Horizontal Accountability for SDG Implementation: A Comparative Cross-National Analysis of Emerging National Accountability Regimes

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction: Accountability as a Key Governance Challenge in Implementing the SDGs

2. Conceptual Framing: Horizontal Accountability in Theory and Its Relevance for Effective SDG Implementation

2.1. Definition and Forms of Accountability

2.2. Horizontal Accountability for SDG Implementation

2.3. The Role of Parliaments in SDG Accountability

- Making or amending laws in a way that ensures consistency with the 2030 Agenda. In 2015, the IPU Assembly adopted the Hanoi Declaration [48], in which member parliaments committed to translate the SDGs into enforceable domestic laws and regulations. In order to make laws that are consistent with the SDGs, it is necessary that parliamentarians are sufficiently informed about the scope and content of the goals in the first place. This requires the organization of training sessions and awareness-raising activities for parliamentarians and parliamentarian staff [49,50,51].

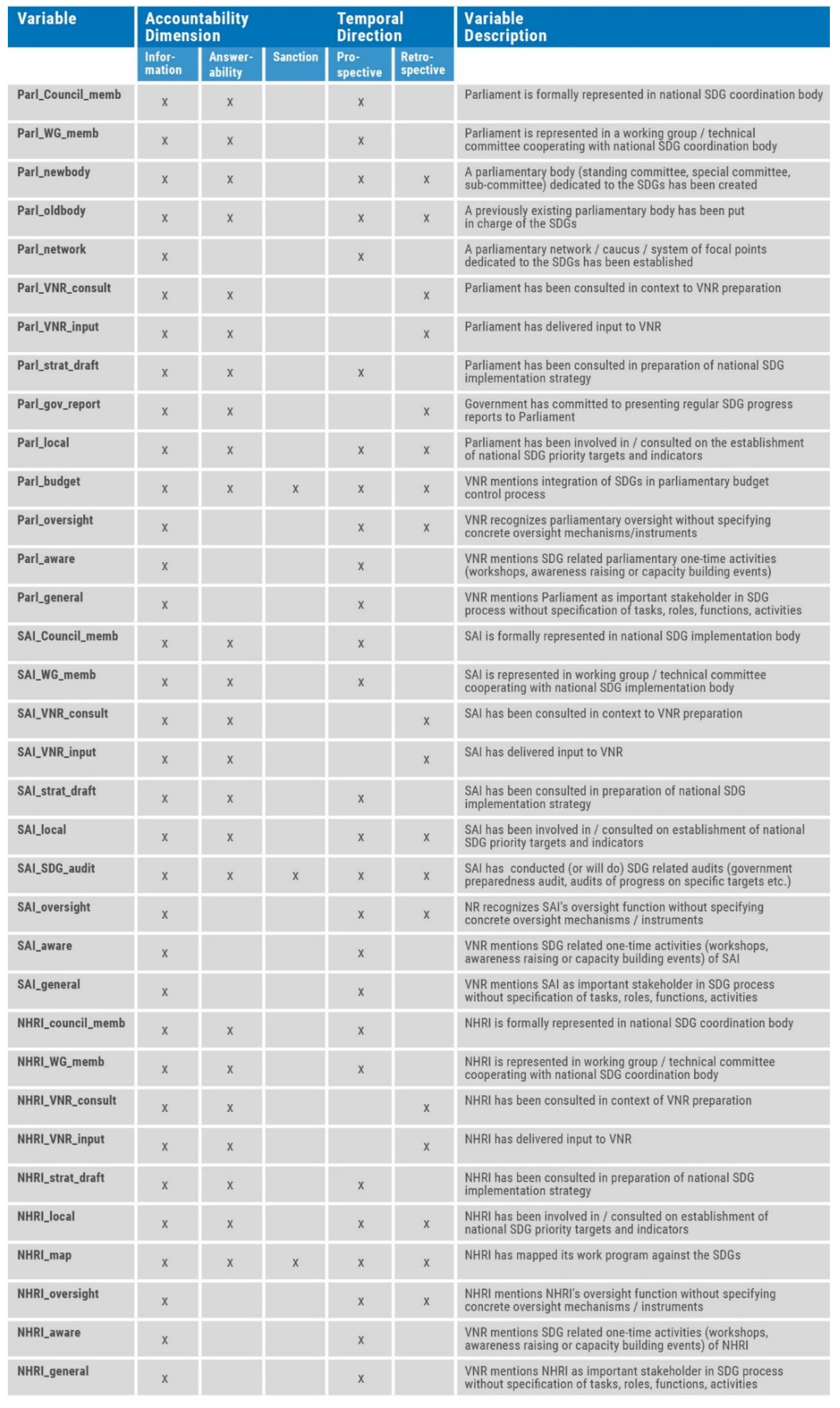

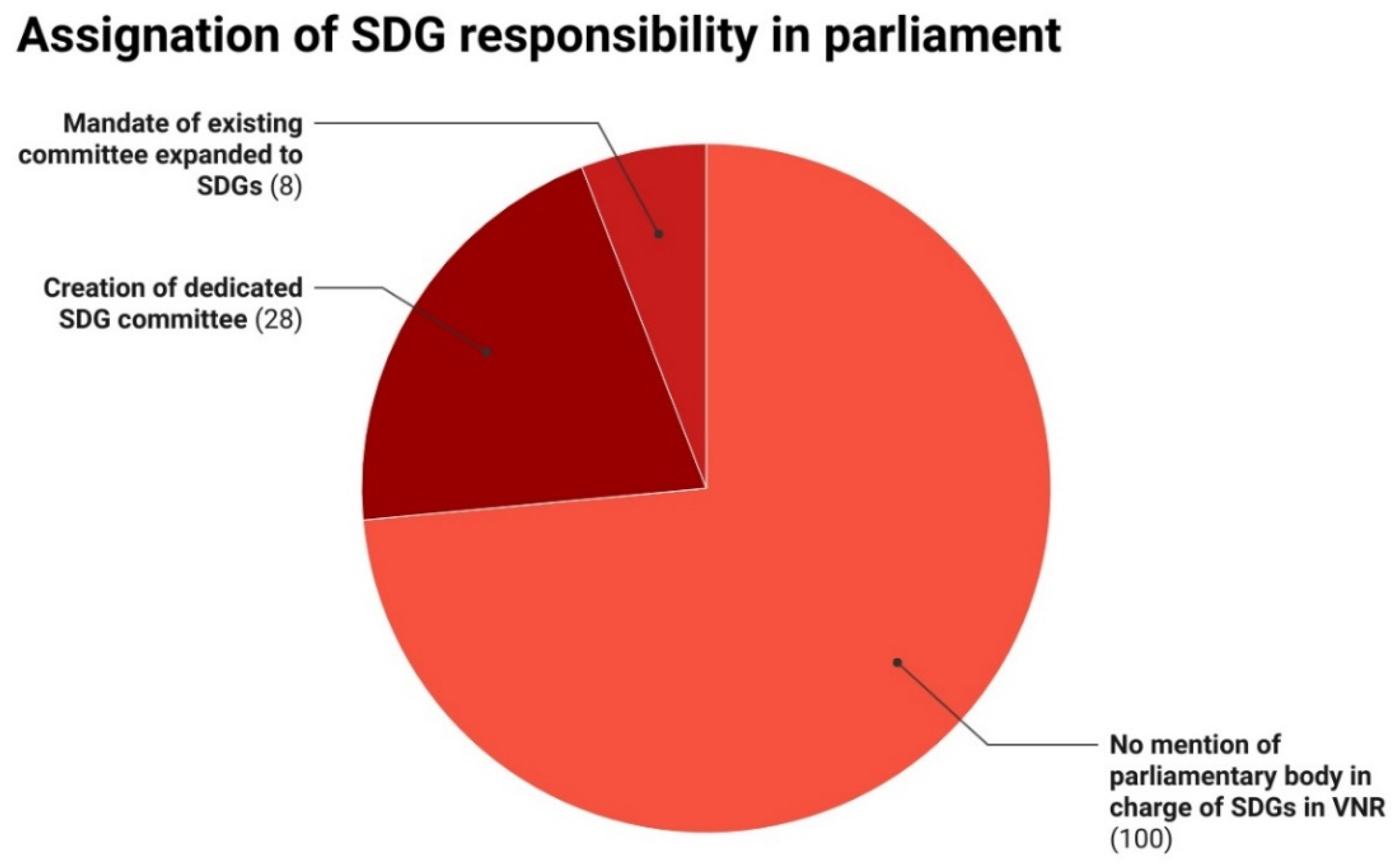

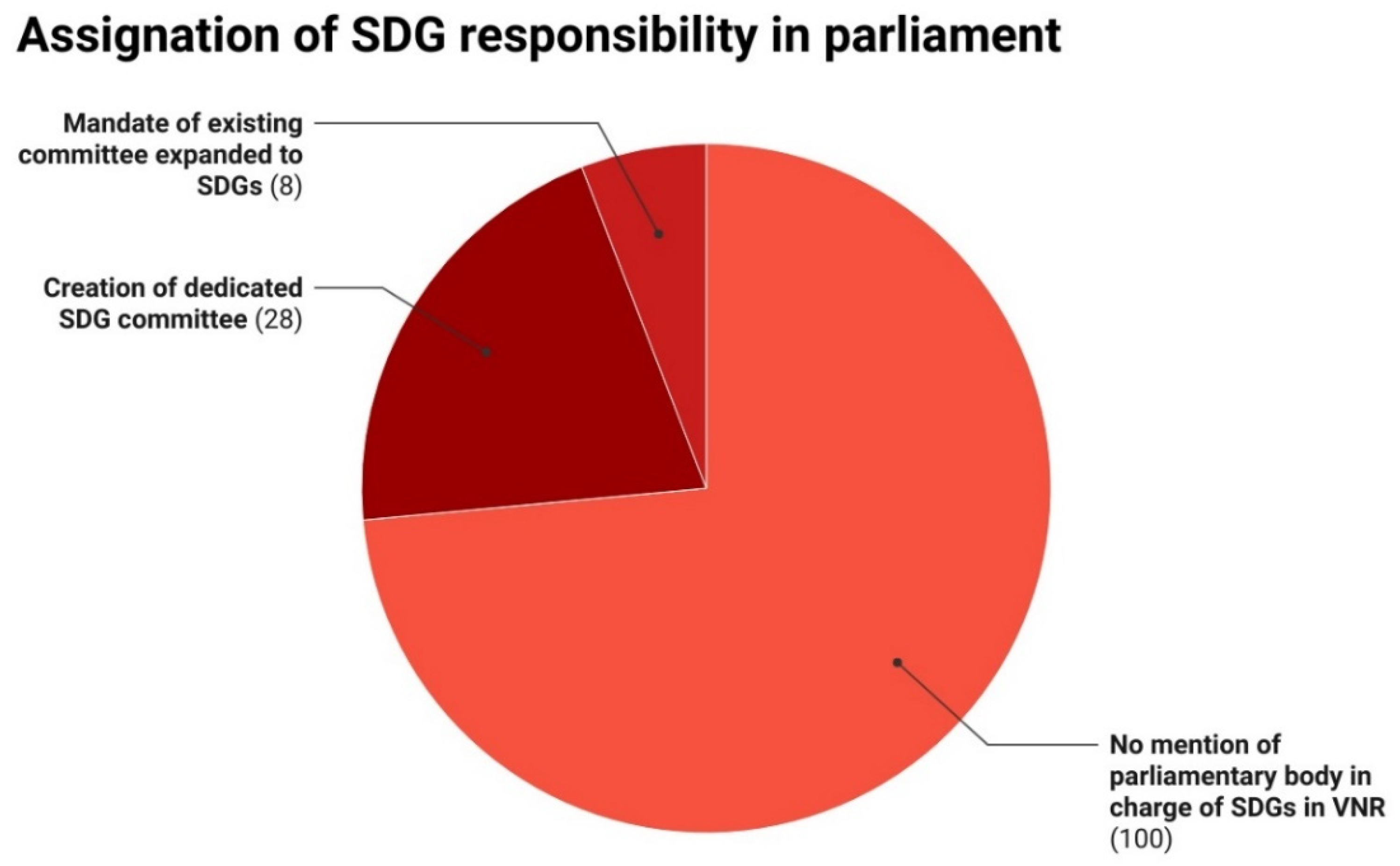

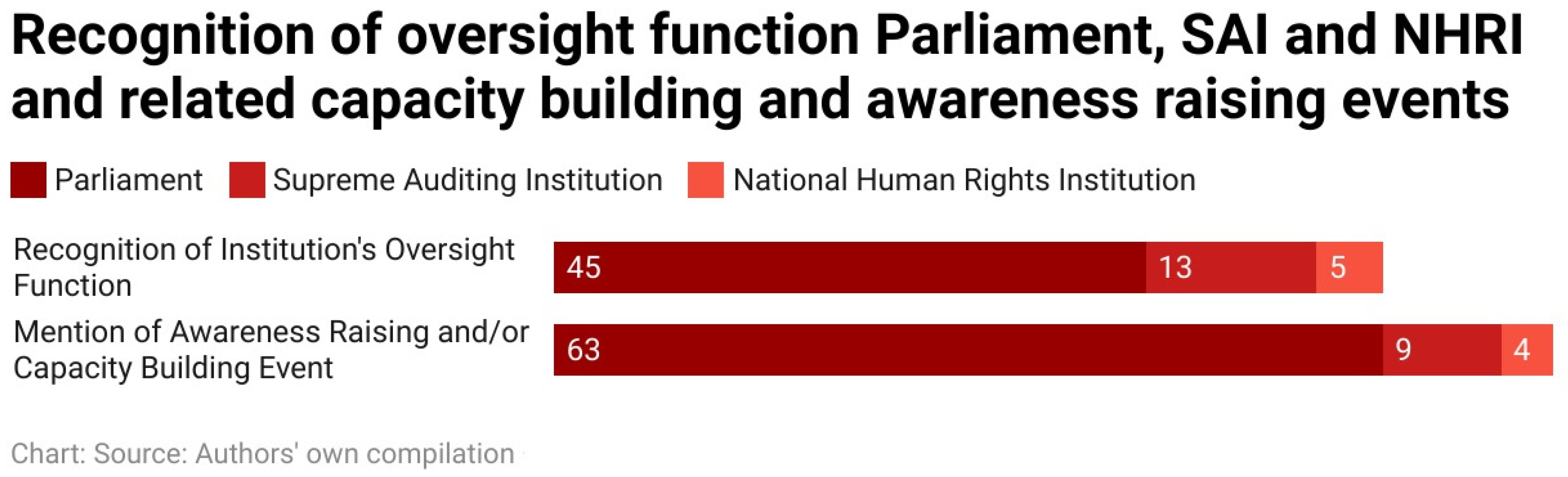

- Monitoring the actions of governments and their agencies in implementing the SDGs. In order to exercise their oversight functions effectively, parliaments need to clearly assign responsibility for the issue to be monitored within their own structures. In the context of the 2030 Agenda, one possibility of doing so is through the establishment of a dedicated parliamentary SDG committee. Committee oversight is one of the strongest mechanisms of retrospective accountability through which parliaments can hold governments accountable for SDG implementation [49,50]. Committees enable parliamentarians to undertake in-depth examinations of government action by allocating more time to specific issues. Parliamentary committees typically have the authority to ask government agencies for information and documents, to interrogate government officials, and to conduct hearings and assessments. Therefore, committees enable parliamentarians to examine, in retrospect, whether policies, regulations, and programs were effectively implemented in support of the SDGs, and if not, to formulate recommendations on how to strengthen future SDG compliance. While the establishment of a new, dedicated SDG committee offers an opportunity for parliaments to make a strong public statement on the importance of the SDGs, parliaments may also decide to use existing structures for SDG oversight. The necessary subject expertise may already exist within committees that are well-established and have funding and supporting staff members at their disposal. Another, though less formalized, way for parliaments to join the forces of different stakeholders for discussing and overseeing SDG action is the establishment of cross-party parliamentary networks, working groups, or caucuses on the SDGs [13]. Such networks do not possess formal mechanisms to demand government explanations. Instead, their work typically aims at creating opportunities for cross-party exchange on possibilities for mainstreaming the SDGs into legislation.

- At the global level, the principal platform for monitoring SDG progress is the United Nations High-level Political Forum on Sustainable Development (HLPF). The HLPF convenes annually to assess progress towards the achievement of the SDGs based on the VNR. The process of conducting a VNR thus presents an opportunity to hold governments accountable for their efforts (or lack thereof) towards meeting the SDGs during the preceding reporting period. While VNR are normally government-led, a broad range of stakeholders, including parliaments, should be involved in the review process in order to provide a balanced account of national progress in SDG achievement [52]. However, conducting a VNR is a complex process and is therefore usually not carried out annually (According to the UN Sustainable Development Knowledge Platform, between 2016 and 2020, 129 countries presented one VNR at the HLPF, 26 countries presented two VNRs, and only two countries (Benin and Togo) presented three VNRs; https://sustainabledevelopment.un.org/vnrs/ (accessed on 17 June 2021)). In order to exercise oversight effectively, parliaments should therefore ask governments to present more frequent periodic progress reports on the SDGs beyond the VNR [13,49]. The tabling of such reports in parliament enables legislators to demand explanation on government SDG action.

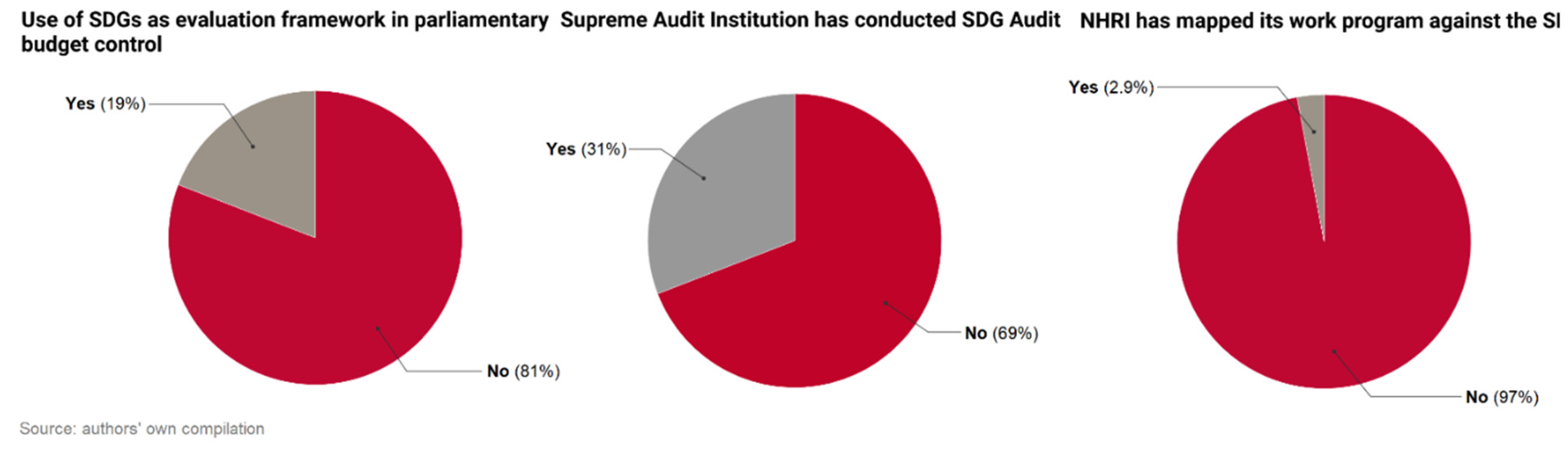

- Budget evaluation that ensures an adequate allocation of financial resources to achieve the SDGs. Although the development of the national budget is formally the responsibility of the executive branch of government, parliaments are responsible for adopting national budgets and overseeing the use of public funds. Parliamentarians also play a crucial role in advocating for budget priorities in advance of the budget preparation process. In some countries, they can even use their law-making and oversight powers to propose formal modifications to the budget once it has been presented to parliament [53,54]. Budgetary control powers thus also equip parliaments with the ability to impose sanctions on the executive branch by not granting budgets for a certain policy [55,56]. Their vital role in the budgeting process helps them to influence government expenditure. Therefore, it has been postulated that parliaments should use the SDGs as an evaluation framework for budget proposals and make sure that government funds are being adequately allocated to nationally defined SDGs [13,49,57].

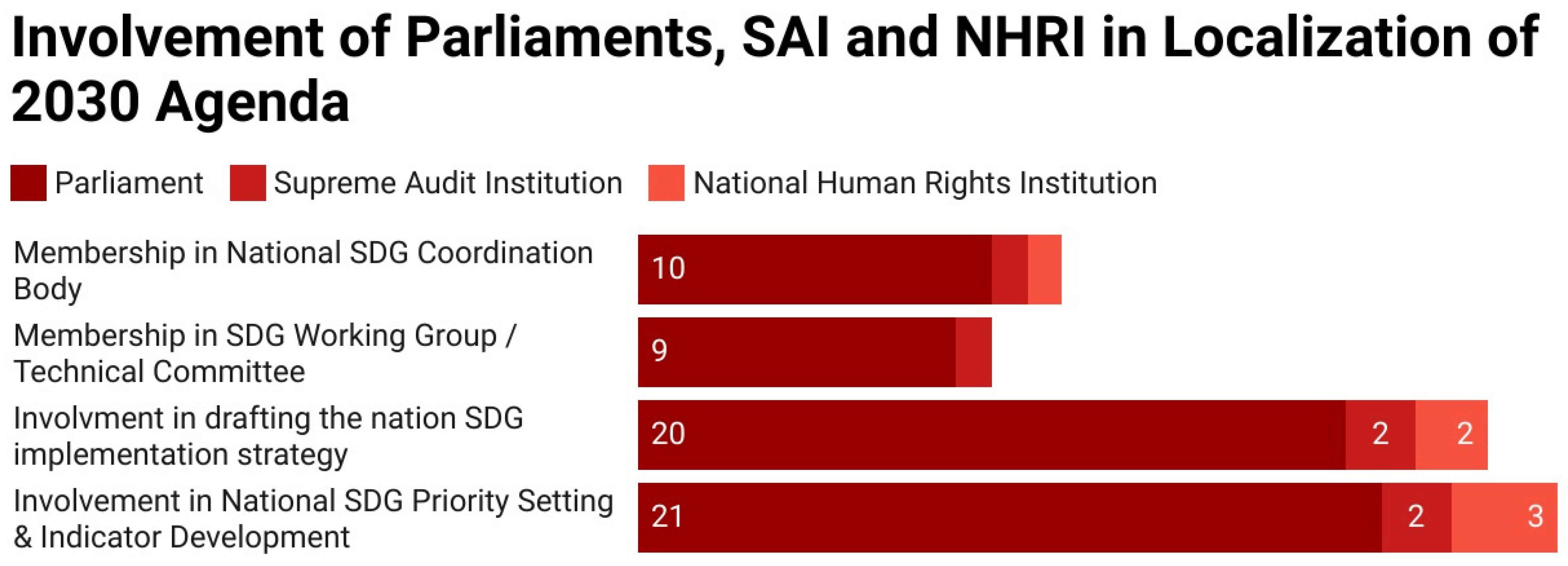

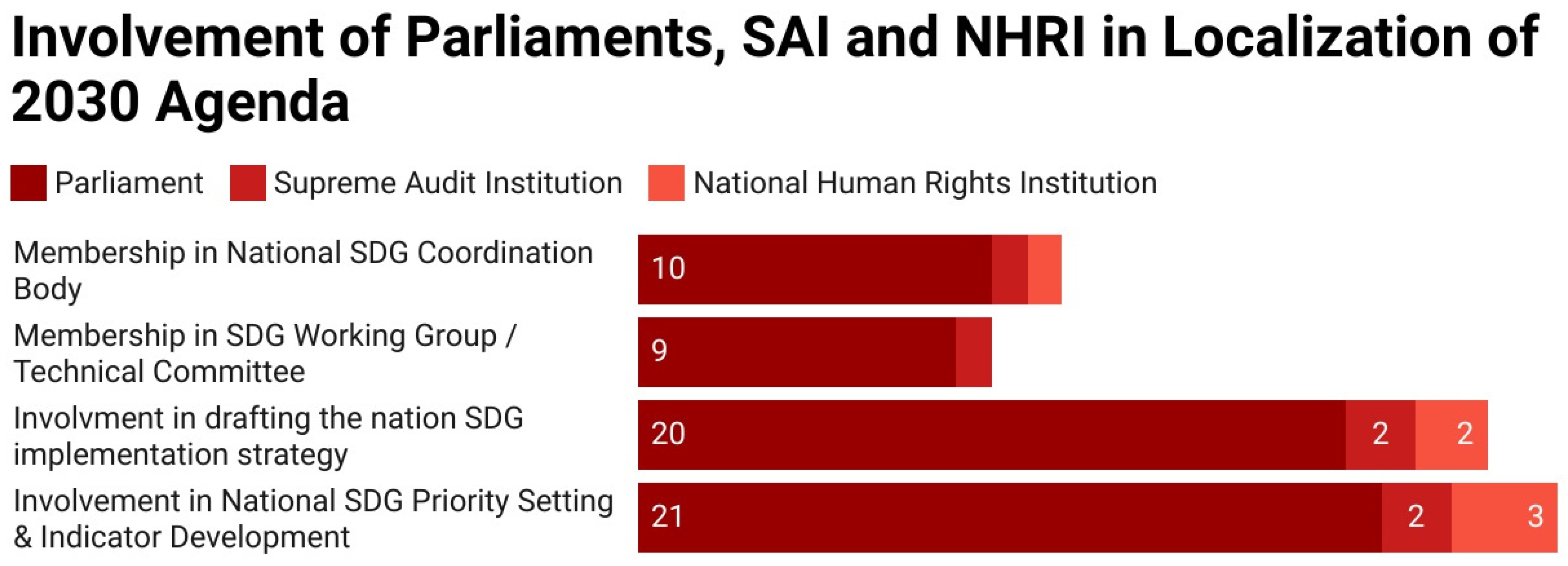

- Representing the interests of their constituents in the process of SDG implementation. The role of parliamentarians in representing the interests of their constituents is crucial for SDG accountability, particularly for vulnerable and marginalized groups who have few opportunities to voice their grievances [13]. The way and degree to which parliament and the government work together on the SDGs is relevant both for the due representation of citizen interests as well as for the integrated and coherent implementation of the SDGs. Governments and parliaments comprise a broad variety of institutions responsible for a wide range of subject areas. A national body responsible for coordinating the SDG efforts of these various institutions is therefore key to ensuring integrated implementation of the SDGs, whereas lack of coordination can lead to inconsistent laws and regulations that result in policy incoherence [12,58,59,60]; consequently, most countries have established some form of taskforce or steering committee to oversee and guide national SDG implementation. While these bodies are usually set up by the executive branch of government, there is broad consensus that it is good practice to provide for their inclusive membership. However, whether or not parliament should be represented in these bodies is a matter of debate. According to the IPU “in many countries, there are still questions about whether parliament should even be part of the SDG coordination body or whether its role should be to monitor the work of these bodies and hold them to account” [47]. From the latter point of view, it might rather be desirable that parliamentarians participate in working groups or technical committees that collaborate with and consult the executive-level national SDG coordination body. The representative function of parliament should also come to bear in the process of national planning as a future-oriented exercise. Since the adoption of the SDGs in 2015, many countries have started to revise their national development plans in order to align them with the SDGs [1] or have adopted specific SDG implementation plans or “road maps”. So far, parliaments seem to be only weakly associated with these processes [47]. However, as representatives of the people, it is the responsibility of parliaments to ensure that government plans and programs meet the needs of their constituencies on the ground. For the adequate and context-sensitive localization of the SDGs, it would thus be desirable that parliamentarians receive the opportunity to feed their constituents’ priorities into these processes. For prospective horizontal accountability to function effectively, parliaments should thus contribute to the development or revision of such plans through wide-ranging, public consultation processes, and only adopt them after a comprehensive review and formal debate [49]. Another potential avenue for parliaments to contribute towards localization of the 2030 Agenda is their involvement in the development of national priority goals and targets and related indicators for progress monitoring. Through adoption of such indicators, governments subject their SDG action to monitoring and make their performance measurable, including the requirement to provide explanations for underperformance.

2.4. The Role of Supreme Auditing Institutions in SDG Accountability

2.5. The Role of National Human Rights Institutions in SDG Accountability

- Provide advice to governments on the promotion of a human-rights-based approach to implementing the 2030 Agenda by assessing the impact of laws, policies, programs, national development plans, administrative practices, and budgets;

- Engage with all stakeholders to raise awareness, build trust, and promote dialogue;

- Assist in shaping national indicators and data collection systems;

- Monitor progress at all levels to identify inequality and discrimination, through innovative and participatory approaches to data-collection and monitoring;

- Engage with and hold governments to account for poor or uneven progress in implementation, by reporting on SDG progress and obstacles to parliaments, the general public, and national, regional, and international mechanisms;

- Respond to, conduct inquiries into, and investigate allegations of rights violations in the context of development and SDG implementation

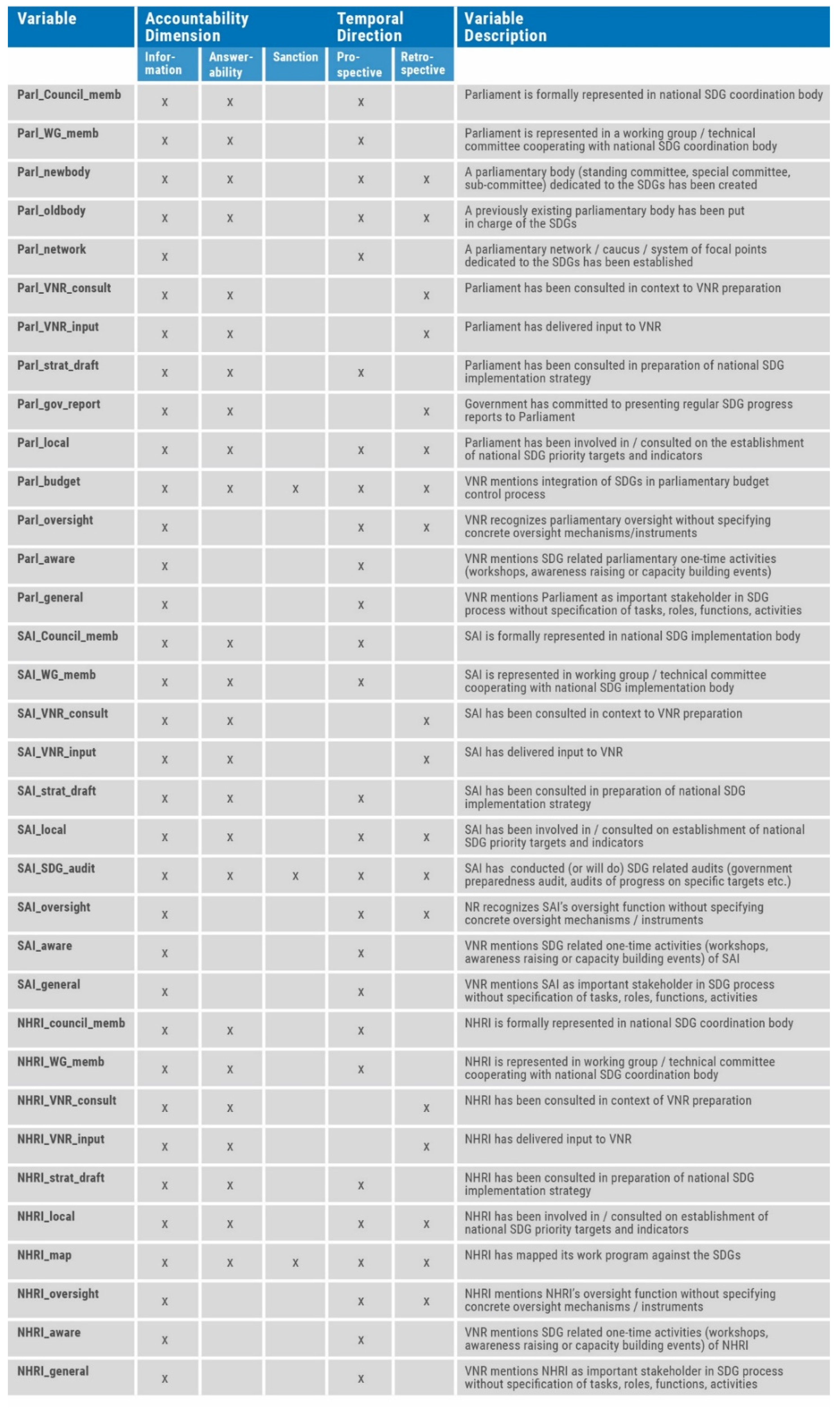

3. Methodology and Data

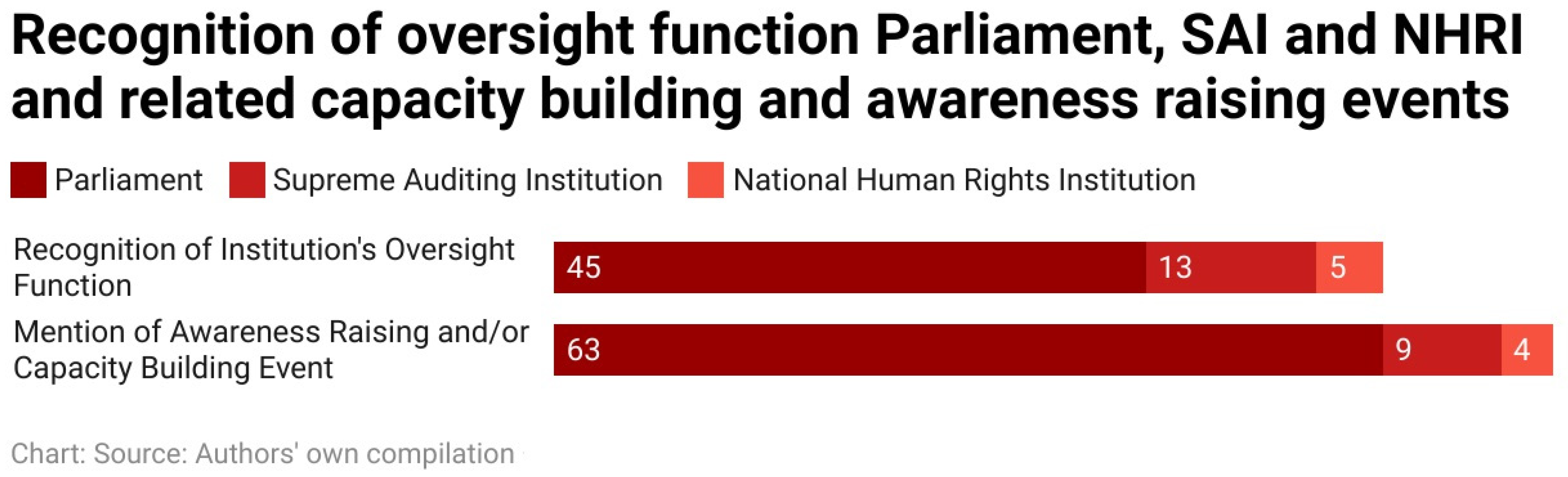

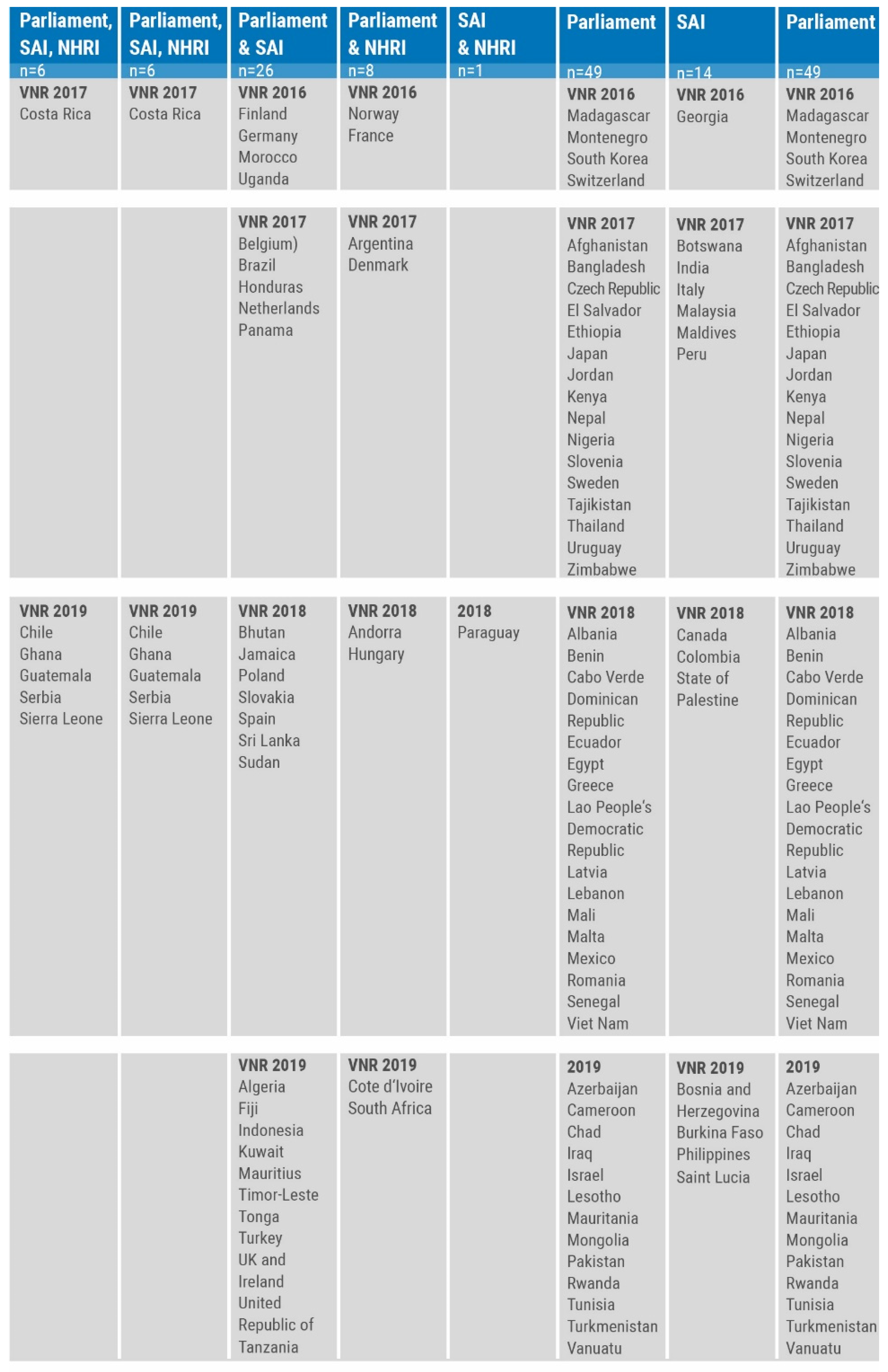

4. Results: Towards Horizontal Accountability in SDG Implementation

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Chimhowu, A.O.; Hulme, D.; Munro, L.T. The ‘New’national development planning and global development goals: Processes and partnerships. World Dev. 2019, 120, 76–89. [Google Scholar] [CrossRef]

- Valensisi, G.; Karingi, S. From global goals to regional strategies: Towards an African approach to SDGs. Afr. Geogr. Rev. 2017, 36, 45–60. [Google Scholar] [CrossRef]

- UNHR; CESR. Who Will Accountable? Human Rights and the Post-2015 Development Agenda; UNHR: Geneva, Switzerland; CESR: New York, NY, USA, 2013. [Google Scholar]

- Amnesty International and CESR. Accountability for the Post-2015 Agenda: A Proposal for a Robust Global Review Mechanism. Amnesty International, CESR, 2015. Available online: https://www.cesr.org/sites/default/files/post-2015_accountability_proposal.pdf (accessed on 17 June 2021).

- UNDP. Follow-Up and Review of the Sustainable Development Goals under the High Level Political Forum; UNDP: New York, NY, USA, 2016. [Google Scholar]

- Biermann, F.; Stevens, C.; Bernstein, S.; Gupta, A.; Kanie, N.; Nilsson, M.; Scobie, M. Global goal setting for improving national governance and policy. In Governing Through Goals: Sustainable Development Goals as Governance Innovation; MIT Press: Cambridge, MA, USA, 2017; Volume 75. [Google Scholar]

- Leininger, J.; Dombrowsky, I.; Breuer, A.; Ruhe, C.; Janetschek, H.; Lotze-Campen, H.; Kriegler, E.; Messner, D.; Nakicenovic, N.; Riahi, K.; et al. Governing the transformations towards sustainability. In Transformations to Achieve the Sustainable Development Goals; IIASA: Laxenburg, Austria, 2018. [Google Scholar]

- Young, O.R. Conceptualization: Goal setting as a strategy for earth system governance. In Governing Through Goals: Sustainable Development Goals as Governance Innovation; MIT Press: Cambridge, MA, USA, 2017; pp. 31–52. [Google Scholar]

- Kanie, N.; Griggs, D.; Young, O.; Waddell, S.; Shrivastava, P.; Haas, P.M.; Broadgate, W.; Gaffney, O.; Kőrösi, C. Rules to goals: Emergence of new governance strategies for sustainable development. Sustain. Sci. 2019, 14, 1745–1749. [Google Scholar] [CrossRef] [Green Version]

- Laberge, M.; Touihri, N. Can SDG 16 Data Drive National Accountability? A Cautiously Optimistic View. Glob. Policy 2019, 10, 153–156. [Google Scholar] [CrossRef]

- Donald, K. Promising the World: Accountability and the SDGs. Health Hum. Rights J. 2016. Available online: https://www.hhrjournal.org/2016/01/promising-the-world-accountability-and-the-sdgs/ (accessed on 17 June 2021).

- Breuer, A.; Leininger, J.; Tosun, J. Integrated Policymaking: Choosing an Institutional Design for Implementing the Sustainable Development Goals (SDGs); Discussion Paper; German Development Institute: Bonn, Germany, 2019. [Google Scholar]

- Cardinal, N.; Romano, J.; Sweeney, E. SDG Accountability Handbook. A Practical Guide for Civil Society; Transparency, Accountability & Participation (TAP) Network: New York, NY, USA, 2019. [Google Scholar]

- Together 2030. Engaging parliaments on the 2030 Agenda and the SDGs: Representation, accountability and implementation. In A Handbook for Civil Society; Together 2030, 2018; Available online: https://sdgtoolkit.org/wp-content/uploads/2018/10/Engaging-parliaments-on-the-2030-Agenda-and-the-SDGs.pdf (accessed on 21 June 2021).

- Kindornay, S. Progressing National SDGs Implementation: An Independent Assessment of the voluntary National Review Reports Submitted to the United Nations High-level Political Forum on Sustainable Development in 2017; Canadian Council for International Co-operation: Ottawa, ON, Canada, 2018. [Google Scholar]

- Smulovitz, C.; Peruzzotti, E. Societal Accountability in Latin America. J. Democr. 2000, 11, 147–158. [Google Scholar] [CrossRef]

- O’Donnell, G. Dissonances. Democratic Critiques of Democracy; University of Notre Dame Press: Notre Dame, IN, USA, 2007. [Google Scholar]

- Bowen, K.J.; Cradock-Henry, N.A.; Koch, F.; Patterson, J.; Häyhä, T.; Vogt, J.; Barbi, F. Implementing the “Sustainable Development Goals”: Towards addressing three key governance challenges—collective action, trade-offs, and accountability. Curr. Opin. Environ. Sustain. 2017, 26, 90–96. [Google Scholar] [CrossRef]

- Karlsson-Vinkhuyzen, S.; Dahl, A.L.; Persson, Å. The emerging accountability regimes for the Sustainable Development Goals and policy integration: Friend or foe? Environ. Plan. C Politics Space 2018, 36, 1371–1390. [Google Scholar] [CrossRef]

- Yamin, A.E.; Mason, E. Why accountability matters for universal health coverage and meeting the SDGs. Lancet 2019, 393, 1082–1084. [Google Scholar] [CrossRef]

- Pillai, K.V.; Slutsky, P.; Wolf, K.; Duthler, G.; Stever, I. Companies’ accountability in sustainability: A comparative analysis of SDGs in five countries. In Sustainable Development Goals in the Asian Context; Springer: Berlin/Heidelberg, Germany, 2017; pp. 85–106. [Google Scholar]

- United Nations. The Sustainable Development Goals Report 2020; United Nations: New York, NY, USA, 2020. [Google Scholar]

- Nature. Get the Sustainable Development Goals back on track. Nature 2020, 577, 7–8. [Google Scholar] [CrossRef]

- Scharpf, F.W. Interaktionsformen: Akteurzentrierter Institutionalismus in der Politikforschung; Leske + Budrich: Opladen, Germany, 2000. [Google Scholar]

- Schedler, A. Conceptualizing accountability. In The Self-Restraining State. Power and Accountability in New Democracies; Schedler, A., Diamond, L., Plattner, M.F., Eds.; Lynne Rienner Publishers: Boulder, CO, USA; London, UK, 1999; Volume 13, p. 17. [Google Scholar]

- Schmitter, P.C. The quality of democracy: The ambiguous virtues of accountability. J. Democr. 2004, 15, 47–60. [Google Scholar] [CrossRef]

- Malena, C.; Forster, R. Social Accountability an Introduction to the Concept and Emerging Practice. 2004. Available online: https://documents1.worldbank.org/curated/en/327691468779445304/pdf/310420PAPER0So1ity0SDP0Civic0no1076.pdf (accessed on 17 June 2021).

- Lindberg, S.I. Mapping accountability: Core concept and subtypes. Int. Rev. Adm. Sci. 2013, 79, 202–226. [Google Scholar] [CrossRef] [Green Version]

- Hilliard, N.; Kovras, I.; Loizides, N. The perils of accountability after crisis: Ambiguity, policy legacies, and value trade-offs. Camb. Rev. Int. Aff. 2021, 34, 1–20. [Google Scholar] [CrossRef] [Green Version]

- Glennon, R.; Ferry, L.; Murphy, P. Our Evaluative Model. In Public Service Accountability; Springer: Berlin/Heidelberg, Germany, 2019; pp. 27–45. [Google Scholar]

- De Ville, K. The role of litigation in human research accountability. Account. Res. Policies Qual. Assur. 2002, 9, 17–43. [Google Scholar] [CrossRef]

- O’Donnell, G. Horizontal Accountability: The Legal Institutionalization of Political Mistrust. In Democratic Accountability in Latin America; Scott, M., Christopher, W., Eds.; Oxford University Press: Oxford, UK, 2003. [Google Scholar] [CrossRef]

- Fearon, J.D. Electoral accountability and the control of politicians: Selecting good types versus sanctioning poor performance. In Democracy, Accountability, and Representation; Przeworski, S.S.A., Manin, B., Eds.; Cambridge University Press: Cambridge, UK, 1999; Volume 55, p. 61. [Google Scholar]

- Ferejohn, J. Incumbent performance and electoral control. Public Choice 1986, 50, 5–25. [Google Scholar] [CrossRef]

- Warren, M.E. Accountability and democracy. In The Oxford Handbook of Public Accountability; Bovens, M., Goodin, R.E., Schillemans, T., Eds.; Oxford University Press: Oxford, UK, 2014; pp. 39–54. [Google Scholar]

- Peruzzotti, E.; Smulovitz, C. Enforcing the Rule of Law: Social Accountability in the New Latin American Democracies; University of Pittsburgh Press: Pittsburgh, PA, USA, 2006. [Google Scholar]

- United Nations. General Assembly, Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: New York, NY, USA, 2015; Volume A/RES/70/1. [Google Scholar]

- Ocampo, J.A.; Gómez-Arteaga, N. Accountability in international governance and the 2030 development agenda. Glob. Policy 2016, 7, 305–314. [Google Scholar] [CrossRef]

- Le Blanc, D. Towards integration at last? The sustainable development goals as a network of targets. Sustain. Dev. 2015, 23, 176–187. [Google Scholar] [CrossRef]

- Pressman, J.L.; Wildavsky, A. Implementation: How Great Expectations in Washington Are Dashed in Oakland; Or, Why it’s Amazing That Federal Programs Work At All, This Being a Saga of the Economic Development Administration as Told by Two Sympathetic Observers Who Seek to Build Morals on a Foundation; University of California Press: Berkely, CA, USA; Los Angeles, CA, USA; London, UK, 1984; Volume 708. [Google Scholar]

- Mueller, D.C. Public choice in perspective. In Perspectives on Public Choice; Mueller, D.C., Ed.; Cambridge University Press: Cambridge, UK, 1997; pp. 1–17. [Google Scholar]

- Morçöl, G. Public Service in Complex Governance Networks. In Public Policy Making in a Globalized World; Lewis, R.J., Ed.; Taylor and Francis: London, UK, 2017; pp. 150–167. [Google Scholar]

- de Vries, G. How National Audit Offices Can Support Implementation of the SDGs. Public Financial Management Blog. 2016. Available online: https://www.intosaicbc.org/wp-content/uploads/2018/08/PMF-Blog-on-SDGs-and-SAIs-role.pdf (accessed on 17 June 2021).

- Tan, X. Constructing a performance-based accountability system for the Chinese government. J. Public Aff. 2014, 14, 154–163. [Google Scholar] [CrossRef]

- Morgenbesser, L. The menu of autocratic innovation. Democratization 2020, 27, 1053–1072. [Google Scholar] [CrossRef]

- Tsakatika, M. A parliamentary dimension for EU soft governance. Eur. Integr. 2007, 29, 549–564. [Google Scholar] [CrossRef]

- Chungong, M. Transforming the SDGs into Everyday Reality: The Role of Parliaments; East-West Center: Honolulu, HI, USA, 2018. [Google Scholar]

- Inter-Parliamentary Union. Hanoi Declaration. The Sustainable Development Goals: Turning Words into Action. In Adopted by 132nd IPU Assembly; IPU: Hanoi, Vietnam, 2015. [Google Scholar]

- Inter-Parliamentary Union. Parliaments and the Sustainable Development Goals. In A self-Assessment Toolkit; Inter-Parliamentary Union: Geneva, Switzerland, 2016. [Google Scholar]

- Inter-Parliamentary Union. Institutionalization of the Sustainable Development Goals in the Work of Parliaments; Inter-Parliamentary Union: Geneva, Switzerland, 2019. [Google Scholar]

- GLOBE; UNEP. Bringing the 2015 Summits Home. An Action Agenda for Legislators; United Nations Environment Programme: Brussels, Belgium, 2016. [Google Scholar]

- Cázarez-Grageda, K. The Whole of Society Approach: Levels of Engagement and Meaningful Participation of Different Stakeholders in the Review Process of the 2030 Agenda; Partners for Review (P4R): Bonn, Germany, 2018. [Google Scholar]

- Hege, E.; Brimont, L.; Pagnon, F. Sustainable development goals and indicators: Can they be tools to make national budgets more sustainable? Public Sect. Econ. 2019, 43, 423–444. [Google Scholar] [CrossRef]

- Deveaux, K.; Rodrigues, C. Parliament’s Role in Implementing the Sustainable Development Goals. A parliamentary Handbook; Global Organization of Parliamentarians Against Corruption (GOPAC); United Nations Development Programme (UNDP); Islamic Development Bank (IDB): Jeddah, Saudi Arabia, 2017. [Google Scholar]

- Müller-Wille, B. Improving the democratic accountability of EU intelligence. Intell. Natl. Secur. 2007, 21, 100–128. [Google Scholar] [CrossRef]

- Peters, D.; Wagner, W.; Deitelhoff, N. The Parliamentary Control of European Security Policy; Arena Oslo: Oslo, Norway, 2008; Volume 6. [Google Scholar]

- Hege, E.; Brimont, L. Integrating SDGs into national budgetary processes. Studies 2018, 5, 18. [Google Scholar]

- SDSN. Getting Started with the Sustainable Development Goals: A Guide for Stakeholders; Sustainable Development Solutions Network (SDSN): New York, NY, USA, 2015. [Google Scholar]

- United Nations. Development Group Mainstreaming the 2030 Agenda: Reference Guide for UN Country Teams; United Nations: New York, NY, USA, 2017. [Google Scholar]

- OECD. Getting Governments Organised to Deliver on the Sustainable Development Goals; United Nations: New York, NY, USA, 2017. [Google Scholar]

- van Winden, E. Auditors of Sustainability: Exploring the Role of Supreme Audit Institutions in the Implementation of the Sutainable Development Goals; Utrecht University: Den Haag, The Netherlands, 2017. [Google Scholar]

- Nagy, S.; Gal, J.; Veha, A. Improving audit functions of supreme audit institutions to promote sustainable development. Appl. Stud. Agribus. Commer. 2012, 6, 63–70. [Google Scholar] [CrossRef]

- OECD. Supreme Audit Institutions and Good Governance: Oversight, Insight and Foresight; OECD: Paris, France, 2016. [Google Scholar]

- Streim, H. Agency problems in the legal political system and supreme auditing institutions. Eur. J. Law Econ. 1994, 1, 177–191. [Google Scholar] [CrossRef]

- Gailmard, S. Accountability and principal-agent models. In The Oxford Handbook of Public Accountability; Bovens, R.E.G., Schillemans, T., Eds.; Oxford University Press: Oxford, UK, 2014; pp. 90–106. [Google Scholar]

- van Leeuwen, S. Auditing international environmental agreements: The role of supreme audit institutions. Environmentalist 2004, 24, 93–99. [Google Scholar] [CrossRef]

- INTOSAI. Strengthening External Public Auditing in INTOSAI Regions. In Proceedings of the Contributions and Results of the INTOSAI Conference, Vienna, Austria, 26–27 May 2010; pp. 1–175. [Google Scholar]

- Lafortune, G.; Schmidt-Traub, G. SDG Challenges in G20 Countries. In Sustainable Development Goals: Harnessing Business to Achieve the SDGs through Finance, Technology, and Law Reform; John Wiley & Sons: Hoboken, NJ, USA, 2019; pp. 219–234. [Google Scholar]

- United Nations. Promoting the Efficiency, Accountability, Effectiveness and Transparency of Public Administration by Strengthening Supreme Audit Institutions; United Nations: New York, NY, USA, 2011; Volume 66, p. 209. [Google Scholar]

- United Nations. Promoting and Fostering the Efficiency, Accountability, Effectiveness and Transparency of Public Administration by Strengthening Supreme Audit Institutions; United Nations General Assembly: New York, NY, USA, 2014; Volume 69, p. 228. [Google Scholar]

- INTOSAI. Are Nations Prepared for Implementation of the 2030 Agenda? Supreme Audit Institutions’ Insights and Recommendations; INTOSAI Development Initiative: Oslo, Norway, 2019. [Google Scholar]

- GANHRI. National Human Rights Institutions Engaging with the Sustainable Development Goals (SDGs); GANHRI: Geneva, Switzerland, 2017. [Google Scholar]

- The Danish Institute for Human Rights. NHRIs’ Independence and Accountability; The Danish Institute for Human Rights: Copenhagen, Denmark, 2013. [Google Scholar]

- Witmer, R.; Moreno, E. The Power of the Pen: Human Rights Ombudsmen and Personal Integrity Violations in Latin America, 1982–2006. Hum. Rights Rev. 2016, 17, 143–164. [Google Scholar]

- ENNHRI. Applying a Human Rights-Based Approach to Poverty Reduction and Measurement. In A Guide for National Human Rights Institutions; European Network of National Human Rights Institutions: Brussels, Belgium, 2019. [Google Scholar]

- United Nations. Principles Relating to the Status of National Institutions (The Paris Principles); United Nations General Assembly: New York, NY, USA, 1993; Volume 48, p. 134. [Google Scholar]

- CNDH; OHCHR. The Mérida Declaration. In The Role of National Human Rights Institutions in implementing the 2030 Agenda for Sustainable Development; CNDH: Mérida, Mexico; OHCHR: Yucatàn, Mexico, 2015. [Google Scholar]

- Schillemans, T. Accountability in the shadow of hierarchy: The horizontal accountability of agencies. Public Organ. Rev. 2008, 8, 175. [Google Scholar] [CrossRef] [Green Version]

- Tosun, J.; Leininger, J. Governing the interlinkages between the sustainable development goals. Glob. Chall. 2017, 1, 1700036. [Google Scholar] [CrossRef]

- Hsieh, H.-F.; Shannon, S.E. Three approaches to qualitative content analysis. Qual. Health Res. 2005, 15, 1277–1288. [Google Scholar] [CrossRef]

- UN-DESA. Handbook for the Preparation of Voluntary National Reviews; United Nations Department of Economic and Social Affairs; High-level Political Forum (HLPF) on Sustainable Development: New York, NY, USA, 2019. [Google Scholar]

- The Republic of Serbia. Towards Equality of Sustainable Opportunities for Everyone and Everywhere in Serbia Through Growing into Sustainability. In Voluntary National Review of the Republic of Serbia on the Implementation of the 2030 Agenda for Sustainable Development; The Republic of Serbia: Belgrade, Serbia, 2019. [Google Scholar]

- Japan VNR. Japan’s Voluntary National Review. Report on the implementation of the Sustainable Development Goals; Japan VNR: Tokyo, Japan, 2017.

- Sudan VNR. Voluntary National Review 2018. In Implementation of Agenda 2030 and the SDGs for Peace and Development in the Sudan; National Population Council: Khartoum, Sudan, 2018. [Google Scholar]

- Bundesrechnungshof Abschließende Mitteilung an das Bundeskanzleramtüber die Prüfung der nationalen Umsetzung der Ziele für Nachhaltige Entwicklung der Vereinten Nationen—Agenda 2030; Bundesrechnungshof: Bonn, Germany, 2019.

- Australian Government. Report on the Implementation of the Sustainable Development Goals; Australian Government: Canberra, Australia, 2018.

- Australian Human Rights Commission. Inquiry into the United Nations Sustainable Development Goals; Australian Human Rights Commission: Sydney, Australia, 2018.

- Bangladesh VNR. Eradicating poverty and promoting prosperity in a changing world. In Voluntary National Review (VNR) 2017; Government of the People’s Republic of Bangladesh: Dhaka, Bangladesh, 2017. [Google Scholar]

- Kenya Parliamentary. Caucus on SDGS & Business Kenya Parliamentary Caucus on SDGS & Business. Available online: https://www.kenyasdgscaucus.org/ (accessed on 17 June 2021).

- Kenya VNR. Implementation of the Agenda 2030 for Sustainable Development in Kenya; Ministry of Devolution and Planning: Neirobi, Kenya, 2017.

- Kuwait VNR. Kuwait VNR. Kuwait Voluntary National Review 2019. In Report on the Implementation of the 2030 Agenda to the UN High-Level Political Forum on Sustainable Development; Government of Kuwait: Kuwait City, Kuwait, 2019. [Google Scholar]

- Madagascar VNR. Rapport National de Revuedu Processus de l’Agenda 2030 pour le Developpement Durable; Ministre de l’Economie et du Plan: Antananarivo, Madagascar, 2016.

- Lao People’s Democratic Republic VNR. Lao People’s Democratic Republic: Voluntary National Review on the Implementation of the 2030 Agenda for Sustainable Development; Government of the Lao People’s Democratic Republic: Vientiane, Lao People’s Democratic Republic, 2018.

- Sierra Leone VNR. 2019 VNR Report on SDGs in Sierra Leone; Government of Sierra Leone, Ministry of Planning and Economic Development: Freetown, Sierra Leone, 2019.

- Cote d’Ivoire VNR. Rapport Volontaire D’Examen National de la Mise en Œuvre des Objectifs de Developpement Durable en Côte D’Ivoire; Ministere du Plan et du Developpement: Abidjan, Ivory Coast, 2019.

- Germany VNR. Report of the German Federal Governmentto theHigh-Level Political Forum on Sustainable Development 2016; The Federal Government: Berlin, Germany, 2016.

- Levy, B. State capacity, accountability and economic development in Africa. Commonw. Comp. Politics 2007, 45, 499–520. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Breuer, A.; Leininger, J. Horizontal Accountability for SDG Implementation: A Comparative Cross-National Analysis of Emerging National Accountability Regimes. Sustainability 2021, 13, 7002. https://doi.org/10.3390/su13137002

Breuer A, Leininger J. Horizontal Accountability for SDG Implementation: A Comparative Cross-National Analysis of Emerging National Accountability Regimes. Sustainability. 2021; 13(13):7002. https://doi.org/10.3390/su13137002

Chicago/Turabian StyleBreuer, Anita, and Julia Leininger. 2021. "Horizontal Accountability for SDG Implementation: A Comparative Cross-National Analysis of Emerging National Accountability Regimes" Sustainability 13, no. 13: 7002. https://doi.org/10.3390/su13137002

APA StyleBreuer, A., & Leininger, J. (2021). Horizontal Accountability for SDG Implementation: A Comparative Cross-National Analysis of Emerging National Accountability Regimes. Sustainability, 13(13), 7002. https://doi.org/10.3390/su13137002