The Incidence of Social Responsibility in the Adoption of Business Practices

Abstract

1. Introduction

2. Literature Review and Hypotheses Development

2.1. The Adoption of Corporate Social Responsibility Practices

2.2. Corporate Social Responsibility Standards

2.3. Interaction of Social Responsibility with Diversity, Environment, and Community

3. Methods

4. Results

4.1. Descriptive Analysis of the Study Variables

4.2. Correlation Analysis

4.3. Verification of the Study Hypotheses

5. Discussion of Results

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Fernández, J.; Sarria, J. Impact of Corporate Social Responsibility on Value Creation from a Stakeholder Perspective. Sustainability 2018, 10, 2062. [Google Scholar] [CrossRef]

- Witkowska, J. Corporate Social Responsability: Selected Theoretical and Em-pirical Aspects. Comp. Econ. Res. 2016, 19, 27–43. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.; Ilavarasan, V. Impact of corporate social responsibility on reputation—Insights from tweets on sustainable development goals by CEOs. Int. J. Inf. Manag. 2019, 48, 39–52. [Google Scholar] [CrossRef]

- Price, J.; Sun, W. Doing good and doing bad: The impact of corporate social responsability and irresponsability on firm performance. J. Bus. Res. 2017, 80, 82–97. [Google Scholar] [CrossRef]

- Rodríguez, C.; Ramos, E. Spirituality, consumer ethics, and sustainability: The mediating role of moral identity. J. Consum. Mark. 2018, 35, 51–63. [Google Scholar] [CrossRef]

- Charini, A.; Vagnoni, E. Differences in implementing corporate social responsibility through SA8000 and ISO 26000 standards. Research from European manufacturing. J. Manuf. Technol. Manag. 2017, 28, 438–457. [Google Scholar] [CrossRef]

- Hahn, R. ISO 26000 and the Standardization of Strategic Management Processes for Sustainability and Corporate Social Responsibility. Bus. Strategy Environ. 2013, 22, 442–455. [Google Scholar] [CrossRef]

- Androniceanu, A. Social Responsability, an Essential Strategic Option for a Sustainable Development in the Field of Bio-Economy. Amfiteatru Econ. 2019, 21, 503–519. [Google Scholar] [CrossRef]

- Mishra, S.; Modi, S. Corporate Social Responsability and Shareholder Walth: The Role of Marketing Capability. J. Mark. 2016, 80, 26–46. [Google Scholar] [CrossRef]

- He, H.; Harris, L. The impact of Covid-19 pandemic on corporate social responsibility and marketing philosophy. J. Bus. Res. 2020, 116, 176–182. [Google Scholar] [CrossRef]

- Lee, V.; Chiew, C. Interrupting transmission of COVID-19: Lessons from containment efforts in Singapore. J. Travel Med. 2020, 27, taaa039. [Google Scholar] [CrossRef]

- Wang, H.; Tong, L.; Takeuchi, R.; George, G. Corporate social responsability: An overview and new research directions. Acad. Manag. J. 2016, 59, 534–544. [Google Scholar] [CrossRef]

- Ferramosca, S.; Verona, R. Framing the evolution of corporate social responsibility as a discipline (1973–2018): A large-scale scientometric analysis. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 178–203. [Google Scholar] [CrossRef]

- De Colle, S.; Henriques, A.; Sarasvathy, S. The Paradox of Corporate Social Responsability Standards. J. Bus. Ethics 2014, 125, 177–191. [Google Scholar] [CrossRef]

- Padilla, C.; Arévalo, D.; Bustamante, M.; Vidal, C. Enterprise Social Responsibility and Financial Performance in the Plastic Industry of Ecuador. Inf. Tecnológica 2017, 28, 93–102. [Google Scholar] [CrossRef]

- Miras, M.; Carrasco, A.; Escobar, B. A review of the meta-analyzes on corporate social responsibility and financial performance. Rev. De Estud. Empresariales Segunda Época 2011, 1, 118–132. Available online: https://revistaselectronicas.ujaen.es/index.php/REE/article/view/576/522 (accessed on 15 November 2020).

- Stoian, C.; Gilman, M. Corporate Social Responsability That “Pays”: A Strategic Approach to CSR for SMEs. J. Small Bus. Manag. 2017, 55, 5–31. [Google Scholar] [CrossRef]

- Sun, W.; Yao, S.; Govind, R. Reexamining Corporate Social Responsibility and Shareholder Value: The Inverted U Shaped Relationship and the Moderation of Mar-keting Capability. J. Bus. Ethics 2019, 160, 1001–1017. [Google Scholar] [CrossRef]

- Platonova, E.; Asutay, M.; Dixon, R.; Mohammad, S. The Impact of Corporate Social Responsibility Disclosure on Financial Performance: Evidence from the GCC Islamic Banking Sector. J. Bus. Ethics 2018, 151, 451–471. [Google Scholar] [CrossRef]

- Isidro, H.; Sobral, M. The Effects of Women on Corporate Boards on Firm Value, Financial Performance, and Ethical and Social Compliance. J. Bus. Ethics 2015, 132, 1–19. [Google Scholar] [CrossRef]

- Pérez, F.; Romeo, M.; Yepes, M. The corporate social responsibility policies for the inclusion of people with disabilities as predictors of employees’ identification, commitment and absenteeism. An. De Psicol. 2018, 34, 101–107. [Google Scholar] [CrossRef]

- Abbas, J. Impact of total quality management on corporate green performance through the mediating role of corporate social responsability. J. Clean. Prod. 2020, 242, 118458. [Google Scholar] [CrossRef]

- Cuadrado, B.; García, R.; Martínez, J. Effect of the composition of the board of directors on corporate social responsibility. Span. Account. Rev. 2015, 18, 20–31. [Google Scholar] [CrossRef]

- Abdullah, S.N. The causes of gender diversity in Malaysian large firms. J. Manag. Gov. 2014, 18, 1137–1159. [Google Scholar] [CrossRef]

- Deigh, L.; Farquhar, J.; Palazzo, M.; Siano, A. Corporate social responsability: Engaging the community. Qual. Mark. Res. 2016, 19, 225–240. [Google Scholar] [CrossRef]

- Keung, C.; Wu, Q.; Zhang, H. Community Social Capital and Corporate Social Responsability. J. Bus. Ethics 2018, 152, 647–665. [Google Scholar] [CrossRef]

- Herciu, M. An Integrative Approach of Corporate Social Responsability. Stud. Bus. Econ. 2016, 11, 73–79. [Google Scholar] [CrossRef]

- ECLAC. The 2030 Agenda and the Sustainable Development Goals: An Opportunity for Latin America and the Caribbean; United Nations Publication: Santiago, Chile, 2018; Available online: https://repositorio.cepal.org/bitstream/handle/11362/40155.4/S1700334_es.pdf?sequence=18&isAllowed=y (accessed on 10 November 2020).

- Gupta, J.; Vegelin, C. Sustainable development goals and inclusive development. Int. Environ. Agreem. Politics Law Econ. 2016, 16, 433–448. [Google Scholar] [CrossRef]

- Sethi, S.; Rovenpor, J.; Demir, M. Enhancing the quality of Reporting in Corporate Social Responsibility Guidance Documents: The Roles of ISO 26000, Global Reporting Initiative and CSR-Sustainability Monitor. Bus. Soc. Rev. 2017, 122, 139–163. [Google Scholar] [CrossRef]

- Jha, A.; Cox, J. Corporate social responsibility and social capital. J. Bank. Financ. 2015, 60, 252–270. [Google Scholar] [CrossRef]

- Chilean Ministry of Economy, Development and Tourism. Creates the Social Responsibility Council for Sustainable Development; Ministerio de Hacienda: Santiago, Chile, 2013.

- Chilean Commission for the Financial Market. General Standard No. 386; Commission for the Financial Market: Santiago, Chile, 2015. [Google Scholar]

- Jaén, M.; Auleta, N.; Bruni, J.; Pocaterra, M. Bibliometric analysis of indexed research on corporate social responsibility in Latin America (2000–2017). Acad. Rev. Latinoam. Adm. 2018, 31, 105–135. [Google Scholar] [CrossRef]

- Harjoto, M.; Laksmana, I.; Lee, R. Board Diversity and Corporate Social Responsibility. J. Bus. Ethics 2015, 132, 641–660. [Google Scholar] [CrossRef]

- Grosser, K. Corporate Social Responsibility and Multi-Stakeholder Governance: Pluralism, Feminist Perspectives and Women’s NGOs. J. Bus. Ethics 2016, 137, 65–81. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C. Board Composition and Corporate Social Responsibility: The Role of Diversity, Gender, Strategy and Decision Making. J. Bus. Ethics 2016, 138, 327–347. [Google Scholar] [CrossRef]

- Ben, W.; Chang, M.; Mclkenny, P. Board Gender Diversity and Corporate Response to Sustainability Initiatives: Evidence from the Carbon Disclosure Project. J. Bus. Ethics 2017, 142, 369–383. [Google Scholar] [CrossRef]

- Orazalin, N.; Baydauletov, M. Corporate social responsibility strategy and corporate environmental and social performance: The moderating role of board gender diversity. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1664–1676. [Google Scholar] [CrossRef]

- Zaid, M.; Wang, M.; Adib, M.; Sahyouni, A.; Abuhijleh, S. Boardroom nationality and gender diversity: Implications for corporate sustainability performance. J. Clean. Prod. 2020, 251, 119652. [Google Scholar] [CrossRef]

- Thekdi, S. Risk Management Should Play a Stronger Role in Developing and Implementing Social Responsibility Policies for Organization. Risk Anal. 2016, 36, 870–873. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board Attributes, Corporate Social Responsibility Strategy, and Corporate Environmental and Social Performance. J. Bus. Ethics 2016, 135, 569–585. [Google Scholar] [CrossRef]

- Yang, Y.; Zheng, X.; Sun, Z. Coal Resource Security Assessment in China: A Study Using Entropy-Weight-Based TOPSIS and BP Neural Network. Sustainability 2020, 12, 2294. [Google Scholar] [CrossRef]

- Moyo, T.; Duffett, R.; Knott, B. Environmental Factors and Stakeholders Influence on Professional Sport Organisations Engagement in Sustainable Corporate Social Responsibility: A South African Perspective. Sustainability 2020, 12, 4504. [Google Scholar] [CrossRef]

- Contini, M.; Annunziata, E.; Rizzi, F.; Frey, M. Exploring the influence of Corporate Social Responsibility (CSR) domains on consumers’ loyalty: An experiment in BRICS countries. J. Clean. Prod. 2020, 247, 119158. [Google Scholar] [CrossRef]

- Yu, Z.; Khan, S.; Liu, Y. Exploring the Role of Corporate Social Responsibility Practices in Enterprises. J. Adv. Manuf. Syst. 2020, 19, 339–461. [Google Scholar] [CrossRef]

- Lee, C.-K.; Kim, J.; Kim, J. Impact of a gaming company’s CSR on resident’s perceived benefits, quality of life and support. Tour. Manag. 2018, 64, 281–290. [Google Scholar] [CrossRef]

- Hernández, R.; Fernández, C.; Baptista, M.D. Investigation Methodology, 6th ed.; McGraw-Hill/Interamericana Editors: Mexico City, Mexico, 2014. [Google Scholar]

- INE. Instructions for the Use of the Database of the Fifth Longitudinal Survey of Companies; Instituto Nacional de Estadísticas: Santiago, Chile, 2019. Available online: https://www.economia.gob.cl/wp-content/uploads/2019/03/Instructivo-uso-de-base-de-datos-ELE-5.pdf (accessed on 15 May 2020).

- Nakamura, E. Is Corporate Social Responsibility in Japanese Firms at the Theoretically Derived Achievable Level? An Analysis of CSR Inefficiency Using a Stochas-tic Frontier Model. Bus. Soc. Rev. 2016, 121, 271–295. [Google Scholar] [CrossRef]

- Strand, R.; Freeman, R.; Hockert, K. Corporate Social Responsability and Sustainability in Scandinavia: An Overview. J. Bus. Ethics 2016, 127, 1–15. [Google Scholar] [CrossRef]

- Smith, J. Corporate responsibility and the plurality of market aims. Bus. Soc. Rev. 2019, 124, 183–199. [Google Scholar] [CrossRef]

- Shi, G.; Sun, J. Corporate Bond Convenants and Social Responsability Investment. J. Bus. Ethics 2015, 131, 285–303. [Google Scholar] [CrossRef]

{kind=link}

| No. | Economic Sectors | Population | Sample | ||

|---|---|---|---|---|---|

| Quantity | Frequency | Quantity | Frequency | ||

| 1 | Accommodation and meal service activities | 152 | 2% | 79 | 2% |

| 2 | Service activities | 705 | 11% | 359 | 11% |

| 3 | Financial and insurance activities | 455 | 7% | 355 | 11% |

| 4 | Professional, scientific and technical activities | 736 | 11% | 392 | 12% |

| 5 | Agriculture, forestry and fishing | 524 | 8% | 206 | 6% |

| 6 | Wholesale and retail | 1.607 | 25% | 706 | 22% |

| 7 | Construction | 462 | 7% | 201 | 6% |

| 8 | Mining and quarrying | 245 | 4% | 123 | 4% |

| 9 | Manufacturing industries | 655 | 10% | 289 | 9% |

| 10 | Information and communications | 206 | 3% | 116 | 4% |

| 11 | Other services | 285 | 4% | 122 | 4% |

| 12 | Electricity, gas and water supply | 62 | 1% | 57 | 2% |

| 13 | Transport and storage | 386 | 6% | 174 | 5% |

| Total | 6.480 | 100% | 3.179 | 100% | |

| Variable | Elements | Operationalization by Company | Source |

|---|---|---|---|

| Dependents | |||

| Diversity Dimension | Degree of formalization of policies related to the Diversity dimension | ((Diversity and Inclusion Policy + Gender Policy + Disability Inclusion Policy)/3) * 100 | [2,3,4,5,9,17,21,22,35,36,37,38,40,50] |

| Environmental Dimension | Degree of formalization of policies related to the Environmental dimension | ((Energy Efficiency Policy + Waste Management Policy + Carbon Footprint Policy + Water Footprint Policy)/4) * 100 | |

| Community dimension | Degree of formalization of policies related to the Community dimension | ((Community Collaboration Policy)/1) * 100 | |

| Independent | |||

| CSR dimension | Measure the degree of formalization of policies related to the ethical and CSR dimension | ((Code of Ethics Policy + CSR Policy)/2) * 100 | [2,3,5,9,20,21,22,31,32,33,34,35,36,37,38,39,40,41,42,43,44,50] |

| Control | |||

| Gender Diversity in the Board | Control the influence of gender diversity on the board | Do you have a woman on the board?

| [1,3,4,9,17,45,46,47] |

| Legal Organization | Control the legal organization of the company | Company type. Yes = 1, No = 0:

| |

| Size | Control the size of the company | Company size. Yes = 1, No = 0:

| |

| N° Sectors | Economic Sectors | Sample Distribution by Size | |||||

|---|---|---|---|---|---|---|---|

| Big | Medium | Small | Micro | Quantity | Freq. | ||

| 1 | Accommodation and meal service activities | 30 | 17 | 16 | 16 | 79 | 2% |

| 2 | Service activities | 231 | 52 | 53 | 23 | 359 | 11% |

| 3 | Financial and insurance activities | 286 | 69 | 0 | 0 | 355 | 11% |

| 4 | Professional, scientific and technical activities | 250 | 32 | 94 | 16 | 392 | 12% |

| 5 | Agriculture, forestry and fishing | 45 | 51 | 59 | 51 | 206 | 6% |

| 6 | Wholesale and retail | 510 | 106 | 45 | 45 | 706 | 22% |

| 7 | Construction | 68 | 49 | 70 | 14 | 201 | 6% |

| 8 | Mining and quarrying | 41 | 21 | 45 | 16 | 123 | 4% |

| 9 | Manufacturing industries | 152 | 21 | 75 | 41 | 289 | 9% |

| 10 | Information and communications | 71 | 6 | 21 | 18 | 116 | 4% |

| 11 | Other services | 22 | 12 | 65 | 23 | 122 | 4% |

| 12 | Electricity, gas and water supply | 35 | 22 | 0 | 0 | 57 | 2% |

| 13 | Transport and storage | 104 | 16 | 34 | 20 | 174 | 5% |

| Total | 1.845 | 474 | 577 | 283 | 3.179 | 100% | |

| 58% | 15% | 18% | 9% | 100% | |||

| N° Sectors | Economic Sectors | Corporate Social Responsibility (CSR) Policy | Code of Ethics Policy | Diversity and Inclusion Policy | Gender Policy | Disability Inclusion Policy | Energy Efficiency Policy | Waste Management Policy | Carbon Footprint Policy | Water Footprint Policy | Community Collaboration Policy | Total Policies | Degree of Coverage by Sector |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Accommodation and meal service activities | 33 | 48 | 37 | 27 | 33 | 28 | 51 | 9 | 12 | 33 | 311 | 39% |

| 2 | Service activities | 186 | 260 | 155 | 100 | 137 | 104 | 148 | 43 | 31 | 141 | 1.305 | 36% |

| 3 | Financial and insurance activities | 158 | 341 | 134 | 92 | 118 | 68 | 60 | 31 | 13 | 121 | 1.136 | 32% |

| 4 | Professional, scientific and technical activities | 203 | 304 | 170 | 114 | 115 | 126 | 167 | 59 | 40 | 158 | 1.456 | 37% |

| 5 | Agriculture, forestry and fishing | 101 | 94 | 64 | 42 | 47 | 80 | 138 | 22 | 35 | 97 | 720 | 35% |

| 6 | Wholesale and retail | 364 | 525 | 306 | 219 | 239 | 248 | 357 | 81 | 67 | 238 | 2.644 | 37% |

| 7 | Construction | 103 | 121 | 75 | 50 | 61 | 57 | 109 | 22 | 13 | 63 | 674 | 34% |

| 8 | Mining and quarrying | 75 | 79 | 54 | 33 | 35 | 51 | 90 | 27 | 27 | 62 | 533 | 43% |

| 9 | Manufacturing industries | 141 | 175 | 127 | 77 | 87 | 118 | 198 | 41 | 41 | 112 | 1.117 | 39% |

| 10 | Information and communications | 46 | 102 | 45 | 38 | 44 | 39 | 38 | 22 | 8 | 49 | 431 | 37% |

| 11 | Other services | 50 | 81 | 47 | 31 | 39 | 36 | 49 | 14 | 11 | 54 | 412 | 34% |

| 12 | Electricity, gas and water supply | 35 | 49 | 22 | 14 | 14 | 29 | 44 | 23 | 14 | 35 | 279 | 49% |

| 13 | Transport and storage | 103 | 119 | 75 | 48 | 50 | 64 | 90 | 30 | 19 | 73 | 671 | 39% |

| Total | 1.598 | 2.298 | 1.311 | 885 | 1.019 | 1.048 | 1.539 | 424 | 331 | 1.236 | 11.689 | 37% | |

| Degree of coverage | 50% | 72% | 41% | 28% | 32% | 33% | 48% | 13% | 10% | 39% | 37% | ||

| Dimension | Policies | N | Sum | Average | D° Adop. | Stand. Desvt. | Variance |

|---|---|---|---|---|---|---|---|

| CSR | Corporate Social Responsibility | 3.179 | 1.598 | 0.503 | 50% | 0.500 | 0.250 |

| Code of Ethics | 3.179 | 2.298 | 0.723 | 72% | 0.448 | 0.200 | |

| Total Dimension | 6.358 | 3.896 | 1.226 | 61% | 0.726 | 0.528 | |

| Diversity | Diversity and Inclusion | 3.179 | 1.311 | 0.412 | 41% | 0.492 | 0.242 |

| Gender | 3.179 | 885 | 0.278 | 28% | 0.448 | 0.201 | |

| Inclusion of Disabled | 3.179 | 1.019 | 0.321 | 32% | 0.467 | 0.218 | |

| Total Dimension | 9.537 | 3.215 | 1.011 | 34% | 1.172 | 1.372 | |

| Environmental | Energy Efficiency | 3.179 | 1.048 | 0.330 | 33% | 0.470 | 0.221 |

| Waste Management | 3.179 | 1.539 | 0.484 | 48% | 0.500 | 0.250 | |

| Carbon Footprint | 3.179 | 424 | 0.133 | 13% | 0.340 | 0.116 | |

| Water Footprint | 3.179 | 331 | 0.104 | 10% | 0.305 | 0.093 | |

| Total Dimension | 12.716 | 3.342 | 1.051 | 26% | 1.206 | 1.455 | |

| Community | Collaboration with the Community | 3.179 | 1.236 | 0.389 | 39% | 0.488 | 0.238 |

| Total Dimension | 3.179 | 1.236 | 0.389 | 39% | 0.488 | 0.238 | |

| Totals | 31.790 | 11.689 | 3.677 | 37% | 2.566 | 6.586 | |

| N° | Policies | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | CSR | 1.000 | ||||||||||

| 2 | Code of Ethics | 0.173 * | 1.000 | |||||||||

| 3 | Diversity and Inclusion | 0.320 * | 0.217 * | 1.000 | ||||||||

| 4 | Gender | 0.258 * | 0.253 * | 0.562 * | 1.000 | |||||||

| 5 | Inclusion of Disabled | 0.277 * | 0.187 * | 0.525 * | 0.530 * | 1.000 | ||||||

| 6 | Energy Efficiency | 0.268 * | 0.077 * | 0.217 * | 0.259 * | 0.257 * | 1.000 | |||||

| 7 | Waste Management | 0.135 * | −0.102 * | 0.087 * | 0.124 * | 0.126 * | 0.419 * | 1.000 | ||||

| 8 | Carbon Footprint | 0.255 * | 0.127 * | 0.220 * | 0.279 * | 0.256 * | 0.400 * | 0.325 * | 1.000 | |||

| 9 | Water Footprint | 0.228 * | 0.096 * | 0.217 * | 0.273 * | 0.240 * | 0.370 * | 0.298 * | 0.687 * | 1.000 | ||

| 10 | Collaboration with the Community | 0.315 * | 0.096 * | 0.217 * | 0.239 * | 0.260 * | 0.340 * | 0.241 * | 0.306 * | 0.294 * | 1.000 | |

| 11 | Total Policies | 0.578 * | 0.369 * | 0.639 * | 0.660 * | 0.645 * | 0.626 * | 0.466 * | 0.618 * | 0.586 * | 0.583 * | 1.000 |

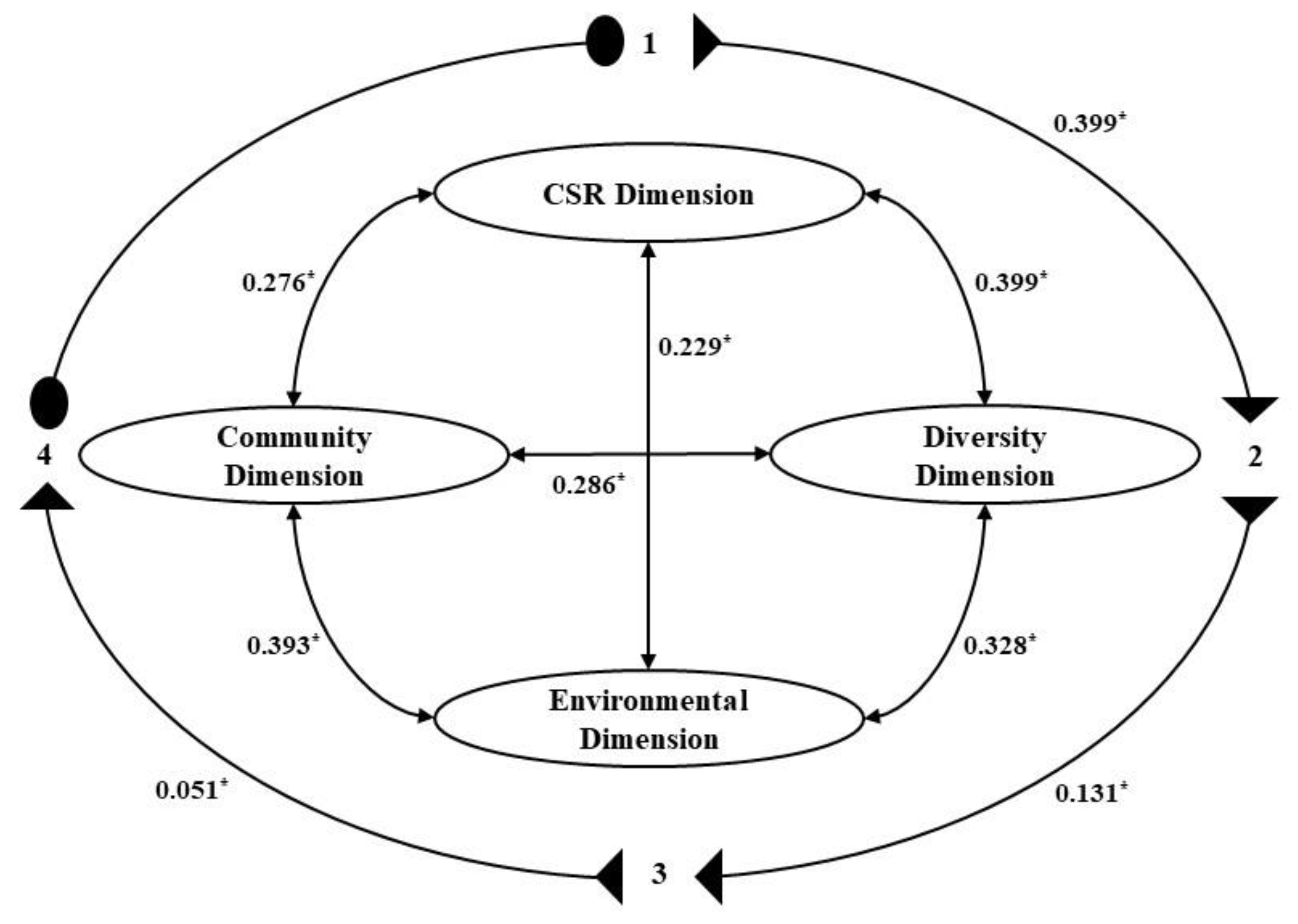

| N° | Dimension | 1 | 2 | 3 | 4 | 5 | Sum of correlations | |||||

| 1 | CSR | 1.000 | 0.904 * | |||||||||

| 2 | Diversity | 0.399 * | 1.000 | 1.013 * | ||||||||

| 3 | Environmental | 0.229 * | 0.328 * | 1.000 | 0.950 * | |||||||

| 4 | Community | 0.276 * | 0.286 * | 0.393 * | 1.000 | 0.955 * | ||||||

| 5 | Total Dimension | 0.625 * | 0.778 * | 0.760 * | 0.583 * | 1.000 | ||||||

| Dim. | N° | Economic Sectors | Const. | Coef. CSR | Stand. Error | R2 Fitted | Global Signif. | Control Variables | ||

|---|---|---|---|---|---|---|---|---|---|---|

| Gender | LO | Size | ||||||||

| a = Diversity Dimension H1 | 1 | Accommodation and meal service activities | 0.295 ** | 0.448 * | 0.105 | 0.297 | 0.000 | No | No | No |

| 2 | Service activities | −0.002 | 0.508 * | 0.055 | 0.181 | 0.000 | Yes | Yes | No | |

| 3 | Financial and insurance activities | 0.173 * | 0.372 * | 0.071 | 0.150 | 0.000 | Yes | No | Yes | |

| 4 | Professional, scientific and technical activities | 0.114 ** | 0.438 * | 0.057 | 0.142 | 0.000 | No | No | No | |

| 5 | Agriculture, forestry and fishing | −0.003 | 0.392 * | 0.058 | 0.191 | 0.000 | Yes | No | No | |

| 6 | Wholesale and retail | 0.102 * | 0.430 * | 0.038 | 0.162 | 0.000 | Yes | No | No | |

| 7 | Construction | 0.840 | 0.300 * | 0.066 | 0.147 | 0.000 | Yes | Yes | No | |

| 8 | Mining and quarrying | 0.091 | 0.448 * | 0.086 | 0.238 | 0.000 | No | No | No | |

| 9 | Manufacturing industries | 0.113 ** | 0.426 * | 0.050 | 0.231 | 0.000 | No | No | No | |

| 10 | Information and communications | −0.194 | 0.651 * | 0.127 | 0.161 | 0.002 | No | No | No | |

| 11 | Other services | −0.102 | 0.576 * | 0.089 | 0.241 | 0.000 | No | No | No | |

| 12 | Electricity, gas and water supply | −0.176 | 0.584 * | 0.160 | 0.161 | 0.032 | No | No | No | |

| 13 | Transport and storage | 0.143 *** | 0.425 * | 0.075 | 0.166 | 0.000 | No | No | No | |

| Total sectors diversity dimension | 0.112 * | 0.419 * | 0.018 | 0.162 | 0.000 | No | No | Yes | ||

| Dim. | N° | Economic Sectors | Const. | Coef. CSR | Stand. Error | R2 Fitted | Global Signif. | Control Variables | ||

|---|---|---|---|---|---|---|---|---|---|---|

| Gender | LO | Size | ||||||||

| b = Environmental Dimension H2 | 1 | Accommodation and meal service activities | 0.155 | 0.275 * | 0.098 | 0.014 | 0.366 | No | No | No |

| 2 | Service activities | 0.125 * | 0.233 * | 0.044 | 0.071 | 0.000 | No | No | No | |

| 3 | Financial and insurance activities | −0.025 | 0.184 * | 0.047 | 0.067 | 0.000 | Yes | No | No | |

| 4 | Professional, scientific and technical activities | 0.099 ** | 0.211 * | 0.047 | 0.073 | 0.000 | No | No | No | |

| 5 | Agriculture, forestry and fishing | 0.365 * | 0.106 ** | 0.048 | 0.032 | 0.096 | No | No | No | |

| 6 | Wholesale and retail | 0.172 * | 0.185 * | 0.030 | 0.064 | 0.000 | No | No | No | |

| 7 | Construction | 0.180 * | 0.175 * | 0.051 | 0.103 | 0.001 | No | No | Yes | |

| 8 | Mining and quarrying | 0.314 * | 0.195 ** | 0.077 | 0.120 | 0.007 | No | No | No | |

| 9 | Manufacturing industries | 0.252 * | 0.207 * | 0.041 | 0.151 | 0.000 | No | No | No | |

| 10 | Information and communications | 0.039 | 0.445 * | 0.092 | 0.220 | 0.000 | No | No | No | |

| 11 | Other services | 0.035 | 0.304 * | 0.072 | 0.118 | 0.008 | No | No | No | |

| 12 | Electricity, gas and water supply | 0.338 *** | 0.280 ** | 0.135 | 0.210 | 0.011 | Yes | No | No | |

| 13 | Transport and storage | 0.268 * | 0.169 * | 0.060 | 0.095 | 0.004 | No | No | Yes | |

| Total environmental dimension sectors | 0.172 * | 0.185 * | 0.015 | 0.056 | 0.000 | No | No | Yes | ||

| Dim. | N° | Economic Sectors | Const. | Coef. CSR | Stand. Error | R2 Fitted | Global Signif. | Control Variables | ||

|---|---|---|---|---|---|---|---|---|---|---|

| Gender | LO | Size | ||||||||

| c = Community Dimension H3 | 1 | Accommodation and meal service activities | 0.052 | 0.471 * | 0.149 | 0.114 | 0.047 | No | No | No |

| 2 | Service activities | 0.211 * | 0.372 * | 0.072 | 0.075 | 0.000 | No | No | No | |

| 3 | Financial and insurance activities | -0.311 * | 0.778 * | 0.084 | 0.217 | 0.000 | Yes | Yes | No | |

| 4 | Professional, scientific and technical activities | 0.235 * | 0.355 * | 0.074 | 0.066 | 0.000 | No | No | No | |

| 5 | Agriculture, forestry and fishing | 0.505 * | 0.308 * | 0.083 | 0.130 | 0.000 | No | No | No | |

| 6 | Wholesale and retail | 0.281 * | 0.199 * | 0.049 | 0.043 | 0.000 | Yes | No | Yes | |

| 7 | Construction | 0.160 ** | 0.425 * | 0.087 | 0.110 | 0.000 | No | No | Yes | |

| 8 | Mining and quarrying | 0.268 * | 0.426 * | 0.111 | 0.194 | 0.000 | No | No | No | |

| 9 | Manufacturing industries | 0.185 * | 0.388 * | 0.069 | 0.110 | 0.000 | No | No | No | |

| 10 | Information and communications | 0.245 | 0.588 * | 0.150 | 0.133 | 0.006 | No | No | No | |

| 11 | Other services | 0.056 | 0.373 * | 0.118 | 0.128 | 0.005 | Yes | No | No | |

| 12 | Electricity, gas and water supply | 0.510 *** | 0.357 *** | 0.209 | 0.122 | 0.070 | No | No | No | |

| 13 | Transport and storage | 0.183 ** | 0.471 * | 0.094 | 0.165 | 0.000 | No | No | No | |

| Total sectors community dimension | 0.194 * | 0.360 * | 0.023 | 0.092 | 0.000 | Yes | No | Yes | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Arenas-Torres, F.; Bustamante-Ubilla, M.; Campos-Troncoso, R. The Incidence of Social Responsibility in the Adoption of Business Practices. Sustainability 2021, 13, 2794. https://doi.org/10.3390/su13052794

Arenas-Torres F, Bustamante-Ubilla M, Campos-Troncoso R. The Incidence of Social Responsibility in the Adoption of Business Practices. Sustainability. 2021; 13(5):2794. https://doi.org/10.3390/su13052794

Chicago/Turabian StyleArenas-Torres, Felipe, Miguel Bustamante-Ubilla, and Roberto Campos-Troncoso. 2021. "The Incidence of Social Responsibility in the Adoption of Business Practices" Sustainability 13, no. 5: 2794. https://doi.org/10.3390/su13052794

APA StyleArenas-Torres, F., Bustamante-Ubilla, M., & Campos-Troncoso, R. (2021). The Incidence of Social Responsibility in the Adoption of Business Practices. Sustainability, 13(5), 2794. https://doi.org/10.3390/su13052794