Evolution of the Spatial Pattern of the Assets and Environmental Liabilities Conversion Rate and Its Influencing Factors

Abstract

:1. Introduction

2. Literature Review

2.1. Research on Environmental Liabilities

2.2. Efficiency Calculation and Index Selection for Environmental Protection Expenditure of Local Government

2.3. Factors Influencing the Conversion Rate of Assets and Environmental Liabilities

2.4. Research Hypotheses

3. Methodology

3.1. Transformation Logic and Model Selection of Assets and Environmental Liabilities

3.2. Efficiency Evaluation Using the Super-SBM Model with Undesirable Outputs

3.3. Spatial Econometric Model and Estimation Method

3.3.1. Spatial Autocorrelation Analysis Model

3.3.2. Spatial Regression Model

3.4. Data Collection and Index Construction

3.4.1. Data Collection

3.4.2. Index Construction

4. Discussion

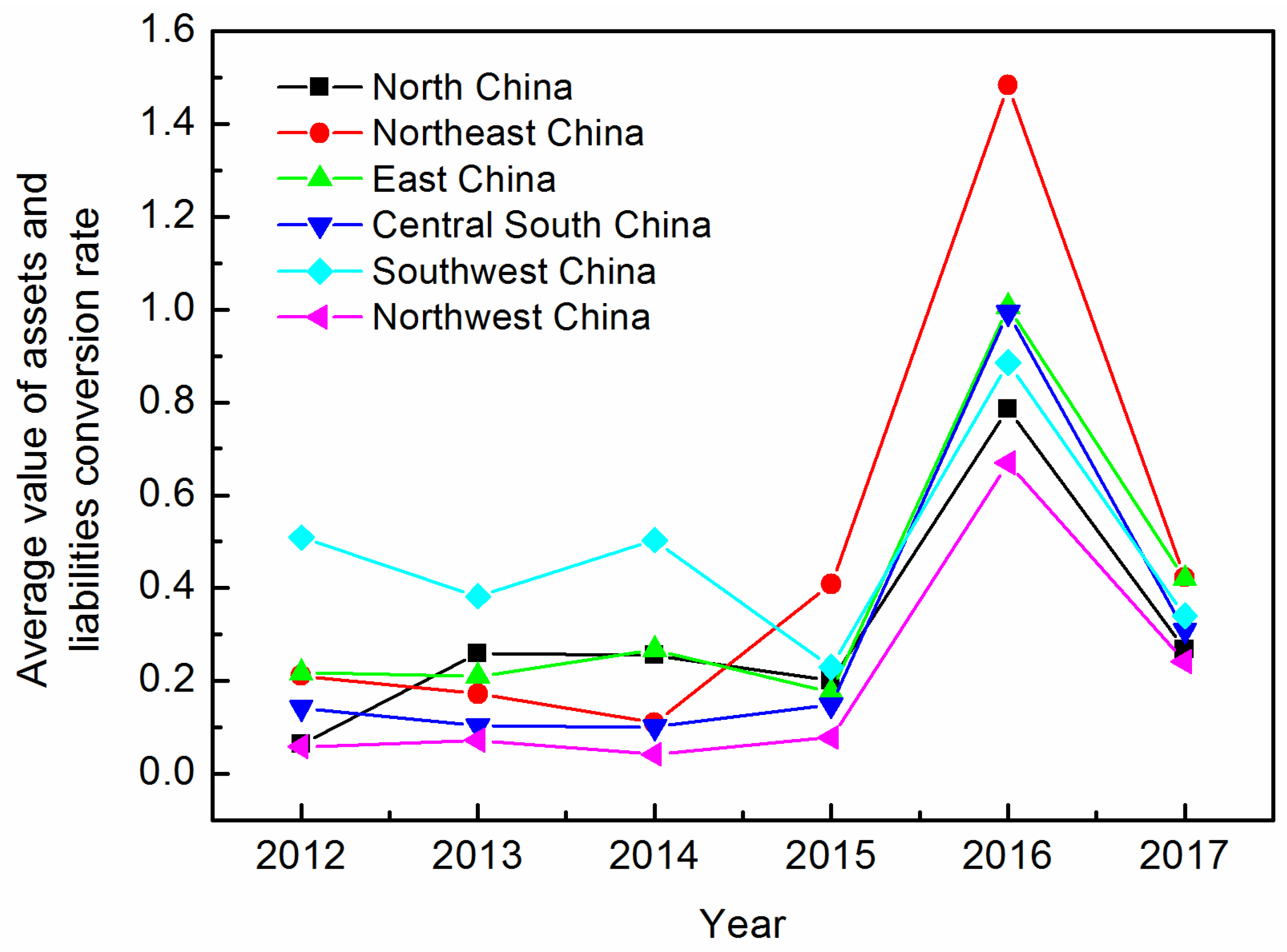

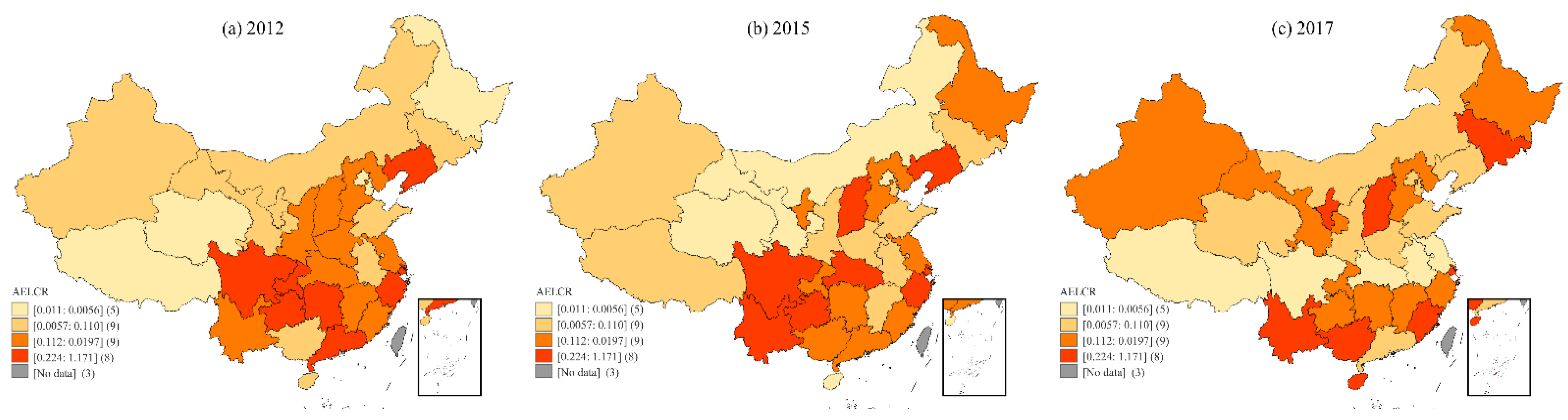

4.1. Calculation of Conversion Rates of Assets and Environmental Liabilities

4.2. Analysis of the Spatial Evolution Characteristics of the Conversion Rates of Assets and Environmental Liabilities

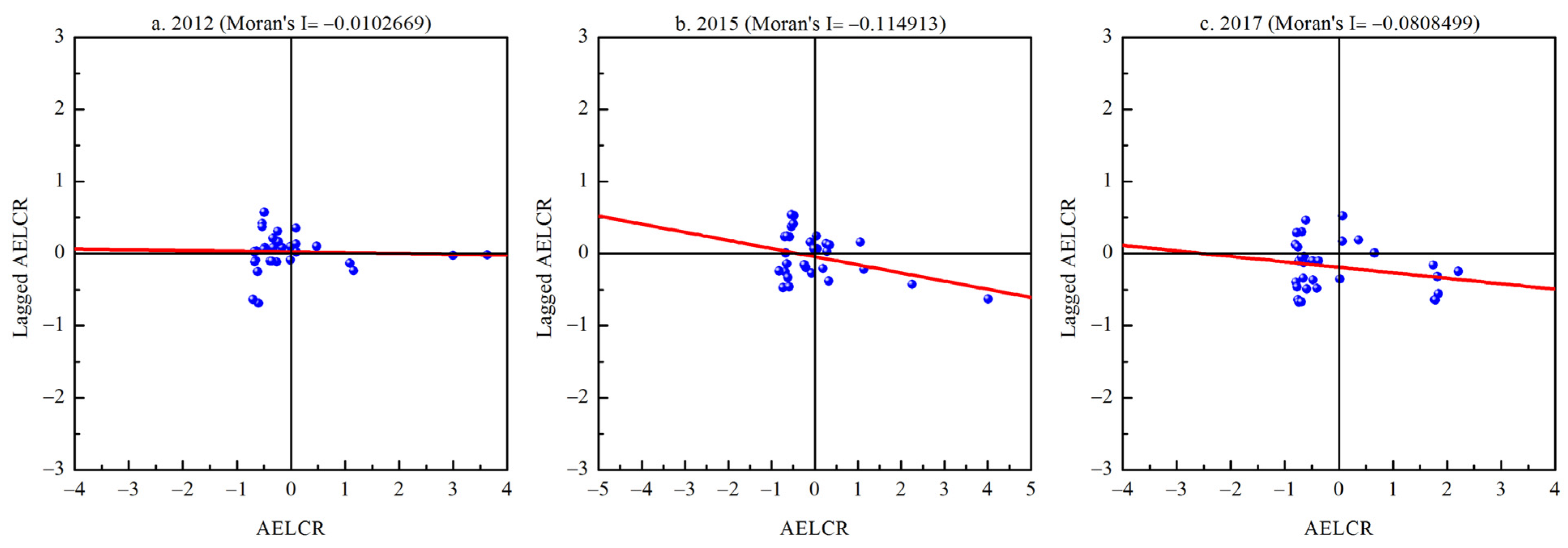

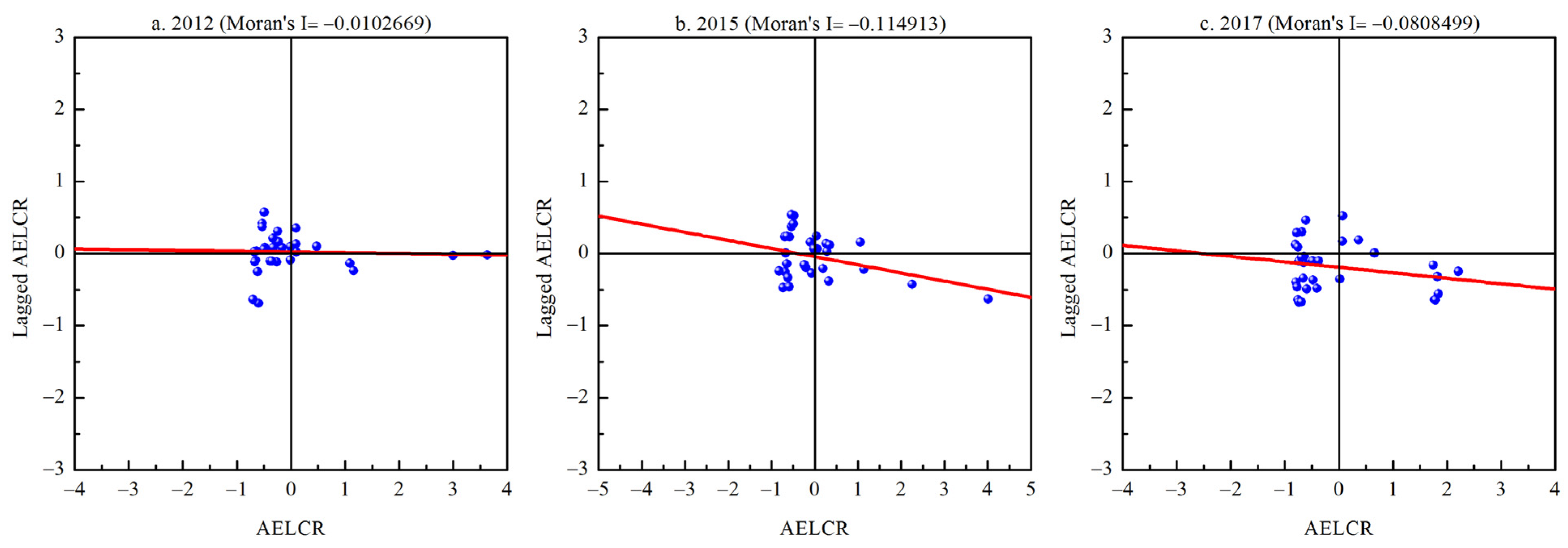

4.2.1. Analysis of Global Spatial Autocorrelations

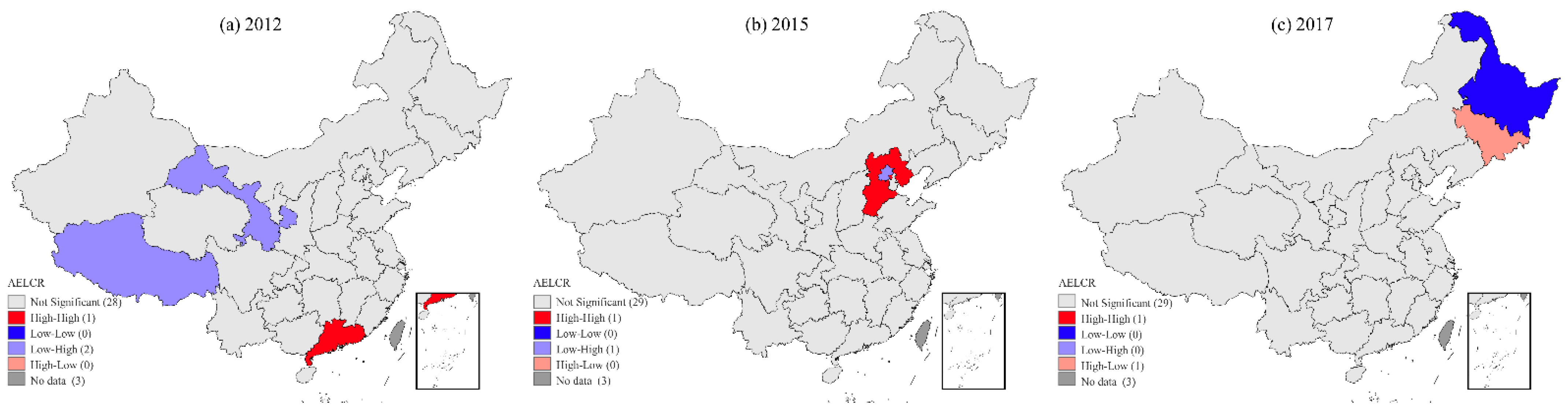

4.2.2. Analysis of Local Spatial Autocorrelations

5. Analysis of Factors Influencing the Spatial Evolution of the Conversion Rates of Assets and Environmental Liabilities

5.1. Index Selection and Data Preprocessing

5.2. Spatial Econometric Modeling and Analysis of Panel Data

5.2.1. Spatial Lag Model (SLM)

5.2.2. Spatial Error Model (SEM)

5.2.3. Analysis of SLM and SEM Model Results

6. Conclusions and Implications

6.1. Conclusions

6.2. Managerial and Policy Implications

7. Limitations and Outlook

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Abraham, K.S. Environmental liability and the limits of insurance. Colum. L. Rev. 1988, 88, 942–988. [Google Scholar] [CrossRef] [Green Version]

- Rauscher, M. Economic Growth and Tax-competition Leviathans. Int. Tax Public Finan. 2005, 12, 457–474. [Google Scholar] [CrossRef] [Green Version]

- Wang, H. Review on the development of resource assets appraisal. China Manag. Inf. 2012, 15, 14–16. [Google Scholar]

- Beltrán-Esteve, M.; Gómez-Limón, J.A.; Picazo-Tadeo, A.J.; Reig-Martínez, E. A metafrontier directional distance function approach to assessing eco-efficiency. J. Prod. Anal. 2014, 41, 69–83. [Google Scholar] [CrossRef]

- Färe, R.; Grosskopf, S.; Lovell, C.A.K.; Pasurka, C. Multilateral productivity comparisons when some outputs are undesirable: A nonparametric approach. Rev. Econ. Stat. 1989, 71, 90–98. [Google Scholar] [CrossRef]

- Chung, Y.H.; Färe, R.; Grosskopf, S. Productivity and undesirable outputs: A directional distance function approach. Environ. Manag. 1997, 51, 229–240. [Google Scholar] [CrossRef] [Green Version]

- Wang, Y.; Wen, Z.; Cao, X.; Zheng, Z.; Xu, J. Environmental efficiency evaluation of China’s iron and steel industry: A process-level data envelopment analysis. Sci. Total Environ. 2020, 707, 135903. [Google Scholar] [CrossRef]

- Chen, L.M.; Wang, W.P.; Wang, B. Economic efficiency, environmental efficiency and ecological efficiency of “two horizontal and three vertical” urbanized areas—An Empirical Analysis Based on mixed directional distance function and composite graph method. Chin. Soft. Sci. 2015, 2, 96–109. [Google Scholar]

- Zhu, H.; Fu, Q.; Wei, Q. Empirical Study on efficiency accounting and influencing factors of local government’s environmental protection expenditure. Chin. J. Popul. Resour. Environ. 2014, 24, 91–96. [Google Scholar]

- Yin, K.; Wang, S.R.; Yao, L.; Liang, J. Ecological efficiency evaluation of environmental protection model cities in China. Acta Ecol. Sin. 2011, 31, 5588–5598. [Google Scholar]

- Huang, Y.P.; Shi, Q.P. Research on regional environmental efficiency and environmental total factors in China—Based on SBM model with R & D input. China Popul. Resour. Environ. 2015, 25, 25–34. [Google Scholar]

- Becerra-Ornelas, A.U.; Nuñez, H.M. The technical efficiency of local economies in Mexico: A failure of decentralized public spending. Ann. Reg. Sci. 2019, 62, 247–264. [Google Scholar] [CrossRef]

- Flick, W.A. Environmental repercussions and the economic structure: An input-output approach: A comment. Rev. Econ. Stat. 1974, 56, 107–109. [Google Scholar] [CrossRef]

- De Borger, B.; Kerstens, K.; Moesen, W.; Vanneste, J. Explaining differences in productive efficiency: An application to Belgian municipalities. Public Choice 1994, 80, 339–358. [Google Scholar] [CrossRef]

- Li, J.; Li, X.M.; Liu, Z.Q. Evaluation and analysis of urban ecological environment based on urbanization development system. China Popul. Resour. Environ. 2009, 19, 156–161. [Google Scholar]

- Liu, B.X.; Wang, B.S.; Xue, G. Efficiency evaluation of local government environmental pollution control in China—Based on three-stage bootstrapped DEA method. J. Zhongnan Univ. Econ. Law 2016, 1, 89–95, 160. [Google Scholar]

- Zeng, X.G. Regional environmental efficiency and its influencing factors in China. Econ. Theor. Bus. Manag. 2011, 10, 103–110. [Google Scholar]

- Chen, M. Does fiscal decentralization increase the efficiency of government environmental governance—Evidence from 31 provinces in China. Contemp. Econ. Manag. 2014, 36, 66–71. [Google Scholar]

- Luo, L.Q.; Guo, X.L.A. study on the win-win balance between provincial environmental protection and economic development in China—Based on the perspective of environmental efficiency. Sci. Technol. Prog. Policy 2016, 33, 40–47. [Google Scholar]

- Rong, J.B.; Yan, L.J.; Huang, S.R.; Zhang, G. Environmental efficiency assessment of Western China under carbon emission constraints. Chin. J. Appl. Ecol. 2015, 26, 1821–1830. [Google Scholar]

- Yuan, H.; Xiu, F.D.; Zhu, C.N.; Jin, N.; Bai, L.Y. Spatial temporal pattern and influencing factors of industrial environmental efficiency in Jiangsu Province. Geogr. Geo-Inf. Sci. 2017, 33, 112–118. [Google Scholar]

- Han, J.; Meng, D.A. Spatial effect of fiscal decentralization on ecological environment: Empirical data from provincial panel. Publ. Fin. Res. 2018, 3, 71–77. [Google Scholar]

- Tone, K. A slacks-based measure of super-efficiency in data envelopment analysis. Eur. J. Oper. Res. 2002, 143, 32–41. [Google Scholar] [CrossRef] [Green Version]

- Gao, J.; Qiao, G.M. Performance evaluation of environmental protection expenditure of provincial local governments Window-SBM three stages model based on pm2.5 bad output. J. Soochow Univ. 2019, 40, 103–111. [Google Scholar]

- Zhang, Y.B.; Ma, C.; Jin, P.Z. The environmental regulation investment efficiency evaluation and its influencing factors analysis of china based on the SBM—TOBIT model of panel data. Econ. Manag. 2014, 36, 171–180. [Google Scholar]

- Niu, T.; Zhao, S.G. An empirical study of the relationship between urban environmental infrastructure investment and economic growth. Urban Stud. 2010, 17, 128–131. [Google Scholar]

- Sun, Y.; Wang, Y.K.; Yao, X.D. Study on environmental benefits evaluation of urban public infrastructure. China Popul. Resour. Environ. 2015, 25, 92–100. [Google Scholar]

- He, X.G.; Wang, Z.L. Energy biased technology progress and green growth transformation: An empirical analysis based on 33 industries of China. China Ind. Econ. 2015, 32, 50–62. [Google Scholar]

- Meng, W.S.; Zhang, Y. Natural resource endowment, path selection of technological progress, and green economic growth: An empirical research based on China’s provincial panel data. Resour. Sci. 2020, 42, 2314–2327. [Google Scholar]

- Wang, P.; Xie, L.W. Pollution control investment, enterprise technical innovation and pollution control efficiency. China Popul. Resour. Environ. 2014, 24, 51–58. [Google Scholar]

- York, R.; Rosa, E.A.; Dietz, T. STIRPAT, IPAT and IMPACT: Analytic Tools for Unpacking the Driving Forces of Environmental Impacts. Ecol. Econ. 2003, 46, 351–365. [Google Scholar] [CrossRef]

- Ge, X.; Zhou, Z.; Zhou, Y.; Ye, X.; Liu, S. A Spatial Panel Data Analysis of Economic Growth, Urbanization and NOx Emissions in China. Int. J. Environ. Res. Public Health 2018, 15, 725. [Google Scholar] [CrossRef] [Green Version]

- Chen, H.; Jia, B.; Lau, S.S.Y. Sustainable urban form for Chinese compact cities: Challenges of a rapid urbanized economy. Habitat Int. 2008, 32, 28–40. [Google Scholar] [CrossRef]

- Liddle, B. Demographic dynamics and per capita environmental impact: Using panel regressions and household decompositions to examine population and transport. Popul. Environ. 2004, 26, 23–39. [Google Scholar] [CrossRef]

- Chen, S.M.; He, L.Y. Environment, Health, and Economic Growth: Optimal Allocation of Energy Tax Revenue. Econ. Res. 2017, 52, 120–134. [Google Scholar]

- Schwartz, J.; Repetto, R. Nonseparable Utility and the Double Dividend Debate: Reconsidering the Tax-Interaction Effect. Environ. Res. Econom. 2000, 15, 149–157. [Google Scholar] [CrossRef]

- Pautrel, X. Pollution and life expectancy: How environmental policy can promote growth. Ecol. Econ. 2009, 68, 1040–1051. [Google Scholar] [CrossRef] [Green Version]

- Marlin, J.T. Accounting for pollution. J. Account 1973, 2, 41–46. [Google Scholar]

- Hoehn, J.P.; Randall, A. A satisfactory benefit cost indicator from contingent valuation. J. Environ. Econ. Manag. 1987, 14, 1226–1247. [Google Scholar] [CrossRef]

- Freeman, A.M., III. The Measurement of Environmental and Resource Values: Theory and Methods; Resources for the Future Press: Washington, DC, USA, 2003. [Google Scholar]

- Xu, J.L. On the problems of resource assets management. Macroeconomics 2005, 1, 34–37. [Google Scholar]

- Beams, F.A.; Fertig, P.E. Pollution control through social cost conversion. J. Account. 1971, 132, 37–42. [Google Scholar]

- Xu, L.; Liu, N.; Zhang, K. Study on the Efficiency of Converting Local Government Economics and Resource Assets to Environmental Liabilities under the Fiscal Restraint: An Empirical Analysis Based on Panel Data of the Sample of Chinese 29 Provinces from 2009 to 2013. Chin. Soft Sci. 2016, 30, 36–42. [Google Scholar]

- Wan, J.X. Performance analysis of China’s budget expenditure on economic growth, resource consumption and environmental protection. Publ. Fin. Res. 2015, 3, 6–10. [Google Scholar]

- Anselin, L. Spatial Econometrics: Methods and Models; Springer: Dordrecht, The Netherlands, 1988. [Google Scholar]

- Getis, A.; Ord, J.K. The Analysis of Spatial Association by Use of Distance Statistics. Geog. Anal. 2010, 24, 127–145. [Google Scholar]

- Anselin, L. Local indicators of spatial association—LISA. Geog. Anal. 1995, 27, 93–115. [Google Scholar] [CrossRef]

- Mátyás, L.; Sevestre, P. (Eds.) The Econometrics of Panel Data: Fundamentals and Recent Developments in Theory and Practice; Advanced Studies in Theoretical and Applied Econometrics; Springer: Berlin/Heidelberg, Germany, 2008; Volume 46. [Google Scholar]

- Huang, J.H.; Yang, X.G.; Hu, Y. Coordination degree and uncoordinated sources of resources, environment and economy—Based on CREE-EIE analysis framework. Chin. Ind. Econ. 2014, 7, 17–30. [Google Scholar]

- Bai, X.J.; Wang, H.F.; Yan, W.K. Resource recession, science and education support and urban transformation—Research on the transformation efficiency of resource-based cities based on the bad output dynamic SBM model. Chin. Ind. Econ. 2014, 11, 30–43. [Google Scholar]

- Liu, H.; Ma, W.; Qian, J.; Cai, J.; Ye, X.; Li, J.; Wang, X. Effect of urbanization on the urban meteorology and air pollution in Hangzhou. J. Meteorol. Res. 2015, 29, 950–965. [Google Scholar] [CrossRef]

- Chen, S.M.; He, L.Y. Environment, health and economic growth: Optimal energy tax income distribution. Econ. Res. J. 2017, 52, 120–134. [Google Scholar]

- Jiang, Y.; Zhu, X. Economic growth and infrastructure construction in China. Bus Rev. 2004, 9, 57–62, 64. [Google Scholar]

- Grossman, G.M.; Krueger, A.B. Environmental Impacts of a North American Free Trade Agreement; National Bureau of Economic Research: Cambridge, MA, USA, 1991; Available online: https://www.nber.org/papers/w3914 (accessed on 28 August 2019).

- Panayotou, T. Empirical Tests and Policy Analysis of Environmental Degradation at Different Stages of Economic Development; No. 992927783402676; International Labour Organization: Geneva, Switzerland, 1993. [Google Scholar]

- Yin, J.; Zheng, M.; Chen, J. The effects of environmental regulation and technical progress on CO2 Kuznets curve: An evidence from China. Energy Policy 2015, 77, 97–108. [Google Scholar] [CrossRef]

- Shao, L. Empirical Analysis on the Impact of Population, Economic Output, Economic Structure and Technological Progress on China’s SO_2 Emissions: Based on Extension of the Grossman Pollution Equation. Stat. Inf. Forum 2011, 26, 45–51. [Google Scholar]

- Davis, I.S. Explaining changes in global sulfur emissions: An econometric decomposition approach. Ecol. Econ. 2002, 42, 201–220. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Index Category | Index | Description |

|---|---|---|---|

| Input indicators | Economic assets | X1 | Industrial pollution control investment completed |

| Resource assets | X2 | Afforestation area | |

| X3 | Groundwater supply | ||

| Desirable outputs | Pollution control | Y1 | Reduced sulfur dioxide emissions |

| Y2 | Reduced NOx emissions | ||

| Y3 | Reduced discharge of chemical oxygen demand in wastewater | ||

| Y4 | Volume of industrial solid waste disposal | ||

| Undesirable output | Environmental protection expenditure | Z | Local government environmental protection expenditure |

| DMU | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Average | Rank |

|---|---|---|---|---|---|---|---|---|

| Beijing | 0.0249 | 0.0258 | 0.0284 | 0.0301 | 0.0627 | 0.0235 | 0.0326 | 29 |

| Tianjin | 0.0193 | 0.0249 | 0.0248 | 0.0496 | 1.1646 | 0.0497 | 0.2222 | 22 |

| Hebei | 0.1288 | 1.0493 | 1.0079 | 0.2027 | 0.7319 | 0.1340 | 0.5424 | 8 |

| Shanxi | 0.1095 | 0.1337 | 0.1614 | 0.6824 | 1.1338 | 1.0636 | 0.5474 | 7 |

| Inner Mongolia | 0.0349 | 0.0639 | 0.0536 | 0.0387 | 0.8382 | 0.0697 | 0.1832 | 24 |

| Liaoning | 0.5094 | 0.3425 | 0.2047 | 1.0678 | 1.4383 | 0.0301 | 0.5988 | 5 |

| Jilin | 0.0966 | 0.1014 | 0.0656 | 0.0736 | 1.9820 | 1.0592 | 0.5631 | 6 |

| Heilongjiang | 0.0283 | 0.0727 | 0.0597 | 0.0852 | 1.0304 | 0.1800 | 0.2427 | 19 |

| Shanghai | 0.4909 | 0.6587 | 1.1444 | 0.4386 | 1.8587 | 1.0857 | 0.9462 | 1 |

| Jiangsu | 0.1963 | 0.1681 | 0.1495 | 0.1870 | 0.6566 | 0.0224 | 0.2300 | 20 |

| Zhejiang | 0.3275 | 0.2314 | 0.2086 | 0.2643 | 1.5961 | 0.3602 | 0.4980 | 9 |

| Anhui | 0.0702 | 0.0842 | 0.0562 | 0.0626 | 0.5967 | 0.0042 | 0.1457 | 27 |

| Fujian | 0.1971 | 0.1676 | 0.0960 | 0.1742 | 0.9426 | 1.0789 | 0.4427 | 10 |

| Jiangxi | 0.1381 | 0.0565 | 0.1259 | 0.0488 | 1.0709 | 0.3590 | 0.2999 | 16 |

| Shandong | 0.1049 | 0.1051 | 0.0867 | 0.0550 | 0.3197 | 0.0293 | 0.1168 | 28 |

| Henan | 0.1256 | 0.0789 | 0.0978 | 0.0722 | 0.6594 | 0.0671 | 0.1835 | 23 |

| Hubei | 0.1548 | 0.1584 | 0.1326 | 0.2603 | 1.0569 | 0.0071 | 0.2950 | 17 |

| Hunan | 0.2236 | 0.0379 | 0.1040 | 0.1378 | 1.0529 | 0.1673 | 0.2872 | 18 |

| Guangdong | 0.2245 | 0.1952 | 0.1705 | 0.1457 | 1.0001 | 0.0836 | 0.3033 | 15 |

| Guangxi | 0.0563 | 0.0738 | 0.0740 | 0.2321 | 1.0005 | 0.4811 | 0.3196 | 14 |

| Hainan | 0.0675 | 0.0779 | 0.0268 | 0.0430 | 1.1883 | 1.0466 | 0.4083 | 11 |

| Chongqing | 0.2260 | 0.2073 | 0.1445 | 0.1681 | 1.2488 | 0.0896 | 0.3474 | 13 |

| Sichuan | 1.0020 | 0.4470 | 1.0091 | 0.2486 | 1.0799 | 0.0151 | 0.6336 | 4 |

| Guizhou | 1.1708 | 0.2522 | 1.0506 | 0.2519 | 1.0457 | 0.3401 | 0.6852 | 3 |

| Yunnan | 0.1339 | 1.0037 | 0.3096 | 0.4203 | 1.0496 | 1.2370 | 0.6923 | 2 |

| Xizang | 0.0111 | 0.0023 | 0.0032 | 0.0605 | 0.0035 | 0.0168 | 0.0162 | 31 |

| Shanxi | 0.1117 | 0.0917 | 0.0811 | 0.0822 | 0.5190 | 0.0528 | 0.1564 | 26 |

| Gansu | 0.0573 | 0.0583 | 0.0436 | 0.0413 | 1.0152 | 0.1375 | 0.2255 | 21 |

| Qinghai | 0.0184 | 0.0141 | 0.0081 | 0.0094 | 0.0055 | 0.0631 | 0.0198 | 30 |

| Ningxia | 0.0650 | 0.1559 | 0.0626 | 0.1992 | 1.2223 | 0.6030 | 0.3847 | 12 |

| Xinjiang | 0.0384 | 0.0393 | 0.0137 | 0.0580 | 0.5891 | 0.3534 | 0.1820 | 25 |

| Average | 0.1988 | 0.1994 | 0.2195 | 0.1900 | 0.9406 | 0.3326 |

| Quadrant | Aggregate Type | Meaning | Spatial Correlation |

|---|---|---|---|

| First quadrant | (H,H) | Area with a high assets and environmental liabilities conversion rate surrounded by areas with high conversion rates | Positive correlation |

| Second quadrant | (L,H) | Area with a low assets and environmental liabilities conversion rate surrounded by areas with high conversion rates | Negative correlation |

| Third quadrant | (L,L) | Area with a low assets and environmental liabilities conversion rate surrounded by areas with low conversion rates | Negative correlation |

| Fourth quadrant | (H,L) | Area with a high assets and environmental liabilities conversion rate surrounded by areas with low conversion rates | Positive correlation |

| Variable | Index | Description |

|---|---|---|

| Regional economic development | AGDP | Per capita GDP |

| Urban environment infrastructure | INE | Urban environmental infrastructure construction investment |

| Provincial technological innovation | ARD | Provincial R&D investment |

| Urbanization | URB | Urban population proportion |

| Resource tax | TY | Resource tax amount |

| Variable | Regression Coefficient | p-Value |

|---|---|---|

| ρ | 0.167968 | 0.000000 *** |

| LnURB | 1.003195 | 0.000000 *** |

| LnTY | −1.177954 | 0.092769 * |

| LnINE | −0.057654 | 0.035989 ** |

| LnAGDP | 0.002469 | 0.8796 |

| LnARD | 0.016775 | 0.086342 * |

| R2 | 0.8993 | |

| LogL | 164.36316 | |

| LM-Test | 50.5341 | 0.000 *** |

| Robust LM-Test | 10.7978 | 0.001 *** |

| Variable | Regression Coefficient | p-Value |

|---|---|---|

| λ | 0.552995 | 0.000000 *** |

| LnURB | 1.002554 | 0.000000 *** |

| LnTY | −1.239060 | 0.111760 |

| LnINE | 0.033583 | 0.268458 |

| LnAGDP | 0.005421 | 0.7538 |

| LnARD | 0.004629 | 0.625861 |

| R2 | 0.8764 | |

| LogL | 178.67727 | |

| LM-Test | 123.4819 | 0.000 *** |

| Robust LM-Test | 83.7456 | 0.000 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, X.; Xia, W.; Huang, Y.; Li, M.; Wan, W. Evolution of the Spatial Pattern of the Assets and Environmental Liabilities Conversion Rate and Its Influencing Factors. Sustainability 2021, 13, 9164. https://doi.org/10.3390/su13169164

Chen X, Xia W, Huang Y, Li M, Wan W. Evolution of the Spatial Pattern of the Assets and Environmental Liabilities Conversion Rate and Its Influencing Factors. Sustainability. 2021; 13(16):9164. https://doi.org/10.3390/su13169164

Chicago/Turabian StyleChen, Xiaofang, Wenlei Xia, Yuan Huang, Mingze Li, and Wei Wan. 2021. "Evolution of the Spatial Pattern of the Assets and Environmental Liabilities Conversion Rate and Its Influencing Factors" Sustainability 13, no. 16: 9164. https://doi.org/10.3390/su13169164

APA StyleChen, X., Xia, W., Huang, Y., Li, M., & Wan, W. (2021). Evolution of the Spatial Pattern of the Assets and Environmental Liabilities Conversion Rate and Its Influencing Factors. Sustainability, 13(16), 9164. https://doi.org/10.3390/su13169164