2.1. Designation as the Most Admired Firms

Being selected as the most admired firms is the management’s new paradigm that spreads all over the world. The Fortune’s America’s Most Admired Companies (AMAC) is widely used to measure firms’ reputation. Since the list is independent, available to the public, and covers a wide range of companies and industries, it is by far the most representative when measuring reputation [

2,

4,

11,

12,

13]. Firms with the highest scores are considered highly reputable [

4].

In South Korea, KMAC consulting is the only research institute in the field of respected firms. KMAC consulting developed a research model that comprehensively evaluates the values of the entire firm since 2004. The KMAC is about acquiring excellent competitiveness confirmed through continuous innovative activities. It is the driving force for achieving excellent management results as an important success factor that discriminates against other companies based on its innovative ability to flexibly respond to changes in the business environment and lead the business environment.

Table 1 below is the evaluation criteria suggested by KMAC consulting. As shown in

Table 1, the candidate companies are selected based on market size by industry and industrial competition. The survey is conducted using the Internet, interviews, telephone calls, and faxes so that a more accurate survey could be conducted in consideration of the situation of the survey subjects. In the case of an industry-specific survey, where more expert and accurate surveys are needed, the executives and analysts are surveyed. Doing so brings a correct understanding and interest in corporate activities to consumers and several other stakeholders by providing directions on what companies will be respected. By recognizing the company’s current position, it seeks to company’s development and presents the direction of enterprise-wide technological innovation under a new paradigm.

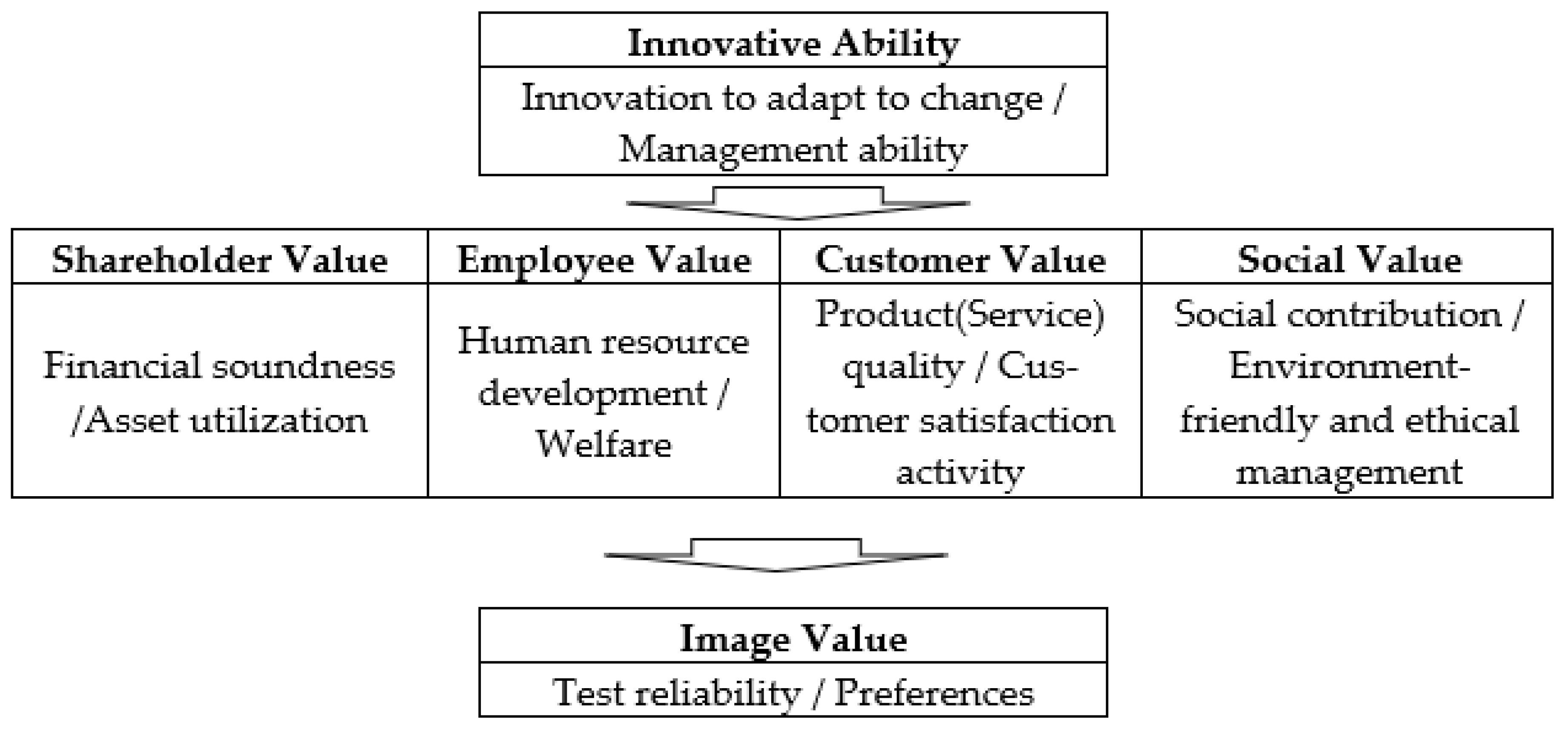

Figure 1 shows the modified figure from the KMAC consulting homepage, which displays criteria used for KMAC consulting. The most admired firms’ criteria are the six core values of shareholders, employees, customers, social, and image. With an innovative ability as a base, the values of shareholders, employees, customers, and social are integrated into image value. Then, the values are integrated to calculate and announce index for KMAC. Finally, the survey results are converted to the scores, and these scores are the rankings of admired companies.

Selected as being admired can be viewed as a process of acquiring a reputation. Barnett et al. (2006) [

15], Cao et al. (2012) [

4], and Cao et al. (2015) [

2] provide the theoretical framework of reputation and postulate that reputation is comprised of collective assessments based on a firm’s long-term behavior. The reputation is higher than a favorable feeling and takes a long time to form trust, confidence, and support [

16]. In general, the reputation, once settled, has characteristics that do not change easily [

17]. The firms with higher reputations are considered accountable, credible, and trustworthy [

18]. In addition, reputation is one of the intangible assets that are difficult to copy, making it a sustainable competitive advantage [

19]. Reputation is vital for the future of industry as companies need to be differentiated when selling their products. Reputable companies concentrate on innovation and product quality to elevate value [

5] for their sustainable existence.

According to the agency theory, reputable firms are expected to reduce information asymmetry among the firms’ stakeholders [

5] because those firms focus on product quality and innovative processes. Reputable firms increase the transparency of the firm’s information environment, and reinforce accounting information accuracy and quality.

Several studies are showing that the reputation, measured as the most admired firms, show the excellent investment performance. Antunovich and Laster (2003) [

12] examine the relationship between the firms with the rankings from Most Admired Companies from Fortune in the U.S. on stock price in a market. The result shows that the firms with the highest scores on the Most Admired Companies are superior to the firms with low scores. Lee and Kim [

20] finds the positive effect of the admired firms on the firm value. These positive scores of the admired firms can be interpreted as being related to the value to the company beyond providing financial information. The non-financial components of these companies’ reputation scores can be the evidence of intangible assets, explaining corporate value.

Reputation also has significant impacts on the market [

2]. First, the firms with good reputations mean the firms with a high level of understanding for the distribution of quality and capabilities and business performance consistent with shareholders. In other words, reputation means that the firms have high-quality management with talented employees and technological innovation, and the factors are value-relevant but difficult to observe. Second, reputation ranking attracts social attention through media. As the firm attracts attention, its stock is of interest to investors, yielding a low equity cost. Firms’ reputation also means high-quality financial reports [

4], reducing information asymmetry [

21]. Information asymmetry reduction lowers the firm’s cost of equity.

2.2. Tax Management

Taxes are forcibly collection from the firms rather than voluntarily. Tax collection from the public is used for financing public expenditure, such as investing in infrastructure, education, and health, regulating social and economic behavior, and redistributing wealth [

22]. Though imposing taxes is inevitable, managing taxes is essential for growth and sustainable development. Hilling and Ostas (2017) [

22] define two ways of managing tax, and they are mitigation and avoidance. Tax mitigation and tax avoidance are in common in that they reduce taxes and are within the law. However, the former incur within the boundary of government intention, while the latter deviates from the intention.

In this study, we focus on tax management in the aspect of tax avoidance. If firms are involved in tax avoidance, there might be an opportunistic behavior that entails direct costs, such as implementation and reputation costs from punishment [

23]. In other words, firms being involved in less tax avoidance not only means a low possibility of managerial opportunism, but also increases the transparency and reliability of accounting information, which will increase firm value [

24,

25].

Studies have examined the factors affecting tax avoidance. Ki [

26] found a negative association between corporate social responsibilities (CSR) activities and tax avoidance. As the firms invest in CSR activities, there is a low possibility of avoiding taxes. Kim and Kwon [

27] examined the effects of CSR activities and the independence of audit committees on tax avoidance. They report that firms that participated in CSR are more likely to avoid taxes than matching firms, indicating that CSR is an effective tax strategy. Armstrong et al. (2016) [

28] reported that in a group with high tax avoidance, the firms with the board with financial expertise and independence less likely avoid tax. The result indicates that good governance reduces the likelihood of avoiding taxes. Gallemore and Labro (2015) [

29] examined the internal control on tax avoidance. Internal control plays a critical role in tax management. Internal control and the ability to monitor management behavior can help ensure the establishment of effective tax planning that can be enforced at the enterprise-wide level. By improving the timeliness and reliability of the financial information, effective internal control reduces the tax risk. Khurana et al. (2018) [

30] investigate tax avoidance in accordance with managerial ability. They define managerial ability as the ability to convert corporate resources for profit, and managers with high capabilities will efficiently allocate the limited resources within the firm to obtain maximum profit. Managers with high abilities will consider tax avoidance as the factor for reducing firm value. Thus, highly capable managers will try to make tax plan to decrease tax avoidance to increase firm value. To sum up, the tax avoidance level lowers depending on the propensity and strategic choice of the firm, which will guide the firm value increment.

There are prior studies that have examined the consequences of tax management. Hanlon and Slemrod (2009) [

31] and Lee and Jung (2008) [

32] showed the market reaction in accordance with the tax avoidance. Both the research suggested that less tax avoidance impact stock market positively. Balakrshman et al. (2014) [

33] reported the firms with low tax avoidance will increase corporate transparency. Low tax avoidance means that the firms’ accounting procedures and environment are traceable and transparent. Improved firms’ transparency will increase firm value by reducing the information asymmetry among stakeholders, increasing capital market efficiency, reducing the investment uncertainty and reducing the cost of capital. Kang (2019) [

6] examined the association between tax avoidance and corporate transparency. The result suggests that the firms involved less in tax avoidance have increased transparency, which plays a vital role in reducing information asymmetry among shareholders, improving capital market efficiency, reducing investment uncertainty, and reducing the cost of capital. Corporate transparency is also associated with preventing corruption, reducing the risks related to shareholder wealth. Chun et al. (2020) [

34] examined the effect of tax avoidance on the cost of equity capital in accordance with the level of the legal environment. They found that the firms in a strong legal environment make tax plans positively incremental to firm value, while the firms in a weak environment use tax avoidance to exploit their personal benefits, yielding high equity risk premiums.

2.3. Hypothesis Development

Thanks to the development of the Internet and social networks, the impact of corporate image on profitability has increased more than in the past. Achieving a high reputation of the company is a gradual process, and overall assessment is built over a long period. It is difficult to copy, but sustainability and competitiveness are earned once a reputation is achieved [

19]. When a firm gains a reputation, it may enjoy the benefits and impact the market positively (Cao et al., 2015) [

2], such as low cost of capital, high-quality management (Khurana et al., 2018) [

30], and higher financial reporting quality (Cao et al., 2012 [

4]).

In the field of accounting study, whether the firm is reputable or not is measured by the scores in KMAC’s index of the most admired firms in South Korea, where the higher the score the better reputation. Being admired implies that the firms are noticeable and visible in the market. Therefore, according to agency theory, reputable firms are recognizable by the investors and stakeholders. In addition, the theory suggests that reputable firms are expected to reduce information asymmetry among the firms’ stakeholders (Kim et al., 2020 [

5]), because those firms signal that they focus on product quality and innovative processes. Thus, reputable firms increase the firms’ information environment’s transparency and reinforce accounting information accuracy and quality.

Firms are the groups for pursuing the maximization of corporate value. Thus, there is a great deal of incentive to minimize actual cash out, such as corporate tax costs. Managing taxes as a strategy to reduce explicit or implicit tax burden enhances the firm value and relates to firms’ sustainability [

35]. Firms sustainably managing taxes are willing to contribute their fair share so that the government can earn adequate tax revenue. In this study, we focus on tax avoidance as a tool for measuring tax management. Tax avoidance is within the boundary of legality, but it can be viewed as unethical or immoral [

22]. If firms are less likely to engage in tax avoidance, their existence will be sustained in the long run [

36]. In addition, firms involved in tax avoidance are labeled as poor corporate citizens, negatively affecting sales [

37]. For example, in early 2000, several firms in the U.S. moved their headquarters to tax havens, saving huge costs on taxes. However, even though the firms save taxes, they experienced a stock crash afterwards [

38]. This means that such firms have been able to save huge taxes, but the firms are accused of being unpatriotic in the media, and the stock has fallen sharply due to these effects. In 2012, Starbucks did not pay any corporate tax in the U.K. despite the huge increase in sales. Negative public opinion caused a boycott against Starbucks stores, a significant decline in corporate reputation, and the closure of many stores [

39]. Even though Starbucks claimed to be compliant with British tax law, reputational damage caused Starbucks to pay tax voluntarily afterward.

According to game theory, fame is regarded as a distinctive characteristic or a signal that an organization establishes a competitive advantage. In a repeated game where one player has private information about the type, other players use the players’ reputation to form their own beliefs and choose their decision strategically to maximize their future benefits. It is called the reputation effect, which reduces agency problems [

2]. The consumers are likely to rely on the reputation since the consumers are the ones who have less information than managers. Similarly, outside investors lack information than managers about the firms’ future action, so a good corporate reputation will allow management to act in ways consistent with fame. Players with a certain level of reputation have an incentive to offset the immediate consequences of the current decision with the long-term impact of reputation [

18]. Firms with reputations are reluctant to engage in activities that may affect the firm’s reputation negatively. Therefore, highly reputable firms may take steps to protect their reputation by not participating in aggressive tax planning. Thus, we conjecture our first hypothesis as follows.

Hypothesis 1 (H1). The firms designated as the most admired firms are less likely to avoid taxes.

With the digitalized environment, information such as corporate immoral management activities and negative results of companies is quickly transmitted to consumers worldwide, which not only reduces the sales of the companies but also has a fatal effect on the companies’ reputation. In addition, global companies recognize that it is an era in which the company’s survival is threatened if problems such as ethics, environment, and labor occur in corporate activities. Thus, concern for Environment, Social, and Governance (ESG) is more than emphasized.

ESG is an extension of corporate social responsibility (CSR), and there are two different perspectives regarding CSR [

40]. First, CSR is viewed as philanthropic and ethical, and it is firm-value neutral and enhances brand value and reputation. In this view, participating in CSR activities can increase long-term corporate value resulting from increased sales, secure human resources, and strengthening the corporate image. ESG activities are believed to be an organization’s shared belief that considers the economic, social environment and other external impacts of corporate behavior [

10]. Hoi et al. (2013) [

10] suggest that the firms with CSR activities are regarded as taking long-term profits by building a positive image, and those firms are reluctant to avoid taxes because of the negative image that it might bring. Thus, ESG motivates the firm to maintain the value of admiration and is likely to forgo excessive tax.

The other perspective is the opportunistic point of view. The opportunistic perspective is that CSR is conducted in a short period of time to support management decisions. In addition, it is used as a means to achieve the private interest of managers, hindering the interests of shareholders and often results in degrading corporate performance [

41]. In this view, aggressive tax avoidance may damage the reputation of companies and business owners and impose potential fines by the tax authorities [

42]. As a part of managing risk, the firm can use ESG activities opportunistically as a pre-defense mechanism against the punishment in the event of a negative incident. Davis et al. (2016) [

43] concluded that CSR activities are considered a tool for building positive image, but firms that actively avoid taxes carry out CSR activities to offset their negative image. Lennox et al. (2013) [

44] found that the firms accused by the SEC of fraudulent accounting had less tax avoidance. This shows that aggressive financial reporting is a more strategic choice of the company, which indicates that such companies have avoided fewer taxes to hide their choices.

In the case of a company that is actively engaged in CSR, if the tax authorities confirm the fact of tax evasion due to tax avoidance, the impact on stakeholders with various investors may significantly damage the corporate image. On the other hand, in the case of companies that do not, even if the tax authorities reveal the tax evasion due to tax avoidance, it can be expected that the impact will be less than that of companies that are active in CSR [

45]. Hilling and Ostas (2017) [

22] argue that firms should comply with tax laws and resist the temptation to take advantage of loopholes, ambiguities, and flaws in legal texts. Taking those perspectives together, we attempt to analyze whether the firms designated as the most admired firms with ESG negatively affect tax avoidance, and we build our second hypothesis as follows.

Hypothesis 2 (H2). Firms that are designated as admired firms and who engage in ESG are less likely to avoid taxes.

{kind=link}