Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach

,

,  , ,

, ,

Abstract

:1. Introduction

- (a)

- What are the major barriers to CSR in the SME sector of Pakistan?

- (b)

- What is the order of preference of the identified barriers?

2. Related Literature

2.1. A Brief History of CSR

2.2. Defining SME in the Context of Pakistan

2.3. A Brief Overview of CSR and Sustainability Initiatives of SMEs

2.4. The State of CSR and Sustainability in the SME Sector of Pakistan

3. Major Barriers for CSR Implementation

3.1. Lack of Top Management Commitment

3.2. Lack of Financial Resources

3.3. Lack of Understanding about CSR

3.4. Lack of Strategic Planning

3.5. Complexity to Implement CSR

3.6. Lack of Regulatory Framework

4. Methodology

5. Results and Discussion

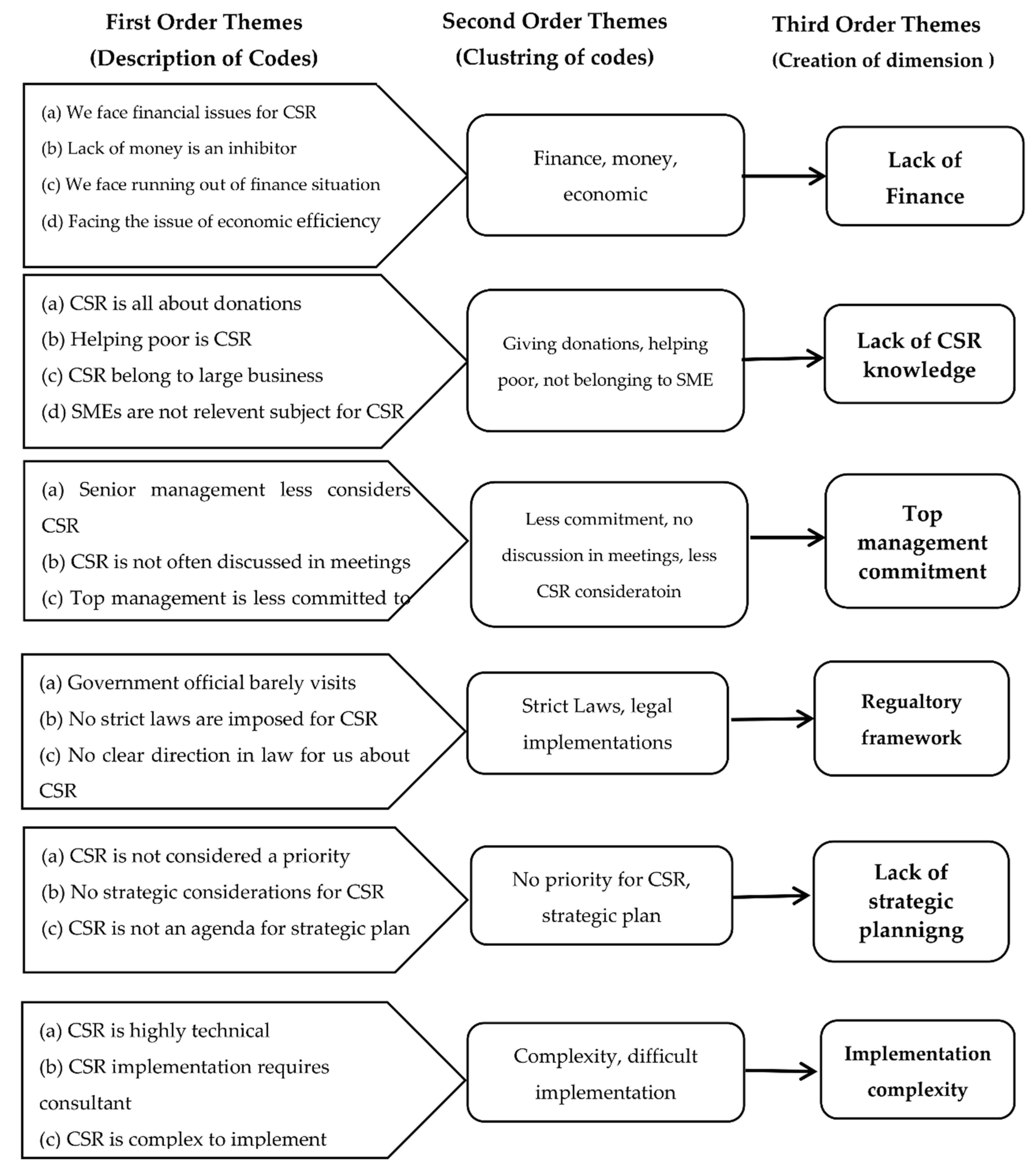

5.1. Lack of Financial Resources

“Look, this is self-explanatory to assess that we belong to a medium-sized business and work in a situation of financial instability. We often find it difficult to meet even our operational expenses due to the tight market environment outside. Therefore, separating finances for such activities (CSR) is something out of the box for us. We want to be a responsible business, but as far as this issue of finances stays with us, it almost seems impossible”………………………………(Respondent P)

“Yes, finance is something that provides you the power to decide with confidence. Given that we are a small player in the industry, one can see how difficult it is for us to survive in the present rivalry situation. To be honest, you hardly find any real situation in which a company is characterized by huge financial constraints (like us), and still, they are actively involved in sustainability or what you say, CSR practices” ………………………………(Respondent J)

“Our enterprise understands the importance of sustainable management. However, the real trouble lies with finances. As you can see, in Pakistan, even large organizations practice CSR only to satisfy legal obligations. In our case, even though we have a concern towards sustainable practices, but our concern remains unaddressed due to poor financial situation” ………………………………(Respondent B)

“The truth is, our organization wants to go for sustainable management, however, we do not have sufficient funds for that. Neither we ever receive any financial help (interest-free or low-interest loans) on the part of the government to implement sustainable practices” ………………………………(Respondent E)

5.2. Lack of CSR Knowledge

“It is to be acknowledged that poor knowledge about the concept of CSR is a bottleneck towards its effective implementation at the level of SME. So far, the general perception here is that CSR is all about donations and charity, etc. I think most of us did not know CSR from the perspective of sustainability” …………………………(Respondent L)

“In my opinion, CSR deals with donations to help the poor in a society. This is what we normally do under the name of CSR” ………………………………(Respondent X)

“Usually, most SMEs do not have a clear knowledge about CSR. My case is a different one, as I completed my graduation from an academically advanced country. This is why I have some improved knowledge about CSR and sustainable practices. Otherwise, you will hardly see someone with an advanced level of knowledge of CSR” ………………………………(Respondent A)

5.3. Lack of Top Management Commitment

“I think it will be unwise to expect sustainability behavior from an enterprise if top management is not actively engaged in all this process. I can tell you that here in our sector, most of the senior managers are purely inclined to achieve the bottom-line objectives, rather than encouraging their workforce to incorporate sustainability into business operations” ………………………………(Respondent R)

“Our top management pays very passive attention towards such initiatives (CSR). I do not remember even a single case during my stay here that content like sustainable management has been placed in the agenda items of a meeting to be attended by the senior management ” ………………………………(Respondent F)

“Top management here in our organization hardly assumes CSR as a business priority. I see here that a CSR policy does exist in our organization. However, for effective implementation, one can easily understand the importance of support from the top. Unfortunately, such support is non-existent. It does not imply that top management never considers CSR, but the problem lies with their passive intentions for such cases” ………………………………(Respondent N)

5.4. Lack of Regulatory Framework

“Look, a regulatory framework is something that decides the direction of each sector. Unfortunately, in the case of SMEs, it seems that the government of Pakistan does not have any clear environmental policy. Barely, I see some government official or any agency that forces us to stick with the sustainability perspective tightly. In fact, everyone enjoys here this freedom, and perhaps this is one of the other reasons that the SME sector is ignorant towards sustainability” ………………………………(Respondent Z)

“From the point of government intervention, some officials are in communication with us. However, they rarely perform any environmental audit or something like that to ensure if an enterprise is following the environmental laws of the state ” ………………………………(Respondent H)

“Perhaps the regulatory framework for environment deals only with the large organizations. Whereas the small operators seem to have an exception in this case. Being a small player, I do not remember anyone from any government agency approached us to ask such questions like sustainability” ………………………………(Respondent V)

5.5. Lack of Strategic Planning for CSR

“Strategic orientation for CSR is less likely to be observed in our policy documents. Though we practice CSR here, but without any strategic intent. I can share my experience of multiple SMEs, which follow CSR without any clear strategic planning considerations. In the absence of such a framework, one can see it is very difficult for an organization to implement a CSR program effectively. As to me, following CSR off and on, without any clear strategic orientation is just like a car moving on the road without knowing its destination” ………………………………(Respondent G)

“Yes, one can say with confidence that there is a clear role of strategic planning for an organization to achieve its sustainability objectives. However, unfortunately, such type of strategic planning is non-evident in this sector” ………………………………….(Respondent D)

5.6. Complexity in Implementation of CSR

“It is generally assumed here that CSR implementation is a complex thing which cannot be implemented by taking simple measures. Given this, we feel it difficult for effective implementation of such plans” ………………………………(Respondent T)

“The complexity of a CSR plan is also a thing that hinders our way towards its implementation. Being a small player, I find it difficult to get that level of complexity for effective implementation of a CSR plan” ……………………………(Respondent M)

6. Implications for Theory Additionally, Policy

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- Part I: Basic Questions

- Are you familiar with the concept of CSR?

- 2.

- What barriers do you perceive that hinder the implementation of the CSR initiatives in your organization?

- Part II: Interview Guide Main Questions

- What do you think are the barriers of CSR in the SME sector of Pakistan?

- What has been your experience in your organization considering CSR initiative implementation?

- In what way do you think your organization is hindered from implementing a CSR program?

- Can you explain what CSR practices your organization could implement but has been hindered from doing so?

References

- Ahmad, N.; Mahmood, A.; Han, H.; Ariza-Montes, A.; Vega-Muñoz, A.; Iqbal Khan, G.; Ullah, Z. Sustainability as a “new normal” for modern businesses: Are smes of pakistan ready to adopt it? Sustainability 2021, 13, 1944. [Google Scholar] [CrossRef]

- Rhou, Y.; Singal, M.; Koh, Y. CSR and financial performance: The role of CSR awareness in the restaurant industry. Int. J. Hosp. Manag. 2016, 57, 30–39. [Google Scholar] [CrossRef]

- Ahmad, N.; Scholz, M.; Arshad, M.Z.; Jafri, S.K.A.; Sabir, R.I.; Khan, W.A.; Han, H. The inter-relation of corporate social responsibility at employee level, servant leadership, and innovative work behavior in the time of crisis from the healthcare sector of pakistan. Int. J. Environ. Res. Public Health 2021, 18, 4608. [Google Scholar] [CrossRef]

- Ullah, Z.; Ahmad, N.; Nazim, Z.; Ramzan, M. Impact of CSR on Corporate Reputation, Customer Loyalty and Organizational Performance. Gov. Manag. Rev. 2020, 5, 195–210. [Google Scholar]

- Sharma, N.K. An Analysis of Corporate Social Responsibility in India. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3676827 (accessed on 11 July 2021).

- Carroll, A.B.; Laasch, O. From managerial responsibility to CSR and back to responsible management. In Research Handbook of Responsible Management; Edward Elgar Publishing: Cheltenham, UK, 2020. [Google Scholar]

- Bowen, H.R.; Johnson, F.E. Social Responsibility of the Businessman; Harper: New York, NY, USA, 1953. [Google Scholar]

- Drucker, P.F. Converting social problems into business opportunities: The new social responsibility. Calif. Manag. Rev. 1984, 26, 53–64. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Sinthupundaja, J.; Chiadamrong, N.; Kohda, Y. Internal capabilities, external cooperation and proactive CSR on financial performance. Serv. Ind. J. 2019, 39, 1099–1122. [Google Scholar] [CrossRef]

- Salam, A.; Hikmat, I.; Haquei, F.; Badariah, E. The Influence of Share Ownership, Funding Decisions, Csr and Financial Performance of Food Industry. Ann. Rom. Soc. Cell Biol. 2021, 12698–12710. [Google Scholar]

- Uyar, A.; Kuzey, C.; Kilic, M.; Karaman, A.S. Board structure, financial performance, corporate social responsibility performance, CSR committee, and CEO duality: Disentangling the connection in healthcare. Corp. Soc. Responsib. Environ. Manag. 2021. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/csr.2141 (accessed on 10 November 2021).

- Bahta, D.; Yun, J.; Islam, M.R.; Bikanyi, K.J. How does CSR enhance the financial performance of SMEs? The mediating role of firm reputation. Econ. Res.-Ekon. Istraživanja 2021, 34, 1428–1451. [Google Scholar] [CrossRef]

- Aldehayyat, J. The role of corporate social responsibility initiatives, error management culture and corporate image in enhancing hotel performance. Manag. Sci. Lett. 2021, 11, 481–492. [Google Scholar] [CrossRef]

- Zou, Z.; Liu, Y.; Ahmad, N.; Sial, M.S.; Badulescu, A.; Zia-Ud-Din, M.; Badulescu, D. What Prompts Small and Medium Enterprises to Implement CSR? A Qualitative Insight from an Emerging Economy. Sustainability 2021, 13, 952. [Google Scholar] [CrossRef]

- McIntyre, J.R.; Ivanaj, S.; Ivanaj, V. CSR and Climate Change Implications for Multinational Enterprises; Edward Elgar Publishing: Cheltenham, UK, 2018. [Google Scholar]

- World Economic Forum, Open Letter from Global CEOs to World Leaders Urging Concrete Climate Action. Available online: https://www.weforum.org/agenda/2015/11/open-letter-from-ceos-to-world-leaders-urging-climate-action/ (accessed on 21 June 2021).

- Allen, M.W.; Craig, C.A. Rethinking corporate social responsibility in the age of climate change: A communication perspective. Int. J. Corp. Soc. Responsib. 2016, 1, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Youmatter. Is Europe in the Right Path for a Sustainable 2030? Available online: https://youmatter.world/en/is-europe-going-in-the-right-path-for-a-sustainable-2030/ (accessed on 21 July 2021).

- GermanWatch. Global Climate Risk Index 2020. Available online: https://www.germanwatch.org/ (accessed on 2 October 2020).

- Ahmad, N.; Ullah, Z.; Arshad, M.Z.; waqas Kamran, H.; Scholz, M.; Han, H. Relationship between corporate social responsibility at the micro-level and environmental performance: The mediating role of employee pro-environmental behavior and the moderating role of gender. Sustain. Prod. Consum. 2021, 27, 1138–1148. [Google Scholar] [CrossRef]

- Kumar, D.; Goyal, P.; Kumar, V. Prioritizing CSR barriers in the Indian service industry: A fuzzy AHP approach. Sci. Ann. Econ. Bus. 2019, 66, 213–233. [Google Scholar] [CrossRef]

- Abbas, M.; Gao, Y.; Shah, S.S.H. CSR and customer outcomes: The mediating role of customer engagement. Sustainability 2018, 10, 4243. [Google Scholar] [CrossRef] [Green Version]

- Mahmood, Z.; Kouser, R.; Iqbal, Z. Why Pakistani small and medium enterprises are not reporting on sustainability practices? Pak. J. Commer. Soc. Sci. (PJCSS) 2017, 11, 389–405. [Google Scholar]

- Hongming, X.; Ahmed, B.; Hussain, A.; Rehman, A.; Ullah, I.; Khan, F.U. Sustainability Reporting and Firm Performance: The Demonstration of Pakistani Firms. SAGE Open 2020, 10, 1–12. [Google Scholar] [CrossRef]

- Raza, J.; Majid, A. Perceptions and practices of corporate social responsibility among SMEs in Pakistan. Qual. Quant. 2016, 50, 2625–2650. [Google Scholar] [CrossRef]

- Asif, M.; Batool, S. Corporate social responsibility measurement approaches: Narrative review of literature on Islamic CSR. J. Islamic Bus. Manag. 2017, 7, 299–312. [Google Scholar]

- Sharma, A.; Singh, G. Conceptualizing corporate social responsibility practice: An integration of obligation and opportunity. Soc. Responsib. J. 2021. [Google Scholar] [CrossRef]

- Arevalo, J.A.; Aravind, D. Corporate social responsibility practices in India: Approach, drivers, and barriers. Corp. Gov. Int. J. Bus. Soc. 2011, 11, 399–414. [Google Scholar] [CrossRef]

- Arlbjørn, J.S.; Warming-Rasmussen, B.; van Liempd, D.; Mikkelsen, O.S. A European Survey on Corporate Social Responsibility; Syddansk Universitet, Institut for Entreprenørskab og Relationsledelse: Kolding, Denmark, 2008. [Google Scholar]

- Arvidsson, S. Communication of corporate social responsibility: A study of the views of management teams in large companies. J. Bus. Ethics 2010, 96, 339–354. [Google Scholar] [CrossRef]

- Pinto, L.; Allui, A. Critical drivers and barriers of corporate social responsibility in Saudi Arabia organizations. J. Asian Financ. Econ. Bus. 2020, 7, 259–268. [Google Scholar] [CrossRef]

- Yates, J.; Leggett, T. Qualitative research: An introduction. Radiol. Technol. 2016, 88, 225–231. [Google Scholar]

- Kuo, T.C.; Kremer, G.E.O.; Phuong, N.T.; Hsu, C.-W. Motivations and barriers for corporate social responsibility reporting: Evidence from the airline industry. J. Air Transp. Manag. 2016, 57, 184–195. [Google Scholar] [CrossRef]

- Yuen, K.F.; Lim, J.M. Barriers to the implementation of strategic corporate social responsibility in shipping. Asian J. Shipp. Logist. 2016, 32, 49–57. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Thomas. A Brief History of Corporate Social Responsibility (CSR). Available online: https://www.thomasnet.com/insights/history-of-corporate-social-responsibility/ (accessed on 28 July 2021).

- Committee for Economic Development. Social Responsibilities of Business Corporations; Committee for Economic Development: Washington, DC, USA, 1971. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Mintzberg, H. Please welcome CSR 2.0. In Rethinking Strategic Management; Springer: Berlin/Heidelberg, Germany, 2019; pp. 43–46. [Google Scholar]

- Visser, W. The Ages and Stages of CSR: From Defensive to Systemic Corporate Sustainability and Responsibility. CSR Int. Inspir. Ser. 2010, 8, 1–2. [Google Scholar]

- Ndubisi, N.O.; Zhai, X.A.; Lai, K.-h. Small and medium manufacturing enterprises and Asia’s sustainable economic development. Int. J. Prod. Econ. 2021, 233, 107971. [Google Scholar] [CrossRef]

- Shah, D.; Syed, A. Framework for SME sector development in Pakistan. Islamabad Plan. Comm. Pak. 2018, 1, 21–23. [Google Scholar]

- Kasi, A.M.; Raziq, A.; Khan, N.R. Exploring Environmental Sustainability Practices in Pakistani SMEs. J. Indep. Stud. Res. Manag. Soc. Sci. Econ. 2019, 17. Available online: https://www.semanticscholar.org/paper/Exploring-Environmental-Sustainability-Practices-in-Kasi-Raziq/671c79ba9ec3713109a20e60d6c1b30b4bcc77bf (accessed on 10 November 2021).

- Olusegun, A.I. Is small and medium enterprises (SMEs) an entrepreneurship? Int. J. Acad. Res. Bus. Soc. Sci. 2012, 2, 487. [Google Scholar]

- OECD. OECD SME and Entrepreneurship Outlook, 3rd ed.; The Organisation for Economic Cooperation and Development: Paris, France, 2005; p. 409. [Google Scholar]

- Dasanayaka, S. SMEs in globalized world: A brief note on basic profiles of Pakistan’s small and medium scale enterprises and possible research directions. Bus. Rev. 2008, 3, 69–77. [Google Scholar]

- Johnson, M.P.; Schaltegger, S. Two decades of sustainability management tools for SMEs: How far have we come? J. Small Bus. Manag. 2016, 54, 481–505. [Google Scholar] [CrossRef]

- Caldera, H.; Desha, C.; Dawes, L. Evaluating the enablers and barriers for successful implementation of sustainable business practice in ‘lean’ SMEs. J. Clean. Prod. 2019, 218, 575–590. [Google Scholar] [CrossRef]

- Tsvetkova, D.; Bengtsson, E.; Durst, S. Maintaining Sustainable Practices in SMEs: Insights from Sweden. Sustainability 2020, 12, 10242. [Google Scholar] [CrossRef]

- Journeault, M.; Perron, A.; Vallières, L. The collaborative roles of stakeholders in supporting the adoption of sustainability in SMEs. J. Environ. Manag. 2021, 287, 112349. [Google Scholar] [CrossRef]

- Bux, H.; Zhang, Z.; Ahmad, N. Promoting sustainability through corporate social responsibility implementation in the manufacturing industry: An empirical analysis of barriers using the ISM-MICMAC approach. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1729–1748. [Google Scholar] [CrossRef]

- Belas, J.; Çera, G.; Dvorský, J.; Čepel, M. Corporate social responsibility and sustainability issues of small-and medium-sized enterprises. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 721–730. [Google Scholar] [CrossRef]

- Verboven, H.; Vanherck, L. Sustainability management of SMEs and the UN sustainable development goals. uwf UmweltWirtschaftsForum 2016, 24, 165–178. [Google Scholar] [CrossRef]

- Burlea-Schiopoiu, A.; Mihai, L.S. An integrated framework on the sustainability of SMEs. Sustainability 2019, 11, 6026. [Google Scholar] [CrossRef] [Green Version]

- Choongo, P. A longitudinal study of the impact of corporate social responsibility on firm performance in SMEs in Zambia. Sustainability 2017, 9, 1300. [Google Scholar] [CrossRef] [Green Version]

- Puppim de Oliveira, J.A.; Jabbour, C.J.C. Environmental management, climate change, CSR, and governance in clusters of small firms in developing countries: Toward an integrated analytical framework. Bus. Soc. 2017, 56, 130–151. [Google Scholar] [CrossRef]

- Ahmad, N.; Scholz, M.; Ullah, Z.; Arshad, M.Z.; Sabir, R.I.; Khan, W.A. The nexus of CSR and co-creation: A roadmap towards consumer loyalty. Sustainability 2021, 13, 523. [Google Scholar] [CrossRef]

- Kong, L.; Sial, M.S.; Ahmad, N.; Sehleanu, M.; Li, Z.; Zia-Ud-Din, M.; Badulescu, D. CSR as a potential motivator to shape employees’ view towards nature for a sustainable workplace environment. Sustainability 2021, 13, 1499. [Google Scholar] [CrossRef]

- Gupta, S.; Nawaz, N.; Alfalah, A.A.; Naveed, R.T.; Muneer, S.; Ahmad, N. The Relationship of CSR Communication on Social Media with Consumer Purchase Intention and Brand Admiration. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1217–1230. [Google Scholar] [CrossRef]

- SECP. Voluntary Guidelines on CSR. Available online: https://www.secp.gov.pk/ur/document/voluntary-guidelines-for-csr-2013/ (accessed on 27 October 2021).

- Smith, A.M.; Wahga, A.I. Reducing the negative environmental impact of SMEs in Pakistan’s leather and tanning industry. In Social Marketing: Rebels with a Cause, 3rd ed.; Hastings, G., Domegan, C., Eds.; Routledge: Hasting, UK, 2017. [Google Scholar]

- Reimer, M.; Van Doorn, S.; Heyden, M.L. Unpacking functional experience complementarities in senior leaders’ influences on CSR strategy: A CEO–Top management team approach. J. Bus. Ethics 2018, 151, 977–995. [Google Scholar] [CrossRef]

- Goyal, P.; Kumar, D. Modeling the CSR barriers in manufacturing industries. Benchmarking: Int. J. 2017, 24, 1871–1890. [Google Scholar] [CrossRef]

- Kumar, D.; Goyal, P.; Kumar, V. Modeling and classification of enablers of CSR in Indian firms. J. Model. Manag. 2019, 14, 456–475. [Google Scholar] [CrossRef]

- Yusliza, M.Y.; Norazmi, N.A.; Jabbour, C.J.C.; Fernando, Y.; Fawehinmi, O.; Seles, B.M.R.P. Top management commitment, corporate social responsibility and green human resource management. Benchmark. Int. J. 2019, 26, 2051–2078. [Google Scholar] [CrossRef]

- Singh, K.; Misra, M. How to bring positive societal change through Corporate Social Responsibility (CSR)? Modeling the social responsible enablers using ISM-MICMAC. In Proceedings of the 2020 IEEE Technology & Engineering Management Conference (TEMSCON), Novi, MI, USA, 3–6 June 2020; pp. 1–6. [Google Scholar]

- Jamali, D.; Lund-Thomsen, P.; Jeppesen, S. SMEs and CSR in developing countries. Bus. Soc. 2017, 56, 11–22. [Google Scholar] [CrossRef]

- Tamvada, M. Corporate social responsibility and accountability: A new theoretical foundation for regulating CSR. Int. J. Corp. Soc. Responsib. 2020, 5, 2. [Google Scholar] [CrossRef] [Green Version]

- Sison, A.J.G. From CSR to corporate citizenship: Anglo-American and continental European perspectives. J. Bus. Ethics 2009, 89, 235–246. [Google Scholar] [CrossRef]

- Mackey, S. Virtue ethics, CSR and “corporate citizenship”. J. Commun. Manag. 2014, 18, 131–145. [Google Scholar] [CrossRef]

- Singh, K.; Misra, M. The evolving path of CSR: Toward business and society relationship. J. Econ. Adm. Sci. 2021. ahead of print. [Google Scholar] [CrossRef]

- Shen, L.; Govindan, K.; Shankar, M. Evaluation of barriers of corporate social responsibility using an analytical hierarchy process under a fuzzy environment—A textile case. Sustainability 2015, 7, 3493–3514. [Google Scholar] [CrossRef] [Green Version]

- Merwe, M.; Wocke, A. An investigation into responsible tourism practices in the South African hotel industry. S. Afr. J. Bus. Manag. 2007, 38, 1–15. [Google Scholar]

- Bello, F.G.; Kamanga, G. Drivers and barriers of corporate social responsibility in the tourism industry: The case of Malawi. Dev. S. Afr. 2020, 37, 181–196. [Google Scholar] [CrossRef]

- Steiner, G.A. Strategic Planning; Simon and Schuster: New York, NY, USA, 2010. [Google Scholar]

- Bryson, J.M. Strategic planning and action planning for nonprofit organizations. Jossey-Bass Handb. Nonprofit Leadersh. Manag. 1994, 2, 154–183. [Google Scholar]

- Boyne, G. Strategic planning. Public Service Improvement: Theories and Evidence; Ashworth, R., Boyne, G.A., Entwistle, T., Eds.; Cardiff University: Cardiff UK, 2010; pp. 60–77. [Google Scholar]

- Epstein, M.J.; Buhovac, A.R.; Yuthas, K. Managing social, environmental and financial performance simultaneously. Long Range Plan. 2015, 48, 35–45. [Google Scholar] [CrossRef]

- Lam, J.S.L.; Lim, J.M. Incorporating corporate social responsibility in strategic planning: Case of ship-operating companies. Int. J. Shipp. Transp. Logist. 2016, 8, 273–293. [Google Scholar] [CrossRef]

- Freeman, E.; Moutchnik, A. Stakeholder management and CSR: Questions and answers. Umw. Wirtsch. Forum 2013, 21, 5–9. [Google Scholar] [CrossRef]

- Sitnikov, C.; Bocean, C. Relationships between corporate social responsibility and strategic planning. In Stages of Corporate Social Responsibility; Springer: Berlin/Heidelberg, Germany, 2017; pp. 121–137. [Google Scholar]

- Blasi, S.; Caporin, M.; Fontini, F. A multidimensional analysis of the relationship between corporate social responsibility and firms’ economic performance. Ecol. Econ. 2018, 147, 218–229. [Google Scholar] [CrossRef]

- Costa, R.; Menichini, T. A multidimensional approach for CSR assessment: The importance of the stakeholder perception. Expert Syst. Appl. 2013, 40, 150–161. [Google Scholar] [CrossRef]

- Mazutis, D.D.; Slawinski, N. Reconnecting business and society: Perceptions of authenticity in corporate social responsibility. J. Bus. Ethics 2015, 131, 137–150. [Google Scholar] [CrossRef]

- Hsu, J.L.; Cheng, M.C. What prompts small and medium enterprises to engage in corporate social responsibility? A study from Taiwan. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 288–305. [Google Scholar] [CrossRef]

- Zhu, Q.; Zhang, Q. Evaluating practices and drivers of corporate social responsibility: The Chinese context. J. Clean. Prod. 2015, 100, 315–324. [Google Scholar] [CrossRef]

- Galetska, T.; Natalya, T.; Topishko, I. Social Responsibility of Economic Enterprises as a Social Good: Practice of the EU and Ukraine. Balt. J. Econ. Stud. 2020, 6, 24–35. [Google Scholar] [CrossRef]

- Morgan, C. 5 Sustainable Living Practices Europe Teaches the Rest of the World. Available online: https://www.yogiapproved.com/life/sustainable-living-europe/ (accessed on 11 August 2021).

- Jia, F.; Zuluaga-Cardona, L.; Bailey, A.; Rueda, X. Sustainable supply chain management in developing countries: An analysis of the literature. J. Clean. Prod. 2018, 189, 263–278. [Google Scholar] [CrossRef]

- Alotaibi, A.; Edum-Fotwe, F.; Price, A.D. Critical barriers to social responsibility implementation within mega-construction projects: The case of the Kingdom of Saudi Arabia. Sustainability 2019, 11, 1755. [Google Scholar] [CrossRef] [Green Version]

- Doane, D. Beyond corporate social responsibility: Minnows, mammoths and markets. Futures 2005, 37, 215–229. [Google Scholar] [CrossRef]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students; Pearson Education: London, UK, 2009. [Google Scholar]

- Schmidt, C. The analysis of semi-structured interviews. Companion Qual. Res. 2004, 253, 258. [Google Scholar]

- Longhurst, R. Semi-structured interviews and focus groups. Key Methods Geogr. 2003, 3, 143–156. [Google Scholar]

- IQAir. Air quality in Pakistan. Available online: https://www.iqair.com/us/pakistan (accessed on 9 May 2021).

- Bailey, B.C.; Peck, S.I. Boardroom strategic decision-making style: Understanding the antecedents. Corp. Gov. Int. Rev. 2013, 21, 131–146. [Google Scholar] [CrossRef]

- Alshbili, I.; Elamer, A.A.; Moustafa, M.W. Social and environmental reporting, sustainable development and institutional voids: Evidence from a developing country. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 881–895. [Google Scholar] [CrossRef]

- Fibre2Fashion. Various Pollutants Released into Environment by Textile Industry. Available online: https://www.fibre2fashion.com/industry-article/6262/various-pollutants-released-into-environment-by-textile-industry (accessed on 29 October 2021).

- NRDC. Encourage Textile Manufacturers to Reduce Pollution. Available online: https://www.nrdc.org/issues/encourage-textile-manufacturers-reduce-pollution (accessed on 29 October 2021).

- Hashmi, G.J.; Dastageer, G.; Sajid, M.S.; Ali, Z.; Malik, M.; Liaqat, I. Leather industry and environment: Pakistan scenario. Int. J. Appl. Biol. Forensics 2017, 1, 20–25. [Google Scholar]

- Creswell, J.W.; Hanson, W.E.; Clark Plano, V.L.; Morales, A. Qualitative research designs: Selection and implementation. Couns. Psychol. 2007, 35, 236–264. [Google Scholar] [CrossRef]

- Miles, M.B.; Huberman, A.M. Qualitative Data Analysis: An Expanded Sourcebook; Sage: Newcastle upon Tyne, UK, 1994. [Google Scholar]

- Braun, V.; Clarke, V. Using thematic analysis in psychology. Qual. Res. Psychol. 2006, 3, 77–101. [Google Scholar] [CrossRef] [Green Version]

- Dixit, S.K.; Priya, S.S. Barriers to corporate social responsibility: An Indian SME perspective. Int. J. Emerg. Mark. 2021. ahead of print. [Google Scholar] [CrossRef]

- Awan, U.; Khattak, A.; Kraslawski, A. Corporate social responsibility (CSR) priorities in the small and medium enterprises (SMEs) of the industrial sector of Sialkot, Pakistan. In Corporate Social Responsibility in the Manufacturing and Services Sectors; Springer: Berlin/Heidelberg, Germany, 2019; pp. 267–278. [Google Scholar]

- Bello, F.G.; Banda, W.; Kamanga, G. Corporate Social Responsibility (CSR) practices in the hospitality industry in Malawi. Afr. J. Hosp. Tour. Leis. 2017, 6, 1–21. [Google Scholar]

- Sarvajayakesavalu, S. Addressing challenges of developing countries in implementing five priorities for sustainable development goals. Ecosyst. Health Sustain. 2015, 1, 1–4. [Google Scholar] [CrossRef]

- Battaglia, M.; Bianchi, L.; Frey, M.; Iraldo, F. An innovative model to promote CSR among SMEs operating in industrial clusters: Evidence from an EU project. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 133–141. [Google Scholar] [CrossRef]

- Baniya, R.; Rajak, K. Attitude, Motivation and barriers for csr engagement among travel and tour operators in Nepal. J. Tour. Hosp. Educ. 2020, 10, 53–70. [Google Scholar] [CrossRef]

- Jenkins, H. A critique of conventional CSR theory: An SME perspective. J. Gen. Manag. 2004, 29, 37–57. [Google Scholar] [CrossRef]

- Aras-Beger, G.; Taşkın, F.D. Corporate Social Responsibility (CSR) in Multinational Companies (MNCs), Small-to-Medium Enterprises (SMEs), and Small Businesses. The Palgrave Handbook of Corporate Social Responsibility; Springer: Gewerbesrasse, Switzerland, 2021; pp. 791–815. [Google Scholar]

- El-Bassiouny, D. Corporate social responsibility (CSR) and the developing world: Highlights on the Egyptian case with implications for CSR education. In Ethics, CSR and Sustainability (ECSRS) Education in the Middle East and North Africa (MENA) Region; Routledge: Abingdon, UK, 2020; pp. 34–50. [Google Scholar]

- Waqas, M.; Dong, Q.-l.; Ahmad, N.; Zhu, Y.; Nadeem, M. Critical barriers to implementation of reverse logistics in the manufacturing industry: A case study of a developing country. Sustainability 2018, 10, 4202. [Google Scholar] [CrossRef] [Green Version]

- World Bank. Regulatory Reform: The Foundation for Sustainable Growth. Available online: https://www.worldbank.org/en/news/feature/2019/03/21/regulatory-reform-the-foundation-for-sustainable-growth (accessed on 30 August 2021).

- Álvarez Jaramillo, J.; Zartha Sossa, J.W.; Orozco Mendoza, G.L. Barriers to sustainability for small and medium enterprises in the framework of sustainable development—Literature review. Bus. Strategy Environ. 2019, 28, 512–524. [Google Scholar]

- Agwu, M. Analysis of the impact of strategic management on the business performance of SMEs in Nigeria. Acad. Strateg. Manag. J. 2018, 17, 1–20. [Google Scholar]

- Galbreath, J. Drivers of corporate social responsibility: The role of formal strategic planning and firm culture. Br. J. Manag. 2010, 21, 511–525. [Google Scholar] [CrossRef]

- Sweeney, L. Corporate social responsibility in Ireland: Barriers and opportunities experienced by SMEs when undertaking CSR. Corp. Gov. Int. J. Bus. Soc. 2007, 7, 516–523. [Google Scholar] [CrossRef]

- Colgan, F. Equality, diversity and corporate responsibility. Equal. Divers. Incl. Int. J. 2011, 30, 719–734. [Google Scholar] [CrossRef]

- Pham, H.; Pham, T.; Dang, C.N. Barriers to corporate social responsibility practices in construction and roles of education and government support. Eng. Constr. Archit. Manag. 2021. ahead of print. [Google Scholar] [CrossRef]

{kind=link}

| Ages | CSR Stage | CSR Interest | CSR Target |

|---|---|---|---|

| Greed | Defensive | Ad hoc based | Stakeholders (government employees, owner, etc.) |

| Philanthropy | Charitable | Programs for community betterment | Local community |

| Marketing | Promotional | Reputation building | General public |

| Management | Strategic | Management systems | Shareholders and NGOs |

| Responsibility | Transformative | Business models | Regulators and customers |

| No | SME Type | Sector | Business Focus | Workforce | Interviewing Person | Duration of Interview | Code |

|---|---|---|---|---|---|---|---|

| 1 | M | Textile | F | 59 | Unit Manager | 42 | P |

| 2 | M | Chemicals | L | 47 | Manager | 40 | L |

| 3 | S | Apparels | F | 21 | Owner/Manager | 33 | M |

| 4 | M | Pharmaceutical | L | 44 | Manager | 48 | N |

| 5 | S | Footwear | L | 19 | Owner/Manager | 30 | J |

| 6 | S | Chemicals | L | 12 | Owner/Manager | 30 | I |

| 7 | S | Apparels | F | 20 | Owner/Manager | 37 | U |

| 8 | M | Textile | F | 81 | Unit Manager | 50 | H |

| 9 | M | Apparels | F | 86 | Manager Operations | 42 | B |

| 10 | S | Pharmaceutical | L | 18 | Owner/Manager | 36 | V |

| 11 | M | Apparels | F | 79 | General Manager | 46 | G |

| 12 | M | Textile | L | 49 | Unit Manager | 38 | Y |

| 13 | S | Footwear | L | 19 | Owner/Manager | 36 | T |

| 14 | M | Textile | F | 88 | Unit Manager | 50 | F |

| 15 | M | Apparels | L | 92 | General Manager | 50 | C |

| 16 | S | Pharmaceutical | L | 18 | Owner/Manager | 38 | X |

| 17 | S | Chemicals | L | 16 | Owner/Manager | 33 | D |

| 18 | M | Apparels | F | 67 | General Manager | 45 | R |

| 19 | M | Textile | F | 58 | Unit Manager | 47 | E |

| 20 | S | Chemicals | L | 16 | Owner/Manager | 28 | S |

| 21 | M | Footwear | L | 74 | Manager Operations | 39 | Z |

| 22 | M | Apparels | F | 83 | General Manager | 43 | A |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mahmood, A.; Naveed, R.T.; Ahmad, N.; Scholz, M.; Khalique, M.; Adnan, M. Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach. Sustainability 2021, 13, 12710. https://doi.org/10.3390/su132212710

Mahmood A, Naveed RT, Ahmad N, Scholz M, Khalique M, Adnan M. Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach. Sustainability. 2021; 13(22):12710. https://doi.org/10.3390/su132212710

Chicago/Turabian StyleMahmood, Asif, Rana Tahir Naveed, Naveed Ahmad, Miklas Scholz, Muhammad Khalique, and Mohammad Adnan. 2021. "Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach" Sustainability 13, no. 22: 12710. https://doi.org/10.3390/su132212710

APA StyleMahmood, A., Naveed, R. T., Ahmad, N., Scholz, M., Khalique, M., & Adnan, M. (2021). Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach. Sustainability, 13(22), 12710. https://doi.org/10.3390/su132212710