4.1. The Results of Reliability, Convergent Validity, Discriminant Validity, and Composite Reliability Tests

Table 3 shows the results of the reliability analysis of the scales corresponding to 8 factors in the model: effort expectancy, performance expectancy, brand image, perceived risk, cost value, social influence, behavioral intention to use online banking services, and decision to choose to use online banking services.

Columns 3, 4, and 6 in

Table 3 show the mean, variance, and Cronbach’s Alpha coefficient of the scale when removing each item, respectively. Column 5 in

Table 3 shows the corrected item-total correlation, which represents the correlation of each item with the rest of the items on the scale.

Table 3 shows that all scales are reliable because Cronbach’s Alpha coefficients are all more than 0.7 [

51]. Specifically, Cronbach’s Alpha coefficients range from 0.797 to 0.885. In addition, the corrected item-total correlation coefficients are all greater than 0.3, showing that the items are reliable.

Next, we perform an Exploratory Factor Analysis by Principal Axis Factoring method with Promax rotation to identify latent factors. The results are presented in

Table 4.

Table 4 shows that KMO has a value of 0.878, which is greater than 0 and less than 1, showing that exploratory factor analysis is consistent with the data [

52]. In addition, Bartlett’s test has a significance level of 0.000 showing that items are correlated with latent factors [

52]. The results of Exploratory Factor Analysis extracted seven latent factors consistent with the research model originally proposed. The exploratory factor analysis results also show that the total variance explained is 58.362%, lower than the 70% threshold. However, according to Hair et al. [

53], in social sciences, a field of research where data information is often inaccurate, a total variance explained of 60% (or even less) is satisfactory. In addition, Fornell and Larcker [

54] also suggested that a total variance explained greater than 50% is satisfactory.

The exploratory factor analysis identified latent factors and measured observed variables for each latent factor. The exploratory factor analysis results are the premise for the next confirmatory factor analysis.

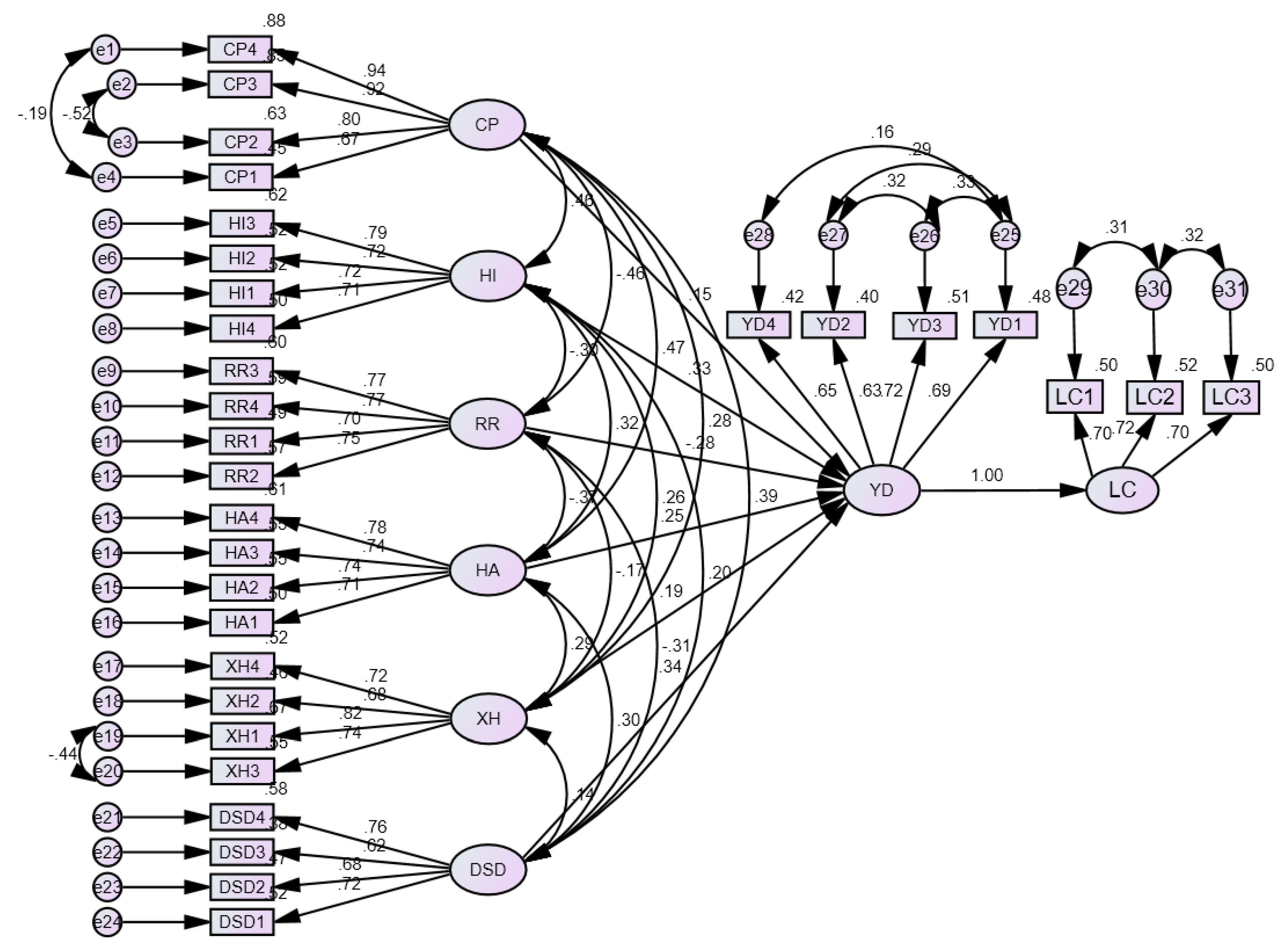

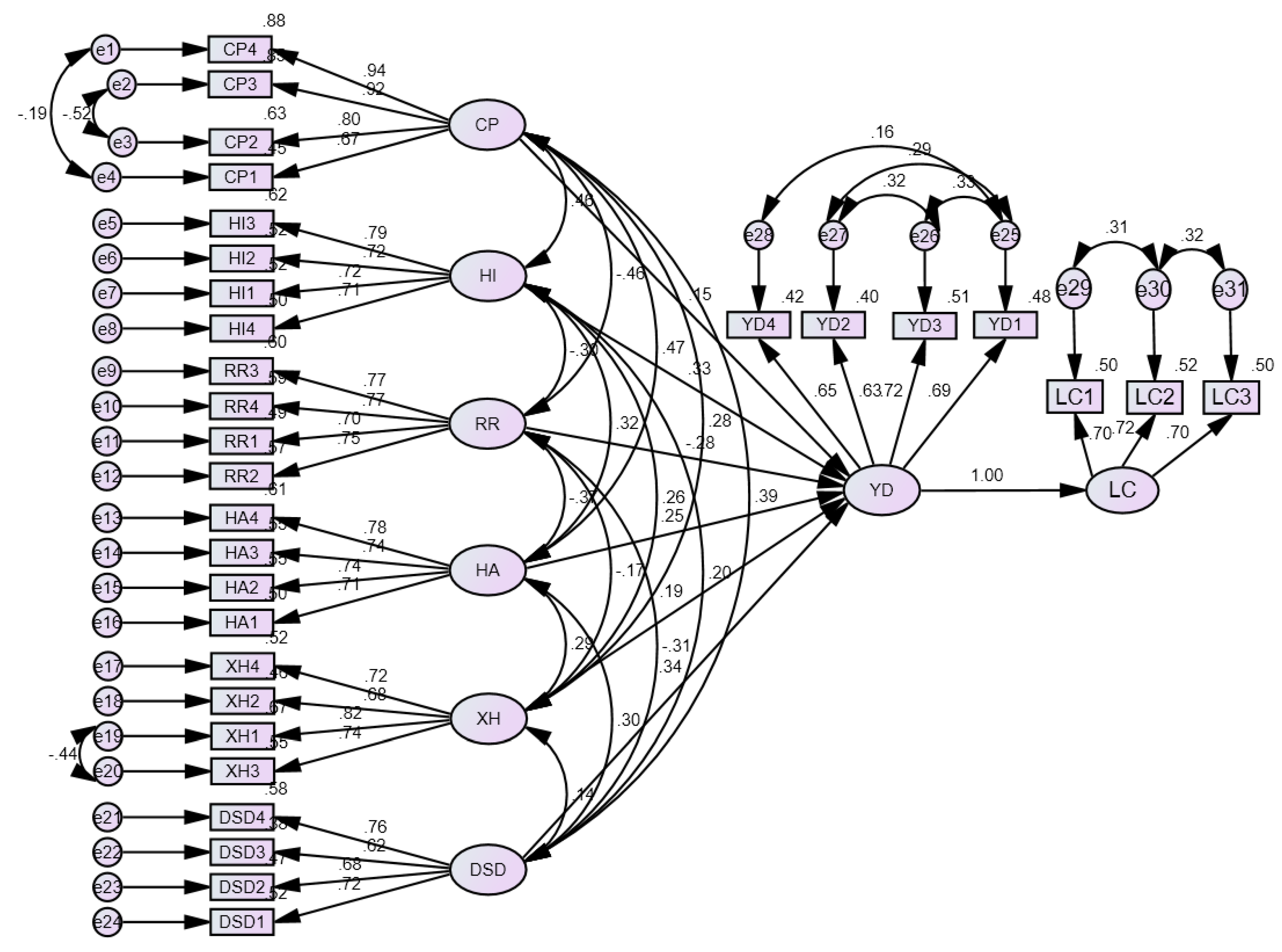

Table 5 below presents the standard loadings of the confirmatory factor analysis.

Table 5 shows that most of the standard loadings are greater than 0.7, with the exception of four standard loadings that are less than 0.7 (but still greater than 0.5). This result implies that the scales have convergence.

To access the goodness of fit of the proposed model, we continue to consider the model’s goodness of fit indicators. They are relative fix index (FRI), adjusted goodness-of-fit index (AGFI), goodness-of-fit index (GFI), normed fit index (NFI), comparative goodness of fit (CFI), Tucker–Lewis Index (TLI), incremental fit index (IFI), and root mean square error of approximation (RMSEA). The values of these indicators are shown in

Table 6.

The Chi-square/df value of 1.932 is lower than the threshold of 3, recommended by Carmines and McIver [

55]. The values of RFI, AGFI, GFI, and NFI are 0.886, 0.890, 0.912, and 0.902, respectively. For the CFI, TLI, and IFI, the obtained values are all greater than 0.90. The RMSEA is also in the desired range between 0.05 and 0.08 [

52]. Thus, the proposed model is consistent with the data.

Table 7 presents the result of the intercorrelation matrix, the values of average variance extracted (AVE), and the composite reliability (CR) of each scale corresponding to each factor in the model. The result shows that AVEs are all greater than 0.5. Therefore, all of the factors in the model converge [

54]. In addition, the correlation coefficients between factors have an absolute value less than 0.85. Therefore, the factors in the model all discriminate [

56]. Finally, the CRs of the factors are all higher than 0.6 [

57].

4.2. The Result of SEM

To test the research hypothesis, we estimate the SEM. The result of the estimations is presented in

Figure 2.

Table 8 shows that the Chi-square/df value of 2.124 is lower than the threshold of 3, recommended by Carmines and McIver [

55]. The values of RFI, AGFI, GFI, and NFI are 0.870, 0.865, 0.890, and 0.887, respectively. For the CFI, TLI, and IFI, the obtained values are all greater than 0.90. The RMSEA is also in the desired range between 0.05 and 0.08 [

52]. Thus, the SEM is consistent with the data.

The result of testing the research hypothesis is presented in

Table 9.

Table 9 shows that the coefficient of the cost value factor is 0.146 and is significant at the level of 1%. Therefore, the cost value has a positive impact on the behavioral intention to use online banking services, and hypothesis 5 (H5) is supported. This result is also consistent with Migliore et al. [

34], Polatoglu and Ekin [

33], Liao and Cheung [

40]. The impact of cost value on behavioral intention to use online banking services in Vietnam is similar to the results obtained from Singapore, Turkey, China, and Italy. In fact, online banking can help customers save transaction time. At the same time, low transaction costs will encourage customers to use online banking services.

Next, the regression coefficient of the performance expectancy is 0.331 and significant at the level of 1%. Thus, the performance expectancy has a positive impact on the behavioral intention to use online banking services, and hypothesis 2 (H2) is supported. This result is also consistent with Polatoglu and Ekin [

33], Gupta and Arora [

31], Alalwan et al. [

32], Yaseen and Qirem [

23], Migliore et al. [

34], and Farzin et al. [

31]. The impact of performance expectancy on behavioral intention to use online banking services in Vietnam is similar to the results obtained from Turkey, India, Jordan, China, and Italy. In fact, online banking in Vietnam is growing in popularity, providing customers with benefits such as instant, fast, and personalized services. Therefore, customers can accept online banking because they believe it is a useful and convenient tool to carry out banking transactions.

The regression coefficient of the perceived risk is −0.282 and significant at the level of 1%. Thus, the perceived risk has a negative impact on the behavioral intention to use online banking services, and hypothesis 4 (H4) is supported. This result is also consistent with Suganthi [

36], Polatoglu and Ekin [

33], Gupta and Arora [

31], Alalwan et al. [

32], Yaseen and Qirem [

23], and Migliore et al. [

34]. The impact of perceived risk on behavioral intention to use online banking services in Vietnam is similar to the results obtained from Malaysia, Turkey, India, and Jordan. In Vietnam, perceived risk is an important aspect when customers form an intention to use or refuse online banking services. The reality of Vietnam’s banking activities in recent years shows that perceived risks stem from customers’ concerns about the lack of security when using online banking services.

The regression coefficient of the brand image is 0.252 and significant at the level of 1%. Thus, the brand image has a positive impact on the behavioral intention to use online banking services, and hypothesis 3 (H3) is supported. This result is also consistent with Hernandez and Mazzon [

58], Poon [

39], Rambocas et al. [

27], and Linh et al. [

28]. With a developing market, like in Vietnam, possible hazards in banking activity are unavoidable. Therefore, banks with big brands typically provide clients comfort of mind while utilizing the service. In addition, the bank’s brand is also a factor that reflects the level of clients while utilizing it.

In addition, the regression coefficient of the social influence is 0.186 and significant at the level of 1%. Thus, the social influence has a positive impact on the behavioral intention to use online banking services, and hypothesis 6 (H6) is supported. This result is also consistent with Tarhini et al. [

21], Gupta and Arora [

31], Farzin et al. [

31], Migliore et al. [

34]. The impact of social influence on behavioral intention to use online banking services in Vietnam is similar to the results obtained from Lebanon, India, China, and Italy. This result shows that, in Vietnam as well as in other countries, when new technologies, such as online banking, are endorsed by influential individuals, customers are more likely to accept them.

The regression coefficient of the effort expectancy is 0.335 and significant at the level of 1%. Thus, the effort expectancy has a positive impact on the behavioral intention to use online banking services, and hypothesis 1 (H1) is supported. This result is also consistent with Gupta and Arora [

31], Alalwan et al. [

32], and Farzin et al. [

31]. The impact of effort expectancy on behavioral intention to use online banking services in Vietnam is similar to the results obtained from India, Jordan, and Iran. This result implies that customers are often looking for technologies to simplify their operations with as little effort as possible. When customers believe that online banking is easy to use, the chances of accepting this service increase significantly.

Finally, the regression coefficient of the behavioral intention to use online banking services is 0.9997 and significant at the level of 1%. Thus, the behavioral intention to use online banking services has a positive impact on the decision to choose online banking services, and hypothesis 7 (H7) is supported. This result is also consistent with Davis [

15], Taylor and Todd [

42], and Kijsanayotin et al. [

59]. Like previous studies, in this study, behavioral intention is proven to be a factor leading to customers’ decision to use services. In fact, when customers intend to use the service in the Vietnamese market, they will almost certainly perform their service use behavior.

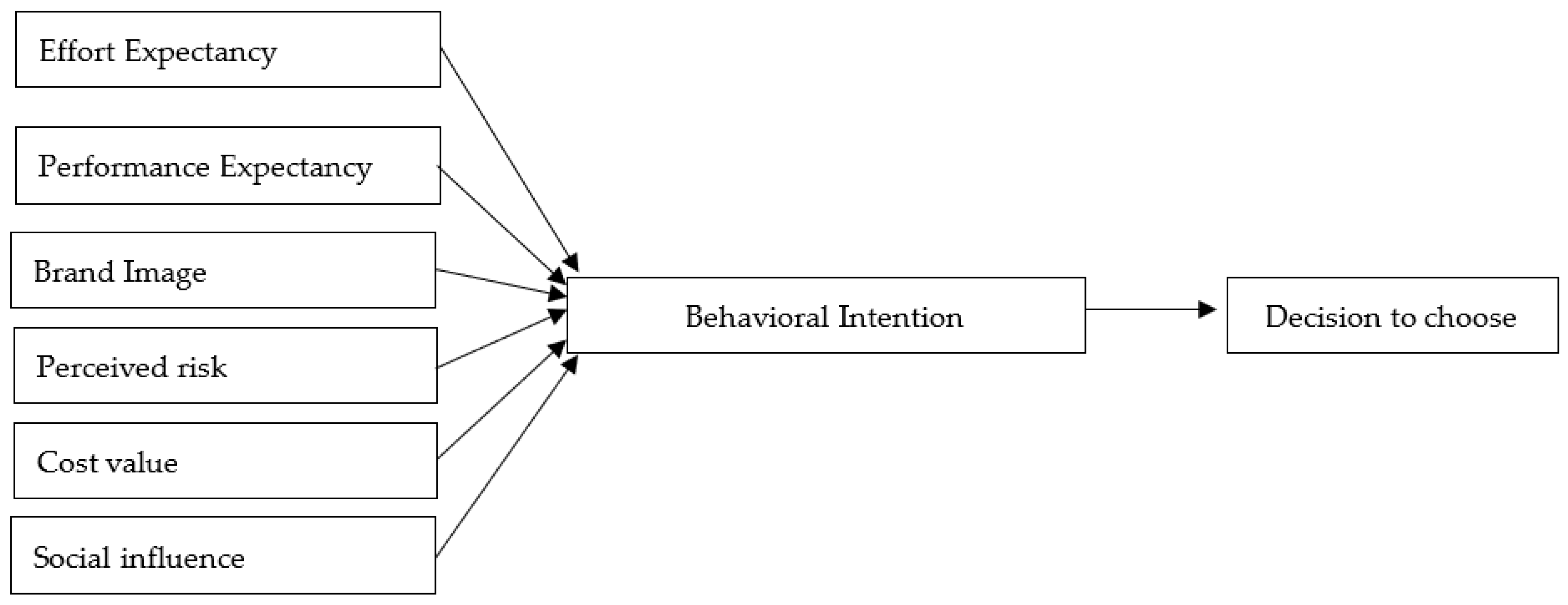

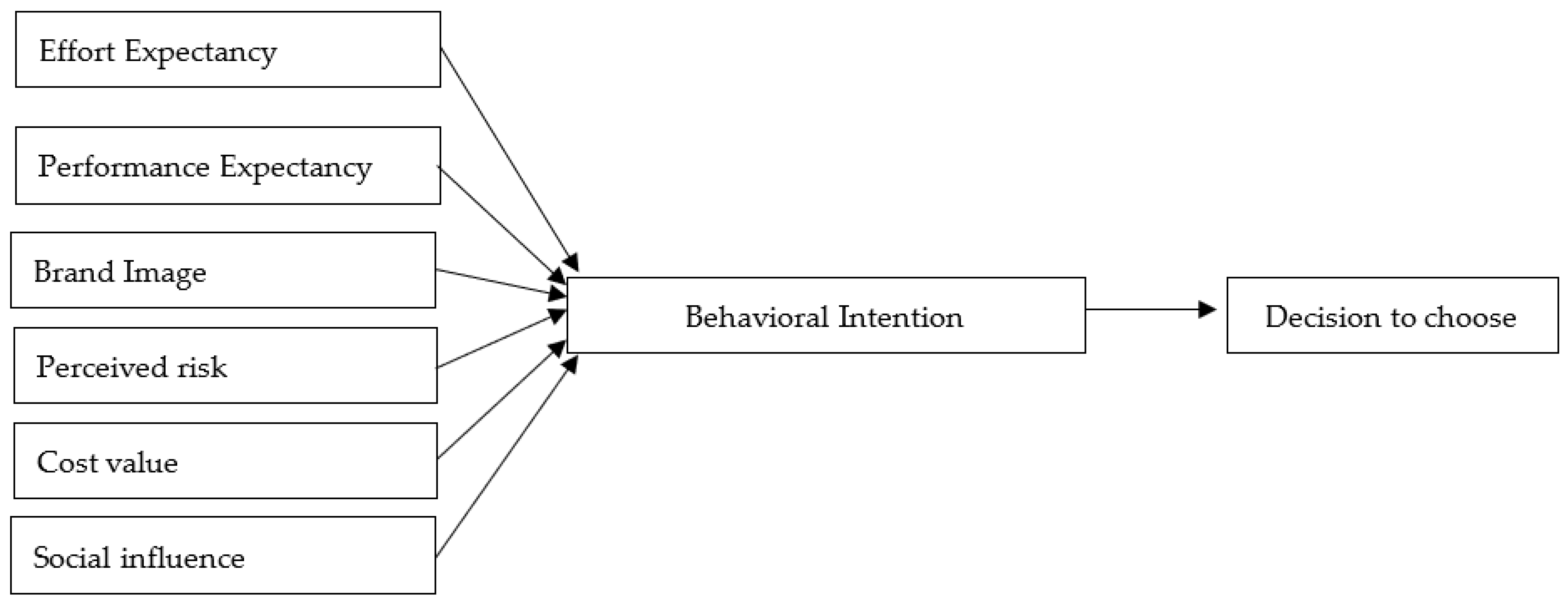

In addition, the standardized regression weights show that effort expectancy has the strongest impact on the behavioral intention to use online banking services. Meanwhile, the cost value factor has the weakest impact on behavioral intention to use online banking services. The other factors in order of affecting the behavioral intention to use online banking services from strong to weak are performance expectancy, perceived risk, brand image, and social influence, respectively.

4.3. The Result of MLP Model

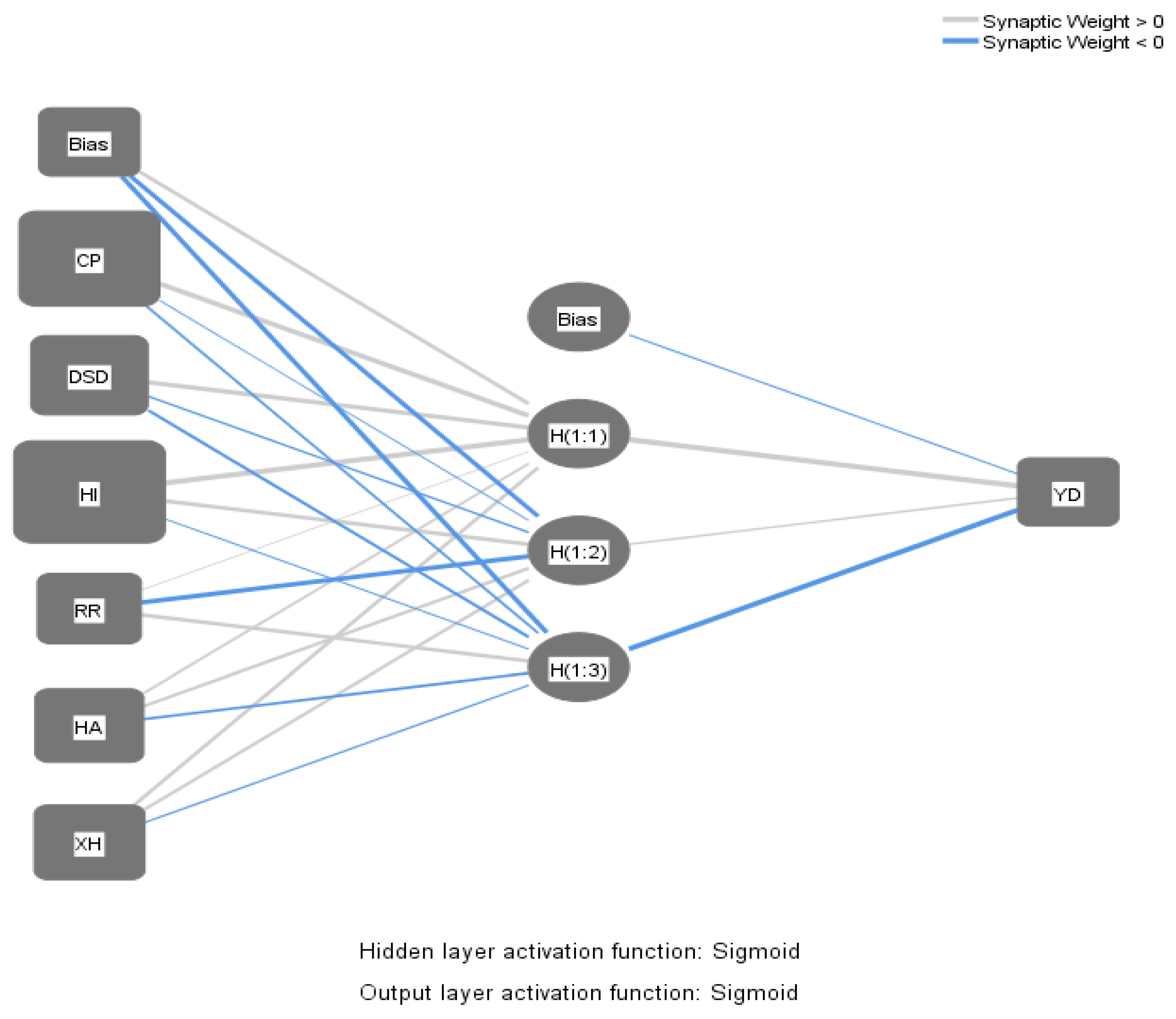

The estimation result of SEM shows that the factors affecting the behavioral intention to use online banking services are cost value, performance expectancy, perceived risk, brand image, social influence, effort expectancy. Therefore, these six factors will be brought to the input layer of the MLP model. The output layer is the behavioral intention to use online banking services factor. To the hidden layer, in the case of six input factors, the number of neurons in the hidden layer is

. Thus, the number of neurons in the hidden layer is 3. The Sigmoid function is used as the activation function of the neurons in the hidden and the output layers. In this study, we use 90% of the sample data to train the model, and the remaining 10% is used to test the accuracy of the model. An MLP model is shown in

Figure 3.

Table 10 shows that the average sum of square errors of 10 models is relatively small (4.100 for the training data and 0.468 for the testing data), which means the prediction level of the model is fairly accurate.

The importance of each influencing factor shows how the intention to use online banking services will change when the influencing factor changes. To see the importance of each influencing factor, we evaluate through the normalized importance of each factor. Specifically, the normalized importance of a factor is the ratio of the factor’s importance to the highest importance. The results of the importance of each factor are presented in

Table 11.

Table 11 shows that the effect of performance expectancy on behavioral intention to use online banking services has the highest importance (100%). At the same time, the impact of social influence on behavioral intention to use online banking services has the lowest importance (33.3%). The remaining factors of importance in order are cost value (79.5%), effort expectancy (56.6%), brand image (56.4%), and perceived risk (36.1%). Thus, when controlling for the non-linear relationship through the MLP model, the impact of the factors on the behavioral intention to use online banking services has changed compared to the results obtained from the SEM.

{kind=link}

{kind=link}

{kind=link}