The Common Good Balance Sheet and Employees’ Perceptions, Attitudes and Behaviors

Abstract

1. Introduction

The Common Good Balance Sheet

2. Review of the Literature

2.1. Employees’ Reactions to CSR

The Role of Sex and Age in Reactions to CSR

2.2. Research Desiderata and the Aim of Our Study

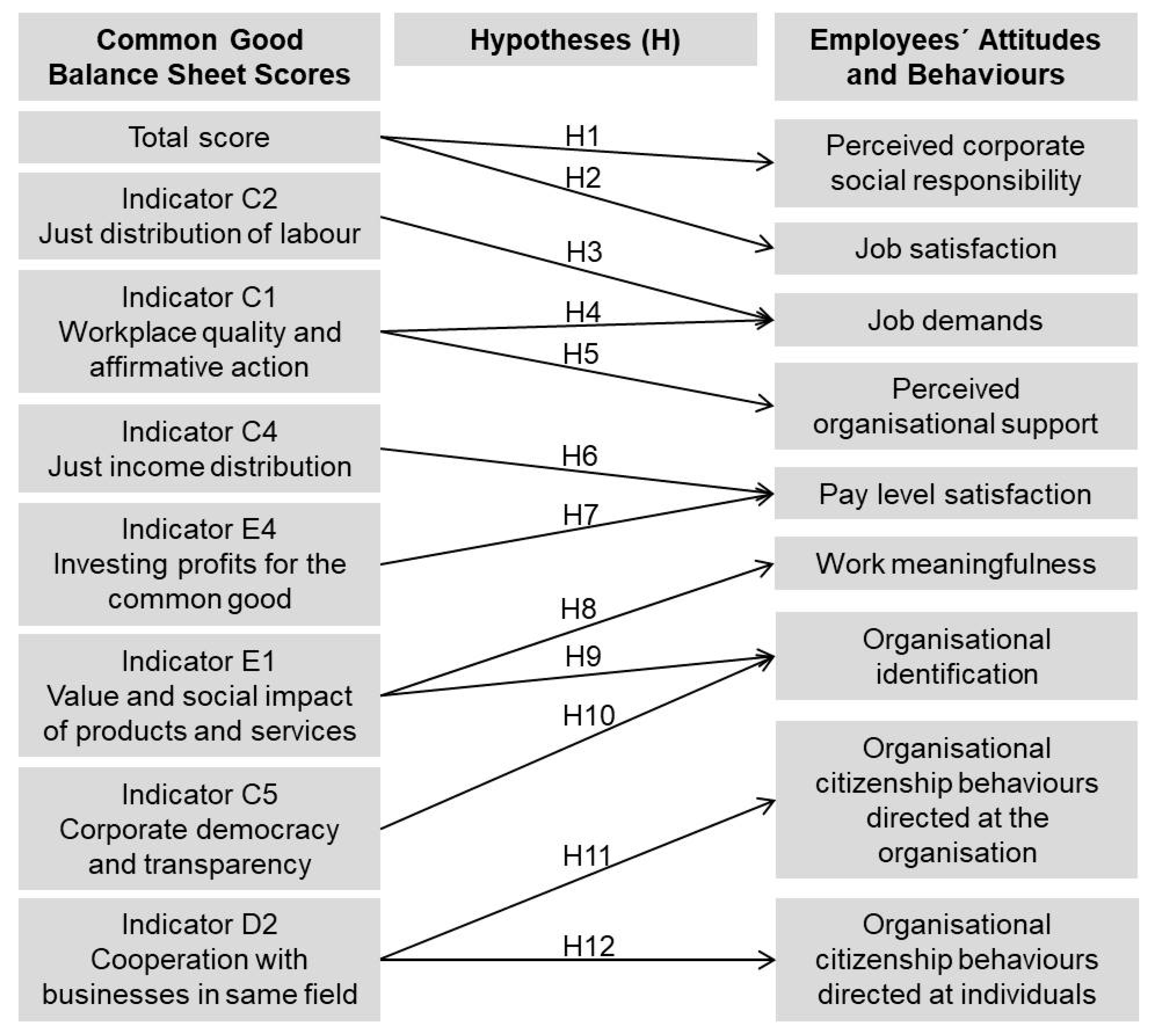

3. Constructs and Hypotheses

3.1. Perceived CSR

3.2. Job Satisfaction

3.3. Job Demands and Perceived Organisational Support

3.4. Pay Level Satisfaction

3.5. Meaningful Work

3.6. Organisational Identification

3.7. Organisational Citizenship Behaviours

4. Methods

4.1. Materials

4.2. Data and Sample

4.3. Procedure

5. Results

5.1. Perceived CSR and Job Satisfaction

5.2. Job Demands and Perceived Organisational Support

5.3. Pay Level Satisfaction

5.4. Meaningful Work

5.5. Organisational Identification

5.6. Organisational Citizenship Behaviours

6. Discussion

6.1. Perceived CSR

6.2. Job Satisfaction

6.3. Job Demands and Perceived Organisational Support

6.4. Pay Level Satisfaction

6.5. Meaningful Work

6.6. Organisational Identification

6.7. Organisational Citizenship Behaviours

6.8. Limitations

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Perceived CSR (from Glavas & Kelley, 2014; responses on a 5-level Likert scale from strongly disagree to strongly agree) |

| Social dimension: |

|

| Ecological dimension: |

|

| Job Satisfaction (from Judge & Klinger, 2008): |

|

| Job Demands (from Fischer & Lück, 2014; responses on a 5-level Likert scale from very dissatisfied to very satisfied or from false to correct): |

| Often, too much is expected from us at work. |

| Are you satisfied with the pace of work? (inverse) |

| Pay Level Satisfaction (from Fischer & Lück, 2014; responses on a 5-level Likert scale from very dissatisfied to very satisfied): |

|

| Perceived Organizational Support (from Eisenberger et al., 2001; responses on a 5-level Likert scale from strongly disagree to strongly agree): |

|

| Meaningful Work (from Steger et al., 2012 and Bunderson & Thompson, 2009; responses on a 5-level Likert scale from absolutely untrue to absolutely true). |

| Positive meaning: |

|

| Meaning-making through work: |

|

| Greater good motivations: |

|

| Organizational Identification (from Mael & Ashfort, 1992; response on a 5-level Likert scale from strongly disagree to strongly agree): |

|

| Organizational Citizenship Behavior (OCB) (from Lee & Allen (2002); responses on a 5-level Likert scale from never to always) |

| OCB-I: |

|

| OCB-O: |

|

References

- The Global Goals. Goal 8: Decent Work and Economic Growth. Available online: https://www.globalgoals.org/8-decent-work-and-economic-growth (accessed on 8 December 2020).

- Jenkins, H. A critique of conventional CSR theory: An SME perspective. J. Gen. Manag. 2004, 29, 37–57. [Google Scholar] [CrossRef]

- Elford, A.C.; Daub, C.-H. Solutions for SMEs challenged by CSR: A multiple cases approach in the food industry within the DACH-region. Sustainability 2019, 11, 4758. [Google Scholar] [CrossRef]

- Heras, I.; Arana, G. Alternative models for environmental management in SMEs: The case of Ekoscan vs. ISO 14001. J. Clean. Prod. 2010, 18, 726–735. [Google Scholar] [CrossRef]

- Steinhöfel, E.; Galeitzke, M.; Kohl, H.; Orth, R. Sustainability reporting in German manufacturing SMEs. Procedia Manuf. 2019, 33, 610–617. [Google Scholar] [CrossRef]

- Johnson, M.P.; Schaltegger, S. Two decades of sustainability management tools for SMEs: How far have we come? J. Small Bus. Manag. 2016, 54, 481–505. [Google Scholar] [CrossRef]

- Wiefek, J.; Heinitz, K. The common good approach in entrepreneurial practice. Z. Wirtsch. Unternehm. 2019, 20, 320–345. [Google Scholar] [CrossRef]

- Felber, C. Gemeinwohl-Ökonomie; Piper: München, Germany, 2018; ISBN 9783492312363. [Google Scholar]

- Gemeinwohl-Ökonomie. Idee & Vision. Available online: https://web.ecogood.org/de/idee-vision/ (accessed on 21 December 2020).

- Gemeinwohl-Ökonomie. Die Gemeinwohl-Ökonomie Gewinnt Global und National an Bedeutung. Available online: https://web.ecogood.org/de/menu-header/news/die-gemeinwohl-okonomie-gewinnt-national-und-international-an-bedeutung/ (accessed on 21 December 2020).

- Europäischer Wirtschafts-und Sozialausschuss. Stellungnahme des Europäischen Wirtschafts-und Sozialausschusses (EWSA) zum Thema "Die Gemeinwohl-Ökonomie: Ein Nachhaltiges Wirtschaftsmodell für den Sozialen Zusammenhalt”; ECO/378 Gemeinwohl-Ökonomie; Europäischer Wirtschafts-und Sozialausschuss (EWSA): Brussels, Belgium, 2015. [Google Scholar]

- BÜNDNIS 90/DIE GRÜNEN Baden-Württemberg; CDU-Landesverband Baden-Württemberg. Baden-Württemberg gestalten: Verlässlich. Nachhaltig. Innovativ. Koalitionsvertrag zwischen BÜNDNIS 90/DIE GRÜNEN Baden Württemberg und der CDU Baden-Württemberg 2016–2021; BÜNDNIS 90/DIE GRÜNEN und CDU-Landesverband: Stuttgart, Germany, 2016; Available online: https://www.baden-wuerttemberg.de/de/regierung/landesregierung/koalitionsvertrag/ (accessed on 21 December 2020).

- CDU Hessen; Bündnis 90/Die Grünen Hessen. Koalitionsvertrag Zwischen CDU Hessen und BÜNDNIS 90/DIE GRÜNEN Hessen für Die 20. Legislaturperiode. Aufbruch im Wandel Durch Haltung, Orientierung und Zusammenhalt; BÜNDNIS 90/DIE GRÜNEN Hessen und CDU Hessen: Wiesbaden, Germany, 2018; Available online: https://www.gruene-hessen.de/partei/files/2018/12/Koalitionsvertrag-CDU-GR%C3%9CNE-2018-Stand-20-12-2018-online.pdf (accessed on 21 December 2020).

- Göring-Eckardt, K.; Hofreiter, A.; Fraktion BÜNDNIS 90/DIE GRÜNEN. Pilotprojekt Gemeinwohl-Bilanz in Bundesunternehmen; Bundesanzeiger Verlag GmbH: Köln, Germany, 2019; Available online: https://dip21.bundestag.de/dip21/btd/19/111/1911148.pdf (accessed on 21 December 2020).

- Gemeinwohl-Ökonomie. Gemeinwohl-Unternehmen. Available online: https://web.ecogood.org/de/die-bewegung/pionier-unternehmen/ (accessed on 21 December 2020).

- Gemeinwohl-Ökonomie. Handbuch zur Gemeinwohl-Bilanz. Available online: https://www.ecogood.org/media/filer_public/c9/cd/c9cd687a-60fc-433e-a7c4-beae86541902/handbuch_v41_cc_release.pdf (accessed on 13 May 2015).

- Ejarque, A.T.; Campos, V. Assessing the economy for the common good measurement theory ability to integrate the SDGs into MSMEs. Sustainability 2020, 12, 10305. [Google Scholar] [CrossRef]

- Felber, C.; Campos, V.; Sanchis, J.R. The common good balance sheet, an adequate tool to capture non-financials? Sustainability 2019, 11, 3791. [Google Scholar] [CrossRef]

- Kny, J. Too big to Do Good? Eine Empirische Studie der Gemeinwohlorientierung von Großunternehmen am Beispiel der Gemeinwohl-Ökonomie; Oekom: München, Germany, 2020; ISBN 9783962382391. [Google Scholar]

- Ollé-Espluga, L.; Muckenhuber, J.; Hadler, M. Job Quality in Economy for the Common Good Firms in Austria and Germany; Working paper CIRIEC 2019/21; 2019; Available online: http://www.ciriec.uliege.be/repec/WP19-21.pdf (accessed on 4 December 2020).

- Meynhardt, T.; Fröhlich, A. Die Gemeinwohl-Bilanz—Wichtige Anstöße, aber im Legitimationsdefizit. Z. Öffentl. Gemeinwirtsch. Unternehm. 2017, 40, 152–176. [Google Scholar] [CrossRef]

- Sanchis, J.R.; Campos, V.; Ejarque, A. Analyzing the Economy for the Common Good Model. Statistical Validation of Its Metrics and Impacts in the Business Sphere; 2018; Available online: https://web.ecogood.org/media/filer_public/4b/89/4b89a0b6-d3ef-45c7-8827-23efb00711f0/ecg-analysis-catedra-ebc-valencia.pdf (accessed on 5 December 2020).

- Heidbrink, L.; Kny, J.; Köhne, R.; Sommer, B.; Stumpf, K.; Welzer, H.; Wiefek, J. Schlussbericht für das Verbundprojekt Gemeinwohl-Ökonomie im Vergleich Unternehmerischer Nachhaltigkeitsstrategien (GIVUN); 2018; Available online: https://www.umweltbundesamt.de/publikationen/von-der-nische-in-den-mainstream (accessed on 31 January 2019).

- Mischkowski, N.S.; Funcke, S.; Kress-Ludwig, M.; Stumpf, K.H. Die Gemeinwohl-Bilanz—Ein Instrument zur Bindung und Gewinnung von Mitarbeitenden und Kund*innen in kleinen und mittleren Unternehmen? NachhaltigkeitsManagementForum| Sustain. Manag. Forum 2018, 26, 123–131. [Google Scholar] [CrossRef]

- Glavas, A.; Kelley, K. The effects of perceived corporate social responsibility on employee attitudes. Bus. Ethics Q. 2014, 24, 165–202. [Google Scholar] [CrossRef]

- Glavas, A.; Godwin, L.N. Is the perception of ‘goodness’ good enough? Exploring the relationship between perceived corporate social responsibility and employee organizational identification. J. Bus. Ethics 2013, 114, 15–27. [Google Scholar] [CrossRef]

- Lee, E.M.; Park, S.-Y.; Lee, H.J. Employee perception of CSR activities: Its antecedents and consequences. J. Bus. Res. 2013, 66, 1716–1724. [Google Scholar] [CrossRef]

- Glavas, A. Corporate social responsibility and organizational psychology: An integrative review. Front. Psychol. 2016, 7, 144. [Google Scholar] [CrossRef] [PubMed]

- Gond, J.-P.; El Akremi, A.; Swaen, V.; Babu, N. The psychological microfoundations of corporate social responsibility: A person-centric systematic review. J. Organ. Behav. 2017, 38, 225–246. [Google Scholar] [CrossRef]

- Rupp, D.E.; Mallory, D.B. Corporate social responsibility: Psychological, person-centric, and progressing. Annu. Rev. Organ. Psychol. Organ. Behav. 2015, 2, 211–236. [Google Scholar] [CrossRef]

- Wang, Y.; Xu, S.; Wang, Y. The consequences of employees’ perceived corporate social responsibility: A meta-analysis. Bus. Ethics A Eur. Rev. 2020, 29, 471–496. [Google Scholar] [CrossRef]

- Del Alonso-Almeida, M.M.; Perramon, J.; Bagur-Femenias, L. Leadership styles and corporate social responsibility management: Analysis from a gender perspective. Bus. Ethics A Eur. Rev. 2017, 26, 147–161. [Google Scholar] [CrossRef]

- Kahreh, M.S.; Babania, A.; Tive, M.; Mirmehdi, S.M. An examination to effects of gender differences on the corporate social responsibility (CSR). Procedia Soc. Behav. Sci. 2014, 109, 664–668. [Google Scholar] [CrossRef]

- Islam, T.; Ali, G.; Sheikh, L. Perceived CSR ans mico-level outcomes: Moderating role of demographics. J. Res. Soc. Pak. 2018, 55, 162–175. [Google Scholar]

- Ko, S.-H.; Moon, T.-W.; Hur, W.-M. Bridging service employees’ perceptions of CSR and organizational citizenship behavior: The moderated mediation effects of personal traits. Curr. Psychol. 2018, 37, 816–831. [Google Scholar] [CrossRef]

- Rosso, B.D.; Dekas, K.H.; Wrzesniewski, A. On the meaning of work: A theoretical integration and review. Res. Organ. Behav. 2010, 30, 91–127. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. On corporate social responsibility, Sensemaking, and the search for meaningfulness through work. J. Manag. 2019, 45, 1057–1086. [Google Scholar] [CrossRef]

- Wiefek, J.; Heinitz, K. Common good-oriented companies: Exploring corporate values, characteristics and practices that could support a development towards degrowth. Manag. Rev. 2018, 29, 311–331. [Google Scholar] [CrossRef]

- Gond, J.-P.; El-Akremi, A.; Igalens, J.; Swaen, V. Corporate Social Responsibility Influence on Employees; ICCSR Research Paper Series, No. 54; 2010; Available online: https://nottingham.ac.uk/business/ICCSR/assets/ibyucpdrvypr.pdf (accessed on 9 February 2016).

- Aguinis, H.; Glavas, A. Embedded versus peripheral corporate social responsibility: Psychological foundations. Ind. Organ. Psychol. 2013, 6, 314–332. [Google Scholar] [CrossRef]

- Locke, E.A. The nature and causes of job satisfaction. In Handbook of Industrial and Organizational Psychology; Dunnette, M.D., Ed.; Rand McNally: Chicago, IL, USA, 1976; pp. 1297–1343. [Google Scholar]

- Dhanesh, G.S. CSR as organization-employee relationship management strategy: A case study of socially responsible information technology companies in India. Manag. Commun. Q. 2014, 28, 130–149. [Google Scholar] [CrossRef]

- Rhoades, L.; Eisenberger, R. Perceived organizational support: A review of the literature. J. Appl. Psychol. 2002, 87, 698–714. [Google Scholar] [CrossRef]

- Eisenberger, R.; Huntington, R.; Hutchison, S.; Sowa, D. Perceived organizational support. J. Appl. Psychol. 1986, 71, 500–507. [Google Scholar] [CrossRef]

- Miceli, M.P.; Lane, M.C. Antecedents of pay satisfaction: A review and extension. In Research in Personnel and Human Resources Management; Rowland, K.K., Ferris, J., Eds.; JAI Press: Greenwich, CT, USA, 1991; pp. 235–309. [Google Scholar]

- Williams, M.L.; McDaniel, M.A.; Nguyen, N.T. A meta-analysis of the antecedents and consequences of pay level satisfaction. J. Appl. Psychol. 2006, 91, 392–413. [Google Scholar] [CrossRef]

- Judge, T.A.; Piccolo, R.F.; Podsakoff, N.P.; Shaw, J.C.; Rich, B.L. The relationship between pay and job satisfaction: A meta-analysis of the literatre. J. Vocat. Behav. 2010, 77, 157–167. [Google Scholar] [CrossRef]

- Shapiro, H.J.; Wahba, M.A. Pay satisfaction: An empirical test of a discrepancy model. Manag. Sci. 1978, 24, 612–622. [Google Scholar] [CrossRef]

- Lips-Wiersma, M.; Wright, S.; Dik, B. Meaningful work: Differences among blue-, pink-, and white-collar occupations. Career Dev. Int. 2016, 21, 534–551. [Google Scholar] [CrossRef]

- Allan, B.A.; Batz-Barbarich, C.; Sterling, H.M.; Tay, L. Outcomes of meaningful work: A meta-analysis. J. Manag. Stud. 2019, 56, 500–528. [Google Scholar] [CrossRef]

- Ashforth, B.E.; Mael, F. Social identity theory and the organization. Acad. Manag. Rev. 1989, 14, 20–39. [Google Scholar] [CrossRef]

- Van Knippenberg, D.; Sleebos, E. Organizational identification versus organizational commitment: Self-definition, social exchange, and job attitudes. J. Organ. Behav. 2006, 27, 571–584. [Google Scholar] [CrossRef]

- Mael, F.; Ashforth, B.E. Alumni and their alma mater: A partial test of the reformulated model of organizational identification. J. Organ. Behav. 1992, 13, 103–123. [Google Scholar] [CrossRef]

- Jones, D.A. The psychology of CSR. In The Oxford Handbook of Corporate Social Responsibility: Psychological and Organizational Perspectives; McWilliams, A., Rupp, D.E., Siegel, D.S., Stahl, G.K., Waldman, D.A., Willness, C.R., Eds.; Oxford University Press: Oxford, UK, 2019; pp. 17–47. ISBN 9780198802280. [Google Scholar]

- John, A.; Qadeer, F.; Shahzadi, G.; Jia, F. Getting paid to be good: How and when employees respond to corporate social responsibility? J. Clean. Prod. 2019, 215, 784–795. [Google Scholar] [CrossRef]

- Lee, K.; Allen, N.J. Organizational citizenship behavior and workplace deviance: The role of affect and cognitions. J. Appl. Psychol. 2002, 87, 131–142. [Google Scholar] [CrossRef]

- Organ, D.W.; Ryan, K. A meta-analytic review of attitudinal and dispositional redictors of organizational citizenship behavior. Pers. Psychol. 1995, 48, 775–802. [Google Scholar] [CrossRef]

- Glavas, A.; Piderit, S.K. How does doing good matter? Effects of corporate citizenship on employees. J. Corp. Citizsh. 2009, 36, 51–70. [Google Scholar] [CrossRef]

- Muthuri, J.N.; Matten, D.; Moon, J. Employee volunteering and social capital: Contributions to corporate social responsibility. Br. J. Manag. 2009, 20, 75–89. [Google Scholar] [CrossRef]

- Gemeinwohl-Ökonomie. Gemeinwohl-Bericht Auditierung. Available online: https://web.ecogood.org/de/unsere-arbeit/gemeinwohl-bilanz/unternehmen/4-gemeinwohl-bericht-audit/ (accessed on 26 December 2020).

- Brislin, R.W.; Freimanis, C. Back-translation: A tool for cross-cultural research. In An Encyclopaedia of Translation: Chinese-English. English-Chinese; Sin-wai, C., Pollard, D.E., Eds.; The Chinese University Press: Hong Kong, China, 2001; ISBN 9622019978. [Google Scholar]

- Judge, T.A.; Klinger, R. Job Satisfaction: Subjective well-being at work. In The Science of Subjective Well-Being; Eid, M., Larsen, R.J., Eds.; The Guilford Press: New York, NY, USA, 2008; pp. 393–413. [Google Scholar]

- Fordyce, M.W. A review of research on the happiness measures: A sixty second index of happiness and mental health. Soc. Indic. Res. 1988, 20, 355–381. [Google Scholar] [CrossRef]

- Fischer, L.; Lück, H.E. Allgemeine Arbeitszufriedenheit. Zs. Soz. Items Skalen (ZIS) 2014. [Google Scholar] [CrossRef]

- Eisenberger, R.; Armeli, S.; Rexwinkel, B.; Lynch, P.D.; Rhoades, L. Reciprocation of perceived organizational support. J. Appl. Psychol. 2001, 86, 42–51. [Google Scholar] [CrossRef]

- Steger, M.F.; Dik, B.J.; Duffy, R.D. Measuring meaningful work: The work and meaning inventory (WAMI). J. Career Assess. 2012, 20, 322–337. [Google Scholar] [CrossRef]

- Bunderson, J.S.; Thompson, J.A. The call of the wild: Zookeepers, callings, and the double-edged sword of deeply meaningful work. Adm. Sci. Q. 2009, 51, 32–57. [Google Scholar] [CrossRef]

- Zogbhi-Manrique-de-Lara, P. Should faith and hope be included in the employees’ agenda?: Linking P-O fit and citizenship behavior. J. Manag. Psychol. 2008, 23, 73–88. [Google Scholar] [CrossRef]

- Bühner, M.; Ziegler, M. Statistik für Psychologen und Sozialwissenschaftler; Pearson Studium: München, Germany, 2009; ISBN 9783863266141. [Google Scholar]

- Field, A. Discovering Statistics Using IBM SPSS Statistics; Sage: Los Angeles, CA, USA, 2018; ISBN 9781526419514. [Google Scholar]

- Urban, D.; Mayerl, J. Angewandte Regressionsanalyse: Theorie, Technik und Praxis; Springer VS: Wiesbaden, Germany, 2018; ISBN 9783658019150. [Google Scholar]

- Jones, D.A.; Newman, A.; Shao, R.; Cooke, F.L. Advances in employee-focused micro-level research on corporate social responsibility: Situating new contributions within the current state of the literature. J. Bus. Ethics 2019, 157, 293–302. [Google Scholar] [CrossRef]

- Hackman, J.R.; Oldham, G.R. Development of the job diagnostic survey. J. Appl. Psychol. 1975, 60, 159–170. [Google Scholar]

- Karasek, R.A. Job demands, job decision latitude, and mental strain: Implications for job redesign. Adm. Sci. Q. 1979, 24, 285–308. [Google Scholar] [CrossRef]

| Human Dignity | Cooperation & Solidarity | Ecological Sustainability | Social Justice | Co-determination & Transparency | |

|---|---|---|---|---|---|

| (A) Suppliers | A1: Ethical supply management: Active examination of the risks of purchased goods and services, consideration of the social and ecological aspects of suppliers and service partners (90) | ||||

| (B) Investors | B1: Ethical financial management: Consideration of social and ecological aspects when choosing financial services; common good-oriented investments and financing (30) | ||||

| (C) Employees, including Business Owners | C1: Workplace quality and affirmative action: Employee-oriented organizational culture and structure, fair employment and payment policies, workplace health and safety, work-life balance, flexible work hours, equal opportunity and diversity (90) | C2: Just distribution of labor: Reduction of overtime, eliminating unpaid overtime, reduction of total work hours, contribution to the reduction of unemployment (50) | C3: Promotion of environmentally friendly behavior of employees: Active promotion of sustainable lifestyle of employees (mobility, nutrition), training and awareness-raising activities, sustainable organizational culture (30) | C4: Just income distribution: Low income disparity within a company, compliance with minimum and maximum wages (60) | C5: Corporate democracy and transparency: Comprehensive transparency within the company, election of managers by employees, democratic decision making on fundamental strategic issues, transfer of property to employees (90) |

| (D) Customers, Products, Services, Business Partners | D1: Ethical customer relations: Ethical business relations with customers, customer orientation and co-determination, joint product development, high quality of service, high product transparency (50) | D2: Cooperation with businesses in same field: Transfer of know-how, personnel, contracts and interest-free loans to other business in the same field, participation in cooperative marketing activities and crisis management (70) | D3: Ecological design of products and services: Offering of ecologically superior products/services; awareness raising programmes, consideration of ecological aspects when choosing customer target groups (90) | D4: Socially oriented design of product and services: Information, products and services for disadvantaged groups, support for value-oriented market structures (30) | D5: Raising social and ecological standards: Exemplary business behavior, development of higher standards with businesses in the same field, lobbying (30) |

| (E) Social Environment | E1: Value and social impact of products and services: Products and services fulfill basic human needs or serve humankind society or the environment (90) | E2: Contribution to the local community: Mutual support and cooperation through financial resources, services, products. logistics, time, know-how, knowledge, contracts, influence (40) | E3: Reduction of environmental impact: Reduction of environmental effects towards a sustainable level, resource, energy, climate, emissions, waste etc. (70) | E4: Investing profits for the common good: Reduction or eliminating dividend payments to extern, payouts to employees, increasing equity, social-ecological investments (60) | E5: Social transparency and co-determination: Common good and sustainability reports, participation in decision-making by local stakeholders and NGO’s (30) |

| Negative Criteria | Violation of ILO norms / human rights (−200), products detrimental to human dignity and human rights (e.g., landmines, nuclear power, GMO’s) (−200), outsourcing to or cooperation with companies which violate human dignity (−150) | Hostile takeover (−200), blocking patents (−100), dumping prices (−200) | Massive environmental pollution (−200), gross violation of environmental standards (−200), planned obsolescence (short lifespan of products) (−100) | Unequal pay for women and men (−200), job cuts or moving jobs overseas despite having made a profit (−150), subsidiaries in tax havens (−200), equity yield rate >10% (−200) | Non-disclosure of subsidiaries (−100), prohibition of a work council (−150), non-disclosure of payments to lobbyists (−200), excessive income inequality within a business (−150) |

| Score | Minimum | Maximum | Mean | SD |

|---|---|---|---|---|

| CGB total (rounded to ten) | 370 | 690 | 452.84 | 81.12 |

| Indicator C1 (in %) | 20 | 79 | 42.86 | 11.41 |

| Indicator C2 (in %) | 10 | 76 | 43.09 | 13.24 |

| Indicator C4 (in %) | 20 | 80 | 47.74 | 20.80 |

| Indicator C5 (in %) | 20 | 57 | 22.19 | 7.24 |

| Indicator D2 (in %) | 30 | 73 | 41.36 | 13.71 |

| Indicator E1 (in %) | 50 | 90 | 58.98 | 8.93 |

| Indicator E4 (in %) | 10 | 100 | 91.23 | 15.74 |

| Company’s Business Field | Number of Total Employees (Rounded to Ten) | N in Sample | % of Total Employees in Sample |

|---|---|---|---|

| Clothing manufacture | 470 | 116 | 35 |

| Elder care | 340 | 10 | 3 |

| Farming | 10 | 8 | 2 |

| Food production | 50 | 9 | 3 |

| Food trade I | 20 | 3 | 1 |

| Food trade II | 170 | 34 | 10 |

| Health care | 250 | 145 | 44 |

| Media production | 330 | 7 | 2 |

| V. | N | M | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 OI | 329 | 4.03 | 0.58 | ||||||||||||||||||

| 2 POS | 327 | 3.56 | 0.92 | 0.524 | |||||||||||||||||

| 3 WM | 331 | 3.45 | 0.76 | 0.606 | 0.581 | ||||||||||||||||

| 4 JS | 320 | 0.01 | 0.89 | 0.446 | 0.657 | 0.591 | |||||||||||||||

| 5 JD | 330 | 2.60 | 0.83 | −0.229 | −0.554 | −0.351 | −0.563 | ||||||||||||||

| 6 PS | 325 | 3.05 | 1.12 | 0.258 | 0.355 | 0.312 | 0.330 | −0.246 | |||||||||||||

| 7 OCB-O | 327 | 3.64 | 0.72 | 0.456 | 0.300 | 0.483 | 0.266 | -0.137 * | 0.123 * | ||||||||||||

| 8 OCB-I | 330 | 4.23 | 0.57 | 0.315 | 0.202 | 0.239 | 0.231 | -0.119 * | 0.145 | 0.376 | |||||||||||

| 9 PCSR | 328 | 4.22 | 0.57 | 0.373 | 0.573 | 0.454 | 0.368 | −0.323 | 0.115 * | 0.307 | 0.196 | ||||||||||

| 10 Age | 328 | 3.29 | 1.60 | 0.141 * | −0.005 | 0.103 | 0.026 | 0.053 | 0.180 | 0.150 | −0.106 | −0.067 | |||||||||

| 11 Sex | 327 | 1.37 | 0.48 | 0.081 | 0.053 | 0.048 | 0.127 * | -0.051 | 0.092 | 0.185 | 0.016 | −0.007 | 0.138 * | ||||||||

| 12 CGB | 331 | 453 | 81 | 0.001 | 0.239 | 0.183 | 0.104 | −0.170 | −0.100 | 0.169 | −0.135 * | 0.317 | 0.100 | 0.034 | |||||||

| 13 C1 | 331 | 43 | 11 | 0.097 | 0.288 | 0.102 | 0.136 | −0.238 | −0.007 | 0.039 | 0.046 | 0.180 | −0.047 | −0.034 | 0.457 | ||||||

| 14 C2 | 331 | 43 | 13 | 0.132 * | 0.136 * | 0.031 | 0.081 | −0.143 * | 0.183 | −0.041 | 0.194 | −0.101 | -0.041 | −0.015 | −0.165 | 0.687 | |||||

| 15 C4 | 331 | 48 | 21 | 0.099 | −0.086 | 0.087 | 0.013 | 0.058 | 0.378 | 0.025 | 0.086 | −0.255 | 0.179 | 0.073 | −0.315 | −0.431 | 0.107 | ||||

| 16 E4 | 331 | 91 | 16 | 0.086 | −0.043 | −0.026 | 0.024 | 0.025 | 0.072 | 0.019 | 0.223 | 0.016 | −0.102 | −0.022 | −0.242 | 0.171 | 0.321 | 0.035 | |||

| 17 E1 | 331 | 59 | 9 | 0.082 | 0.028 | 0.155 | 0.058 | −0.002 | 0.320 | 0.119 * | 0.043 | −0.042 | 0.234 | 0.134 * | 0.227 | −0.243 | −0.014 | 0.777 | −0.116 * | ||

| 18 D2 | 331 | 41 | 14 | 0.077 | 0.034 | 0.188 | 0.065 | 0.001 | 0.276 | 0.148 | −0.020 | 0.015 | 0.248 | 0.113 * | 0.330 | −0.306 | −0.283 | 0.715 | −0.119 * | 0.904 | |

| 19 C5 | 331 | 22 | 7 | 0.113 * | 0.216 | 0.230 | 0.122 * | −0.193 | 0.200 | 0.116 * | 0.010 | 0.015 | 0.175 | 0.036 | 0.511 | 0.515 | 0.454 | 0.320 | −0.306 | 0.496 | 0.445 |

| Criterium | PCSR (H1) Robust SD (HC3), N = 323 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score CGB + Age + Sex | 0.130 | 0.119 | 0.000 | |||

| Predictor | ||||||

| Constant | 3.266 (2.930, 3.601) | 0.171 | 0.000 | |||

| Score CGB | 0.002 (0.002, 0.003) | 0.000 | 0.345 | 0.000 | ||

| 35–54 years | −0.132 (−0.253, −0.012) | 0.061 | −0.118 | 0.032 | ||

| >54 years | −0.114 (−0.352, 0.123) | 0.121 | −0.061 | 0.344 | ||

| Men | 0.025 (−0.094, 0.144) | 0.060 | 0.022 | 0.678 | ||

| Criterium | JS (H2) Confidence Intervals, Standard Errors and PS Based on 1000 Bootstrap Samples. N = 317 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score CGB + Age + Sex | 0.030 | 0.018 | 0.047 | |||

| Predictor | ||||||

| Constant | −0.549 (−1.066, 0.008) | 0.284 | 0.054 | |||

| Score CGB | 0.001 (0.000, 0.002) | 0.001 | 0.101 | 0.058 | ||

| 35–54 years | −0.041 (−0.253, 0.179) | 0.109 | −0.023 | 0.708 | ||

| >54 years | 0.108 (−0.266, 0.438) | 0.186 | 0.034 | 0.564 | ||

| Men | 0.183 (0.026, 0.431) | 0.099 | 0.128 | 0.016 | ||

| Criterium | JD (H3) N = 326 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score C2 + Age + Sex | 0.030 | 0.018 | 0.045 | |||

| Predictor | ||||||

| Constant | 2.933 (2.587, 3.279) | 0.176 | 0.000 | |||

| Score C2 | −0.009 (−0.016, −0.002) | 0.004 | −0.146 | 0.009 | ||

| 35–54 years | 0.159 (−0.044, 0.361) | 0.103 | 0.093 | 0.124 | ||

| >54 years | 0.024 (−0.321, 0.369) | 0.175 | 0.008 | 0.891 | ||

| Men | −0.114 (−0.302, 0.074) | 0.096 | −0.066 | 0.234 | ||

| Criterium | JD (H4) N = 326 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score C1 + Age + Sex | 0.068 | 0.056 | 0.000 | |||

| Predictor | ||||||

| Constant | 3.310 (2.932, 3.689) | 0.193 | 0.000 | |||

| Score C1 | −0.018 (-0.026, −0.010) | 0.004 | −0.244 | 0.000 | ||

| 35–54 years | 0.151 (−0.047, 0.349) | 0.101 | 0.089 | 0.134 | ||

| >54 years | 0.015 (−0.323, 0.352) | 0.171 | 0.005 | 0.932 | ||

| Men | −0.124 (−0.308, 0.061) | 0.094 | −0.072 | 0.187 | ||

| Criterium | POS (H5) Confidence Intervals, Standard Errors and PS Based on 1000 Bootstrap Samples. N = 322 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score C1 + Age + Sex | 0.108 | 0.097 | 0.000 | |||

| Predictor | ||||||

| Constant | 2.481 (2.066, 2.869) | 0.219 | 0.001 | |||

| Score C1 | 0.025 (0.016, 0.034) | 0.004 | 0.313 | 0.001 | ||

| 35–54 years | −0.113 (−0.318, 0.111) | 0.099 | −0.061 | 0.253 | ||

| >54 years | 0.203 (−0.180, 0.563) | 0.187 | 0.062 | 0.288 | ||

| Men | 0.160 (−0.055, 0.372) | 0.098 | 0.085 | 0.105 | ||

| Criterium | PS (H6) Confidence Intervals, Standard Errors and PS Based on 1000 Bootstrap Samples. N = 321 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score C4 + Age + Sex | 0.155 | 0.145 | 0.000 | |||

| Predictor | ||||||

| Constant | 1.906 (1.615, 2.200) | 0.152 | 0.001 | |||

| Score C4 | 0.019 (0.013, 0.025) | 0.003 | 0.354 | 0.001 | ||

| 35–54 years | 0.281 (0.034, 0.525) | 0.121 | 0.123 | 0.024 | ||

| >54 years | 0.281 (−0.264, 0.820) | 0.256 | 0.072 | 0.275 | ||

| Men | 0.107 (−0.130, 0.350) | 0.124 | 0.046 | 0.391 | ||

| Criterium | WM (H8) Confidence Intervals, Standard Errors and PS Based on 1000 Bootstrap Samples. N = 326 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score E1 + Age + Sex | 0.035 | 0.023 | 0.023 | |||

| Predictor | ||||||

| Constant | 2.746 (2.218, 3.289) | 0.284 | 0.001 | |||

| Score E1 | 0.011 (0.001, 0.020) | 0.005 | 0.129 | 0.022 | ||

| 35–54 years | 0.062 (−0.106, 0.245) | 0.088 | 0.040 | 0.479 | ||

| >54 years | 0.269 (−0.069, 0.580) | 0.162 | 0.103 | 0.095 | ||

| Men | 0.025 (−0.153, 0.197) | 0.088 | 0.016 | 0.783 | ||

| Criterium | OI (H10) Confidence Intervals, Standard Errors and PS Based on 1000 Bootstrap Samples. N = 323 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score C5 + Age + Sex | 0.040 | 0.028 | 0.011 | |||

| Predictor | ||||||

| Constant | 3.729 (3.533, 3.929) | 0.104 | 0.001 | |||

| Score C5 | 0.008 (−0.002, 0.016) | 0.004 | 0.102 | 0.052 | ||

| 35–54 years | 0.154 (0.018, 0.291) | 0.071 | 0.134 | 0.040 | ||

| >54 years | 0.201 (−0.052, 0.460) | 0.129 | 0.101 | 0.120 | ||

| Men | 0.076 (−0.045, 0.197) | 0.060 | 0.065 | 0.215 | ||

| Criterium | OCB-O (H11) N = 322 | |||||

|---|---|---|---|---|---|---|

| Equation | R2 | Adj. R2 | b | SE B | ß | p |

| Score D2 + Age + Sex | 0.079 | 0.068 | 0.000 | |||

| Predictor | ||||||

| Constant | 3.273 (3.005, 3.542) | 0.136 | 0.000 | |||

| Score D2 | 0.005 (−0.001, 0.011) | 0.003 | 0.100 | 0.088 | ||

| 35–54 years | 0.056 (−0.112, 0.225) | 0.086 | 0.039 | 0.510 | ||

| >54 years | 0.419 (0.115, 0.723) | 0.155 | 0.170 | 0.007 | ||

| Men | 0.231 (0.074, 0.389) | 0.080 | 0.158 | 0.004 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wiefek, J.; Heinitz, K. The Common Good Balance Sheet and Employees’ Perceptions, Attitudes and Behaviors. Sustainability 2021, 13, 1592. https://doi.org/10.3390/su13031592

Wiefek J, Heinitz K. The Common Good Balance Sheet and Employees’ Perceptions, Attitudes and Behaviors. Sustainability. 2021; 13(3):1592. https://doi.org/10.3390/su13031592

Chicago/Turabian StyleWiefek, Jasmin, and Kathrin Heinitz. 2021. "The Common Good Balance Sheet and Employees’ Perceptions, Attitudes and Behaviors" Sustainability 13, no. 3: 1592. https://doi.org/10.3390/su13031592

APA StyleWiefek, J., & Heinitz, K. (2021). The Common Good Balance Sheet and Employees’ Perceptions, Attitudes and Behaviors. Sustainability, 13(3), 1592. https://doi.org/10.3390/su13031592