Greenhouse Gas Emissions in the Industrial Processes and Product Use Sector of Saudi Arabia—An Emerging Challenge

,

,

,

,  , , ,

, , ,  and

and

Abstract

:1. Introduction

2. Methodology

2.1. Data Sources

2.2. GHG Emission Estimation

3. Results

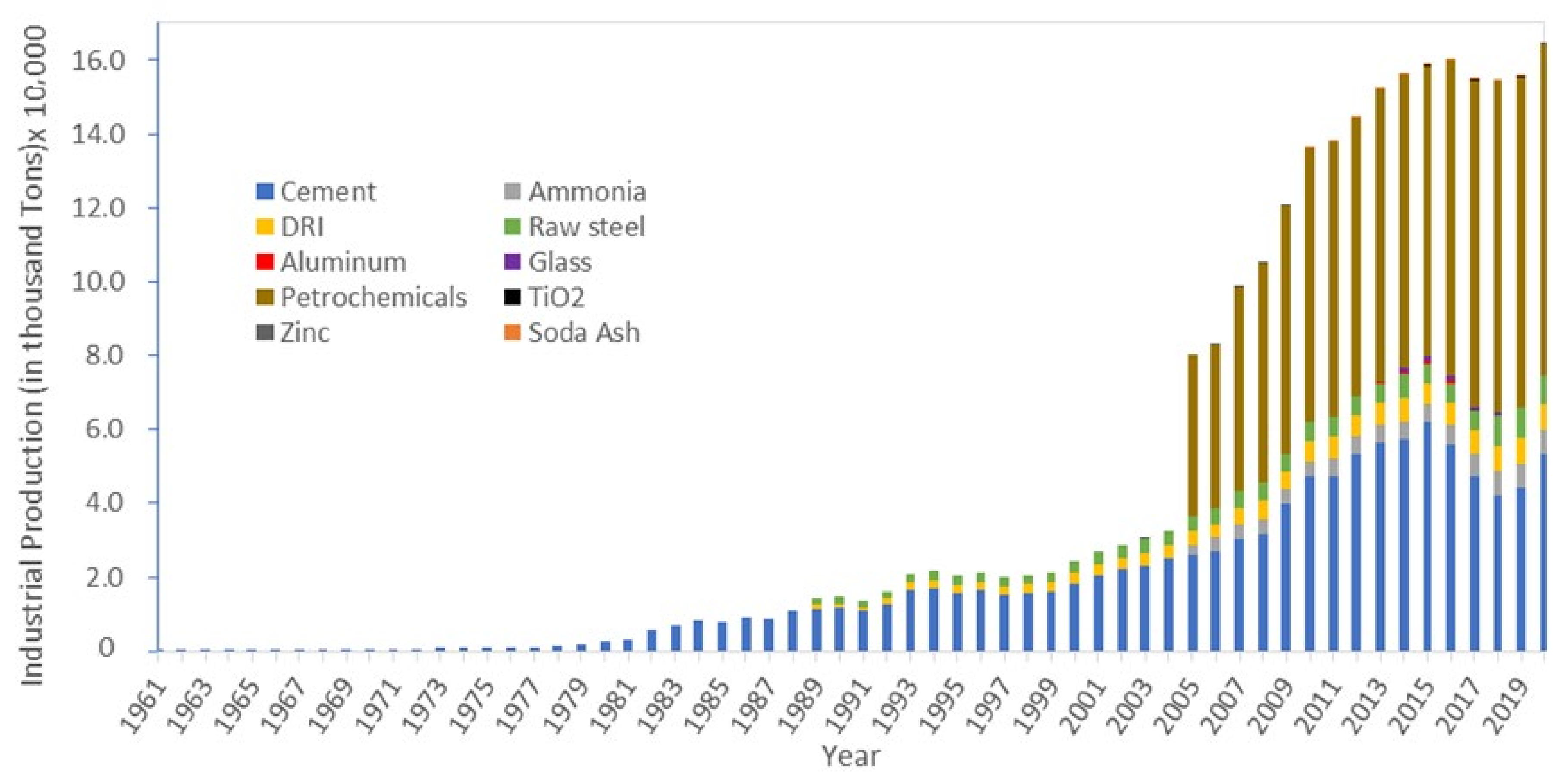

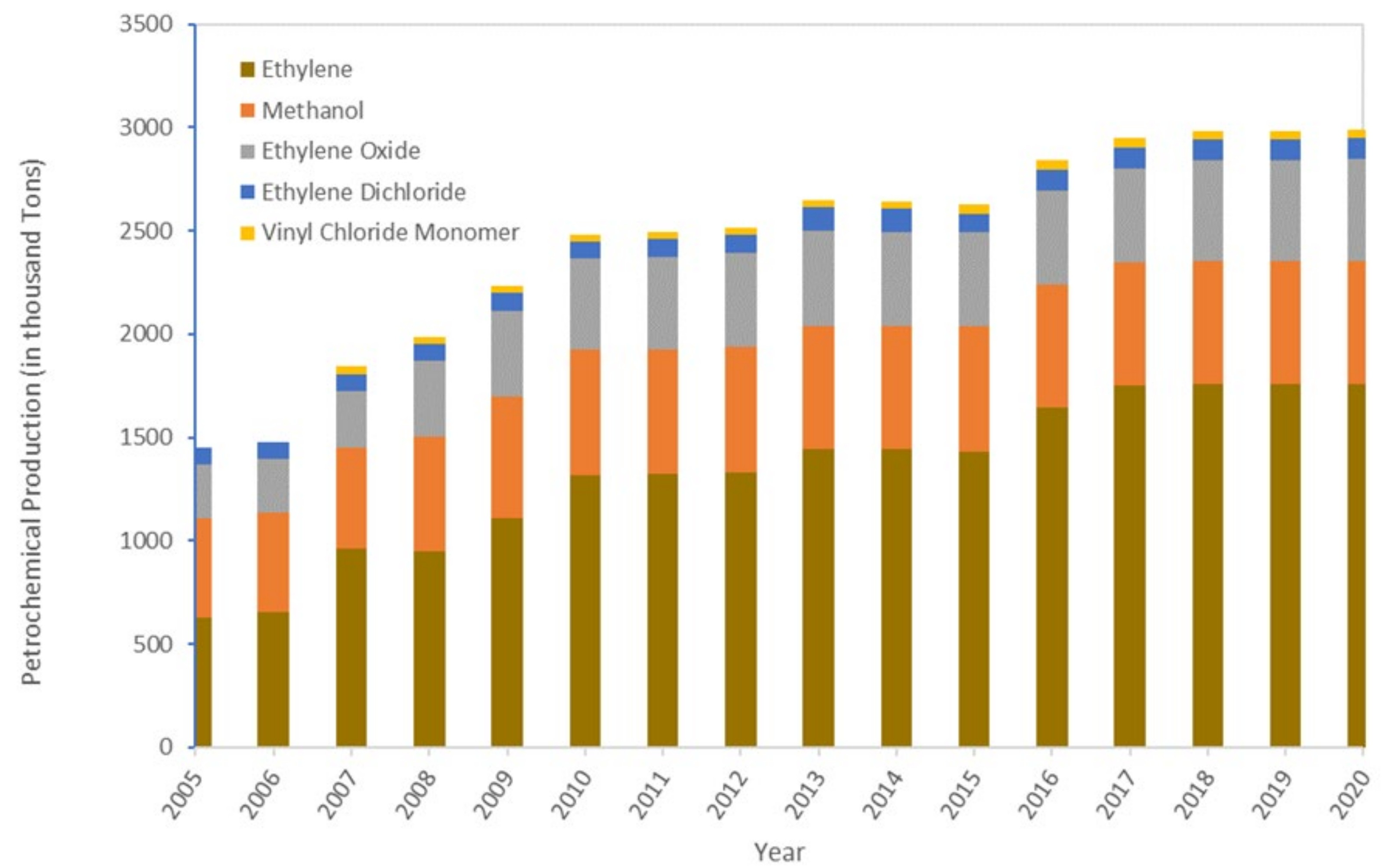

3.1. Evolution of the IPPU Sector

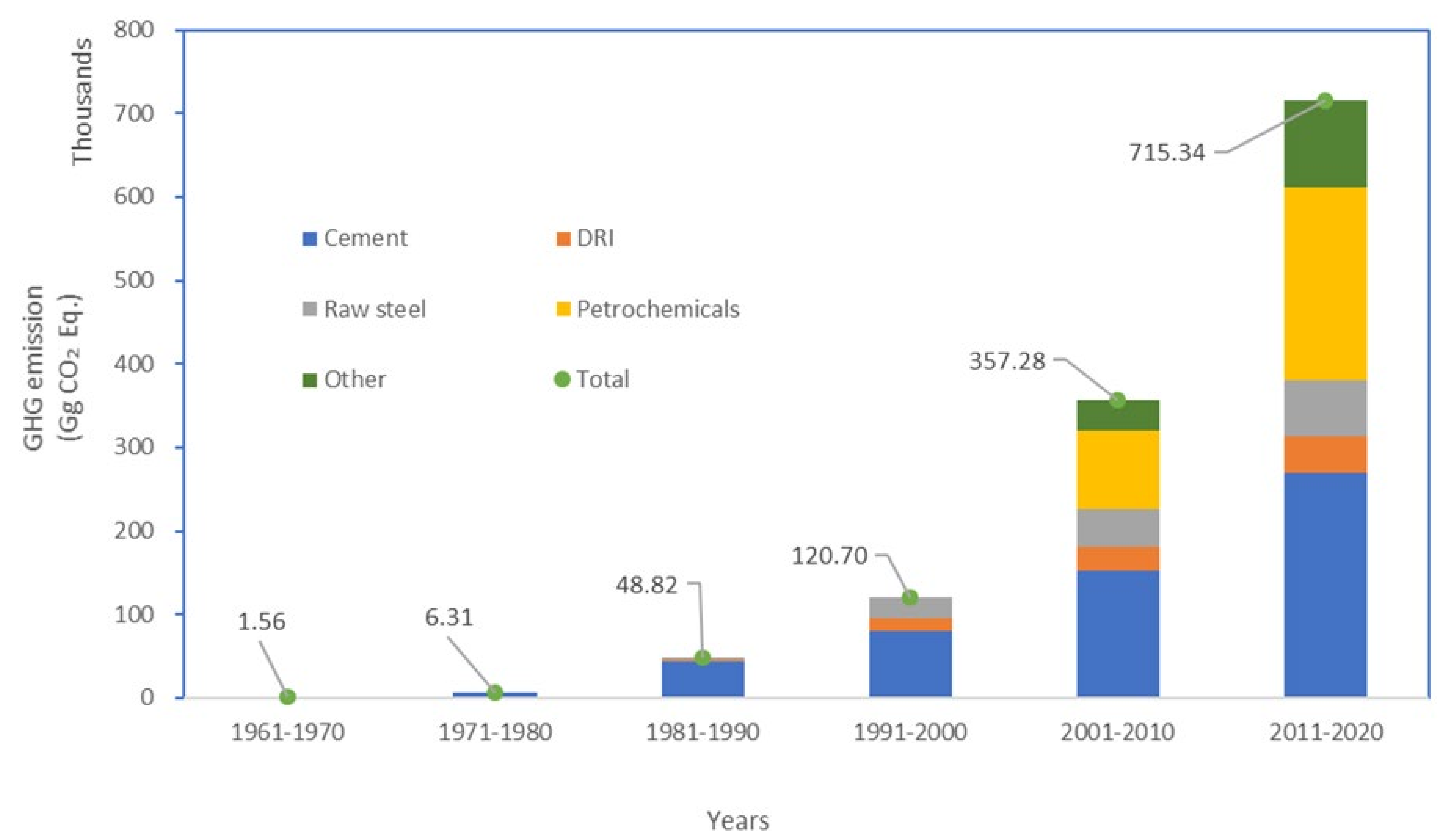

3.2. Historical GHG Emissions from the IPPU Sector

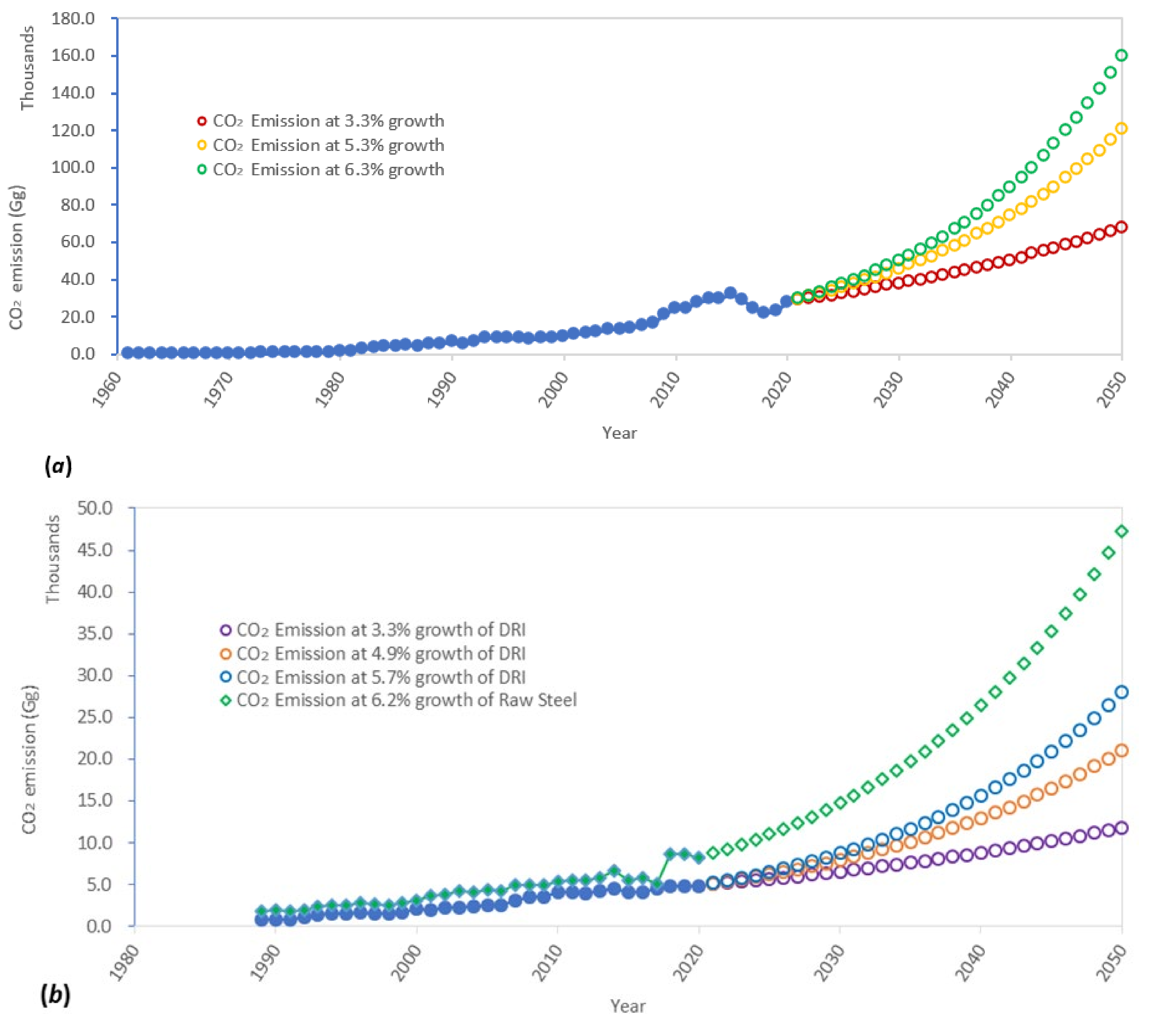

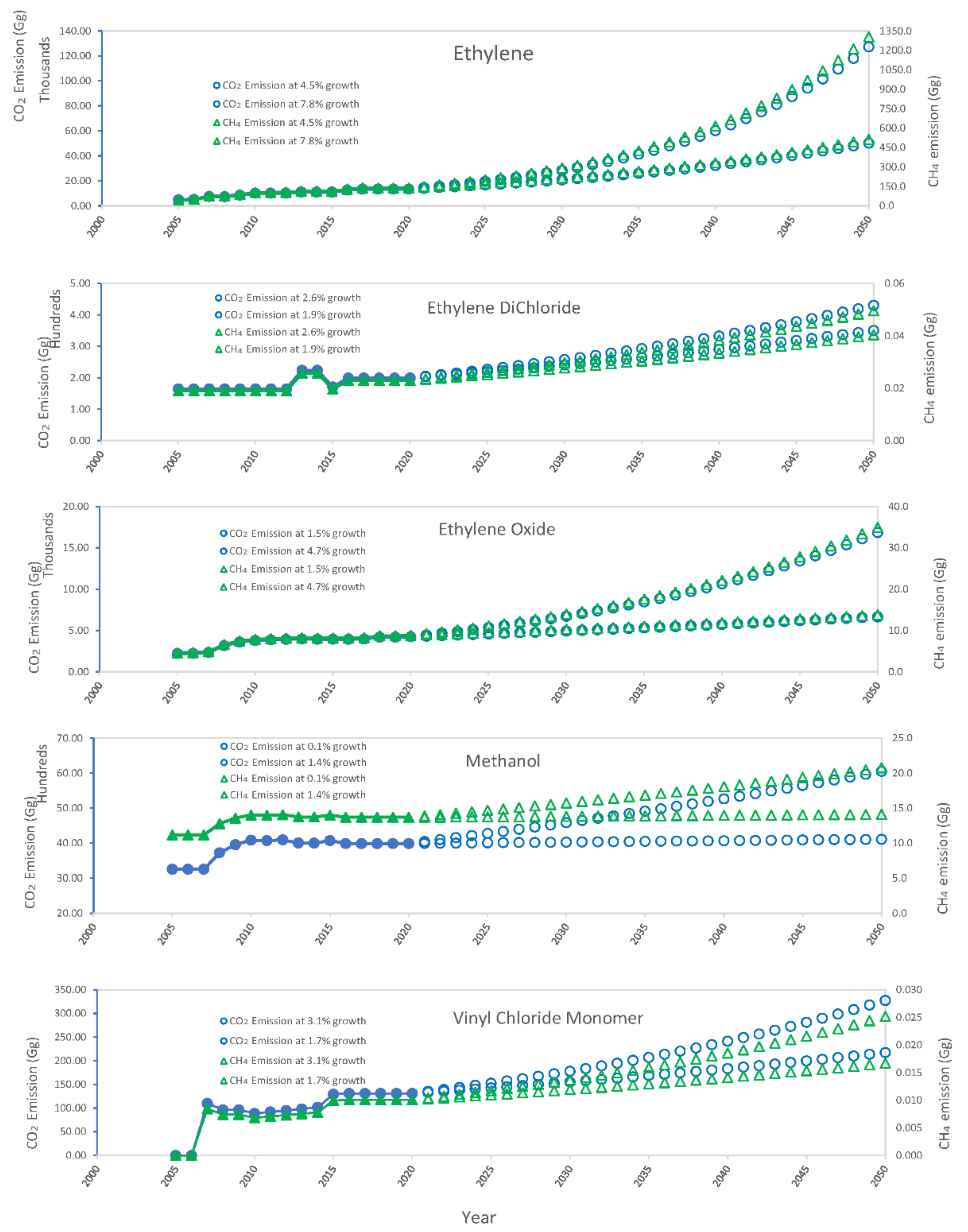

3.3. Prediction of GHG Emissions

4. Discussion

4.1. Energy Efficiency

4.2. Emissions Efficiency

4.3. Efficiency of Material in Production Process

- Reducing material, manufacturing, and construction losses: Every year, about 10% of paper, 25% of steel, and 50% of aluminum is scrapped and recycled internally. Process changes and new design methodologies could reduce these losses [87].

- Reusing previously used materials: A comprehensive research study [86] determined that there are no prohibitive technological hurdles to recycling structural steel in construction, that there is a revenue possibility, and that the prospective supply is growing.

4.4. Material Efficiency in Product Design

4.5. Using Products More Intensively

4.6. Reducing Overall Demand for Product Services

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Bob, M.; Rahman, N.; Elamin, A.; Taher, S. Rising groundwater levels problem in urban areas: A case study from the Central Area of Madinah City, Saudi Arabia. Arab. J. Sci. Eng. 2016, 41, 1461–1472. [Google Scholar] [CrossRef]

- DNA. First Biannual Update Report (BUR), Saudi Arabia. 2018. Available online: https://cdmdna.gov.sa/ (accessed on 3 February 2022).

- Alshammari, Y.; Sarathy, S. Achieving 80% greenhouse gas reduction target in Saudi Arabia under low and medium oil prices. Energy Policy 2017, 101, 502–511. [Google Scholar] [CrossRef]

- Rahman, S.; Khondaker, A. Mitigation measures to reduce greenhouse gas emissions and enhance carbon capture and storage in Saudi Arabia. Renew. Sustain. Energy Rev. 2012, 16, 2446–2460. [Google Scholar] [CrossRef]

- Rahman, M.M.; Rahman, S.M.; Rahman, M.S.; Hasan, A.; Shoaib, S.A.; Rushd, S. Greenhouse Gas Emissions from Solid Waste Management in Saudi Arabia—Analysis of Growth Dynamics and Mitigation Opportunities. Appl. Sci. 2021, 11, 1737. [Google Scholar] [CrossRef]

- Ikram, M.; Zhang, Q.; Sroufe, R.; Shah, S. Towards a sustainable environment: The nexus between ISO 14001, renewable energy consumption, access to electricity, agriculture and CO2 emissions in SAARC. Sustain. Prod. Consum. 2020, 22, 218–230. [Google Scholar] [CrossRef]

- Omri, A.; Euchi, J.; Hasaballah, A.; Al-Tit, A. Determinants of environmental sustainability: Evidence from Saudi Arabia. Sci. Total Environ. 2019, 657, 1592–1601. [Google Scholar] [CrossRef]

- Alshuwaikhat, H.; Mohammed, I. Sustainability matters in national development visions—Evidence from Saudi Arabia’s Vision for 2030. Sustainability 2017, 9, 408. [Google Scholar] [CrossRef] [Green Version]

- Ikram, M.; Ferasso, M.; Sroufe, R.; Zhang, Q. Assessing green technology indicators for cleaner production and sustainable investments in a developing country context. J. Clean. Prod. 2021, 322, 129090. [Google Scholar] [CrossRef]

- Kyriakopoulos, L.; Ikram, M.; Sroufe, R.; Awan, U.; Abid, N. Enabling progress in developing economies: A novel hybrid decision-making model for green technology planning. Sustainability 2021, 14, 258. [Google Scholar] [CrossRef]

- Akadiri, A.; Akadiri, S.S.; Gungor, H. The role of natural gas consumption in Saudi Arabia’s output and its implication for trade and environmental quality. Energy Policy 2019, 129, 230–238. [Google Scholar] [CrossRef]

- USEIA. U.S. Energy Information Administration. 2020. Available online: https://www.eia.gov/international/data/world#/?tl_type=p&tl_id=2-A&pa=0000000000002&ct=0&ord=SA&c=ruvvvvvfvtvnvv1urvvvvfvvvvvvfvvvou20evvvvvvvvvnvvuvo&f=A (accessed on 3 February 2022).

- Liu, Z.; Dong, H.; Geng, Y.; Lu, C.; Ren, W. Insights into the regional greenhouse gas (GHG) emission of industrial processes: A case study of Shenyang, China. Sustainability 2015, 6, 3669–3685. [Google Scholar] [CrossRef] [Green Version]

- Dong, X.; Guo, J.; Höök, M.; Pi, G. Sustainability assessment of the natural gas industry in China using principal component analysis. Sustainability 2008, 7, 6102–6118. [Google Scholar] [CrossRef] [Green Version]

- Arruda, L.R.; de Jesus Lameira, V.; Quelhas, O.L.G.; Pereira, F.N. Sustainability in the Brazilian heavy construction industry: An analysis of organizational practices. Sustainability 2013, 5, 4312–4328. [Google Scholar] [CrossRef] [Green Version]

- Dentoni, V.; Grosso, B.; Massacci, G. Environmental sustainability of the alumina industry in Western Europe. Sustainability 2014, 6, 9477–9493. [Google Scholar] [CrossRef] [Green Version]

- Duan, Y.; Mu, H.; Li, N.; Rosen, M.A.; Wang, B.; Zhang, N. Analysis of the relationship between China’s IPPU CO2 emissions and the industrial economic growth. Sustainability 2016, 8, 426. [Google Scholar] [CrossRef] [Green Version]

- Ussiri, D.A.N.; Lal, R. Carbon Sequestration for Climate Change Mitigation and Adaptation; Springer International Publishing: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- NCEI. Global Climate Report-September 2021. Available online: https://www.ncei.noaa.gov/news/global-climate-202112 (accessed on 15 March 2022).

- Cadez, S.; Czerny, A. Carbon management strategies in manufacturing companies: An exploratory note. J. East Eur. Manag. Stud. 2010, 15, 348–360. [Google Scholar] [CrossRef] [Green Version]

- Cadez, S.; Czerny, A. Climate change mitigation strategies in carbon-intensive firms. J. Clean. Prod. 2016, 112, 4132–4143. [Google Scholar] [CrossRef]

- Cadez, S.; Guilding, C. Examining distinct carbon cost structures and climate change abatement strategies in CO2 polluting firms. Account. Audit. Account. J. 2017, 30, 1041–1064. [Google Scholar] [CrossRef]

- Cadez, S.; Czerny, A.; Letmathe, P. Stakeholder pressures and corporate climate change mitigation strategies. Bus. Strategy Environ. 2019, 28, 1–14. [Google Scholar] [CrossRef]

- UNFCC. The Intended Nationally Determined Contributions of the Kingdom of Saudi Arabia under the UNFCCC, Submitted to the UNFCCC Secretariat. Available online: https://andp.unescwa.org/sites/default/files/2021-10/KSA-INDCs%20English%5B1%5D.pdf (accessed on 15 March 2022).

- IPCC. 2006 IPCC Guidelines for National Greenhouse Gas Inventories. Available online: https://www.ipcc-nggip.iges.or.jp/public/2006gl/index.html (accessed on 15 March 2022).

- GASTAT (General Authority of Statistics). Kingdom of Saudi Arabia. Statistical Yearbooks. 2018. Available online: https://www.stats.gov.sa/en/46 (accessed on 15 March 2022).

- GPCA (Gulf Petrochemicals and Chemicals Association). 2020. Available online: https://www.gpca.org.ae/ (accessed on 15 March 2022).

- World Steel Association. Steel Statistical Yearbooks. 2020. Available online: https://worldsteel.org/steel-by-topic/statistics/steel-statistical-yearbook/ (accessed on 15 March 2022).

- USGS. U.S. Geological Survey-Africa and the Middle East. 2016. Available online: https://www.usgs.gov/centers/national-minerals-information-center/africa-and-middle-east#sa (accessed on 15 March 2022).

- Glass International. Glass Industry Worldwide-Statistics & Facts-Statista. 2018. Available online: https://www.statista.com/topics/4108/glass/#dossierKeyfigures (accessed on 15 March 2022).

- SAMA (Saudi Arabian Monetary Agency). 2020. Available online: https://sama.gov.sa/en-US/EconomicReports/Pages/AnnualReport.aspx (accessed on 15 March 2022).

- GASTAT (General Authority for Statistics). Statistical Year Books. 2019. Available online: https://www.stats.gov.sa/en/46 (accessed on 15 March 2022).

- CEIC. Saudi Arabia Cement Production. 2022. Available online: https://www.ceicdata.com/en/saudi-arabia/cement-production (accessed on 15 March 2022).

- IPCC. Revised 1996 IPCC Guidelines for National Greenhouse Gas Inventories. Available online: https://ci.nii.ac.jp/naid/10017506839/ (accessed on 15 March 2022).

- GPG. Good Practice Guidance and Uncertainty Management in National Greenhouse Gas Inventories. 2000. Available online: https://www.ipcc-nggip.iges.or.jp/public/gp/english/index.html (accessed on 15 March 2022).

- IPCC. 2006 IPCC Guidelines for National Greenhouse Gas Inventories Volume 3 Industrial Processes and Product Use. Available online: https://www.ipcc-nggip.iges.or.jp/public/2006gl/vol3.html (accessed on 15 March 2022).

- Roychoudhury, J. Saudi Arabian Cement Companies: Upgrading through Leveraging Overcapacity. 2020. Available online: https://www.kapsarc.org/research/publications/saudi-arabian-cement-companies-upgrading-through-leveraging-overcapacity/ (accessed on 15 March 2022).

- KAPSARC. The Future of the Petrochemicals Industry and Sino-Saudi Cooperation; KAPSARC: Riyadh, Saudi Arabia, 2020. [Google Scholar]

- Howarth, N.; Lanza, A.; AlShehri, T. Saudi Arabia’s 2018 CO2 Emissions Fall Faster Than Expected; KAPSARC: Riyadh, Saudi Arabia, 2020. [Google Scholar]

- Dasgupta, S.P.P.; Roy, J.; Bera, A.; Sharma, A. Growth accounting for six energy intensive industries in India. J. Ind. Stat. 2012, 1, 1–15. [Google Scholar]

- Allwood, J.M.; Cullen, J.M.; Milford, R.L. Options for achieving a 50% cut in industrial carbon emissions by 2050. Environ. Sci. Technol. 2010, 44, 1888–1894. [Google Scholar] [CrossRef] [PubMed]

- Schafer, A. Structural Change in Energy Use. Energy Policy 2005, 33, 429–437. [Google Scholar] [CrossRef]

- Saygin, D.; Patel, M.K.; Worrell, E.; Tam, C.; Gielen, D.J. Potential of best practice technology to improve energy efficiency in the global chemical and petrochemical sector. Energy 2011, 36, 5779–5790. [Google Scholar] [CrossRef]

- Gutowski, T.G.; Sahni, S.; Allwood, J.M.; Ashby, M.F.; Worrell, E. The energy required to produce materials: Constraints on energy-intensity improvements, parameters of demand. Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 2013, 371, 20120003. [Google Scholar] [CrossRef] [PubMed]

- Masanet, E.R. Energy benefits of electronic controls at small and medium sized U.S. manufacturers. J. Ind. Ecol. 2010, 14, 696–702. [Google Scholar] [CrossRef]

- DoE, U. Waste Heat Reduction and Recovery for Improving Furnace Efficiency, Productivity and Emissions Performance. Available online: https://www.energy.gov/sites/prod/files/2014/05/f15/35876.pdf (accessed on 2 February 2022).

- DoE, U. Waste Heat Recovery: Technology Opportunities in the US Industry. Available online: https://www1.eere.energy.gov/manufacturing/intensiveprocesses/pdfs/waste_heat_recovery.pdf (accessed on 2 February 2022).

- Plastics Europe. Plastics—The Facts 2021. Available online: https://plasticseurope.org/wp-content/uploads/2021/12/Plastics-the-Facts-2021-web-final.pdf (accessed on 2 February 2022).

- Sardeshpande, V.; Gaitonde, U.N.; Banerjee, R. Model based energy benchmarking for glass furnace. Energy Convers. Manag. 2007, 48, 2718–2738. [Google Scholar] [CrossRef]

- Dosho, Y. Sustainable concrete waste recycling. Proc. Ice-Constr. Mater. 2008, 161, 47–62. [Google Scholar] [CrossRef]

- Matar, W.; Murphy, F.; Pierru, A.; Rioux, B.; Wogan, D. Efficient industrial energy use: The first step in transitioning Saudi Arabia’s energy mix. Energy Policy 2017, 105, 80–92. [Google Scholar] [CrossRef]

- DNA (Saudi Designated National Authority). Third National Communication of Saudi Arabia. Available online: https://unfccc.int/files/national_reports/non-annex_i_natcom/application/pdf/saudi_arabia_nc3_22_dec_2016.pdf (accessed on 2 February 2022).

- Saudi Aramco. Citizenship Report. Available online: http://argaamplus.s3.amazonaws.com/3cf5161a-240e-4aa0-adc5-a16c618a2ab5.pdf (accessed on 2 February 2022).

- Saudi Aramco. Annual Review. Available online: https://www.aramco.com/-/media/publications/corporate-reports/ar-2014-saudiaramco-english-full.pdf (accessed on 3 February 2022).

- IEA. Iron and Steel Technology Roadmap. 2020. Available online: https://www.oecd-ilibrary.org/energy/iron-and-steel-technology-roadmap_3dcc2a1b-en (accessed on 3 February 2022).

- Talaei, A.; Ahiduzzaman, M.; Davis, M.; Gemechu, E.; Kumar, A. Potential for energy efficiency improvement and greenhouse gas mitigation in Canada’s iron and steel industry. Energy Effic. 2020, 13, 1213–1243. [Google Scholar] [CrossRef]

- Arvedi, G.; Mazzolari, F.; Bianchi, A.; Holleis, G.; Siegl, J.; Angerbauer, A. The Arvedi Endless Strip Production line (ESP): From liquid steel to hot-rolled coil in seven minutes. Rev. Métallurgie 2008, 105, 398–407. [Google Scholar] [CrossRef]

- Vogl, V.; Åhman, M.; Nilsson, L.J. Assessment of hydrogen direct reduction for fossil-free steelmaking. J. Clean. Prod. 2018, 203, 736–745. [Google Scholar] [CrossRef]

- Fischedick, M.; Marzinkowski, J.; Winzer, P.; Weigel, M. Techno-economic evaluation of innovative steel production technologies. J. Clean. Prod. 2014, 84, 563–580. [Google Scholar] [CrossRef] [Green Version]

- Hasanbeigi, A.; Price, L.K.; McKane, A.T. The State-of-the-Art Clean Technologies (SOACT) for Steelmaking Handbook. Available online: https://www.jisf.or.jp/business/ondanka/eco/docs/SOACT-Handbook-2nd-Edition.pdf (accessed on 3 February 2022).

- Hasanbeigi, A.; Arens, M.; Price, L. Alternative emerging ironmaking technologies for energy-efficiency and carbon dioxide emissions reduction: A technical review. Renew. Sustain. Energy Rev. 2014, 33, 645–658. [Google Scholar] [CrossRef]

- Talaei, A.; Pier, D.; Iyer, A.V.; Ahiduzzaman, M.; Kumar, A. Assessment of long-term energy efficiency improvement and greenhouse gas emissions mitigation options for the cement industry. Energy 2019, 170, 1051–1066. [Google Scholar] [CrossRef]

- IEA (International Energy Agency). Energy Technology Transitions for Industry. Strategies for the Next Industrial Revolution; IEA: Paris, France, 2009. [Google Scholar] [CrossRef]

- IPCC. Climate Change 2014 Mitigation of Climate Change. Working Group III Contribution to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change Ottmar; IPCC: Geneva, Switzerland, 2014; ISBN 9781107654815. [Google Scholar]

- IEA (International Energy Agency). Energy Technology Perspectives 2012: Pathways to a Clean Energy System. Available online: https://www.iea.org/reports/energy-technology-perspectives-2012 (accessed on 3 February 2022).

- IEA (International Energy Agency). Are We Entering A Golden Age of Gas? Available online: https://www.iea.org/reports/weo-special-report-are-we-entering-a-golden-age (accessed on 3 February 2022).

- IEA (International Energy Agency). Combined Heat & Power and Emissions Trading: Options for Policy Makers. Available online: https://iea.blob.core.windows.net/assets/633211a0-259d-4964-b549-6bdeb62f9345/CombinedHeatPowerandEmissionsTrading.pdf (accessed on 3 February 2022).

- IEA (International Energy Agency). Sustainable Energy Technologies for Today …and Tomorrow; IEA: Paris, France, 2009. [Google Scholar] [CrossRef]

- IEA (International Energy Agency). Solutions for a low-carbon energy future. Int. Energy Agency 2011, 1, 1–35. [Google Scholar]

- IEA (International Energy Agency). Scenarios & Strategies To 2050; IEA: Paris, France, 2008. [Google Scholar] [CrossRef]

- Sims, R.; Mercado, P.; Krewitt, W.; Bhuyan, G.; Flynn, D.; Holttinen, H.; Jannuzzi, G.; Khennas, S.; Liu, Y.; Nilsson, L.J.; et al. Integration of Renewable Energy into Present and Future Energy Systems. Renew. Energy Sources Clim. Chang. Mitig. 2011, 8, 609–706. [Google Scholar] [CrossRef] [Green Version]

- Kuramochi, T.; Ramírez, A.; Turkenburg, W.; Faaij, A. Comparative assessment of CO2 capture technologies for carbon-intensive industrial processes. Prog. Energy Combust. Sci. 2012, 38, 87–112. [Google Scholar] [CrossRef]

- Zhang, Y.; Lu, X.; Ji, X. Carbon Dioxide Capture; World Meteorological Organization: Geneva, Switzerland, 2019. [Google Scholar] [CrossRef]

- EPA. Global Anthropogenic Non-CO2 Greenhouse Gas Emissions: 1990–2030 How to Obtain Copies How to Obtain the Data For Further Information; Office Atmospheric Programs Climate Change Division U.S. Environmental Protection Agency: Washington, DC, USA, 2011. [Google Scholar]

- Cullen, J.M.; Allwood, J.M.; Bambach, M.D. Mapping the Global Flow of Steel: From Steelmaking to End-Use Goods. Environ. Sci. Technol. 2012, 46, 13048–13055. [Google Scholar] [CrossRef]

- Henriques, M.F.; Dantas, F.; Schaeffer, R. Potential for reduction of CO2 emissions and a low-carbon scenario for the Brazilian industrial sector. Energy Policy 2010, 38, 1946–1961. [Google Scholar] [CrossRef]

- Takeda, K.; Anyashiki, T.; Sato, T.; Oyama, N.; Watakabe, S.; Sato, M. Recent Developments and Mid- and Long-Term CO2 Mitigation Projects in Ironmaking. Steel Res. Int. 2011, 82, 512–520. [Google Scholar] [CrossRef]

- IEA (International Energy Agency). Implementing Energy Efficiency Policies: Are IEA Member Countries on Track? IEA: Paris, France, 2009. [Google Scholar]

- Wang, D.; Gmitter, A.; Sadoway, D. Production of Oxygen Gas and Liquid Metal by Electrochemical Decomposition of Molten Iron Oxide. J. Electrochem. Soc. 2011, 158, 512–520. [Google Scholar] [CrossRef]

- Mittal, A.; Rakshit, D. Energy audit and waste heat recovery from kiln hot shell surface of a cement plant. Therm. Sci. Eng. Prog. 2020, 19, 100599. [Google Scholar] [CrossRef]

- Fierro, J.J.; Escudero-Atehortua, A.; Nieto-Londoño, C.; Giraldo, M.; Jouhara, H.; Wrobel, L.C. Evaluation of waste heat recovery technologies for the cement industry. Int. J. Thermofluids 2020, 7–8, 100040. [Google Scholar] [CrossRef]

- Naranjo, M.; Brownlow, D.T.; Garza, A. CO2 capture and sequestration in the cement industry. Energy Procedia 2011, 4, 2716–2723. [Google Scholar] [CrossRef] [Green Version]

- Hasanbeigi, A.; Menke, C.; Therdyothin, A. Technical and cost assessment of energy efficiency improvement and greenhouse gas emission reduction potentials in Thai cement industry. Energy Effic. 2011, 4, 93–113. [Google Scholar] [CrossRef]

- Van Deventer, J.S.J.; Provis, J.L.; Duxson, P. Technical and commercial progress in the adoption of geopolymer cement. Miner. Eng. 2012, 29, 89–104. [Google Scholar] [CrossRef]

- Erisman, J.W.; Sutton, M.A.; Galloway, J.; Klimont, Z.; Winiwarter, W. How a century of ammonia synthesis changed the world. Nat. Geosci. 2008, 1, 636–639. [Google Scholar] [CrossRef]

- Allwood, J.M.; Cullen, J.M.; Carruth, M.A. Sustainable Materials with Both Eyes Open; Gabriel Thoumi Sustainability Collection; UIT Cambridge Limited: Cambridge, UK, 2012; ISBN 9781906860073. [Google Scholar]

- Milford, R.L.; Allwood, J.M.; Cullen, J.M. Assessing the potential of yield improvements, through process scrap reduction, for energy and CO2 abatement in the steel and aluminium sectors. Resour. Conserv. Recycl. 2011, 55, 1185–1195. [Google Scholar] [CrossRef]

- Roy, J.; Dasgupta, S.; Chakravarty, D. Energy Efficiency: Technology, Behavior, and Development. In The Handbook of Global Energy Policy; Wiley: Hoboken, NJ, USA, 2013; pp. 282–302. [Google Scholar]

- Cooper, D.R.; Allwood, J.M. Reusing Steel and Aluminum Components at End of Product Life. Environ. Sci. Technol. 2012, 46, 10334–10340. [Google Scholar] [CrossRef]

- Skelton, A.; Allwood, J. The incentives for supply chain collaboration to improve material efficiency in the use of steel: An analysis using input output techniques. Ecol. Econ. 2013, 89, 33–42. [Google Scholar] [CrossRef]

- Tekkaya, A.E.; Schikorra, M.; Becker, D.; Biermann, D.; Hammer, N.; Pantke, K. Hot profile extrusion of AA-6060 aluminum chips. J. Mater. Process. Technol. 2009, 209, 3343–3350. [Google Scholar] [CrossRef]

- Carruth, M.; Allwood, J.; Moynihan, M. The technical potential for reducing metal requirements through lightweight product design. Resour. Conserv. Recycl. 2011, 57, 48–60. [Google Scholar] [CrossRef]

- Ashby, M.F. Materials and the Environment, 2nd ed.; Butterworth-Heinemann: Boston, MA, USA, 2013; ISBN 978-0-12-385971-6. [Google Scholar]

- Orr, J.; Darby, A.; Tim, I.; Mark, E.; Otlet, M. Concrete structures using fabric formwork. Struct. Eng. 2011, 89, 20–26. [Google Scholar] [CrossRef]

- Müller, N.; Harnisch, J. A Blueprint for a Climate Friendly Cement industry. WWF–Lafarge Conservation Partnership. Available online: https://awsassets.panda.org/downloads/englishsummary__lr_pdf.pdf (accessed on 3 February 2022).

- Gustavsson, J.; Cederberg, C.; Sonesson, U. Global Food Losses and Food Waste. Save Food Interpack Düsseldorf Ger. Available online: https://www.fao.org/3/i2697e/i2697e.pdf (accessed on 3 February 2022).

- Kainuma, M.; Miwa, K.; Ehara, T.; Akashi, O.; Asayama, Y. A low-carbon society: Global visions, pathways, and challenges. Clim. Policy 2013, 13, 5–21. [Google Scholar] [CrossRef]

- Michaelis, P.; Jackson, T. Material and energy flow through the UK iron and steel sector. Part 1: 1954–1994. Resour. Conserv. Recycl. 2000, 29, 131–156. [Google Scholar] [CrossRef]

- Hatayama, H.; Daigo, I.; Matsuno, Y.; Adachi, Y. Outlook of the World Steel Cycle Based on the Stock and Flow Dynamics. Environ. Sci. Technol. 2010, 44, 6457–6463. [Google Scholar] [CrossRef]

- Pauliuk, S.; Wang, T.; Müller, D.B. Moving Toward the Circular Economy: The Role of Stocks in the Chinese Steel Cycle. Environ. Sci. Technol. 2012, 46, 148–154. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Industry Type | Information Source | Period | Reference |

|---|---|---|---|

| Cement Production | General Authority for Statistics, Statistical Yearbooks | 1965–2013, 2019 | [2,27,32,33] |

| Designated National Authority Kingdom of Saudi Arabia | 2014–2018 | ||

| CEICdata | 2020 | ||

| Soda Ash Production | General Authority for Statistics, Statistical Yearbooks | 2010–2019 | [26] |

| Ammonia Production | Gulf Petrochemicals and Chemicals Association | 2005–2020 | [27] |

| Titanium Dioxide | Gulf Petrochemicals and Chemicals Association | 2009–2020 | |

| Petrochemicals Production | Gulf Petrochemicals and Chemicals Association | 2005–2020 | |

| Iron and Steel Production | World Steel Association, Steel Statistical Yearbooks | 1989–2020 | [28] |

| U.S. Geological Survey Minerals Yearbook | |||

| Aluminum Production | U.S. Geological Survey Minerals Yearbook | 2013–2016 | [29] |

| Glass Production | Glass Production Capacity, Glass International | 2014–2018 | [30] |

| Zinc Production | Saudi Arabian Monetary Agency | 2003–2020 | [31] |

| IPPU Sector | Greenhouse Gas Name | Carbon Emissions Factor (Tons CO2/Tons Produced) |

|---|---|---|

| Raw Steel | CO2 | 1.060 |

| Direct Reduced Steel | CO2 | 0.700 |

| Cement | CO2 | 0.520 |

| Soda Ash | CO2 | 0.415 |

| Ammonia | CO2 | 1.694 |

| Titanium Dioxide | CO2 | 1.430 |

| Primary Aluminum (Prebake) | CO2 | 1.600 |

| Glass | CO2 | 0.200 |

| Zinc | CO2 | 3.660 |

| Ethylene | CO2 | 0.760 |

| CH4 | 6.000 | |

| Ethylene Dichloride | CO2 | 0.196 |

| CH4 | 0.0226 | |

| Methanol | CO2 | 0.670 |

| CH4 | 2.300 | |

| Ethylene Oxide | CO2 | 0.863 |

| CH4 | 1.790 | |

| Vinyl Chloride Monomer | CO2 | 0.294 |

| CH4 | 0.023 |

| Range of Years | Y/Y Growth Rate (%) | |||||||

|---|---|---|---|---|---|---|---|---|

| Cement | DRI | Steel | Petrochemical | |||||

| Ethylene | Ethylene Dichloride | Methanol | Ethylene Oxide | Vinyl Chloride Monomer | ||||

| 2010–2020 (10 yrs) | 3.3 | 3.3 | 6.5 | 4.5 | 2.6 | 0.1 | 1.5 | 3.1 |

| 2005–2020 (15 yrs) | 5.3 | 4.9 | 5.7 | 7.8 | 1.9 | 1.4 | 4.7 | 1.7 |

| 2000–2020 (20 yrs) | 6.3 | 5.7 | 6.4 | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rahman, M.M.; Rahman, M.S.; Chowdhury, S.R.; Elhaj, A.; Razzak, S.A.; Abu Shoaib, S.; Islam, M.K.; Islam, M.M.; Rushd, S.; Rahman, S.M. Greenhouse Gas Emissions in the Industrial Processes and Product Use Sector of Saudi Arabia—An Emerging Challenge. Sustainability 2022, 14, 7388. https://doi.org/10.3390/su14127388

Rahman MM, Rahman MS, Chowdhury SR, Elhaj A, Razzak SA, Abu Shoaib S, Islam MK, Islam MM, Rushd S, Rahman SM. Greenhouse Gas Emissions in the Industrial Processes and Product Use Sector of Saudi Arabia—An Emerging Challenge. Sustainability. 2022; 14(12):7388. https://doi.org/10.3390/su14127388

Chicago/Turabian StyleRahman, Muhammad Muhitur, Mohammad Shahedur Rahman, Saidur R. Chowdhury, Alaeldeen Elhaj, Shaikh Abdur Razzak, Syed Abu Shoaib, Md Kamrul Islam, Mohammed Monirul Islam, Sayeed Rushd, and Syed Masiur Rahman. 2022. "Greenhouse Gas Emissions in the Industrial Processes and Product Use Sector of Saudi Arabia—An Emerging Challenge" Sustainability 14, no. 12: 7388. https://doi.org/10.3390/su14127388

APA StyleRahman, M. M., Rahman, M. S., Chowdhury, S. R., Elhaj, A., Razzak, S. A., Abu Shoaib, S., Islam, M. K., Islam, M. M., Rushd, S., & Rahman, S. M. (2022). Greenhouse Gas Emissions in the Industrial Processes and Product Use Sector of Saudi Arabia—An Emerging Challenge. Sustainability, 14(12), 7388. https://doi.org/10.3390/su14127388