Learning from Positive Impact Organizations: A Framework for Strategic Innovation

Abstract

:1. Introduction

2. Differentiating Sustainability Organizations from Traditional Firms

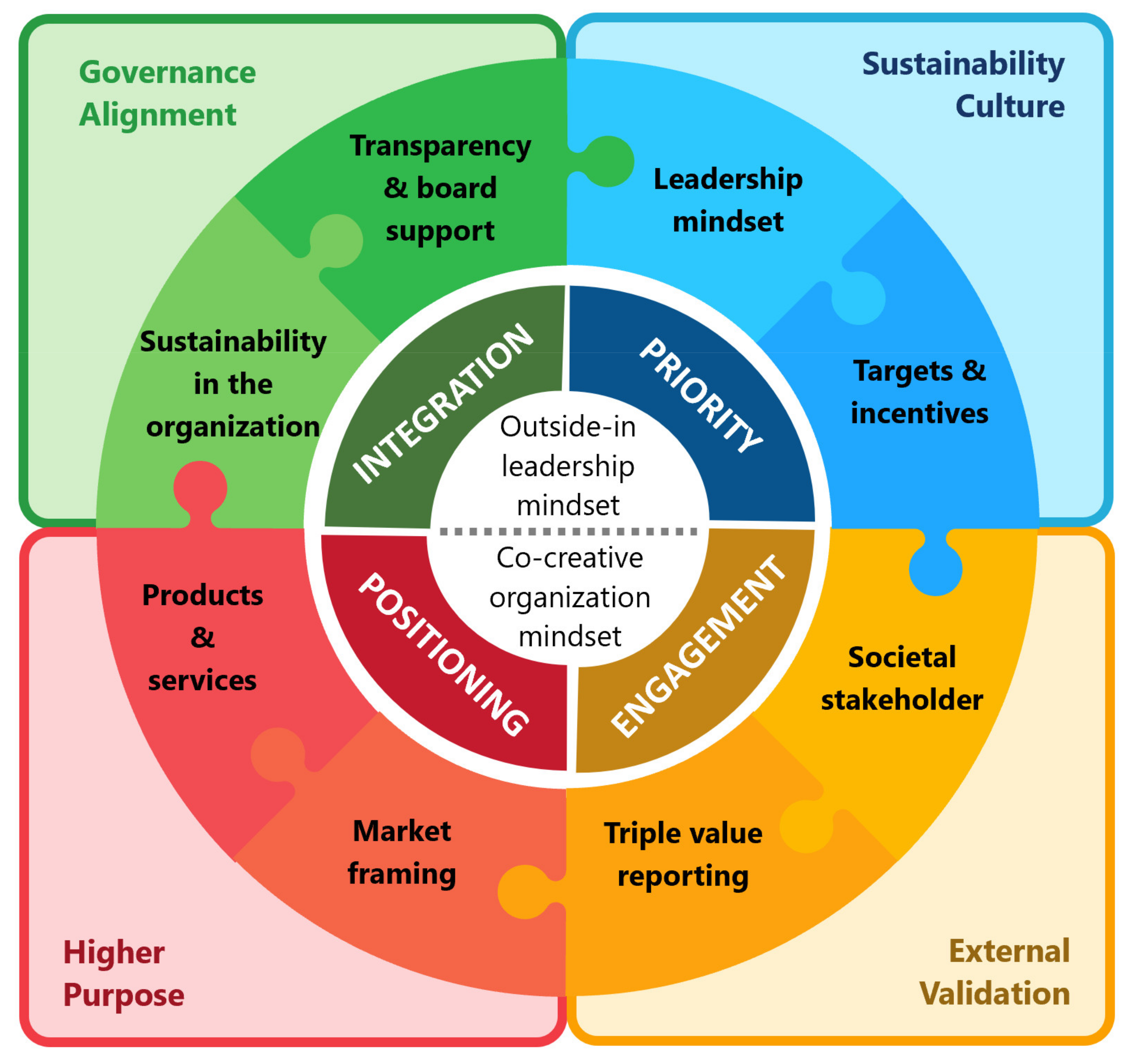

2.1. Governance Alignment

2.2. Sustainability Culture

2.3. External Validation

2.4. Higher Purpose

3. The Research Methodology

- (a)

- The suggestion of the required mindset shift from “inside-out” to “outside-in” so that an organization can become truly sustainable and hence create a positive impact;

- (b)

- The business sustainability typology (BST) which serve to determine the progressive steps in transforming from an early to advanced to true sustainability organization type;

- (c)

- The four identified strategic differentiators of Section 2 which serve as a basis for the Strategic Innovation Canvas.

3.1. Selecting the Case Study Organizations

3.2. Quantative Stakeholder Survey across Case Study Organizations

- -

- All truly sustainability companies (BST 3.0) scored significantly better than all early-stage sustainable companies (BST 1.0) companies across all survey questions, validating the BST types;

- -

- All small companies rated significantly better than large ones;

- -

- All services companies rated significantly better than manufacturing companies;

- -

- There are two strong predictors in transforming towards true business sustainability: leadership and external stakeholders.

3.3. Qualitative and Comparative Case Study Analysis

- -

- -

- -

- -

- -

- -

- -

- Furthermore, a single case study: Rhomberg is a small non-listed company in the building and construction sector in Austria. The case researcher was Urs von Arx [44].

3.4. Model Verification and Simplification

- (a)

- Two distinct mindset shifts associated with the two most significant predictors of success of achieving a positive impact transformation process;

- (b)

- A verified Positive Impact Framework allowing organizations to assess their progress;

- (c)

- The Strategic Innovation Canvas as a simplified tool for organizations to identify strategic innovation priorities to create a positive impact.

4. The Mindsets and Practices of Positive Impact Organizations

4.1. Two Mindset Shifts as Key Predictors of Success

- -

- The outside-in leadership mindset: Leaders who “gets it” have redefined their role and the role of the organization in society. They see themselves as one with the world around them and, hence, broaden their focus to serve the common good. Such leaders derive their purpose from providing a positive contribution to society and the planet, and by aligning their organizational processes to ensure the long-term well-being of the organization;

- -

- The co-creative organization mindset: An organization that excels in how it engages with its external stakeholders is externally oriented and open. Such an organization is able to work as fluently outside of its boundaries as across its internal departments or divisions. Experience of multi-stakeholder processes has shown that such organizations have successfully learned to work with stakeholders and players outside of its traditional boundaries. These organizations are able to effectively translate its positive impact purpose in practice by co-creating innovative solutions with external stakeholders [46].

- -

- The integration challenge of a governance alignment: organizations that have implemented alignment in governance are able to attract suitable investors and are likely to have a board that is more supportive of a progressive sustainability agenda. This makes it significantly easier to integrate sustainability deeply within the organization.

- -

- The priority challenge observed in the organizational culture: organizations with an advanced sustainability culture are inspired and led by a leader or a leadership team that gets the outside–in perspective of sustainability. Such organizations often attract employees who carry a desire to create positive impact in their hearts. Their compensation system is aligned with broader sustainability goals and the organization measures its ambitious sustainability goals. This priority ensures that in times of a crisis, the sustainability topic does not get put on the back-burner.

- -

- The engagement challenge to achieve a positive external validation: organizations that benefit from a positive external recognition of their sustainability efforts have learned to excel in how to engage with external stakeholders. Although traditional firms often consider external stakeholders are a potential danger and handle them with “silver gloves”, truly sustainable firms have learned their lessons in how to engage authentically with critical civil society players and how to integrate constructive external views in their operational decision-making processes. Such open stakeholder engagement becomes the source of entirely new “outside-in” ideas that the organization can translate into new business opportunities.

- -

- The positioning challenge to accomplish the organization’s higher purpose: such organizations have rewritten their purpose in a way to demonstrate their desire to create a positive impact for society and the planet. What differentiates advanced sustainability organizations from other firms with impact-oriented purpose statement is the fact that they have translated such a purpose into their products and services. They have reconsidered and identified markets which are relevant to them. Other firms have often not been able to make this translation from a lofty purpose to an amended or expanded product or service offering and they not only risk facing credibility issues but also cannot benefit from the opportunities such a new purpose potentially holds for them.

4.2. The Positive Impact Framework (PIF) for Measuring Progress

4.3. The Strategic Innovation Canvas (SIC) for Getting Started

4.4. Relevance to Practice

5. Contribution, limitations, and Further Research

5.1. Contribution

5.2. Limitations

5.3. Further Research

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- The leaders of this company have a clear vision for sustainability.

- The leaders of this company take a long-term view when making decisions.

- The leaders of this company have a clear business case for pursuing the goals of sustainability.

- The leaders of this company integrate sustainability into their decision-making.

- The leaders of this company are able to inspire others about sustainability-focused issues and initiatives.

- The leaders of this company are willing to take measured risks in pursuit of sustainability.

- The leaders of this company are knowledgeable of the issues pertaining to sustainability.

- The leaders of this company are personally committed to issues pertaining to sustainability.

- This company has embedded sustainability into the operating procedures and policies.

- This organization has an Enterprise-wide management system for sustainability.

- This company has integrated sustainability-related goals into the performance management system.

- Rewards and compensation are clearly linked to the organization’s sustainability goals.

- The level of trust within this organization is high.

- Most people in this company believe that a commitment to sustainability is essential to the company.

- Continual learning is a core focus of this organization.

- People in this organization are encouraged to learn more about sustainability from external sources.

- This organization rewards innovation.

- This company has a strong track record of implementing large-scale change successfully.

- This company has a strong track record for implementing incremental (small, continuous) change success.

- People in this company actively challenge the status quo.

- This company has a clear strategy for engaging all internal stakeholders in its sustainability efforts.

- By and large, people in this company are engaged in work that is connected to sustainability goals.

- Most employees believe that the organization values them and their contribution.

- This company has mechanisms in place to actively engage with external stakeholders about its sustainability.

- This company encourages sustainability in its supply chain.

- This company sends a clear and consistent message to external stakeholders about its commitment to sustainability.

References

- Meadows, D.H.; Randers, J.M.; Dennis, L. The Limits to Growth: The 30-Year Update; Chelsea Green Publishing Co: White River Junction, VT, USA, 2004. [Google Scholar]

- Michaelis, L. The role of business in sustainable consumption. J. Clean. Prod. 2003, 11, 915–921. [Google Scholar] [CrossRef]

- Jackson, T. Prosperity without growth. In Economics for a Finite Planet; Taylor & Francis: London, UK, 2011; p. 187. [Google Scholar]

- Muff, K.; Kapakla, A.; Dyllick, T. The Gapframe—Translating the SDGs into relevant national grand challenges for strategic business opportunities. Int. J. Manag. Educ. 2017, 15, 363–383. [Google Scholar] [CrossRef]

- Wiek, A.; Withycombe, L.; Redman, C.L. Key competencies in sustainability: A reference framework for academic program development. Sustain. Sci. 2011, 6, 203–218. [Google Scholar] [CrossRef] [Green Version]

- Russell, R. Leadership in the Decade of Action. 2020. Available online: https://www.russellreynolds.com/insights/thought-leadership/Documents/Leadership%20for%20the%20Decade%20of%20Action.pdf (accessed on 7 July 2020).

- Nagler, J. We Become What We Think—The Key Role of Mindsets in Human Development. International Science Council. Published Online. 2020. Available online: https://council.science/human-development/latest-contributions/we-become-what-we-think-the-key-role-of-mindsets-in-human-development/ (accessed on 13 August 2020).

- Colby, C.C. The Relationship between Product Design and Business Models in the Context of Sustainability. Master’s Thesis, University of Montreal, Montreal, QC, Canada, 2011. [Google Scholar]

- Landrum, N.E. Stages of Corporate Sustainability: Integrating the Strong Sustainability Worldview. Organ. Environ. 2018, 31, 287–313. [Google Scholar] [CrossRef]

- Dunphy, D.; Griffiths, A.; Benn, S. Organisational Change for Corporate Sustainability; Routledge: London, UK; New York, NY, USA, 2003. [Google Scholar]

- Adams, R.; Jeanrenaud, S.; Bessant, J.; Overy, P.; Denyer, D. Innovating for Sustainability—A Systematic Review of the Body of Knowledge. The Network for Business Sustainability (NBS). 2012. Available online: https://ore.exeter.ac.uk/repository/bitstream/handle/10036/4105/Adams%202012-%20NBS%20Systematic%20Review%20Innovation.pdf?sequence=8 (accessed on 3 August 2020).

- Dyllick, T.; Muff, K. Clarifying the meaning of sustainable business—Introducing a typology from business-as-usual to true business sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef] [Green Version]

- Muff, K.; Dyllick, T. An Organizational Roadmap of Business Sustainability. 2014. Available online: https://ssrn.com/abstract=2442211 (accessed on 30 April 2014).

- PWC/SAM. The Sustainability Yearbook; PWC/SAM: Zurich, Switzerland, 2006. [Google Scholar]

- Network for Business Sustainability (NBS). Definition of Business Sustainability. 2012. Available online: http://nbs.net/about/what-we-do/ (accessed on 30 November 2012).

- Eccles, R.G.; Ioannoui, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Schawbel, D. Unilever’s Paul Polman: Why Today’s Leaders Need to Commit to a Purpose. Forbes. 21 November 2017. Available online: https://www.forbes.com/sites/danschawbel/2017/11/21/paul-polman-why-todays-leaders-need-to-commit-to-a-purpose/ (accessed on 2 May 2019).

- Mackey, J.; Sisodia, R. Conscious. Capitalism; Harvard Business School Press: Boston, MA, USA, 2013. [Google Scholar]

- KPMG. The Road Ahead. The KPMG Survey of Corporate Responsibility Reporting 2017. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf (accessed on 5 June 2020).

- Bertels, S.; Papania, L.; Papania, D. Embedding Sustainability in Organizational Culture: A Systematic Review of the Body of Knowledge, Network for Business Sustainability. 2010. Available online: https://www.nbs.net/articles/systematic-review-organizational-culture (accessed on 3 January 2021).

- Miller Perkins, K. Leadership and Purpose: How to Create a Sustainable Culture; Routledge: Sheffield, UK, 2019. [Google Scholar]

- Miller Perkins, K. Sustainability: Culture and Leadership Assessment; Miller Consultants Inc.: Louisville, KY, USA, 2011; Available online: www.millerconsultants.com/sustainability.php (accessed on 21 July 2021).

- Grayson, D.; Coulter, C.; Lee, M. The Future of Business Leadership; Routledge: London, UK; New York, NY, USA, 2018. [Google Scholar]

- Pless, N.; Maak, T.; Waldman, D. Different Approaches toward Doing the Right Thing: Mapping the Responsibility Orientations of Leaders. Acad. Manag. Perspect. 2012, 4–12. [Google Scholar] [CrossRef]

- Dyllick, T.; Muff, K. Transitioning: What does sustainability for business really mean? And when is a business truly sustainable? In Sustainable Business: A One Planet. Approach; Jeanrenaud, S., Jeanrenaud, J.P., Gosling, J., Eds.; Wiley: Chichester, UK, 2017; pp. 381–407. [Google Scholar]

- Dyllick, T.; Rost, Z. Towards True Product Sustainability. J. Clean. Production 2017, 162, 346–360. [Google Scholar] [CrossRef]

- Business and Sustainable Development Commission. Better Business Better World. Presented at the World Economic Forum in January 2017. Available online: http://report.businesscommission.org/uploads/Executive-Summary.pdf (accessed on 1 May 2020).

- March, R.; The Positive Impact Scorecard. Standard & Poor’s. Published 15 April 2020. Available online: https://www.spglobal.com/marketintelligence/en/news-insights/blog/the-positive-impact-scorecard (accessed on 25 May 2020).

- Malnight, T.W.; Buche, I.; Dhanaraj, C. Put Purpose at the Core of Your Strategy—It’s How Successful Companies Redefine Their Businesses; Harvard Business Review; Joshua Macht: Baltimore, MD, USA, 2019; pp. 2–11. [Google Scholar]

- Yin, R.K. Case Study Research: Design and Methods; Applied Social Research Methods Series; Sage Publications: Newbury, CA, USA, 1989; Volume 34. [Google Scholar]

- Yin, R.K. Applications of Case Study Research; Applied Social Research Methods Series; Sage Publications: Newbury, CA, USA, 1993; Volume 34. [Google Scholar]

- Narbel, F. Alternative Bank Schweiz AG: A Banking Model for the Future. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Narbel, F. Merkur Cooperative Bank. In Award-Winning Case Studies 2019; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- Oguine, H. Blue Orchard: A Sustainability Case Study. In Award-Winning Case Studies 2019; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- Oguine, H. Meso Impact Finance: A Sustainability Case Study. In Award-Winning Case Studies 2019; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- Hashmi, G. Lancaster Hotel London: Glamour and sustainability: Thriving on a strong sustainability culture as a pioneer in hospitality. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Hashmi, G. Beechenhill Farm Hotel’s meaningful legacy: Evolving from the sustainability of business towards the business of sustainability in hospitality. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Gull, S. Interloop Limited: A journey from ethics to business sustainability. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Gull, S. Dynamic Sportswear Ltd.: Compliance or muddling through sustainability. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Bukhari, N. Pebbles (PVT) Ltd sustainable real estate develops: Building hope. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Bukhari, N. ICI Pakistan Ltd.: Sustainability through adversity. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Muff, K., Ed.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Luca, F. Journey to True Sustainability in the World Cosmetics Industry: The Business Case of Intercos Group. In Award-Winning Case Studies 2019; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- Luca, F. Successful Sustainability Strategy: Procter & Gamble Case. In Award-Winning Case Studies 2019; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- Von Arx, U. Rhomberg Bau: Sustainability makes sense. In Award-Winning Case Studies 2015; A Special Issue of Building Sustainable Legacies; Ionescu-Somers, A., Ed.; Taylor Francis: Sheffield, UK, 2019. [Google Scholar]

- WBCSD. World Business Council for Sustainable Development: Vision 2050—Time to Transform; WBCSD: Geneva, Switzerland, 2021; Available online: https://timetotransform.biz/ (accessed on 1 July 2021).

- Muff, K. Five Superpowers for Co-Creators—How Change Makers and Business Can. Achieve the Sustainable Development Goals; Routledge: Sheffield, UK, 2018. [Google Scholar]

- Rimanoczy, I. The Sustainability Mindset Principles—A Guide to Developing a Mindset for a Better World; Routledge: London, UK; New York, NY, USA, 2020. [Google Scholar]

- Flammer, C.; Bansal, P. Does a long-term orientation create value? Evidence from a regression discontinuity. Strateg. Manag. J. 2017, 38, 1827–1847. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Polman, P. Sustainability lessons from the front lines. MIT Sloan Management Review. Winter 2017, 58, 71–78. [Google Scholar]

- Mirvis, P.; Googins, B.K. Stages of Corporate Citizenship: A Developmental Framework. In The Center for Corporate Citizenship at Boston College. 2006. Available online: https://www.google.com/search?q=mirvis+and+googins+framework&sxsrf=ALeKk01SDOfwJyYFMQvU7u0FmqTtX (accessed on 21 July 2021).

- Muff, K. Verantwortungsvolle Unternehmensführung und die SDGS. In Verantwortungsvolle Unternehmensführung im österreichischen Mittelstand; Ortiz, D., Czuray, M., Scholz, M., Eds.; Springer Gabler: Wiesbaden, Germany, 2020; pp. 29–40. [Google Scholar]

- Woods, M. 93% of CEOs Believe Business Should Create Positive Impact Beyond Profit. The Young Presidents Organizations YPO. 24 January 2019. Available online: https://www.ypo.org/2019/01/93-of-ceos-believe-business-should-create-positive-impact-beyond-profit/ (accessed on 23 October 2019).

- Business Roundtable. Business Roundtable Redefines the Purpose of a Corporation to Promote ‘An Economy That Serves All Americans’. 19 September 2019. Available online: https://www.businessroundtable.org/business-roundtable-redefines-the-purpose-of-a-corporation-to-promote-an-economy-that-serves-all-americans (accessed on 23 October 2019).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| # | Company | Country | Author | BST Type | Year Founded | Ownership | Size | Industry |

|---|---|---|---|---|---|---|---|---|

| 1 | Alternative Bank Schweiz | Switzerland | F. Narbel | 3.0 Founded | 1990 | Not listed | small | Services |

| 2 | Beechenhill Farm Hotel | UK | G. Hashmi | 2.0 | 1984 | Not listed | small | Services |

| 3 | Blue Orchard | Switzerland | H. Oguine | 3.0 Founded | 2001 | Not listed | small | Services |

| 4 | Dynamic Sportswear | Pakistan | S. Gull | 1.0 | 1992 | Not listed | large | manufact. |

| 5 | ICI Pakistan | Pakistan | N. Burkhari | 1.0 | 1944 | Listed | large | manufact. |

| 6 | Intercos | Italy | F. Luca | 1.0 | 1972 | Listed | large | manufact. |

| 7 | Interloop Ltd. | Pakistan | S. Gull | 2.0 | 1992 | Unlisted public | large | manufact. |

| 8 | Lancaster London Hotel | UK | G. Hashmi | 3.0 Transf. | 1967 | Not listed | small | Services |

| 9 | Merkur Andelskasse | Denmark | F. Narbel | 3.0 Founded | 1982 | Not listed | small | Services |

| 10 | Meso Impact Finance | Luxem-bourg | H. Oguine | 3.0 Founded | 2012 | Not listed | small | Services |

| 11 | Pebbles Pvt | Pakistan | N. Burkhari | 3.0 Transf. | 2008 | Not listed | large | manufact. |

| 12 | Procter & Gamble | US | F. Luca | 1.0 | 1837 | Listed | large | manufact. |

| 13 | Rhomberg | Austria | U. von Arx | 3.0 Transf. | 1886 | Not listed | small | manufact. |

| Foundations | Research | Output |

|---|---|---|

| Mindset shift inside-out to outside-in | Quantitative stakeholder survey across case study companies | The two predictors of success related to the two identified mindset shifts |

| Business Sustainability Typology | Qualitative and comparative case study analysis | The Positive Impact Framework |

| The four strategic differentiators of PIOs | Model simplification with practice testing | The Strategic Innovation Canvas |

| Correlations | Leadership Index | Systems Index | Climate Index | Change Index | Internal Stake-Holder Index | |

|---|---|---|---|---|---|---|

| LEADERSHIP INDEX | Pearson Correlation | |||||

| Sig. (2-tailed) | ||||||

| N | ||||||

| SYSTEMS INDEX | Pearson Correlation | 0.824 ** | ||||

| Sig. (2-tailed) | 0.000 | |||||

| N | 849 | |||||

| CLIMATE INDEX | Pearson Correlation | 0.746 ** | 0.713 ** | |||

| Sig. (2-tailed) | 0.000 | 0.000 | ||||

| N | 850 | 944 | ||||

| CHANGE INDEX | Pearson Correlation | 0.667 ** | 0.641 ** | 0.718 ** | ||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | |||

| N | 845 | 938 | 939 | |||

| INTERNAL STAKEHOLDER INDEX | Pearson Correlation | 0.817 ** | 0.801 ** | 0.765 ** | 0.682 ** | |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | ||

| N | 842 | 935 | 936 | 936 | ||

| EXTERNAL STAKEHOLDER INDEX | Pearson Correlation | 0.802 ** | 0.802 ** | 0.714 ** | 0.684 ** | 0.824 ** |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |

| N | 836 | 834 | 835 | 836 | 836 | |

| Logistical Regression Analysis of Indices | |||||

|---|---|---|---|---|---|

| The Variables Entered: | B | S.E. | Wald | df | Sig. |

| LEADERSHIP INDEX * | −1.871 | 0.303 | 38.021 | 1 | 0.000 |

| EXT. STAKEHOLDER INDEX * | −1.249 | 0.295 | 17.958 | 1 | 0.000 |

| INTERNAL STAKE INDEX | −0.171 | 0.295 | 0.334 | 1 | 0.564 |

| CLIMATE INDEX | 0.925 | 0.323 | 8.190 | 1 | 0.004 |

| CHANGE INDEX | 0.788 | 0.257 | 9.369 | 1 | 0.002 |

| SYSTEMS INDEX | 0.430 | 0.316 | 1.854 | 1 | 0.173 |

| Constant | 0.862 | 0.374 | 5.317 | 1 | 0.021 |

| Leadership Variables in the Equation | |||||

|---|---|---|---|---|---|

| The Variables Entered: | B | S.E. | Wald | df | Sig. |

| The leaders of this company integrate sustainability into their decision-making. * | −0.919 | 0.262 | 12.342 | 1 | 0.000 |

| The leaders of this company are willing to take measured risks in pursuit of sustainability. * | −0.668 | 0.197 | 11.541 | 1 | 0.001 |

| The leaders of this company have a clear vision for sustainability. * | −0.588 | 0.257 | 5.248 | 1 | 0.022 |

| The leaders of this company are able to inspire others about sustainability-focused issues and initiatives * | −0.574 | 0.242 | 5.640 | 1 | 0.018 |

| The leaders of this company have a clear business case for pursuing the goals of sustainability. | −0.069 | 0.252 | 0.075 | 1 | 0.784 |

| The leaders of this company take a long-term view when making decisions. | −0.052 | 0.206 | 0.065 | 1 | 0.799 |

| The leaders of this company are knowledgeable of the issues pertaining to sustainability. | −0.336 | 0.243 | 1.905 | 1 | 0.168 |

| The leaders of this company are personally committed to issues pertaining to sustainability. | −0.219 | 0.250 | 0.764 | 1 | 0.382 |

| Constant | 1.054 | 0.345 | 9.332 | 1 | 0.002 |

| External Stakeholders Variables in the Equation | |||||

|---|---|---|---|---|---|

| The Variables Entered: | B | S.E. | Wald | df | Sig. |

| This company sends a clear and consistent message to external stakeholders about its commitment to sustainability. * | −1.286 | 0.227 | 32.151 | 1 | 0.000 |

| This company has mechanisms in place to actively engage with external stakeholders about its sustainability initiatives. * | −0.917 | 0.200 | 20.972 | 1 | 0.000 |

| This company encourages sustainability in its supply chain. * | −0.865 | 0.222 | 15.115 | 1 | 0.000 |

| Constant | 0.977 | 0.344 | 8.074 | 1 | 0.004 |

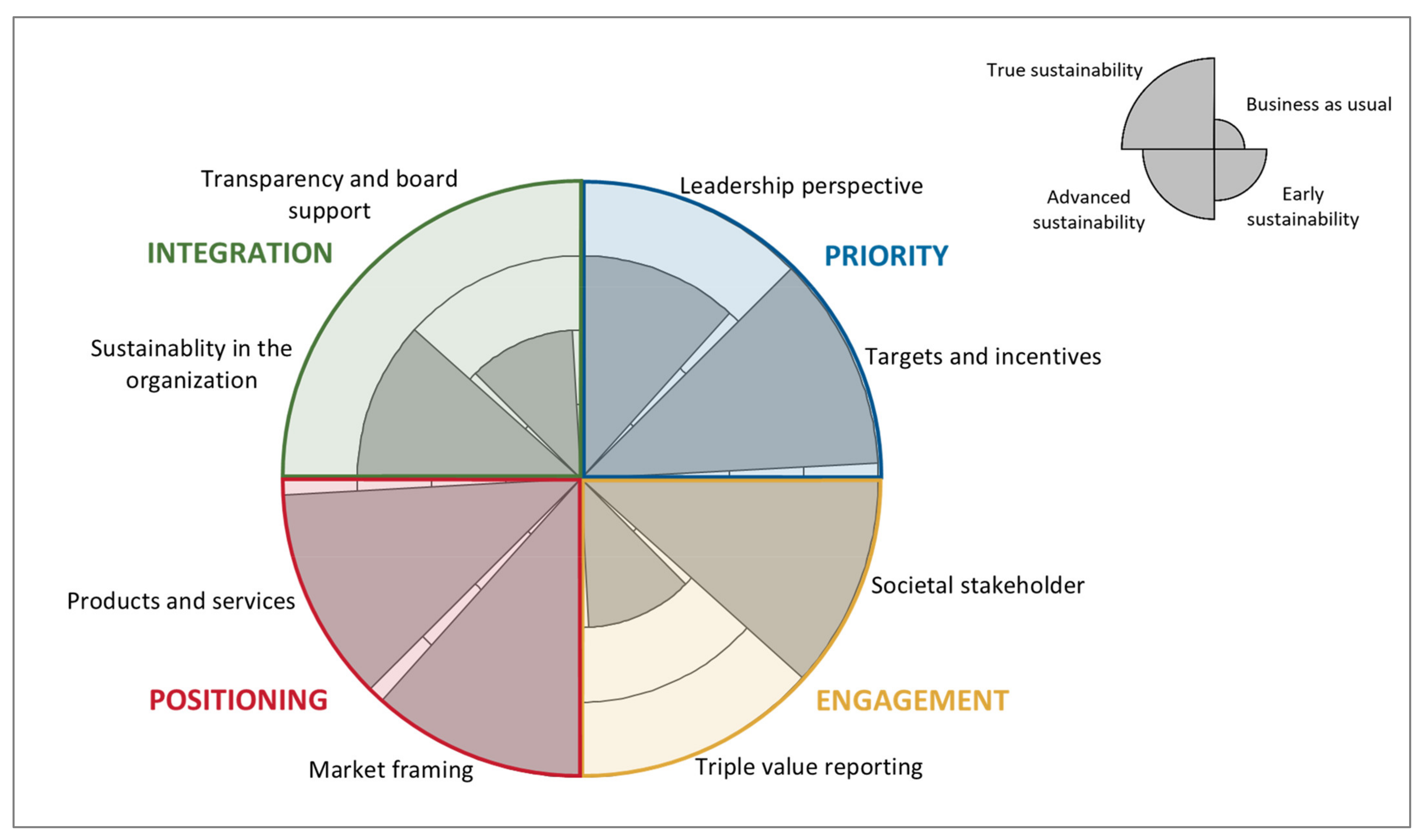

| Action Dimensions | Key Literature Reference | Case Study Reference |

|---|---|---|

| Sustainability in the organization | Miller Perkins [22] | All cases |

| Transparency and board support | Eccles et al. [14] | All cases, in particular Alternative Bank Schweiz |

| Leadership perspective | Pless, Maak, and Waldmann [20] | All cases, in particular Rhomberg |

| Targets and incentives | Eccles et al. [14] | All cases, in particular Alternative Bank Schweiz |

| Societal stakeholder | Eccles et al. [14] | All cases, in particular Beechenhill |

| Triple value reporting | Dyllick and Muff [12] | All cases, in particular Alternative Bank Schweiz, Blue Orchard, Beechenhill |

| Market framing | Dyllick and Muff [12] | All cases, in particular Pebbles, Rhomberg, Lancaster London |

| Products and services | Dyllick and Muff [12] | All cases, in particular Rhomberg, Merkur Andelskasse, Meso Impact Finance |

| The Positive Impact Framework | |||||

|---|---|---|---|---|---|

| Mind Set | Innovation | Action Dimensions | Reducing Impact (Early Sustainability) | Redefining Impact (Advanced Sustainability) | Increasing Positive Impact (True Sustainability) |

| Outside leadership mindset | Integration | Sustainability in the Organization | Societal challenges are managed centrally by a specialized function | Societal challenges are integrated into various functions and areas | The organization has organized itself around societal challenges and includes outside players in an open and dynamic structure |

| Transparency and Board Support | The organization has primarily introduced defensive policies and guidelines to protect against risks | The organization’s board ensures triple-bottom line goals are integrated into internal policies, guidelines and structures | The organization’s board advocates the integration of relevant societal stakeholders into all decision-making processes on all levels of the organization | ||

| Priority | Leadership Perspective | Opportunity seeker | Integrator | Idealist | |

| Targets and Incentives | Short term, qualitative targets | Smart targets and some non-financial incentives for management | Smart, science-based targets and sustainability incentives for all employees, management and board members | ||

| Co-creative organization mindset | Engagement | Triple Value Reporting | Selective reporting as a response to outside demands | Reporting on all material aspects relevant for the organization | Reporting on societal and environmental value |

| Societal stakeholder | The organization reacts to external pressure | The organization reaches out to its traditional stakeholders | The organization redefines its role as one of many responsible societal stakeholders | ||

| Positioning | Market Framing | The organization is responding to outside pressures in existing markets | The organization is exploring new market opportunities and emerging segments inside or outside existing markets | The organization is transforming existing markets or defining new markets allowing for significant repositioning | |

| Products and services | Qualitative, social or environmental improvements of existing products and services | Systematic improvements incl. all relevant dimensions and the whole value chain | Development of new products and services with a net positive impact on sustainability challenges | ||

| Next Steps-Suggestions for Organizations Seeking to Increase Their Positive Impact: |

|---|

|

|

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Muff, K. Learning from Positive Impact Organizations: A Framework for Strategic Innovation. Sustainability 2021, 13, 8891. https://doi.org/10.3390/su13168891

Muff K. Learning from Positive Impact Organizations: A Framework for Strategic Innovation. Sustainability. 2021; 13(16):8891. https://doi.org/10.3390/su13168891

Chicago/Turabian StyleMuff, Katrin. 2021. "Learning from Positive Impact Organizations: A Framework for Strategic Innovation" Sustainability 13, no. 16: 8891. https://doi.org/10.3390/su13168891

APA StyleMuff, K. (2021). Learning from Positive Impact Organizations: A Framework for Strategic Innovation. Sustainability, 13(16), 8891. https://doi.org/10.3390/su13168891