1. Introduction

Seed is an essential input for food production and vitally important to all of us. In our western society the exchange of seed, like many goods and services, is governed by the rules of the free market, even if this view is not universally shared or liked around the world. This paper considers organic seed in the marketplace and the factors that are likely to impact on supply and demand.

Economic theory of free markets assumes that the balance between supply and demand is regulated by price, and that this is the most efficient way to allocate scarce resources. In an ideal market, increases in demand will lead to increases in price and this will stimulate more production, resulting in an improved supply. Fall in demand should result in a fall in price; and if fewer producers cover their production costs, they will no longer produce so that overall supply is reduced. David Bateman considering the Economics of organic in 1994 [

1] compared Adam Smith’s metaphor of the ‘invisible hand’ to a voting system, in which each consumer (or in this case organic farmer or grower) is given the opportunity to express her or his choices and preferences.

The ideal market is assumed to be competitive, i.e., large numbers of buyers and sellers compete freely based on access to perfect information. Many economists and policy makers believe that there should be as little intervention as possible from regulations in any market and intervention is only justified if market failure exists.

Organic agriculture in Europe is regulated by the European Organic Regulations (at present EC/834/2007 [

2] and related Implementing Legislation). This includes the requirement that organic producers should use seed multiplied under organic farming conditions, which is considered important for a fully organic cycle. In this article, in line with use in the regulation, seed multiplied under organic conditions is referred to as ‘organic seed’. However, there has been a chronic lack of organic seed on the market, both in terms of overall quantity and range of varieties available [

3]. Therefore, farmers can currently obtain authorisations (also called derogations) for the use of non-organic seed (i.e., untreated conventional seed) as an exception to the rule, if they can demonstrate that no organic seed is available for the required varieties or cultivars at national level. Databases of organic seed availability have been set up in the EU Member States.

A new Organic Regulation (EC/848/2018) [

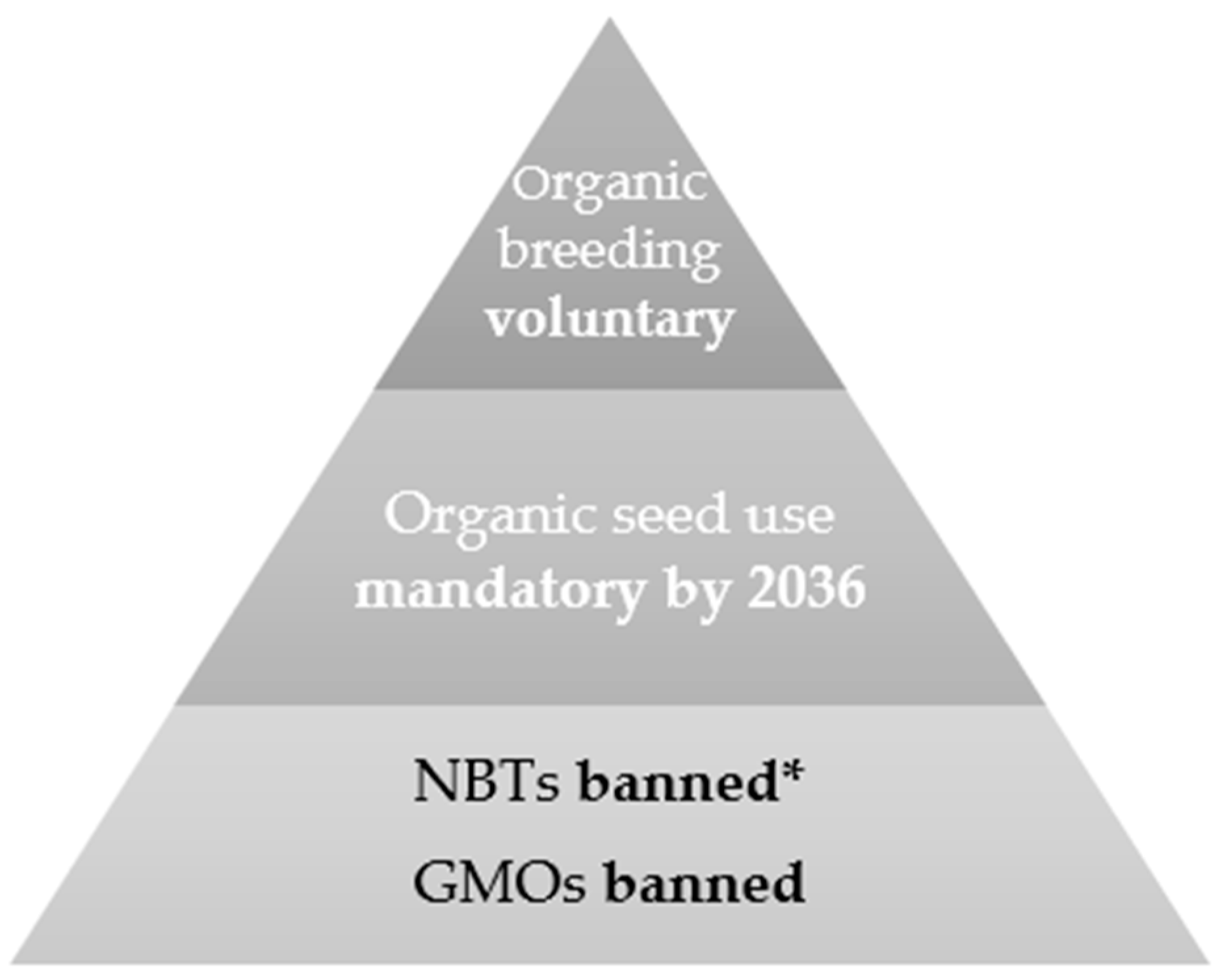

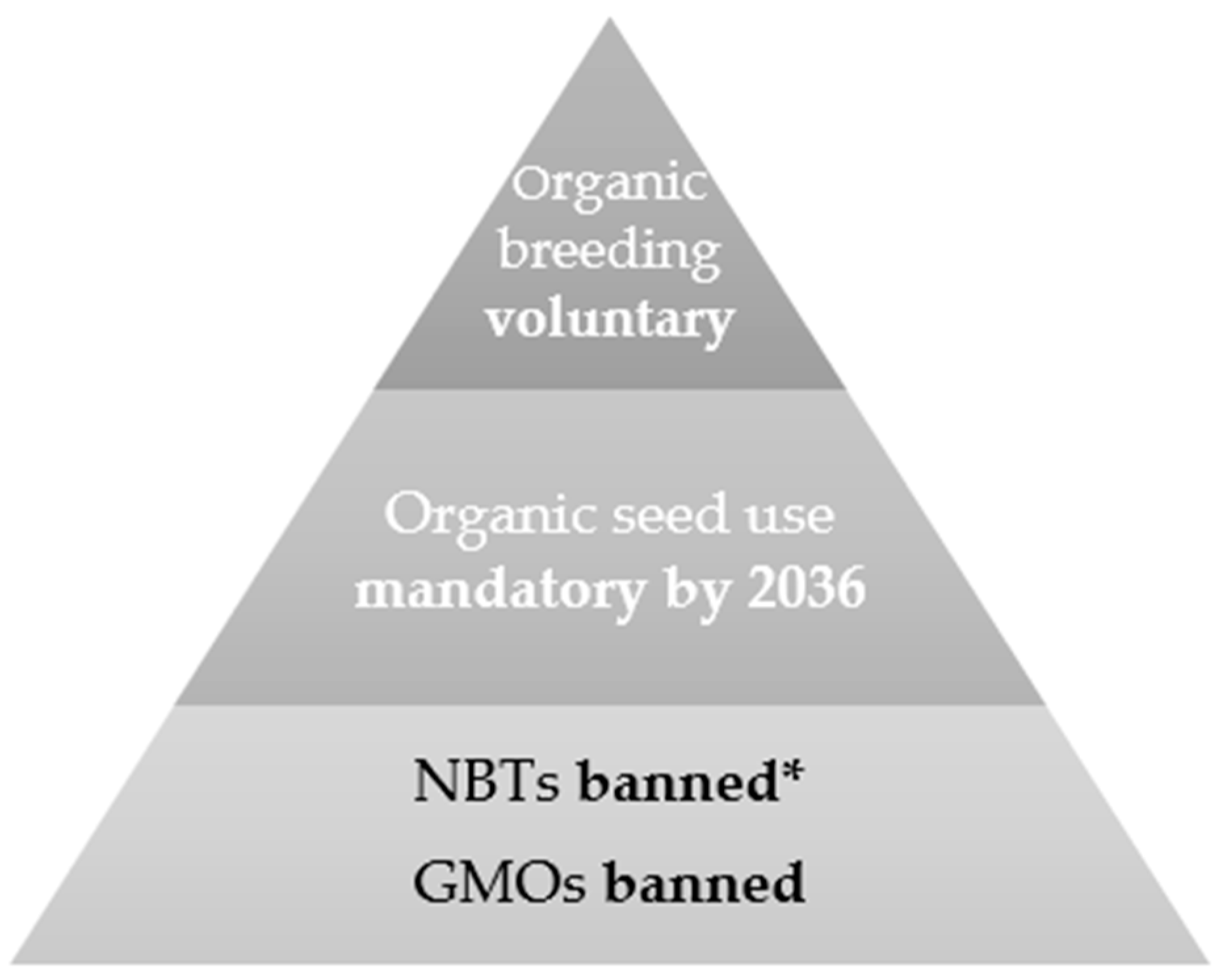

4] coming into force from 2022 envisages that all derogations to use non-organic seed will be phased out by 2036. By then the requirement will be to use only organic seed and vegetative propagation material. This applies to all the crops that are grown in organic, even the minor ones. In contrast, the use of varieties specifically bred under organic farming conditions or adapted to organic farming practices is not required by the regulations [

5] (see

Figure 1). The availability and use of such varieties and cultivars remain limited but no accurate data are available. The organic seed market is also impacted by the regulations for certified seed that requires producers to choose registered varieties and certified suppliers for many crops. The use of any Genetically Modified Organisms (GMOs) is banned in organic farming.

This paper aims to answer the question of whether the assumptions of economic theory apply to the organic seed sector, i.e., whether the market can deliver 100% organic seed and sufficient organic varieties. After presenting the approach, it examines the regulatory environment, supply and demand and the availability of information; presents some points of discussion; and draws conclusions for further development of the organic seed market in Europe.

2. Materials and Methods

The material presented and discussed in this paper originates from three different research activities carried out within the European LIVESEED project.

2.1. Case Studies of Organic Seed Supply Chains

A case study approach [

8] was used to analyse seed supply chains of combinable arable crops (i.e., cereals and pulses), horticulture (i.e., vegetables and fruit) and forage crops (i.e., legumes and grasses) [

9]. Case studies made use of the value chain framework and included the mapping of key actors, from the crop breeder to the consumer of products grown with the specific seed. We conducted 68 interviews with staff of seed companies, breeders and with researchers. The analysis of the cases aimed to identify typical business models for organic seed supply chains and technical, regulatory and market challenges. We paid particular attention to what was common and different between the three sectors and between the different parts of Europe. In addition to the crop sectors in general, the analysis looked in more detail at specific crops, which are particularly important for the organic sector and land use in Europe, such as wheat, carrots and ryegrass [

9].

2.2. A Survey of Organic Farmers

An online survey with organic farmers in Europe was conducted to identify what affects the use of organic seed by farmers. Data were collected in 2018 and 2019 from 749 organic farmers in 20 countries in four regions in Europe: Centre (Austria, Belgium, France, Germany, Luxembourg, Netherlands, Switzerland); East (Bulgaria, Czechia, Hungary, Poland, Romania, Slovakia), North (Denmark, Estonia, Finland, Ireland, Latvia, Lithuania, Sweden, United Kingdom) and South (Croatia, Cyprus, Greece, Italy, Malta, Portugal, Slovenia, Spain). Further details on the survey approach, the questionnaire and sample characteristics are presented by Orsini et al. in 2020 [

10,

11].

2.3. Estimates of Organic Seed Supply and Demand

An integrated approach to identify supply and demand of organic seed in Member States and Switzerland was developed and tested within the project (for more details see Solfanelli et al., 2020 [

12]). The total demand was estimated for selected crops combining 2016 data on the organic land area (from annual survey of FiBL/AMI) [

13]) with estimated typical seed rates for each crop in organic production (obtained through a literature review and validated by an expert survey). The share of organic seed, non-organic (i.e., untreated conventional) seed and farm-saved seed used by organic farmers was estimated by combining demand data with the results of the organic farmer survey described above. As far as possible, these estimates were validated by further 37 interviews with experts in 18 EU countries in 2019.

3. Results

The commercial seed market in Europe is an important agricultural input market and a large share of supply is concentrated on very few players. The organic seed market is closely related to the seed market in general but is smaller (albeit difficult to estimate accurately in size) and less well researched. Many companies operate both in the organic and conventional sector but there are also a few specialist companies that only deal with organic seed and specific varieties for this sector.

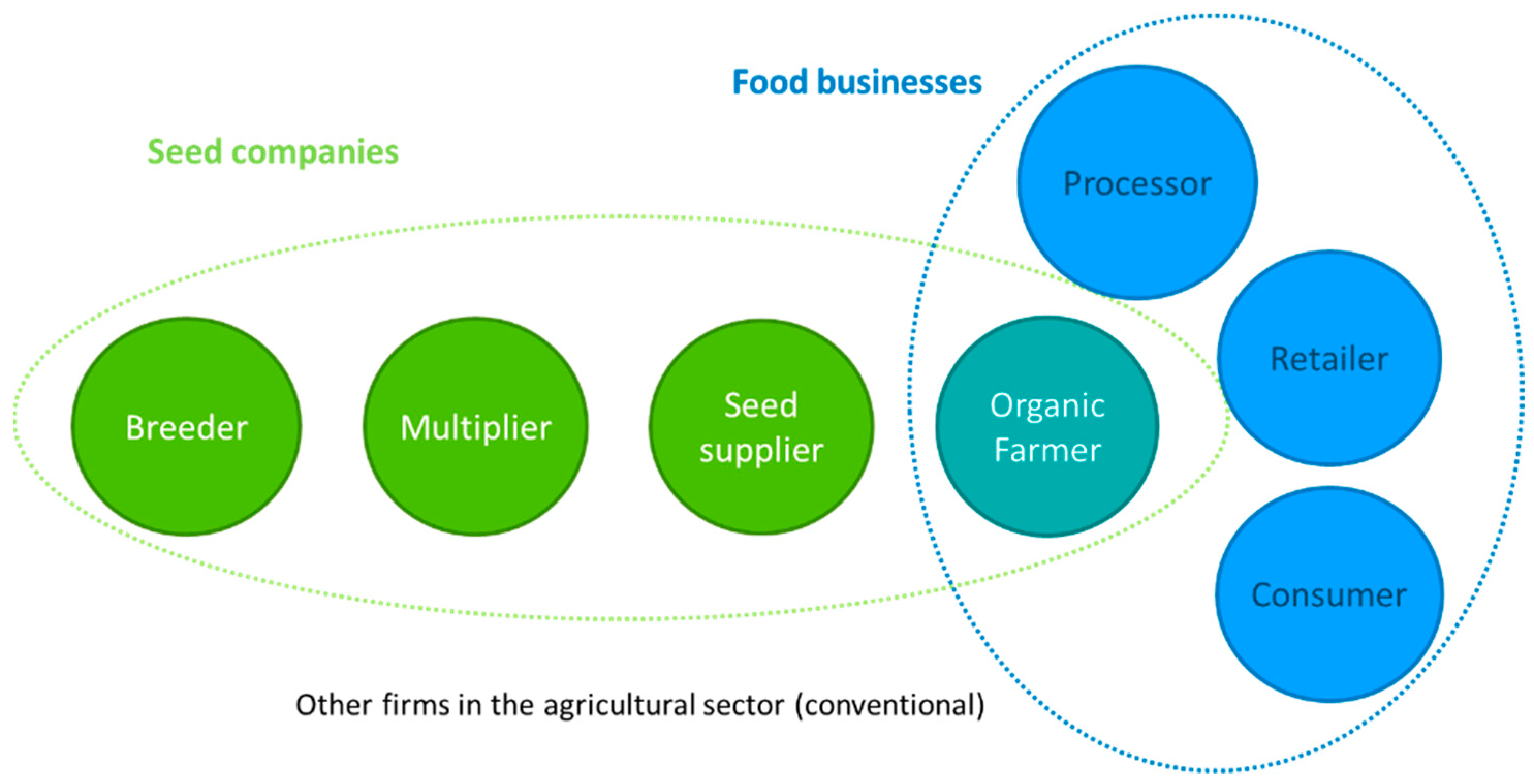

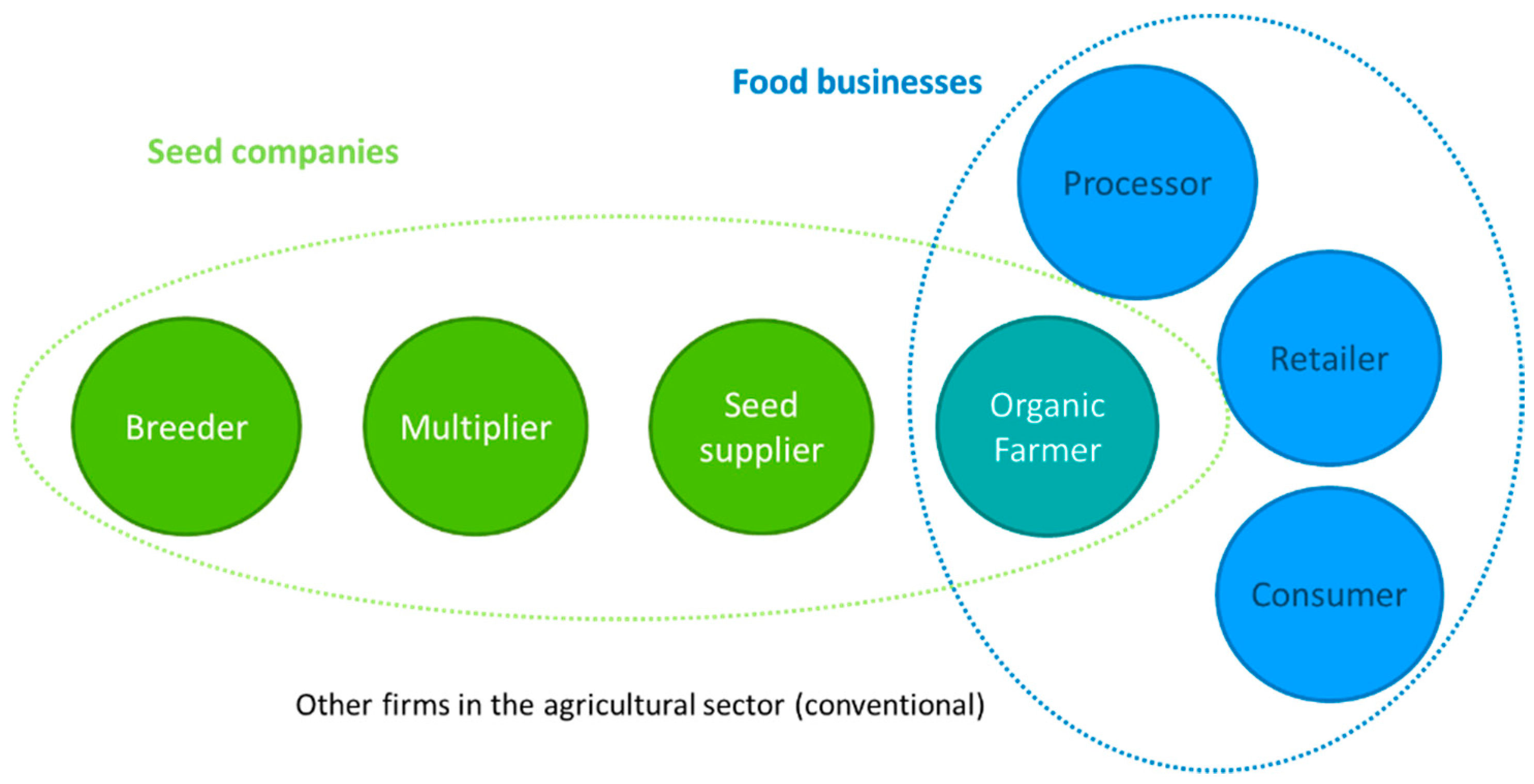

The case studies mapped actors in the organic seed supply chains in the three different sectors of arable, vegetables/fruit and forage crops (see

Figure 2). Stakeholders include breeders, seed multipliers and companies that supply seed to farmers, who can also be multipliers of organic seed. The producers in turn sell their products in the food market, which thus links consumers and food processors and retailers indirectly to the seed supply chain. Some differences between the sectors and European regions were observed which are outlined below.

3.1. Diversity of Crops Using Seed Grown in Europe

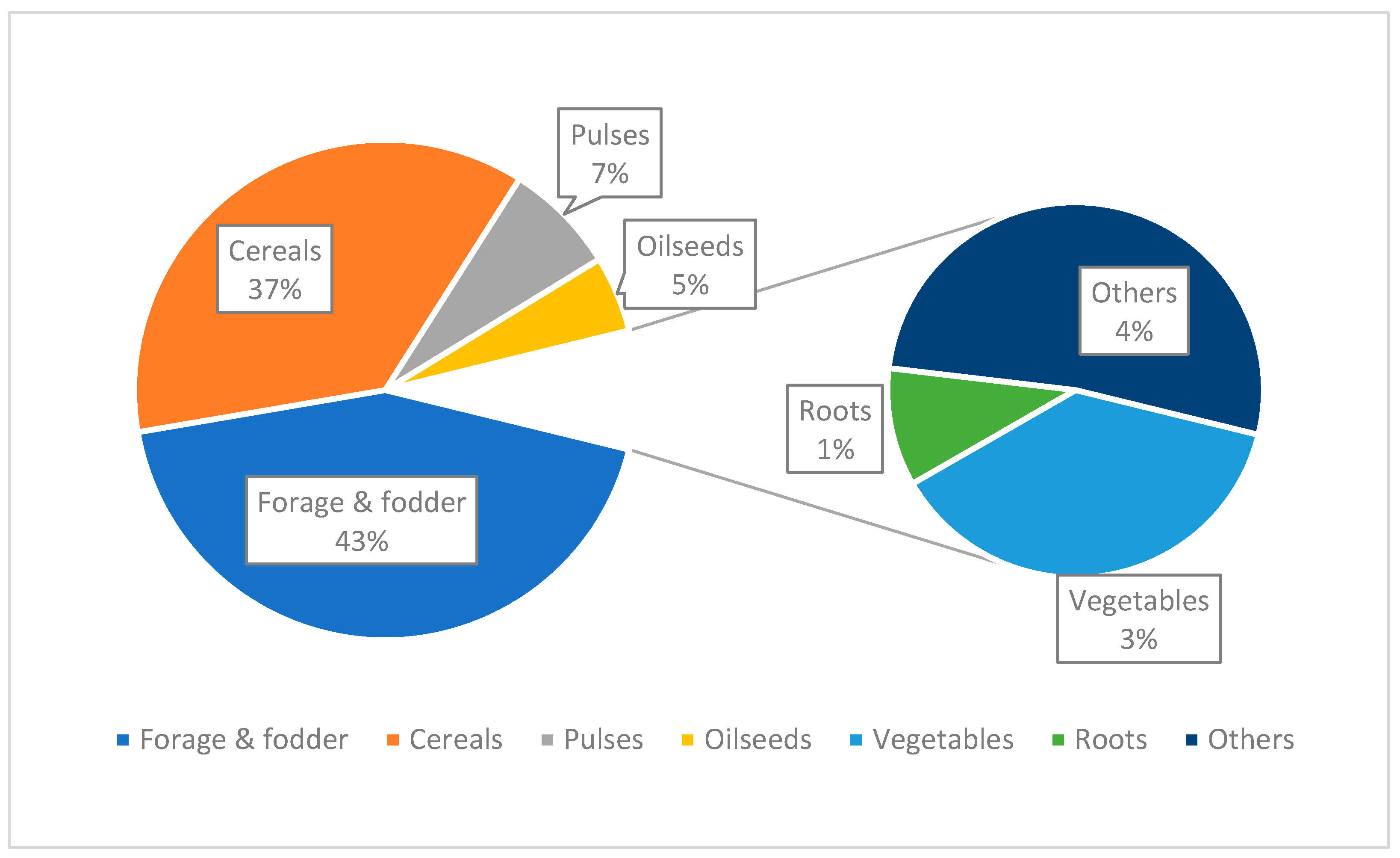

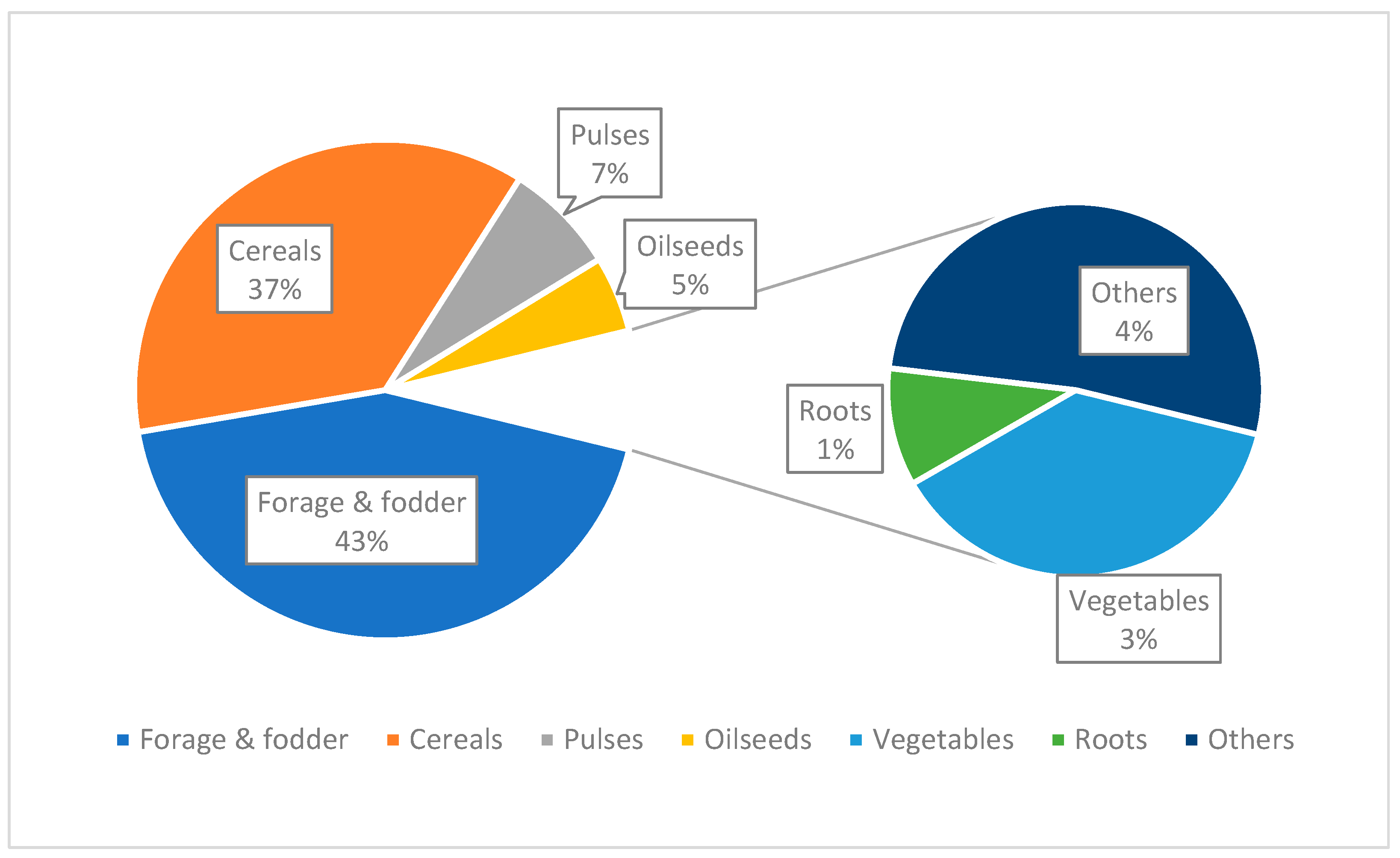

Combinable crops, horticulture and forage crops together represent a large proportion of organic arable land in the EU. Forage seed will also be used for reseeding permanent pastures and there is some seed use for some permanent crops, but this occurs much less regularly. We therefore focus here on organic arable land, which covered 6.5 million hectares in 2019 and corresponds to 45% of the total organic land in the EU (

Figure 3). Arable land nearly doubled between 2013 and 2019, with an increase of approximately 6% between 2018 and 2019. By country, the largest areas of organic arable cropping land are found in France (1.3 million ha), Italy (1 million ha) and Germany (0.7 million ha). In 2019, 2.5 million ha was used to grow forage and green fodder crops including temporary grasslands and other small-seeded legumes (e.g., clovers and lucerne). Cereals also represent an important cropping category (2.4 million ha in 2019) of which wheat is most widely grown; dry pulses account for 0.5 million ha [

13,

14].

3.2. The Regulatory Environment of the Organic Seed Market

The organic seed market is impacted by regulations governing organic food and farming as well as by general seed regulations. The organic regulations state that organic farmers have to use organic seed, but under certain circumstances derogations for the use of non-organic seed can be granted [

9]. Under the current organic regulations, Member States can develop their own lists of crops for which derogations are no longer possible (National Annexes or Category 1 lists) and Category 3 lists of crops for which a general derogation is granted. This was done in six EU Member States (Belgium, Netherlands, Luxembourg, France, Germany and Sweden) and in Switzerland.

A new organic regulation will enter into force in 2022 [

4]. This will phase out derogations for the use non-organic seed by organic farmers by 2036. Organic seed use will become mandatory and multiplication will need to be developed or scaled-up for many species (including some major and many minor species) to meet this demand (see also

Section 3.1). For many crops, not only the main species but also sub-species and crop type groups will need to be considered, e.g., carrots for processing and for the fresh market, cherry and salad tomatoes and tomatoes for processing. For all these crop types, many varieties and/or cultivars suited to the different soil and climatic conditions are likely to be grown by organic growers in different parts of Europe.

The organic seed market is also impacted by general seed legislation. The current regime has been criticised and evaluated as not being conducive to the management of crop genetic diversity [

15,

16], which is also of great importance to organic farming. This is illustrated by debates about agrobiodiversity, farmers’ rights to seed sovereignty and the privatisation of plant genetic resources [

17,

18]. Exemptions were established for the marketing of conservation and amateur varieties and Composite Cross Populations [

17]. A new Regulation on Plant Reproductive Material was planned, but after decades of struggle to reconcile the demands of the seed legislation with the rights of farmers to save and exchange seed and failure to secure the required support, the European Commission withdrew its legislative proposal in May 2015 [

17].

The new organic regulation 248/2018 clearly recognises the importance of genetic diversity for organic farmers and allows the use seed and plant reproductive materials for crops that can adapt to diverse local soil and climate conditions, are disease resistant and suit the specific cultivation practices of organic agriculture [

4]. Different strategies to increase diversity are mentioned, including the use of populations, seed mixtures and cultivars arising from heritage varieties and organic breeding and participatory on-farm breeding. The resulting seed will have a higher level of phenotypic and genotypic diversity but would not necessarily fulfil the current requirements for variety registration in terms of the DUS criteria (Distinctiveness, Uniformity and Stability). The new organic regulation also recognises the need to develop breeding programs to contribute to the development of the organic sector and permits the use of ‘heterogeneous material’ outside the current seed legislation [

4] although not explicitly stating the range of crops grown for which such breeding effort is needed. Breeding initiatives for organic crops that were considered in our case studies are mostly in their infancy and likely to be small, but accurate data on volumes traded are lacking. The recognition of the need for diversity in the new organic regulation illustrates a lack of alignment between the organic regulation and the general seed regulations.

3.3. Supply of Organic Seed in Europe

The supply of organic seed comes from about 800 larger and smaller seed businesses (breeders and traders), as well as farmers and growers that multiply organic seed crops. There are considerable differences in the level of availability of organic seed and in the supply chain organisation between arable, vegetable and forage crops. The following observations about trends in these three sectors are based on the status-quo analysis of the organic seed sector and case studies from the LIVESEED project [

9,

12].

3.3.1. Arable Crops

The most important combinable arable crops are soft wheat, durum wheat and pulses.

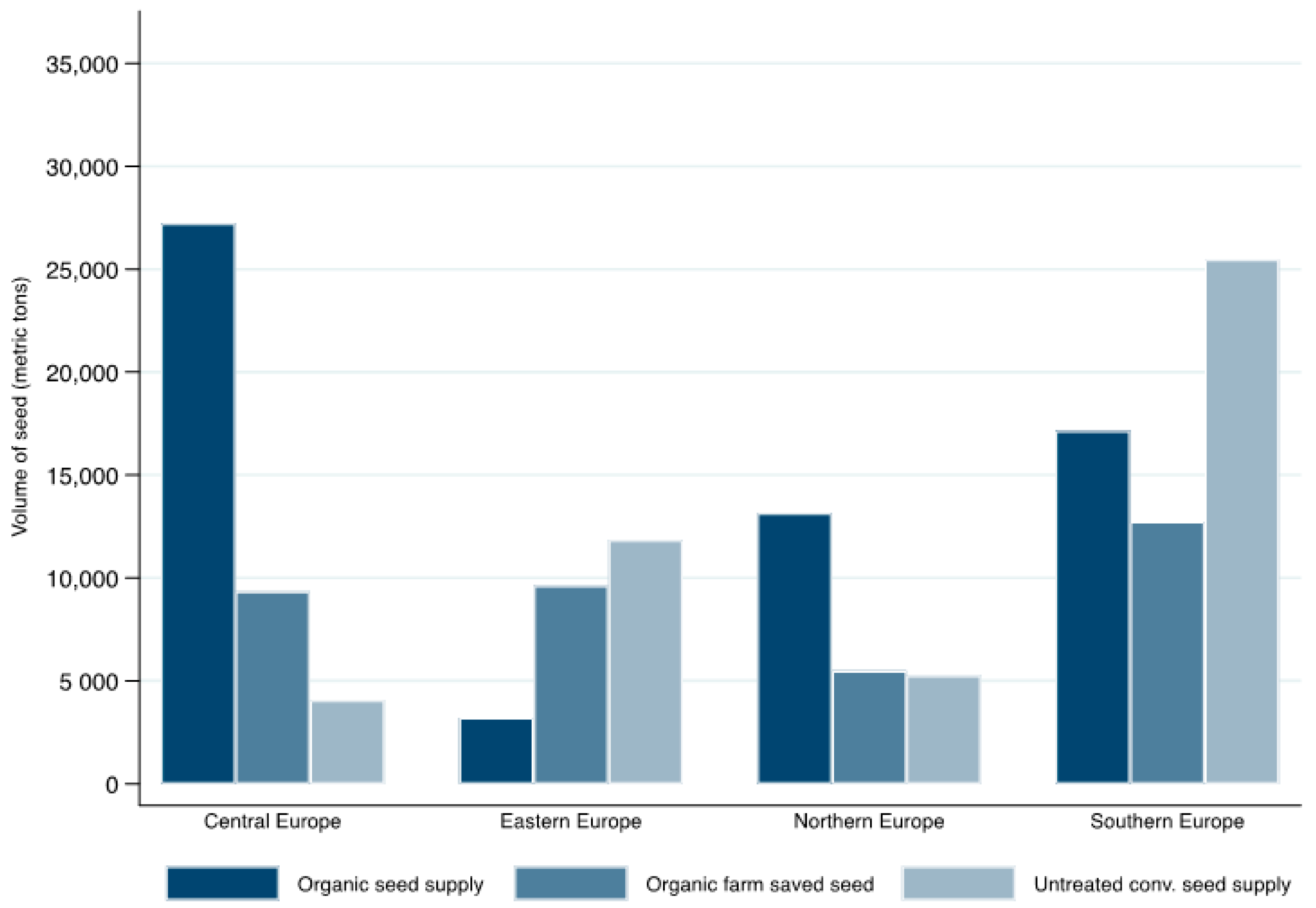

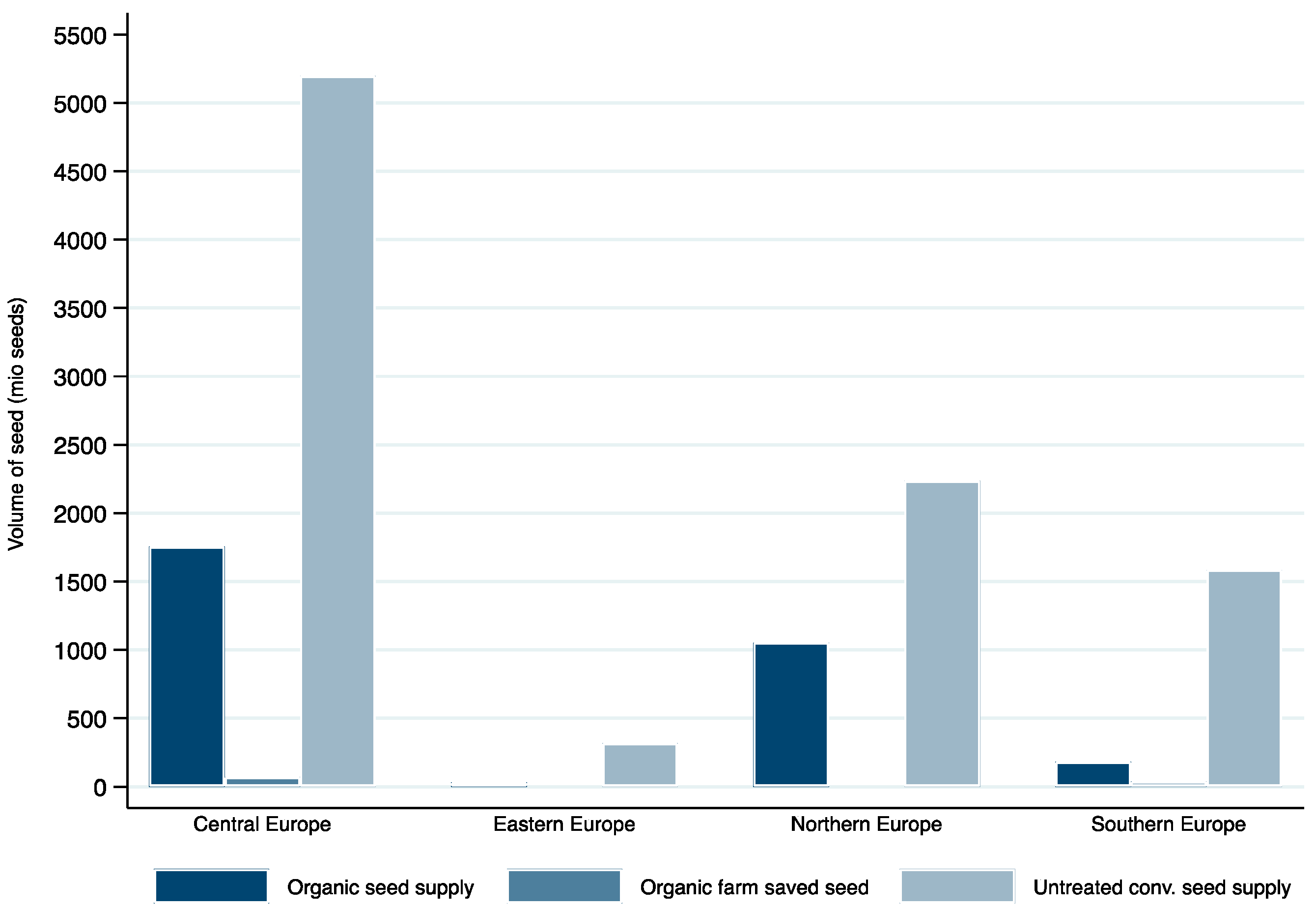

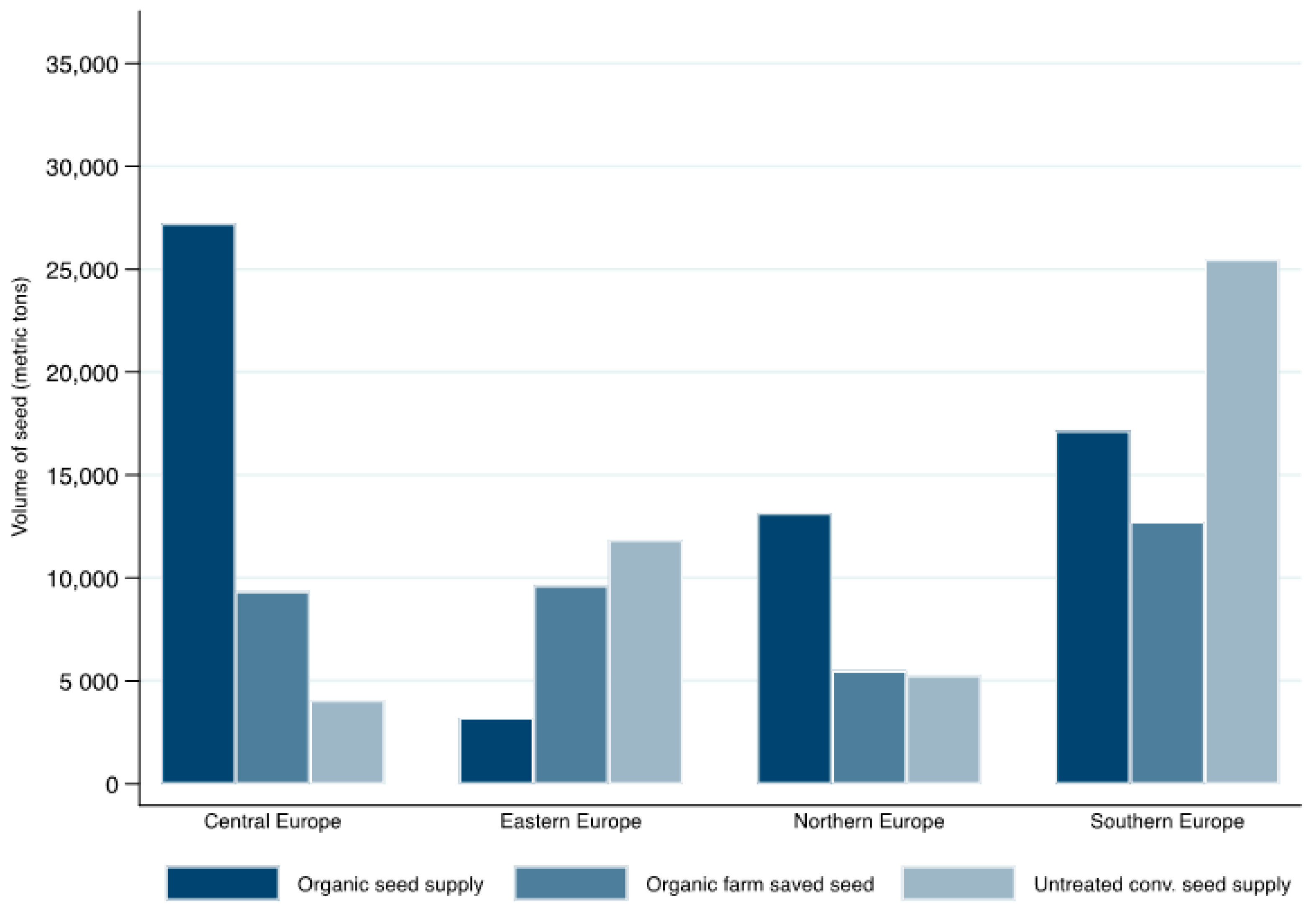

Figure 4 shows the estimated amount of wheat seed used in organic farming in EU countries and Switzerland in 2016 (see [

12] for details). The largest proportions of organic seed supply for this crop were registered in Central and Northern EU countries, with 67% and 55% respectively. In contrast, Southern and Eastern EU countries were characterised by the lowest organic seed supply, with 31% and 13% of the total potential demand respectively.

The companies operating in the organic arable seed sector are normally small to medium size businesses that produce organic seed and sell through merchants or directly to farmers. Vertical supply chain integration with breeders and seed traders is common, and seed production may be outsourced to farmers or farmers’ cooperatives. Supply of organic arable crop seed is concentrated in a few countries mainly in Central Europe, notably France, Germany, Austria, Italy and the Netherlands. Farmers in other countries have to buy imported organic seed. Smaller seed companies and farmers’ cooperatives with close connections to the organic sector tend to multiply only organic seed from both conventional and some organically bred varieties. Examples of medium-sized companies that also carry out some breeding of organic varieties were found in Denmark, Germany and Italy. Companies multiplying seed for organic farming mostly from conventionally bred varieties anticipate that this market will grow and expect it to become more profitable in future.

In addition to commercial breeding, we also identified several not-for-profit and community-based initiatives—the so-called informal seed sector—and some public breeding. All organic breeders we interviewed agreed on the need to develop specific breeding programs for organic durum and soft wheat. However, this is currently constrained by the small size of the market and thus low returns on investment in dedicated organic breeding programs, as well as by a lack of Value for Cultivation and Use (VCU) procedures for variety testing under organic conditions in most countries. Some conventional breeders are seeking to develop varieties suitable to both conventional and organic farming, which would allow access to a potentially larger market and higher return on investment.

3.3.2. Vegetable Crops

There are a considerable number of vegetable crops grown by organic growers, such as fresh beans, peas, carrots and onion grown from seed and brassicas, tomatoes and leeks grown from transplants, amongst many, many others. Carrots are characterised by a high share of the land area but also by a high number of derogation requests (+55% in the period from 2014 to 2016). From a technical point of view, organic carrot seed production is particularly challenging. Seven EU countries out of twelve with a national annex placed this crop in Category 3 [

19].

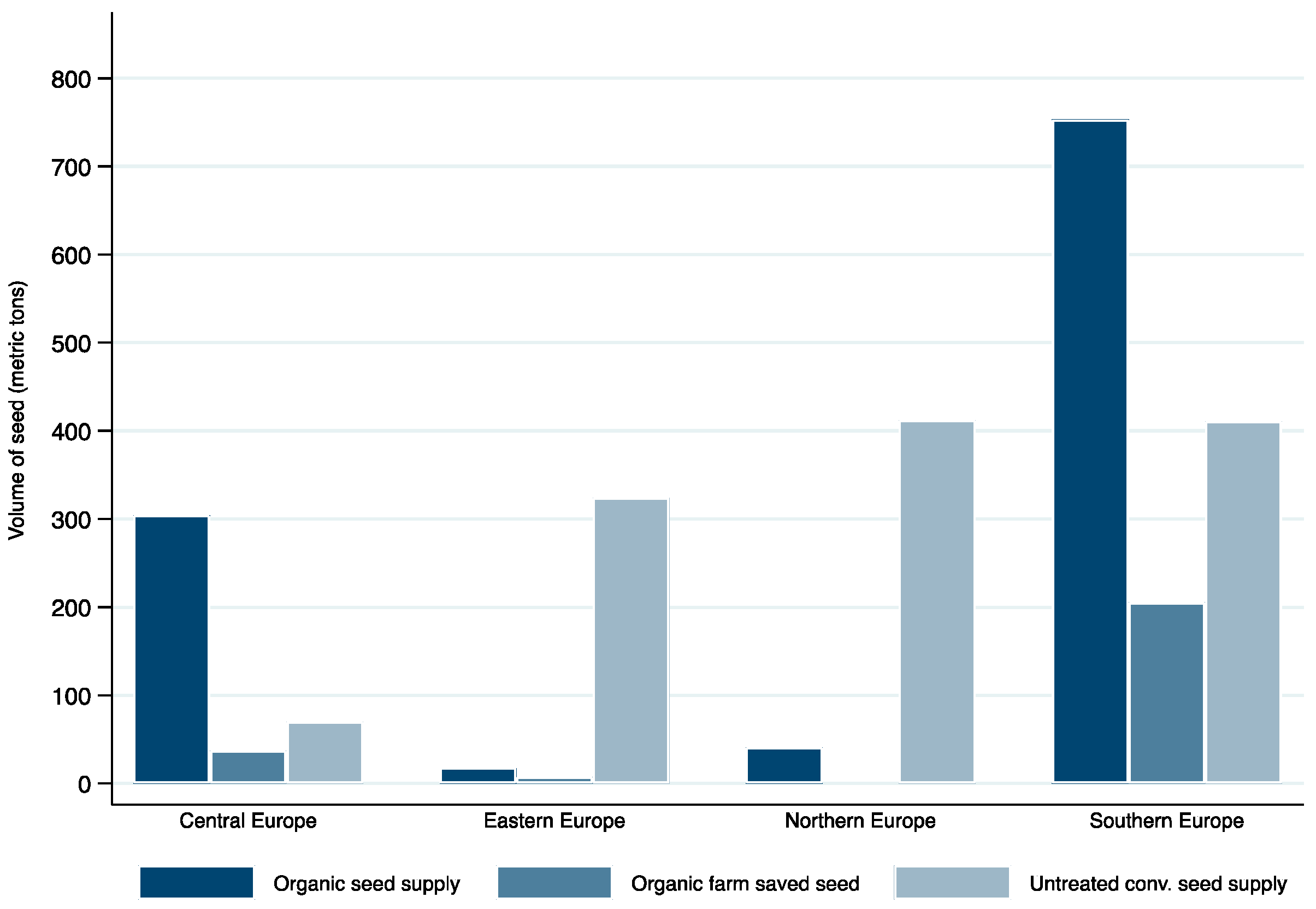

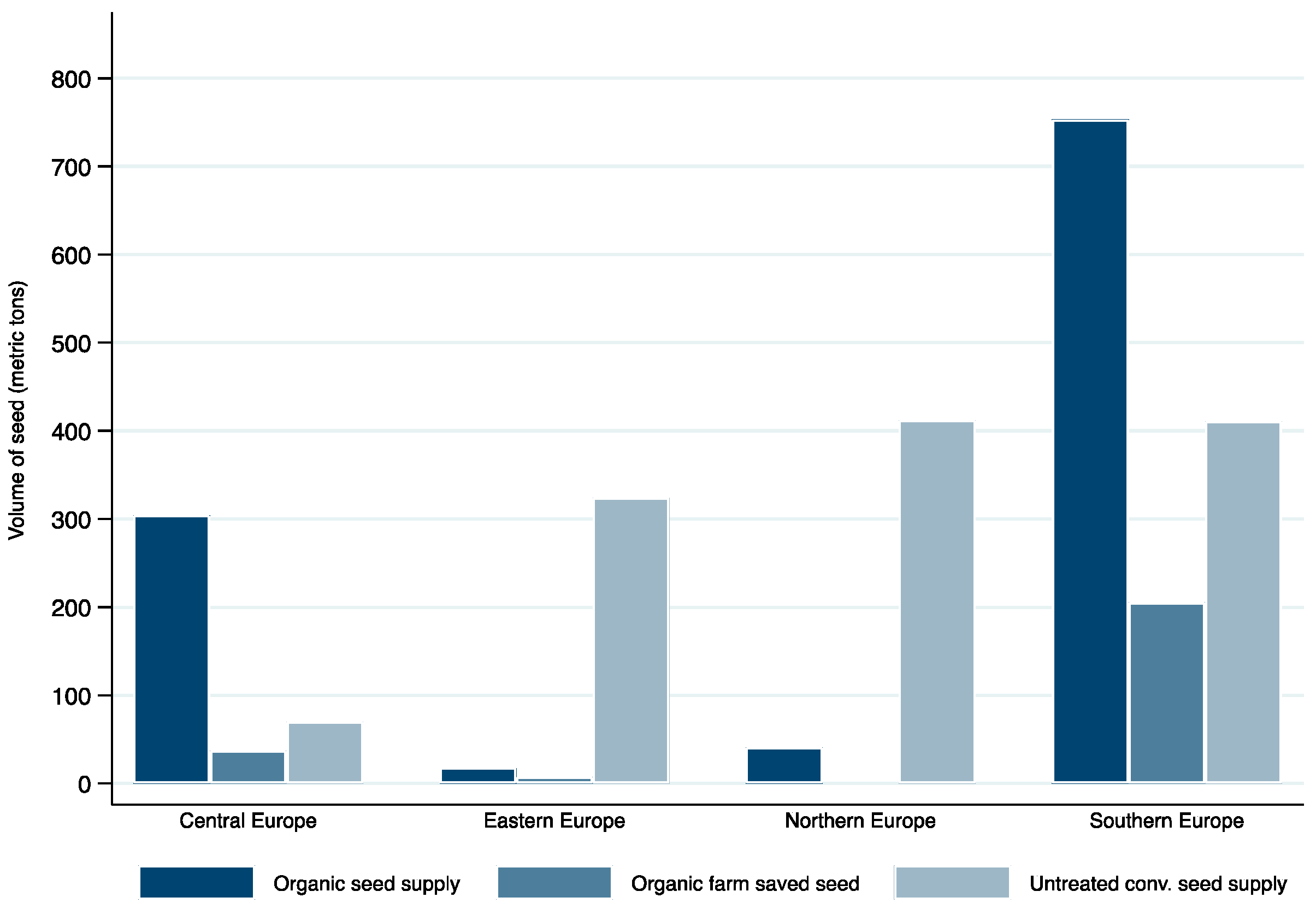

Figure 5 shows the estimated amount of carrot seed used in organic farming in the EU countries in 2016. The organic carrot seed supply is relatively low in all EU regions, with Eastern and Southern countries showing the highest use of non-organic seed: 91% and 88% respectively.

A strong integration between breeding and seed multiplication characterises the organic seed vegetable sector too, with several big companies producing seed from their own varieties/cultivars and breeding activities. This could be a result of many company mergers in this sector [

19]. Some very small organic companies mainly specialise in open pollinated varieties and community seed supplies. For vegetables that are grown from transplant (e.g., cauliflower), the transplant producers are often involved in choosing seed varieties [

20]. Supply of organic seed for vegetables and fruit is concentrated in Central Europe. The vegetable seed industry is very little developed in many Eastern and Southern European countries, such as Estonia, Bulgaria and Portugal [

9,

21].

Seed companies of the vegetable sector mainly invest in the breeding of crops that are expected to be profitable and concentration in vegetable breeding can be observed worldwide. These companies see no need for specific breeding focused on organic farming. In contrast, there are a number of mainly smaller organic companies and/or initiatives involving farmers that work with a wider range of crops and mostly with open pollinated varieties/cultivars for organic producers. Breeding activities exclusively for the organic sector by private companies have partly developed in response to the dominance of F1 hybrids and varieties bred with cell fusion in the conventional market. Breeding activities are also undertaken by public research institutes or private foundations receiving funding from stakeholders downstream in the supply chain.

Many interviewees supported public-private cooperation to improve the availability of cultivars adapted to organic growing. Some advocated a pre-financing model based on value-chain partnership as a promising approach for the development of organically bred varieties, both in the vegetable and arable sector. This financing model is currently only present in a very few countries and for a limited number of major crops. A weakness of such a model is that it is strongly reliant on the voluntary commitment of private actors like retailers, who decide to dedicate resources to organic breeding to differentiate their organic produce with private labels.

3.3.3. Forage Crops

Forage accounts for a substantial share of organic arable land, because of the need to include clover/grass mixtures as fertility building crops in organic rotations. The same species might also be used as green manures or catch crops. Some farmers grow very diverse mixtures (e.g., mixed herb leys) of many different species of grasses, clovers and herbs [

22]. It is often difficult for farmers and retailers to find organic seed of all the crop species and varieties needed in the mixtures.

Most forage seed multiplication is located in Central and Northern Europe. Lucerne (alfalfa) is the only exception and is mostly multiplied organically in Italy and France. Due to the sparse nature of the data, lucerne is the only forage crop for which estimates of the organic seed supply at EU level were provided. The estimated amount of organic seed supply for lucerne is 1.100 metric tons, which represents approximately one-third of the total potential demand in EU countries, though with differences between the regions [

12] (

Figure 6).

Some countries (e.g., Belgium, France, Germany, United Kingdom and Switzerland) consider the organic content in the seed mixture as a whole and have set a minimal percentage for the mixture (60 to 70% organic) whilst in others (e.g., Austria, Denmark, Italy and the Netherlands), the organic status of each component of the mixture is considered separately. The number of derogation requests tends to be higher in countries where farmers need to apply for derogations for each individual component. In this case, derogations are the only option whenever a particular component is not available organically. When farmers want to use a highly diverse mixture with less frequently grown species and varieties of clovers, grasses and herbs many derogation requests need to be made.

Among businesses involved with organic forage seed, interaction in the supply chain appears to be mainly between seed companies and farmers. This is in contrast to the other sectors where interaction with breeders and organic food businesses are normally observed. Breeding and seed multiplication are often carried out by different companies. Some larger companies undertaking seed production as well as breeding operate in North-Western Europe. Most companies trade with both conventional and organic forage seed and crop mixtures. Many forage seed companies that were interviewed reported growth attributed to market opportunities as a consequence of the greening measures of the EU Common Agricultural Policies (CAP), as well as the growth of organic land area in some countries.

Breeding for organic farming conditions for forage is far less developed than for arable crops and vegetables. We identified one breeding program for ryegrass and clover that works in a public-private partnership, which remains also an important financing model for conventional breeding of forage plants.

3.4. Demand

The demand side is represented by 430,794 organic producers [

14] of whom some but not all will buy organic seed: those who save their own or exchange seed do not participate in the market. The organic land area for arable crops, vegetables and forage crops has increased in the past decade, which has caused an increase in demand for organic seed [

12]. The use of untreated conventional seed under derogation is still common for most crops and in all European regions [

9,

23].

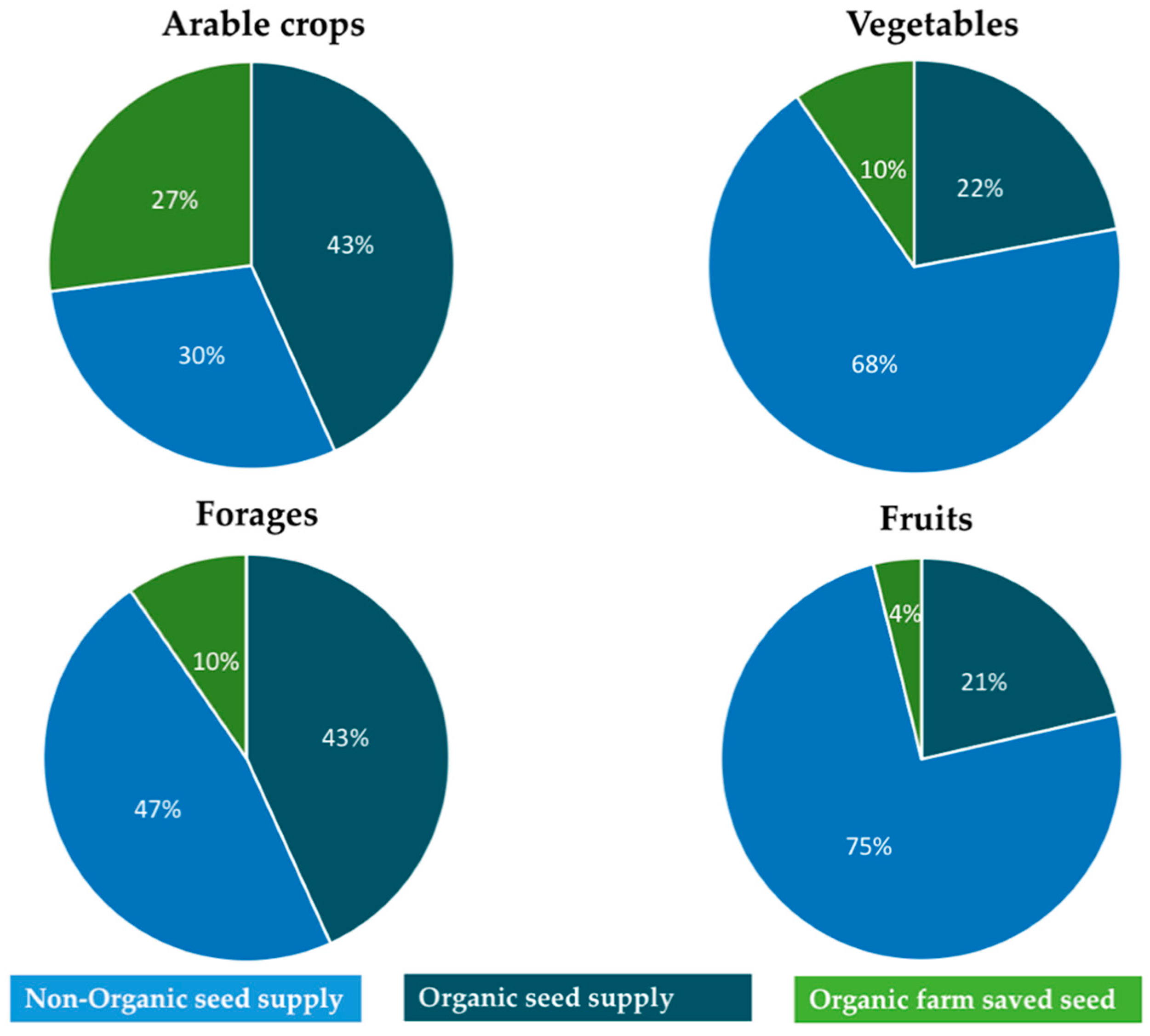

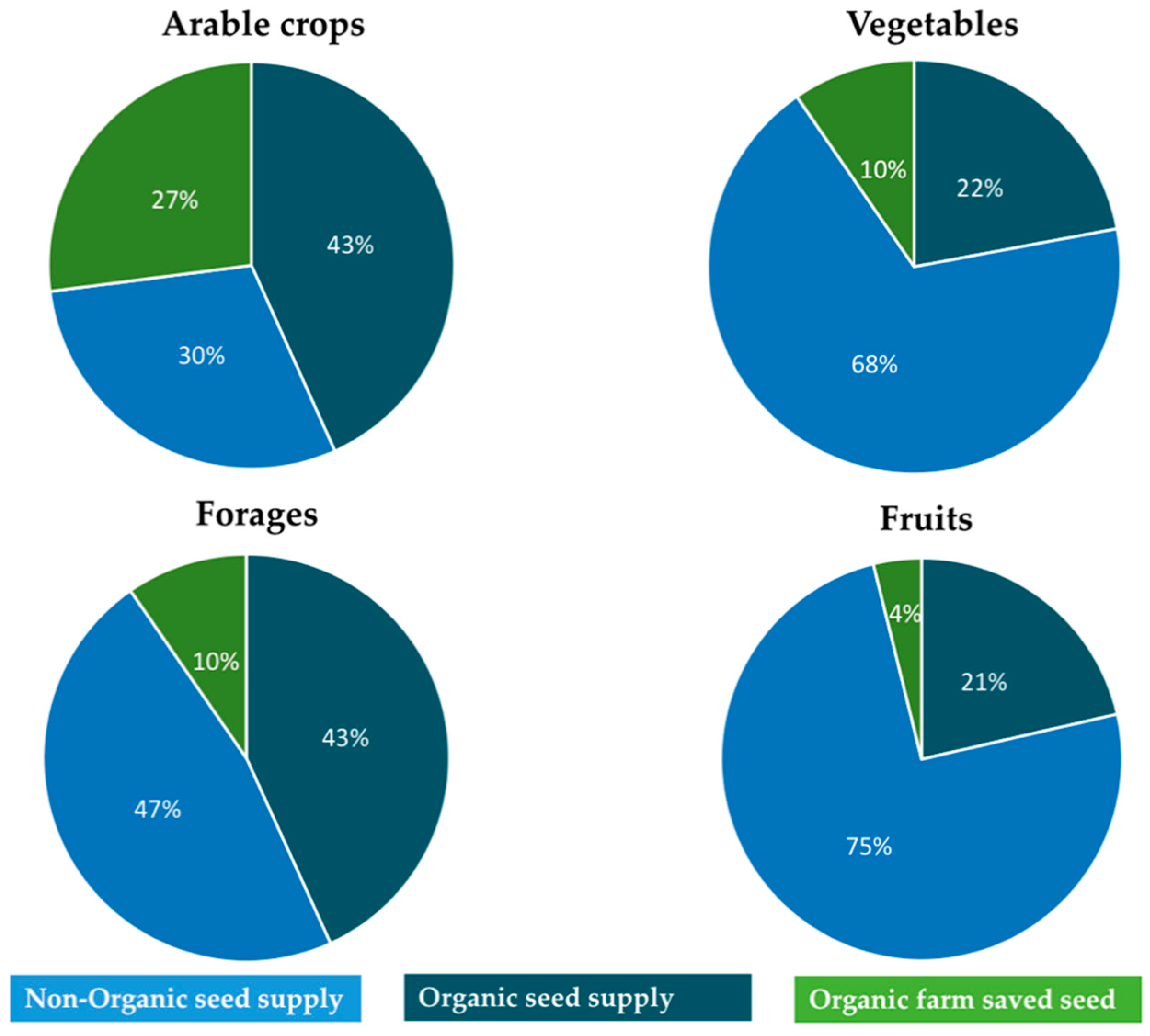

Figure 7 shows the estimated percentage of the different types of seed used by organic farmers in all EU Member States and Switzerland in 2016. The largest share of organic seed supply was found for arable and forage crops with 43% of the total potential demand. Vegetables and fruits had the highest use of non-organic seed with 68% and 75% respectively.

Although using organic seed has cost implications for farmers, the results of the LIVESEED farmer survey imply that this does not appear to be the main barrier. The farmers indicated a positive attitude towards organic seed use. When asked about what actions would increase the likelihood of more organic seed use in future, they referred to the availability of locally adapted varieties and the need for more investments in breeding for organic farming rather than a shortage of organic seed due to limited seed multiplication. Another important result of the survey is that ‘social norm’ is a major factor in organic farmers’ use of organic seed. It is possible that once organic seed use has diffused to the majority of farmers, further uptake would be accelerated [

10,

11].

Organic consumers interact only indirectly with the organic seed market through the products they choose. Their attitude to organic seed has not been studied in great detail. A Swedish study concluded that consumers are aware of heritage cereals, with bread and pasta regarded as the most popular future heritage cereals products; taste, flavour, freshness, texture, health aspects and origin emerged as relevant attributes [

24]. Consumers were also found to positively evaluate products of open source seed, regardless of whether they fully understand the concept or not [

25].

The idea behind the supply-chain-based pre-financing model for organic breeding that was advocated for organic vegetable crops and for other organic breeding by some of our interview partners is that consumers as well as traders can make a financial contribution to this sector. However, a general literature review of organic consumption behaviour from a marketing perspective concluded that although in studies consumers often claim to buy organic products because of altruistic motives that have a public utility (e.g., environmental protection), in practice, attributes representing an individual utility (e.g., health, taste and quality) are the main driving forces for organic food consumption. The empirical evidence for differences between committed and occasional organic consumers [

26] could imply that some organic consumers are willing to support breeding activities, whereas others are less likely to do so. Consumers might show higher willingness to pay for the use of varieties that have better nutritional qualities, or other attributes to which they directly relate, such as heritage cereals [

24] or landrace vegetables [

27]. However, a high price represents a well-known barrier to organic food consumption [

26] and any supply-chain financed breeding scheme would need to balance the need for additional funding with a potentially negative impact on product demand because of a higher price premium.

3.5. Access to Information

Regarding access to information, the organic seed market in Europe has many shortcomings. There is almost no information about the performance of varieties under organic conditions. Variety trials that would provide producers with such information exist for soft wheat (spring and winter) in 13 countries with well-established organic markets for soft wheat. Some trials for durum wheat have started in Italy and Greece and lupine is tested in Austria, Germany and Poland [

28]. This leaves organic producers of other cereals and of other crops having to rely on the information of seed suppliers without access to independent information.

Organic seed databases provide some information on availability of organic seed. Member States use databases of the organic seed and plant material that is available, which are also used by the control bodies to assess the availability when a farmer applies to be permitted to use non-organic seed. However, organic seed databases do not contain data on price and do not operate across the whole of Europe. There is also no public information about the trends and developments of organic and non-organic seed use for all crops grown in organic farming.

4. Discussion

Increasing the diversity from farm to fork is important in making our food systems more sustainable, promoting locally adapted farming systems, providing autonomy to farmers, supporting local short and fair supply chains and reconnecting farmers and consumers. Diversity of crops grown is also one of the principles of organic farming, for example expressed as a requirement for multi-annual crop rotations in the European Regulation. It is widely recognised that organic farming leads to improvements in biodiversity relating both to cultivated (i.e., crops grown) and wild biodiversity [

29]. Most European countries have in common that at present demand for organic seed is larger than supply for many crops or crop sectors, as indicated by the continued use of non-organic seed in Europe. The new growth target of 25% for organic land area in Europe set out in the Farm to Fork strategy [

30] is expected to lead to a further increase in demand for organic seed.

Supply of organic seed is mainly concentrated in Central Europe, in countries with better developed organic markets. The concentration of supply means that farmers elsewhere must either rely on imported organic seed, likely to be from varieties commonly grown in the exporting countries, use farm-saved seed, or continue to apply for derogations for the use of non-organic seed. The continued high use of derogations indicates that the current system has not facilitated the development of the organic seed sector, which was a central aim for its introduction. Nudge-based regulatory strategies may help with increasing organic seed demand; these have been shown to be working for other environmental-friendly practises [

31,

32]. However, if organic seed use becomes mandatory much more seed and reproductive material will need to be produced organically to realise the full potential of agrobiodiversity with and for organic farming. To produce enough organic seed for all the many crop species, sub-species, cultivars and varieties of grains, oilseeds, pulses, vegetables, fruits, grasses, clovers and herbs including those grown in mixtures represents is a considerable challenge for the organic seed sector.

Our survey has shown that organic farmers want varieties that perform well under organic conditions, and they consider the lack of availability of organic seed for a wider range of varieties to be a limiting factor in more organic seed use. Organic breeders and others in the sector are convinced about the need to develop specific organic breeding programs, partly also in response to a growing concentration in the seed sector, perceived as a threat to diversity by many. Our research has shown that there are clear differences with respect to the prevalence of organic breeding activities between the different crop sectors and the different regions of Europe. More variety testing under organic conditions would provide farmers with better information and could also help to generate more objective evidence that varieties bred for organic farming also perform well in organic fields. Some in the organic sector would like to see the organic regulation extended to cover organic breeding as well as seed multiplication. In our view, there is a danger that demanding that all varieties used by organic farmers must be organically bred could reduce the choice for farmers, leading in turn to potential conflicts with the crop diversification.

5. Conclusions

The answer to the question that the paper poses must be ‘no’, the market alone cannot deliver the 100% organic seed that the new Organic Regulation requires. The organic seed market cannot be categorised as a well-functioning competitive market. Demand is outstripping supply, but historically this has not led to investment in sufficient quantity to increase supply and thus reduce reliance on using non-organic seed under derogations. The market certainly cannot supply 100% organic varieties, with an organic breeding sector that is in its infancy and characterised by a shortage of funds.

The European Farm to Fork and Biodiversity strategies aim for much further growth of the organic land area with a target of 25% by 2030 [

30,

33]. This will lead to further increases in demand for organic seed and potential shortages of supply. Given the current poor functioning of the organic seed market as well as technical problems in many sectors, policy intervention is justified but instruments need to be chosen with care. Nudging farmers to use more organic seed may help in securing a more stable demand, though bottlenecks in supply need to be solved, too. Better information about the organic seed market might lead to a greater willingness to invest, but the planned tightening of the organic regulation in terms of reducing derogations to use non-organic seed could have unintended consequences, including a reduction in the ability of organic farms to make use of and deliver high agrobiodiversity.

A stepwise approach to phase out derogations needs to be adopted, i.e., one that allows time to plan the increase in organic seed production by seed companies, as well as time for the usage of organic seed to catch on with an increasing number of organic farmers. The phasing out also needs to be accompanied by measures to avoid seed shortages and make the organic seed sector competitive. There is a clear need for investment in research to overcome technical difficulties related to seed multiplication under organic conditions and the use of public funds for breeding activities suitable for organic agriculture also appears fully justified. Organic agriculture has an important role to play in moving governmental support for agriculture and food systems towards systems that deliver on the Sustainable Development Goals (in line with ‘public funds for public goods’), even if powerful vested interests command ever greater market power [

34].

After all,

‘seed is not only a tradeable commodity. ‘Seed is not just the source of life, it is the very foundation of our being. For millions of years seed has evolved freely to give us the diversity and richness of life on the planet. Without the freedom to save, protect and share renewable seeds we will have neither bread nor freedom’ Vandana Shiva in [

35] (p. 438).

Author Contributions

Conceptualisation, S.P.; methodology, S.P., S.O., F.S.; investigation, F.S., S.O.; writing—original draft preparation, all authors; writing—review and editing, all authors; funding acquisition, S.P., R.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the European Commission Horizon 2020 Research and Innovation programme through the project LIVESEED, under Grant Agreement No 727230, and by the Swiss State Secretariat for Education, Research and Innovation under contract number 17.00090.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Acknowledgments

We acknowledge support of the experts in seed supply chains that were interviewed, of other colleagues in the LIVESEED project and for proofreading.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Bateman, D.I. Organic farming and society: An economic perspective. In The Economics of Organic Farming; Lampkin, N.H., Padel, S., Eds.; CAB International: Wallingford, UK, 1994; pp. 45–65. [Google Scholar]

- Council of the EU. Council Regulation (EC) No 834/2007 of 28 June 2007 on Organic Production and Labelling of Organic Products and Repealing Regulation (EEC) No 2092/91. Off. J. Eur. Union 2007, 8, 139–161. [Google Scholar]

- Solfanelli, F.; Ozturk, E.; Zanoli, R.; Orsini, S.; Petitti, M.; Ortolani, L.; Schäfer, F.; Messmer, M. The State of Organic Seed in Europe; LIVESEED booklet; IFOAM organics Europe: Bruxelles, Belgium, 2021; Available online: https://www.liveseed.eu/wp-content/uploads/2019/12/FNL-FNL-Web-Interactive-NOV19-Booklet2-LIVESEED_web.pdf (accessed on 15 January 2021).

- EC. Regulation (EU) 2018/848 of the European Parliament and of the Council of 30 May 2018 on Organic Production and Labelling of Organic Products and Repealing Council Regulation (EC) No 834/2007. Off. J. Eur. Union 2018, L150, 1–92. [Google Scholar]

- Van Lammerts Bueren, E.T.; Myers, J.R. (Eds.) Organic Crop Breeding; Wiley-Blackwell: Oxford, UK, 2012; ISBN 9781119945932. [Google Scholar]

- Lombardo, L.; Zelasco, S. Biotech Approaches to Overcome the Limitations of Using Transgenic Plants in Organic Farming. Sustainability 2016, 8, 497. [Google Scholar] [CrossRef] [Green Version]

- Husaini, A.M.; Sohail, M. Time to Redefine Organic Agriculture: Can’t GM Crops Be Certified as Organics? Front. Plant Sci. 2018, 9, 423. [Google Scholar] [CrossRef] [PubMed]

- Yin, R.K. Case Study Research: Design and Methods, 5th ed.; Sage Publications: London, UK, 2014. [Google Scholar]

- Orsini, S.; Solfanelli, F.; Winter, E.; Padel, S.; Ozturk, E. Report Describing Three Crop Case Studies Investigating in Detail the Socio-Economic Factors Influencing the Behaviour of Various Stakeholders Regarding the Use of Organic Seed; LIVESEED Project Report; Organic Research Centre: Newbury, UK, 2019. [Google Scholar]

- Orsini, S.; Costanzo, A.; Solfanelli, F.; Zanoli, R.; Padel, S.; Messmer, M.; Winter, E.; Schäfer, F. Factors affecting the use of organic seed by organic farmers in Europe. Sustainability 2020, 12, 8540. [Google Scholar] [CrossRef]

- Orsini, S.; Padel, S.; Solfanelli, F.; Costanzo, A.; Zanoli, R. Report on Relative Importance of Factors Encouraging or Discouraging Farmers to Use Organic Seed in Organic Supply Chains; LIVESEED Project Report; Organic Research Centre: Newbury, UK, 2020. [Google Scholar]

- Solfanelli, F.; Ozturk, E.; Orsini, S.; Schäfer, F.; Messmer, M.; Zanoli, R. The EU Organic Seed Sector—Statistics on Organic Seed Supply and Demand; Working paper of the LIVESEED Project; Università Politecnica delle Marche—D3A: Ancona, Italy, 2020; Available online: https://orgprints.org/38616 (accessed on 10 June 2021).

- FiBL Statistics. Available online: https://statistics.fibl.org/europe.html (accessed on 10 June 2021).

- Willer, H.; Travnicek, J.; Meier, C.; Schlatter, B. (Eds.) The World of Organic Agriculture, Statistics and Emerging Trends 2021; IFOAM; FiBL: Frick, Switzerland, 2021. [Google Scholar]

- Winge, T. Seed Legislation in Europe and Crop Genetic Diversity. In Sustainable Agriculture Reviews; Lichtfouse, E., Ed.; Springer: Cham, Switzerland, 2015; Volume 15, pp. 1–64. ISBN 978-3-319-09131-0. [Google Scholar]

- Prip, C.; Fauchald, O.K. Securing Crop Genetic Diversity: Reconciling EU Seed Legislation and Biodiversity Treaties. Rev. Eur. Comp. Int. Environ. Law 2016, 25, 363–377. [Google Scholar] [CrossRef]

- Fehér, J.; Padel, S.; Rossi, A.; Drexler, D.; Oehen, B. Diversified Food System: Policy to Embed Crop Genetic Diversity in Food Value Chains; Diversifood Booklet No. 5. 2019. Available online: http://www.diversifood.eu/wp-content/uploads/2017/09/Booklet5Diversifood_WEB.pdf (accessed on 15 January 2021).

- Kotschi, J.; Wirz, J. Who Pays for Seeds? Thoughts on Financing Organic Plant Breeding. 2015. Available online: https://www.opensourceseeds.org/sites/default/files/downloads/Who_pays_for_seeds.pdf (accessed on 31 December 2020).

- Van Elsen, A.; Gotor, A.A.; di Vicente, C.; Traon, D.; Genatas, J.; Negri, V.; Amat, L.; Chable, V. Plant Breeding for an EU Bio-based Economy: The Potential of Public Sector and Public/Private Partnerships; Publications Office of the European Union: Luxembourg, 2013. [Google Scholar]

- Raaijmakers, M.; Schäfer, F. Report on Political Obstacles and Bottlenecks on the Implementation of the Rules for Organic Seed in the Organic Regulation: LIVESEED Project Report; Bionext: Ede, The Netherlands, 2019. [Google Scholar]

- Renaud, E.N.; van Bueren, E.T.L.; Jiggins, J. The meta-governance of organic seed regulation in the USA, European Union and Mexico. Int. J. Agric. Resour. Gov. Ecol. 2016, 12, 262. [Google Scholar] [CrossRef]

- Rosenfeld, A.; Rayns, F. Sort Out Your Soil, 2nd ed., Undated. Available online: https://www.cotswoldseeds.com/downloads/sort%20out%20your%20soil%202%20website.pdf (accessed on 8 June 2021).

- Willer, H.; Schlatter, B.; Travnicek, J.; Kemper, L.; Lernoud, J. (Eds.) The World of Organic Agriculture, Statistics and Emerging Trends 2020; IFOAM; FiBL: Frick, Switzerland, 2020. [Google Scholar]

- Wendin, K.; Mustafa, A.; Ortman, T.; Gerhardt, K. Consumer Awareness, Attitudes and Preferences Towards Heritage Cereals. Foods 2020, 9, 742. [Google Scholar] [CrossRef] [PubMed]

- Kliem, L.; Wolter, H.; Sivers-Glotzbach, S. Consumer Perceptions and Evaluation of the Open Source Seeds License. In Proceedings of the EUCARPIA Conference on Breeding and Seed Sector Innovations for Organic Food Systems, Cēsis, Latvia, 8–10 March 2021. [Google Scholar]

- Hemmerling, S.; Hamm, U.; Spiller, A. Consumption behaviour regarding organic food from a marketing perspective—a literature review. Org. Agr. 2015, 5, 277–313. [Google Scholar] [CrossRef]

- Missio, J.C.; Rivera, A.; Figàs, M.R.; Casanova, C.; Camí, B.; Soler, S.; Simó, J. A Comparison of Landraces vs. Modern Varieties of Lettuce in Organic Farming During the Winter in the Mediterranean Area: An Approach Considering the Viewpoints of Breeders, Consumers, and Farmers. Front. Plant Sci. 2018, 9, 1491. [Google Scholar] [CrossRef] [PubMed]

- Kovács, T.; Pedersen, M.T. Overview on the Current Organizational Models for Cultivar Testing for Organic Agriculture over Some EU Countries; LIVESEED Project Report: Bruxelles, Belgium, 2019. [Google Scholar]

- Sanders, J.; Heß, J. Leistungen des Ökologischen Landbaus für Umwelt und Gesellschaft; Thünen-Report No. 65; Thünen-Institut: Braunschweig, Germany, 2019. [Google Scholar]

- EC. A Farm to Fork Strategy for a Fair, Healthy and Environmentally-Friendly Food System: Brussels, 20.5.2020 COM(2020) 381 Final, Brussels. 2020. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:ea0f9f73-9ab2-11ea-9d2d-01aa75ed71a1.0001.02/DOC_1&format=PDF (accessed on 18 June 2021).

- Kuhfuss, L.; Préget, R.; Thoyer, S.; Hanley, N. Nudging farmers to enrol land into agri-environmental schemes: The role of a collective bonus. Eur. Rev. Agric. Econ. 2016, 43, 609–636. [Google Scholar] [CrossRef]

- Peth, D.; Mußhoff, O.; Funke, K.; Hirschauer, N. Nudging Farmers to Comply With Water Protection Rules—Experimental Evidence From Germany. Ecol. Econ. 2018, 152, 310–321. [Google Scholar] [CrossRef] [Green Version]

- EC. EU Biodiversity Strategy for 2030: Bringing Nature back into Our Lives. Communication from the Commission the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. COM(2020) 380 Final; European Commission: Brussels, Switzerland, 2020. [Google Scholar]

- Eyhorn, F.; Muller, A.; Reganold, J.P.; Frison, E.; Herren, H.R.; Luttikholt, L.; Mueller, A.; Sanders, J.; Scialabba, N.E.-H.; Seufert, V.; et al. Sustainability in global agriculture driven by organic farming. Nat. Sustain. 2019, 2, 253–255. [Google Scholar] [CrossRef] [Green Version]

- Capra, F.; Luisi, P.L. The Systems View of Life: A Unifying Vision/Fritjof Capra, Pier Luigi Luisi; Cambridge University Press: Cambridge, UK, 2014; ISBN 978-1-107-01136-6. [Google Scholar]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}