. Determinants of Pro Environmental Behaviour in a Circular Program for Plastic Packaging: A Case of Plastic Heroes in Amsterdam. Master’s Thesis, Erasmus University Rotterdam, Rotterdam, The Netherlands, 2017. [Google Scholar]

- Hahladakis, J.N.; Iacovidou, E. An Overview of the Challenges and Trade-Offs in Closing the Loop of Post-Consumer Plastic Waste (PCPW): Focus on Recycling. J. Hazard. Mater. 2019, 380, 120887. [Google Scholar] [CrossRef] [PubMed]

- European Comission. A European Strategy For Plastics in a Circular Economy. Available online: https://www.europarc.org/wp-content/uploads/2018/01/Eu-plastics-strategy-brochure.pdf (accessed on 23 March 2022).

- European Comission Closing the Loop—An EU Action Plan for the Circular Economy. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:8a8ef5e8-99a0-11e5-b3b7-01aa75ed71a1.0012.02/DOC_1&format=PDF (accessed on 23 March 2022).

- VNG. Nieuwe Afspraken Raamovereenkomst Verpakkingen 2013–2022. Available online: https://vng.nl/sites/default/files/2019-11/20190906_ledenbrief_nieuwe-afspraken-raamovereenkomst-verpakkingen-2013-2022.pdf (accessed on 23 March 2022).

- Thoden van Velzen, E.U.; Bos-Brouwers, H.E.J.; Groot, J.J.; Bing, X.; Jansen, M.; Luijsterburg, B. Scenarios Study on Post-Consumer Plastic Packaging Waste Recycling; Wageningen UR Food & Biobased Research Rapport 1408; Wageningen UR; Wageningen UR: Wageningen, The Netherlands, 2013. [Google Scholar]

- Cimpan, C.; Maul, A.; Jansen, M.; Pretz, T.; Wenzel, H. Central Sorting and Recovery of MSW Recyclable Materials: A Review of Technological State-of-the-Art, Cases, Practice and Implications for Materials Recycling. J. Environ. Manag. 2015, 156, 181–199. [Google Scholar] [CrossRef]

- Afvalfonds Verpakkingen. Packaging Waste Management Contribution. Available online: https://afvalfondsverpakkingen.nl/en/packaging-waste-management-contribution (accessed on 23 March 2022).

- Brouwer, M.T.; Thoden van Velzen, E.U.; Augustinus, A.; Soethoudt, H.; De Meester, S.; Ragaert, K. Predictive Model for the Dutch Post-Consumer Plastic Packaging Recycling System and Implications for the Circular Economy. Waste Manag. 2018, 71, 62–85. [Google Scholar] [CrossRef] [Green Version]

- Feil, A.; Pretz, T.; Jansen, M.; Thoden van Velzen, E.U. Separate Collection of Plastic Waste, Better than Technical Sorting from Municipal Solid Waste? Waste Manag. Res. 2017, 35, 172–180. [Google Scholar] [CrossRef]

- Bing, X.; Bloemhof-Ruwaard, J.M.; van der Vorst, J.G.A.J. Sustainable Reverse Logistics Network Design for Household Plastic Waste. Flex. Serv. Manuf. J. 2014, 26, 119–142. [Google Scholar] [CrossRef]

- Thoden van Velzen, E.U.; Smeding, I.; Brouwer, M.T.; Maaskant, E. Comparison of the Quality of Mechanically Recycled Plastics Made from Separately Collected and Mechanically Recovered Plastic Packaging Waste. Waste to Resources 2021 Conference, Hanover Germany, May. 2021. Available online: https://www.researchgate.net/publication/351746182_Comparison_of_the_quality_of_mechanically_recycled_plastics_made_from_separately_collected_and_mechanically_recovered_plastic_packaging_waste (accessed on 23 March 2022).

- Picuno, C.; Alassali, A.; Chong, Z.K.; Kuchta, K. Flows of Post-Consumer Plastic Packaging in Germany: An MFA-Aided Case Study. Resour. Conserv. Recyc. 2021, 169, 105515. [Google Scholar] [CrossRef]

- Machado Leitão, T.; Lima Navarro, L.L.; Flórido Cameira, R.; Silva, E.R. Serious Games in Business Process Management: A Systematic Literature Review. Bus. Proc. Manag. J. 2021, 27, 685–721. [Google Scholar] [CrossRef]

- Serranti, S.; Bonifazi, G. Techniques for Separation of Plastic Wastes. In Use of Recycled Plastics in Eco-Efficient Concrete; Elsevier: Amsterdam, The Netherlands, 2019; pp. 9–37. ISBN 978-0-08-102676-2. [Google Scholar]

- Lanezki, M.; Siemer, C.; Wehkamp, S. “Changing the Game—Neighbourhood”: An Energy Transition Board Game, Developed in a Co-Design Process: A Case Study. Sustainability 2020, 12, 10509. [Google Scholar] [CrossRef]

- Manshoven, S.; Gillabel, J. Learning through Play: A Serious Game as a Tool to Support Circular Economy Education and Business Model Innovation. Sustainability 2021, 13, 13277. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y.; Clark, T. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; Wiley: Hoboken, NJ, USA, 2010; ISBN 978-0-470-87641-1. [Google Scholar]

- KIDV. Plastics Chain. Available online: https://kidv.nl/kunststofketen (accessed on 23 March 2022).

- Cramer, J. Key Drivers for High-Grade Recycling under Constrained Conditions. Recycling 2018, 3, 16. [Google Scholar] [CrossRef] [Green Version]

- Forrest, A.; Giacovazzi, L.; Dunlop, S.; Reisser, J.; Tickler, D.; Jamieson, A.; Meeuwig, J.J. Eliminating Plastic Pollution: How a Voluntary Contribution From Industry Will Drive the Circular Plastics Economy. Front. Mar. Sci. 2019, 6, 627. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Material Circularity (%) | Financial Circularity (%) | |

|---|---|---|

| Status quo | 29.63 | 36.17 |

| Policy 1 | 25.71 | 38.69 |

| Policy 2 | 36.89 | 48.48 |

| Policy 3 | 31.84 | 40.29 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Çevikarslan, S.; Gelhard, C.; Henseler, J. Improving the Material and Financial Circularity of the Plastic Packaging Value Chain in The Netherlands: Challenges, Opportunities, and Implications. Sustainability 2022, 14, 7404. https://doi.org/10.3390/su14127404

Çevikarslan S, Gelhard C, Henseler J. Improving the Material and Financial Circularity of the Plastic Packaging Value Chain in The Netherlands: Challenges, Opportunities, and Implications. Sustainability. 2022; 14(12):7404. https://doi.org/10.3390/su14127404

Chicago/Turabian StyleÇevikarslan, Salih, Carsten Gelhard, and Jörg Henseler. 2022. "Improving the Material and Financial Circularity of the Plastic Packaging Value Chain in The Netherlands: Challenges, Opportunities, and Implications" Sustainability 14, no. 12: 7404. https://doi.org/10.3390/su14127404

APA StyleÇevikarslan, S., Gelhard, C., & Henseler, J. (2022). Improving the Material and Financial Circularity of the Plastic Packaging Value Chain in The Netherlands: Challenges, Opportunities, and Implications. Sustainability, 14(12), 7404. https://doi.org/10.3390/su14127404