1. Introduction

The Hungarian Information and Communication Technology (ICT) sector plays an essential role in the economy and support Industry 4.0. The ICT sector contributed five percent of the total Gross Domestic Product (GDP) in the last three years. The sector also supports other sectors, such as the manufacturing sector, which had the highest GDP contribution, with a value of 22% [

1]. Furthermore, the innovative applications of the ICT industry ease the tasks of other industries, such as wholesale trade, government services, commercial property, and logistics, when undertaking e-commerce.

About 1800 ICT firms [

2] provide communication technologies that enable users to access, store, retrieve, and manipulate information in digital forms [

3,

4]. They recruited about 60,000 staff in 2018, and this increased by about 30% in 2020 [

5]. They obtained revenues of about 7 million Euros in 2018, and this amount grew by approximately 45% in 2019. In general, the profits of ICT companies have tended to increase over the last three years. The increasing returns continue climbing, followed by the challenges of achieving and retaining significant revenues. The promising profit has attracted ICT firms to compete with others in a competitive market [

6]. As a result, approximately 10% of ICT firms have shut down two years ago [

5].

ICT firms clash with their competitors, and encounter challenges in a disruptive era, which is illustrated by the fact that start-up firms disrupt the existing firms from the market because the newcomer corporates offer innovative products [

7,

8]. ICT firms should collaborate with their business partners to improve innovation toward the exchange of the inflows and outflows of communicated information between them [

9]. To enable the smooth inflows and outflows of shared information, ICT businesses require trust in their business partners. Innovation also increases potential market, which is connected to improve business performance [

10].

The correlation between trust and business performance continues to be a controversial area of investigation. Evidence from several cohort studies indicated a strong relationship between inter-organizational trust and business performance [

11,

12,

13,

14,

15]. Their results contrast with the findings of Oláh et al. [

16].

Therefore, this study proposed innovation as a moderating variable, improving the correlation between inter-organizational trust and financial performance. The relationship between trust in business partners and innovation is not clearly stated in the context of social capital [

17,

18]. In addition, some scholars obtained different findings. One group of researchers supported the idea that inter-organizational trust positively influenced innovation [

19,

20,

21,

22]. Another group claimed that there was no direct influence operating between trust in business partners and innovation [

23,

24].

Prior studies supported the idea that trust in business partners improved the combination and exchange of resources between collaborating parties, which influenced innovation [

25,

26]. Other studies proved that inter-organizational trust improved innovative processes, economies of scale, and sales [

27]. Innovation also developed product performance positively influencing financial performance [

28,

29]. Additionally, the company maintained an ideal level of trust that supported innovation [

30].

The study argues that the extent of trust in business partners improves financial performance [

11,

12,

13,

14,

15]. The research also claims that innovation strengthens the relationship between inter-organizational trust and financial performance [

19,

20,

21,

22]. Thus, the study raised three research questions:

RQ1: How does inter-organizational trust improve financial performance?

RQ2: How does inter-organizational trust enhance innovation?

RQ3: How does innovation improve financial performance?

Subsequently, the research proposed three hypotheses: firstly, inter-organizational trust has a positive effect on financial performance. Secondly, a higher level of inter-organizational trust positively affects innovation, and thirdly, innovation positively affects financial performance within different firm categories. The study had two objectives. The initial goal is to investigate the level of inter-organizational trust on financial performance and innovation. Later, the study observes the role of innovation in improving financial performance. The study also looked at a summary of the perspectives of social capital, trust, innovation, and financial performance to develop three hypotheses. It then described how the research was carried out, discussed the results, extended the findings, and elaborated the conclusions.

4. Results

4.1. Company Profiles

This section outlines the characteristics of ICT companies that have been surveyed in this study. The debate starts with the analysis of the categories and staff of the ICT firms.

There are three categories of firms observed-micro, small and medium-categorized enterprises as shown in

Table 3. In terms of the categories of the enterprises observed, the largest percentage of small businesses was 44%. The ratio of micro-enterprises then differed slightly to around four percent of small companies. Medium-size firms were the smallest share.

A total of 2615 employees were employed by the companies observed. In fact, with over 1400 people, the mid-size firms employed the most. Next, there were nearly half of all employees in the small companies of 1000. Finally, micro-entities employed about 200 workers, almost one-tenth of the total, with no workforces and with one and nine workers. This study referred to the International Standard for All Economic Activities for Industry Classification (ISIC). The companies studied were in division 62, and ICT enterprises are classified into four corporate services. In category 62.01, ICT enterprises are capable of delivering IT technology know-how involving creation, modification, test and supporting software. Division 62.02 includes companies that are experts in formulating, designing and developing computer systems that integrate computer hardware, software and communication technologies. Finally, ICT businesses that provide a variety of computer services, both applied and specialized, are classified as category 62.09 [

4].

Table 4 displays the number of businesses assessed with a cross-tabulation of their expertise and firm type. The highest number of surveyed ICT companies-44-supplied competence in computer programming, with half of them being small businesses. Following that, 30 of the examined ICT enterprises provided information and technology consultation, a market dominated by micro-sized and small-categorized businesses. Other information technology activities were provided by 20 observed corporations, as well as a similar number of small and micro-businesses-nine each. Finally, the businesses that supply computer operating services had the fewest number.

4.2. Assessment of Constructs

This part looked at how well the constructions and structural models were measured. First, the research examined how constructs were measured in terms of different sorts of formative and reflective indicators. The evaluation of reflective constructs reveals the indicators’ reliability, validity, variances, and collinearity. Meanwhile, reliability, convergent validity, collinearity, and substantial weight are identified in the examination of formative conceptions [

74,

76]. The structural model is examined in terms of goodness of fit, path coefficient of regression, coefficient of determination, and mediation path analysis once the constructs have been evaluated [

74,

78].

The study constructed financial performance to be composed of formative indicators. Consequently, the construct of latent variables should accomplish requirements of reliability, convergent validity, collinearity, and significant weight. Meanwhile, the study investigated inter-organizational trust and innovation, which reflected their indicators. The assessment of reflective constructs should achieve reliability, validity, collinearity, and good variances.

The first assessments investigated the reflective indicators of inter-organizational trust and innovation.

Table 5 shows the figures of observed variables, including the values of Cronbach’s Alpha (CA), Dillon-Goldstein (D.G.) rho, Average Variance Extracted (AVE), and Variance Inflation Factor (VIF). The values mentioned above are used to support the examination of the constructs. The CA and D.G. rho values indicate reliable and consistent constructs. Meanwhile, the VIF value reveals the collinearity level of the indicators.

At this point, this study examined the internal reliability ratio with CA.

Table 5 demonstrates that the CA coefficient of inter-organizational trust was about 0.7, meanwhile the CA number of innovation was about 0.8. Therefore, we concluded that those two latent variables met the internal consistency assumption. This study also indicated that the values of D.G. rho for inter-organizational trust and innovation were above 0.7 as the rule thumb. Definitively, this study indicated that internal consistency and uni-dimensionality were attained through inter-organizational trust and innovation indicators. The internal reliability indicated the constructs of those two latent variables were sufficiently consistent, constructing the two unobserved variables. The uni-dimensionality described the observed variables of inter-organizational trust and innovation reflected their indicators. Besides, the uni-dimensionality illustrated that indicators of inter-organizational trust had a strong association and signified as a single concept. Similarly, the constructs of innovation could be interpreted.

The constructs of inter-organizational trust and innovation had VIF values below three, as shown in

Table 5. Consequently, those two latent variables’ indicators met the non-collinearity assumption, which indicates the indicators had not correlated with each other.

The subsequent evaluation of the reflective indicators concentrated on examining the convergent validity of the constructs. This study indicated that the AVE values of inter-organizational trust and financial performance were above 0.7, which indicate the good variance due to the measurement error. Therefore, this study concluded that inter-organizational trust and innovation met the convergent validity, which clarified their constructs, explaining at least 50% of the variance of the constructs. Innovation had an AVE value of 0.826, which indicate a good variance of indicators. The final evaluation was the measurement of discriminant validity. The requirement is that the AVE value of a construct should be greater than the highest correlation of any other construct.

Table 6 shows the comparison between the AVE values and the correlation of their constructs.

As seen in

Table 6, the AVE values were greater than any other construct relationships. Thus, this study clarified that inter-organizational trust and innovation reflected discriminant validity. It also indicated that the constructs’ degree of inter-organizational trust and innovation were empirically distinguished from other constructs in the structural model. To conclude, inter-organizational trust and innovation indicators passed the requirements such as reliability, validity, collinearity, and variances of the indicators to perform as reflective indicators.

This study also examined financial performance as a formative construct. The evaluation of formative indicators comprises reliability, convergent validity, collinearity, and significant weight [

74,

76]. The first evaluation was to identify the internal reliability of the constructs. The D.G. rho value’s financial performance constructs were higher than 0.7 as the minimal value, as shown in

Table 5. Therefore, this study assumed that the indicators of financial performance were internally reliable and consistent. The internal reliability clarified that the constructs of financial performance significantly and consistently explained the degree of their variance.

This study then examined the convergent validity of the constructs of financial performance regarding the value of the outer loading factor.

Table 7 illustrates the loading factors of financial performance, all of which were higher than 0.7 as the standard point. As a result, this research revealed that two observed variables of financial performance met the convergent validity requirement. This implies that two formative indicators of financial performance are related to construct a formative variable. Two indicators of financial performance had a Variance Inflation Factor (VIF) value below three, as shown in

Table 5. According to the findings of this study, two observable indicators of financial performance did not correlate with one another. This meant that the two observed variables satisfied a non-collinearity condition.

Finally, this research examined the significance of the weight dimension of financial performance.

Table 8 depicts the summary of the weight dimension, which is the primary standard to evaluate each indicator’s relative significance in formative measurement models. The significant weight dimension refers to the critical value which is positioned between the lower and upper bound. The result of the research showed that Return on Equity (ROE) and Return on Capital Employed (ROCE) were significant. A significant indicator weight indicates that the constructs have good measurement quality as formative indicators [

74,

76].

To sum up, the constructs of financial performance accomplished the criteria in terms of reliability, convergent validity, collinearity, and significant weight. As a result, two constructs of financial performance could provide formative measures.

4.3. Evaluation of The Model

We then examined the structural model in terms of the inner model and outer model. The examination implemented the Goodness of Fit (GoF) to reveal the good model.

Table 9 illustrates the results of the GoF test.

This study examines the fit of models according to the goodness of fit (GoF) values, which indicates a good measurement of a PLS-SEM analysis model [

75,

79]. The inner model illustrates good associations between the latent variables and the indicators. Meanwhile, the outer model represents the directions of inter-organizational trust improving financial performance through innovation. The suggested cut-off point of the two models is 0.60 [

76,

80]. We found that the model had good outer and inner models due to the values of GoF above the cut-off point.

We performed a bootstrap test to evaluate the mediating variable. The approach is effortlessly suitable for the PLS-SEM analysis [

75]. We analyzed the direct and indirect effect of the model which proposed innovation as a mediator in improving the relationship between inter-organizational trust and financial performance.

Table 10 shows how innovation was examined as a mediating variable.

Innovation had a role as a complementary mediating variable. It implied that innovation had a complementing effect with inter-organizational trust. Therefore, innovation had significantly mediated the direction between inter-organizational trust and financial performance.

4.4. Examination of Hypotheses

This section examines and investigates the three following hypotheses.

Interorganizational trust has a positive effect on financial performance (H1);

A higher level of inter-organizational trust has a positive effect on innovation (H2);

Innovation has a positive effect on financial performance (H3).

Table 11 shows the examination of three hypotheses and coefficient of determination. The results appear to tally with this study’s expectancies.

Statistical analyses were performed, applying a significance level of 10 percent. This study disclosed interesting findings regarding the examination of hypotheses.

The first hypothesis was accepted. It was unsurprising to find a significant relationship between trust in business partners and financial performance. This result also supported the previous results of various researchers, namely, Fang et al. [

81], Moeller [

82], Gaur et al. [

12], Wei et al. [

70], Bien et al. [

11], and Shahmehr et al. [

13]. In the framework of transaction costs, trust in business partners involves managing transaction costs, namely searching costs, negotiating fees, and controlling costs. Meanwhile, the company can optimize its assets to support production. As a consequence, production is optimized while reducing total costs offers the prospect of enhancing profits. Consequently, this result went against that of Palmatier et al. [

83], who showed that trust in business partners had a disturbing if the incoherent effect on business performance. Furthermore, this study also conflicted with previous studies by Moeller [

82] and Al-Hakim and Lu [

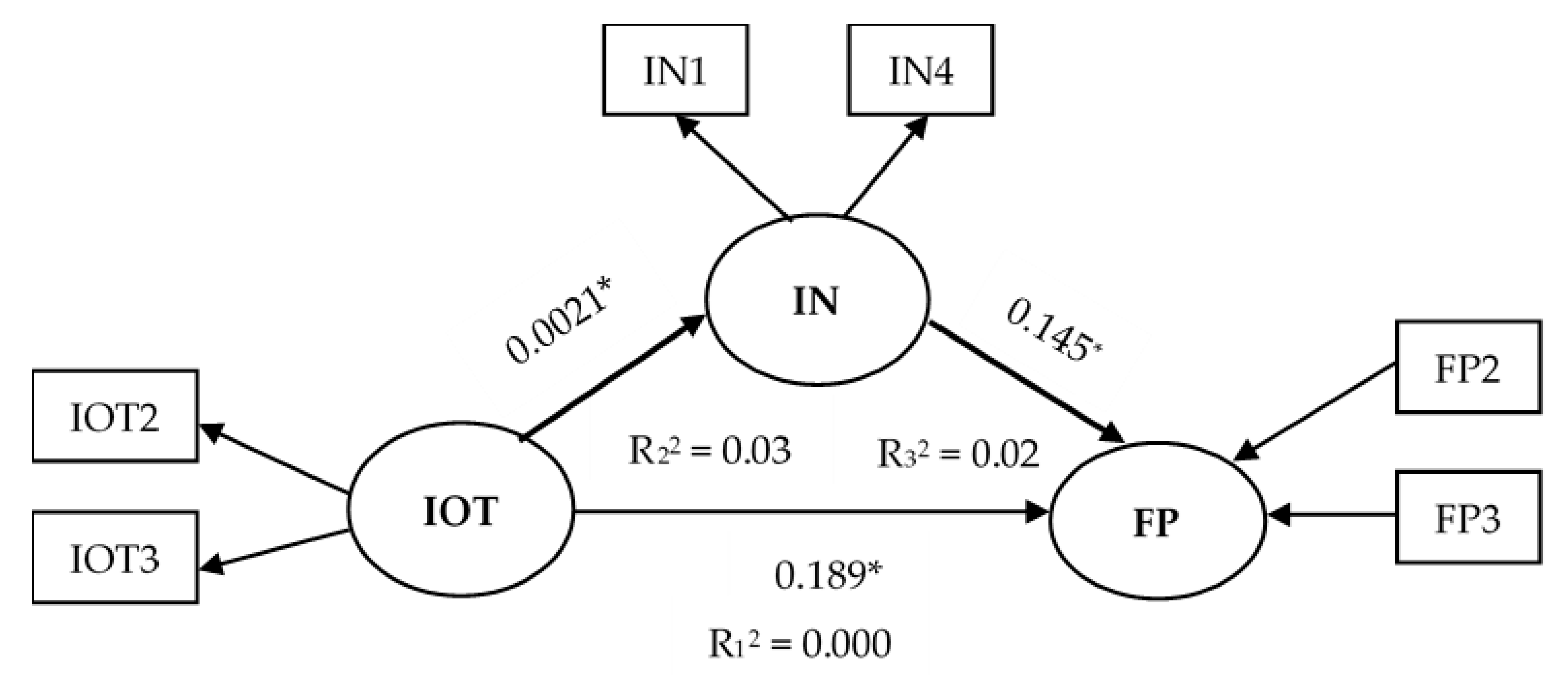

84], who revealed that confidence in business associates did not modify business performance. This research disclosed that inter-organizational trust contributed to about four percent of the variance in financial performance.

Furthermore, this study proved the positive relationship between trust in business partners and innovation. This result supported previous studies by Corsten and Felde [

19] and Y.-H. Tsai et al. [

35], who showed that trust in business partners had a positive relationship with innovation. This study also revealed that inter-organizational trust was related to innovation opportunities within ICT companies. Inter-organizational trust encourages the companies and their business partners to focus their endeavors on improving innovation prospects by enriching their chances of achieving innovation [

32]. Extending the result, trust in business partners encourages the effective exchange of knowledge, which improves innovation [

11]. The previous argument is consistent with Fawcett et al. [

85], who claim that sharing knowledge encourage entities to boost cooperation, innovation, and competitive performance. In conclusion, inter-organizational trust had a positive connection with innovation [

22]. This study also observed that inter-organizational trust determined below one percent of the variance in innovation.

Finally, the direction between innovation and financial performance was accepted. This result supported Zaheer et al. [

15] and Vaccaro et al. [

29]. Social capital theory supports the idea that an ICT company can achieve innovation opportunities through networks and knowledge transfers between business networks. In turn, an ICT company and its partners can transform information into knowledge and critical innovation. In this context, ICT companies successfully develop innovation to improve financial performance [

23]. This study supported the idea that innovation positively influenced financial performance [

29], and also showed that innovation contributed about two percent of the variance in financial performance.

5. Discussion

This study illustrates the model of the hypotheses in

Figure 2.

This study contributed to literature to a certain extent. First, this study discovered a strong, positive association between inter-organizational trust and financial performance. Thus, it supported the idea of a positive relationship between trust in business partners and business performance. Furthermore, the study emphasized that a higher level of trust in business partners [

86] positively impacted business performance [

50,

87,

88,

89]. As a significant contribution, the financial performance of the company was used as a proxy for business performance in this study. The study supported work by other researchers, namely, Fang et al. [

81], Moeller [

82], Gaur et al. [

12], Wei et al. [

70], Bien et al. [

11], and Shahmehr et al. [

13], who argued that inter-organizational trust enhanced financial performance.

Companies can expand production through the use of internal resources or outsourcing. When a company predicts that the beneficial impact of outsourcing will exceed that of internal improvement, it will decide to borrow assets from its partners. Therefore, a corporation needs to control transaction expenses such as the cost of finding, negotiating fees and monitoring costs to accomplish business collaboration. Trust in business partners works as hierarchical governance in support of co-operation in order to encourage business associates to reach an agreement to support manufacturing or outsourcing within the firm [

26,

86,

90]. It, thus, enhances production, sales and profit-related financial performance, while reducing expenses.

On the other hand, this study contradicted scholars who claimed that trust in business partners had an inconsistent effect on company performance [

83], or that trust in a business partner did not have a direct effect on business performance [

84]. This study reached the opposite conclusion to Moeller [

82], and Oláh et al. [

24], who revealed that trust in business partners did not affect financial performance.

Also supported was the idea that inter-organizational trust positively affected innovation. Therefore, this research corroborated previous results of various scholars, namely Corsten and Felde [

19] and Y.-H. Tsai et al. [

35]. The study emphasizes that inter-organizational trust prompts an exchange of resources and knowledge between companies and their business partners. Shared resources and knowledge cultivate innovation capabilities. According to the study, inter-organizational trust only contributed below one percent of the variance in innovation. Extending the discussion, this study recommended that various variables impact both innovations directly and business partner confidence. Scholars have previously claimed that the R&D budget [

91], inter-functional coordination and practice in human resources [

17], rapid response of market information and technology [

92] improve innovative levels. This research also suggested that the intermediary variables which contribute to innovations, such as mutually cooperative work, the use of technology to transmit information, the adoption of current knowledge and technology and the flexibility and opportunism [

93].

This study indicated that innovation was closely related to financial performance. Vaccaro et al. [

29] and Zaheer et al. [

15] have been backed by this result. According to the idea of social capital, there is an important role of trust in supporting the combination and exchange of resources. The combination and resources exchange then produce value for the company by having a substantial and beneficial impact on products innovations [

26]. In addition to innovation, this study also specifies that successful relevancy and network involvement have a substantial financial impact [

82]. Indeed, both quality and cost improvements are significant and associated with financial performance [

94]. According to the findings of this study, innovation mediated the relationship between intra-organizational trust and financial success. As anticipated, innovation had the potential to mediate the direction of inter-organizational trust in financial performance. This study found that inter-organizational trust and innovation explained approximately six percent of the variability in financial performance. In a nation like Hungary, this finding was noteworthy, and it was similar to facts in European nations such as Denmark, Ireland, and Wales [

95].

ICT firms can sustain themselves in a disruptive era through strategic approaches, as follows: they should set up their resources, processes, and values to confront newcomers emerging with new types of innovations. They should innovate to develop products or services to obtain potential profits, and then sustain them in a competitive market [

7,

8]. This study argued that Hungarian ICT corporates were a good model in which inter-organizational trust improved innovation. ICT firms had a high level of innovative methods, new procedures, and systems. Consequently, Hungarian ICT firms could sustain in a disruptive era by offering innovative products or services to their best customers to gain good potential profit margins.

Besides, ICT companies should offer competitive prices, improve the performance of products or services, and create market demand [

96]. Those strategies could support ICT firms in meeting the challenges of disruptive technologies in a disruptive era. According to the study’s findings, a firm should create shared connection ties, confidence in partners, and mutuality, which are strongly related to the intention to share information to accomplish innovation [

97] to compete under commercial pressure in a disruptive era. Innovation also improves financial performance. ICT companies should achieve innovation to compete in a disruptive era because innovation can improve business growth and anticipate volatile markets. A firm should innovate continuously, developing unique processes or systems, further developing innovative products and services, and applying an up-to-date approach to innovation. As a result, potential innovation improves profitability related to ROE, and ROCE, as shown in this study.

We noticed that the manuscript contained two flaws. First, three coefficient determinations (R

2) were below six percent. The lowest R

2 was the relationship between inter-organizational trust and innovation. Therefore, we suggested that future studies would examine the mediating variables in improving the relationship of aforesaid two variables, namely working in partnership with international customers, using technology to disseminate knowledge, responding to knowledge about technology, and being flexible and opportunistic [

93]. We suggested that future studies include will assess financial performance using measures other than profitability, such as liquidity, leverage, and efficiency. As a result of the correct measurement, the future outcomes will have good variances. Second, we admitted that the number of samples was a minimum sample size. As a result, this research recommended increasing the number of proportionate samples representing micro, small, medium, and large ICT firms in the event of a pandemic in both developing and industrialized countries.

The findings, research questions, results of hypotheses, and further agenda are summarized in

Table 12.

,

,

{kind=link}

{kind=link}