Does Slack Buffer? Market Performance after Environmental Shock

Abstract

:1. Introduction

2. Literature Review and Research Hypotheses

2.1. Slack Resources

2.2. Environmental Shock

2.3. Environmental Shock and Effects of Slack

2.4. The Severity of Environmental Shock and Effects of Slack

3. Method

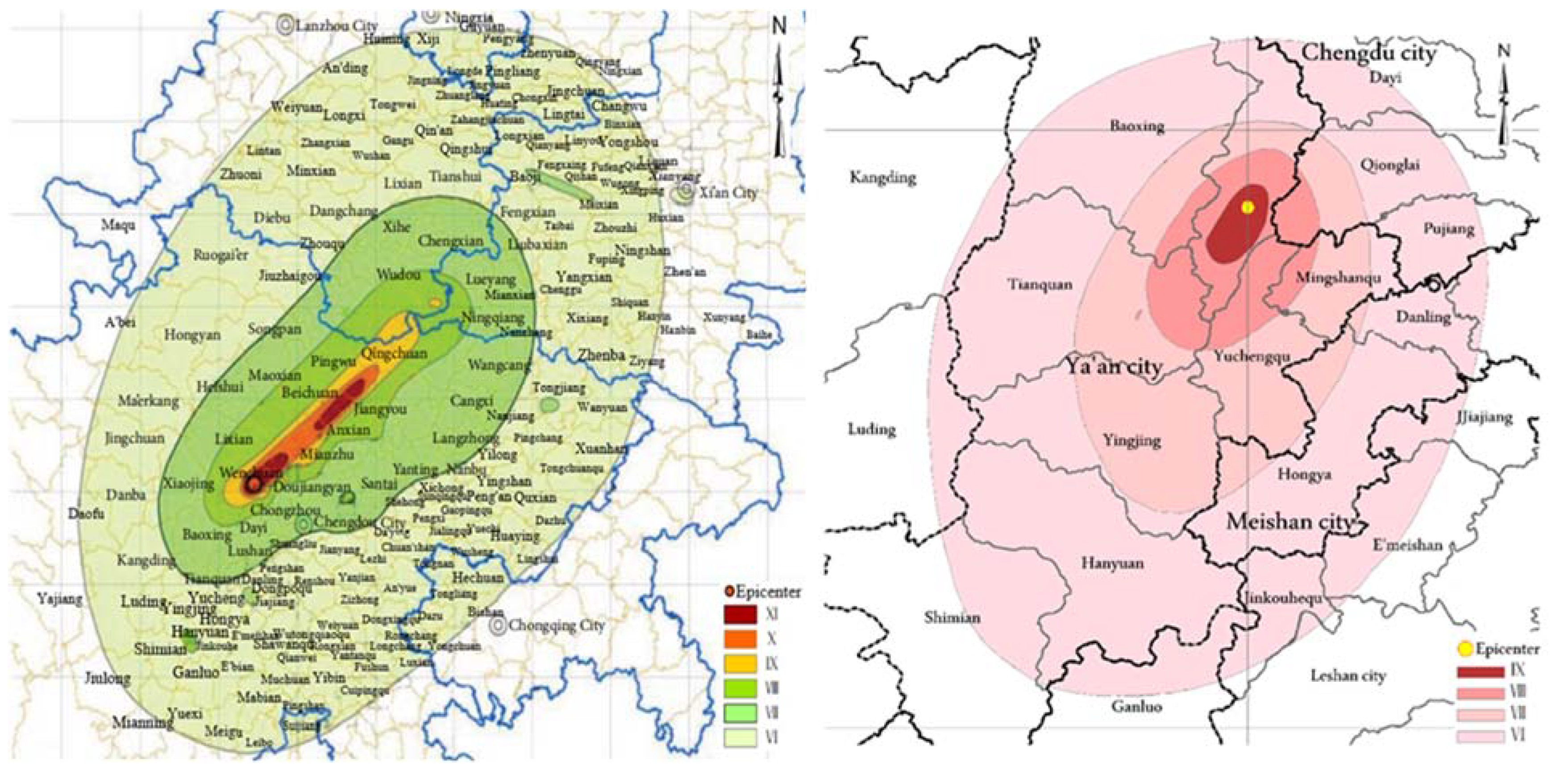

3.1. Sample

3.2. Measures

3.3. Statistical Method

4. Results

5. Discussion

5.1. Buffer Effect

5.2. Environmental Shocks

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Salvato, C.; Sargiacomo, M.; Amore, M.D.; Minichilli, A. Natural disasters as a source of entrepreneurial opportunity: Family business resilience after an earthquake. Strateg. Entrep. J. 2020, 14, 594–615. [Google Scholar] [CrossRef]

- You, X.; Jia, S.; Dou, J.; Su, E. Is organizational slack honey or poison? Experimental research based on external investors’ perception. Emerg. Mark. Rev. 2020, 44, 100698. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Wolf, G.; Chase, R.B.; Tansik, D.A. Antecedents of organizational slack. Acad. Manag. Rev. 1988, 13, 601–614. [Google Scholar] [CrossRef]

- Voss, G.B.; Sirdeshmukh, D.; Voss, Z.G. The effects of slack resources and environmental threat on product exploration and exploitation. Acad. Manag. J. 2008, 51, 147–164. [Google Scholar] [CrossRef] [Green Version]

- Bradley, S.W.; Shepherd, D.A.; Wiklund, J. The importance of slack for new organizations facing ‘tough’environments. J. Manag. Stud. 2011, 48, 1071–1097. [Google Scholar] [CrossRef]

- Osiyevskyy, O.; Shirokova, G.; Ritala, P. Exploration and exploitation in crisis environment: Implications for level and variability of firm performance. J. Bus. Res. 2020, 114, 227–239. [Google Scholar] [CrossRef]

- Wan, W.P.; Yiu, D.W. From crisis to opportunity: Environmental jolt, corporate acquisitions, and firm performance. Strateg. Manag. J. 2009, 30, 791–801. [Google Scholar] [CrossRef]

- Cyert, R.M.; March, J.G. A Behavioral Theory of the Firm; Prentice Hall: Englewood Cliffs, NJ, USA, 1963. [Google Scholar]

- Duan, Y.; Wang, W.; Zhou, W. The multiple mediation effect of absorptive capacity on the organizational slack and innovation performance of high-tech manufacturing firms: Evidence from Chinese firms. Int. J. Prod. Econ. 2020, 229, 107754. [Google Scholar] [CrossRef]

- Paeleman, I.; Vanacker, T. Less is more, or not? On the interplay between bundles of slack resources, firm performance and firm survival. J. Manag. Stud. 2015, 52, 819–848. [Google Scholar] [CrossRef]

- George, G. Slack resources and the performance of privately held firms. Acad. Manag. J. 2005, 48, 661–676. [Google Scholar] [CrossRef]

- Carnes, C.; Xu, K.; Sirmon, D.; Karadag, R. How competitive action mediates the resource slack-performance relationship: A meta-analytic approach. J. Manag. Stud. 2018, 56, 57–90. [Google Scholar] [CrossRef] [Green Version]

- Guo, F.; Zou, B.; Zhang, X.; Bo, Q.; Li, K. Financial slack and firm performance of SMMEs in China: Moderating effects of government subsidies and market-supporting institutions. Int. J. Prod. Econ. 2019, 223, 107530. [Google Scholar] [CrossRef]

- Kovach, J.J.; Hora, M.; Manikas, A.; Patel, P.C. Firm performance in dynamic environments: The role of operational slack and operational scope. J. Oper. Manag. 2015, 37, 1–12. [Google Scholar] [CrossRef]

- Lungeanu, R.; Stern, I.; Zajac, E.J. When do firms change technology-sourcing vehicles? The role of poor innovative performance and financial slack. Strateg. Manag. J. 2016, 37, 855–869. [Google Scholar] [CrossRef]

- Tabesh, P.; Vera, D.; Keller, R. Unabsorbed slack resource deployment and exploratory and exploitative innovation: How much does CEO expertise matter? J. Bus. Res. 2019, 94, 65–80. [Google Scholar] [CrossRef]

- Soetanto, D.; Jack, S. Slack resources, exploratory and exploitative innovation and the performance of small technology-based firms at incubators. J. Technol. Transf. 2018, 43, 1–19. [Google Scholar] [CrossRef]

- Jensen, M.; Meckling, W. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Bourgeois, L.J., III. On the measurement of organizational slack. Acad. Manag. Rev. 1981, 6, 29–39. [Google Scholar] [CrossRef]

- Cheng, J.L.; Kesner, I.F. Organizational slack and response to environmental shifts: The impact of resource allocation patterns. J. Manag. 1997, 23, 1–18. [Google Scholar] [CrossRef]

- Sun, Y.; Du, S.; Ding, Y. The Relationship between Slack Resources, Resource Bricolage, and Entrepreneurial Opportunity Identification—Based on Resource Opportunity Perspective. Sustainability 2020, 12, 1199. [Google Scholar] [CrossRef] [Green Version]

- Martin, G.P.; Wiseman, R.M.; Gomez-Mejia, L.R. Going short-term or long-term? CEO stock options and temporal orientation in the presence of slack. Strateg. Manag. J. 2016, 37, 2463–2480. [Google Scholar] [CrossRef]

- Vanacker, T.; Collewaert, V.; Zahra, S. Slack resources, firm performance and the institutional context: Evidence from privately held European firms. Strateg. Manag. J. 2017, 38, 1305–1326. [Google Scholar] [CrossRef]

- Godoy-Bejarano, J.; Ruiz-Pava, G.; Téllez, D. Environmental complexity, slack, and firm performance. J. Econ. Bus. 2020, 112, 105933. [Google Scholar] [CrossRef]

- Symeou, P.; Zyglidopoulos, S.; Gardberg, N. Corporate environmental performance: Revisiting the role of organizational slack. J. Bus. Res. 2018, 96, 169–182. [Google Scholar] [CrossRef]

- Steensma, H.K.; Corley, K.G. Organizational context as a moderator of theories on firm boundaries for technology sourcing. Acad. Manag. J. 2001, 44, 271–291. [Google Scholar] [CrossRef]

- Thompson, J.D. Organizations in Action; McGraw-Hill: New York, NY, USA, 1967. [Google Scholar]

- Haveman, H.; Russo, M.; Meyer, A. Organizational environments in flux: The impact of regulatory punctuations on organizational domains, CEO succession, and performance. Organ. Sci. 2001, 12, 253–273. [Google Scholar] [CrossRef] [Green Version]

- Hendricks, K.; Singhal, V.; Zhang, R. The effect of operational slack, diversification, and vertical relatedness on the stock market reaction to supply chain disruptions. J. Oper. Manag. 2009, 27, 233–246. [Google Scholar] [CrossRef]

- de la Hiz, D.I.L.; Ferron-Vilchez, V.; Aragon-Correa, J.A. Do firms’ slack resources influence the relationship between focused environmental innovations and financial performance? More is not always better. J. Bus. Ethics 2019, 159, 1215–1227. [Google Scholar] [CrossRef]

- Teirlinck, P. Engaging in new and more research-oriented R&D projects: Interplay between level of new slack, business strategy and slack absorption. J. Bus. Res. 2020, 120, 181–194. [Google Scholar] [CrossRef]

- Tan, J.; Peng, M.W. Organizational slack and firm performance during economic transitions: Two studies from an emerging economy. Strateg. Manag. J. 2003, 24, 1249–1263. [Google Scholar] [CrossRef]

- Singh, J.V. Performance, slack, and risk taking in organizational decision making. Acad. Manag. J. 1986, 29, 562–585. [Google Scholar] [CrossRef]

- Kim, C.; Bettis, R.A. Cash is surprisingly valuable as a strategic asset. Strateg. Manag. J. 2014, 35, 2053–2063. [Google Scholar] [CrossRef]

- Bentley, F.; Kehoe, R. Give them some slack—They’re trying to change! The benefits of excess cash, excess employees, and increased human capital in the strategic change context. Acad. Manag. J. 2018, 63, 181–204. [Google Scholar] [CrossRef]

- Troilo, G.; De Luca, L.; Atuahene-Gima, K. More Innovation with Less? A strategic contingency view of slack resources, information search, and radical innovation. J. Prod. Innov. Manag. 2014, 31, 259–277. [Google Scholar] [CrossRef]

- Deb, P.; David, P.; O’Brien, J. When is cash good or bad for firm performance? Strateg. Manag. J. 2017, 38, 436–454. [Google Scholar] [CrossRef]

- Meyer, A.D. Adapting to environmental jolts. Adm. Sci. Q. 1982, 27, 515–537. [Google Scholar] [CrossRef] [PubMed]

- Coff, R.W. When competitive advantage doesn’t lead to performance: The resource-based view and stakeholder bargaining power. Organ. Sci. 1999, 10, 119–133. [Google Scholar] [CrossRef]

- Barberis, N.; Thaler, R. A survey of behavioral finance. In Handbook of the Economics of Finance; Constantinides, G.M., Harris, M., Stulz, R.M., Eds.; Elsevier: Amsterdam, The Netherlands, 2003; Volume 1, pp. 1053–1128. [Google Scholar]

- Linnerooth-Bayer, J.; Surminski, S.; Bouwer, L.M.; Noy, I.; Mechler, R. Insurance as a response to loss and damage? In Loss and Damage from Climate Change: Concepts, Methods and Policy Options; Mechler, R., Bouwer, L.M., Schinko, T., Surminski, S., Linnerooth-Bayer, J., Eds.; Springer: Cham, Switzerland, 2019; pp. 483–512. [Google Scholar] [CrossRef] [Green Version]

- Nason, R.S.; Patel, P.C. Is cash king? Market performance and cash during a recession. J. Bus. Res. 2016, 69, 4242–4248. [Google Scholar] [CrossRef]

- Yu, L.; Lai, K.K. A distance-based group decision-making methodology for multi-person multi-criteria emergency decision support. Decis. Support Syst. 2011, 51, 307–315. [Google Scholar] [CrossRef]

- Cavallo, A.; Cavallo, E.; Rigobon, R. Prices and supply disruptions during natural disasters. Rev. Income Wealth 2014, 60, 449–471. [Google Scholar] [CrossRef]

- Park, A.; Wang, S. Benefiting from disaster? Public and private responses to the Wenchuan earthquake. World Dev. 2017, 94, 38–50. [Google Scholar] [CrossRef]

- Liu, J.; Wang, S. Analysis of the differentiation in human vulnerability to earthquake hazard between rural and urban areas: Case studies in 5.12 Wenchuan Earthquake (2008) and 4.20 Ya’an Earthquake (2013), China. J. Hous. Built Environ. 2015, 30, 87–107. [Google Scholar] [CrossRef]

- Hosono, K.; Miyakawa, D.; Uchino, T.; Hazama, M.; Ono, A.; Uchida, H.; Uesugi, I. Natural disasters, damage to banks, and firm investment. Int. Econ. Rev. 2016, 57, 1335–1370. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Q.; Zhang, Y.; Yang, X.; Su, B. Automatic recognition of seismic intensity based on RS and GIS: A case study in Wenchuan Ms8. 0 earthquake of China. Sci. World J. 2014, 2014, 878149. [Google Scholar] [CrossRef]

- Lin, Y.-H.; Chen, C.-J.; Lin, B.-W. The dual-edged role of returnee board members in new venture performance. J. Bus. Res. 2018, 90, 347–358. [Google Scholar] [CrossRef]

- Vanacker, T.; Collewaert, V.; Paeleman, I. The relationship between slack resources and the performance of entrepreneurial firms: The role of venture capital and angel investors. J. Manag. Stud. 2013, 50, 1070–1096. [Google Scholar] [CrossRef]

- Miller, K.D.; Leiblein, M.J. Corporate risk-return relations: Returns variability versus downside risk. Acad. Manag. J. 1996, 39, 91–122. [Google Scholar] [CrossRef]

- Sirmon, D.G.; Hitt, M.A.; Ireland, R.D. Managing firm resources in dynamic environments to create value: Looking inside the black box. Acad. Manag. Rev. 2007, 32, 273–292. [Google Scholar] [CrossRef] [Green Version]

- Hendricks, K.B.; Jacobs, B.W.; Singhal, V.R. Stock market reaction to supply chain disruptions from the 2011 Great East Japan Earthquake. Manuf. Serv. Oper. Manag. 2020, 22, 683–699. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1. Stock Price | 0.098 | 17.285 | 1 | |||||||

| 2. Firm Age | 14.508 | 5.114 | −0.033 | 1 | ||||||

| 3. Firm Size | 4.663 | 9.449 | −0.085 * | 0.004 | 1 | |||||

| 4. Product Diversification | 3.631 | 2.152 | 0.028 | 0.024 | 0.208 ** | 1 | ||||

| 5. External Resource | −13.828 | 86.648 | 0.042 | −0.032 | 0.027 | 0.105 ** | 1 | |||

| 6. Severity | 0.032 | 1.786 | −0.009 | 0.024 | −0.043 | 0.084 * | 0.123 ** | 1 | ||

| 7. Unabsorbed Slack | −0.307 | 2.902 | 0.001 | −0.021 | 0.077 * | 0.000 | 0.045 | 0.009 | 1 | |

| 8. Absorbed Slack | 0.055 | 2.131 | −0.027 | 0.015 | −0.069 | −0.084 * | −0.014 | 0.001 | 0.005 | 1 |

| Variable | All Firms (Number of Group = 249, N = 688) | Balanced Firms (Number of Group = 211, N = 633) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 | Model 13 | Model 14 | |

| Firm Age | 0.094 | 0.087 | 0.111 | 0.115 | 0.089 | 0.116 | 0.138 | 0.163 | 0.158 | 0.167 | 0.161 | 0.159 | 0.183 | 0.197 |

| (0.160) | (0.159) | (0.159) | (0.159) | (0.161) | (0.162) | (0.160) | (0.173) | (0.171) | (0.172) | (0.172) | (0.174) | (0.176) | (0.174) | |

| Firm Size | −0.203 *** | −0.144 * | −0.158 ** | −0.164 ** | −0.201 *** | −0.199 *** | −0.196 *** | −0.184 *** | −0.118 + | −0.137 * | −0.143 * | −0.182 *** | −0.184 *** | −0.182 *** |

| (0.043) | (0.062) | (0.057) | (0.063) | (0.043) | (0.044) | (0.045) | (0.043) | (0.062) | (0.057) | (0.064) | (0.043) | (0.043) | (0.044) | |

| Product Diversification | −0.030 | −0.053 | −0.071 | −0.063 | −0.009 | −0.026 | 0.030 | −0.212 | −0.242 | −0.235 | −0.235 | −0.197 | −0.214 | −0.176 |

| (0.298) | (0.300) | (0.297) | (0.297) | (0.305) | (0.301) | (0.298) | (0.306) | (0.308) | (0.309) | (0.311) | (0.314) | (0.311) | (0.311) | |

| Ownership | 2.451 + | 2.437 + | 2.414 + | 2.203 | 2.414 + | 2.387 + | 2.286 | 1.923 | 1.903 | 1.879 | 1.792 | 1.903 | 1.856 | 1.837 |

| (1.387) | (1.389) | (1.386) | (1.420) | (1.395) | (1.387) | (1.419) | (1.475) | (1.476) | (1.479) | (1.527) | (1.481) | (1.477) | (1.513) | |

| External Resource | −0.003 | −0.003 | −0.004 | −0.004 | −0.003 | −0.004 | −0.006 | −0.012 | −0.012 | −0.010 | −0.011 | −0.012 | −0.010 | −0.013 |

| (0.012) | (0.012) | (0.012) | (0.012) | (0.012) | (0.012) | (0.011) | (0.016) | (0.016) | (0.016) | (0.016) | (0.016) | (0.016) | (0.015) | |

| Earthquake Type | 0.417 | 0.562 | 0.728 | 1.199 | 0.417 | 0.737 | 1.320 | 1.446 | 1.631 | 1.634 | 1.801 | 1.445 | 1.761 | 2.086 |

| (1.497) | (1.505) | (1.510) | (1.674) | (1.495) | (1.488) | (1.636) | (1.583) | (1.593) | (1.600) | (1.761) | (1.582) | (1.578) | (1.724) | |

| Effect Type | −0.783 | −0.742 | −0.693 | −0.739 | −0.869 | −1.064 | −1.112 | −0.446 | −0.395 | −0.317 | −0.409 | −0.494 | −0.689 | −0.772 |

| (1.859) | (1.872) | (1.869) | (1.859) | (1.851) | (1.851) | (1.827) | (1.850) | (1.861) | (1.866) | (1.864) | (1.846) | (1.849) | (1.825) | |

| Unabsorbed Slack | −0.327 | −1.318 * | −1.272 * | −0.369 | −1.339 * | −1.290 * | ||||||||

| (0.231) | (0.557) | (0.539) | (0.237) | (0.564) | (0.545) | |||||||||

| Absorbed Slack | 0.185 | 1.147 ** | 1.187 ** | 0.115 | 1.220 ** | 1.249 ** | ||||||||

| (0.274) | (0.368) | (0.374) | (0.263) | (0.418) | (0.424) | |||||||||

| During-shock period Dummy | −2.140 | −2.163 | −2.400 | −2.460 | −1.959 | −1.975 | −2.169 | −2.252 | ||||||

| (1.770) | (1.780) | (1.785) | (1.782) | (1.826) | (1.836) | (1.843) | (1.843) | |||||||

| Post-shock period Dummy | −2.985 + | −2.863 + | −3.356 + | −3.347 + | −1.974 | −1.857 | −2.313 | −2.319 | ||||||

| (1.726) | (1.706) | (1.740) | (1.741) | (1.798) | (1.773) | (1.819) | (1.821) | |||||||

| During-shock period Dummy × Unabsorbed Slack | 1.439 ** | 1.433 * | 1.446 ** | 1.442 * | ||||||||||

| (0.512) | (0.604) | (0.514) | (0.570) | |||||||||||

| Post-shock period Dummy × Unabsorbed Slack | 1.738 + | 1.805 ** | 1.730 + | 1.776 ** | ||||||||||

| (0.913) | (0.647) | (0.949) | (0.670) | |||||||||||

| During-shock period Dummy × Absorbed Slack | −1.722 + | −0.923 | −2.320 ** | −1.478 * | ||||||||||

| (0.887) | (0.760) | (0.818) | (0.740) | |||||||||||

| Post-shock period Dummy × Absorbed Slack | −1.189 ** | −1.130 * | −1.329 ** | −1.442 ** | ||||||||||

| (0.389) | (0.489) | (0.437) | (0.516) | |||||||||||

| Severity | −0.265 | −0.370 | −0.122 | −0.249 | ||||||||||

| (0.353) | (0.353) | (0.355) | (0.354) | |||||||||||

| During-shock period Dummy × Unabsorbed Slack × Severity | −0.155 | −0.092 | ||||||||||||

| (0.203) | (0.189) | |||||||||||||

| Post-shock period Dummy × Unabsorbed Slack × Severity | 0.555 *** | 0.558 ** | ||||||||||||

| (0.162) | (0.179) | |||||||||||||

| During-shock period Dummy × Absorbed Slack × Severity | 1.391 *** | 1.359 *** | ||||||||||||

| (0.339) | (0.365) | |||||||||||||

| Post-shock period Dummy × Absorbed Slack × Severity | 0.110 | −0.087 | ||||||||||||

| (0.293) | (0.262) | |||||||||||||

| Constant | −1.590 | −1.747 | −0.454 | −1.119 | −1.500 | −0.002 | −1.321 | −3.390 | −3.657 | −2.464 | −2.555 | −3.367 | −2.223 | −3.016 |

| (10.189) | (10.200) | (10.342) | (10.372) | (10.207) | (10.355) | (10.422) | (15.738) | (15.758) | (16.004) | (16.019) | (15.770) | (16.008) | (16.116) | |

| R2 | 0.0880 | 0.0893 | 0.1181 | 0.1185 | 0.0876 | 0.1237 | 0.1223 | 0.1403 | 0.1430 | 0.1450 | 0.1353 | 0.1388 | 0.1564 | 0.1556 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, X.; Zhang, S. Does Slack Buffer? Market Performance after Environmental Shock. Sustainability 2021, 13, 9493. https://doi.org/10.3390/su13179493

Li X, Zhang S. Does Slack Buffer? Market Performance after Environmental Shock. Sustainability. 2021; 13(17):9493. https://doi.org/10.3390/su13179493

Chicago/Turabian StyleLi, Xiaoxiang, and Shuhan Zhang. 2021. "Does Slack Buffer? Market Performance after Environmental Shock" Sustainability 13, no. 17: 9493. https://doi.org/10.3390/su13179493

APA StyleLi, X., & Zhang, S. (2021). Does Slack Buffer? Market Performance after Environmental Shock. Sustainability, 13(17), 9493. https://doi.org/10.3390/su13179493