1. Introduction

In the literature there is a debate of whether engaging in corporate social responsibility (CSR) activities is beneficial [

1,

2,

3]. Some studies have shown that CSR activities are solely a manifestation of agency conflicts between a firm’s shareholders and managers, who particularly benefit from engaging in CSR at the expense of a firm’s shareholders [

4,

5], while other research has shown that engaging in environmental, social, and governance (ESG) is value-enhancing due to the hypothesis that well-governed corporations can achieve both, higher profits and better social conditions [

2,

6,

7,

8].

In line with these arguments, there is mixed evidence in the literature regarding the relationship between a firm’s CSR activities and its stock performance, especially during times of crisis. Albuquerque et al. [

9], Lins et al. [

10] and Ding et al. [

11] find that high CSR-rated firms are associated with better stock performance in terms of higher stock returns and lower stock volatility during times of crisis. In contrast, Bae et al. [

12] and Demers et al. [

13] stress that a firm’s CSR performance is unrelated to its stock performance after the COVID-19 crisis unfolded, thus CSR does not make firms more resilient in times when market uncertainty is high.

In this paper, we therefore investigate whether there is a link between CSR activities and a firm’s stock performance in terms of higher stock returns and lower stock volatility in the beginning of 2020, because the unexpected and exogenous COVID-19 shock serves as a brilliant opportunity to test this relationship. Particularly, we aim to answer two main research questions.

First, does engaging in CSR activities create shareholder value and does good-quality CSR make European firms more resilient during times of crisis? Although there is a growing strand of literature investigating the effect of good-quality CSR when market uncertainty is high [

9,

10,

11,

12,

13], our understanding of whether CSR is of particular importance for European firms, especially during times of crisis, is still limited.

Second, we pose the research question of whether CSR is even more important for firms headquartered in certain countries depending on the countries’ characteristics. In this respect, we examine whether the effect of good-quality CSR is even more pronounced in low-trust or high-trust European countries. While Lins et al. [

10] investigate the impact of CSR in high-trust US regions, this is the first study investigating the impact of good-quality CSR depending on a countries’ level of societal trust. Further, we explore additional country characteristics as proposed in Karolyi et al. [

14] and Neukirchen et al. [

15] who investigate characteristics such as the quality of security market regulations, the level of legal protection standards, as well as the level of disclosure standards.

We employ a sample of 1452 firms from 16 different European countries to examine whether high CSR-rated firms outperformed those with very low CSR ratings. To do so, we obtain Refinitiv’s ESG ratings from Thomson Reuters Eikon as they are primarily used in the CSR literature [

9,

12,

13], and also financial data from Compustat/Capital IQ.

Our research design is closely related to Albuquerque et al. [

9], Bae et al. [

12], and Lins et al. [

10]. Specifically, we employ several multivariate regression models where the dependent variable is either a firm’s cumulative raw stock return or a firm’s cumulative abnormal stock return during the so-called “collapse period” from 3 February 2020 until 23 March 2020 proposed by Fahlenbrach et al. [

16] where the COVID-19 pandemic hit financial markets. Additionally, we use a firm’s volatility and idiosyncratic volatility over the collapse period as dependent variables to test whether effective CSR is associated with a reduction in stock volatility. As our main independent variables of interest, we use the raw ESG scores and a dummy variable set to one if a firm’s ESG score is larger than the median score within the respective country, and zero otherwise.

Our results are mixed, consistent with the related literature. Comparable to the results found in Bae et al. [

12] and Demers et al. [

13], we do not find statistically significant coefficients on our ESG measures when we employ a firm’s cumulative raw stock return as the dependent variable. However, our results are in line with Albuquerque et al. [

9], when using market adjusted abnormal stock returns in our regressions. We find positive and highly statistically significant coefficients on our ESG measures indicating that a one standard deviation increase in ESG scores is associated with on average a 2.59% higher abnormal return during the collapse period. Further, we document that firms with higher ESG scores are also associated with lower idiosyncratic volatility. We find our results to be robust to different observation periods and when controlling for several firm characteristics as used in related studies [

9,

10,

12,

16]. We also employ industry and country fixed effects to ensure the validity of our results.

In additional tests, we examine whether ESG is even more value-enhancing in specific countries. Particularly, we find that ESG is of significant importance in low-trust countries, and in countries which exhibit poorer security regulations and where lower disclosure standards prevail. Our results differ in some extent from those found in Lins et al. [

10] who show that CSR is more important in high-trust US regions during the global financial crisis (GFC). However, Bae et al. [

12] find only weak support for this hypothesis during the COVID-19 crisis. In this respect, Engelhardt et al. [

17] investigate a cross-country setting and find that financial volatility is significantly higher in low-trust countries in response to COVID-19 cases. Thus, our results indicate that engaging in ESG activities in low-trust countries may reduce uncertainty among market participants during the COVID-19 pandemic.

The remainder of this paper is structured as follows. In

Section 2, we employ a theoretical framework and a comprehensive literature review.

Section 3 describes our dataset.

Section 4 presents our results. In

Section 5, we perform robustness checks and

Section 6 concludes.

2. Theoretical Background

There is an evolving body of research investigating the relationship between a firm’s CSR performance and firm value and so far, the existing literature shows ambiguous results [

1,

2,

3,

18,

19,

20,

21,

22,

23,

24,

25,

26,

27,

28,

29]. Beginning with Friedman [

30], there is an ongoing discussion of whether companies should maximize shareholder value or stakeholder wealth. Classical shareholder theory suggests that CSR is solely a donation from a firm’s shareholders to stakeholders [

31]. In this respect, firms which are socially unresponsive have lower costs and could therefore earn higher profits than socially responsive firms [

32]. Thus, socially responsive firms generally face competitive disadvantages compared to socially unresponsive firms and should have lower valuations [

33].

Similarly, some authors have argued that CSR activities might be solely a manifestation of agency conflicts between a firm’s shareholders and managers. In that sense, managers might invest in CSR activities in order to boost their personal image among relevant stakeholder groups at the expense of a firm’s shareholders [

4,

5]. Following this argument, a firm’s CSR performance is either unrelated to its value or can even damage a firm’s valuation because of high agency costs [

12,

23,

24,

29].

The opposite view on the relationship between CSR and firm value is that engaging in CSR activities is value-enhancing due to the hypothesis that well-governed corporations can achieve both, higher profits and better social conditions [

2,

6,

7,

8]. This view on CSR is also summarized as “doing well by doing good” [

9]. In this respect, several studies have highlighted a positive relationship between a firm’s CSR performance and its financial performance [

1,

2,

22,

26,

34,

35]. Dai et al. [

36] document that CSR efforts increase a firm’s operational efficiency and its firm value. El Ghoul et al. [

37] show that firms with good-quality CSR have substantially lower cost of capital. Their findings also support the view that high-CSR rated firms exhibit lower financial risks and are thus valued higher by investors. Deng et al. [

21] investigate whether CSR is value enhancing for acquiring firms’ shareholders and find that high CSR acquirers exhibit significantly higher merger announcement returns. Albuquerque, Koskinen, and Zhang [

38] argue that CSR significantly reduces systematic risk and strengthens firm value. Further, Flammer [

1] states that the effect of shareholder CSR proposals lead to significantly higher abnormal stock returns.

The effect of CSR has also been studied during times of financial crises. Cornett et al. [

39] find that the relationship between banks’ CSR quality and their financial performance is positive; thus banks particularly benefit from engaging in CSR activities after the Great Recession in 2009. Further, Lins et al. [

10] stress that non-financial firms which are socially responsible had better capital market outcomes in terms of higher stock returns during the GFC. Additionally, they find that high-CSR rated firms had higher profitability and growth compared to low-CSR rated firms.

Several recent papers have also examined the current COVID-19 crisis. Albuquerque et al. [

9] and Ding et al. [

11], who primarily focus on the US market, document that high CSR-rated firms exhibit better financial performance in terms of higher stock returns and lower stock volatility during the ongoing COVID-19 crisis. In contrast to these studies, Bae et al. [

12] as well as Demers et al. [

13] find that a firm’s CSR performance is either unrelated to its financial performance after the COVID-19 crisis hit financial markets. Thus, firms which are socially responsible were generally not more resilient.

3. Data

Our sample consists of 1452 publicly-listed European firms from 16 different European countries. To measure a firm’s ESG performance, we obtain Refinitiv’s ESG ratings from Thomson Reuters Eikon which have also been used in the CSR literature [

9,

13]. Particularly, we collect Refinitiv’s ESG ratings for the year 2019. Refinitiv measures corporate environmental, social, and governance performance into several sub-dimensions. A firm’s environmental performance is covered by the categories resource use, emissions, and innovation. Social performance is measured by the sub-dimensions workforce, human rights, community, and product responsibility, and governance performance is evaluated in the sub-dimensions management, stakeholders, and CSR strategy [

40]. We then extend our dataset by adding stock and accounting data from Compustat/Capital IQ.

Our main independent variable of interest is

ESG Score which measures a firm’s ESG performance. Additionally, we construct the dummy variable

High ESG, which is set to one if a firm’s ESG score is larger than the median score within the respective country, and zero otherwise. Our main dependent variables of interest are a firm’s cumulative raw stock return as well as a firm’s cumulative abnormal stock return for the period from 3 February 2020 until 23 March 2020. This period is the so-called “collapse period” as proposed by Fahlenbrach et al. [

16] where the COVID-19 pandemic hit financial markets. We calculate abnormal returns based on a market model estimation similar to Albuquerque et al. [

9]. Specifically, a firm’s abnormal stock return is the difference between the logarithmic stock return and the expected stock return. The expected stock return is the CAPM beta times the market return of the respective country where we estimate beta factors based on the firm’s stock returns and the respective market return for the year 2019.

We also employ several control variables which have also been used in the existing literature [

9,

10,

12,

16] and provide definitions of these variables in

Table A1 in the

Appendix A.

After merging our datasets, our final sample consists of 1452 European firms, for which we gather data on ESG ratings and data on stock performance. Regarding control variables, there are several observations missing which is the reason why we take several regression specifications into account.

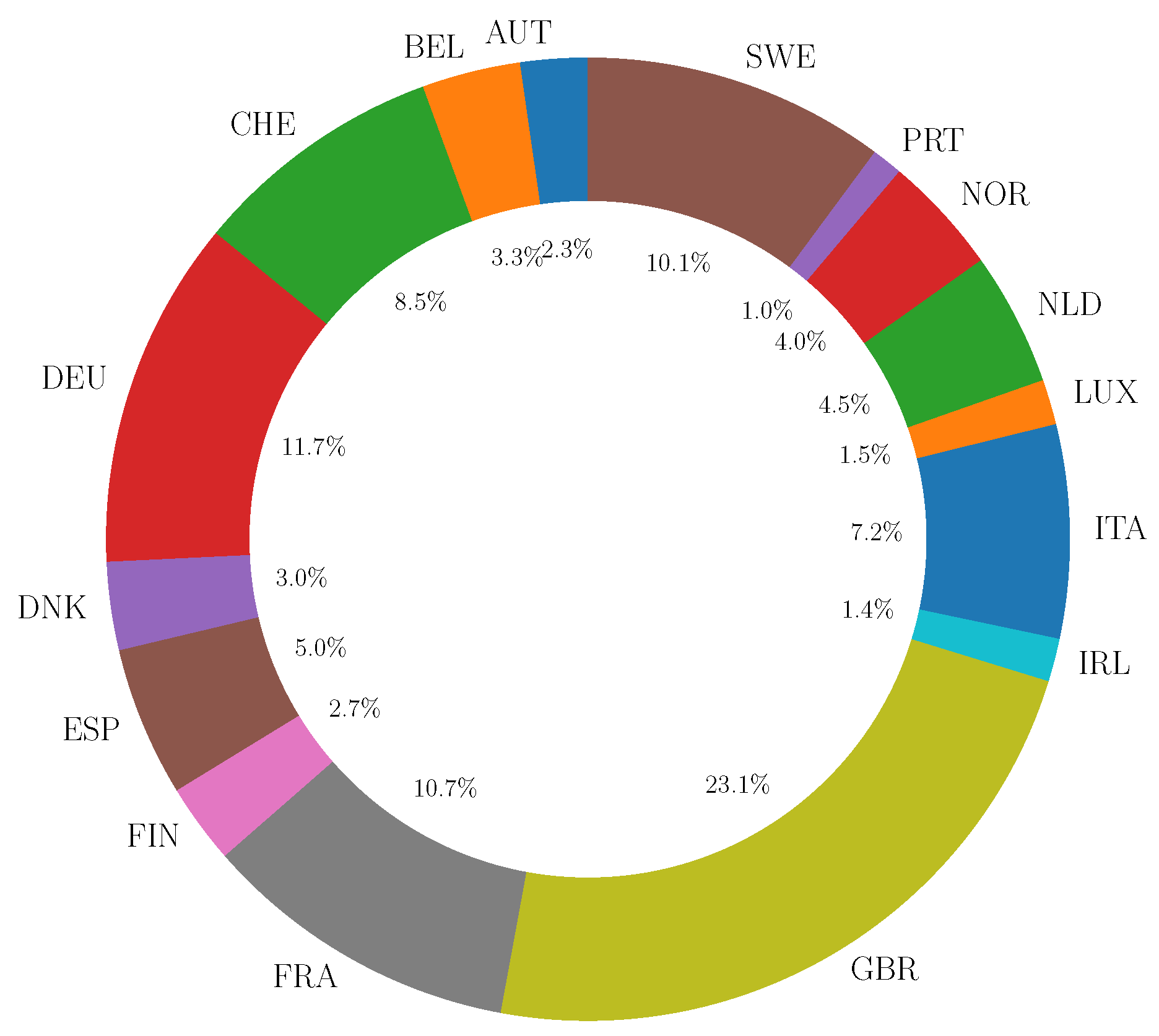

Figure 1 shows the weights of the 16 different European countries in which the firms are headquartered in. For instance, 23.1% of the firms are located in the UK and 11.7% are German firms.

Table 1 presents summary statistics for our final dataset. Mean cumulative stock returns are highly negative (

%) and the respective standard deviation is

% which indicates that firms’ stock prices experience large fluctuations during the collapse period from 3 February 2020 until 23 March 2020. Although Fahlenbrach et al. [

16] consider a dataset consisting of US firms, we find very similar summary statistics regarding firms’ cumulative stock returns. Further, the mean ESG score amounts to

% with a standard deviation of

%. In terms of control variables, the average firm in our dataset has a size of

$ billion, a cash over assets ratio of

%, and a financial leverage of

%.

Before we examine the association between corporate ESG performance and stock returns in a multivariate setting, we first perform a correlation analysis in

Table 2. Regarding pairwise correlations, we find that the correlations are generally weak, except for the positive correlations between

Size and our ESG measures and

ROE and

Profitability. Further, we find a negative correlation of

between

ESG Score and

Historical Volatility and a correlation of

between

Momentum and

Historical Volatility. The main independent variable of interest

ESG Score and the cumulative (abnormal) stock return which are used as the dependent variables in the upcoming multivariate regressions, show a positively weak and statistically significant correlation of 1% (4%).

We additionally present univariate tests in

Table 3 to compare firm characteristics of

High ESG and

Low ESG firms. Concerning firm size,

High ESG firms are on average significantly larger than

Low ESG firms.

High ESG firms exhibit significantly higher financial leverage and higher long-term debt over assets ratios, while we find that

High ESG firms tend to have a significantly lower

Tobin’s Q, a lower cash over assets ratio, a lower market-to-book ratio, and a lower historical stock volatility.

5. Robustness

We perform a variety of robustness checks to ensure the validity of our findings. First, we test whether our main results persist when we change the observation period. Specifically, we rerun our baseline regressions (I) over the whole first quarter of 2020 as in Albuquerque et al. [

9], and (II) over the so-called “fever period” from Ramelli and Wagner [

50] from 24 February 2020 to 20 March 2020. However, our results remain qualitatively similar.

Second, we follow Albuquerque et al. [

9] and use ES ratings in our analyses. We thus omit the governance score in unreported regressions and find very similar results compared to our previous findings. Additionally, we break down the ESG score into E, S, and G and use the scores separately as done in Albuquerque et al. [

9]. Although not reported for reasons of brevity, we find similar baseline results. Our results are also in line with Albuquerque et al. [

9], who show that a firm’s ES performance is of significant importance while a firm’s governance score is not useful to explain stock returns over the crisis period. Although Albuquerque et al. [

9] primarily examining the US market, we find a similar pattern for European stock markets.

Third, we test whether our findings are driven by the performance of firms which are domiciled in the UK, as these firms amount to approximately 25% of our observations. Although we find that the coefficient on

ESG Score is positive and statistically significant, the coefficient is slightly smaller in magnitude compared to the results found in

Table 4. We also see a similar picture when we rerun the baseline regression in

Table 5 when the dependent variable is a firm’s idiosyncratic volatility. Further, we exclude firms from the financial sector and firms with low stock liquidity, i.e., firms with a market capitalization below

$250 million as proposed by Lins et al. [

10] and Neukirchen et al. [

15]. Overall, our results remain qualitatively similar when performing several robustness exercises.

6. Conclusions

The COVID-19 crisis led to enormous uncertainty on financial markets along with a dramatic decline in stock prices and higher financial volatility. In this paper, we studied whether firms with higher ESG ratings perform significantly better during the COVID-19 crisis. We investigate a sample consisting of 1452 firms from 16 different European countries and argue that firms with better ESG performance had significantly higher cumulative abnormal returns and exhibit significantly lower idiosyncratic volatility in the beginning of 2020. Our results hold in several multivariate specifications as well as when applying a variety of robustness checks.

Our findings have implications for the financial sector and its market participants. From the firm’s perspective, engaging in CSR significantly pays off in terms of better stock performance. Thus, good quality CSR is making firms more resilient when market uncertainty is high, and therefore managers should increase their commitment to develop an appropriate CSR strategy.

From an investor’s perspective, good quality CSR is an important factor regarding a firm’s stock performance, especially during times of crisis. When facing investment decisions, CSR is even more important in low-trust countries, and in countries which exhibit poorer security regulations and where lower disclosure standards prevail.

Finally, as with most research in this field, our research has certain limitations. First, we only consider a rather small observation period, and thus our paper only addresses the short term effects of good quality CSR on stock performance during the COVID-19 crisis. However, the crisis is still present and studying the long term effects of CSR is an interesting field for future research. Second, we only use data from a single data source to construct our CSR measure and there might be other proxies to capture the quality of a firm’s CSR performance. Third, there are existing additional country characteristics. Studying whether CSR significantly pays off in certain countries depending on the countries’ characteristics, for instance in freer countries, leaves space for further research and could provide deeper insights.

{kind=link}