1. Introduction

China has announced its carbon emission reduction targets for 2030 and 2060. There are few options for China’s power system to fulfill these targets except two alternatives. One is to integrate increasing shares of generations from variable renewable energy (VRE) [

1]. The other is to make clean and effective utilization of thermal power units, which have been accounting for a significant share of China’s power supply [

2]. The former inevitably produces higher demand for system flexibility, which is mainly provided by thermal power units in China [

3]. The more VRE is integrated, the lower load rate these inflexible units operate at, which hinders higher operating hours, longer life cycle, and better energy efficiency for thermal power units recommended by the latter [

4].

To alleviate this contradiction, the Chinese government has retrofitted thermal power units to be more flexible with lower minimum load levels, faster ramping rate, and shorter startup-shutdown time by a series of flexibility modification schemes since 2016 [

5,

6]. Prior researches, therefore, evaluate whether the thermal power units are modified to be flexible enough by adopting these schemes [

7,

8]. Flexibility modification of thermal power units has been proved to be the most feasible approach for China to add power system flexibility in the short term [

9,

10]. It has an advantage in lower lead times and costs compared to investing in gas-fired peak regulation power stations and pumped storages [

11]. Until the end of 2019, about 57.75 MW flexibility modification of thermal power units had been completed, accounting for 25% of the total modification plan [

12].

Financial incentives have been provided for coal power plants to actively go flexible, represented by the release of the deep peak regulation ancillary service market since 2017 [

13]. It is a motivation schedule for reducing the power output of thermal power units with different compensation prices for several load intervals [

14]. This new revenue stream has been important in offsetting revenue losses for thermal power units due to their lower operating hours [

15]. In 2019, thermal power units released 18.9 billion kWh electricity for adding VRE consumption, merely driven by deep peak regulation ancillary services market [

16].

However, thermal power generators are not motivated enough to participate in implementing flexibility modification and deep peak regulation themselves, not only due to insufficient compensation and uncertain long term expectations for this incentive policy but also thanks to increasing risks for safe and economical operation and decreasing energy efficiency [

12]. Besides, there is still a problem of insufficient funds for renovation since these generators have been faced with tremendous operational pressure in recent years, considering their continuous declines in utilization hours.

Therefore, the market design of this financial aid needs to be further improved so that more flexibility modifications could be implemented [

17]. Before that, it is crucial to determine when to start up or shut down power units and how to dispatch their power outputs to meet system power demand and spinning reserve requirements while satisfying generation constraints over a specific time series [

18,

19]. These problems are traditionally called unit commitment (UC).

The most popular solution technique for this large-scale, mixed-integer, combinatorial and nonlinear programming problem is mixed-integer linear programming (MILP) [

20,

21]. The efficient optimized commercial solvers and various toolboxes developed for this technique lead to its flexible and convenient application [

22]. A typical modeling framework called MILP-UC was developed in 2006 to solve UC problems by MILP techniques [

23]. Based on this research, this paper further applies this model in China’s policy scenarios, but the objective function and constraints of this MILP-UC model are remodified according to the

Production Simulation of New Energy Power System developed by China Electric Power Research Institute [

24].

This paper aims to seek out a pathway for future high VRE integration based on practical experience in flexibility modification of thermal power units and the deep peak regulation ancillary service market. The policy effects on timely completion for planned VRE integration, adequate motivation for thermal power units to implement flexibility modification, and activeness for modified units to participate in deep peak regulation are evaluated. The analysis framework highlighted in this study contains MILP-UC modeling, which is applied to acquire economical dispatching results. Three flexibility modification schemes and two price rules for the deep peak regulation ancillary service market are established and simulated on this basis. The comparisons among three modification schemes and sensitivity analysis indicate whether and when a scheme ought to be adopted and how flexible a modification scheme should become. The discussions towards added revenue from a single market, a dual market, or an added “cash inflow” including reduced generation cost for each scheme under typical VRE curtailment rate explain which price rule applies to what situation. Results provide compelling evidence for the promoting effect of this policy mix on integrating VRE and suggest that this analysis framework appears to be effective in selecting flexibility modification schemes and future policy optimization.

The remaining sections are outlined as follows.

Section 2 introduces a brief description of the MILP-UC formulation, highlights an analysis framework based on this modeling, and establishes several policy scenarios for simulation. In

Section 3, the results for flexibility modification and deep peak regulation ancillary service market are discussed in detail.

Section 4 concludes.

3. Results and Discussions

3.1. Flexibility Modification of Thermal Power Units

3.1.1. Comparison among Three Modification Schemes

The flexibility performance of a power unit is determined by its minimum load rate, ramping rate, startup time, and shutdown time. Thus, flexibility modification aims to retrofit thermal power units (especially coal-fired power units) to occupy a higher regulation depth, to be quickly started, adjusted, and stopped.

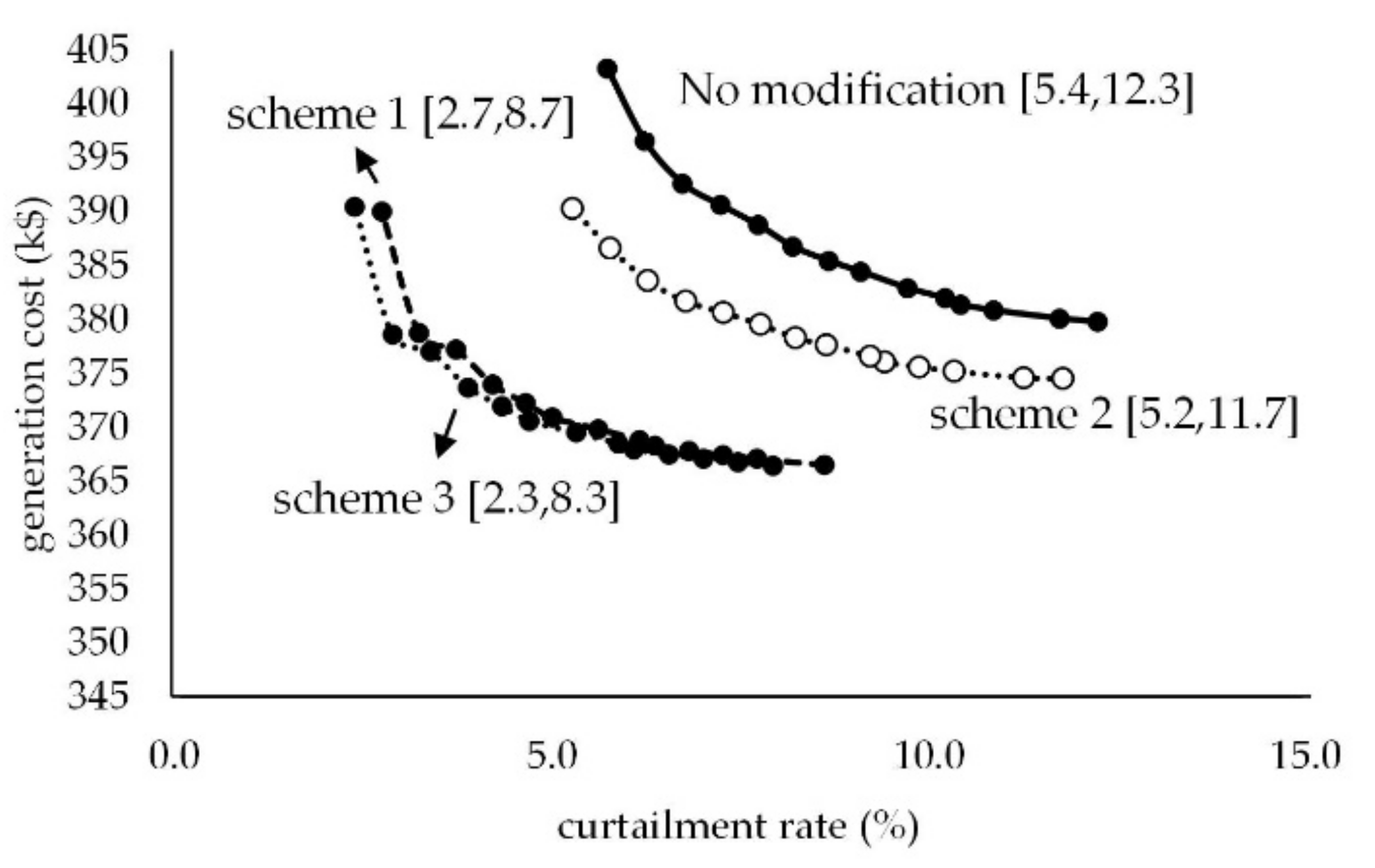

As illustrated in

Figure 1, the more flexible the thermal power units become, the lower the curtailment rate is. Under the most economical dispatching, each scheme could realize the minimum generation cost under a certain curtailment rate. These certain rates for scheme 1 and scheme 3 achieve 8.7% and 7.9%, separately reduced by 3.6% and 4.4% compared with the basic scheme. In contrast, the same decrease fulfilled by scheme 2 is only 0.6%. Thus, scheme 3 and scheme 1 inevitably bring more VRE integration than scheme 2. Each scheme has a certain curtailment interval, which means curtailment rate value must be involved in this interval once the scheme is adopted. The minimum limit of interval means the lowest curtailment rate this scheme could achieve, while the maximum limit of interval means the best curtailment rate with a minimum generation cost. These intervals are marked beside corresponding curves in

Figure 1. Interval length as well as maximum and minimum interval limits become lower from “no modification”, “scheme 2”, and “scheme 1” to “scheme 3”.

Under a certain curtailment rate, three modification schemes all enjoy apparent drops in generation cost compared with the basic one, as shown in

Figure 1. As the curtailment rate drops down, the increased rate of generation cost for each scheme keeps going up. This is more prominent for scheme 1 and scheme 3. When the curtailment rate is below 5%, the generation cost explosively grows and reaches an extremely high floor. When it is between 5% and 10%, the generation cost drops with the increase of curtailment rate more slowly. However, the generation cost for scheme 2 and the basic scheme without modification during curtailment rate interval from 5 to 10% declines faster. For curtailment rate above 10%, scheme 2 and the basic one could achieve a minimum and stable generation cost.

3.1.2. Sensitivity Analysis

China plans to supply an increasing share of its generation from VRE. Provinces across mainland China have different electricity supply structures. For some provinces near the national load center, such as Guangdong province, the VRE integration is so low that the fluctuation of VRE power output cannot influence the dispatching result. In contrast, for some provinces near the VRE resources in Northeast and Northwest China, the instantaneous power output for VRE could achieve 80% of its consumption load, which can easily affect the dispatching results of unit commitment.

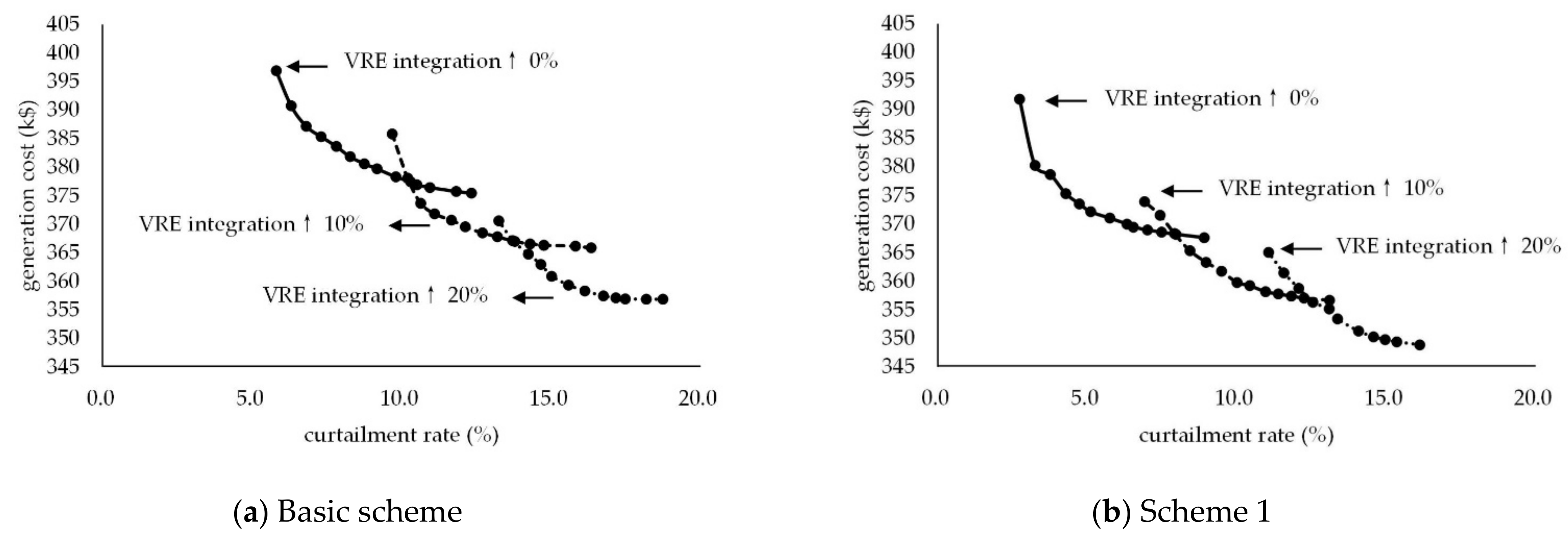

A high share of VRE integration is considered in this case. As illustrated in

Figure 2, when the VRE integration level increases by 10%, the total generation cost for both schemes drops; meanwhile, the curtailment rate becomes higher. This circumstance becomes more obvious if the VRE integration level increases by 20%.

The curtailment interval varies after flexibility modification, as shown in

Table 4. The minimum and the maximum interval limits and the interval length for scheme 1 become smaller. The decrease for these two limits and interval length from the basic scheme to scheme 1 tends to be lower when VRE integration keeps going high. The promotion effect for flexibility modification is more obvious under lower VRE integration.

In particular, there are two nodes for three curves in

Figure 2. For the basic scheme, it is more economical to increase VRE integration by 10% due to lower total generation cost when the stipulated curtailment rate is higher than 10.4%. Similarly, it is more economical to increase VRE integration by 20% when the stipulated curtailment rate is even higher than 13.7%. As for scheme 1, these two critical points for the curtailment rate are 7.7% and 11.4%. The flexibility modification releases more possibility for integrating high shares of VRE with relatively low curtailment rate.

Electricity load determines total VRE consumption; the fluctuation of load also puts forward a higher requirement for system flexibility. In China, the present peak regulation capacity and the regulation performance of thermal power units are relatively sufficient to track the rolling electricity load alone but are not enough to further shave the variable power output.

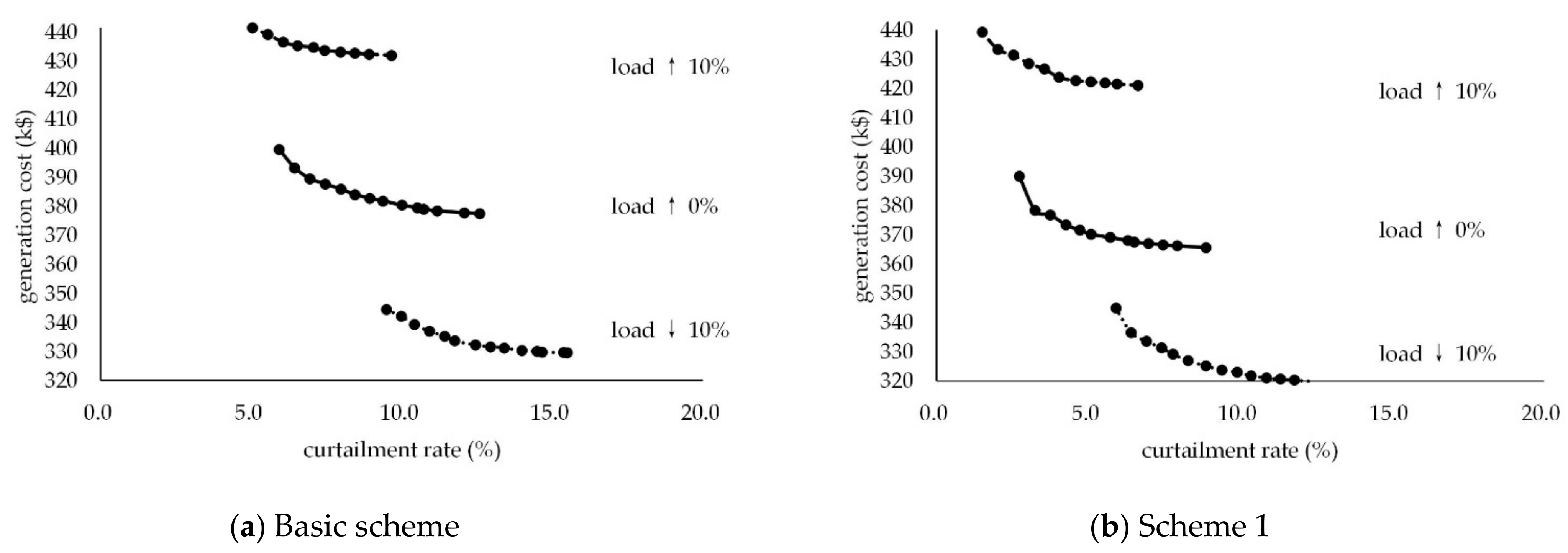

Total increase and decrease for electricity load are both considered in this case. As illustrated in

Figure 3, when the load drops by 10%, VRE power output for both schemes occupies more of the electricity load, which increases the VRE curtailment rate. On the contrary, the curtailment rate declines when the electricity load increases by 10%. The generation cost keeps the same change as electricity load considering supply–demand balance.

The curtailment rate interval under different electricity loads varies after flexibility modification, as shown in

Table 5. The minimum and the maximum interval limits for scheme 1 become smaller. The increase for these two limits when electricity load drops by 10% is higher than the decrease for them when load rises by 10%. This increase or decrease for scheme 1 is lower than that for the basic scheme. The change of curtailment rate interval is less sensitive to electricity load after flexibility modification.

There are no nodes for the three curves in

Figure 3. The maximum or the minimum limit of curtailment rate interval become critical points. For the basic scheme, more electricity load should be added if the stipulated curtailment rate is below 5.8%, and some electricity load could be removed if it is above 12.3%. As for scheme 1, the two critical points for the curtailment rate are 2.7% and 8.7%. These critical points provide a reference for electricity substitution and demand-side response preparing for further implementation in China.

3.1.3. Discussions

Considering the comparison between different modification schemes alone, if the future targeted curtailment rate is between 5% and 10%, scheme 1 and scheme 3 have a similar and better effect on completing the administrative task of reducing curtailment rate under high VRE penetration. The generation cost is still within the controllable and acceptable range. To integrate more share of VRE with a curtailment rate lower than 5%, only these two schemes could be adopted, but inevitably high generation cost remains to be paid. If there is no severe constraint in curtailment rate, for instance, if it could be above 10%, there is no need for large-scale and in-depth flexibility modification. Scheme 2 or even no modification is enough to achieve the target.

However, if the economic effect is firstly taken into consideration, results are changed. Considering the generation cost of unit commitment only, there is no doubt to choose scheme 3 due to its lowest curtailment rate under a certain cost value. The flexibility modification decreases the total generation cost of the VRE thermal power unit commitment. If the modification cost is further considered, why should this little power system choose a more expensive scheme since scheme 1 has a similar effect to scheme 3? There is also no doubt that scheme 1 will be chosen, but whether to choose scheme 1 or scheme 2 on this basis remains a question. It mostly depends on whether or not the reduced VRE curtailment rate is worth the higher modification cost.

Therefore, to integrate an increasing share of VRE, flexibility modification of thermal power units is necessary, but more modification and more flexibility improvement do not indicate inevitability. It depends on the trade-offs between cost reduction and target completion. Since generation cost mainly consists of coal consumption cost in China, this trade-off also reflects the balance between carbon emission (produced by coal consumption) and compulsory VRE curtailment level. The increased VRE integration offsets some carbon emissions by substituting previous thermal power integration, but the lower the VRE curtailment level is, the higher the carbon emission produced by per-kWh coal-fired power generation will be. Whether the total carbon emission varies after these three schemes are adopted remains to be investigated from the perspective of the whole power system.

The sensitivity analysis further reveals a fact that flexibility modification of thermal power units is an effective approach to reduce VRE curtailment, but it will be a little less effective under future high VRE integration. More approaches should be applied for the occasion. Besides, maintaining a proper curtailment rate contributes to integrating high shares of VRE, and the best critical point for introducing higher VRE integration could be determined according to regulatory requirements for curtailment rate. Flexibility modification also contributes to improving these critical points. It is also proved that flexibility modification improves VRE integration capability to resist curtailment risks under low electricity load. Additionally, flexibility modification of thermal power units makes it easier for demand-side sources to participate in reducing VRE curtailment rate and releases pressure for integrating more VRE when electricity load growth slows down.

3.2. Deep Peak Regulation Ancillary Service Market

3.2.1. Added Electricity for Dual Market

As illustrated in

Table A2, for five typical curtailment rates, 24 h time–series power outputs of modified units under scheme 1, scheme 2, scheme 3, and the basic scheme are separately given. For every modified unit, its dispatched 24 h time–series power outputs vary from the related one for the basic scheme after flexibility modification. For three modification schemes under five stipulated curtailment rates, the differential value between dispatched 24 h time–series power outputs for modified units and that for the same units under no modification is calculated. For these fifteen differential value series of 24 h time–series power outputs, the total sum for each of them separately means total electricity increase involved in electricity market (Market A) and is shown in

Table 6.

Considering the load rate interval established in this case, the electricity increase involved in the deep peak regulation ancillary service market (Market B) is separately calculated under three load rate intervals, also shown in

Table 6. For instance, one part of electricity involved in Market B, which is collectively generated by Unit No.1 at load rates above 30% but below 50%, decreases by 109 MWh after scheme 1 is applied when the stipulated curtailment rate is 8.3%. Meanwhile, the other part of electricity involved in Market B is generated by the same unit at load rates below 30% and increases by 120 MWh. The sum of these two parts, 11 MWh, is the total electricity increase involved in Market B with a load rate below 50%. Considering price rules for these two markets, a further economical calculation is conducted on this basis.

3.2.2. Added Revenue from Deep Peak-Regulation Ancillary Service Market

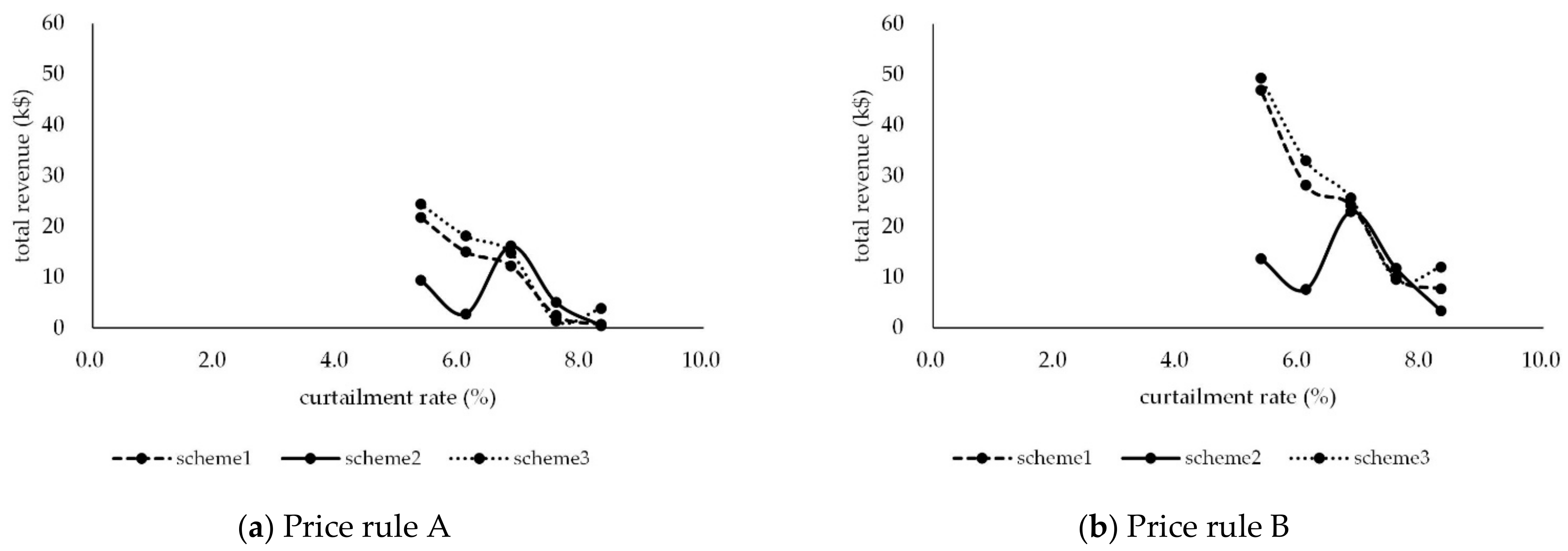

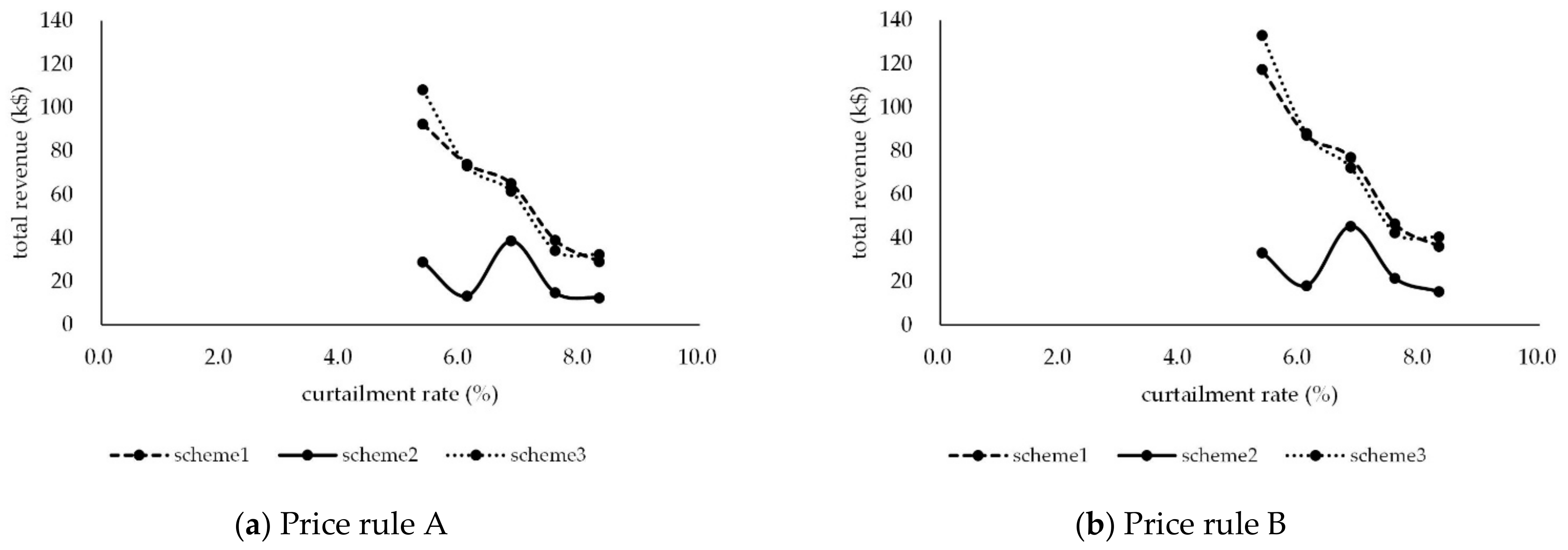

As established in this case, “Price rule A: unified price for all load rate interval” or “Price rule B: the price for load rate below 30% is twice of the price for load rate between 30% and 50%”, the revenues added from the deep peak regulation market for each modification schemes under five stipulated curtailment rates are further considered. They are calculated with added electricity involved in Market B and price interval limit for its corresponding load rate. The results under two price rules are shown in

Figure 4.

The revenue for scheme 1 under both price rules keeps increasing when the curtailment rate is cut down from 8.3% to 5.4%. The revenue for scheme 3 under two price rules firstly drops when the curtailment rate turns from 8.3% to 7.6%, due to reduced electricity involved in related load interval, and then enjoys a rising curve that nearly coincides with the revenue curve for scheme 1. Scheme 1 and scheme 3 add so much flexibility that the lower the curtailment rate is, the higher total revenue becomes. This circumstance becomes more obvious when price rule B is adopted. In contrast, the revenue for scheme 2 firstly rises, then drops after curtailment rate gets close to 7%, and rises again finally. Once the realistic scheme 2 is applied, allowing a proper curtailment level (e.g., 7%) may achieve more revenue from the deep peak regulation ancillary service market.

Considering revenue from the deep peak regulation ancillary service market alone, it is not always economical to adopt scheme 1 and scheme 3 rather than scheme 2. When the stipulated curtailment rate is above 6.5% or 6.8%, the revenue for scheme 1 or scheme 3 is lower than that for scheme 2. Once price rule B is adopted, there is still no revenue advantage for scheme 1 and scheme 3 when the stipulated curtailment rate is above 6.8%. Besides, if the modification cost is further considered and the stipulated VRE curtailment rate is high, there is no need to introduce expensive flexibility modification schemes such as scheme 1 and scheme 3 since their added revenue is even less than that acquired from cheaper scheme 2.

However, when the VRE curtailment rate decreases to 6.8% or even less, the flexibility modification adds revenue indeed. The more units retrofitted to be more flexible, the more revenue brought from the deep peak regulation ancillary service market. This circumstance is more visible once price rule B is adopted. Neither price rule is motivated enough for thermal power units to retrofit themselves to be more flexibly dispatched under a high stipulated curtailment rate.

3.2.3. Added Dual-Market Revenue

Thermal power units not only acquire compensation revenue from the deep peak regulation ancillary service market but also increase their revenue from the electricity market after flexibility modification. The more flexible the power units are, the more opportunity they have to generate at a high load rate, especially in future power systems with high VRE penetration.

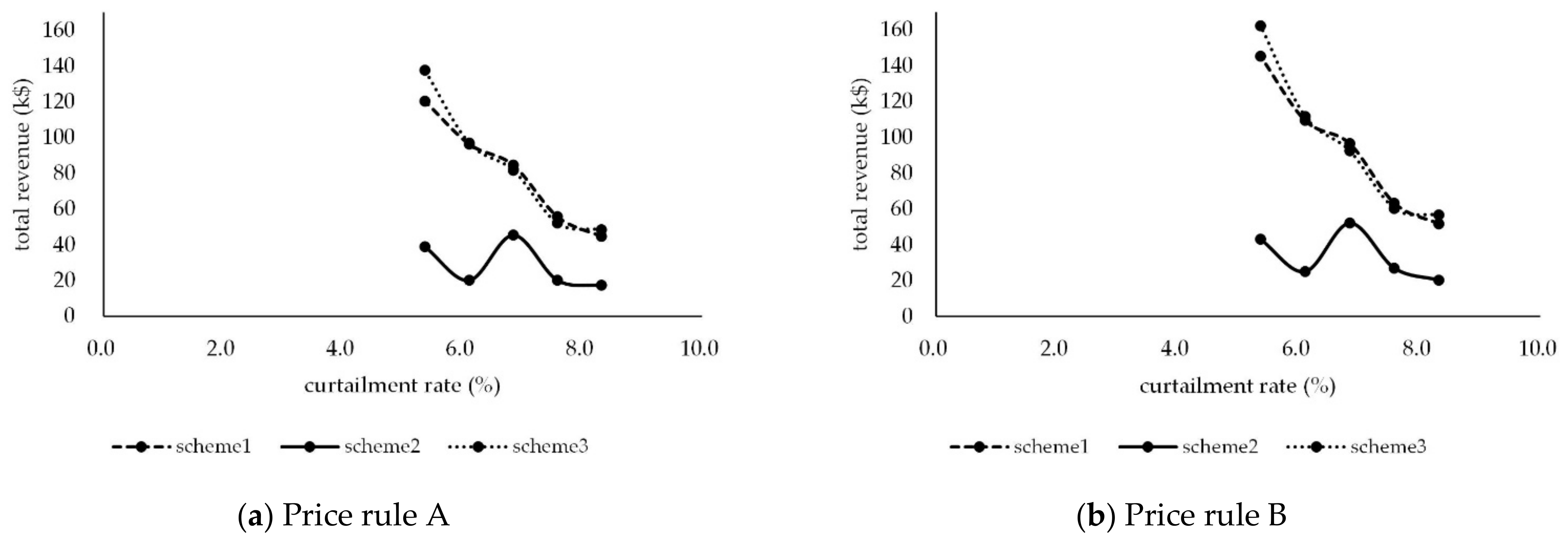

The added revenue from the electricity market is simply calculated with a unified electricity price (0.28 CNY per kWh) and related electricity increase, illustrated in

Table 6. Both revenues from the electricity market and revenues from the deep peak regulation ancillary service market are added up, and the results are shown in

Figure 5.

The total revenue from two markets for scheme 1 and scheme 3 under both price rules keeps increasing when the curtailment rate decreases from 8.3% to 5.4%, while the revenue curve for scheme 2 varies the same as that in

Section 3.2.2. Total revenue from two markets is almost twice the amount from the deep peak regulation ancillary service market alone. Another difference is that these two revenue curves for scheme 1 and scheme 3 are closer to each other when price rule A is adopted and get even closer under rule B.

Considering revenue from two markets together, it is always economical to adopt scheme 1 and scheme 3 rather than scheme 2. However, the revenue for scheme 3 is lower than that for scheme 1 when the curtailment rate is cut down from 8.3% to 6.1%. If price rule B is adopted, this differential value is much larger. As mentioned before, the flexibility modification scale and the degree for scheme 1 are almost half of scheme 3. On this basis, there is no doubt to choose scheme 1 rather than scheme 3 under related curtailment rate interval, in consideration of trade-offs between modification cost and dual-market revenue. Once the stipulated curtailment rate is below 6.1%, the more expensive modification scheme 3 is worth adopting.

3.2.4. Added Cash Inflows from Dual-Market Revenue and Reduced Generation Cost

The stipulated price and the load rate interval not only directly influence the dual-market revenue added by flexibility modification but also cut down the total generation cost of unit commitment. Both added revenue and reduced cost could be regarded as “cash inflow” from an investment perspective, which contributes to offsetting revenue losses for thermal power units due to lower operating hours.

The added cash inflow is illustrated in

Figure 6. There is no doubt that the total amount increases significantly under both price rules. Especially, the cash inflow curves for scheme 1 and scheme 3 are extremely close to each other. Modifying two inflexible units acquires almost the same cash inflow as that of modifying one when the curtailment rate is cut down from 8.3% to 6.1%. This provides further references for selecting economic flexibility modification schemes.

3.2.5. Discussions

The price rule for the deep peak regulation ancillary service market has two important concerns: load rate interval and price interval. The former defines the access standard while the latter defines the motivation effect. More subdivided intervals and bigger price differences lead to more revenues that thermal power could acquire. Flexibility modification makes units more flexible to contribute more reduced power output, which consequently brings more compensation revenue. More motivated price rule is encouraged when the stipulated curtailment rate is relatively severe, and only under this price rule do the expensive flexibility modification schemes deserve consideration. A simpler and more economical scheme could be applied if there is no rigorous constraint for curtailment rate, since there is no apparent revenue difference among schemes on this basis.

If dual-market revenue is further considered, thermal power units benefit more from flexibility modification. They have an advantage in flexibly adjusting themselves to track fluctuation of electricity load and VRE power output and consequently earn more from electricity increase for the electricity market, especially under high VRE integration and low stipulated curtailment rate. There is usually no doubt that the more flexible the units are modified to be, the more total revenue will be brought from two markets and the more modification cost remains to be paid. However, the marginal utility of flexibility modification investment decreases once the units are retrofitted to be flexible enough, especially for cases with no severe curtailment rate constraint.

If reduced generation cost is considered together with the dual-market revenue, both of these cash inflows motivate thermal power units to participate in flexibility modification. Similarly, price rule B is preferentially encouraged to attract more units to reduce their power output when there is a tough target for curtailment rate, especially under future high VRE integration.

There remains further work to be studied. If the initial modification investment is set to be cash outflow, and the revenue from the dual market together with reduced generation cost is set to be cash inflow, a cash flow table within different curtailment rates for these three modification schemes in one typical day could be acquired. More typical days could be chosen to represent a year according to load and power output characteristics. Repeating the modeling and the simulation above, the cash flow table would be enlarged. If its cash flow starts from the operation date, the net present value (NPV), the internal rate of return (IRR), and the payback period of investment could be calculated within a certain discount rate. On this basis, modification schemes could be selected from the perspective of the whole life cycle.

3.3. Comparative Analysis and Empirical Implementation Evidence in China

Similar studies have been developed by official institutes such as State Grid Energy Research Institute (SGERI) and China Electric Power Research Institute (CEPRI) [

16,

24]. All these studies revealed similar policy effects but are conducted based on a more complex provincial or regional power system. Besides, this paper paid more attention to detailed selection for modification schemes and price rules under different conditions rather than just evaluation for policy effects. According to the case study from SGERI in 2019, when the minimum technical power output for 8 GW of thermal power units dropped to 40% of their rated installed capacity, the VRE curtailment decreased by 1.71 TWh, while this amount achieved 2.92 TWh if the minimum technical power output rate was retrofitted to 30%. The same two amounts respectively achieved 2.94 TWh and 4.76 TWh if the modification plan covered 16 GW of thermal power units. The maximum decrease for VRE curtailment rate achieved 13.3%. It was verified that deeper regulation length and larger modification scale both contribute to reducing VRE curtailment. As reported by CEPRI at the annual conference of the Chinese Society for Electrical Engineering in 2017, reduced VRE curtailment for a provincial power system ought to be 1.1 TWh if 15.48 GW of thermal power units were retrofitted to enjoy a decrease for minimum technical power output from 60% to 40% of rated capacity. However, the actual cover scale for flexibility modification plan and reduced VRE curtailment brought by it merely achieved 2.5 GW and 0.07 TWh. Meanwhile, the actual modification for Northwest China only covered about 1% of its total capacity of the thermal power unit, and related VRE curtailment was no more than 0.2 TWh. It was also verified that the actual implementation of flexibility modification did not go as smoothly as expected when this unique policy mix was firstly adopted, and more activeness for participation remains to be activated. However, with continuous encouragement from China’s government, six provincial peak regulation ancillary service markets and six regional markets were established by the end of March 2020. This successfully makes deep peak regulation a profitable selection and indeed contributes to integrating and consuming more VRE electricity. Typically, the regional peak regulation ancillary service market for Northwest China had cumulatively increased system flexibility by 3.35 GW and reduced VRE curtailment by 10.03 TWh.

There are many experiences and patterns to promote VRE electricity consumption in a market-oriented way in areas with mature electricity markets such as Europe and the United States. However, they are not quite suitable for China’s cases because China’s electricity market is still in the initial stage of construction. Thus, the flexibility modification and the peak regulation ancillary service market provide a unique way for China to remove the congenital deficiency of peak regulation ability and the lack of a corresponding market mechanism for effective activation. As the most valid incentive among this policy mix, compensation prices for different provincial and regional markets have been introduced, but some of them are still not activated enough, while others are beyond the affordability of contributors. A more balanced price system should be introduced, and some provinces have attempted to adopt relative policies. It is also universal and especially applicable for those countries without mature electricity markets to develop incentives for releasing system flexibility. Other countries with mature electricity markets, especially electricity spot markets, can motivate market subjects by node electricity price, and there is no need for them to additionally design a new independent market for deep peak regulation.

For further discussions, the market design for the deep peak regulation ancillary service market should be further improved and, in coordination with other policy frameworks, should be issued or be prepared to be implemented in China.

China’s government implemented its new scheme of provincial renewable portfolio standard (RPS) in January 2020, which directly assesses the consumed VRE electricity in total electricity consumption. Under administrative order for fulfilling quotas, more system flexibility needs to be released to integrate more VRE under a low curtailment rate. It would be the most feasible option for most provinces in Northwest and Northeast China to motivate integration potential by adopting flexibility modification of thermal power units and the deep peak regulation ancillary service market. In addition, assessing subjects could complete their obligated quota by buying green certificates from VRE producers or abundant VRE electricity consumption from those who have completed their target. Both trading markets need to be further designed and meanwhile be coordinated with a deep peak regulation ancillary service market.

The thermal power unit is usually considered to be the unit that pays the bill for carbon trading. However, this is not reasonable considering their contributions to integrating renewables through deep peak regulation. Two alternatives remain for further consideration. Thermal power units which actively participate in the deep peak regulation ancillary service market should be out of the assessment. Instead, the reduced carbon emissions should be converted into added carbon quota. On this basis, those thermal power units with relatively small capacity, high flexibility, and high carbon emissions should be encouraged to jointly join both markets to earn more rather than directly retire, while units with huge capacity, low flexibility, and green emission performance should be utilized as effectively as possible.

More in-depth reforms of China’s power system will inevitably lead the electricity market to a real-time electricity spot market. If the load rate intervals and the price intervals are infinitely subdivided, a price for every bus inside power grid branches will be formed. This price reflects the real balance between power supply and demand, which could spontaneously guide the dispatched 24 h time–series power outputs for all kinds of power units to achieve an economical level. There is no need for a deep peak regulation ancillary service market in that circumstance. However, the international price rules and the trading mechanism for the electricity spot market are not suitable for China, as these two markets still need further modification to cooperate in the short-term.

4. Conclusions

This policy mix for flexibility modification and deep peak regulation ancillary service market is of great importance for reducing VRE curtailment rate and will inevitably play a significant role in future high VRE integration. Prior studies have either been single-optimization ones or have not focused on the intrinsic relationship between these two policy frameworks.

This paper established a MILP-UC model and acquired different economical dispatching results under five typical stipulated VRE curtailment rates with 24 h time–series power output for all integrated power units. Three flexibility modification schemes for thermal power units and two price rules for the deep peak regulation ancillary service market were developed. Each economical dispatching result for these three schemes was separately compared with a related one that contained no modification under the same curtailment rate, and sensitivity analysis was conducted considering VRE integration and electricity load. Total electricity increases involved in the dual market were calculated. On this basis, the added revenue from the deep peak regulation ancillary service market, the added revenue from the dual market, and the added cash inflow from dual market revenue and reduced generation cost were further calculated, compared, and discussed under different price rules. The results illustrated that flexibility modification of thermal power units is an effective approach to integrate increasing shares of VRE, especially under low stipulated curtailment rate. These findings extend applications of MILP-UC modeling, confirming that the modification scheme selection is a trade-off between cost reduction and curtailment requirement. There is no need for adopting expensive schemes with more modified units and more flexible performance unless the reduced VRE curtailment rate is worth the higher modification cost. In addition, other improvements noted in this paper included a three-step compensation revenue evaluation under different rules. Results indicated that a more motivated price rule is needed when the stipulated curtailment rate is relatively severe, especially under future high VRE integration. Besides, the marginal utility of flexibility modification investment decreases once the units have been flexibly retrofitted to their critical degree, especially for circumstances with no rigorous curtailment rate constraint. It is recommended that flexibility modification should be further enlarged via but not limited to a more targeted compensation price, which is motivated enough for generators but affordable for allocation entities. Meanwhile, demand-based trade-offs for flexibility modification should be further considered by generators rather than blind investment.

Most notably, this is an extended study to collectively investigate the effectiveness of the flexibility modification and the deep peak regulation ancillary service market and their connections based on the proposed analysis framework. However, some limitations are worth noting. The case applied in this paper is not complicated enough to reflect actual policy effect in real power systems, and “cash flow” calculation is not completely developed. Future work should therefore include follow-up work to evaluate whether the scheme is economical via a long term cash flow calculation and also whether the market design for deep peak regulation ancillary service continues to be in coordination with other policy frameworks based on a more realistic case or testing system [

44].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}