The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics

Abstract

1. Introduction

2. Literature Review

3. Data and Methodology

4. Results and Discussion

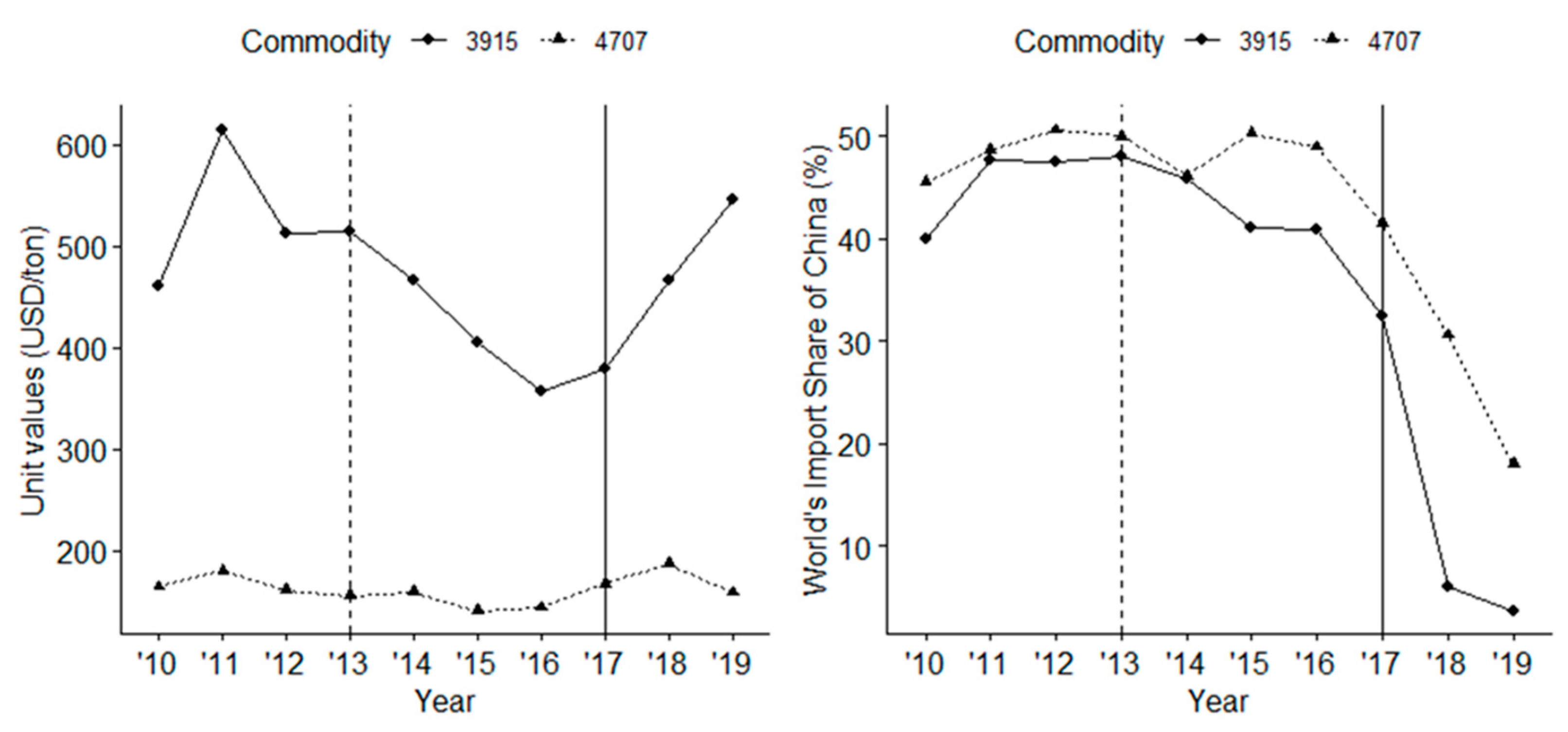

4.1. The Impact of OGF and National Sword on Chinese Waste Imports

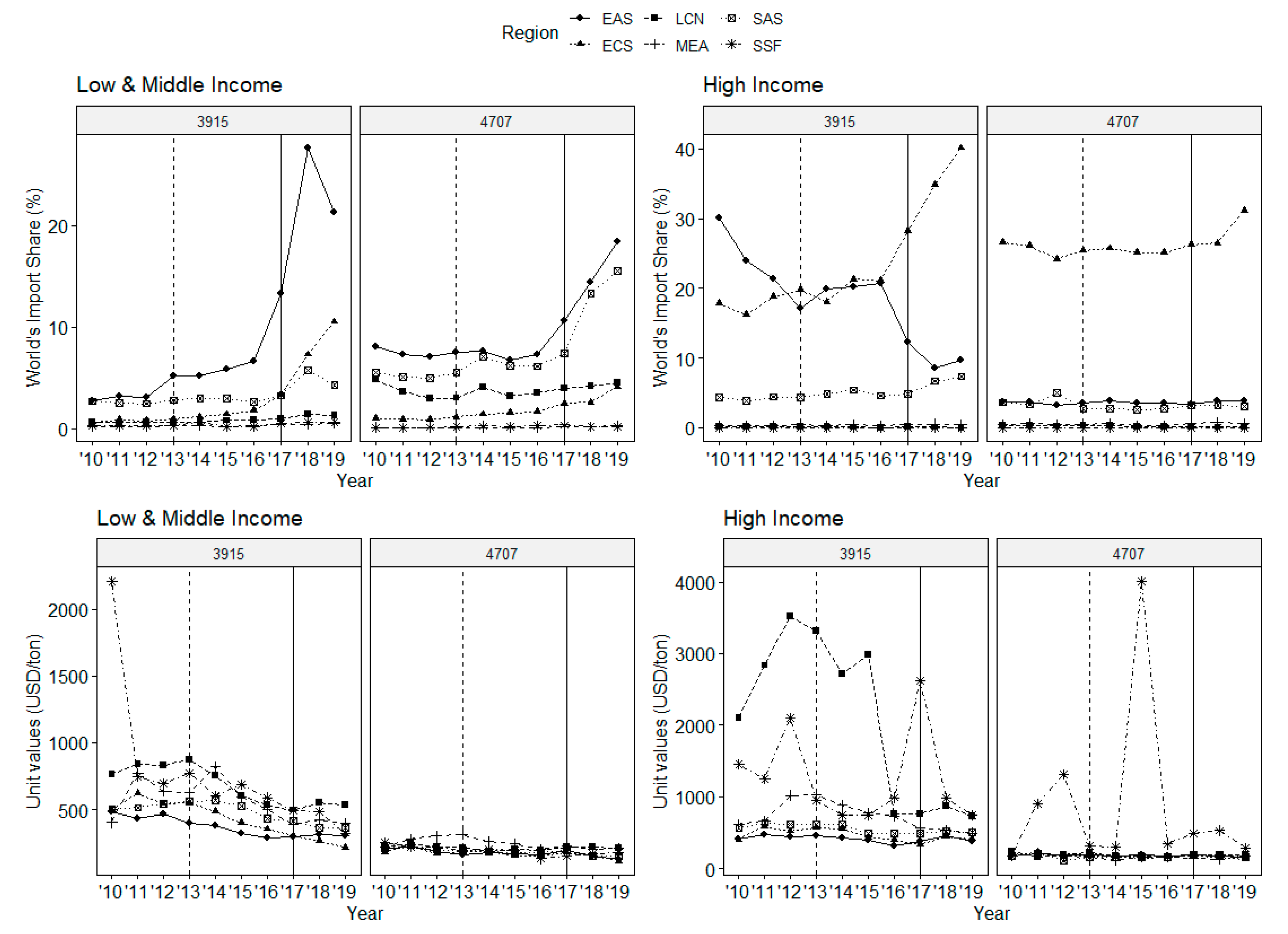

4.2. The Trade Diversion Impact of OGF and National Sword

4.3. Impact on Shipping Logistics

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| High Income | Low & Middle Income | |

|---|---|---|

| East Asia & Pacific | Australia, Brunei Darussalam, French Polynesia, Japan, Korea Rep., New Caledonia, New Zealand, Singapore | Cambodia, Fiji, Indonesia, Lao PDR, Malaysia, Mongolia, Myanmar, Papua New Guinea, Philippines, Solomon Islands, Thailand, Vietnam |

| Europe & Central Asia | Austria, Belgium, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Faroe Islands, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Lithuania, Netherlands, Norway, Poland, Portugal, Romania, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, United Kingdom | Albania, Belarus, Bulgaria, Russian Federation, Serbia, Turkey, Ukraine |

| Latin America & Caribbean | Antigua and Barbuda, The Bahamas, Barbados, Chile, Panama, Trinidad and Tobago, Uruguay | Argentina, Belize, Bolivia, Brazil, Colombia, Costa Rica, Cuba, Dominica, Dominican Republic, Ecuador, El Salvador, Guatemala, Guyana, Haiti, Honduras, Jamaica, Mexico, Nicaragua, Paraguay, Peru, St. Lucia, St. Vincent & the Grenadines, Suriname, Venezuela RB |

| Middle East & North Africa | Bahrain, Israel, Kuwait, Malta, Oman, Qatar, Saudi Arabia, United Arab Emirates | Algeria, Djibouti, Egypt Arab Rep., Iran Islamic Rep., Jordan, Lebanon, Morocco, Syrian Arab Republic, Tunisia, Yemen Rep. |

| North America | Canada, United States | |

| Sub-Saharan Africa | Mauritius | Cabo Verde, Cameroon, Congo Rep., Cote d’Ivoire, Ethiopia, Ghana, Kenya, Mali, Mauritania, Mozambique, Namibia, Nigeria, Senegal, Sierra Leone, South Africa, Sudan, Tanzania, Uganda, Zambia, Zimbabwe |

| South Asia | Afghanistan, Bangladesh, India, Nepal, Pakistan, Sri Lanka |

Appendix B

References

- Kellenberg, D. The economics of the international trade of waste. Annu. Rev. Resour. Econ. 2015, 7, 109–125. [Google Scholar] [CrossRef]

- Grace, R.; Turner, R.K.; Walter, I. Secondary materials and international trade. J. Environ. Econ. Manag. 1978, 5, 172–186. [Google Scholar] [CrossRef]

- Yore, G.W. Secondary materials and international trade: A comment on the domestic market. J. Environ. Econ. Manag. 1979, 6, 199–203. [Google Scholar] [CrossRef]

- Baggs, J. International trade in hazardous waste. Rev. Int. Econ. 2009, 17, 1–16. [Google Scholar] [CrossRef]

- Kellenberg, D. Trading wastes. J. Environ. Econ. Manag. 2012, 64, 68–87. [Google Scholar] [CrossRef]

- Copeland, B.R.; Taylor, M.S. Trade, spatial separation, and the environment. J. Int. Econ. 1999, 47, 137–168. [Google Scholar] [CrossRef]

- UN Comtrade. United Nations Commodity Trade Statistics Database. Available online: http://comtrade.un.org (accessed on 1 July 2020).

- Matsuda, T.; Hanaoka, S.; Kawasaki, T. Cost analysis of bulk cargo containerization. Marit. Policy Manag. 2020, 1–20. [Google Scholar] [CrossRef]

- Balkevicius, A.; Sanctuary, M.; Zvirblyte, S. Fending off waste from the west: The impact of China’s Operation Green Fence on the international waste trade. World Econ. 2020. [Google Scholar] [CrossRef]

- Jambeck, J.R.; Geyer, R.; Wilcox, C.; Siegler, T.R.; Perryman, M.; Andrady, A.; Narayan, R.; Law, K.L. Plastic waste inputs from land into the ocean. Science 2015, 347, 768–771. [Google Scholar] [CrossRef] [PubMed]

- Resource-Recycling. Operation Green Fence Is Deeply Affecting Export Markets, 2013. Resource Recycling News. 12 April 2013. Available online: https://resource-recycling.com/recycling/2013/04/12/operation-green-fence-is-deeply-affecting-export-markets/ (accessed on 14 September 2020).

- WTO. Catalogue of Solid Wastes Forbidden to Import into China by the End of 2017 (4 Classes, 24 Kinds). Notification No. G/TBT/N/CHN/1211. 2017. Available online: http://tbtims.wto.org/en/RegularNotifications/View/137356 (accessed on 1 July 2020).

- Resource Recycling. From Green Fence to Red Alert: A China Timeline. Resource Recycling News. 13 February 2017. Available online: https://resource-recycling.com/recycling/2018/02/13/green-fence-red-alert-china-timeline/ (accessed on 15 September 2020).

- Basel Convention. Questions and Answers Related to the Basel Convention Plastic Waste Amendments. Available online: http://www.basel.int/Implementation/Plasticwaste/PlasticWasteAmendments/FAQs/tabid/8427/Default.aspx (accessed on 14 September 2020).

- Sun, M. The effect of border controls on waste imports: Evidence from China’s Green Fence campaign. China Econ. Rev. 2019, 54, 457–472. [Google Scholar] [CrossRef]

- Brooks, A.L.; Wang, S.; Jambeck, J.R. The Chinese import ban and its impact on global plastic waste trade. Sci. Adv. 2018. [Google Scholar] [CrossRef] [PubMed]

- Wang, W.; Themelis, N.J.; Sun, K.; Bourtsalas, A.C.; Huang, Q.; Zhang, Y.; Wu, Z. Current influence of China’s ban on plastic waste imports. Waste Dispos. Sustain. Energy 2019, 1, 67–78. [Google Scholar] [CrossRef]

- Huang, Q.; Chen, G.; Wang, Y.; Chen, S.; Xu, L.; Wang, R. Modelling the global impact of China’s ban on plastic waste imports. Resour. Conserv. Recycl. 2020, 154, 104607. [Google Scholar] [CrossRef]

- Wang, C.; Zhao, L.; Lim, M.K.; Chen, W.-Q.; Sutherland, J.W. Structure of the global plastic waste trade network and the impact of China’s import Ban. Resour. Conserv. Recycl. 2020, 153, 104591. [Google Scholar] [CrossRef]

- Head, K.; Mayer, T. Chapter 3—Gravity Equations: Workhorse, Toolkit, and Cookbook. In Handbook of International Economics; Helpman, E., Gopinath, G., Rogoff, K., Eds.; Elsevier: Amsterdam, The Netherlands, 2014; Volume 4, pp. 131–195. [Google Scholar]

- Berglund, C.; Söderholm, P. An Econometric Analysis of Global Wastepaper Recovery and Utilization. Environ. Resour. Econ. 2003, 26, 429–456. [Google Scholar] [CrossRef]

- Van Beukering, P.J.H.; Bouman, M.N. Empirical Evidence on Recycling and Trade of Paper and Lead in Developed and Developing Countries. World Dev. 2001, 29, 1717–1737. [Google Scholar] [CrossRef]

- Helpman, E.; Krugman, P.R. Trade Policy and Market Structure; MIT Press: Cambridge, MA, USA, 1989. [Google Scholar]

- Maskus, K.E.; Wilson, J.S.; Otsuki, T. Quantifying the Impact of Technical Barriers to Trade: A Framework for Analysis; Policy Research Working Paper Series; World Bank: Washington, DC, USA, 2000; p. 2512. [Google Scholar]

- Bao, X.; Chen, W.C. The Impacts of Technical Barriers to Trade on Different Components of International Trade: Impacts of TBT on International Trade. Rev. Dev. Econ. 2013, 17, 447–460. [Google Scholar] [CrossRef]

- Hummels, D.; Klenow, P.J. The Variety and Quality of a Nation’s Exports. Am. Econ. Rev. 2005, 95, 704–723. [Google Scholar] [CrossRef]

- Theofanis, S.; Boile, M. Empty marine container logistics: Facts, issues and management strategies. GeoJournal 2009, 74, 51–65. [Google Scholar] [CrossRef]

- Tamvakis, M. International Seaborne Trade. In The Blackwell Companion to Maritime Economics; Tally, W., Ed.; Blackwell Publishing Ltd.: Hoboken, NJ, USA, 2012. [Google Scholar]

- Rodrigue, J.P. The Geography of Transport Systems, 4th ed.; Routledge: Abingdon, UK, 2017. [Google Scholar]

- Sanders, U.; Riedl, J.; Schlingmeier, J.; Roeloffs, C. Bringing the Sharing Economy to Shipping, The Boston Consulting Group. 2016. Available online: https://www.bcg.com/publications/2016/transportation-travel-tourism-bringingsharing-economy-to-shipping.aspx (accessed on 29 August 2018).

- Asian Development Bank. Strengthening Disaster Resilience. 2019. Available online: https://www.adb.org/documents/adb-annual-report-2019 (accessed on 14 December 2020).

- World Bank. List of Economies. June 2020. Available online: http://shop.ifrs.org/files/CLASS20.pdf (accessed on 1 July 2020).

- Resource-Recycling. OCC and Mixed Paper: A Tale of Two Exports, 2018. Resource Recycling News. 11 December 2018. Available online: https://resource-recycling.com/recycling/2018/12/11/occ-and-mixed-paper-a-tale-of-two-exports/ (accessed on 14 September 2020).

- TIME. Southeast Asia Pushes Back against Global Garbage Trade. 2019. Available online: https://time.com/5598032/southeast-asia-plastic-waste-malaysia-philippines/ (accessed on 10 September 2020).

- Berg, P.; Lingqvist, O. Pulp, Paper, and Packaging in the Next Decade: Transformational Change. McKinsey & Company. 2019. Available online: https://www.mckinsey.com/industries/paper-and-forest-products/ourinsights/pulp-paper-and-packaging-in-the-next-decade-transformationalchange (accessed on 10 September 2020).

| Commodity | Margin | National Sword (2017) | Operation Green Fence (2013) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Quantity Change (%) | Unit Value Change (%) | Quantity Change (%) | Unit Value Change (%) | ||||||

| Total Change | UV Change | Share Change | Total Change | UV Change | Share Change | ||||

| Waste Plastic (3915) | Total | −92.1 | 27.4 | 31.5 | −4.1 | −7.3 | −22.3 | −22.0 | −0.3 |

| Entry | 0.0 | 0.6 | 0.0 | 0.6 | 0.1 | 0.1 | 0.0 | 0.1 | |

| Exit | −3.3 | −3.8 | −3.8 | 0.0 | −0.4 | −0.5 | −0.5 | 0.0 | |

| Intensive | −88.8 | 30.6 | 35.3 | −4.7 | −7.0 | −21.8 | −21.5 | −0.3 | |

| Used Paper (4707) | Total | −56.0 | 12.7 | 34.8 | −22.2 | −8.6 | −17.1 | −7.3 | −9.8 |

| Entry | 0.2 | 0.4 | 0.0 | 0.4 | 0.2 | 0.2 | 0.0 | 0.2 | |

| Exit | −0.3 | −0.3 | −0.3 | 0.0 | −0.2 | −0.1 | −0.1 | 0.0 | |

| Intensive | −55.9 | 12.6 | 35.1 | −22.6 | −8.6 | −17.2 | −7.2 | −10.0 | |

| Commodity | Country Group | Before 2017 | After 2017 | Quantity Change (%) | UV Change (%) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Quantity (1000 tons) | Share (%) | UV (USD/tons) | Quantity (1000 tons) | Share (%) | UV (USD/tons) | Total Change | Pure UV | Share Change | |||

| Waste Plastic (3915) | Europe & Central Asia (HIC) | 3,168 | 32% | 333 | 87 | 11% | 407 | −30.7 | −15.8 | 5.3 | −21.1 |

| East Asia & Pacific (HIC) | 2,168 | 22% | 371 | 82 | 10% | 570 | −20.8 | −5.6 | 10.1 | −15.7 | |

| East Asia & Pacific (LMY) | 2,000 | 20% | 477 | 511 | 64% | 511 | −14.8 | 59.0 | 10.8 | 48.1 | |

| North America (HIC) | 1,822 | 18% | 358 | 65 | 8% | 470 | −17.5 | −4.5 | 9.3 | −13.8 | |

| Latin America & Caribbean (LMY) | 415 | 4% | 373 | 15 | 2% | 512 | −4.0 | −2.5 | −1.5 | −1.1 | |

| Used Paper (4707) | North America (HIC) | 30,011 | 53% | 138 | 13,704 | 55% | 172 | −28.6 | 14.5 | 11.1 | 3.4 |

| Europe & Central Asia (HIC) | 17,360 | 30% | 143 | 6,201 | 25% | 178 | −19.6 | −1.6 | 4.3 | −5.9 | |

| East Asia & Pacific (HIC) | 8,886 | 16% | 156 | 4,561 | 18% | 193 | −7.6 | −1.2 | 20.0 | −21.2 | |

| Latin America & Caribbean (LMY) | 671 | 1% | 152 | 195 | 1% | 215 | −0.8 | −0.7 | −0.6 | −0.1 | |

| Middle East & North Africa (HIC) | 48 | 0% | 192 | 155 | 1% | 209 | 0.2 | 0.3 | −0.0 | 0.4 | |

| East Asia & Pacific (LMY) | 5 | 0% | 151 | 197 | 1% | 213 | 0.3 | 1.0 | 0.0 | 1.0 | |

| Commodity | Margin | National Sword (2017) | Operation Green Fence (2013) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| East Asia & Pacific (LMY) | Europe & Central Asia (LMY) | South Asia (LMY) | Europe & Central Asia (HIC) | East Asia & Pacific (LMY) | Europe & Central Asia (LMY) | South Asia (LMY) | Europe & Central Asia (HIC) | ||

| Waste Plastic (3915) | Total | 161.4 | 266.3 | 20.7 | 16.5 | 75.2 | 57.8 | 20.5 | 13.2 |

| Entry | 6.9 | 30.4 | 3.0 | 3.8 | 5.9 | 15.5 | 6.1 | 2.5 | |

| Exit | −1.0 | −1.9 | −3.1 | −1.1 | −4.7 | −6.1 | −1.9 | −2.7 | |

| Intensive | 155.5 | 237.8 | 20.8 | 13.8 | 74.0 | 48.4 | 16.2 | 13.5 | |

| Used Paper (4707) | Total | 101.4 | 76.7 | 104.0 | −0.2 | −5.6 | 52.9 | 23.7 | −5.1 |

| Entry | 5.5 | 8.8 | 1.1 | 0.3 | 1.5 | 8.9 | 0.8 | 0.9 | |

| Exit | −1.4 | −1.6 | −1.2 | −0.4 | −2.3 | −1.2 | −1.1 | −0.5 | |

| Intensive | 97.3 | 69.4 | 104.2 | −0.1 | −4.8 | 45.2 | 24.0 | −5.4 | |

| Routes | Main Haul | Backhaul | Imbalance | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2017 (mil. TEU) | 2019 (mil. TEU) | %Change | 2017 (mil. TEU) | 2019 (mil. TEU) | %Change | 2017 (mil. TEU) | 2019 (mil. TEU) | %Change | |

| FE-North America | 18.6 | 18.7 | 0.8 | 8.0 | 7.4 | −6.8 | 10.6 | 11.3 | 6.4 |

| FE-Europe | 15.8 | 16.7 | 5.4 | 7.8 | 8.2 | 4.2 | 8.0 | 8.5 | 6.5 |

| FE-IS and ME | 7.5 | 7.0 | −6.4 | 2.8 | 2.8 | −0.4 | 4.7 | 4.2 | −10.1 |

| Europe-IS and ME | 3.9 | 4.0 | 4.3 | 2.7 | 2.9 | 5.2 | 1.1 | 1.2 | 2.3 |

| Europe-North America | 4.7 | 5.1 | 9.1 | 2.7 | 3.0 | 10.2 | 1.9 | 2.1 | 7.5 |

| North America-South and Central America | 2.9 | 2.9 | 0.5 | 2.5 | 2.5 | 1.9 | 0.4 | 0.4 | −7.8 |

| FE-South and Central America | 3.6 | 3.9 | 6.5 | 1.8 | 1.9 | 8.0 | 1.8 | 1.9 | 5.0 |

| FE-Oceania | 2.6 | 2.6 | 0.4 | 1.6 | 1.6 | −1.8 | 1.0 | 1.0 | 3.8 |

| FE-Sub Saharan Africa | 2.8 | 3.2 | 13.8 | 1.2 | 1.3 | 9.9 | 1.7 | 1.9 | 16.5 |

| Europe-Sub Saharan Africa | 2.0 | 2.2 | 7.8 | 0.8 | 0.8 | 1.8 | 1.2 | 1.3 | 12.0 |

| Others | 7.0 | 7.5 | 7.4 | 4.7 | 5.1 | 8.2 | 2.3 | 2.4 | 5.8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tran, T.; Goto, H.; Matsuda, T. The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics. Sustainability 2021, 13, 987. https://doi.org/10.3390/su13020987

Tran T, Goto H, Matsuda T. The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics. Sustainability. 2021; 13(2):987. https://doi.org/10.3390/su13020987

Chicago/Turabian StyleTran, Trang, Hiromasa Goto, and Takuma Matsuda. 2021. "The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics" Sustainability 13, no. 2: 987. https://doi.org/10.3390/su13020987

APA StyleTran, T., Goto, H., & Matsuda, T. (2021). The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics. Sustainability, 13(2), 987. https://doi.org/10.3390/su13020987