Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda

Abstract

1. Introduction

2. Theoretical Background

- (1)

- social value creation and corporate social responsibility (henceforth CSR) studies;

- (2)

- social enterprise (henceforth, SE) studies primarily focused on the issues of performance and accountability;

- (3)

- environmental impact studies;

- (4)

- public sector and impact finance studies;

- (5)

- developing economies studies.

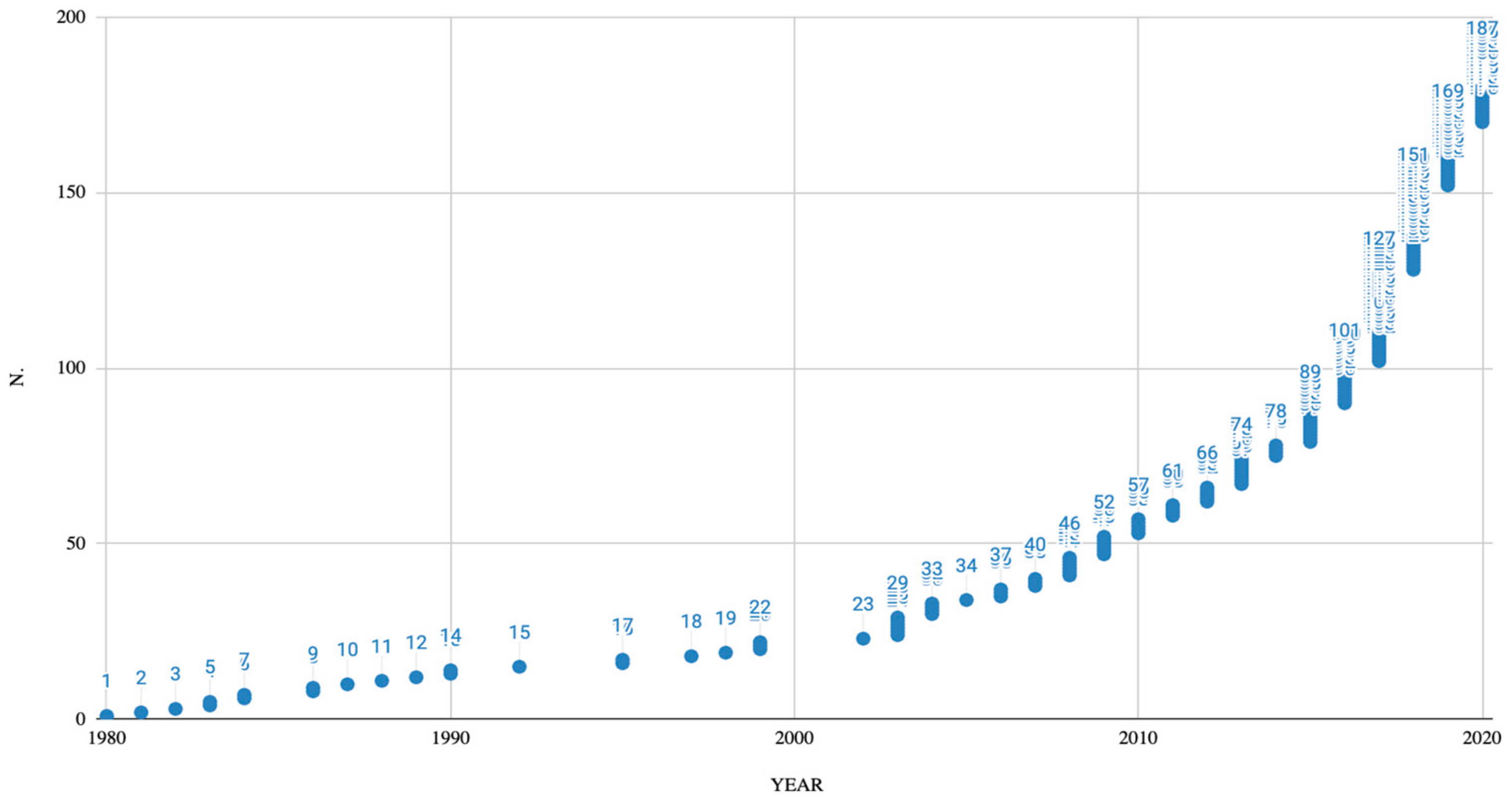

3. Method

- Identifying previous studies that mapped the evolution of SIA models and then analysing those studies to verify whether they provided clusters or groups of SIA models;

- Investigating the models already reviewed by previous studies and the new SIA models proposed since the last mapping study to highlight emerging patterns and to shape the future research agenda in this field of research.

4. Six Studies in the Search for SIA Models

- o

- Cluster 1 (Simple Social Quantitative) contains models based on quantitative indicators. These models are easy, applicable to any sector and intend to produce a quantitative measure of the social impact and of the impact on employees with a retrospective time frame.

- o

- Cluster 2 (Holistic Complex) contains models characterised by a holistic purpose, and this explains the presence of both qualitative and quantitative variables. The aim of these models is to provide evidence to obtain funding, so they focus on reporting and communication of the results achieved. These are also applicable to any sector, but in this case, the complexity is high.

- o

- Cluster 3 (Qualitative Screening) consists of models based on qualitative variables and are usually focused on holistic impacts. They are retrospective and have a basic level of complexity.

- o

- Cluster 4 (Management) contains models based on qualitative or quantitative variables that aim to measure different types of impacts. They are used for managerial or certification reasons. Usually, they are applied to ongoing activities.

5. Model Mapping

6. Discussion and Conclusions

6.1. Contributions to the Literature

6.2. Implications for Managers

6.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A

| SIA MODELS | |||

| 1 | AA1000AP | 47 | Logic model builder |

| 2 | Acumen Lean Data | 48 | LuxFLAG ESG Label |

| 3 | Acumen scorecard | 49 | Measuring impact framework |

| 4 | Anticipated Impact Measurement and Monitoring (AIMM) | 50 | Methodology for impact analysis and assessment |

| 5 | AtKisson compass assessment for investors | 51 | MetODD-SDG |

| 6 | Best available charitable option | 52 | MicroRate |

| 7 | Bridges Ventures Impact Radar | 53 | Movement above the US$1 a day threshold |

| 8 | CERISE-IDIA | 54 | MSCI ESG Ratings Methodology |

| 9 | Charity analysis framework | 55 | Ongoing Assessment of Social Impacts (OASIS) |

| 10 | Cost per impact | 57 | Outcome star |

| 11 | Cradle-to-cradle certification | 58 | Practical quality assurance system for small organisations (PQASSO)/Trusted Charity |

| 12 | Dalberg Approach | 59 | Progress out of poverty index |

| 13 | DTA Fit for purpose | 60 | Prove it! |

| 14 | Eco-mapping | 61 | Public value scorecard |

| 15 | EFQM | 62 | Quality first |

| 16 | EMAS | 63 | RobecoSam 3 step SDG Framework |

| 17 | Environmental, Social and Governance (ESG) Scores | 65 | SASB Standard |

| 18 | EPIC | 67 | SDG Impact Practice Standard |

| 19 | ESG Disclosure score | 68 | Social accounting and audit |

| 20 | ESG Relevance Score | 69 | Social Business Scorecard |

| 21 | ESG Risk Rating | 70 | Social enterprise balanced scorecard |

| 22 | European Impact Investing Luxembourg | 71 | Social enterprise mark |

| 23 | Expected return | 73 | Social Impact Measurement for Local Economies (SIMPLE) |

| 24 | Family of measures | 74 | Social rating |

| 25 | Finance Initiative Impact Radar | 75 | Social return assessment |

| 26 | FMO ESG Toolkits | 76 | Social return on investment |

| 27 | FTSE ESG Ratings | 77 | Social Value Maturity Index |

| 28 | Global Alliance for Banking on Values (GABV) | 78 | Social value metrics |

| 29 | Global Impact Investing Rating System (GIIRS) | 79 | Sopact-tool |

| 30 | GOGLA Impact Metrics | 80 | SPI4 |

| 31 | GRI sustainability reporting framework | 82 | Standard Ethics Rating (SER) |

| 32 | HIP Rating | 83 | Star social firm |

| 33 | HIPSO Harmonized Indicators for Private Sector Operations | 84 | Success measures data system |

| 34 | VALORIS method | 85 | The B impact rating system |

| 35 | Impact Analysis for Corporate Finance & Investments (Tool prototype) | 86 | The big picture |

| 36 | Impact Due Diligence Tools | 87 | The Committee on Sustainability Assessment (COSA) Methodology |

| 37 | Impact Management Project (IMP) Five Dimensions | 88 | The FINCA client assessment tool |

| 38 | Impact Multiple of Money (IMM) | 89 | The Impact Due Diligence Guide |

| 39 | Impact Risk Classification (IRC) | 90 | The SRI LABEL |

| 40 | Impact-Weighted Accounts | 91 | Third sector performance dashboard |

| 41 | Inrate ESG Impact Rating Methodology | 92 | TIMM |

| 42 | Inventory of Business Indicators (SDG Compass) | 94 | Trucost |

| 43 | IRIS + (and IRIS) | 96 | Volunteering impact assessment toolkit |

| 44 | ISS ESG Corporate Rating | 97 | Wallace assessment tool |

| 45 | ISS SDG Impact rating | 98 | Y Analytics |

| 46 | LM3 | ||

References

- OECD. Policy Brief on Social Impact Measurement for Social Enterprises. In Policies for Social Entrepreneurship; European Commission Luxembourg: Luxembourg, 2015; ISBN 978-92-79-47475-0. Available online: https://www.oecd.org/social/PB-SIM-Web_FINAL.pdf (accessed on 15 April 2021).

- Young, D.R.; Searing, E.A.; Brewer, C.V. The Social Enterprise Zoo: A Guide for Perplexed Scholars, Entrepreneurs, Philanthropists, Leaders, Investors, and Policymakers; Edward Elgar Publishing: Cheltenham, UK, 2016. [Google Scholar]

- OECD. International Migration Outlook 2018; OECD Publishing: Paris, France, 2018. [Google Scholar] [CrossRef]

- Tang, M.; Liao, H.; Wan, Z.; Herrera-Viedma, E.; Rosen, M.A. Ten Years of Sustainability (2009 to 2018): A Bibliometric Overview. Sustainability 2018, 10, 1655. [Google Scholar] [CrossRef]

- Clark, C.; Rosenzweig, W.; Long, D.; Olsen, S. Double Bottom Line Project Report: Assessing Social Impact in Double Bottom Line Ventures; Working Paper Series No. 13; University of California: Berkeley, CA, USA, 2004. [Google Scholar]

- Grieco, C.; Michelini, L.; Iasevoli, G. Measuring value creation in social enterprises: A cluster analysis of social impact assessment models. Nonprofit Volunt. Sect. Q. 2015, 44, 1173–1193. [Google Scholar] [CrossRef]

- Lyon, F.; Sepulveda, L. Mapping social enterprises: Past approaches, challenges and future directions. Soc. Enterp. J. 2009, 5, 83–94. [Google Scholar] [CrossRef]

- Then, V.; Schober, C.; Rauscher, O.; Kehl, K. Social Return on Investment Analysis; Springer: Berlin, Germany, 2017. [Google Scholar]

- Corvo, L.; Pastore, L. The Usefulness of Sharing Social Impact Data. Early Findings from an International Benchmarking on SROI Assessments. J. Entrep. Organ. Divers. (JEOD) Creat. Commons Attrib. 2020, 9, 45–61. [Google Scholar] [CrossRef]

- Massey, A.; Johnston-Miller, K. Governance: Public governance to social innovation? Policy Politics 2016, 44, 663–675. [Google Scholar] [CrossRef]

- Klemelä, J. Licence to operate: Social Return on Investment as a multidimensional discursive means of legitimating organisational action. Soc. Enterp. J. 2016, 12, 387–408. [Google Scholar] [CrossRef]

- Emerson, J. The Blended Value Proposition: Integrating Social and Financial Returns. Calif. Manag. Rev. 2003, 45, 35–51. [Google Scholar] [CrossRef]

- Maas, K.; Liket, K. Social impact measurement: Classification of methods. In Environmental Management Accounting and Supply Chain Management; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Nicholls, A. Measuring Impact in Social Entrepreneurship: New Accountabilities to Stakeholders and Investors? ERSC Seminar, Local Government Research Unit: London, UK, 2005. [Google Scholar]

- Dietz, T. Theory and method in social impact assessment. Sociol. Inq. 1987, 57, 54–69. [Google Scholar] [CrossRef]

- Vanclay, F. Conceptual and methodological advances in social impact assessment. The international handbook of social impact assessment. Concept. Methodol. Adv. 2003, 1–9. [Google Scholar] [CrossRef]

- Bakar, A.A.; Osman, M.M.; Bachok, S.; Zen, I. Social impact assessment: How do the public help and why do they matter? Procedia-Soc. Behav. Sci. 2015, 170, 70–77. [Google Scholar] [CrossRef][Green Version]

- Hervieux, C.; Voltan, A. Toward a systems approach to social impact assessment. Soc. Enterp. J. 2019, 15, 264–286. [Google Scholar] [CrossRef]

- Arvidson, M.; Lyon, F. Social Impact Measurement and Non-profit Organisations: Compliance, Resistance, and Promotion. Volunt. Int. J. Volunt. Nonprofit Organ. 2014, 25, 869–886. [Google Scholar] [CrossRef]

- Manzoor, F.; Wei, L.; Nurunnabi, M.; Subhan, Q.A.; Shah, S.I.A.; Fallatah, S. The Impact of Transformational Leadership on Job Performance and CSR as Mediator in SMEs. Sustainability 2019, 11, 436. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The Big Idea: Creating Shared Value. How to reinvent capitalism—And unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Porter, M.E.; Hills, G.; Pfitzer, M.; Patscheke, S.; Hawkins, E. Measuring Shared Value: How to Unlock Value by Linking Business and Social Results; by FSG Creative Commons Attribution-NoDerivs 3.0. 2012. Available online: https://www.hbs.edu/ris/Publication%20Files/Measuring_Shared_Value_57032487-9e5c-46a1-9bd8-90bd7f1f9cef.pdf (accessed on 15 April 2021).

- Kozień, A. The Principle of Sustainable Development as the Basis for Weighing the Public Interest and Individual Interest in the Scope of the Cultural Heritage Protection Law in the European Union. Sustainability 2021, 13, 3985. [Google Scholar] [CrossRef]

- Emerson, J.; Wachowicz, J.; Chun, S. Social return on investment: Exploring aspects of value creation in the nonprofit sector. In Social Purpose Enterprises and Venture Philanthropy in the New Millennium; Investor Perspectives, REDF Workshop; REDF: San Francisco, CA, USA, 2000; Volume 2, pp. 130–173. Available online: https://redf.org/wp-content/uploads/REDF-Box-Set-Vol.-2-SROI-Paper-2000.pdf (accessed on 15 April 2021).

- Latané, B. The psychology of social impact. Am. Psychol. 1981, 36, 343. [Google Scholar] [CrossRef]

- Bergmann, T.; Utikal, H. How to Support Start-Ups in Developing a Sustainable Business Model: The Case of an European Social Impact Accelerator. Sustainability 2021, 13, 3337. [Google Scholar] [CrossRef]

- Clark, C.; Brennan, L. Entrepreneurship with social value: A conceptual model for performance measurement. Acad. Entrep. J. 2012, 18, 17. [Google Scholar]

- Yang, C.-L. Building a Performance Assessment Model for Social Enterprises-Views on Social Value Creation. Sci. J. Bus. Manag. 2014, 2, 1. [Google Scholar] [CrossRef]

- Ebrahim, A.S.; Rangan, V.K. The Limits of Nonprofit Impact: A Contingency Framework for Measuring Social Performance. SSRN Electron. J. 2010. [Google Scholar] [CrossRef]

- Bagnoli, L.; Megali, C. Measuring Performance in Social Enterprises. Nonprofit Volunt. Sect. Q. 2009, 40, 149–165. [Google Scholar] [CrossRef]

- Dart, R. The legitimacy of social enterprise. Nonprofit Manag. Leadersh. 2004, 14, 411–424. [Google Scholar] [CrossRef]

- Ruttman, R. New ways to invest for social and environmental impact. In Investing for Impact: How Social Entrepreneurship Is Redefining the Meaning of Return; Credit Suisse with Schwab Foundation for Social Entrepreneurship: Zurig/Davos, UK, 2012; Available online: https://www.longfinance.net/media/documents/cs_impactinvesting_2012.pdf (accessed on 15 April 2021).

- Esposito, P.; Brescia, V.; Fantauzzi, C.; Frondizi, R. Understanding Social Impact and Value Creation in Hybrid Organizations: The Case of Italian Civil Service. Sustainability 2021, 13, 4058. [Google Scholar] [CrossRef]

- Nicholls, A. ‘We do good things, don’t we?’: ‘Blended Value Accounting’ in social entrepreneurship. Account. Organ. Soc. 2009, 34, 755–769. [Google Scholar] [CrossRef]

- Nicholls, A. Institutionalizing social entrepreneurship in regulatory space: Reporting and disclosure by community interest companies. Account. Organ. Soc. 2010, 35, 394–415. [Google Scholar] [CrossRef]

- Di Fabio, A.; Peiroó, J.M. Human Capital Sustainability Leadership to Promote Sustainable Development and Healthy Organizations: A New Scale. Sustainability 2018, 10, 2413. [Google Scholar] [CrossRef]

- Esteves, A.M.; Franks, D.M.; Vanclay, F. Social impact assessment: The state of the art. Impact Assess. Proj. Apprais. 2012, 30, 34–42. [Google Scholar] [CrossRef]

- Richmond, B.J.; Mook, L.; Jack, Q. Social accounting for nonprofits: Two models. Nonprofit Manag. Leadersh. 2003, 13, 308–324. [Google Scholar] [CrossRef]

- Zappalà, G.; Lyons, M. Recent Approaches to Measuring Social Impact in the Third Sector: An Overview; Centre for Social Impact: Sydney, NSW, Australia, 2009; Available online: https://www.socialauditnetwork.org.uk/files/8913/2938/6375/CSI_Background_Paper_No_5_-_Approaches_to_measuring_social_impact_-_150210.pdf (accessed on 15 April 2021).

- Zamagni, S.; Venturi, P.; Rago, S. Valutare l’impatto sociale. La questione della misurazione nelle imprese sociali. Impresa Soc. 2015, 6, 77–97. [Google Scholar]

- Corvo, L.; Pastore, L. The challenge of Social Impact Bond: The state of the art of the Italian context. Eur. J. Islam. Financ. 2019. [Google Scholar] [CrossRef]

- Meneguzzo, M.; Galeone, P. La finanza sociale. In Pubblico, Privato, Non Profit: Le Prospettive Comuni in Europa e in Italia; Rubbettino: Soveria Mannelli, Italy, 2016. [Google Scholar]

- Biancone, P.P.; Radwan, M. Social Finance and Unconventional Financing Alternatives: An Overview. Eur. J. Islam. Financ. 2018. [Google Scholar] [CrossRef]

- Brown, A.; Swersky, A. The First Billion; The Boston Consulting Group, Big Society Capital: London, UK, 2012. [Google Scholar]

- Wilson, K.E. Social Investment: New Investment Approaches for Addressing Social and Economic Challenges. In OECD Science, Technology and Industry Policy Paper; No. 15; OECD Publishing: Paris, France, 2014; Available online: https://ssrn.com/abstract=2501247 (accessed on 15 April 2021).

- Aucamp, I.; Lombard, A. Can social impact assessment contribute to social development outcomes in an emerging economy? Impact Assess. Proj. Apprais. 2017, 36, 173–185. [Google Scholar] [CrossRef]

- Olsen, S.; Galimidi, B. Catalog of Approaches to Impact Measurement: Assessing Social Impact in Private Ventures; Rockfeller Foundation: New York, NY, USA, 2008; Available online: http://www.midot.org.il/Sites/midot/content/Flash/CATALOG%20OF%20APPROACHES%20TO%20IMPACT%20MEASUREMENT.pdf (accessed on 15 April 2021).

- Rinaldo, H. Getting Started in Social Impact Measurement: A Guide to Choosing How to Measure Social Impact; Norwich Guild: Norwich, UK, 2010; Available online: https://www.socialauditnetwork.org.uk/files/8113/4996/6882/Getting_started_in_social_impact_measurement_-_270212.pdf (accessed on 15 April 2021).

- Boffo, R.; Patalano, R. Esg Investing: Practices, Progress and Challenges; Technical Report; OECD: Paris, France, 2020. [Google Scholar]

- OECD. OECD Social Impact Investment 2019: The Impact Imperative for Sustainable Development; OECD Publishing: Paris, France, 2019. [Google Scholar]

- Faraudello, A.; Barreca, M.; Iannaci, D.; Lanzara, F. The Impact of Social Enterprises: A Bibliometric Analysis from 1991 to 2020. Int. J. Financ. Res. 2021, 12, 3. [Google Scholar] [CrossRef]

- Arce-Gomez, A.; Donovan, J.D.; Bedggood, R.E. Social impact assessments: Developing a consolidated conceptual framework. Environ. Impact Assess. Rev. 2015, 50, 85–94. [Google Scholar] [CrossRef]

- Spiess-Knafl, W.; Scheck, B. Impact Investing: Instruments, Mechanisms and Actors; Springer: Berlin, Germany, 2017. [Google Scholar]

- Bonilla-Alicea, R.J.; Fu, K. Systematic Map of the Social Impact Assessment Field. Sustainability 2019, 11, 4106. [Google Scholar] [CrossRef]

- Lenzo, P.; Traverso, M.; Salomone, R.; Ioppolo, G. Social Life Cycle Assessment in the Textile Sector: An Italian Case Study. Sustainability 2017, 9, 2092. [Google Scholar] [CrossRef]

- Biancone, P.P.; Secinaro, S.; Brescia, V.; Iannaci, D. Communication and Data Processing in Local Public Group: Transparency and Accountability. Int. J. Bus. Manag. 2018, 13, 20–37. [Google Scholar] [CrossRef][Green Version]

- Biancone, P.; Secinaro, S.; Brescia, V.; Iannaci, D. The Popular Financial Reporting between Theory and Evidence. Int. Bus. Res. 2019, 12, 45. [Google Scholar] [CrossRef]

- Welch, E.W. The relationship between transparent and participative government: A study of local governments in the United States. Int. Rev. Adm. Sci. 2012, 78, 93–115. [Google Scholar] [CrossRef]

- Secinaro, S.; Calandra, D.; Petricean, D.; Chmet, F. Social Finance and Banking Research as a Driver for Sustainable Development: A Bibliometric Analysis. Sustainability 2020, 13, 330. [Google Scholar] [CrossRef]

- Baraibar-Diez, E.; Luna, M.; Odriozola, M.D.; Llorente, I. Mapping Social Impact: A Bibliometric Analysis. Sustainability 2020, 12, 9389. [Google Scholar] [CrossRef]

- Burdge, R.J. Benefiting from the practice of social impact assessment. Impact Assess. Proj. Apprais. 2003, 21, 225–229. [Google Scholar] [CrossRef]

- Mitzinneck, B.C.; Besharov, M.L. Managing Value Tensions in Collective Social Entrepreneurship: The Role of Temporal, Structural, and Collaborative Compromise. J. Bus. Ethics 2019, 159, 381–400. [Google Scholar] [CrossRef]

- Secinaro, S.; Corvo, L.; Brescia, V.; Iannaci, D. Hybrid organizations: A Systematic Review of the Current Literature. Int. Bus. Res. 2019, 12, 1–21. [Google Scholar] [CrossRef][Green Version]

- Barman, E. What is the Bottom Line for Nonprofit Organizations? A History of Measurement in the British Voluntary Sector. Volunt. Int. J. Volunt. Nonprofit Organ. 2007, 18, 101–115. [Google Scholar] [CrossRef]

- Aznar-Crespo, P.; Aledo, A.; Melgarejo-Moreno, J.; Vallejos-Romero, A. Adapting Social Impact Assessment to Flood Risk Management. Sustainability 2021, 13, 3410. [Google Scholar] [CrossRef]

{kind=link}

| Criteria for Searching and Selecting Articles | Web of Science Database | Scopus Database | Description |

|---|---|---|---|

| Searching articles using the keywords | 101 | 245 | The keywords used for searching are “Social impact assessment” OR “Social performance assessment” OR “Nonfinancial performance assessment” OR “Social return assessment” OR “ESG assessment” OR “Impact investing assessment” AND “Model*”. |

| Selecting documents only in the article and review category | 84 | 214 | Documents in the article and review category were selected since those in other categories are not peer-reviewed or academic contributions. |

| Selecting articles written in English | 82 | 207 | We selected documents that are written in English. |

| Adding articles from both databases | 289 | 82 articles from the Web of Science and 207 from Scopus databases were added to a single spreadsheet. | |

| Removing duplicate documents from the lists in the databases | 231 | 58 duplicates were removed. | |

| Checking Title, Abstract and Keywords | 187 | The focus of 44 articles was not SIA models. | |

| Adding more articles after checking the grey literature (NEF—New economic foundation; Tools and Resources for Assessing Social Impact—TRASI database) | 43 | An additional 43 articles coming from grey literature are focused on SIA models. | |

| Finalizing the number of articles considered for this study | 230 | Finally, we reached 230 articles for consideration in this study. | |

| SIA Mapping | ||||||

|---|---|---|---|---|---|---|

| Groups/clusters | Clark et al. [5] | Olsen and Galimidi [47] | Zappalà and Lyons [39] | Rinaldo [48] | Maas and Liket [13] | Grieco et al. [6] |

| (1) Process models/methods | (1) Rating systems | (1) Social Accounting and Audit (SAA) | (1) Monitoring and evaluation tools | (1) Process methods | (1) Simple Social Quantitative | |

| (2) Impact models/methods | (2) Assessment systems | (2) Logic Models | (2) Quality tools | (2) Impact methods | (2) Holistic Complex | |

| (3) Monetisation models/methods | (3) Management systems | (3) Social Return on Investment (SROI) | (3) Outcome tools | (3) Monetisation | (3) Qualitative Screening | |

| - | - | - | - | - | (4) Management | |

| Grieco et al. [6] | |

|---|---|

| Variables | References |

| (1) Data typology | Nicholls [14] |

| (2) Impact typology | Rinaldo [48] |

| (3) Purpose | Clark et al. [5], Rinaldo [48], Maas and Liket [13] |

| (4) Model complexity | Zappalà and Lyons [39], Maas and Liket [13] |

| (5) Sector | Olsen and Galimidi [47] |

| (6) Time frame | Maas and Liket [13] |

| (7) Developer | Identified by the authors [6] |

| Authors | Year of Publication | No. of Models Analysed | Emerging Patterns (No.) | Sources |

|---|---|---|---|---|

| Clark et al. [5] | 2004 | 9 | 3 | GL + I |

| Olsen and Galimidi [47] | 2008 | 25 | 3 | GL + I |

| Zappalà and Lyons [39] | 2009 | N.A. | 3 | AL |

| Rinaldo [48] | 2010 | 19 | 3 | GL |

| Maas and Liket [13] | 2011 | 30 | - | AGL + I |

| Grieco et al. [6] | 2015 | 76 | 4 | AGL |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Corvo, L.; Pastore, L.; Manti, A.; Iannaci, D. Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda. Sustainability 2021, 13, 4750. https://doi.org/10.3390/su13094750

Corvo L, Pastore L, Manti A, Iannaci D. Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda. Sustainability. 2021; 13(9):4750. https://doi.org/10.3390/su13094750

Chicago/Turabian StyleCorvo, Luigi, Lavinia Pastore, Arianna Manti, and Daniel Iannaci. 2021. "Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda" Sustainability 13, no. 9: 4750. https://doi.org/10.3390/su13094750

APA StyleCorvo, L., Pastore, L., Manti, A., & Iannaci, D. (2021). Mapping Social Impact Assessment Models: A Literature Overview for a Future Research Agenda. Sustainability, 13(9), 4750. https://doi.org/10.3390/su13094750