Framework of Blockchain-Supported E-Commerce Platform for Small and Medium Enterprises

Abstract

:1. Introduction

2. Literature

2.1. SME Financing

2.2. Platform Operations

2.3. Blockchain Technology

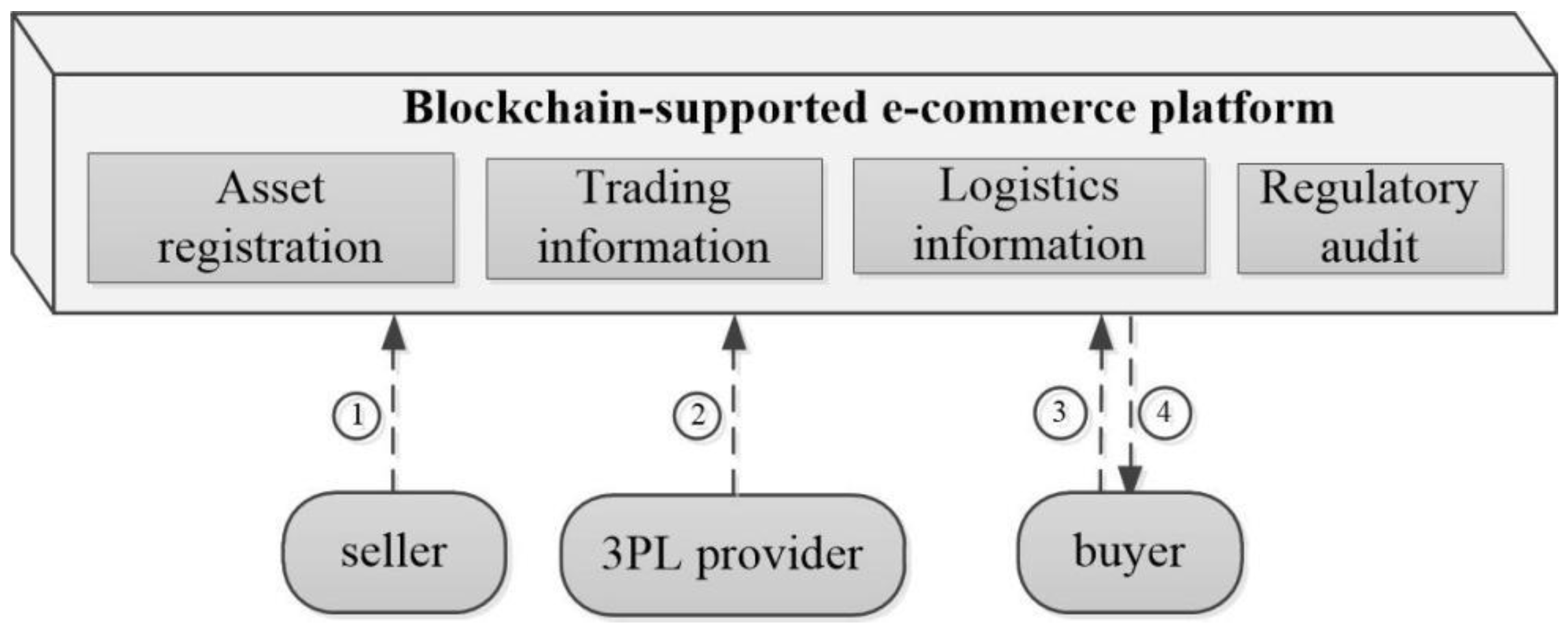

3. Conceptual Framework

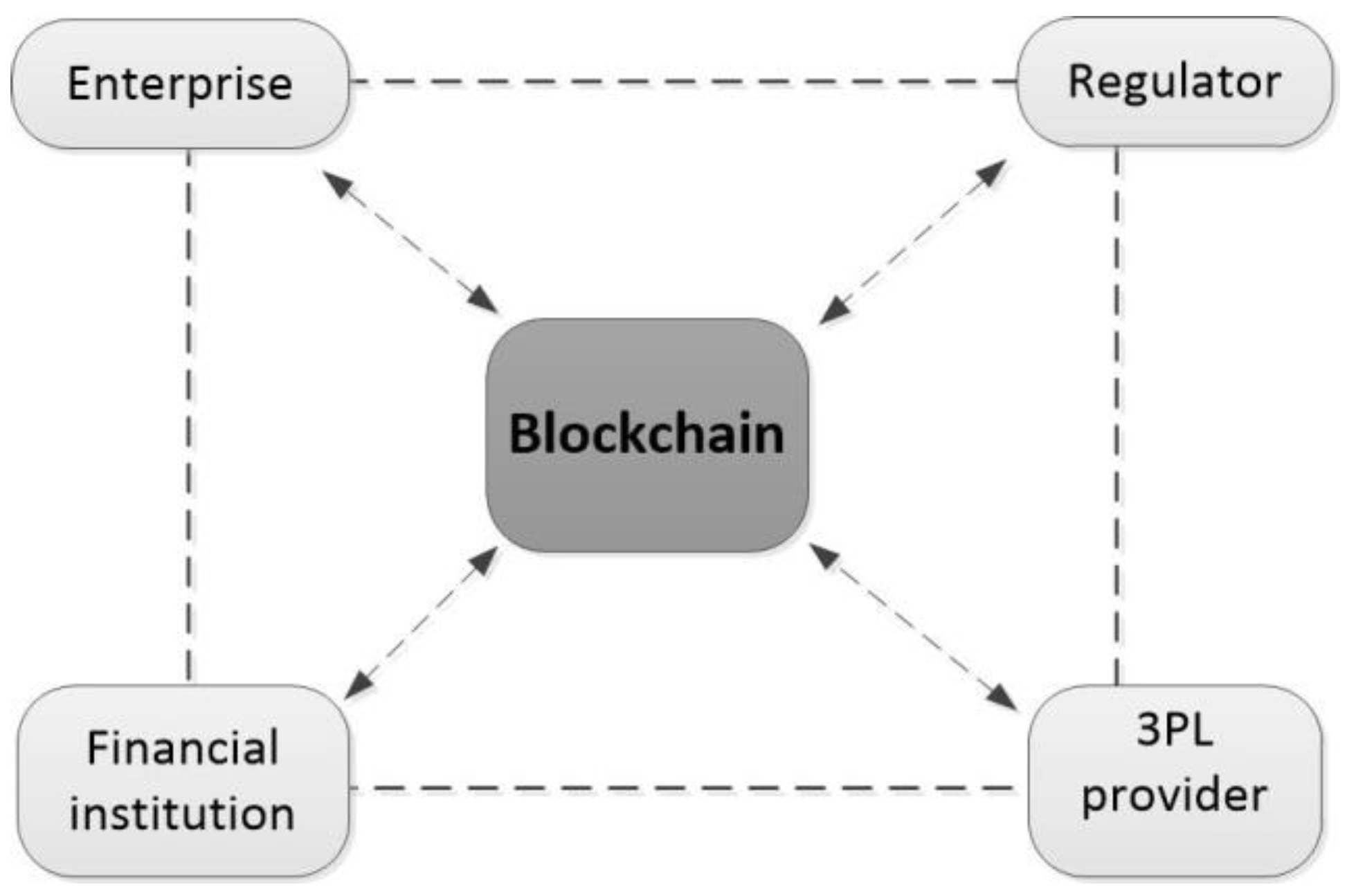

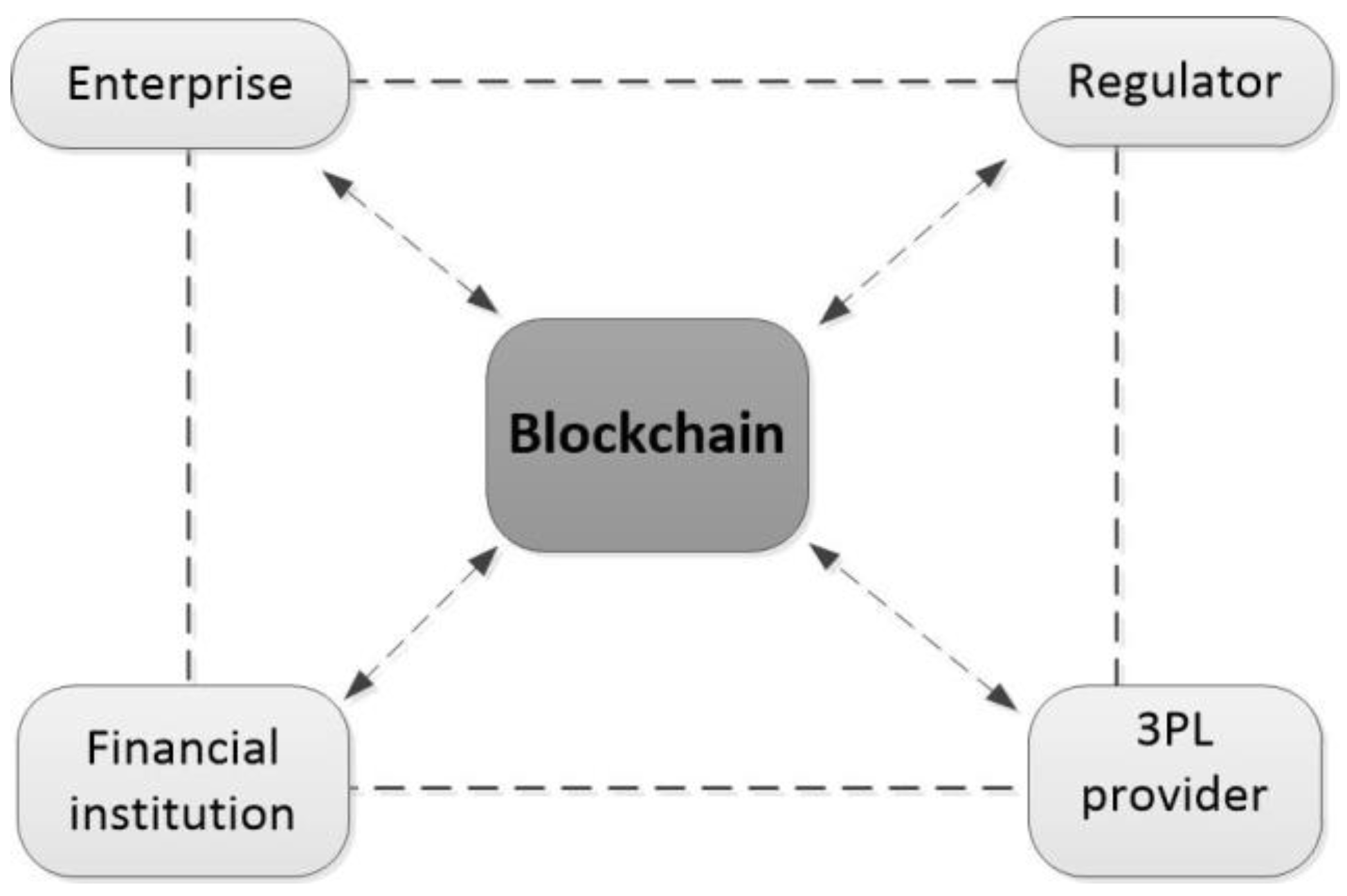

3.1. Nodal Types

- (1)

- Enterprise

- (2)

- 3PL provider

- (3)

- Financial institution

- (4)

- Regulator

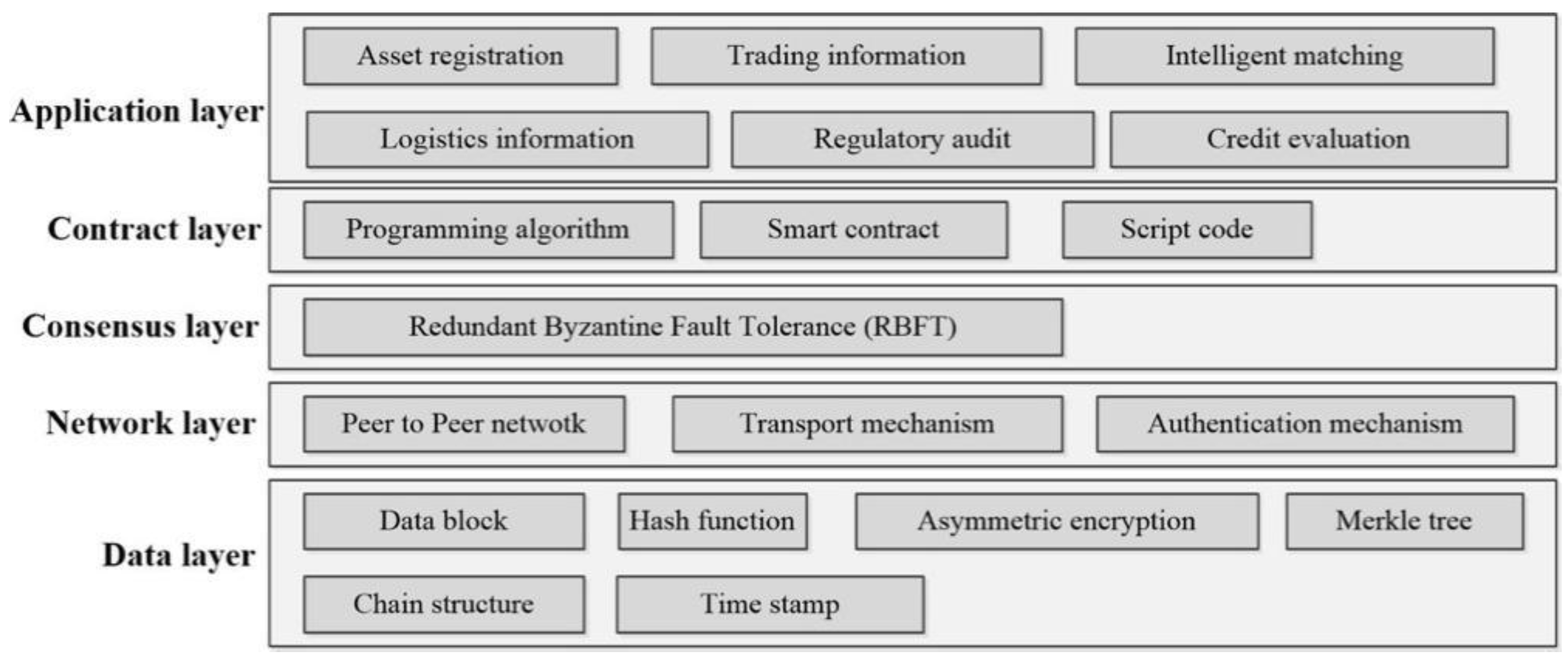

3.2. Conceptual Framework

- (1)

- Asset registration

- (2)

- Trading information

- (3)

- Intelligent matching

- (4)

- Logistics information

- (5)

- Regulatory audit

- (6)

- Credit evaluation

4. Application of Blockchain-Supported E-Commerce Platform

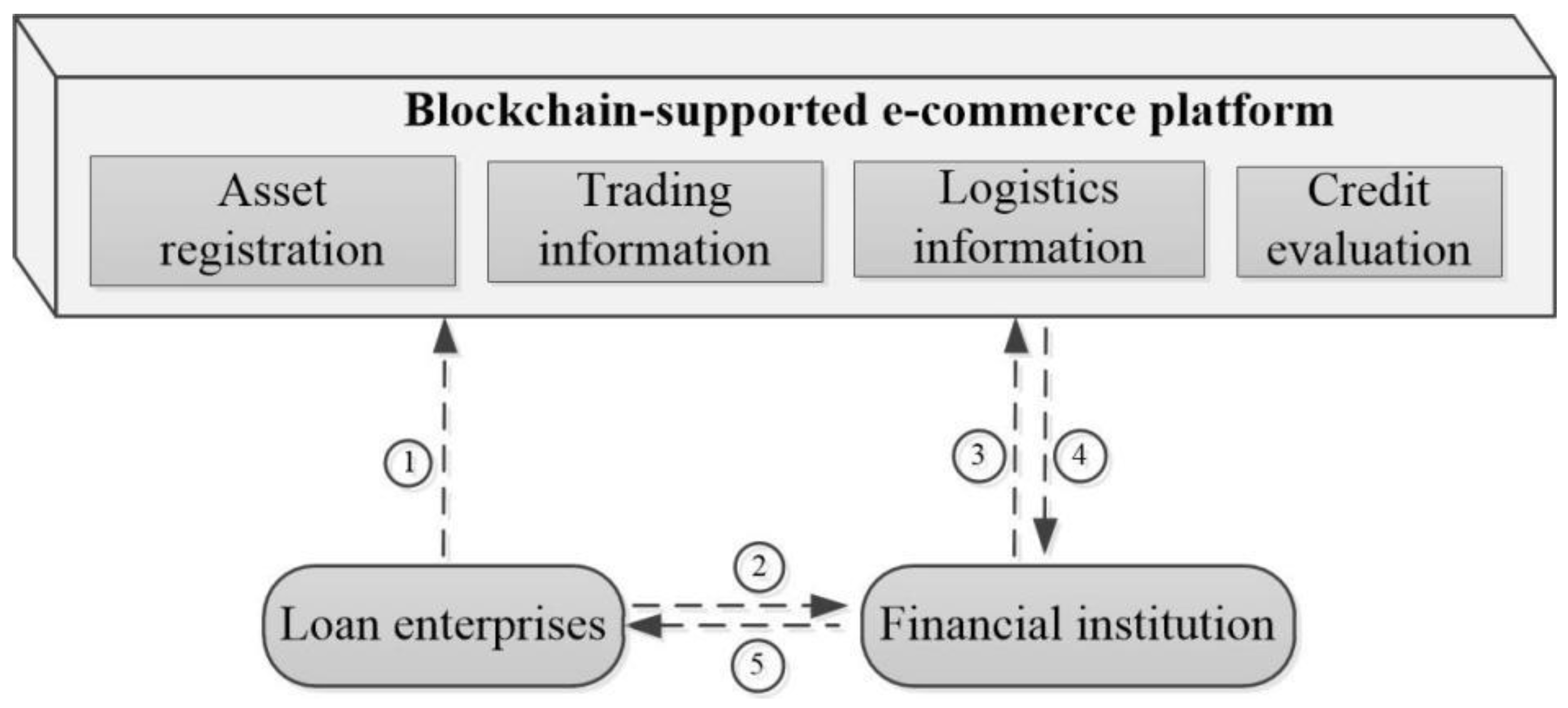

4.1. Enterprise Financing

- (1)

- Loan enterprises call asset registration modules to submit their own enterprise qualification to the platform, which includes the registered capital of the enterprise, company type, qualification certificate, and other information. Moreover, with the dynamic adjustment of enterprises, they must constantly update their own data on the platform.

- (2)

- In the process of development, enterprises encounter capital problems and apply for data financing from financial institutions.

- (3)

- Financial institutions call the credit evaluation module to assess the credit of the loan enterprise.

- (4)

- The credit evaluation module receives the assessment requirements of the bank. It evaluates the loan enterprise based on enterprise qualification information, historical transaction information, inventory information, and order information, and it returns the evaluation results to financial institutions.

- (5)

- According to the evaluation results, financial institutions sign relevant loan contracts with loan enterprises and generate smart contracts according to the contracts. When the conditions of smart contracts are met, banks issue loans to enterprises. When an enterprise fails to fulfill its repayment obligations according to the contract, the smart contract will automatically suspend other business activities of the enterprise.

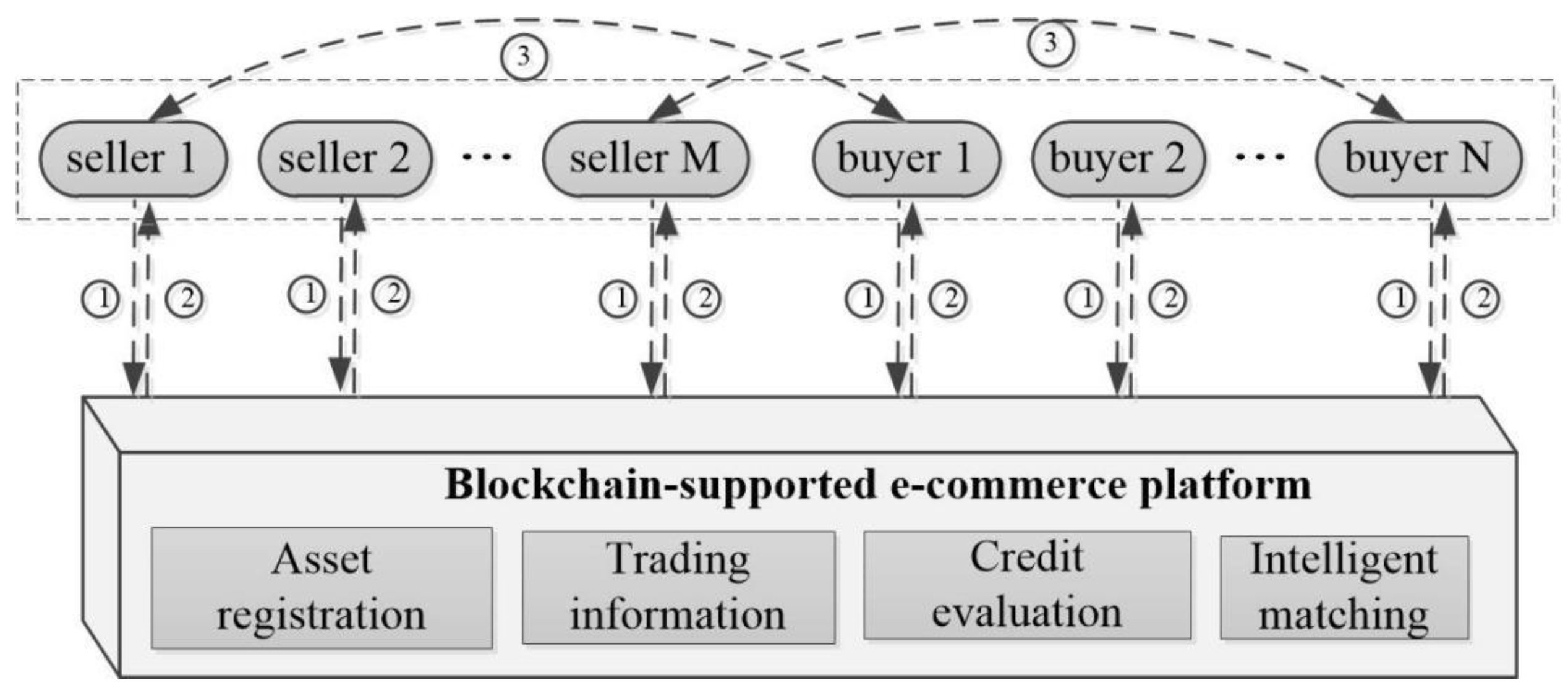

4.2. Transaction Matching

- (1)

- SMEs call an asset-registration module to submit data. The buyer uploads the type, quantity, and expected price range of purchased goods, and the seller uploads the type, quantity, and price range of inventory goods.

- (2)

- The transaction module calls the credit evaluation module to evaluate the ability of sellers and buyers, which mainly assesses the payment ability of buyers and the commodity supply ability of sellers in the transaction process. If the assessment result meets trading requirements, the intelligent matching algorithm compares the demand and supply of all parties, obtains the optimal matching scheme, and returns the results to the enterprise.

- (3)

- The seller and buyer conclude the transaction contract according to the intelligent matching result and generate an intelligent contract according to the contract. When the conditions of the intelligent contract are met, the seller will automatically deliver the goods, and the buyer will submit the payment for goods to complete the transaction process. When the seller fails to provide the goods on time or the buyer fails to submit the payment as required, the smart contract will automatically suspend the later transaction of the seller or the buyer and upload the transaction results to the platform. Owing to data transparency and unforgeability, it will have a greater impact on the subsequent transaction of the enterprise, thereby compelling the enterprise to actively adhere to the terms of the contract and avoid opportunistic behaviors.

4.3. Transaction Tracking

- (1)

- In the trading process, the seller uploads the production information to the platform, which includes raw material procurement, production link records, and final product packaging. The platform calls the regulatory audit module to identify the authenticity of the information, and these data are then submitted to the trading information module.

- (2)

- The seller delivers final products to 3PL, which provides goods transportation and handover services between the buyer and seller. 3PL also uploads logistics information to the logistics information module during transportation.

- (3)

- The sellers need to check the authenticity and legitimacy of the goods when they receive goods, so they apply to the platform to obtain product information.

- (4)

- After receiving the application, the platform calls the transaction information module and logistics information module to access product information, and returns these data to the seller. According to these data, the seller decides whether the product meets contract requirements.

5. Discussion

6. Conclusions

6.1. Concluding Remarks

6.2. Managerial Insights

6.3. Future Studies

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Ayyagari, M.; Beck, T.; Demirguc-Kunt, A. Small and Medium Enterprises Across the Globe. Small Bus. Econ. 2007, 29, 415–434. [Google Scholar] [CrossRef]

- Berisha, G.; Pula, J.S. Defining small and medium enterprises: A critical review. Acad. J. Bus. Adm. Law Soc. Sci. 2015, 1, 17–28. [Google Scholar]

- Bigliardi, B.; Colacino, P.; Dormio, A.I. Innovative Characteristics of Small and Medium Enterprises. J. Technol. Manag. Innov. 2011, 6, 83–93. [Google Scholar] [CrossRef] [Green Version]

- Lee, S.; Park, G.; Yoon, B.; Park, J. Open innovation in SMEs—An intermediated network model. Res. Policy 2010, 39, 290–300. [Google Scholar] [CrossRef]

- Rosenbusch, N.; Brinckmann, J.; Bausch, A. Is innovation always beneficial? A meta-analysis of the relationship between innovation and performance in SMEs. J. Bus. Ventur. 2011, 26, 441–457. [Google Scholar] [CrossRef] [Green Version]

- World Bank. Small and Medium Enterprises Finance. Available online: https://www.worldbank.org/en/topic/smefinance (accessed on 18 November 2020).

- Liu, W. Boosting SMEs with better and innovative financing services. J. Sys. Manag. Sci. 2014, 4, 15–23. [Google Scholar]

- Hu, Y.; Wang, F. Research on financing model of the Chinese SMEs in supply chain finance. Int. J. Econ. Financ. Manag. Sci. 2016, 4, 235. [Google Scholar] [CrossRef]

- Zhi, B.; Wang, X.; Xu, F. Impawn rate optimisation in inventory financing: A canonical vine copula-based approach. Int. J. Prod. Econ. 2020, 227, 107659. [Google Scholar] [CrossRef]

- Mol-Gómez-Vázquez, A.; Hernández-Cánovas, G.; Koëter-Kant, J. Do foreign banks intensify borrower discouragement? The role of developed European institutions in ameliorating SME financing constraints. Int. Small Bus. J. Res. Entrep. 2019, 38, 3–20. [Google Scholar] [CrossRef] [Green Version]

- Moscalu, M.; Girardone, C.; Calabrese, R. SMEs’ growth under financing constraints and banking markets integration in the euro area. J. Small Bus. Manag. 2019, 58, 707–746. [Google Scholar] [CrossRef]

- Di Carlo, F.; Mazzuto, G.; Bevilacqua, M.; Ciarapica, F. Retrofitting a Process Plant in an Industry 4.0 Perspective for Improving Safety and Maintenance Performance. Sustainability 2021, 13, 646. [Google Scholar] [CrossRef]

- Huang, Y.; Chai, Y.; Liu, Y.; Shen, J. Architecture of next-generation e-commerce platform. Tsinghua Sci. Technol. 2019, 24, 18–29. [Google Scholar] [CrossRef]

- Gonçalves, R.; Rocha, T.; Martins, J.; Branco, F.; Oliveira, M.A.-Y. Evaluation of e-commerce websites accessibility and usability: An e-commerce platform analysis with the inclusion of blind users. Univers. Access Inf. Soc. 2017, 17, 567–583. [Google Scholar] [CrossRef]

- D’Adamo, I.; González-Sánchez, R.; Medina-Salgado, M.; Settembre-Blundo, D. E-Commerce Calls for Cyber-Security and Sustainability: How European Citizens Look for a Trusted Online Environment. Sustainability 2021, 13, 6752. [Google Scholar] [CrossRef]

- Saberi, S.; Kouhizadeh, M.; Sarkis, J.; Shen, L. Blockchain technology and its relationships to sustainable supply chain management. Int. J. Prod. Res. 2018, 57, 2117–2135. [Google Scholar] [CrossRef] [Green Version]

- Secinaro, S.; Calandra, D.; Biancone, P. Blockchain, trust, and trust accounting: Can blockchain technology substitute trust created by intermediaries in trust accounting? A theoretical examination. Int. J. Manag. Pract. 2021, 14, 129–145. [Google Scholar] [CrossRef]

- Song, Q.; Chen, Y.; Zhong, Y.; Lan, K.; Fong, S.; Tang, R. A Supply-chain System Framework Based on Internet of Things Using Blockchain Technology. ACM Trans. Internet Technol. 2021, 21, 1–24. [Google Scholar] [CrossRef]

- Wang, R.; Lin, Z.; Luo, H. Blockchain, bank credit and SME financing. Qual. Quant. 2019, 53, 1127–1140. [Google Scholar] [CrossRef]

- Lorne, F.T.; Daram, S.; Frantz, R.; Kumar, N.; Mohammed, A.; Muley, A. Blockchain Economics and Marketing. J. Comput. Commun. 2018, 06, 107–117. [Google Scholar] [CrossRef] [Green Version]

- Cai, Y.; Choi, T.; Zhang, J. Platform Supported Supply Chain Operations in the Blockchain Era: Supply Contracting and Moral Hazards*. Decis. Sci. 2020. [Google Scholar] [CrossRef]

- Gao, F. Data encryption algorithm for e-commerce platform based on blockchain technology. Discret. Contin. Dyn. Syst. S 2019, 12, 1457–1470. [Google Scholar] [CrossRef] [Green Version]

- Chen, L.; Lee, W.-K.; Chang, C.-C.; Choo, K.-K.R.; Zhang, N. Blockchain based searchable encryption for electronic health record sharing. Future Gener. Comput. Syst. 2019, 95, 420–429. [Google Scholar] [CrossRef]

- Van Engelenburg, S.; Janssen, M.; Klievink, B. A Blockchain Architecture for Reducing the Bullwhip Effect. In International Symposium on Business Modeling and Software Design; Springer: Cham, Switzerland, 2018; pp. 69–82. [Google Scholar]

- Yuan, R.; Xia, Y.-B.; Chen, H.-B.; Zang, B.-Y.; Xie, J. ShadowEth: Private Smart Contract on Public Blockchain. J. Comput. Sci. Technol. 2018, 33, 542–556. [Google Scholar] [CrossRef]

- Ismanto, L.; Ar, H.S.; Fajar, A.N.; Sfenrianto; Bachtiar, S. Blockchain as E-Commerce Platform in Indonesia. J. Phys. Conf. Ser. 2019, 1179, 012114. [Google Scholar] [CrossRef]

- Sensini, L.; Vazquez, M. Effects of Working Capital Management on SME Profitability: Evidence from an Emerging Economy. Int. J. Bus. Manag. 2021, 16, p85. [Google Scholar] [CrossRef]

- Dai, R.M.; Kostini, N.; Tresna, P.W. The influence of financial attitude and financial literacy on behavioral finance: A study on leading small and medium enterprises in Cimahi City, Indonesia. Rev. Integrat. Bus. Econ. Res. 2021, 10, 322–329. [Google Scholar]

- Lu, Q.; Liu, B.; Yu, K. Effect of supplier-buyer cooperation on supply chain financing availability of SMEs. Int. J. Logist. Res. Appl. 2021, 1–19. [Google Scholar] [CrossRef]

- Gupta, H.; Barua, M.K. A novel hybrid multi-criteria method for supplier selection among SMEs on the basis of innovation ability. Int. J. Logist. Res. Appl. 2017, 21, 201–223. [Google Scholar] [CrossRef]

- Zhao, S.; Lu, X. Accounts Receivable Financing and Supply Chain Coordination under the Government Subsidy. In Proceedings of the International Conference on Information Science and Technology, Chengdu, China, 21–23 May 2021; pp. 477–484. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, X.; Wang, L.; Zhao, X.; Gao, J. Financing capital-constrained third-party logistic firms: Fourth party logistic driven financing mode vs. private lending driven financing mode. Int. J. Prod. Res. 2021, 1–20. [Google Scholar] [CrossRef]

- Emtehani, F.; Nahavandi, N.; Rafiei, F.M. A joint inventory–finance model for coordinating a capital-constrained supply chain with financing limitations. Financ. Innov. 2021, 7, 1–39. [Google Scholar] [CrossRef]

- Wang, J.; Huang, P.; Zhao, H.; Zhang, Z.; Zhao, B.; Lee, D.L. Billion-Scale Commodity Embedding for E-commerce Recommendation in Alibaba. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, London, UK, 19–23 August 2018; pp. 839–848. [Google Scholar]

- Ritala, P.; Golnam, A.; Wegmann, A. Coopetition-based business models: The case of Amazon.com. Ind. Mark. Manag. 2014, 43, 236–249. [Google Scholar] [CrossRef]

- Fearnside, P. Business as usual: A resurgence of deforestation in the Brazilian Amazon. Yale Environ. 2017, 360, 1–6. [Google Scholar]

- Baiman, S.; Fischer, P.E.; Rajan, M.V. Information, contracting, and quality costs. Manag. Sci. 2000, 46, 776–789. [Google Scholar] [CrossRef]

- A Starbird, S. Penalties, rewards, and inspection: Provisions for quality in supply chain contracts. J. Oper. Res. Soc. 2001, 52, 109–115. [Google Scholar] [CrossRef]

- Babich, V.; Tang, C. Managing Opportunistic Supplier Product Adulteration: Deferred Payments, Inspection, and Combined Mechanisms. Manuf. Serv. Oper. Manag. 2012, 14, 301–314. [Google Scholar] [CrossRef] [Green Version]

- Rui, H.; Lai, G. Sourcing with Deferred Payment and Inspection under Supplier Product Adulteration Risk. Prod. Oper. Manag. 2015, 24, 934–946. [Google Scholar] [CrossRef]

- Krishna, M.B.; Dugar, A. Product Authentication Using QR Codes: A Mobile Application to Combat Counterfeiting. Wirel. Pers. Commun. 2016, 90, 381–398. [Google Scholar] [CrossRef]

- Wazid, M.; Das, A.K.; Khan, M.K.; Al-Ghaiheb, A.A.-D.; Kumar, N.; Vasilakos, A.V. Secure Authentication Scheme for Medicine Anti-Counterfeiting System in IoT Environment. IEEE Internet Things J. 2017, 4, 1634–1646. [Google Scholar] [CrossRef]

- Shaik, C. Preventing Counterfeit Products using Cryptography, QR Code and Webservice. Comput. Sci. Eng. Int. J. 2021, 11, 1–11. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2019. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 11 February 2012).

- Lin, Q.; Wang, H.; Pei, X.; Wang, J. Food Safety Traceability System Based on Blockchain and EPCIS. IEEE Access 2019, 7, 20698–20707. [Google Scholar] [CrossRef]

- Creydt, M.; Fischer, M. Blockchain and more—Algorithm driven food traceability. Food Control 2019, 105, 45–51. [Google Scholar] [CrossRef]

- Rejeb, A.; Keogh, J.G.; Treiblmaier, H. Leveraging the Internet of Things and Blockchain Technology in Supply Chain Management. Future Internet 2019, 11, 161. [Google Scholar] [CrossRef] [Green Version]

- Dwivedi, S.K.; Amin, R.; Vollala, S. Blockchain based secured information sharing protocol in supply chain management system with key distribution mechanism. J. Inf. Secur. Appl. 2020, 54, 102554. [Google Scholar] [CrossRef]

- Chang, S.E.; Chen, Y.-C.; Lu, M.-F. Supply chain re-engineering using blockchain technology: A case of smart contract-based tracking process. Technol. Forecast. Soc. Chang. 2019, 144, 1–11. [Google Scholar] [CrossRef]

- Wang, S.; Li, D.; Zhang, Y.; Chen, J. Smart Contract-Based Product Traceability System in the Supply Chain Scenario. IEEE Access 2019, 7, 115122–115133. [Google Scholar] [CrossRef]

- Dolgui, A.; Ivanov, D.; Potryasaev, S.; Sokolov, B.; Ivanova, M.; Werner, F. Blockchain-oriented dynamic modelling of smart contract design and execution in the supply chain. Int. J. Prod. Res. 2019, 58, 2184–2199. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Blockchain | Description | Reference |

|---|---|---|

| Chain structure | The chain structure of blockchain ensures the authenticity and transparency of data. | [18,19,20,21] |

| Encryption algorithm | The encryption algorithm of blockchain addresses the contradiction between data privacy protection and information sharing requirements. | [22,23,24] |

| Smart contract | The smart contract of blockchain ensures the automatic execution of transactions based on presupposed conditions. | [25,26] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jiang, J.; Chen, J. Framework of Blockchain-Supported E-Commerce Platform for Small and Medium Enterprises. Sustainability 2021, 13, 8158. https://doi.org/10.3390/su13158158

Jiang J, Chen J. Framework of Blockchain-Supported E-Commerce Platform for Small and Medium Enterprises. Sustainability. 2021; 13(15):8158. https://doi.org/10.3390/su13158158

Chicago/Turabian StyleJiang, Ji, and Jin Chen. 2021. "Framework of Blockchain-Supported E-Commerce Platform for Small and Medium Enterprises" Sustainability 13, no. 15: 8158. https://doi.org/10.3390/su13158158

APA StyleJiang, J., & Chen, J. (2021). Framework of Blockchain-Supported E-Commerce Platform for Small and Medium Enterprises. Sustainability, 13(15), 8158. https://doi.org/10.3390/su13158158