Predictive Role of Ex Ante Strategic Firm Characteristics for Sustainable Initial Public Offering (IPO) Survival

Abstract

:1. Introduction

2. Literature Review and Hypotheses

2.1. Share Premium and IPO Survival

2.2. Firm Size

2.3. Listed Capital

2.4. Offer Size

2.5. Risk Factors

3. Methods

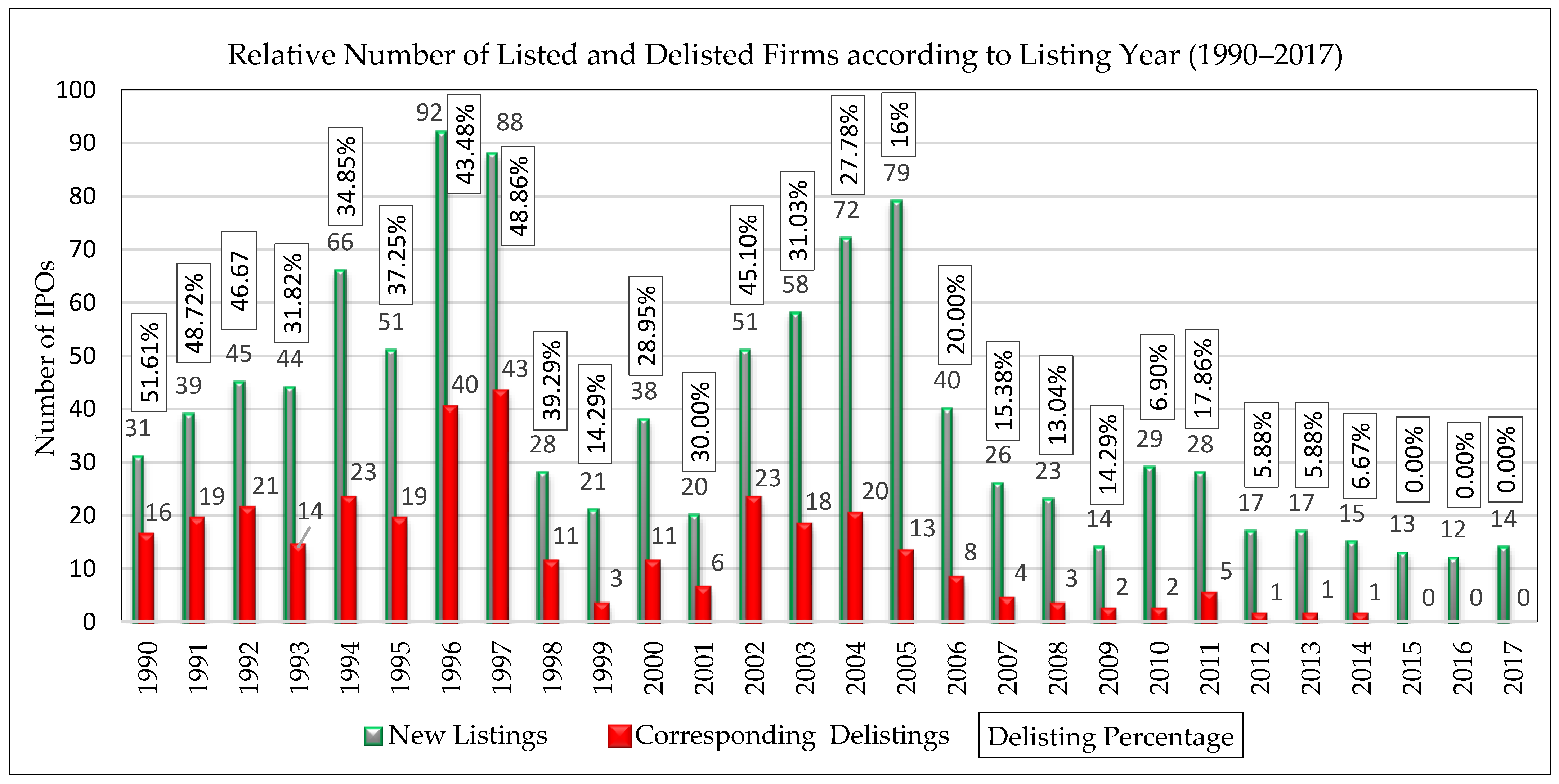

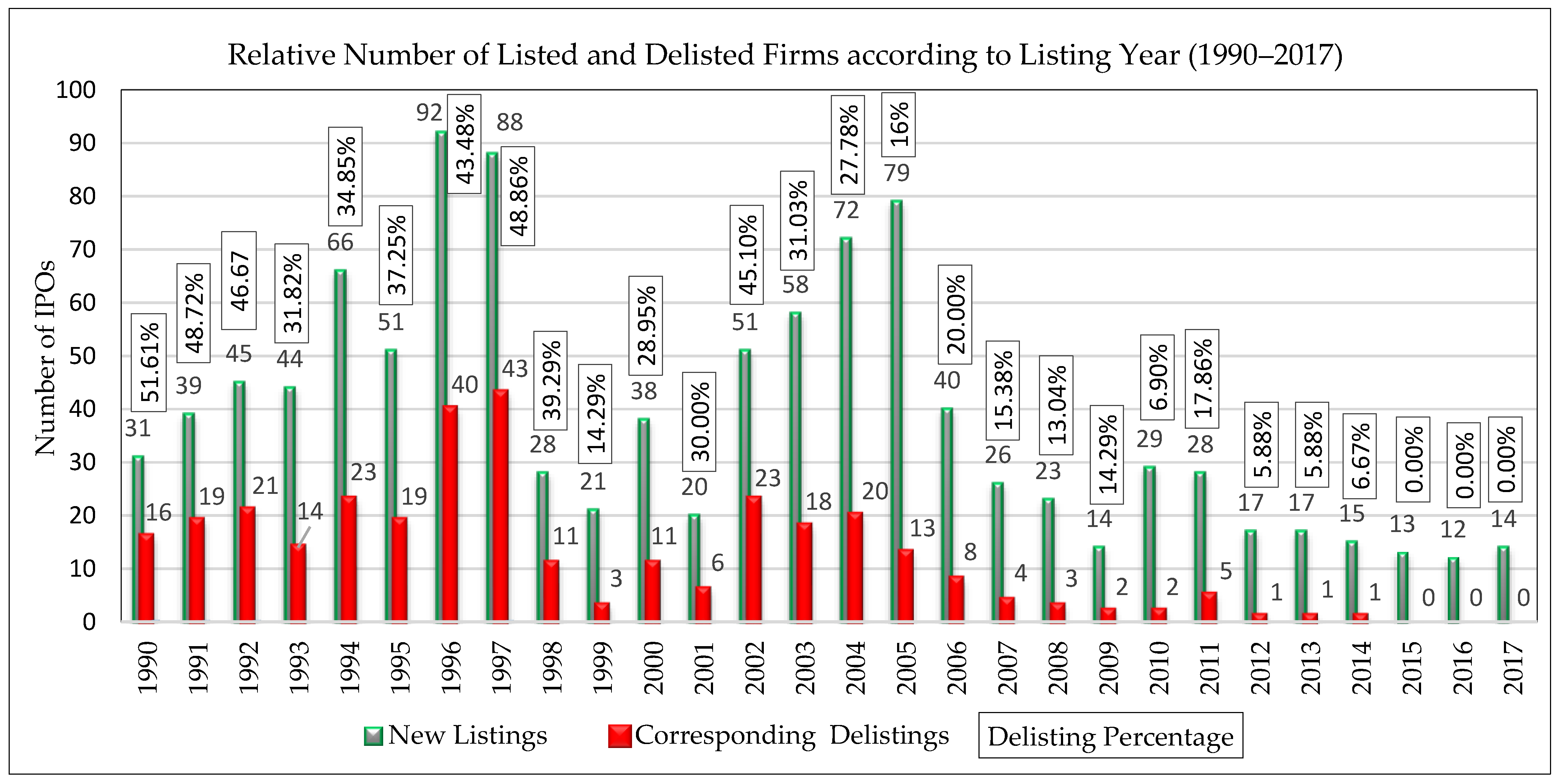

3.1. Research Design and Data Description

3.2. Model and Variable Description

4. Results

4.1. Overall Descriptive Statistics

4.2. Variance Inflation Factor

4.3. Survival Specific Descriptive Statistics

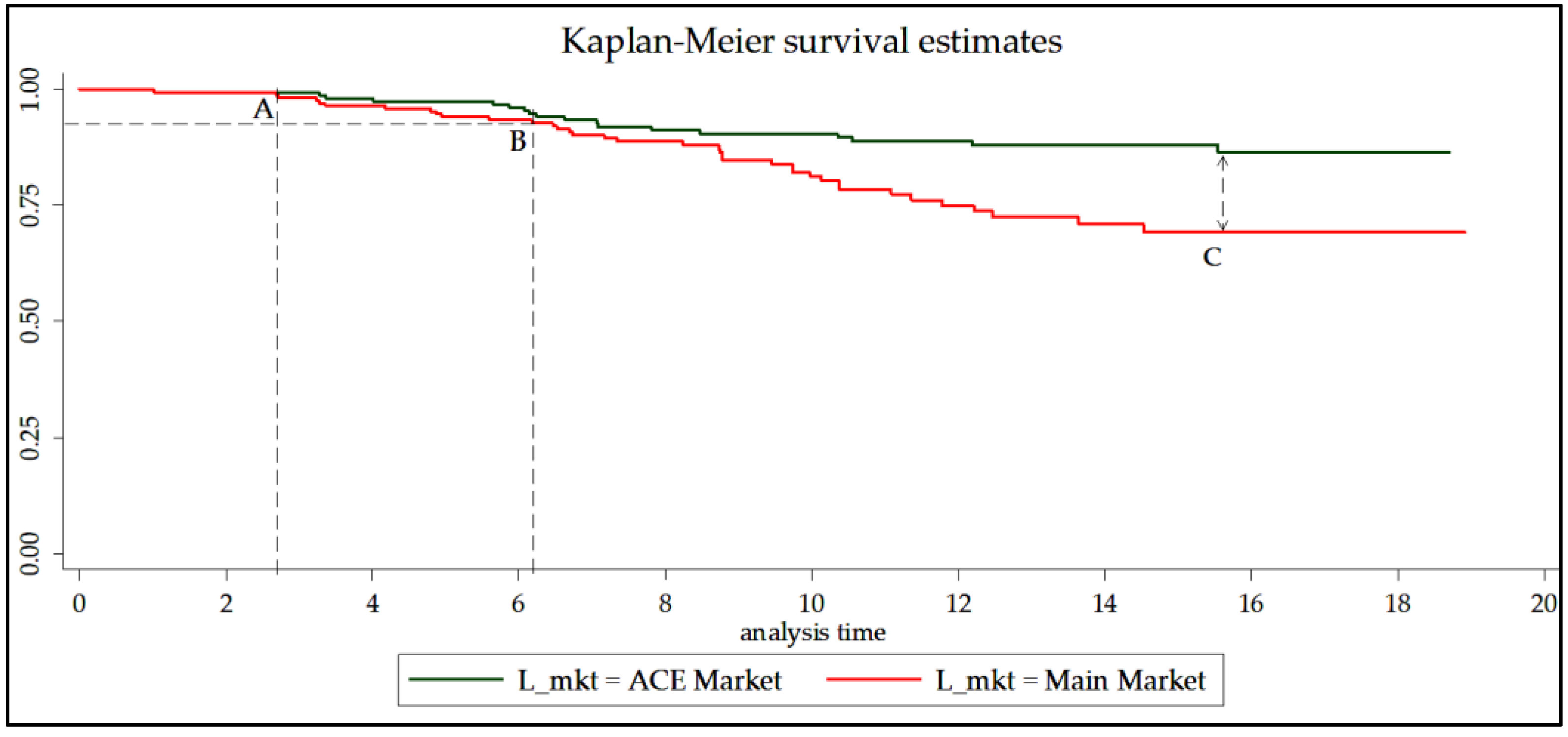

4.4. Kaplan–Meier (KM) Survival Estimates

4.5. Inferential Statistics Cox Proportional Hazard Model

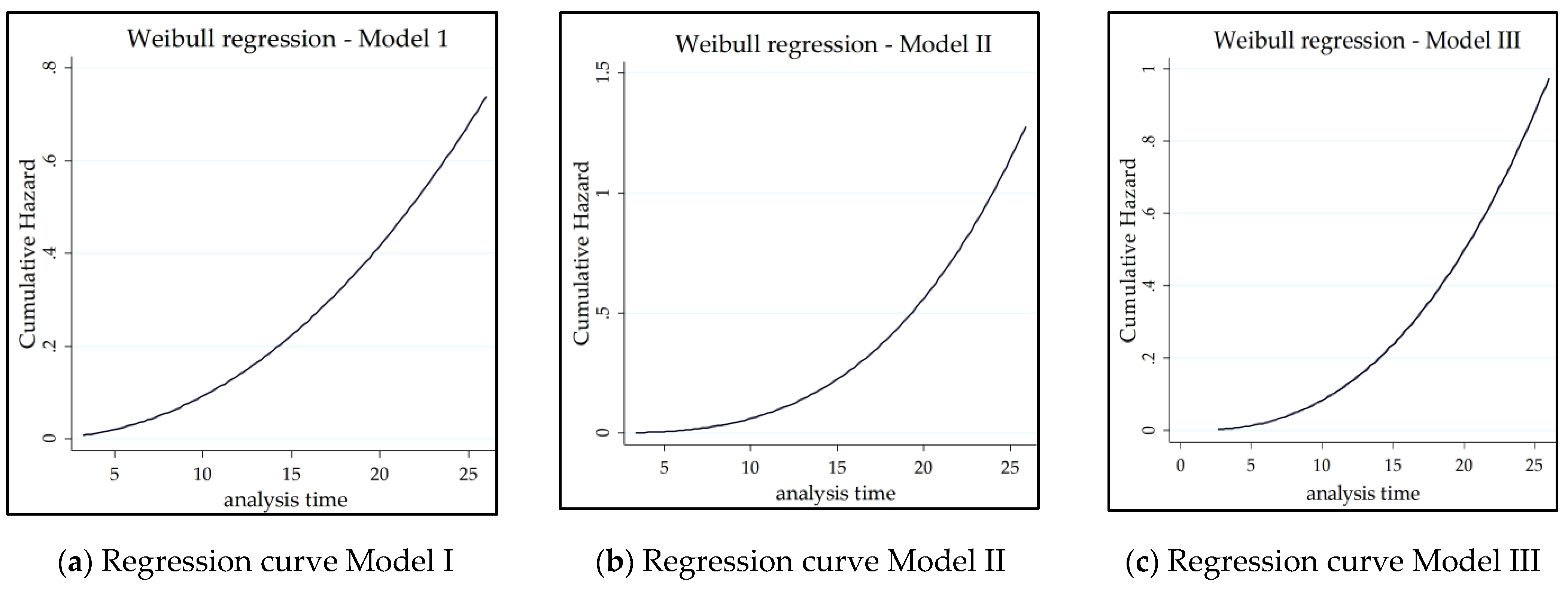

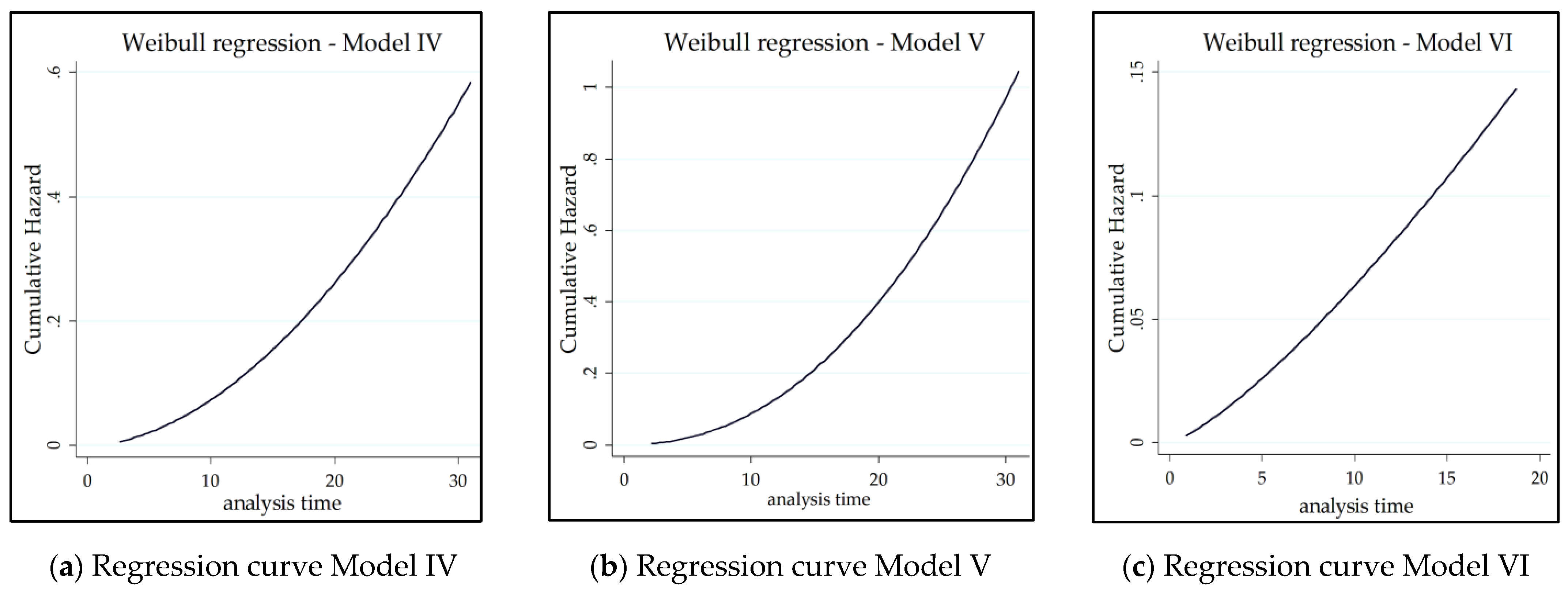

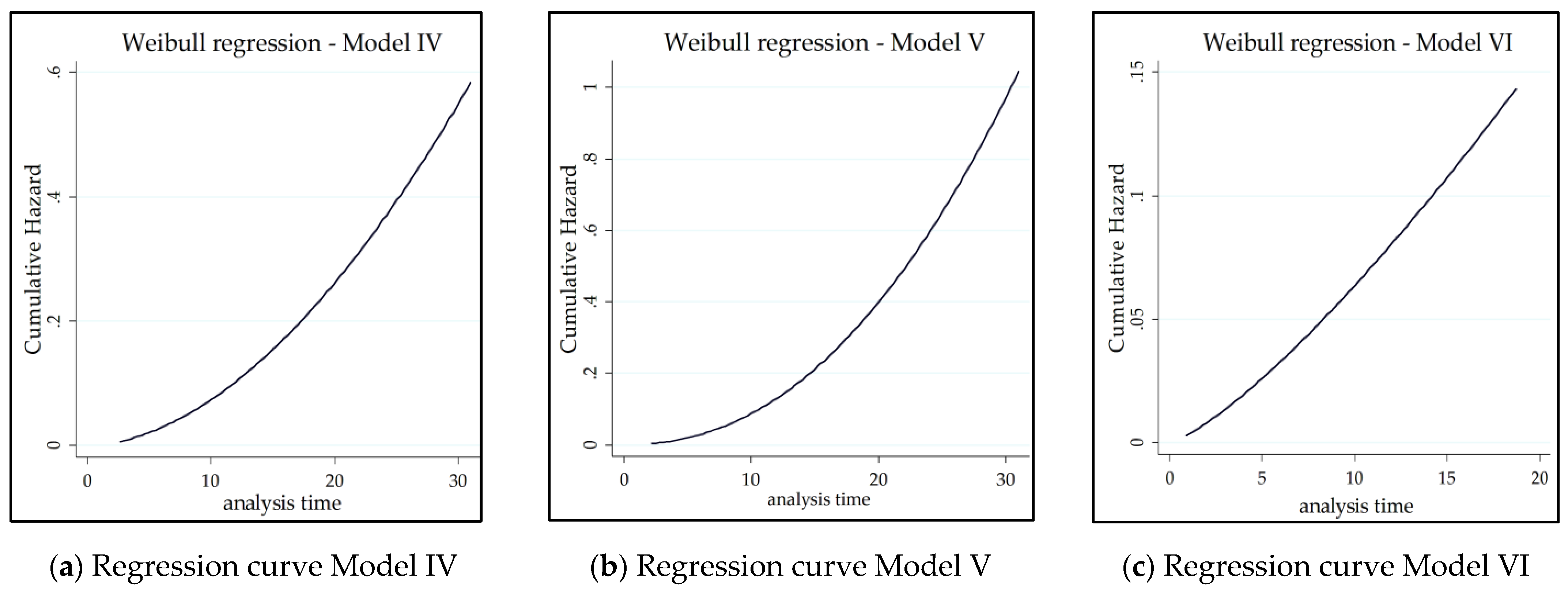

4.6. Robustness Tests

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ayadi, R.; Abid, I.; Guesmi, K. Survival of reorganized firms in France. Financ. Res. Lett. 2021, 38. [Google Scholar] [CrossRef]

- Espenlaub, S.; Goyal, A.; Mohamed, A. Impact of legal institutions on IPO survival: A global perspective. J. Financ. Stab. 2016, 25, 98–112. [Google Scholar] [CrossRef]

- Balios, D.; Eriotis, N.; Missiakoulis, S.; Vasiliou, D. Delisted versus voluntary delisted versus remain listed: An ordered analysis. Appl. Econ. Lett. 2014, 22, 66–70. [Google Scholar] [CrossRef]

- Kashefi Pour, E.; Lasfer, M. Why do companies delist voluntarily from the stock market? J. Bank. Financ. 2013, 37, 4850–4860. [Google Scholar] [CrossRef]

- Algebaly, E.-A.M.; Ibrahim, Y.; Ahmad-Zaluki, N.A. The determinants of involuntary delisting rate in the Egyptian IPO equity market. Rev. Account. Financ. 2014. [Google Scholar] [CrossRef]

- Helbing, P. A review on IPO withdrawal. Int. Rev. Financ. Anal. 2019, 62, 200–208. [Google Scholar] [CrossRef]

- Feng, C.; Patel, P.C.; Xiang, K. The well-trodden path: Complementing market and entrepreneurial orientation with a strategic emphasis to influence IPO survival in the United States. J. Bus. Res. 2020, 110, 370–385. [Google Scholar] [CrossRef]

- Serio, R.G.; Dickson, M.M.; Giuliani, D.; Espa, G. Green Production as a Factor of Survival for Innovative Startups: Evidence from Italy. Sustainability 2020, 12, 9464. [Google Scholar] [CrossRef]

- Josefy, M.A.; Harrison, J.S.; Sirmon, D.G.; Carnes, C. Living and Dying: Synthesizing the Literature on Firm Survival and Failure across Stages of Development. Acad. Manag. Ann. 2017, 11, 770–799. [Google Scholar] [CrossRef]

- Espenlaub, S.; Khurshed, A.; Mohamed, A. IPO Survival in a Reputational Market. J. Bus. Financ. Account. 2012, 39, 427–463. [Google Scholar] [CrossRef]

- Martinez, I.; Serve, S. Reasons for Delisting and Consequences: A Literature Review and Research Agenda. J. Econ. Surv. 2017, 31, 733–770. [Google Scholar] [CrossRef]

- Jain, B.A.; Martin, C.L.M.C.L. The Association Between Audit Quality and Post-IPO Performance: A Survival Analysis Approach. Rev. Account. Financ. 2005, 4, 50–75. [Google Scholar] [CrossRef]

- Chi, J.; McWha, M.; Young, M. The performance and the survivorship of New Zealand IPOs. Int. Rev. Financ. Anal. 2010, 19, 172–180. [Google Scholar] [CrossRef]

- Ferris, S.P.; Hao, Q.; Liao, M.-Y. The Effect of Issuer Conservatism on IPO Pricing and Performance*. Rev. Financ. 2013, 17, 993–1027. [Google Scholar] [CrossRef]

- Austin, P.C. A Tutorial on Multilevel Survival Analysis: Methods, Models and Applications. Int. Stat. Rev. 2017, 85, 185–203. [Google Scholar] [CrossRef] [PubMed]

- Ahmad, W.; Jelic, R. Lockup Agreements and Survival of UK IPOs. J. Bus. Financ. Account. 2014, 41, 717–742. [Google Scholar] [CrossRef] [Green Version]

- Alhadab, M.; Clacher, I.; Keasey, K. Real and accrual earnings management and IPO failure risk. Account. Bus. Res. 2015, 45, 55–92. [Google Scholar] [CrossRef]

- Macey, J.; O’Hara, M.; Pompilio, D. Down and out in the stock market: The law and economics of the delisting process. J. Law Econ. 2008, 51, 683–713. [Google Scholar] [CrossRef] [Green Version]

- Bhattacharya, U.; Borisov, A.; Yu, X. Firm mortality and natal financial care. J. Financ. Quant. Anal. 2015, 50, 61–88. [Google Scholar] [CrossRef]

- Lewellyn, K.B. A cross-national investigation of IPO activity: The role of formal institutions and national culture. Int. Bus. Rev. 2014, 23, 1167–1178. [Google Scholar] [CrossRef]

- Fertala, N. The shadow of death: Do regional differences matter for firm survival across native and immigrant entrepreneurs? Empirica 2007, 35, 59–80. [Google Scholar] [CrossRef]

- Cattaneo, M.; Meoli, M.; Vismara, S. Financial regulation and IPOs: Evidence from the history of the Italian stock market. J. Corp. Financ. 2015, 31, 116–131. [Google Scholar] [CrossRef]

- Derouiche, I.; Sassi, S.; Toumi, N. The control-ownership wedge and the survival of French IPOs. J. Appl. Account. Res. 2018, 19, 271–294. [Google Scholar] [CrossRef]

- Shari, W. Survival of the Malaysian initial public offerings. Manag. Sci. Lett. 2019, 607–620. [Google Scholar] [CrossRef]

- Iwasaki, I.; Kočenda, E. Survival of service firms in European emerging economies. Appl. Econ. Lett. 2019, 27, 340–348. [Google Scholar] [CrossRef]

- Makrominas, M.; Yiannoulis, Y. IPO determinants of delisting risk: Lessons from the Athens Stock Exchange. In Accounting Forum; Routledge: London, UK, 12 March 2021; pp. 1–25. [Google Scholar]

- Souitaris, V.; Zerbinati, S.; Peng, B.; Shepherd, D. Should I stay or should I go? Founder power and exit via initial public offering. Acad. Manag. J. 2020, 63, 64–95. [Google Scholar] [CrossRef]

- Ghahroudi, M.R.; Hoshino, Y.; Fakhraei, E. Ownership Structure, Capital Structure, and Firm Survival. Int. J. Econ. Financ. 2019, 11, 1–19. [Google Scholar] [CrossRef]

- Baumöhl, E.; Iwasaki, I.; Kočenda, E. Institutions and determinants of firm survival in European emerging markets. J. Corp. Financ. 2019, 58, 431–453. [Google Scholar] [CrossRef] [Green Version]

- Corhay, A.; Teo, S.; Tourani Rad, A. The long run performance of Malaysian initial public offerings (IPO): Value and growth effects. Manag. Financ. 2002, 28, 52–65. [Google Scholar] [CrossRef]

- Ahmad-Zaluki, N.A.; Campbell, K.; Goodacre, A. The Long Run Share Price Performance of Malaysian Initial Public Offerings (IPOs). J. Bus. Financ. Account. 2007, 34, 78–110. [Google Scholar] [CrossRef]

- Low, S.-W.; Yong, O. Explaining over-subscription in fixed-price IPOs—Evidence from the Malaysian stock market. Emerg. Mark. Rev. 2011, 12, 205–216. [Google Scholar] [CrossRef]

- Mohd Rashid, R.; Abdul-Rahim, R.; Yong, O. The influence of lock-up provisions on IPO initial returns: Evidence from an emerging market. Econ. Syst. 2014, 38, 487–501. [Google Scholar] [CrossRef]

- Tajuddin, A.H.; Abdullah, N.A.H.; Taufil-Mohd, K.N. Does Growth Opportunity Matter in Explaining the Oversubscription Phenomena of Malaysian IPO? Procedia Soc. Behav. Sci. 2016, 219, 748–754. [Google Scholar] [CrossRef] [Green Version]

- Albada, A.; Yong, O.; Mat Hassan, M.E.; Abdul-Rahim, R. Retention Ratio, Lock-Up Period and Prestige Signals and Their Relationship With Initial Public Offering (IPO) Return: Malaysian Evidence. Asian Acad. Manag. J. Account. Financ. 2018, 14, 1–23. [Google Scholar] [CrossRef]

- Albada, A.; Low, S.-W.; Yong, O. Prestige signals and heterogeneity of opinion regarding IPO values: Malaysian evidence. Int. J. Emerg. Mark. 2019, 15, 302–319. [Google Scholar] [CrossRef]

- Albada, A.; Yong, O.; Low, S.-W. Relationship between prestige signals and over-subscription ratio. Int. J. Manag. Financ. 2019, 15, 564–579. [Google Scholar] [CrossRef]

- Albada, A.; Yong, O.; Low, S.-W. Signalling Effect of Auditor Reputation and Lock-up Period on Over-Subscription Ratio: Evidence from Malaysian Fixed-Price IPOs. Int. J. Bus. Soc. 2020, 21, 253–267. [Google Scholar] [CrossRef]

- Albada, A.; Yong, O. A Review of IPO Under-pricing Phenomenon in Asia. Int. J. Bank. Financ. 2020, 14, 1–26. [Google Scholar] [CrossRef]

- Spence, M. Job Market Signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2010, 37, 39–67. [Google Scholar] [CrossRef]

- Akerlof, G. The Market for Lemons: Qualitative Uncertainty and the Market Mechanism. Q. J. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Leland, H.E.; Pyle, D.H. Informational asymmetries, financial structure, and financial intermediation. J. Financ. 1977, 32, 371–387. [Google Scholar] [CrossRef]

- Daily, C.M.; Certo, S.T.; Dalton, D.R. Investment bankers and IPO pricing: Does prospectus information matter? J. Bus. Ventur. 2005, 20, 93–111. [Google Scholar] [CrossRef]

- Ding, R. Disclosure of Downside Risk and Investors’ Use of Qualitative Information: Evidence from the IPO Prospectus’s Risk Factor Section. Int. Rev. Financ. 2016, 16, 73–126. [Google Scholar] [CrossRef]

- Bhabra, H.S.; Pettway, R.H. IPO prospectus information and subsequent performance. Financ. Rev. 2003, 38, 369–397. [Google Scholar] [CrossRef]

- Carpentier, C.; Suret, J.-M. The survival and success of Canadian penny stock IPOs. Small Bus. Econ. 2011, 36, 101–121. [Google Scholar] [CrossRef] [Green Version]

- Van der Goot, T.; van Giersbergen, N.; Botman, M. What determines the survival of internet IPOs? Appl. Econ. 2009, 41, 547–561. [Google Scholar] [CrossRef]

- Mousa, F.-t.; Bierly, P.E.; Wales, W.J. Different strokes: IPO risk factors, investor valuation, and firm survival. J. Manag. Organ. 2014, 20, 348. [Google Scholar] [CrossRef]

- Gao, L.; Rezaee, Z.; Yu, J. Peer firms’ earnings predictability and pricing efficiency–evidence from IPOs*. Eur. J. Financ. 2020, 26, 1332–1353. [Google Scholar] [CrossRef]

- Loughran, T.; Ritter, J. Why has IPO underpricing changed over time? Financ. Manag. 2004, 33, 5–37. [Google Scholar] [CrossRef] [Green Version]

- Bayar, O.; Chemmanur, T.J. What drives the valuation premium in IPOs versus acquisitions? An empirical analysis. J. Corp. Financ. 2012, 18, 451–475. [Google Scholar] [CrossRef]

- Guo, H. IPO first-day return and ex ante equity premium. J. Financ. Quant. Anal. 2011, 46, 871–905. [Google Scholar] [CrossRef]

- Ljungqvist, A.; Nanda, V.; Singh, R. Hot markets, investor sentiment, and IPO pricing. J. Bus. 2006, 79, 1667–1702. [Google Scholar] [CrossRef]

- Riaz, S.; Hanifa, M.H.; Zainir, F. Does Foreign Institutional Equity Participation Instigate Sustainable Corporate Investment Efficiency? Evidence from Emerging Economies. Sustainability 2021, 13, 4190. [Google Scholar] [CrossRef]

- Moosa, I. The myth of too big to fail. J. Bank. Regul. 2010, 11, 319–333. [Google Scholar] [CrossRef] [Green Version]

- Fishman, A.; Don-Yehiya, H.; Schreiber, A. Too big to succeed or too big to fail? Small Bus. Econ. 2018, 51, 811–822. [Google Scholar] [CrossRef]

- Hensler, D.A.; Rutherford, R.C.; Springer, T.M. The survival of initial public offerings in the aftermarket. J. Financ. Res. 1997, 20, 93–110. [Google Scholar] [CrossRef]

- Helbing, P.; Lucey, B.M.; Vigne, S.A. The determinants of IPO withdrawal–Evidence from Europe. J. Corp. Financ. 2019, 56, 415–436. [Google Scholar] [CrossRef] [Green Version]

- Baker, M.; Wurgler, J. Market timing and capital structure. J. Financ. 2002, 57, 1–32. [Google Scholar] [CrossRef]

- Schultz, P. Unit initial public offerings: A form of staged financing. J. Financ. Econ. 1993, 34, 199–229. [Google Scholar] [CrossRef]

- Ng, S.H.; Lee, C.S. Does IPO prospectus in Malaysia disclose relevant risk? Asia-Pac. J. Bus. Adm. 2019, 11, 301–323. [Google Scholar] [CrossRef]

- Edelmann, D.; Welchowski, T.; Benner, A. A consistent version of distance covariance for right-censored survival data and its application in hypothesis testing. Biometrics 2021. [Google Scholar] [CrossRef]

- Kaplan, E.L.; Meier, P. Nonparametric estimation from incomplete observations. J. Am. Stat. Assoc. 1958, 53, 457–481. [Google Scholar] [CrossRef]

- Cox, D.R. Regression models and life-tables. J. R. Stat. Soc. Ser. B Methodol. 1972, 34, 187–202. [Google Scholar] [CrossRef]

- Pelaez-Verdet, A.; Loscertales-Sanchez, P. Key Ratios for Long-Term Prediction of Hotel Financial Distress and Corporate Default: Survival Analysis for an Economic Stagnation. Sustainability 2021, 13, 1473. [Google Scholar] [CrossRef]

- Zhang, J.; Thomas, L.C. Comparisons of linear regression and survival analysis using single and mixture distributions approaches in modelling LGD. Int. J. Forecast. 2012, 28, 204–215. [Google Scholar] [CrossRef] [Green Version]

- Okwo, H.; Ezenwakwelu, C.; Igwe, A.; Imhanrenialena, B. Firm size and age mediating the firm survival-hedging effect: Hayes’3-Way parallel approach. Sustainability 2019, 11, 887. [Google Scholar] [CrossRef] [Green Version]

- Schoenfeld, D. Partial residuals for the proportional hazards regression model. Biometrika 1982, 69, 239–241. [Google Scholar] [CrossRef]

- Patel, K.; Kay, R.; Rowell, L. Comparing proportional hazards and accelerated failure time models: An application in influenza. Pharm. Stat. J. Appl. Stat. Pharm. Ind. 2006, 5, 213–224. [Google Scholar] [CrossRef] [PubMed]

- Yan, J.; Williams, D.W. Timing is everything? Curvilinear effects of age at entry on new firm growth and survival and the moderating effect of IPO performance. J. Bus. Ventur. 2020. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Listing Market (L_mkt) | Year of Inception | New Name | Renamed or Merger Year | Merged With | Status |

|---|---|---|---|---|---|

| Main Board | 1974 | Main Market | 2009 | - | Active |

| Second Board | 1988 | - | 2009 | Main Market | Merged |

| MESDAQ Market | 2002 | ACE Market | 2009 | - | Active |

| Listing Market (L_mkt) | Duration | Population Total Listed IPOs | Sample IPOs | Sample Delisted IPOs | Sample Percentage | Sample Percentage Delisting | Follow-Up Period |

|---|---|---|---|---|---|---|---|

| Second Board (SB) | 1990–2009 | 461 | 432 | 151 | 93.71% | 34.95% | 6 Years (2010–2015) |

| Main Board (MB) | 1990–2009 | 325 | 272 | 86 | 83.69% | 31.62% | 6 Years (2010–2015) |

| Main Market (including MB) | 1990–2017 | 429 | 350 | 104 | 81.59% | 29.71% | 3 Years (2018–2020) |

| Main Market and Second Board | 1990–2017 | 890 | 782 | 255 | 87.87% | 32.61% | 3 Years (2018–2020) |

| ACE Market | 2002–2017 | 179 | 161 | 18 | 89.94% | 11.18% | 3 Years (2018–2020) |

| Total 1 | 1990–2017 | 1069 | 943 | 273 | 88.21% | 28.95% | - |

| Variable | Notation | Definition | Measurement | Data Source |

|---|---|---|---|---|

| Dependent Variable Survival Time | S_t | IPO tracking period (listing period + follow-up) | Number of years from listing date to delisting date or cutoff date (follow-up period), whichever is the earliest | Investor Digest, Bursa Malaysia (BM) |

| Censoring | δ | IPO listing status at follow-up cutoff date | 0 = Alive IPOs 1 = Delisted IPOs | Historical Data Package BM; delisting info BM |

| Explanatory Variables: | ||||

| Exposure Variable Listing Markets | L_mkt | IPO listing markets/listing boards | Dummy Variable 1 = Main Market/Board 0 = Otherwise | BM, IPO prospectus |

| Effect Modifiers Share Premium | S_pr | The positive difference between the offer price and par value | No. of times of the par value | IPO prospectus, Investor Digest, Historical Data BM |

| Firm Size | F_size | Pro forma total assets adjusted by utilization of IPO proceeds | Log of adjusted total assets | IPO prospectus |

| Listed Capital | L_cap | Outstanding listed pro forma capital adjusted by public issue | The ratio of outstanding shares to authorized shares | Investor Digest, IPO prospectus |

| Offer Size | O_size | Total number of shares against the public issue and offer for sale shares | Sum of public issue and offer for sale shares to total outstanding shares adjusted by new shares | IPO prospectus |

| Risk Factors | R_fac | Risk factors disclosed in IPO prospectus | Number of risk factors | IPO prospectus |

| Control Variables: | ||||

| Leverage | F_lev | Financial leverage | The ratio of total liabilities to total assets adjusted by IPO proceeds utilization | IPO prospectus |

| Firm Age | F_age | Firms age from incorporating as a private entity to the listing date | Number of years as a private firm at IPO listing date | IPO prospectus, Eikon DataStream, S&P 500. |

| Profitability | EPS | Profitability from equity investors’ perspective | Net profit attributable to equity shareholders to total outstanding shares adjusted by new shares | IPO prospectus |

| Measure | L_mkt 1 | Obs. | S_t | S_pr | F_size | L_cap | O_size | R_fac | F_Lev | F_age | EPS |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Main Market 2 | 350 | 16.30246 | 2.67866 | 8.46921 | 0.52141 | 0.25164 | 20.12857 | 0.42430 | 10.10860 | 0.46358 |

| Median(P50) | 350 | 16.03425 | 2.00000 | 8.37204 | 0.53306 | 0.24910 | 20.00000 | 0.42111 | 7.40273 | 0.21000 | |

| St. Dev. | 350 | 7.64349 | 2.41770 | 0.55817 | 0.22667 | 0.11519 | 5.19069 | 0.20964 | 9.18306 | 1.30826 | |

| Minimum | 350 | 2.71233 | 1.00000 | 7.28140 | 0.04500 | 0.00844 | 9.00000 | 0.00096 | 0.52877 | 0.01000 | |

| Maximum | 350 | 30.9726 | 25.0000 | 10.42852 | 1.00000 | 0.73802 | 33.00000 | 0.93989 | 48.23014 | 17.21000 | |

| P25 | 350 | 9.90685 | 1.55000 | 8.09596 | 0.36000 | 0.15675 | 16.00000 | 0.25984 | 1.90685 | 0.12000 | |

| P75 | 350 | 23.33425 | 2.80000 | 8.69587 | 0.68667 | 0.31451 | 23.0000 | 0.56524 | 16.56712 | 0.39000 | |

| Mean | Second Board 3 | 432 | 19.26332 | 2.42958 | 7.81756 | 0.62914 | 0.24722 | 16.60417 | 0.43460 | 7.44954 | 0.61539 |

| Median(P50) | 432 | 18.74247 | 2.20000 | 7.84194 | 0.66241 | 0.21440 | 16.00000 | 0.43431 | 4.46164 | 0.31000 | |

| St. Dev. | 432 | 6.11855 | 1.02992 | 0.27559 | 0.23545 | 0.11237 | 4.28706 | 0.17144 | 7.04759 | 1.08301 | |

| Minimum | 432 | 3.35616 | 0.80000 | 6.35237 | 0.01960 | 0.04762 | 7.00000 | 0.00600 | 0.59178 | 0.02000 | |

| Maximum | 432 | 30.88493 | 8.00000 | 8.66832 | 1.00000 | 0.68000 | 33.00000 | 0.91485 | 32.67671 | 13.0000 | |

| P25 | 432 | 14.71233 | 1.70000 | 7.63846 | 0.40000 | 0.15221 | 13.50000 | 0.30257 | 1.66986 | 0.19000 | |

| P75 | 432 | 24.43151 | 2.80000 | 8.00486 | 0.80000 | 0.30000 | 19.0000 | 0.55016 | 12.05890 | 0.57000 | |

| Mean | ACE Market | 161 | 12.72593 | 4.10111 | 7.56939 | 0.55312 | 0.24123 | 21.54658 | 0.24581 | 4.95810 | 0.13843 |

| Median(P50) | 161 | 15.03562 | 3.80000 | 7.54817 | 0.52800 | 0.25000 | 22.00000 | 0.20659 | 2.87397 | 0.04300 | |

| St. Dev. | 161 | 4.64068 | 2.04399 | 0.33177 | 0.19600 | 0.08901 | 4.37885 | 0.19117 | 5.45643 | 0.30176 | |

| Minimum | 161 | 3.17232 | 1.00000 | 6.03257 | 0.12600 | 0.00467 | 11.00000 | 0.00098 | 0.41370 | 0.01000 | |

| Maximum | 161 | 18.70685 | 12.30000 | 8.49100 | 1.00000 | 0.69400 | 31.00000 | 0.85981 | 30.64658 | 2.20000 | |

| P25 | 161 | 9.46027 | 2.50000 | 7.36152 | 0.41600 | 0.20198 | 18.00000 | 0.10417 | 1.44110 | 0.02400 | |

| P75 | 161 | 16.16986 | 5.00000 | 7.77245 | 0.67332 | 0.26900 | 25.00000 | 0.34638 | 6.55890 | 0.08200 | |

| Mean | Overall | 943 | 17.04824 | 2.80741 | 8.01705 | 0.57618 | 0.24784 | 18.75610 | 0.39854 | 8.01112 | 0.47761 |

| Median(P50) | 943 | 16.80822 | 2.30000 | 7.93715 | 0.58632 | 0.24396 | 18.00000 | 0.39765 | 4.76986 | 0.23000 | |

| St. Dev. | 943 | 6.93408 | 1.92827 | 0.54528 | 0.23112 | 0.10978 | 5.07961 | 0.20191 | 7.89919 | 1.10212 | |

| Minimum | 943 | 2.71233 | 0.80000 | 6.03257 | 0.01960 | 0.00467 | 7.00000 | 0.00096 | 0.41370 | 0.01000 | |

| Maximum | 943 | 30.97260 | 25.00000 | 10.42852 | 1.00000 | 0.73802 | 33.00000 | 0.93989 | 48.23014 | 17.21000 | |

| P25 | 943 | 11.78904 | 1.70000 | 7.66421 | 0.40000 | 0.15385 | 15.00000 | 0.24497 | 1.68219 | 0.11000 | |

| P75 | 943 | 23.19452 | 3.20000 | 8.25957 | 0.79200 | 0.30000 | 22.00000 | 0.54061 | 12.66027 | 0.43000 |

| Variable | Main Market | Second Board | ACE Market | Overall | ||||

|---|---|---|---|---|---|---|---|---|

| VIF | 1/VIF | VIF | 1/VIF | VIF | 1/VIF | VIF | 1/VIF | |

| S_pr | 1.17 | 0.851883 | 1.14 | 0.880361 | 1.25 | 0.800395 | 1.08 | 0.925182 |

| F_size | 1.27 | 0.789376 | 1.31 | 0.765597 | 1.16 | 0.864142 | 1.22 | 0.822302 |

| L_cap | 1.01 | 0.989758 | 1.06 | 0.941093 | 1.04 | 0.957045 | 1.04 | 0.957214 |

| O_size | 1.03 | 0.974681 | 1.04 | 0.956989 | 1.17 | 0.856547 | 1.01 | 0.985508 |

| R_fac | 1.24 | 0.809270 | 1.04 | 0.961294 | 1.04 | 0.959995 | 1.18 | 0.850260 |

| F_lev | 1.08 | 0.927637 | 1.21 | 0.827443 | 1.08 | 0.927709 | 1.15 | 0.866860 |

| F_age | 1.02 | 0.976099 | 1.11 | 0.897270 | 1.15 | 0.869248 | 1.06 | 0.945860 |

| EPS | 1.04 | 0.958682 | 1.13 | 0.881727 | 1.03 | 0.970610 | 1.05 | 0.952089 |

| Listing Market (L_mkt) | No. of IPOs | Delisted IPOs (δ1) | Censored IPOs (δ0) | Time at Risk tj | Hazard Rate 1 | Survival Time 2 | ||

|---|---|---|---|---|---|---|---|---|

| 25% | 50% | 75% | ||||||

| Second Board 3 (1990–2009) | 432 | 151 | 281 | 508.6851 | 0.2968437 | 14.89 | 25.39 | - |

| Main Board 3 (1990–2009) | 272 | 86 | 186 | 312.1378 | 0.275519 | 15.13 | 23.02 | - |

| Main Market 4 (1990–2017) | 350 | 104 | 246 | 403.4075 | 0.257803 | 16.05 | - | - |

| Main Market and Main Board 5 (1990–2017) | 782 | 255 | 527 | 912.4386 | 0.279471 | 15.13 | 27.12 | - |

| ACE Market 6 (2002–2017) | 161 | 18 | 143 | 170.8219 | 0.105372 | 11.70 | - | - |

| Overall (All Markets) | 943 | 273 | 670 | 1117.8223 | 0.244224 | 16.20 | 28.15 | - |

| Listing Market (L_mkt) | Events Observed | Events Expected |

|---|---|---|

| Second Board | 151.00 | 153.71 |

| Main Board | 86.00 | 83.29 |

| Total | 237.00 | 237.00 |

| Listing Market (L_mkt) | No. of IPOs | Delisted IPOs (δ1) | Censored IPOs (δ0) | Time at Risk tj | Hazard Rate | Survival Time | ||

|---|---|---|---|---|---|---|---|---|

| 25% | 50% | 75% | ||||||

| ACE Market 1 | 161 | 18 | 143 | 170.7406 | 0.105423 | - | - | - |

| Main Market 2 | 171 | 37 | 134 | 168.6655 | 0.219369 | 11.89 | - | - |

| Overall | 332 | 55 | 277 | 339.4061 | 0.1620477 | - | - | - |

| Listing Market (L_mkt) | Events Observed | Events Expected |

|---|---|---|

| ACE Market | 18.00 | 29.08 |

| Main Market | 37.00 | 25.92 |

| Total | 55.00 | 55.00 |

| Variable | Model 1: Main Board (MB) | Model II: Second Board (SB) | Model III: Combined MB and SB | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coeff. | p-Value | HR | P(PH) | Coeff. | p-Value | HR | P(PH) | Coeff. | p-Value | HR | P(PH) | |

| S_pr | −0.4521 *** | 0.003 | 0.63627 | 0.1570 | −0.2903 *** | 0.002 | 0.74798 | 0.6868 | −0.2347 *** | 0.000 | 0.69472 | 0.1724 |

| (−2.94) | (−3.12) | (−4.69) | ||||||||||

| F_size | 0.71600 *** | 0.001 | 2.04623 | 0.1839 | 1.59514 *** | 0.000 | 4.92905 | 0.2952 | 0.92963 *** | 0.000 | 2.53357 | 0.2986 |

| (3.23) | (5.10) | (5.62) | ||||||||||

| L_cap | −1.29391 ** | 0.010 | 0.27419 | 0.2185 | −0.89374 ** | 0.016 | 0.40912 | 0.8811 | −1.0342 *** | 0.000 | 0.35549 | 0.3542 |

| (−2.56) | (−2.42) | (−3.61) | ||||||||||

| O_size | 0.47465 | 0.609 | 1.60745 | 0.3097 | −0.041816 | 0.603 | 0.65825 | 0.6642 | −0.16225 | 0.788 | 0.85022 | 0.5834 |

| (0.51) | (−0.52) | (−0.27) | ||||||||||

| R_fac | 0.09594 *** | 0.000 | 1.10069 | 0.4255 | 0.10807 *** | 0.000 | 1.11413 | 0.1342 | 0.08595 *** | 0.000 | 1.08974 | 0.1992 |

| (3.74) | (5.50) | (3.67) | ||||||||||

| F_lev | 0.39941 | 0.397 | 1.49093 | 0.9354 | 0.16479 | 0.744 | 1.17915 | 0.2273 | 0.41198 | 0.215 | 1.50980 | 0.4555 |

| (0.85) | (0.33) | (1.24) | ||||||||||

| F_age | −0.03093 ** | 0.034 | 0.96953 | 0.9894 | −0.0338 *** | 0.007 | 0.96672 | 0.5347 | −0.0301 *** | 0.001 | 0.97031 | 0.8728 |

| (−2.11) | (−2.70) | (−3.29) | ||||||||||

| EPS | −0.03081 | 0.855 | 0.96966 | 0.1908 | 0.58896 | 0.400 | 1.06066 | 0.2844 | 0.031062 | 0.615 | 1.03155 | 0.2014 |

| (−0.18) | (0.84) | (0.50) | ||||||||||

| L_mkt | - | - | - | - | - | - | - | - | −0.9937 *** | 0.000 | 0.37018 | 0.1610 |

| - | - | - | - | - | - | - | - | (−5.32) | ||||

| Obs. (IPOs) | 272 | 432 | 704 | |||||||||

| Total Delisted | 86 | 151 | 237 | |||||||||

| IPO Interval | 1990–2009 | 1990–2009 | 1990–2009 | |||||||||

| Follow-up | 6 Years (2010–2015) | 6 Years (2010–2015) | 6 Years (2010–2015) | |||||||||

| Log likelihood | −412.101 | −784.285 | −1371.044 | |||||||||

| LR chi2 (8) | 49.93 | 93.72 | LR chi2 (9) = 117.68 | |||||||||

| Prob > chi2 | 0.0000 | 0.0000 | 0.0000 | |||||||||

| Variable | Model IV: Main Market (MM) | Model V: Main Market Including SB | Model VI: ACE Market | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coeff. | p-Value | HR | P(PH) | Coeff. | p-Value | HR | P(PH) | Coeff. | p-Value | HR | P(PH) | |

| S_pr | −0.4401 *** | 0.001 | 0.64392 | 0.2059 | −0.2465 *** | 0.000 | 0.781462 | 0.2464 | 0.2070 * | 0.056 | 1.23003 | 0.8292 |

| (−3.38) | (−3.64) | (1.91) | ||||||||||

| F_size | 0.48613 ** | 0.018 | 1.62601 | 0.2011 | 0.27038 ** | 0.024 | 1.31046 | 0.1604 | 1.08747 | 0.222 | 2.96676 | 0.9287 |

| (2.36) | (2.26) | (1.22) | ||||||||||

| L_cap | −0.84342 * | 0.053 | 0.43023 | 0.1712 | −0.66977 ** | 0.013 | 0.51182 | 0.2223 | −0.8305 | 0.509 | 0.043602 | 0.9071 |

| (−1.94) | (−2.47) | (−0.66) | ||||||||||

| O_size | −0.14809 | 0.857 | 0.86234 | 0.8560 | −0.43415 | 0.436 | 0.64781 | 0.4064 | −3.9501 | 0.245 | 0.01925 | 0.2054 |

| (−0.18) | (−0.78) | (−1.16) | ||||||||||

| R_fac | 0.07404 *** | 0.001 | 1.07685 | 0.2895 | 0.08062 *** | 0.000 | 1.08396 | 0.1371 | 0.04562 | 0.443 | 1.04667 | 0.5017 |

| (3.36) | (5.65) | (0.77) | ||||||||||

| F_lev | 0.77476 * | 0.087 | 2.17008 | 0.6604 | 0.78492 ** | 0.014 | 2.19224 | 0.3952 | −0.2033 | 0.884 | 0.81599 | 0.2081 |

| (1.71) | (2.45) | (−0.15) | ||||||||||

| F_age | −0.02336 * | 0.058 | 0.97690 | 0.5609 | −0.0302 *** | 0.000 | 0.97020 | 0.6410 | 0.00611 | 0.917 | 1.00613 | 0.6633 |

| (−1.90) | (−3.52) | (0.10) | ||||||||||

| EPS | −0.03372 | 0.795 | 0.966838 | 0.2778 | 0.03032 | 0.575 | 1.03078 | 0.1738 | 0.44848 | 0.523 | 1.56593 | 0.5522 |

| (−0.26) | (0.56) | (0.64) | ||||||||||

| Obs. (IPOs) | 350 | 782 | 161 | |||||||||

| Total Delisted | 104 | 255 | 18 | |||||||||

| IPO Interval | 1990–2017 | 1990–2017 | 2002–2017 | |||||||||

| Follow-up | 3 Years (2018–2020) | 3 Years (2018–2020) | 3 Years (2018–2020) | |||||||||

| Log likelihood | −527.074 | −1505.252 | −81.653 | |||||||||

| LR chi2 (8) | 42.79 | 88.30 | 11.33 | |||||||||

| Prob > chi2 | 0.0000 | 0.0000 | 0.1836 | |||||||||

| Variable | Model I: Main Board (MB) | Model II: Second Board (SB) | Model III: Overall MB and SB | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Coeff. | p-Value | HR | Coeff. | p-Value | HR | Coeff. | p-Value | HR | |

| S_pr | −0.46718 *** | 0.002 | 0.62676 | −0.28077 *** | 0.002 | 0.75519 | −0.36134 *** | 0.000 | 0.69673 |

| (−3.03) | (−3.06) | (−4.70) | |||||||

| F_size | 0.72968 *** | 0.001 | 2.07442 | 1.69018 *** | 0.000 | 5.42048 | 0.95046 *** | 0.000 | 2.58690 |

| (3.32) | (5.52) | (5.74) | |||||||

| L_cap | −1.32667 *** | 0.009 | 0.26535 | −0.95218 ** | 0.010 | 0.38589 | −1.22495 *** | 0.000 | 0.29377 |

| (−2.63) | (−2.57) | (−4.22) | |||||||

| O_size | 0.45871 | 0.620 | 1.58203 | −0.55709 | 0.486 | 0.57286 | −0.20311 | 0.736 | 0.81618 |

| (0.50) | (−0.70) | (−0.34) | |||||||

| R_fac | 0.09726 *** | 0.000 | 1.10214 | 0.10757 *** | 0.000 | 1.11356 | 0.09809 *** | 0.000 | 1.10306 |

| (3.79) | (5.47) | (6.39) | |||||||

| F_lev | 0.34886 | 0.457 | 1.41746 | 0.08898 | 0.860 | 1.09306 | 0.36154 | 0.274 | 1.43554 |

| (0.74) | (0.18) | (1.09) | |||||||

| F_age | −0.03289 ** | 0.024 | 0.96764 | −0.03740 *** | 0.003 | 0.96328 | −0.03703 *** | 0.000 | 0.96364 |

| (−2.26) | (−2.99) | (−3.94) | |||||||

| EPS | −0.02612 | 0.877 | 0.97421 | 0.06406 | 0.357 | 1.06616 | 0.04373 | 0.476 | 1.04470 |

| (−0.15) | (0.92) | (0.71) | |||||||

| L_mkt | −1.09828 *** | 0.000 | 0.33344 | ||||||

| (−5.83) | |||||||||

| _Cons | −13.6148 *** | 0.000 | 1.22 × 10−6 | −23.6359 *** | 0.000 | 5.43 × 10−11 | −16.04666 *** | 0.000 | 1.07 × 10−7 |

| (−7.04) | (−8.81) | (−11.35) | |||||||

| /ln_p | 0.77589 *** | 0.000 | - | 1.15824 *** | 0.000 | - | 0.99056 *** | 0.000 | - |

| p | 2.17253 | - | - | 3.18434 | - | - | 2.69274 | - | - |

| 1/p | 0.46029 | - | - | 0.31403 | - | - | 0.37136 | - | - |

| Obs. (IPOs) | 272 | 432 | 704 | ||||||

| Total Delisted | 86 | 151 | 234 | ||||||

| IPO Interval | 1990–2009 | 1990–2009 | 1990–2009 | ||||||

| Follow-up | 6 Years (2010–2015) | 6 Years (2010–2015) | 6 Years (2010–2015) | ||||||

| Log likelihood | −168.893 | −224.090 | −404.83729 | ||||||

| LR chi2 (8) | 51.97 | 102.43 | 139.51 | ||||||

| Prob > chi2 | 0.0000 | 0.0000 | 0.0000 | ||||||

| Variable | Model IV: Main Market (MM) | Model V: Main Market (MM) Including Second Board (SB) | Model VI: ACE Market | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Coeff. | p-Value | HR | Coeff. | p-Value | HR | Coeff. | p-Value | HR | |

| S_pr | −0.45706 *** | 0.001 | 0.63314 | −0.23559 *** | 0.000 | 0.79009 | 0.23023 ** | 0.037 | 1.25890 |

| (−3.48) | (−3.51) | (2.08) | |||||||

| F_size | 0.47001 ** | 0.021 | 1.60001 | 0.21605 * | 0.068 | 1.24116 | 1.14890 | 0.190 | 3.15475 |

| (2.31) | (1.83) | (1.31) | |||||||

| L_cap | −0.89913 ** | 0.038 | 0.40692 | −0.72069 *** | 0.008 | 0.48641 | −0.87942 | 0.480 | 0.41502 |

| (−2.08) | (−2.66) | (−0.71) | |||||||

| O_size | −0.07236 | 0.929 | 0.93018 | −0.49420 | 0.376 | 0.61005 | −3.54465 | 0.290 | 0.02887 |

| (−0.09) | (−0.89) | (−1.06) | |||||||

| R_fac | 0.07639 *** | 0.001 | 1.07938 | 0.08045 *** | 0.000 | 1.08378 | 0.04623 | 0.443 | 1.04732 |

| (3.46) | (5.62) | (0.77) | |||||||

| F_lev | 0.71214 | 0.116 | 2.03835 | 0.73366 ** | 0.021 | 2.08269 | −0.23095 | 0.868 | 0.79377 |

| (1.57) | (2.31) | (−0.17) | |||||||

| F_age | −0.02530 ** | 0.040 | 0.97501 | −0.03344 *** | 0.000 | 0.96710 | 0.01366 | 0.813 | 1.01375 |

| (−2.06) | (−3.90) | (0.24) | |||||||

| EPS | −0.02984 | 0.822 | 0.97059 | 0.03899 | 0.467 | 1.03977 | 0.52777 | 0.455 | 1.69515 |

| (−0.23) | (0.73) | (0.75) | |||||||

| _Cons | −10.54 *** | 0.000 | 0.000026 | −9.63597 *** | 0.000 | 0.000065 | −15.12096 ** | 0.028 | 2.71 × 10−7 |

| (−6.13) | (−9.32) | (−2.20) | |||||||

| /ln_p | 0.60666 *** | 0.000 | - | 0.78814*** | 0.000 | - | 0.25813 | 0.237 | - |

| p | 1.834312 | - | - | 2.19931 | - | - | 1.29451 | - | - |

| 1/p | 0.54516 | - | - | 0.45468 | - | - | 0.77249 | - | - |

| Obs. (IPOs) | 350 | 782 | 161 | ||||||

| Total Delisted | 104 | 255 | 18 | ||||||

| IPO Interval | 1990–2017 | 1990–2017 | 2002–2017 | ||||||

| Follow-up | 3 Years (2018–2020) | 3 Years (2018–2020) | 3 Years (2018–2020) | ||||||

| Log likelihood | −228.548 | −496.19335 | −64.24333 | ||||||

| LR chi2 (8) | 45.07 | 86.45 | 12.13 | ||||||

| Prob > chi2 | 0.0000 | 0.0000 | 0.1456 | ||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ahmad, I.; Ismail, I.; Shaharuddin, S.S. Predictive Role of Ex Ante Strategic Firm Characteristics for Sustainable Initial Public Offering (IPO) Survival. Sustainability 2021, 13, 8063. https://doi.org/10.3390/su13148063

Ahmad I, Ismail I, Shaharuddin SS. Predictive Role of Ex Ante Strategic Firm Characteristics for Sustainable Initial Public Offering (IPO) Survival. Sustainability. 2021; 13(14):8063. https://doi.org/10.3390/su13148063

Chicago/Turabian StyleAhmad, Iftikhar, Izlin Ismail, and Shahrin Saaid Shaharuddin. 2021. "Predictive Role of Ex Ante Strategic Firm Characteristics for Sustainable Initial Public Offering (IPO) Survival" Sustainability 13, no. 14: 8063. https://doi.org/10.3390/su13148063

APA StyleAhmad, I., Ismail, I., & Shaharuddin, S. S. (2021). Predictive Role of Ex Ante Strategic Firm Characteristics for Sustainable Initial Public Offering (IPO) Survival. Sustainability, 13(14), 8063. https://doi.org/10.3390/su13148063