Abstract

Building upon prior literature on the role of executives in tax payments, this study investigates the relationship between a CEO’s political connections and tax avoidance behavior as a typical type of social irresponsibility of a corporation. We propose that CEOs who are well connected to politicians through family, academic, and professional ties tend to adopt riskier strategic choices such as tax avoidance. We employ a multi-faceted method to quantify political connections in a more comprehensive and delicate way. Empirical results from 4,706 firm-year observations in South Korea between 2003 and 2014 provide support for our predictions. In addition, we test competing hypotheses on the moderating role of CEO tenure and find that such a tendency diminishes as the focal CEO stays in the position longer.

1. Introduction

Tax payments make up a large part of the costs in business operations. Improving firm profitability can be done through increasing financial accounting earnings as well as reducing tax expenses. It is important for CEOs to legally reduce tax payments and gain tax benefits, and the in-house tax divisions use their tools at their disposal to reduce tax obligations [1]. As tax expenses increase in association with financial performance, the contradiction translates to a big difference between the accounting income and the taxable income. This is called the book-tax difference (BTD). Among many empirical studies that analyzed BTD for earnings quality [2,3], Hanlon [4] concluded that the reported BTD is potentially a red flag for investors.

In association with corporate transparency and sustainability, tax avoidance or sheltering has received increasing attention from both policymakers and academics [5]. However, most prior empirical studies have been conducted on cross-sectional variations in tax avoidance that are influenced by firm-level factors such as the scale of international operations [6], financial leverage [7,8], and management incentives [9,10,11]. Recently, there has been some research on executives’ role in tax avoidance [5,12]. Among them, Dyreng, Hanlon, and Maydew [12] found that individual top executives have incremental effects on a firm’s tax avoidance which could not be explained by other firm factors such as current and past profitability, or R&D intensity. There were also studies on the impact of managers’ political orientation on corporate tax avoidance [13,14]. This study describes a firm’s tax avoidance behavior as corporate social irresponsibility (CSIR) and aims to explore the antecedent factors that can influence it.

Prior studies have demonstrated that politically connected CEOs create and attain economic advantages from their network advantages [15,16,17,18]. These advantages include gaining new business opportunities and overcoming difficulties through the government’s favorable treatment or policies [19]. By analyzing the political connections of CEOs, one could assume certain strategic decisions that will be made by those CEOs. For example, political connections influence strategic decisions such as financing [20], quality of accounting information [21], and corporate social responsibility (CSR) activities [22,23]. Existing studies have also emphasized that CSIR is related to performance in terms of market value, financial evaluation, performance prediction, and financial risk [24].

Recently, studies began to examine the relationship between corporate political activities (CPA) and tax avoidance [25]. Politically connected firms tend to disclose accounting reports of low quality [21] to manipulate net earnings and therefore expose them to high tax aggressiveness. However, politically sensitive contractors tend to pay high tax costs and those that have high bargaining power over governments tend to lower tax expenditure [26]. Although tax decisions are made based on the internal accounting system, they are also made strategically depending on the external relationships. Moreover, firms tend to lower taxes through tax-related CPAs and political lobbying activities [27].

Building upon prior studies on the roles that executives play in tax avoidance [5,12], this study investigates the effects of CEO political connections on tax avoidance as a prevalent type of CSIR in companies listed on the Korean stock exchange. In addition, we examine the moderating role of CEO tenure on the relationship between CEO political connections and tax avoidance behavior.

2. Theory and Hypotheses

2.1. Corporate Social Irresponsibility and Tax Avoidance

Research on CSR and CSIR has basically centered around how social norms, markets, and institutions can create profits while solving complex social problems individually or jointly [28]. Among several possible antecedents of CSR and CSIR, this paper focuses on the role of key decision-makers. For example, Dharwadkar et al. [29] showed that directors with a legal background are more likely to understand the context of legal and institutional complexities in order to deal with CSIR-related issues effectively. In other words, there is a possibility that corporate decision-makers who have a good understanding of legal and institutional voids are placed in a situation where they can think about tax avoidance as a means to maximize profits while preemptively predicting various risks that companies can confront [30].

CEOs endeavor to increase accounting income, which is the indicator of firm performance while attempting to decrease the overall tax payment within the legal boundary. To achieve both purposes, BTD takes place, and this difference leads to tax avoidance. It is easy to identify BTD as accounting income and taxable incomes are measured for different purposes and are reported based on different rules. Accounting rules are used in order to measure the future value of the firm, whereas tax rules are formed as the social consensus for political purposes.

Although accounting income and taxable incomes are reported and audited by third-party accountants, there is room for opportunistic and irresponsible behaviors during the tax reporting process [9,31]. In some cases, such behaviors could be justifiable, but their actions tend to be counter-normative. Particularly in a society with weaker investor protection and tax regulation enforcement, these actions tend to lead to fraudulence [32]. Extant empirical research shows that counter-normative behavior leads to higher costs for firms from lawsuits, financial losses through settlement, declining sales, and increases in the cost of capital which could also extend to market share deterioration and other costs associated with a negative reputation [33,34].

Therefore, tax avoidance is controversial in nature in terms of credible communication and sustainable management [13]. Some scholars argue the opposite opinion, as low effective tax rates and future tax rate volatility do not increase future stock price volatility, and therefore tax avoidance is not risky [35]. However, such a conclusion is based on ex post facto analysis that does not take into account potential risks that did not take place.

There are two kinds of risks associated with tax avoidance. First, there is the risk of additional taxation. Large BTD aiming at tax avoidance measures attracts tax investigators. When confirmed, firms are liable for the additional tax, which puts the entire firm at high risks. Wilson [36] also warned about the riskiness of individual tax shelter behaviors, as they can expose firms to fines, penalties, and other risks. When firms have high exposure to the government or their business performance is highly dependent on the government, tax avoidance could have a bigger impact on the overall firm performance [26]. In order to avoid such risks, lobbyists, in-house tax specialists, or third-party accountants are hired. One can refer to the case that Enron paid $88 million in fees to its tax advisers to avoid paying $2 billion of taxes in the US [37].

Firms’ opportunistic behaviors have been analyzed by various scholars. Efendi et al. [38] showed that the more in-the-money stock options a firm has, the more it is likely to misstate financial statements. Firth et al. [39] showed that when firms are highly leveraged or are planning for issuing more equities, CEOs are likely to manipulate and report falsified financial statements. However, misreporting leads to high bank loan contracting that could in the end become a serious drawback to the company [40]. There are various punishments for corporate financial fraud [32]. Tax avoidance, itself, is not a fraudulent act, but a huge BTD may lead to punitive taxes.

Second, the reputational risk should be noted. When tax avoidance is revealed, it is very likely that firms receive severe criticism from the general public for being socially irresponsible, and therefore, tarnish their own reputation. Tax duty is the basic responsibility of a member of society, such that excessive tax avoidance creates unfairness and mistrust among the members of the society [41]. Hoi et al. [42] also stated that socially irresponsible firms tend to avoid tax payments. Lanis and Richardson [43] showed that firms that are transparent about their CSR disclosures tend to lessen tax aggressiveness. Although many big firms publish reports that contain socially responsible conduct, it is already well known that even these companies engage in large-scale tax avoidance and evasion [37], and therefore, they are conceived as hypocritical. Apart from tax investigation, firms that have the stigma of tax avoidance will be perceived negatively in their future businesses. Social irresponsibility will tarnish not only firm brands but also individual reputations. If a CEO is stigmatized for financial fraud, her or his reputation will be seriously harmed in the executive labor market and among the general public [33]. This applies similarly to board members as well [44].

2.2. CEO Political Connections and Tax Avoidance

Leuz and Oberholzer-Gee [20] examined the relationship between political connections and global financing and found that politically connected firms tend to raise domestic capital by choosing to remain less transparent. If firms are transparent in foreign financing, it is difficult to gain political benefits as well. Therefore, firms that are politically well connected at home tend to use their connections in making important strategic choices and therefore this makes firm operations and businesses less transparent over time. This process shows clearly in accounting books. Chaney, Faccio, and Parsley [21] showed that politically well-connected firms tend to have a poorer quality of earnings than those that are less connected. As the connected firms face less market pressure to be transparent, they tend to disclose lower quality accounting information. Even if they face social pressure, they are protected by politicians from getting penalized for their low-quality accounting information.

One of our interviewees for this research, who is a former member of the National Assembly of Korea, commented that “Tax investigation is one of the most sensitive issues for companies. It is very difficult for politicians to directly influence tax investigations, but CEOs in Korea tend to perceive that their political connections will help them to get away from unfavorable investigations.” Although most CEOs are not tax experts, they make decisions regarding the ins and outs of common tax strategies [12]. While tax avoidance entails reputational risks and nontax risks [1], CEOs with political connections may avoid such risks associated with tax avoidance for the following reasons.

First, a CEO’s strategic choices for tax avoidance can depend on confidential information she or he acquired on the government’s plans for tax policies in the future. Politically connected firms have easier access to legislators [23,45] and could obtain confidential information in advance to strategically plan for tax evasion and therefore mitigate such associated risks. In the US, such information is acquired through lobbyists or tax experts, while in less advanced countries, such information is often acquired through communications among unofficial elite groups.

Second, politically connected firms tend to effectively deal with tax detection risks. Duchin and Sosyura [46] argued that political connections served as an insurance mechanism against extreme events. Kim and Zhang [31] showed that in the US, tax aggressiveness was more prevalent among firms that were associated with politicians (e.g., firms that appointed ex-politicians as their board members). In other words, politically connected firms tend to avoid tax detection via their lower quality disclosure [21]. In the case of Korea, political connections are not formed primarily through political lobbying but rather established through personal informal ties. Such informal connections also serve as an insurance mechanism against tax detection risks.

Third, the more politically connected a CEO is, the more acute she or he is in dealing with reputational risks or other nontax risks. If a firm were to be socially perceived as an irresponsible member of society that evaded taxes, it would be difficult to repair the tarnished reputation. Multinational companies such as Google, Apple, and Starbucks have been severely criticized for their tax evasion [47]. However, if these firms were politically well connected, they would be more likely to effectively overcome such reputational risks despite the pressure from the media and the general public. The underlying basis to connect businessmen with politicians is a coalition built in elite groups in power. CEOs that are members of such a coalition will be better able to tackle reputational risks against the media than those who do not belong to that circle.

In short, political connection influences strategic choices of tax avoidance. Richter, Samphantharak, and Timmons [27] showed that companies in the US that have high lobbying expenditures tend to spend less on tax payments. Specifically, a 1% increase in lobbying expenditure leads to a 0.5~1.6% reduction in tax payments. Adhikari et al. [48] found out that politically connected Malaysian firms pay significantly lower effective tax rates. Similarly, political rent-seeking is prevalent and highly lucrative in China for lower tax rates and politically connected firms have gained preferential treatment from tax investigators for fraudulent financial reporting [49]. Therefore, CEOs with high political connections have higher access to confidential information, and thus, could prevent them from tax detection risks and mitigate reputational risks. This mechanism increases the CEO’s tendencies to seek tax avoidance. Based on the arguments presented thus far, we develop the following hypothesis.

Hypothesis 1 (H1).

CEO political connections are positively associated with a firm’s tax avoidance behavior.

2.3. The Moderating Role of CEO Tenure

The neoclassical view of the firm holds that human resources, including the CEOs, are homogeneous and substitutable [50]. In reality, however, they are heterogeneous; there are big differences in the capabilities of managers, and such differences influence a firm’s behavior and performance accordingly [51,52,53]. A CEO, as the representative of the company, has a great influence on the firm’s decisions. However, CEOs are not tax experts and they only make decisions for the ins and outs of common tax strategies [12].

Several studies have revealed that a manager’s individual preference affects the firm’s voluntary disclosure and financial reporting outcomes [54,55]. A CEO’s tenure affects firm decisions [56]. Yet not much light has been shed on the role of a CEO’s tenure on tax avoidance. Among the few, Dyreng, Hanlon, and Maydew [12] found that CEOs who had more experience of tax aggressiveness in previously occupied firms tended to make more aggressive decisions on tax avoidance. However, no attention has been paid to the relationship between CEO tenure in the current firm and tax avoidance. Based on the two theoretical considerations below, we develop competing hypotheses on the moderating role of CEO tenure between CEO political connections and tax avoidance behavior.

From the perspective of personal capabilities and experiences, on the one hand, CEOs with longer tenures will be better able to take strategic decisions regarding tax shelters. Hambrick and Fukutomi [57] argued that the more experienced CEOs were, the more likely they would be to have a greater breadth and depth of capabilities than younger and less tenured leaders. Long-tenured CEOs might have acquired a good deal of knowledge and skills regarding their organizations, businesses, regulations, and various dimensions of management. Likewise, a CEO’s tenure implies more knowledge, skill repertoires, and experiences accumulated around tax avoidance as well [49]. This would lead them to work cleverly around the rules and regulations and utilize them favorably for tax avoidance. Thus,

Hypothesis 2a (H2a).

CEO tenure positively moderates the positive relationship between political connections and tax avoidance behavior.

From the perspective of personal motivation and power, on the other hand, when CEOs extend their terms, they will have less incentive to take risks associated with aggressive tax reduction. During the early years in the position, most CEOs need to prove their qualifications and gain support from corporate stakeholders and may try to utilize political connections to minimize tax payments. However, as a CEO stays longer in the position, her or his status in the firm tends to stabilize, which contributes to the accumulation of power as well as experiences [58]. In this situation, CEOs may perceive latent risks associated with tax avoidance leveraged by political connections more seriously and refrain from aggressive tax strategies. Given the accumulated power in the current organization, CEOs with longer tenures will be less motivated by short-term performance increases and even feel aggressive tax avoidance unnecessary. In addition, longer-tenured CEOs tend to manage long-term personal reputations in the executive labor market and among the general public. Therefore, as CEO tenure lengthens, CEO political connections can mitigate risk-taking tendencies for tax avoidance based. Thus,

Hypothesis 2b (H2b).

CEO tenure negatively moderates the positive relationship between political connections and tax avoidance behavior.

3. Method

3.1. Data and Sample

This study employed a sample of companies listed on the Korea Stock Exchange from 2003 to 2014. We collected data from the Korea Information Service (KIS) database, which provides corporate profiles and financial information. The KIS is a leading credit-rating agency and the biggest corporate information provider in Korea, and their database has been widely used in previous research based on samples of Korean firms [59]. This study excluded financial services firms from the sample, because their accounting schemes are different to some extent from those in other industries. We selected firms with the most common fiscal year—from January to December. In addition, we analyzed companies that reported a positive net profit before tax. To alleviate distortions coming from outliers of dependent and independent variables, we winsorized the top and bottom 1% of all continuous variables. Our final sample contained 614 firms with 4,706 observations over 12 years.

Information on CEOs was collected from several sources. First, the CEO’s name was identified on the first page of the firm’s annual report, and CEO tenure information was manually gathered from the annual reports on the Data Analysis Retrieval and Transfer System (DART) provided by the Financial Supervisory Service. CEO biographical information was pulled from KISLINE and the databases for Korea’s three major newspapers [60,61,62]. KISLINE provides background information regarding education, family, friends, and careers. The databases for Korea’s three major newspapers include the political careers of corporate decision-makers. Government websites [63,64] provide more detailed information on the roles that CEOs have played in politics—e.g., as members of the assembly and the cabinet. In-depth personal information was collected from various sources provided by one of Korea’s major search engines [65], mainly on CEO regional and educational backgrounds, national examination certificates, and work history. In the cases of missing political information, the three major media databases were used. Other in-depth personal information was collected from Naver.com (accessed on July 2020) which is the most popular internet portal in Korea, The Map of Personal Connections in Korea, The Legacy of Chaebol Families, and The 58 Power Groups in Business Circles.

3.2. Measures

3.2.1. Dependent Variable

We adopted the methods used by Desai and Dharmapala [66], which capture tax avoidance tendencies from the differences between accounting income and taxable income that cannot be explained. As can be seen from Equation (1), the residual BTD is determined from the regression analysis. The firm and year fixed effect model was used to extract the residual. The taxable income was calculated using income tax expense + {(deferred tax assetst − deferred tax assetst−1) − (deferred tax liabilitiest − deferred tax liabilitiest−1)}, then divided by the tax rate. The total accruals were calculated by subtracting the operating cash flow from the net income [67], divided by the beginning of year assets.

where:

- book-tax difference for firm i in year t; and

- total accruals for firm i in year t.

3.2.2. Independent Variable

We counted political connections from three types: (1) family ties and marital relationships; (2) educational background based on high schools or universities; (3) professional ties examining whether the CEOs passed one of the four major national entrance exams for legal, government, diplomatic, and technical officials. These political connections are strong in nature and are formed within the closed inner circle of people. This paper counts political connections from all these three types that the executives have cultivated in the past [68]. For example, if a CEO graduated from an elite school such as Gyeonggi High School, then politicians from the same high school were all considered. The same applied to all educational degrees. In the case of family ties, politicians in the CEO’s family were all counted. As the alumni among those who passed major national entrance examinations also form a strong elite group in Korea, the number of politicians who passed the exams in the same year were counted as eligible political connections.

The ratings of these ties were calculated in relative terms in that a CEO with the highest number of ties was given the highest score of one, and those that followed were given lower scores in proportion to their number of ties. This is a more sophisticated and improved method compared to the ones used by Siegel [69] that measured political capital with CEO’s educational and regional background without considering any politicians, or by Kim and Cannella Jr [59] who used political ties formed around regional, educational, and family ties as dummy variables.

3.2.3. Moderating Variable

We measured CEO tenure according to the number of years a CEO had worked for the current firm.

3.2.4. Control Variables

For firm-specific variables, we controlled for the return on assets (ROA); firm size (natural logarithm of total assets); property, plant, and equipment (PPE) divided by total assets; R&D intensity (R&D expenses divided by total assets); advertising intensity; leverage ratio (long-term debts divided by total assets); change in net operating loss dummy; market-to-book ratio; and intangible assets (reported intangibles divided by lagged total assets). For governance-related variables, we controlled for the CEO’s educational background, board size, outside director ratio, prior political career, and outside directors’ prior political careers.

4. Results

Table 1 shows the means, standard deviations, and correlation matrix for the variables. Overall, the correlations showed low to intermediate values. All of the variance inflation factor (VIF) scores were below 2, and the mean VIF score was 1.24. Therefore, multicollinearity did not pose a serious concern.

Table 1.

Descriptive statistics.

Table 2 shows the estimates for the fixed effects regressions for tax avoidance. Model 1 reports the estimated results with controlled variables only, while subsequent models test specific hypotheses. As shown in Model 2, the estimated coefficient of CEO political connections for tax avoidance was statistically significant with a positive sign (β = 0.005, p < 0.05). The coefficient and significance level in Model 3 confirmed the result. Thus, Hypothesis 1, which predicted a positive influence of CEO political connections on tax avoidance behavior, was supported.

Table 2.

Regression results.

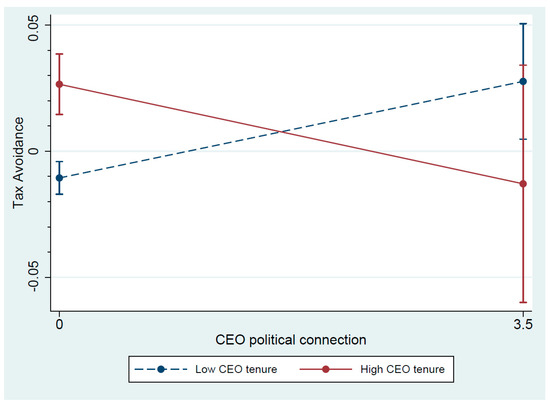

Concerning the competing hypotheses, the estimated coefficient of the interaction term between CEO political connections and CEO tenure in Model 3 was statistically significant with a negative sign (β = −0.006, p < 0.05). This indicates that CEO political connections mitigated risk-taking tendencies for tax avoidance as tenure increased. Therefore, among the competing hypotheses, Hypothesis 2b was supported while 2a was not. Figure 1 depicts the negative moderating role of CEO tenure.

Figure 1.

Moderating role of CEO tenure.

5. Discussion

While political relations are steadily sought after by journalistic investigation, there has been thriving academic research on their antecedents and consequences as well [15]. In that regard, our study would improve our understanding of the elusive, yet important aspect of sustainability management in a rigorous way.

Extending prior studies [31,70], this study measured CEO political connections in a more comprehensive manner. Specifically, this study measured corporate political connections based on a CEO’s social ties. We considered social ties within the elite group in Korea, given that such networks have functioned as an established communication mechanism for confidential information and are often more important than official political ties and lobbies. Since 2004, the Election Law has prohibited official political lobbying in Korea. However, businessmen and politicians continue to form networks through personal ties derived from their academic and family backgrounds as well as their alumni communities built from the national bar examinations.

This study considered CEO tenure as an important moderator. While CEOs with longer tenures can take advantage of their knowledge and skills accumulated in the position to find clever ways for tax avoidance, they may have less incentive for such aggressive behavior given their stabilized status in the organization and reputational risk in the society. Our empirical analysis revealed that the interaction between political connections and tenure had a negative impact on tax avoidance tendencies. This finding can be interpreted to mean that CEOs that are well connected to power elite groups actively use their networks for tax avoidance in their early stage of tenure, but, as their tenure matures, they tend to shy away from taking risky choices such as tax avoidance. This might be because tax avoidance using political power tends to become a burden rather than an incentive for CEOs with accumulated power and reputation in their organization and the wider society.

6. Conclusions

This study aimed to extend existing studies on the linkage between corporate political connections and tax avoidance behavior. There has been a surge in recent studies examining corporate tax sheltering [11,43,71], but a number of important issues have remained unexplored [14].

This study provides practical implications for corporate stakeholders. While firms can benefit from corporate political connections, specifically in less transparent economies, stakeholders must be conscious of the potential risks associated with information asymmetry and future political pressure. Moreover, the negative moderation of CEO tenure on the relationship between political connections and tax avoidance should be sensibly considered in appointing and monitoring top management.

This study has limitations and leaves room for a future research agenda. First, we measured tax payments based on income statements. However, there might exist slight discrepancies in BTD according to information sources. This limitation is held across studies on tax avoidance, but a more sophisticated measurement needs to be developed to reduce such discrepancies. Second, this paper assumed that tax avoidance is a risky strategic choice made by CEOs. However, as Guenther, Matsunaga, and Williams [35] suggested, future studies should also consider and investigate the existence or the degree of riskiness associated with tax avoidance. Third, with regard to CEO tenure, further attempts should be made to delve into other factors that may affect a CEO’s capabilities and/or incentives for tax aggressiveness. Fourth, the consequences of the tax avoidance behavior, and in turn, their impact on corporate political activities should also be investigated to provide a more dynamic view of the phenomenon.

In addition, our conclusions may not be generalizable under different cultural and institutional contexts. The Korean context may share similar characteristics to other Confucian countries in Asia, where relational advantages play a huge role, but may be less applicable to countries with different social and cultural traits. Such reservation calls for extensive search and analyses on the determinants of corporate donations in other institutional contexts. Future studies that properly consider these aspects will indeed help increase our understanding of tax avoidance as a perennial type of CSIR in many countries.

Author Contributions

Conceptualization, J.-H.K. and J.-H.L.; data curation, J.-H.K.; formal analysis, J.-H.K.; methodology J.-H.K. and J.-H.L.; supervision, J.-H.L.; writing—original draft preparation, J.-H.K.; writing—review and editing, J.-H.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

All relevant data sources are presented in the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Scholes, M.; Wolfson, M.; Erickson, M.; Maydew, E.; Shevlin, T. Taxes and Business Strategy: A Planning Approach, Pearson Prentice-Hall; Pearson Prentice-Hall: Upper Saddle River, NJ, USA, 2009. [Google Scholar]

- Mills, L.F.; Newberry, K.J. The influence of tax and nontax costs on book-tax reporting differences: Public and private firms. J. Am. Tax. Assoc. 2001, 23, 1–19. [Google Scholar] [CrossRef]

- Phillips, J.; Pincus, M.; Rego, S.O. Earnings management: New evidence based on deferred tax expense. Account. Rev. 2003, 78, 491–521. [Google Scholar] [CrossRef]

- Hanlon, M. The persistence and pricing of earnings, accruals, and cash flows when firms have large book-tax differences. Account. Rev. 2005, 80, 137–166. [Google Scholar] [CrossRef]

- Hanlon, M.; Heitzman, S. A review of tax research. J. Account. Econ. 2010, 50, 127–178. [Google Scholar] [CrossRef] [Green Version]

- Dyreng, S.D.; Lindsey, B.P. Using financial accounting data to examine the effect of foreign operations located in tax havens and other countries on US multinational firms’ tax rates. J. Account. Res. 2009, 47, 1283–1316. [Google Scholar] [CrossRef]

- Graham, J.R.; Tucker, A.L. Tax shelters and corporate debt policy. J. Financ. Econ. 2006, 81, 563–594. [Google Scholar] [CrossRef]

- Lisowsky, P. Seeking shelter: Empirically modeling tax shelters using financial statement information. Account. Rev. 2010, 85, 1693–1720. [Google Scholar] [CrossRef]

- Rego, S.O.; Wilson, R. Equity risk incentives and corporate tax aggressiveness. J. Account. Res. 2012, 50, 775–810. [Google Scholar] [CrossRef]

- Gaertner, F.B. CEO After-Tax compensation incentives and corporate tax avoidance. Contemp. Account. Res. 2014, 31, 1077–1102. [Google Scholar] [CrossRef] [Green Version]

- Armstrong, C.S.; Blouin, J.L.; Jagolinzer, A.D.; Larcker, D.F. Corporate governance, incentives, and tax avoidance. J. Account. Econ. 2015, 60, 1–17. [Google Scholar] [CrossRef] [Green Version]

- Dyreng, S.D.; Hanlon, M.; Maydew, E.L. The effects of executives on corporate tax avoidance. Account. Rev. 2010, 85, 1163–1189. [Google Scholar] [CrossRef]

- Christensen, D.M.; Dhaliwal, D.S.; Boivie, S.; Graffin, S.D. Top management conservatism and corporate risk strategies: Evidence from managers’ personal political orientation and corporate tax avoidance. Strateg. Manag. J. 2015, 36, 1918–1938. [Google Scholar] [CrossRef] [Green Version]

- Francis, B.B.; Hasan, I.; Sun, X.; Wu, Q. CEO political preference and corporate tax sheltering. J. Corp. Financ. 2016, 38, 37–53. [Google Scholar] [CrossRef] [Green Version]

- Faccio, M. Politically connected firms. Am. Econ. Rev. 2006, 96, 369–386. [Google Scholar] [CrossRef] [Green Version]

- Fisman, R. Estimating the value of political connections. Am. Econ. Rev. 2001, 91, 1095–1102. [Google Scholar] [CrossRef] [Green Version]

- Johnson, S.; Mitton, T. Cronyism and capital controls: Evidence from Malaysia. J. Financ. Econ. 2003, 67, 351–382. [Google Scholar] [CrossRef] [Green Version]

- Ma, C.; Yang, J.; Chen, L.; You, X.; Zhang, W.; Chen, Y. Entrepreneurs’ social networks and opportunity identification: Entrepreneurial passion and entrepreneurial alertness as moderators. Soc. Behav. Personal. Int. J. 2020, 48, 1–12. [Google Scholar] [CrossRef]

- Hadani, M.; Schuler, D.A. In search of El Dorado: The elusive financial returns on corporate political investments. Strateg. Manag. J. 2013, 34, 165–181. [Google Scholar] [CrossRef]

- Leuz, C.; Oberholzer-Gee, F. Political relationships, global financing, and corporate transparency: Evidence from Indonesia. J. Financ. Econ. 2006, 81, 411–439. [Google Scholar] [CrossRef]

- Chaney, P.K.; Faccio, M.; Parsley, D. The quality of accounting information in politically connected firms. J. Account. Econ. 2011, 51, 58–76. [Google Scholar] [CrossRef] [Green Version]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef] [Green Version]

- Zhang, J.; Marquis, C.; Qiao, K. Do political connections buffer firms from or bind firms to the government? A study of corporate charitable donations of Chinese firms. Organ. Sci. 2016, 27, 1307–1324. [Google Scholar] [CrossRef]

- Kölbel, J.F.; Busch, T.; Jancso, L.M. How media coverage of corporate social irresponsibility increases financial risk. Strateg. Manag. J. 2017, 38, 2266–2284. [Google Scholar] [CrossRef]

- Brown, J.L.; Drake, K.; Wellman, L. The benefits of a relational approach to corporate political activity: Evidence from political contributions to tax policymakers. J. Am. Tax. Assoc. 2015, 37, 69–102. [Google Scholar] [CrossRef]

- Mills, L.F.; Nutter, S.E.; Schwab, C.M. The effect of political sensitivity and bargaining power on taxes: Evidence from federal contractors. Account. Rev. 2013, 88, 977–1005. [Google Scholar] [CrossRef]

- Richter, B.K.; Samphantharak, K.; Timmons, J.F. Lobbying and taxes. Am. J. Political Sci. 2009, 53, 893–909. [Google Scholar] [CrossRef]

- Vurro, C.; Dacin, M.T.; Perrini, F. Institutional antecedents of partnering for social change: How institutional logics shape cross-sector social partnerships. J. Bus. Ethics 2010, 94, 39–53. [Google Scholar] [CrossRef]

- Dharwadkar, R.; Guo, J.; Shi, L.; Yang, R. Corporate social irresponsibility and boards: The implications of legal expertise. J. Bus. Res. 2021, 125, 143–154. [Google Scholar] [CrossRef]

- Rose, J.M. Corporate directors and social responsibility: Ethics versus shareholder value. J. Bus. Ethics 2007, 73, 319–331. [Google Scholar] [CrossRef]

- Kim, C.; Zhang, L. Corporate political connections and tax aggressiveness. Contemp. Account. Res. 2016, 33, 78–114. [Google Scholar] [CrossRef]

- Yiu, D.W.; Xu, Y.; Wan, W.P. The deterrence effects of vicarious punishments on corporate financial fraud. Organ. Sci. 2014, 25, 1549–1571. [Google Scholar] [CrossRef]

- Karpoff, J.M.; Lee, D.S.; Martin, G.S. The consequences to managers for cooking the books. J. Financ. Econ. 2008, 88, 193–215. [Google Scholar] [CrossRef]

- Strachan, J.L.; Smith, D.B.; Beedles, W.L. The price reaction to (alleged) corporate crime. Financ. Rev. 1983, 18, 121–132. [Google Scholar] [CrossRef]

- Guenther, D.A.; Matsunaga, S.R.; Williams, B.M. Is tax avoidance related to firm risk? Account. Rev. 2016, 92, 115–136. [Google Scholar] [CrossRef]

- Wilson, R.J. An examination of corporate tax shelter participants. Account. Rev. 2009, 84, 969–999. [Google Scholar] [CrossRef]

- Sikka, P. Smoke and mirrors: Corporate social responsibility and tax avoidance. Account. Forum 2010, 34, 153–168. [Google Scholar] [CrossRef]

- Efendi, J.; Srivastava, A.; Swanson, E.P. Why do corporate managers misstate financial statements? The role of option compensation and other factors. J. Financ. Econ. 2007, 85, 667–708. [Google Scholar] [CrossRef]

- Firth, M.; Rui, O.M.; Wu, W. Cooking the books: Recipes and costs of falsified financial statements in China. J. Corp. Financ. 2011, 17, 371–390. [Google Scholar] [CrossRef]

- Graham, J.R.; Li, S.; Qiu, J. Corporate misreporting and bank loan contracting. J. Financ. Econ. 2008, 89, 44–61. [Google Scholar] [CrossRef] [Green Version]

- Christensen, J.; Murphy, R. The social irresponsibility of corporate tax avoidance: Taking CSR to the bottom line. Development 2004, 47, 37–44. [Google Scholar] [CrossRef]

- Hoi, C.K.; Wu, Q.; Zhang, H. Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. Account. Rev. 2013, 88, 2025–2059. [Google Scholar] [CrossRef]

- Lanis, R.; Richardson, G. The effect of board of director composition on corporate tax aggressiveness. J. Account. Public Policy 2011, 30, 50–70. [Google Scholar] [CrossRef]

- Fich, E.M.; Shivdasani, A. Financial fraud, director reputation, and shareholder wealth. J. Financ. Econ. 2007, 86, 306–336. [Google Scholar] [CrossRef]

- Werner, T. Gaining access by doing good: The effect of sociopolitical reputation on firm participation in public policy making. Manag. Sci. 2015, 61, 1989–2011. [Google Scholar] [CrossRef]

- Duchin, R.; Sosyura, D. The politics of government investment. J. Financ. Econ. 2012, 106, 24–48. [Google Scholar] [CrossRef]

- Wayne, L. How Delaware Thrives as a Corporate Tax Haven. New York Times, 30 June 2012. [Google Scholar]

- Adhikari, A.; Derashid, C.; Zhang, H. Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. J. Account. Public Policy 2006, 25, 574–595. [Google Scholar] [CrossRef]

- Wu, S.; Levitas, E.; Priem, R.L. CEO tenure and company invention under differing levels of technological dynamism. Acad. Manag. J. 2005, 48, 859–873. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. Managing with style: The effect of managers on firm policies. Q. J. Econ. 2003, 118, 1169–1208. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Castanias, R.P.; Helfat, C.E. Managerial resources and rents. J. Manag. 1991, 17, 155–171. [Google Scholar] [CrossRef]

- Penrose, E.; Penrose, E.T. The Theory of the Growth of the Firm; Oxford University Press: Oxford, UK; Blackwell: Oxford, UK, 2009. [Google Scholar]

- Bamber, L.S.; Jiang, J.; Wang, I.Y. What’s my style? The influence of top managers on voluntary corporate financial disclosure. Account. Rev. 2010, 85, 1131–1162. [Google Scholar] [CrossRef]

- Dejong, D.; Ling, Z. Managers: Their effects on accruals and firm policies. J. Bus. Financ. Account. 2013, 40, 82–114. [Google Scholar] [CrossRef]

- Barker III, V.L.; Mueller, G.C. CEO characteristics and firm R&D spending. Manag. Sci. 2002, 48, 782–801. [Google Scholar]

- Hambrick, D.C.; Fukutomi, G.D. The seasons of a CEO’s tenure. Acad. Manag. Rev. 1991, 16, 719–742. [Google Scholar] [CrossRef]

- Simsek, Z. CEO tenure and organizational performance: An intervening model. Strateg. Manag. J. 2007, 28, 653–662. [Google Scholar] [CrossRef]

- Kim, Y.; Cannella Jr, A.A. Social capital among corporate upper echelons and its impacts on executive promotion in Korea. J. World Bus. 2008, 43, 85–96. [Google Scholar] [CrossRef]

- Yonhap News Person Information. Available online: http://sales.yonhapnews.co.kr/YNA/ContentsSales/ContentsData/YISW_PeopleHome.aspx (accessed on 12 December 2020).

- Chosun Profile. Available online: http://db.chosun.com/people (accessed on 20 December 2020).

- Joins People. Available online: http://people.joins.com (accessed on 22 December 2020).

- National Assembly. Available online: http://www.assembly.go.kr (accessed on 23 January 2021).

- Office of the President. Available online: http://www.president.go.kr (accessed on 4 January 2021).

- Naver Peope Serch. Available online: http://people.search.naver.com (accessed on 4 January 2021).

- Desai, M.A.; Dharmapala, D. Corporate tax avoidance and high-powered incentives. J. Financ. Econ. 2006, 79, 145–179. [Google Scholar] [CrossRef] [Green Version]

- Hribar, P.; Collins, D.W. Errors in estimating accruals: Implications for empirical research. J. Account. Res. 2002, 40, 105–134. [Google Scholar] [CrossRef]

- Zhu, H.; Chung, C.-N. Portfolios of political ties and business group strategy in emerging economies: Evidence from Taiwan. Adm. Sci. Q. 2014, 59, 599–638. [Google Scholar] [CrossRef]

- Siegel, J. Contingent political capital and international alliances: Evidence from South Korea. Adm. Sci. Q. 2007, 52, 621–666. [Google Scholar] [CrossRef] [Green Version]

- Wu, W.; Wu, C.; Zhou, C.; Wu, J. Political connections, tax benefits and firm performance: Evidence from China. J. Account. Public Policy 2012, 31, 277–300. [Google Scholar] [CrossRef]

- Chen, S.; Chen, X.; Cheng, Q.; Shevlin, T. Are family firms more tax aggressive than non-family firms? J. Financ. Econ. 2010, 95, 41–61. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).