Financial Literacy and Sustainable Consumer Behavior

Abstract

1. Introduction

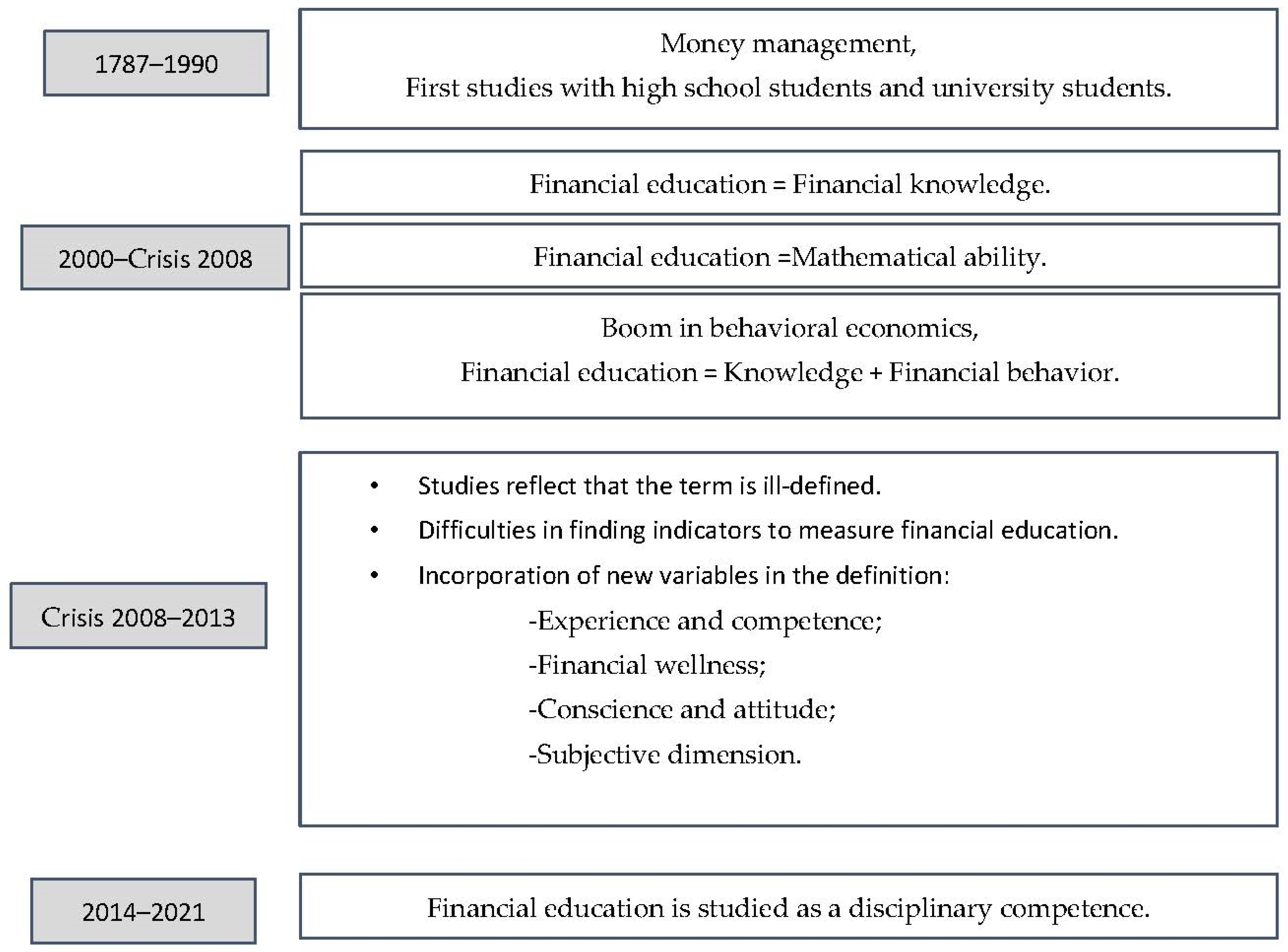

2. Literature Review and Research Assumptions

3. Methods and Data Collection

3.1. Methods

3.2. Data Collection

4. Empirical Analysis and Results

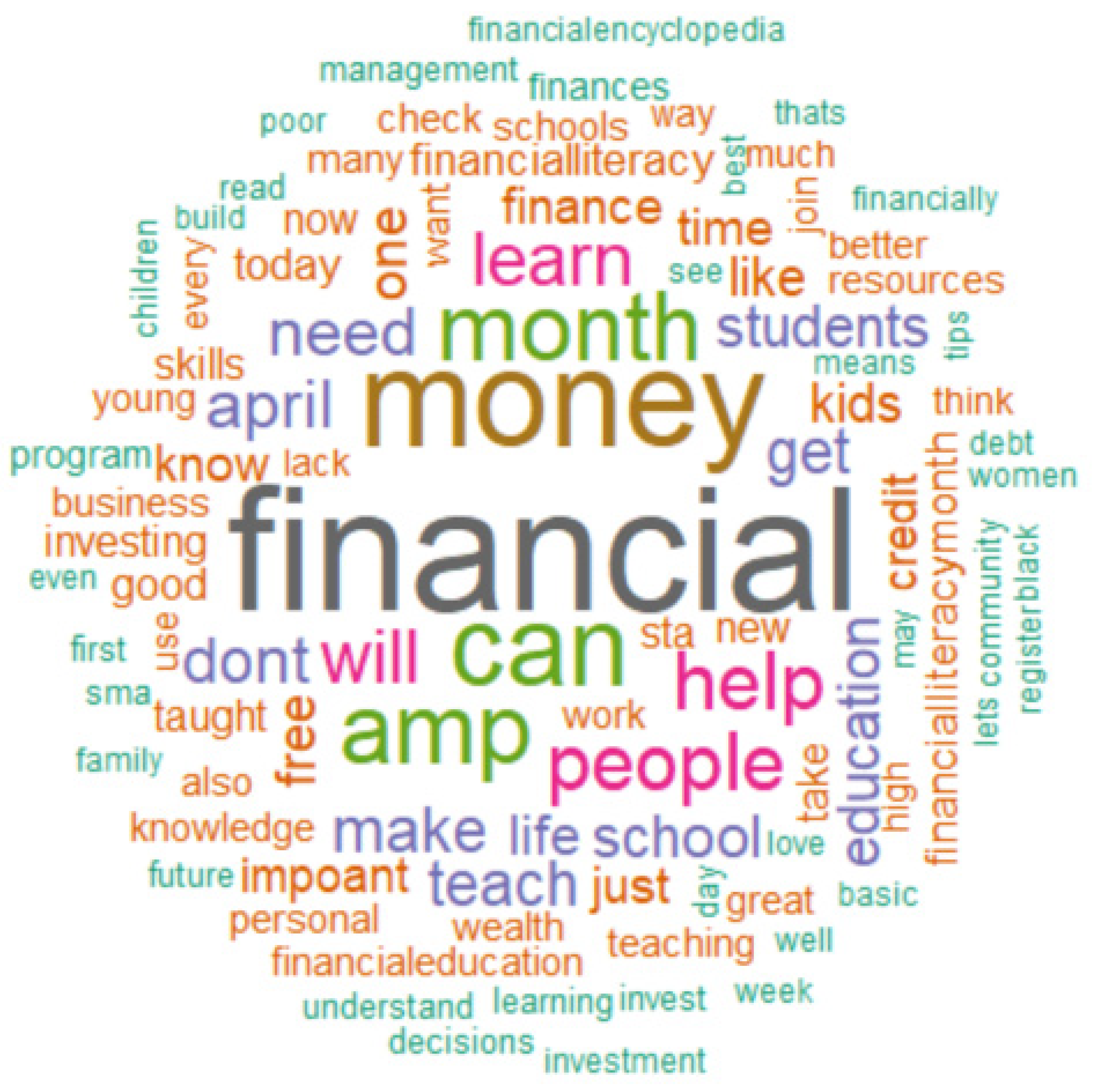

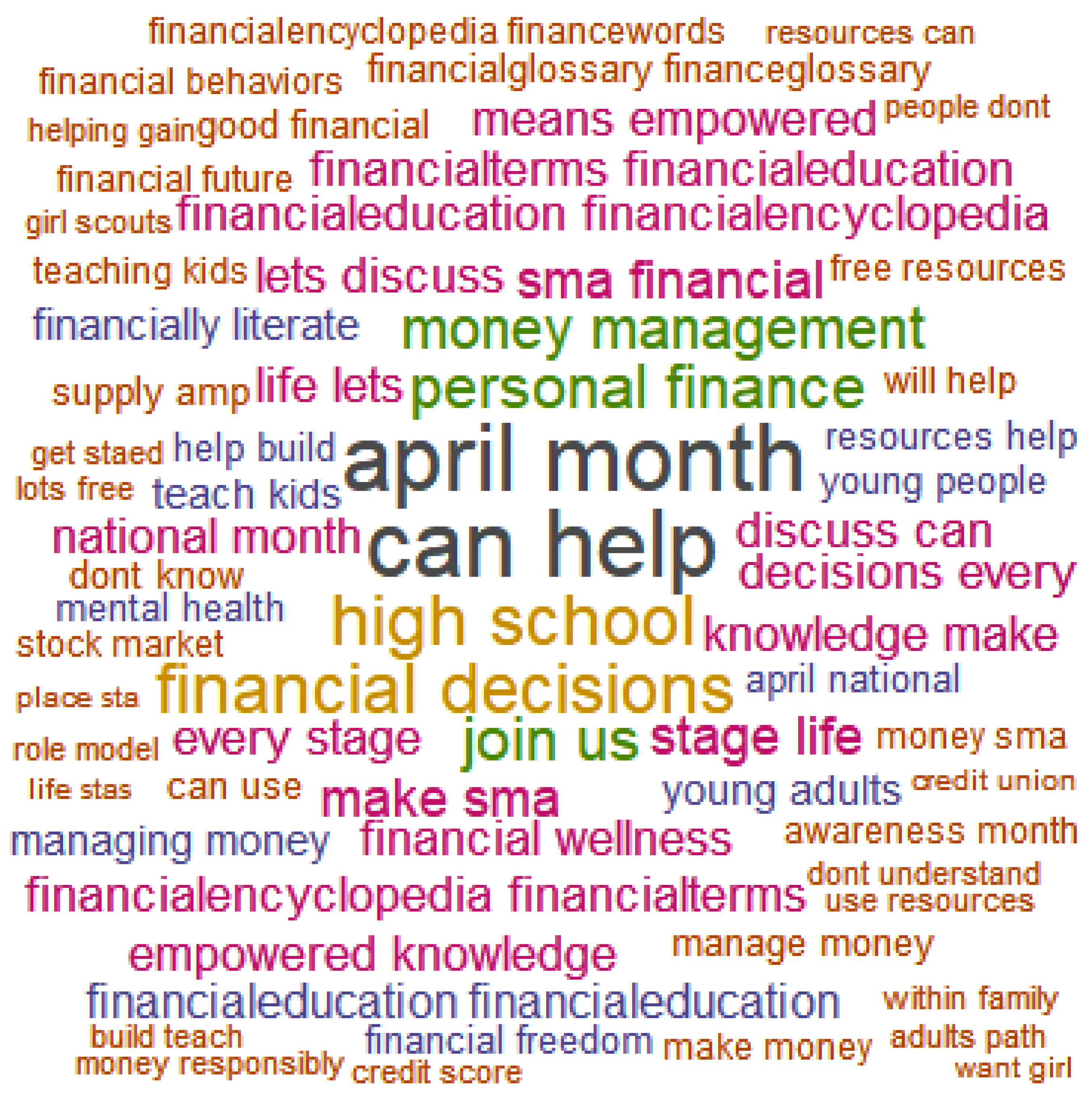

4.1. NLP Analysis

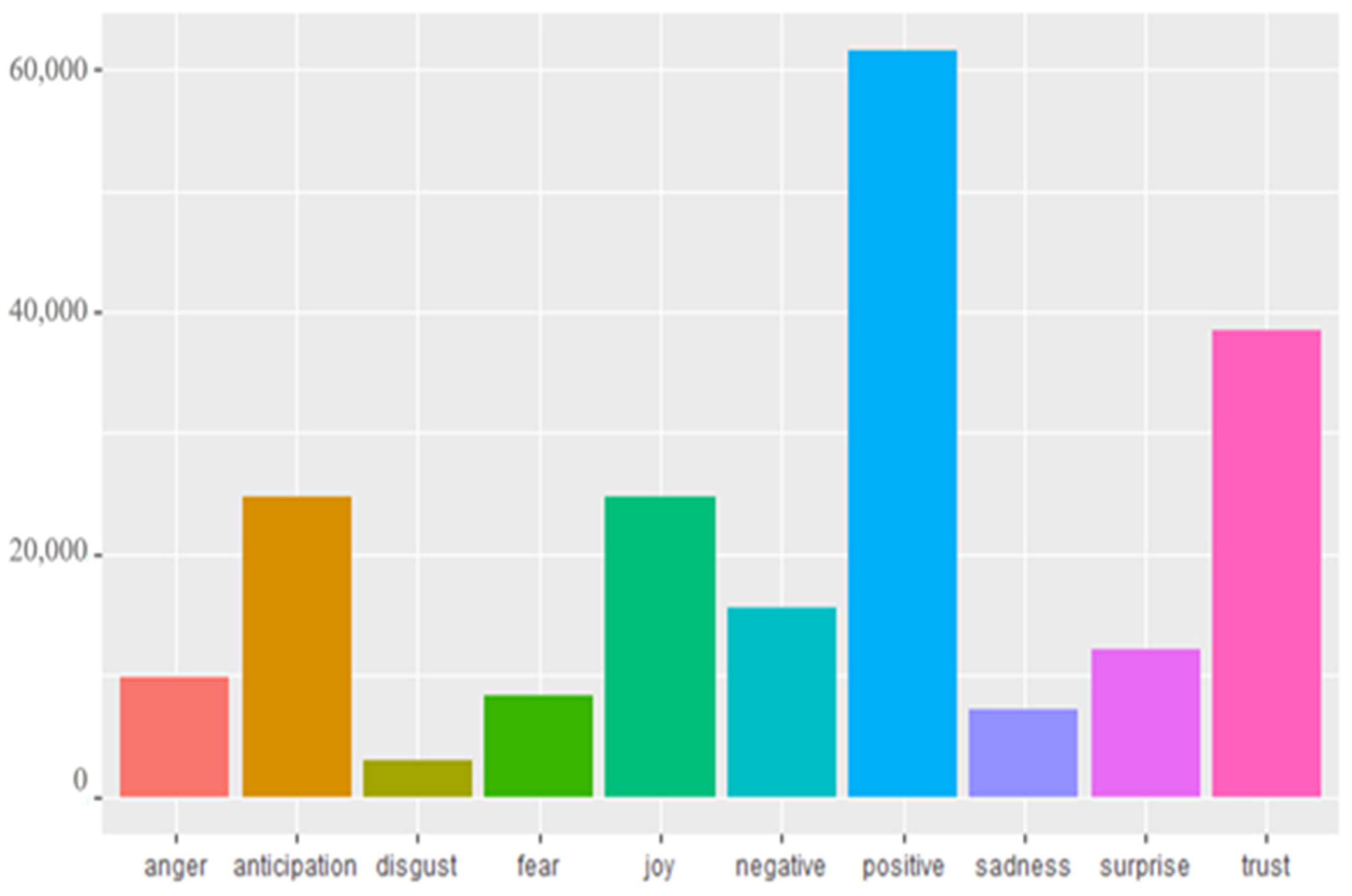

4.2. Analysis of Sentiments

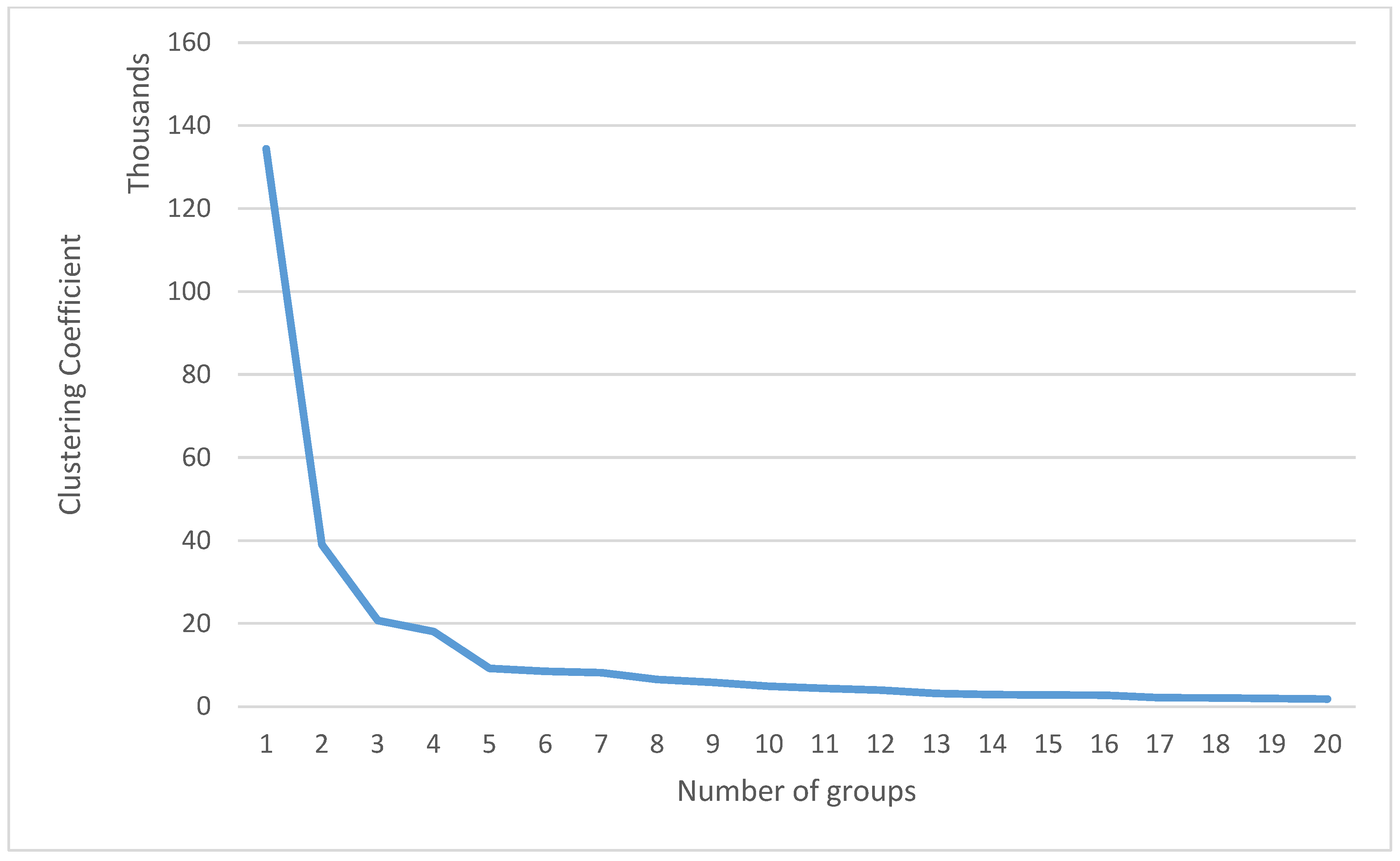

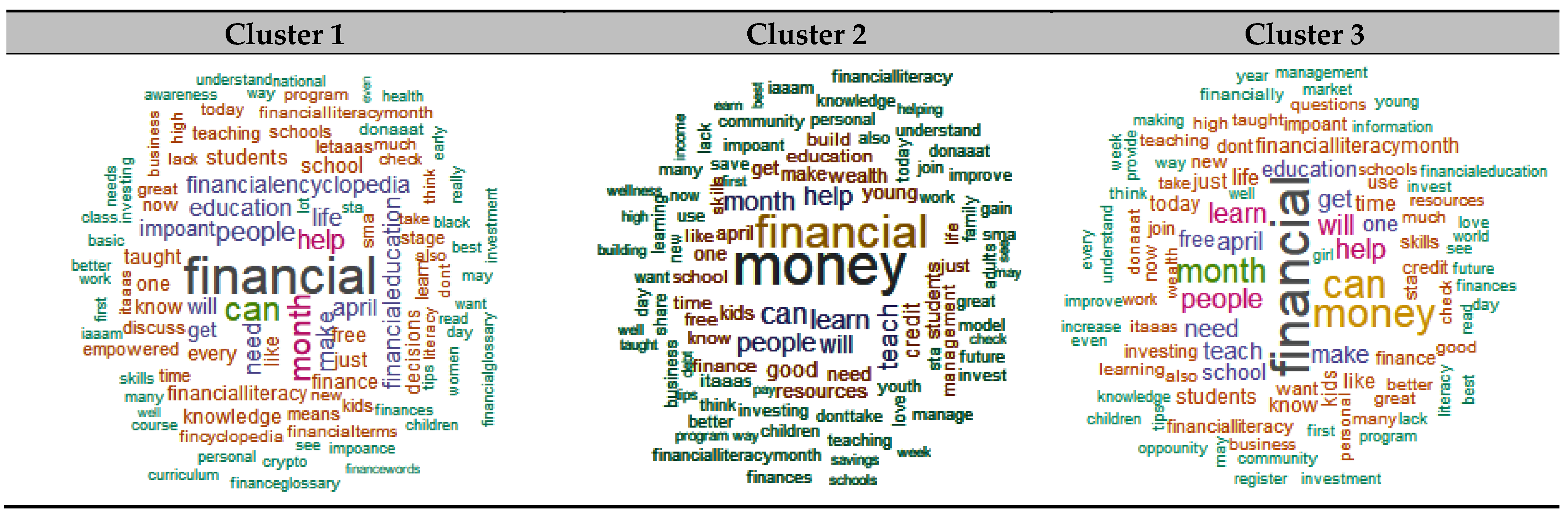

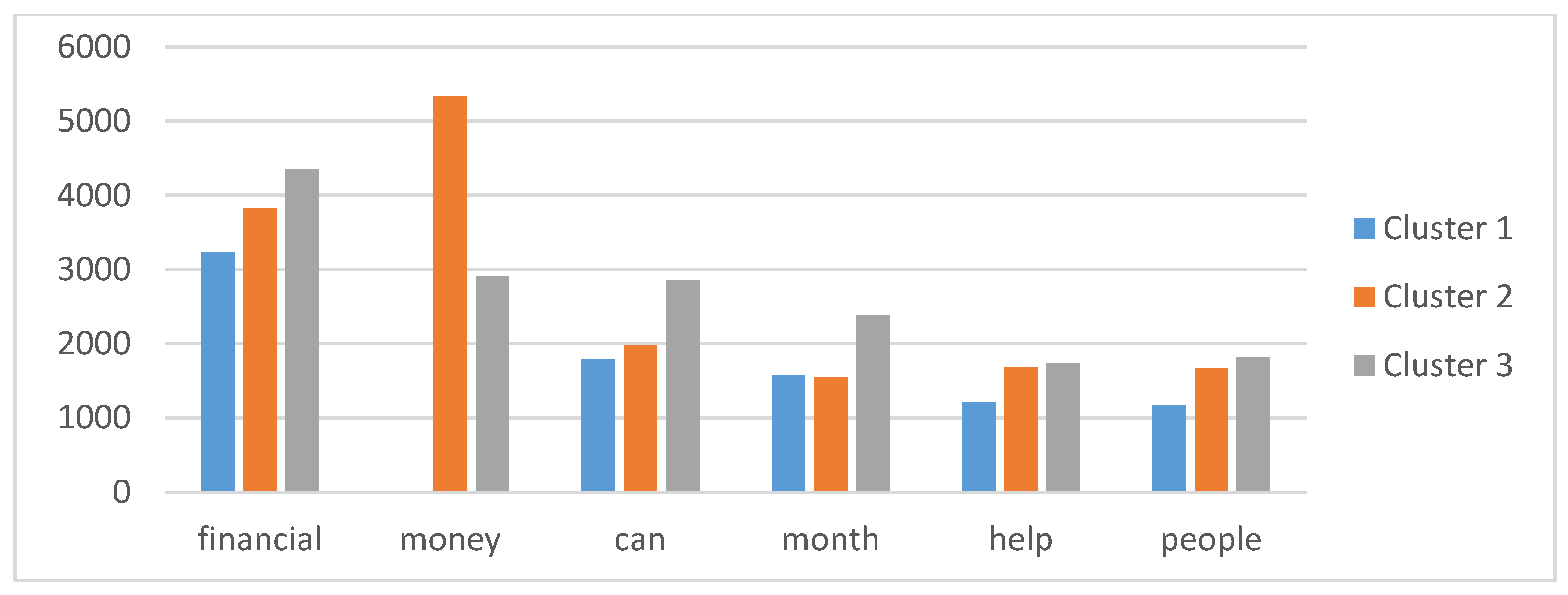

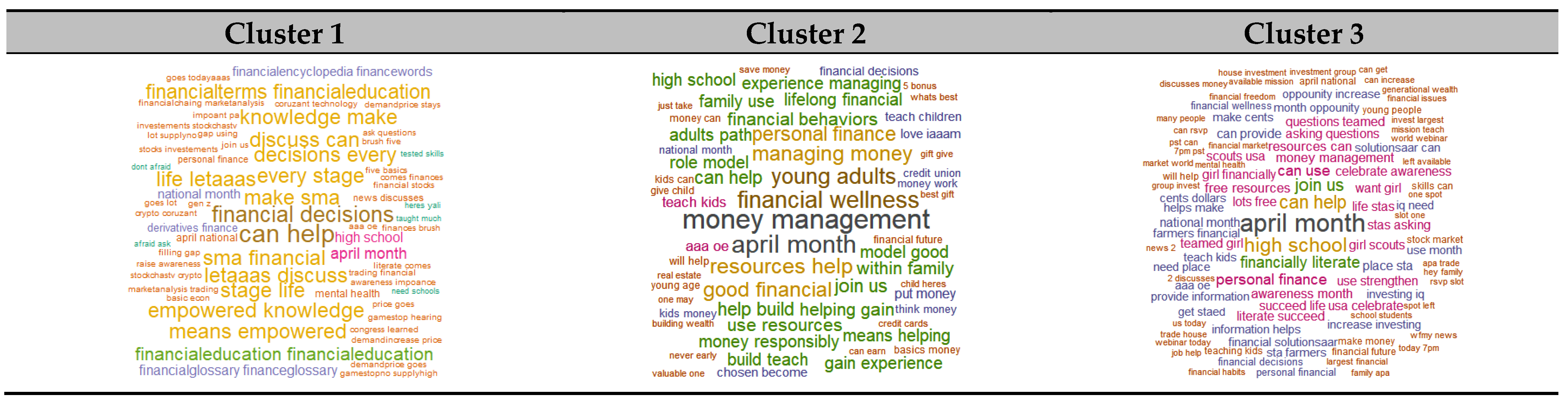

4.3. Cluster Analysis

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| John Adams (1787) | All the perplexities, confusion and distress in America arise not from defects in their Constitution or Confederation, nor from want of honor or virtue, so much as downright ignorance of the nature of coin, credit, and circulation. |

| Noctor M, Stoney S, Stradling R (1992) | Financial literacy as the decision-making ability regarding money management. Defined the term, “the ability to make informed judgments and to take effective decisions regarding the use and management of money |

| Moore DL (2003) | Financial knowledge, experiences, and behaviors are linked in a relational way. Financial experiences and behaviors together contribute to financial knowledge levels and gains in competency. Key to this assumption is the idea that with more experience and education, individuals become more sophisticated and competent in their financial dealings. |

| OCDE (2005) | The process by which financial consumers/investors improve their understanding of financial products and concepts and, through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, to make informed choices, to know where to go for help, and to take other effective actions to improve their financial well-being. |

| Widdowson D, Hailwood K (2007) | Financial literacy includes basic computation ability, understanding the yields and risks of financial decisions, familiarity with basic financial management concepts, knowing the channels for consultation and assistance, and the ability to understand the content of suggestions |

| Mandell L (2007) | The ability to evaluate the new and complex financial instruments and make informed judgments in both choice of instruments and extent of use that would be in their own best long-run interest. |

| Lusardi A, Mitchell OS. (2008) | Knowledge of basic financial concepts, such as the working of interest compounding, the difference between nominal and real values, and the basics of risk diversification. The ability to make simple decisions regarding debt contracts, in particular how one applies basic knowledge about interest compounding, measured in the context of everyday financial choices. |

| Hung A, Parker AM, Yoong J (2009) | Knowledge of basic economic and financial concepts, and the ability to use that knowledge and other financial skills to manage financial resources effectively for a lifetime of financial wellbeing |

| Mandell L (2009) | Financial literacy generally refers to the ability of consumers to make financial decisions in their own best short- and long-term interests. |

| Huston SJ (2010) | Financial literacy education, which is aimed at improving a person’s level of knowledge and/or ability, can and should be tailored to suit different demographics, life stages and learning styles—certainly not as a one-size-fits-all approach. Thus, it is important to clearly differentiate financial literacy from financial literacy education. Financial literacy has an additional application dimension which implies that an individual must have the ability and confidence to use his/her financial knowledge to make financial decisions. |

| Remund DL (2010) | Financial literacy is a measure of the degree to which one understands key financial concepts and possesses the ability and confidence to manage personal finances through appropriate, short-term decision making and sound, long-range financial planning, while mindful of life events and changing economic conditions |

| Lusardi A, Mitchell OS (2011) | The knowledge of basic financial concepts and ability to do simple calculations. |

| Atkinson A, Messy F (2012) | Financial literacy is a combination of knowledge, attitude and behavior. Financial literacy is a combination of awareness, knowledge, skill, attitude and behavior necessary to make sound financial decisions and ultimately achieve individual financial wellbeing |

| OECD, 2014 | Knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life. |

| Xiao JJ, Chen C, Sun L (2015) | Financial literacy can be categorized as objective or subjective. Objective financial literacy refers to consumers’ actual financial knowledge, usually measured by scores of financial quizzes. Subjective financial literacy is the financial knowledge level self-evaluated by consumers themselves. Both objective and subjective financial literacy factors were used to predict financial behavior |

| Paiella M (2016) | Financial literacy is the ability to collect important information, and also differentiate between diverse financial options, discussing financial issues, planning and proficiently answer that affect financial decision making. |

| Firli A (2017) | Financial literacy is a conceptual model containing six basic components: (1) Saving Borrowings; (2) Personal Budgeting; (3) Economic Issues; (4) Financial Concepts; (5) Financial Services; (6) Investing. |

| Kasman M, Heuberger B, Hammond RA (2018) | Financial literacy as a construct that reflects dynamic relationships between knowledge, skills, behavior, and other relevant factors |

| Hanson TA, Olson PM (2018) | Financial literacy has been shown to affect a wide range of financial behavior; therefore, understanding methods to improve financial literacy is vital for improving financial outcomes in personal finance. |

| Kadoya Y, Khan MSR (2020) | Financial literacy means understanding the value of money and how to maximize the benefits of money utilization. |

| OCDE (2020) | Combination of awareness, knowledge, skills, attitudes and behaviors necessary to make good financial decisions and, ultimately, achieve individual financial well-being. |

References

- Krechovská, M. Financial Literacy as a Path to Sustainability; 2015; Available online: http://www.fek.zcu.cz/tvp/doc/2015-2.pdf (accessed on 13 August 2021).

- Kadoya, Y.; Khan, M.S.R. Financial Literacy in Japan: New Evidence Using Financial Knowledge, Behavior, and Attitude. Sustainability 2020, 12, 3683. [Google Scholar] [CrossRef]

- Hira, T.K. Promoting sustainable financial behaviour: Implications for education and research. Int. J. Consum. Stud. 2012, 36, 502–507. [Google Scholar] [CrossRef]

- Zait, A.; Bertea, P.E. Financial literacy–Conceptual definition and proposed approach for a measurement instrument. J. Account. Manag. 2015, 4, 37–42. [Google Scholar]

- Allgood, S.; Walstad, W. Financial literacy and credit card behaviors: A cross-sectional analysis by age. Numeracy 2013, 6, 1–26. [Google Scholar] [CrossRef]

- Knoll, M.A.Z.; Houts, C. The Financial Knowledge Scale: An Application of Item Response Theory to the Assessment of Financial Literacy. J. Consum. Aff. 2012, 46, 381–410. [Google Scholar] [CrossRef]

- Li, X. When financial literacy meets textual analysis: A conceptual review. J. Behav. Exp. Finance 2020, 28, 100402. [Google Scholar] [CrossRef]

- Fernandes, D.; Lynch, J.G., Jr.; Netemeyer, R.G. Financial literacy, financial education, and downstream financial behaviors. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Martínez, M.L.C.; Aragón, P. Twitter, del sondeo a la sonda: Nuevos canales de opinión, nuevos métodos de análisis. Más Poder Local 2012, 12, 50–56. [Google Scholar]

- Garay Anaya, G. Las finanzas conductuales, el alfabetismo financiero y su impacto en la toma de decisiones financieras, el bienestar económico y la felicidad. Rev. Perspect. 2015, 36, 7–34. [Google Scholar]

- Sanfey, A.G.; Loewenstein, G.; McClure, S.M.; Cohen, J.D. Neuroeconomics: Cross-currents in research on decision-making. Trends Cogn. Sci. 2006, 10, 108–116. [Google Scholar] [CrossRef] [PubMed]

- Zahera, S.A.; Bansal, R. Do investors exhibit behavioral biases in investment decision making? A systematic review. Qual. Res. Financ. Mark. 2018, 10, 210–251. [Google Scholar] [CrossRef]

- Hilgert, M.A.; Hogarth, J.M.; Beverly, S.G. Household financial management: The connection between knowledge and behavior. Fed. Res. Bull. 2003, 89, 309. [Google Scholar]

- Bakken, M.R. Money Management Understanding of Tenth Grade Students. Master’s Thesis, University of Alberta, Edmonton, AB, Canada, 1966. [Google Scholar]

- Danes, S.M.; Hira, T.K. Money Management Knowledge of College. J. Stud. Financ. Aid 1987, 17, 1. [Google Scholar]

- Bernheim, B.D.; Garrett, D.; Maki, D. Education and saving:: The long-term effects of high school financial curriculum mandates. J. Public Econ. 2001, 80, 435–465. [Google Scholar] [CrossRef]

- Noctor, M.; Stoney, S.; Stradling, R. Financial Literacy: A Discussion of Concepts and Competencies of Financial Literacy and Opportunities for Its Introduction into Young People’s Learning (Report Prepared for the National Westminster Bank); National Foundation for Education Research: London, UK, 1992. [Google Scholar]

- Ouachani, S.; Belhassine, O.; Kammoun, A. Measuring financial literacy: A literature review. Manag. Finance 2020, 47, 266–281. [Google Scholar] [CrossRef]

- Chen, H.; Volpe, R.P. An analysis of personal financial literacy among college students. Financ. Serv. Rev. 1998, 7, 107–128. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Planning and Financial Literacy: How Do Women Fare? Am. Econ. Rev. 2008, 98, 413–417. [Google Scholar] [CrossRef]

- Huston, S.J. Measuring Financial Literacy. J. Consum. Aff. 2010, 44, 296–316. [Google Scholar] [CrossRef]

- Huang, J.; Nam, Y.; Sherraden, M.S. Financial Knowledge and Child Development Account Policy: A Test of Financial Capability. J. Consum. Aff. 2012, 47, 1–26. [Google Scholar] [CrossRef]

- Hogarth, J.M.; Hilgert, M.A. Financial knowledge, experience and learning preferences: Preliminary results from a new survey on financial literacy. Consum. Interest Annu. 2002, 48, 1–7. [Google Scholar]

- Muñoz-Murillo, M.; Álvarez-Franco, P.B.; Restrepo-Tobón, D.A. The role of cognitive abilities on financial literacy: New experimental evidence. J. Behav. Exp. Econ. 2020, 84, 101482. [Google Scholar] [CrossRef]

- Mason, C.; Wilson, R. Conceptualising financial literacy. Occas. Pap. 2000, 1–42. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1028.5352&rep=rep1&type=pdf (accessed on 4 July 2021).

- Kahneman, D.; Smith, V. Foundations of behavioral and experimental economics. Nobel Prize. Econ. Doc. 2002, 1, 1–25. [Google Scholar]

- Moore, D.L. Survey of Financial Literacy in Washington State: Knowledge, Behavior, Attitudes, and Experiences; Washington State Department of Financial Institutions: Olympia, WA, USA, 2003. [CrossRef]

- Brüggen, E.C.; Hogreve, J.; Holmlund, M.; Kabadayi, S.; Löfgren, M. Financial well-being: A conceptualization and research agenda. J. Bus. Res. 2017, 79, 228–237. [Google Scholar] [CrossRef]

- Worthington, A.C. Predicting Financial Literacy in Australia. Wollongon, Australia, 2006. Available online: https://ro.uow.edu.au/cgi/viewcontent.cgi?article=1124&context=commpapers (accessed on 13 August 2021).

- Widdowson, D.; Hailwood, K. Financial literacy and its role in promoting a sound financial system. Reserve Bank N. Z. Bull. 2007, 70, 37. [Google Scholar]

- Lusardi, A.; Mitchell, O.S. Financial literacy around the world: An overview. J. Pension-Econ. Finance 2011, 10, 497–508. [Google Scholar] [CrossRef]

- Huhmann, B.A.; McQuitty, S. A model of consumer financial numeracy. Int. J. Bank Mark. 2009, 27, 270–293. [Google Scholar] [CrossRef]

- Paiella, M. Financial literacy and subjective expectations questions: A validation exercise. Res. Econ. 2016, 70, 360–374. [Google Scholar] [CrossRef]

- Krische, S.D. Individual Investors’ Financial Literacy and Numerical Skills. Contemp. Account. Res. 2014. [Google Scholar] [CrossRef]

- Mandell, L. Financial Education in High School; University of Chicago Press: Chicago, IL, USA, 2013; pp. 257–279. [Google Scholar]

- Norvilitis, J.; Szablicki, P.B.; Wilson, S.D. Factors Influencing Levels of Credit-Card Debt in College Students1. J. Appl. Soc. Psychol. 2003, 33, 935–947. [Google Scholar] [CrossRef]

- Žižek, S. A permanent economic emergency. New Left Rev. 2010, 64, 85–95. [Google Scholar]

- Altman, E.I.; Sabato, G.; Wilson, N. The value of non-financial information in SME risk management. J. Crédit. Risk 2010, 6, 95–127. [Google Scholar] [CrossRef]

- Altman, M. Implications of behavioural economics for financial literacy and public policy. J. Socio-Econ. 2012, 41, 677–690. [Google Scholar] [CrossRef]

- Hung, A.A.; Parker, A.M.; Yoong, J. Defining and Measuring Financial Literacy. 2009. Available online: https://www.rand.org/pubs/working_papers/WR708.html (accessed on 13 August 2021).

- Remund, D.L. Financial Literacy Explicated: The Case for a Clearer Definition in an Increasingly Complex Economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Atkinson, A.; Messy, F. Measuring financial literacy: Results of the OECD/International Network on Financial Education (INFE) pilot study. Meas. Financ. Lit. 2012. [Google Scholar] [CrossRef]

- De Beckker, K.; De Witte, K.; Van Campenhout, G. Financial Literacy—A Cross Country Analysis. 2017. Available online: https://onlinelibrary.wiley.com/doi/10.1111/ijcs.12534. (accessed on 13 August 2021).

- Compen, B.; De Witte, K.; Schelfhout, W. The role of teacher professional development in financial literacy education: A systematic literature review. Educ. Res. Rev. 2019, 26, 16–31. [Google Scholar] [CrossRef]

- Allgood, S.; Walstad, W. The effects of perceived and actual financial knowledge on credit card behavior. Netw. Financ. Inst. Work. Pap. 2011, 15, 1–26. [Google Scholar] [CrossRef][Green Version]

- Xiao, J.J.; Chen, C.; Sun, L. Age differences in consumer financial capability. Int. J. Consum. Stud. 2015, 39, 387–395. [Google Scholar] [CrossRef]

- Thaler, R.H.; Sunstein, C.R.; Balz, J.P. Choice architecture. Behav. Found. Public Policy 2013. Available online: https://www.degruyter.com/document/doi/10.1515/9781400845347-029/html (accessed on 13 August 2021).

- Thomson, S. Financing the Future: Australian Students’ Results in the PISA 2012 Financial Literacy Assessment. 2014. Available online: https://research.acer.edu.au/ozpisa/16/ (accessed on 13 August 2021).

- Firli, A. Factors that Influence Financial Literacy: A Conceptual Framework. IOP Conf. Ser. Mater. Sci. Eng. 2017, 180, 12254. [Google Scholar] [CrossRef]

- Kasman, M.; Heuberger, B.; Hammond, R.A. A Review of Large Scale Youth Financial Literacy Education Policies and Programs; The Brookings Institution, 2018; Available online: https://www.brookings.edu/wp-content/uploads/2018/10/ES_20181001_Financial-Literacy-Review.pdf (accessed on 13 August 2021).

- Rai, K.; Dua, S.; Yadav, M. Association of Financial Attitude, Financial Behaviour and Financial Knowledge Towards Financial Literacy: A Structural Equation Modeling Approach. FIIB Bus. Rev. 2019, 8, 51–60. [Google Scholar] [CrossRef]

- Hanson, T.A.; Olson, P.M. Financial literacy, and family communication patterns. J. Behav. Exp. Financ. 2018, 19, 64–71. [Google Scholar] [CrossRef]

- Behrman, J.R.; Mitchell, O.S.; Soo, C.K.; Bravo, D. How financial literacy affects household wealth accumulation. Am. Econ. Rev. 2012, 102, 300–304. [Google Scholar] [CrossRef] [PubMed]

- Lusardi, A.; Samek, A.; Kapteyn, A.; Glinert, L.; Hung, A.; Heinberg, A. Visual tools and narratives: New ways to improve financial literacy. J. Pension-Econ. Finance 2017, 16, 297–323. Available online: https://www.cambridge.org/core/journals/journal-of-pension-economics-and-finance/article/abs/visual-tools-and-narratives-new-ways-to-improve-financial-literacy/6CA7426CF88099809C1460076C8357CD (accessed on 13 August 2021). [CrossRef]

- Sivaramakrishnan, S.; Srivastava, M.; Rastogi, A. Attitudinal factors, financial literacy, and stock market participation. Int. J. Bank Mark. 2017, 35, 818–841. [Google Scholar] [CrossRef]

- Deuflhard, F.; Georgarakos, D.; Inderst, R. Financial Literacy and Savings Account Returns. J. Eur. Econ. Assoc. 2018, 17, 131–164. [Google Scholar] [CrossRef]

- Duca, J.V.; Kumar, A. Financial literacy and mortgage equity withdrawals. J. Urban Econ. 2014, 80, 62–75. [Google Scholar] [CrossRef]

- Serido, J.; Shim, S.; Tang, C. A developmental model of financial capability: A framework for promoting a successful transition to adulthood. Int. J. Behav. Dev. 2013, 37, 287–297. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Klapper, L.; Singer, D. Financial Inclusion, and Inclusive Growth: A Review of Recent Empirical Evidence. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2958542 (accessed on 13 August 2021).

- Ingale, K.K.; Paluri, R.A. Financial literacy and financial behaviour: A bibliometric analysis. Rev. Behav. Financ. 2020. ahead-of-print. [Google Scholar] [CrossRef]

- Goyal, K.; Kumar, S. Financial literacy: A systematic review and bibliometric analysis. Int. J. Consum. Stud. 2021, 45, 80–105. [Google Scholar] [CrossRef]

- Lim, W.M. A blueprint for sustainability marketing: Defining its conceptual boundaries for progress. Mark. Theory 2016, 16, 232–249. [Google Scholar] [CrossRef]

- Lim, W.M. Inside the sustainable consumption theoretical toolbox: Critical concepts for sustainability, consumption, and marketing. J. Bus. Res. 2017, 78, 69–80. [Google Scholar] [CrossRef]

- Williams, S.A.; Terras, M.; Warwick, C. What do people study when they study Twitter? Classifying Twitter related academic papers. J. Doc. 2013, 69, 384–410. [Google Scholar] [CrossRef]

- Bakshy, E.; Hofman, J.M.; Mason, W.A.; Watts, D.J. Everyone’s an influencer: Quantifying influence on twitter. In Proceedings of the Fourth ACM International Conference on Web Search and Data Mining—WSDM ’11, Hong Kong, China, 9–12 February 2011; pp. 65–74. [Google Scholar]

- Luke, D. A User’s Guide to Network Analysis in R; Springer Science and Business Media LLC: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Mariani, J.; Francopoulo, G.; Paroubek, P.; Vernier, F. The NLP4NLP Corpus (II): 50 Years of Research in Speech and Language Processing. Front. Res. Metrics Anal. 2019, 3, 37. [Google Scholar] [CrossRef]

- Kaptein, R. Learning to Analyze Relevancy and Polarity of Tweets. CEUR Workshop Proceedings-CLEF (Online Working Notes/Labs/Workshop). 2012. Available online: http://ceur-ws.org/Vol-1178/CLEF2012wn-RepLab-Kaptein2012.pdf (accessed on 13 August 2021).

- Ahuja, V.; Shakeel, M. Twitter Presence of Jet Airways-Deriving Customer Insights Using Netmography and Wordclouds. Procedia Comput. Sci. 2017, 122, 17–24. [Google Scholar] [CrossRef]

- Haddaway, N.R. The use of web-scraping software in searching for grey literature. Grey J. 2015, 11, 186–190. [Google Scholar]

- Bhuta, S.; Doshi, A.; Doshi, U.; Narvekar, M. A review of techniques for sentiment analysis Of Twitter data. In Proceedings of the 2014 International Conference on Issues and Challenges in Intelligent Computing Techniques (ICICT), Ghaziabad, India, 7–8 February 2014; pp. 583–591. [Google Scholar]

- Taboada, M.; Brooke, J.; Tofiloski, M.; Voll, K.; Stede, M. Lexicon-based methods for sentiment analysis. Comput. Linguist. 2011, 37, 267–307. [Google Scholar] [CrossRef]

- Mohammad, S.M.; Turney, P.D. NRC Emotion Lexicon; Institute for Ocean Technology: Nova Scotia, ON, Canada, 2013. [Google Scholar]

- Mohammad, S.M. Practical and ethical considerations in the effective use of emotion and sentiment lexicons. arXiv 2020, arXiv:2011.03492. [Google Scholar]

- Ali, R.S.H.; El Gayar, N. Sentiment Analysis using Unlabeled Email data. In Proceedings of the 2019 International Conference on Computational Intelligence and Knowledge Economy (ICCIKE), Amity University Dubai, Dubai, United Arab Emirates, 11–12 December 2019; pp. 328–333. [Google Scholar] [CrossRef]

- Coletta, L.F.; da Silva, N.F.; Hruschka, E.R.; Hruschka, E.R. Combining classification and clustering for tweet sentiment analysis. In Proceedings of the 2014 Brazilian Conference on Intelligent Systems, Sao Paulo, Brazil, 18–22 October 2014; pp. 210–215. [Google Scholar]

- Gupta, S.; Banerjee, B. Unsupervised Event Detection Using Self-learning-based Max-margin Clustering: Analysis on Streaming Tweets. IETE J. Res. 2018, 66, 569–578. [Google Scholar] [CrossRef]

- Rehioui, H.; Idrissi, A. New Clustering Algorithms for Twitter Sentiment Analysis. IEEE Syst. J. 2020, 14, 530–537. [Google Scholar] [CrossRef]

- Burscher, B.; Vliegenthart, R.; de Vreese, C.H. Frames beyond words: Applying cluster and sentiment analysis to news coverage of the nuclear power issue. Soc. Sci. Comput. Rev. 2016, 34, 530–545. [Google Scholar] [CrossRef]

- Harakawa, R.; Takimura, S.; Ogawa, T.; Haseyama, M.; Iwahashi, M. Consensus Clustering of Tweet Networks via Semantic and Sentiment Similarity Estimation. IEEE Access 2019, 7, 116207–116217. [Google Scholar] [CrossRef]

- Garre, M.; Cuadrado, J.J.; Sicilia, M.A.; Rodríguez, D.; Rejas, R. Comparación de diferentes algoritmos de clustering en la estimación de coste en el desarrollo de software. REICIS. Rev. Española Innov. Calid. Ing. Softw. 2007, 3, 6–22. [Google Scholar]

- Fisher, D.H. Knowledge acquisition via incremental conceptual clustering. Mach. Learn. 1987, 2, 139–172. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Análisis Multivariante; Prentice Hall Madrid: Madrid, Spain, 1999. [Google Scholar]

- Searle, S.R.; Casella, G.; McCulloch, C.E. Variance Components; Wiley Series in Probability and Statistics: Hoboken, NJ, USA, 1992. [Google Scholar]

- Subactagin-Matto, A.; Goncalves-Rorke, M. Improving the Fiscal Fitness of Young Adults: Translating Knowledge into Action. JANZSSA 2010, 35, 45–54. [Google Scholar]

- Lusardi, A.; Mitchell, O.S. Financial Literacy and Planning: Implications for Retirement Wellbeing. 2006. Available online: https://www.researchgate.net/publication/4878786_Financial_Literacy_and_Planning_Implications_for_Retirement_Wellbeing (accessed on 13 August 2021).

- Campbell, J.Y. Household Finance. J. Financ. 2006, 61, 1553–1604. [Google Scholar] [CrossRef]

- Ameliawati, M.; Setiyani, R. The Influence of Financial Attitude, Financial Socialization, and Financial Experience to Financial Management Behavior with Financial Literacy as the Mediation Variable. KnE Soc. Sci. 2018, 3, 811–832. [Google Scholar] [CrossRef]

- Anderson, J.; Richard, H.; Thaler, C.R. Nudge: Improving Decisions about Health, Wealth, and Happiness. Econ. Philos. 2010, 26, 369. [Google Scholar] [CrossRef]

- Gómez, F. Educación Financiera: Retos y Lecciones a Partir de Experiencias Representativas en el Mundo. 2009. Available online: http://repositorioproyectocapital.com/wp-content/uploads/2018/02/En-breve-10-educacion-financiera-retos-lecciones-2009-spa.pdf (accessed on 13 August 2021).

- Taylor, M.A.; Geldhauser, H.A. Low-income older workers. In Aging and Work in the 21st Century; Lawrence Erlbaum Associates Publishers: Hillsdale, NJ, USA, 2007; pp. 25–50. [Google Scholar]

- Ispierto, A.; Martínez-García, I.; Ruiz Suárez, G.R. Educación Financiera y Decisiones de Ahorro e Inversión. un Análisis de la Encuesta de Competencias Financieras (ECF) (Financial Education and Savings and Investment Decisions: An Analysis of the Survey of Financial Competences (ECF)). 2021. Available online: https://www.cnmv.es/DocPortal/Publicaciones/MONOGRAFIAS/Encuesta_de_comp_financ_ES.pdf (accessed on 13 August 2021).

- Taft, M.K.; Hosein, Z.Z.; Mehrizi, S.M.T. The Relation between Financial Literacy, Financial Wellbeing and Financial Concerns. Int. J. Bus. Manag. 2013, 8, p63. [Google Scholar] [CrossRef]

- Goetzmann, W.N. Money Changes Everything; Princeton University Press: Princeton, NJ, USA, 2017. [Google Scholar]

- Zapata-Aguilar, A.; Cabrera-Ignacio, E.; Hernández-Arce, J.; Martínez-Morales, J. Educación financiera entre jóvenes universitarios: Una visión general. Educación 2016, 3, 1–8. [Google Scholar]

- Lusardi, A. Financial literacy: Do people know the ABCs of finance? Public Underst. Sci. 2015, 24, 260–271. [Google Scholar] [CrossRef] [PubMed]

- Grohmann, A.; Menkhoff, L. School, parents, and financial literacy shape future financial behavior. DIW Econ. Bull. 2015, 5, 407–412. [Google Scholar]

- Zaleskiewicz, T.; Traczyk, J. Emotions and Financial Decision Making, Psychological Perspectives on Financial Decision Making; Springer: Berlin/Heidelberg, Germany, 2020; pp. 107–133. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Date 14 March 2021 from 30 May 2021 | Weekly Download of Tweets | Accumulated Tweets |

|---|---|---|

| 14 March–21 March | 3916 | 3916 |

| 22 March–28 March | 4485 | 8401 |

| 29 March–4 April | 5346 | 13,747 |

| 5 April–11 April | 6410 | 20,157 |

| 12 April–18 April | 6216 | 26,373 |

| 19 April–25 April | 6166 | 32,539 |

| 26 April–2 May | 5994 | 38,533 |

| 3 May–9 May | 4617 | 43,150 |

| 10 May–16 May | 3481 | 46,631 |

| 17 May–23 May | 3458 | 50,089 |

| 24 May–30 May | 3730 | 53,819 |

| Stage | Combined Cluster | Coefficients | Cluster Coefficients | Number of Clusters | |

|---|---|---|---|---|---|

| Cluster 1 | Cluster 2 | ||||

| 1 | 53,811 | 53,819 | 0.000 | 0 | 1 |

| 2 | 53,798 | 53,818 | 0.000 | 0.000 | 2 |

| 3 | 34,849 | 53,817 | 0.000 | 0.000 | 3 |

| 4 | 51,557 | 53,816 | 0.000 | 0.000 | 4 |

| 5 | 34,844 | 53,815 | 0.000 | 0.000 | 5 |

| (53,793 skipped rows) | |||||

| 53,799 | 12 | 26 | 92,503.829 | 1820.381 | 20 |

| 53,800 | 37 | 87 | 94,407.402 | 1903.573 | 19 |

| 53,801 | 4 | 6 | 96,455.778 | 2048.375 | 18 |

| 53,802 | 14 | 25 | 98,588.518 | 2132.741 | 17 |

| 53,803 | 9 | 12 | 101,315.067 | 2726.549 | 16 |

| 53,804 | 1 | 2 | 104,068.079 | 2753.012 | 15 |

| 53,805 | 8 | 14 | 106,907.505 | 2839.426 | 14 |

| 53,806 | 27 | 359 | 110,061.445 | 3153.940 | 13 |

| 53,807 | 5 | 1554 | 114,020.362 | 3958.917 | 12 |

| 53,808 | 23 | 24 | 118,372.435 | 4352.074 | 11 |

| 53,809 | 1 | 15 | 123,234.197 | 4861.761 | 10 |

| 53,810 | 8 | 56 | 129,056.246 | 5822.049 | 9 |

| 53,811 | 8 | 20 | 135,559.716 | 6503.470 | 8 |

| 53,812 | 1 | 4 | 143,715.133 | 8155.417 | 7 |

| 53,813 | 9 | 37 | 152,199.658 | 8484.526 | 6 |

| 53,814 | 9 | 23 | 161,365.722 | 9166.063 | 5 |

| 53,815 | 8 | 27 | 179,420.814 | 18,055.093 | 4 |

| 53,816 | 5 | 8 | 200,134.650 | 20,713.835 | 3 |

| 53,817 | 1 | 9 | 239,150.698 | 39,016.049 | 2 |

| 53,818 | 1 | 5 | 373,583.953 | 134,433.255 | 1 |

| ANOVA | Cluster 1 | Cluster 2 | Cluster 3 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| gl | F | p-Valor | Average | Sd | Average | Sd | Average | Sd | |

| Anger | 2 | 4223.736 | 0 | 0.1 | 0.329 | 0.63 | 0.715 | 0.29 | 0.517 |

| Anticipation | 2 | 16,416.391 | 0 | 0.16 | 0.407 | 1.66 | 1.081 | 0.76 | 0.738 |

| Disgust | 2 | 435.238 | 0 | 0.06 | 0.249 | 0.17 | 0.452 | 0.1 | 0.314 |

| Fear | 2 | 1681.358 | 0 | 0.15 | 0.381 | 0.48 | 0.737 | 0.23 | 0.473 |

| Joy | 2 | 36,594.183 | 0 | 0.1 | 0.074 | 1.93 | 1.113 | 0.75 | 0.507 |

| Sadness | 2 | 833.411 | 0 | 0.15 | 0.388 | 0.38 | 0.706 | 0.22 | 0.470 |

| Surprise | 2 | 11,463.502 | 0 | 0.03 | 0.17 | 0.96 | 0.884 | 0.37 | 0.515 |

| Trust | 2 | 22,458.211 | 0 | 0.32 | 0.563 | 2.42 | 1.236 | 1.24 | 0.887 |

| Negative | 2 | 792.458 | 0 | 0.37 | 0.679 | 0.72 | 1.098 | 0.46 | 0.704 |

| Positive | 2 | 55,068.906 | 0 | 0.44 | 0.524 | 3.91 | 1.473 | 1.98 | 0.800 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Muñoz-Céspedes, E.; Ibar-Alonso, R.; de Lorenzo Ros, S. Financial Literacy and Sustainable Consumer Behavior. Sustainability 2021, 13, 9145. https://doi.org/10.3390/su13169145

Muñoz-Céspedes E, Ibar-Alonso R, de Lorenzo Ros S. Financial Literacy and Sustainable Consumer Behavior. Sustainability. 2021; 13(16):9145. https://doi.org/10.3390/su13169145

Chicago/Turabian StyleMuñoz-Céspedes, Ester, Raquel Ibar-Alonso, and Sara de Lorenzo Ros. 2021. "Financial Literacy and Sustainable Consumer Behavior" Sustainability 13, no. 16: 9145. https://doi.org/10.3390/su13169145

APA StyleMuñoz-Céspedes, E., Ibar-Alonso, R., & de Lorenzo Ros, S. (2021). Financial Literacy and Sustainable Consumer Behavior. Sustainability, 13(16), 9145. https://doi.org/10.3390/su13169145