Corporate Social Responsibility Strategies in Spanish Electric Cooperatives. Analysis of Stakeholder Engagement

Abstract

1. Introduction

2. Theoretical Framework

2.1. Strategic Management of CSR: Models, Regulations, Legislation and Guidelines

2.2. CSR and SDGs in Spanish Electric Cooperatives

2.3. CSR Management with Stakeholders in Electric Cooperatives

3. Methods

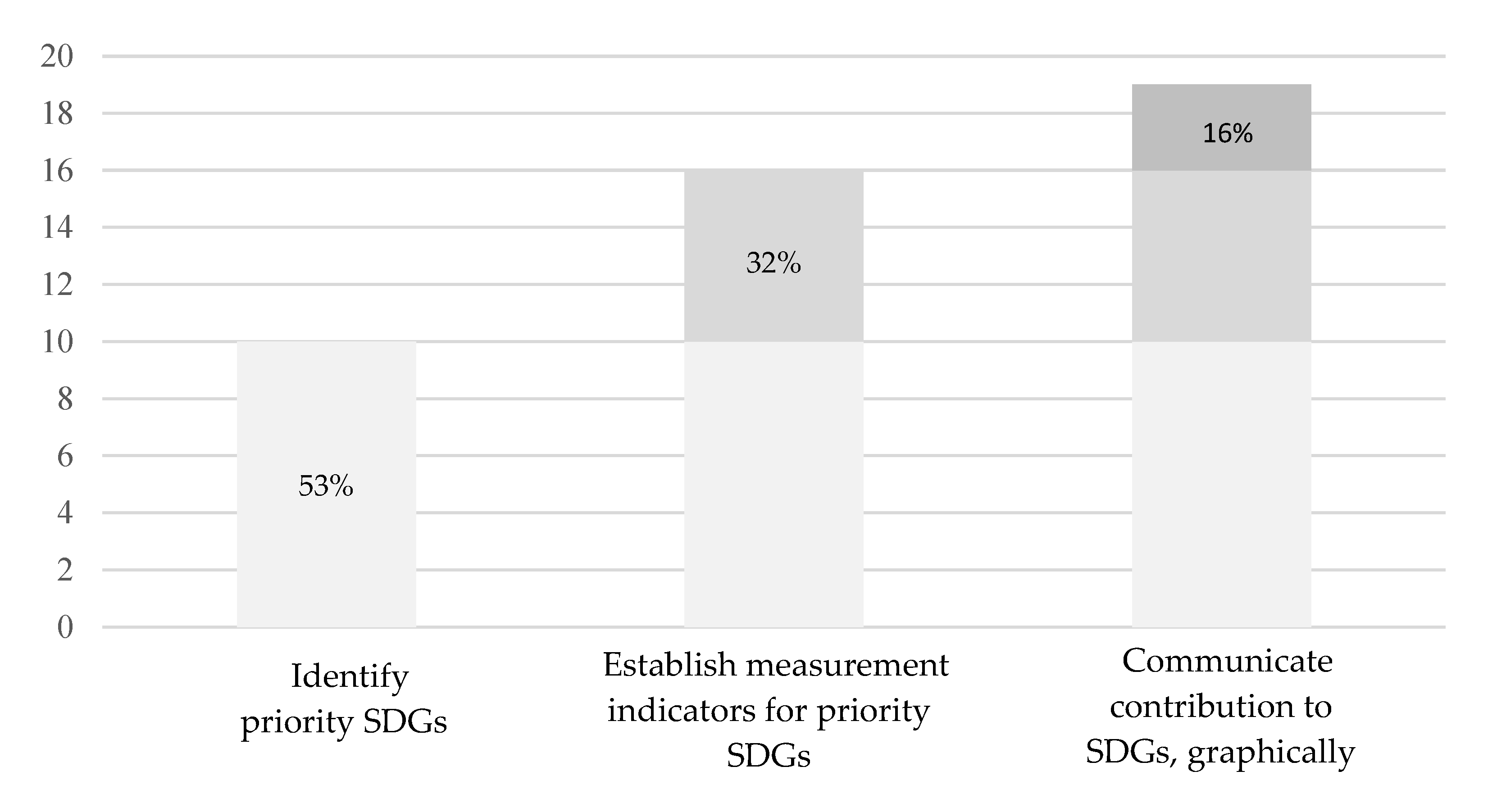

4. Results

5. Conclusions and Future Lines of Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- Management is aware of the importance of integrating corporate social responsibility actions.

- Management is aware of the importance of CSR, has defined a CSR policy and has communicated it to stakeholders.

- Management has defined its CSR policy, and has a framework document with objectives, goals, and programs in line with its CSR policy.

- Management has a CSR framework document and has allocated resources for the implementation of CSR in organizational management.

- In addition, management is committed to the continuous improvement of the CSR management system.

- Management is aware of the need to establish communication mechanisms for CSR reporting.

- Management is aware of the need and ensures that effective CSR communication channels are established and implemented.

- Management, in addition to establishing CSR communication channels, has a procedure to disseminate progress in its CSR management.

- Management encourages stakeholder participation in CSR through its communication channels and collects opinions through surveys or other methods.

- In addition, the organization analyzes the feedback given to its CSR communication for the purposes of continuous improvement.

- The organization has a clear management approach to maximize profits in a sustainable way.

- The organization has a clear management approach and has established the necessary control mechanisms and systems to ensure managers meet the established values.

- The organization, in addition to control mechanisms, has established management systems to account for the impact of its decisions.

- Through the previous mechanisms, the organization analyses and evaluates its economic, social, and environmental impacts.

- In addition to the above, the organization assumes and demonstrates a public commitment to information transparency.

- The organization has the right policies to ensure fairness and equality to workers.

- The organization has management policies and mechanisms in place to ensure legal compliance in labor matters.

- The organization has equity and equality policies in place, mechanisms to ensure legal compliance in labor matters, and formalized documents of the systems of remuneration, selection, promotion, working hours, permits, conciliation, etc.

- The organization has perception and performance data and indicators to evaluate and monitor the effectiveness of HR policies described above.

- In addition, the organization aligns HR management plans with its business strategy.

- The organization has an estimate of its direct and indirect contribution to the local economy.

- Based on the estimation of its contribution, the organization performs one-off actions that promote local employment.

- In addition to these actions, the organization systematically incorporates the local aspect into its purchasing and recruitment processes.

- The organization has indicators to measure its contribution to the development of the local economy.

- The organization analyses the results of the above actions and proposes improvements in its policies to promote local development.

- Management is aware of the importance of meeting the needs of stakeholders.

- The organization, aware of its importance, has identified and classified its stakeholders.

- The organization, in addition to identifying and classifying stakeholders, has a document that establishes communication channels with its stakeholders.

- The organization has defined, classified, prioritized stakeholders, and has established processes for their participation in relevant corporate aspects.

- In addition, management takes into account stakeholder expectations to define the organization’s strategy.

- The organization is aware of its responsibility in improving the social aspects of community life.

- The organization contributes to the organization of cultural and sporting events in the local community.

- The organization allocates a specific budget to the promotion of the community’s cultural and sporting events.

- The organization has a plan to channel the promotion and funding of social and cultural initiatives.

- As a result, the organization adopts the principles of improving the social aspects of community life.

- The organization guarantees compliance with environmental regulations.

- The organization has taken steps beyond the legal aspects to reduce external and internal environmental impacts of production.

- The organization has implemented environmental plans, which include measures to prevent and manage environmental risks.

- The organization has also deployed its environmental plans to its suppliers and distributors.

- The organization has reviewed the results of its environmental plans together with its stakeholders to make improvements.

- The organization provides clear, accurate, and truthful information about its products/services on labeling and other technical documents.

- The organization, in addition to labeling and technical documentation, establishes communication channels to answer frequently asked questions, including those related to social, environmental, and after-sales service aspects.

- The organization, in addition to providing clear information, establishes communication channels to disseminate advice for the responsible use of its products or services.

- The organization accepts consumers’ suggestions for improvement via established communication channels.

- In addition to the above, the organization applies suggestions for improvement by introducing social and environmental criteria into its innovation processes.

- No, it is not aware (press “next” button and submit questionnaire).

- Yes, it is aware and has collected information about them.

- Yes, it is aware, has collected information about them, and has shown interest in contributing to their achievement.

- Given this interest, the organization has established a priority plan to contribute to their achievement.

- Yes.

- No.

- Yes.

- No.

- Yes.

- No.

- Yes.

- No.

- Yes.

- No.

- No.

- Yes, it provides network access to the most disadvantaged sectors.

- Yes, it offers accessible service packages for most disadvantaged groups.

- Yes, it provides access in the most disadvantaged sectors, offers accessible service packages to disadvantaged groups.

- Yes, it combines different network, product, or price actions (social bonds, discounts, deferrals, and payment splits) to promote access to energy to disadvantaged groups.

- It does not apply because the organization does not have its own network.

- No.

- Yes, preventive actions are performed periodically.

- Yes, preventive actions are performed following a plan to reduce the number of interruptions equivalent to the installed capacity (NIEPI indicator).

- □

- It does not apply because the organization does not have its own network.

- □

- No.

- □

- Yes, preventive actions are performed periodically.

- □

- Yes, preventive actions are performed following a plan to reduce the average interruption time equivalent to the installed capacity (TIEPI).

- □

- No.

- □

- The percentage of marketed electricity from emissions-free technologies is higher than the previous year.

- □

- The 100% renewable origin of electricity has been certified by the National Commission on Markets and Competition (CNMC).

- □

- The marketing of 100% renewable energy is the purpose of the organization.

- □

- It does not apply because the organization does not generate energy.

- □

- The percentage of renewable origin electricity is higher than the previous year.

- □

- The 100% renewable origin of electricity has been certified by the National Commission on Markets and Competition (CNMC).

- □

- The production and marketing of 100% renewable energy is the purpose of the organization.

- □

- No.

- □

- Improvements have been made to buildings and facilities, and processes to improve energy efficiency have been implemented.

- □

- No.

- □

- Yes.

- □

- No.

- □

- Yes.

- □

- No.

- □

- Yes, the organization measures its carbon footprint according to the “GHG Protocol” or the ISO Norm 14064-1.

- □

- In addition to measuring its carbon footprint, the organization has specific policies to curb climate change.

- □

- No.

- □

- Yes, it has done so by using its own indicators.

- □

- Yes, it has done so from the life cycle perspective (ISO/TS 14072:2014).

- □

- No.

- □

- Yes, to internal audiences.

- □

- Yes, to external audiences using its own (web) platforms.

- □

- Yes, to internal and external audiences.

- □

- Yes, there is a plan to raise social awareness on climate change aimed at all stakeholders.

References

- McKie, D.; Heath, R. Public relations as a strategic intelligence for the 21st century: Contexts, controversies, and challenges. Public Relat. Rev. 2016, 42, 298–305. [Google Scholar] [CrossRef]

- Kramer, M.R.; Porter, M.E. Estrategia y sociedad: El vínculo entre ventaja competitiva y responsabilidad social corporativa. Harv. Bus. Rev. 2006, 84, 42–56. [Google Scholar]

- Johnston, K.; Taylor, M. The Handbook of Communication Engagement; Wiley & Sons: Hoboken, NJ, USA, 2018. [Google Scholar]

- Mozas-Moral, A.; Puentes-Poyatos, R. La responsabilidad social corporativa y sus paralelismos con las sociedades cooperativas. REVESCO 2010, 103, 75–100. [Google Scholar]

- Torres-Pérez, F.J. Análisis legal de la implementación de la RSC en las Sociedades Cooperativas. Rev. Jurídica Portucalense 2017, 21, 57–79. [Google Scholar]

- Boronat-Navarro, M.; Pérez-Aranda, J.A. Consumers’ perceived corporate social responsibility evaluation and support: The moderating role of consumer information. Tour. Econ. 2019, 25, 613–638. [Google Scholar] [CrossRef]

- Shahidul, H.; Jamilah, H. Ethics in Public Relations and Responsible Advocacy Theory. Malays. J. Commun. Jilid 2017, 33, 147–157. [Google Scholar]

- Kim, S.; Lee, H. The Effect of CSR Fit and CSR Authenticity on the Brand Attitude. Sustainability 2020, 12, 275. [Google Scholar] [CrossRef]

- Cramer, J.; Jonker, J.; Van Der Heijden, A. Making sense of corporate social responsibility. J. Bus. Ethics 2004, 55, 215–222. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2012, 103, 351–383. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. The causal effect of corporate governance on corporate social responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Lane, A.B.; Devin, B. Operationalizing stakeholder engagement in CSR: A process approach. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 267–280. [Google Scholar] [CrossRef]

- Raufflet, E. Responsabilidad social corporativa y desarrollo sostenible: Una perspectiva histórica y conceptual. Cuad. De Adm. 2010, 43, 23–32. [Google Scholar]

- Server-Izquierdo, R.; Lajara-Camilleri, N. La gestión sostenible de las cooperativas. Los valores y principios cooperativos como referencia. AECA 2016, 115, 60–61. [Google Scholar]

- Torres-Valdés, R.; Campillo-Alhama, C. Desarrollo local y relaciones públicas para grupos desfavorecidos en la Comunidad de Madrid. Prism. Soc. 2013, 10, 394–432. [Google Scholar]

- Salas-Fumás, V. Responsabilidad social corporativa (RSC) y creación de valor compartido. La RSC según Michael Porter y Mark Kramer. Rev. De Responsab. Soc. De La Empresa 2011, 3, 15–40. [Google Scholar]

- Rodrigues, M.; do Céu Alves, M.; Oliveira, C.; Vale, V.; Vale, J.; Silva, R. Dissemination of social accounting information: A bibliometric review. Economies 2021, 9, 41. [Google Scholar] [CrossRef]

- Rodrigues, M.; Franco, M. The formulation and implementation of corporate sustainability strategy in organizations. In Management in Public Administration Information and Technology Education; Severo de Almeida, F.A., Malheiro da Silva, A., Tristão, G., Conti de Freitas, C., Eds.; University of Porto-FLUP: Porto, Portugal, 2019. [Google Scholar]

- Rodrigues, M.; Franco, M. The Corporate Sustainability Strategy in Organisations: A Systematic Review and Future Directions. Sustainability 2019, 11, 6214. [Google Scholar] [CrossRef]

- Mochales-González, G. Modelo Explicativo de la Responsabilidad Social Corporativa Estratégica. Ph.D. Thesis, Faculty of Economics and Business, Complutense University of Madrid, Madrid, Spain, 2014. [Google Scholar]

- Vargas-Sánchez, A.; Vaca-Acosta, R.M. Responsabilidad social corporativa y cooperativismo: Vínculos y potencialidades. CIRIEC 2005, 31, 207–230. [Google Scholar]

- REScoop.eu is the European Federation of Citizen Energy Cooperatives. Available online: https://www.rescoop.eu/ (accessed on 26 May 2021).

- Pérez, I.C.; Celador, Á.C.; Zubiaga, J.T. Las cooperativas de energía renovable como instrumento para la transición energética en España. Energy Policy 2018, 123, 215–229. [Google Scholar]

- Falcón Pérez, C.E. Las cooperativas energéticas como alternativa al sector eléctrico español: Una oportunidad de cambio. Actual. Jurid. Ambient. 2020, 104, 50–108. [Google Scholar]

- Zadek, S. Titans or Titanic: Towards a Public Fiduciary. Bus. Prof. Ethics J. 2012, 31, 207–230. [Google Scholar] [CrossRef]

- Roper, J.; Hurst, B. Public relations, futures planning and political talk for addressing wicked problems. Public Relat. Rev. 2019, 45, 101828. [Google Scholar] [CrossRef]

- L’Etang, J.; McKie, D.; Snow, N.; Xifra, J. The Routledge Handbook of Critical Public Relations; Routledge: London, UK, 2015. [Google Scholar]

- Ingenhoff, D.; Marschlich, S. Corporate diplomacy and political CSR: Similarities, differences and theoretical implications. Public Relat. Rev. 2019, 45, 348–371. [Google Scholar] [CrossRef]

- Ozdora, E.; Ferguson, M.A.; Duman, S.A. Corporate social responsibility and CSR fit as predictors of corporate reputation: A global perspective. Public Relat. Rev. 2016, 42, 79–81. [Google Scholar] [CrossRef]

- Grunig, J.E.; Hunt, T. Managing Public Relations; Harcourt Brace Jovanovich College Publishers: Fort Worth, TX, USA, 1984. [Google Scholar]

- Eding, E.; Scholtens, B. Corporate social responsibility and shareholder proposals. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 648–660. [Google Scholar] [CrossRef]

- Garriga, E.; Melé-Carné, D. Corporate Social Responsibility Theories: Mapping the Territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Melé-Carné, D. Corporate social responsibility theories. In The Oxford Handbook of Corporate Social Responsibility; Crane, A., Matten, D., McWilliams, A., Moon, J., Siegel, D.S., Eds.; Oxford University Press: New York, NY, USA, 2008. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Freeman, R.E. The new story of business: Towards a more responsible capitalism. Bus. Soc. Rev. 2017, 122, 449–465. [Google Scholar] [CrossRef]

- Martínez-García-de-Leaniz, P.; Rodríguez-del-Bosque-Rodríguez, I. Revisión teórica del concepto y estrategias de medición de la responsabilidad social corporativa. Prism. Soc. 2013, 11, 321–350. [Google Scholar]

- Rodríguez-Martínez, A.; Moyano-Fuentes, J.; Jiménez-Delgado, J.J. Estado actual de la investigación en Responsabilidad Social Corporativa a nivel organizativo: Consensos y desafíos futuros. CIRIEC 2015, 85, 143–179. [Google Scholar] [CrossRef]

- Visser, W. CSR 2.0 and the New DNA of Business. J. Bus. Syst. Gov. Ethics 2010, 5, 7–22. [Google Scholar]

- Servera-Francés, D.; Fuentes-Blasco, M.; Piqueras-Tomás, L. The Importance of Sustainable Practices in Value Creation and Consumers’ Commitment with Companies’ Commercial Format. Sustainability 2020, 12, 9852. [Google Scholar] [CrossRef]

- Carroll, A. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Quazi, A.M.; O’Brien, D. An Empirical Test of a Cross-national Model of Corporate Social Responsibility. J. Bus. Ethics 2000, 25, 33–51. [Google Scholar] [CrossRef]

- Strandberg, L. La implementación de la RSC en la cadena de valor. Cuad. De La Cátedra “La Caixa” 2010, 6, 1–30. [Google Scholar]

- Zadek, S. El camino hacia la responsabilidad corporativa. Harv. Bus. Rev. 2005, 83, 60–69. [Google Scholar]

- Zadek, S. The Civil Corporation: The New Economy of Corporate Citizenship; Routledge: London, UK, 2007. [Google Scholar]

- CSR Strategy of Spanish Companies. Available online: http://www.mitramiss.gob.es/es/rse/eerse/index.htm (accessed on 28 April 2021).

- Visser, W.; Courtice, P. Sustainability Leadership: Linking Theory and Practice. SSRN 2011, 1–14. [Google Scholar] [CrossRef]

- Portal de la Responsabilidad Social. Available online: http://www.mitramiss.gob.es/es/rse/index.htm (accessed on 28 April 2021).

- International Integrated Reporting Council. The International <IR> Framework; International Integrated Reporting Council: London, UK, 2014. [Google Scholar]

- Global Reporting Initiative (GRI). Available online: https://www.globalreporting.org/Pages/default.aspx (accessed on 28 April 2021).

- Global Reporting Initiative (GRI). Available online: www.globalreporting.org/standards (accessed on 28 April 2021).

- Brundtland, G.; Khalid, M.; Agnelli, S.; Al-Athel, S.; Chidzero, B.; Fadika, L. Report of the World Commission on Environment and Development: Our Common Future; Development and International Co-operation: Environment; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- United Nations. Report of the United Nations Conference on Environment and Development; United Nations Publication: New York, NY, USA, 1992. [Google Scholar]

- The UN Global Compact. Available online: https://widgets.weforum.org/history/1999.html (accessed on 28 April 2021).

- United Nations Conference on Sustainable Development, Rio+20. Available online: https://sustainabledevelopment.un.org/rio20 (accessed on 28 April 2021).

- UN 2030 Agenda. Available online: https://www.un.org/sustainabledevelopment/es/ (accessed on 28 April 2021).

- Grushina, S.V. Collaboration by design: Stakeholder engagement in GRI sustainability reporting guidelines. Organ. Environ. 2017, 30, 366–385. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Amor-Esteban, V.; Galindo-Álvarez, D. Communication Strategies for the 2030 Agenda Commitments: A Multivariate Approach. Sustainability 2020, 30, 366–385. [Google Scholar]

- Ali, S.; Hussain, T.; Zhang, G.; Nurunnabi, M.; Li, B. The Implementation of Sustainable Development Goals in “BRICS” Countries. Sustainability 2018, 10, 2513. [Google Scholar] [CrossRef]

- SDG Compass. La Guía Para la Acción Empresarial en los ODS; United Nations: New York, NY, USA, 2016. [Google Scholar]

- Haro del Rosario, A.; Benítez-Sánchez, M.N.; Caba-Pérez, M.C. Responsabilidad social corporativa en el sector eléctrico. Finanzas Y Política Económica 2011, 3, 49–64. [Google Scholar]

- Gobierno de España. Spanish CSR Strategy; Ministerio de Empleo y Seguridad Social: Madrid, Spain, 2014. [Google Scholar]

- Law 54/1997, of November 27, on the Electricity Sector. Gobierno de España. Available online: https://www.boe.es/buscar/pdf/1997/BOE-A-1997-25340-consolidado.pdf (accessed on 10 May 2020).

- National Commission on Markets and Competition. Available online: https://www.cnmc.es/ (accessed on 28 April 2021).

- United Nations Division for Sustainable Development Goals. Available online: https://www.un.org/spanish/esa/desa/aboutus/dsd.html (accessed on 28 April 2021).

- Duque-Orozco, Y.; Cardona-Acevedo, M.; Rendón-Acevedo, J.A. Responsabilidad social empresarial: Teorías, índices, estándares y certificaciones. Cuad. De Adm. 2013, 29, 1–11. [Google Scholar] [CrossRef]

- Herremans, I.M.; Nazari, J.A.; Mahmoudian, F. Stakeholder relationships, engagement, and sustainability reporting. J. Bus. Ethics 2016, 138, 417–435. [Google Scholar] [CrossRef]

- Rodríguez-Fernández, M.; Gaspar-González, A.I.; Sánchez-Teba, E.M. Sustainable social responsibility through stakeholders engagement. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2425–2436. [Google Scholar] [CrossRef]

- Dopazo-Fraguío, P. Informes de responsabilidad social corporativa (RSC): Fuentes de información y documentación. Rev. Gen. De Inf. Y Doc. 2012, 22, 279–305. [Google Scholar]

- Orozco-Toro, J.A.; Ferré-Pavia, C. La comunicación estratégica de la responsabilidad social. Razón Y Palabra 2013, 83, 342–357. [Google Scholar]

- Arenas-Torres, F.; Bustamante-Ubilla, M.; Campos-Troncoso, R. The Incidence of Social Responsibility in the Adoption of Business Practices. Sustainability 2021, 13, 2794. [Google Scholar] [CrossRef]

- Grunig, J. Publics, audiences and marjet segments: Segmentation principles for campaigns. In Information Campaigns: Balancing Social Values and Social Change; Salmon, C.T., Ed.; Sage: Newbury Park, CA, USA, 1989. [Google Scholar]

- Grunig, J. A situational theory of publics: Conceptual history, recent challenges and new research. In Public Relations Research: An International Perspective; Moss, D., MacManus, T., Vercic, D., Eds.; International Thomson Business Press: London, UK, 1997. [Google Scholar]

- IESE. PWC. Código de Gobierno Para la Empresa Sostenible; IESE: Barcelona, Spain, 2010. [Google Scholar]

- Esman, M.J. The Elements of Institution Building. In Institution Building and Development; Eaton, J.W., Ed.; Sage: Beverly Hills, CA, USA, 1972. [Google Scholar]

- Stocker, F.; de Arruda, M.P.; de Mascena, K.M.C.; Boaventura, J.M.G. Stakeholder engagement in sustainability reporting: A classification model. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2071–2080. [Google Scholar] [CrossRef]

- Hu, B.; Zhang, T.; Yan, S. How Corporate Social Responsibility Influences Business Model Innovation: The Mediating Role of Organizational Legitimacy. Sustainability 2020, 12, 2667. [Google Scholar] [CrossRef]

- Guillamon-Saorin, E.; Kapelko, M.; Stefanou, S.E. Corporate Social Responsibility and Operational Inefficiency: A Dynamic Approach. Sustainability 2018, 10, 2277. [Google Scholar] [CrossRef]

- Lunenberg, K.; Gosselt, J.; De Jong, M. Framing CSR fit: How corporate social responsibility activities are covered by news media. Public Relat. Rev. 2016, 42, 943–951. [Google Scholar] [CrossRef]

- Kvasničková Stanislavská, L.; Pilař, L.; Margarisová, K.; Kvasnička, R. Corporate Social Responsibility and Social Media: Comparison between Developing and Developed Countries. Sustainability 2020, 12, 5255. [Google Scholar] [CrossRef]

- SGD Compass. Available online: https://sdgcompass.org/ (accessed on 28 April 2021).

- European Foundation for Quality Management (EFQM). Available online: http://www.efqm.es/ (accessed on 28 April 2021).

- Morsing, M.; Schultz, M. Corporate social responsibility communication: Stakeholder information, response and involvement strategies. Bus. Ethics A Eur. Rev. 2006, 15, 323–338. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| GRI 100: Universal Standards | |

| GRI 101: Foundation | |

| GRI 102: General Disclosures | |

| GRI 103: Management Approach | |

| GRI 200: Economic | GRI 300: Environmental |

| GRI 201: Economic Performance GRI 202: Market Presence GRI 203: Indirect Economic Impacts GRI 204: Procurement Practices GRI 205: Anti-corruption GRI 206: Anti-competitive Behavior GRI 207: Tax | GRI 301: Materials GRI 302: Energy GRI 303: Water and Effluents GRI 304: Biodiversity GRI 305: Emissions GRI 306: Waste GRI 307: Environmental Compliance GRI 308: Supplier Environmental Assessment |

| GRI 400: Social | |

| GRI 401: Employment GRI 402: Labor/Management Relations GRI 403: Occupational Health and Safety GRI 404: Training and Education GRI 405: Diversity and Equal Opportunity GRI 406: Non-discrimination GRI 407: Freedom of Association and Collective Bargaining GRI 408: Child Labor GRI 409: Forced or Compulsory Labor GRI 410: Security Practices GRI 411: Rights of Indigenous Peoples GRI 412: Human Rights Assessment GRI 413: Local Communities GRI 414: Supplier Social Assessment GRI 415: Public Policy GRI 416: Customer Health and Safety GRI 417: Marketing and Labeling GRI 418: Customer Privacy GRI 419: Socioeconomic Compliance | |

| CSR Observatory https://observatoriorsc.org/ (accessed on 6 September 2020). | 2004 |

| White Paper on CSR in Spain http://www.congreso.es/public_oficiales/L8/CONG/BOCG/D/D_423.PDF (accessed on 6 September 2020). | 2006 |

| Royal Decree that creates and regulates the National Council of CSR (CERSE) (2008) https://www.boe.es/buscar/pdf/2008/BOE-A-2008-3868-consolidado.pdf (accessed on 6 September 2020). | 2008 |

| Spanish CSR strategy. Ministry of Employment and Social Security (2014–2020) http://www.mitramiss.gob.es/es/rse/eerse/index.htm (accessed on 6 September 2020). | 2014 |

| Action Plan for implementing the 2030 AGENDA (High Commissioner for the 2030 Agenda. Presidency of the Government of Spain) http://www.exteriores.gob.es/Portal/es/SalaDePrensa/Multimedia/Publicaciones/Documents/PLAN%20DE%20ACCION%20PARA%20LA%20IMPLEMENTACION%20DE%20LA%20AGENDA%202030.pdf (accessed on 6 September 2020). | 2018 |

| Law 11/2018, of 28 December, amending the Commercial Code, the revised text of Capital Companies Law approved by Royal Legislative Decree 1/2010, of 2 July, and Law 22/2015, of 20 July, on Account Auditing, on Non-Financial Information and Diversity. https://www.boe.es/boe/dias/2018/12/29/pdfs/BOE-A-2018-17989.pdf (accessed on 6 September 2020). | 2018 |

| Cooperative | Locality | Province | Website |

|---|---|---|---|

| CEA | Alginet | Valencia | http://www.electricadealginet.com (accessed on 9 September 2020). |

| CEC | Callosa del Segura | Alicante | http://electricadecallosa.es/publica/ (accessed on 9 September 2020). |

| COOPELEC | Guadassuar | Valencia | https://www.electricaguadassuar.es/ (accessed on 9 September 2020). |

| COOPERATIVA ELECTRICA DE CASTELLAR | Valencia | Valencia | https://coopcastellar.com/ (accessed on 9 September 2020). |

| E + P | Pamplona | Navarra | http://www.emasp.org (accessed on 9 September 2020). |

| ECONACTIVA | Guadalajara | Guadalajara | http://www.econactiva.es (accessed on 9 September 2020). |

| EDFA SERRALLO | Grao de Castellón | Castellón | https://www.economiasolidaria.org/entidades/cooperativa-electrica-edfa-serrallo (accessed on 9 September 2020). |

| EFIDUERO | Trabanca | Salamanca | http://www.efiduero.com (accessed on 9 September 2020). |

| ELÉCTRICA ALBATERENSE | Albatera | Alicante | http://coopealbaterense.es/ (accessed on 10 September 2020). |

| ELECTRICA ALGIMIA DE ALFARA | Algimia Alfara | Valencia | https://www.electricaalgimia.com/(accessed on 10 September 2020). |

| ELECTRICA CATRALENSE | Catral | Alicante | http://www.cooperativaelectricacatral.es (accessed on 10 September 2020). |

| ELECTRICA DE CHERA | Chera | Valencia | https://electricadechera.wordpress.com/ (accessed on 10 September 2020). |

| ELÉCTRICA DE MELIANA | Meliana | Valencia | http://www.electricademeliana.com (accessed on 10 September 2020). |

| ELÉCTRICA DE VINALESA | Vinalesa | Valencia | http://www.coop-vinalesa.com/(accessed on 10 September 2020). |

| ELÉCTRICA DEL POZO | Madrid | Madrid | http://www.electricadelpozo.es (accessed on 10 September 2020). |

| ENERBI | Biar | Alicante | http://www.coopelectricabiar.com (accessed on 10 September 2020). |

| ENERCOOP | Crevillente | Alicante | http://www.enercoop.es (accessed on 11 September 2020). |

| ENERGÍA CASABLANCA | Almenara | Castellón | https://www.casablanca.cl/(accessed on 11 September 2020). |

| ENERKORE | Durando | Bizkaia | http://www.enerkore.es (accessed on 11 September 2020). |

| GOIENER | Ordizia | Guipúzcoa | http://www.goiener.com (accessed on 11 September 2020). |

| HELIA COOP V | Engera | Valencia | http://www.helialuz.es (accessed on 11 September 2020). |

| LA CORRIENTE | Madrid | Madrid | http://https://lacorrientecoop.es/ (accessed on 11 September 2020). |

| MEGARA ENERGÍA | Soria | Soria | htpp://www.megaraenergia.com (accessed on 11 September 2020). |

| MUSEROS FLUIDO ELECTRICO | Museros | Valencia | http://www.muserosfluidoelectrico.com/(accessed on 11 September 2020). |

| SOLABRIA RENOVABLES | Santander | Cantabria | http://www.solabria.es (accessed on 12 September 2020). |

| SOM ENERGÍA | Girona | Girona | http://www.somenergia.coop (accessed on 12 September 2020) |

| SOT DE CHERA | Sot de Chera | Valencia | http://www.sotdechera.es/es/content/cooperativa-electrica-sot-chera (accessed on 12 September 2020) |

| SUCA ENERGÍA | El Ejido | Almeria | http://energia.gruposuca.com/ (accessed on 12 September 2020) |

| SDG 7 of the 2030 Agenda | GRI Indicators | Description |

|---|---|---|---|

| 7.1. Ensure universal access | EU-23 | Programs to improve access to electricity and customer support service. | |

| EU-26 | Percentage of population unserved in licensed distribution or service area. | ||

| EU-28 | Power outage frequency. | ||

| EU29 | Average power outage duration. | ||

| 7.2. Increase substantially the share of renewable energy in the global energy mix | EU-10 | Installed power from renewable sources. | |

| EU-30 | Energy produced from renewable sources. | ||

| 302-1 | Type of domestic energy consumption. | ||

| 7.3. Double the global rate of improvement in energy efficiency | 302-4 | Reducing energy consumption. | |

| 302-5 | Reductions in energy requirements for products and services. | ||

| EU-30 | Average plant availability factor by energy source and regulatory regime. | ||

| 7.4. Enhance international cooperation to facilitate access to clean energy research and technology, including renewable energy, energy efficiency, and advanced and cleaner fossil-fuel technology, and promote investment in energy infrastructure and clean energy technology | EU-8 | R&D costs to provide reliable and sustainable electricity. | |

| SDG 13 of the 2030 Agenda | GRI Indicators | Description |

|---|---|---|---|

| 13.1 Implement the commitment undertaken by developed-country parties to the UN Framework Convention on Climate Change. | 302-1 | Proportion of energy consumed from renewable energy. | |

| 302-4 | Reduction in energy consumption. | ||

| 13.2. Strengthen resilience and adaptive capacity to climate-related hazards and natural disasters in all countries. | 302-5 | Savings on green products and services. | |

| 305-1 | Direct greenhouse gas emissions. | ||

| EU-30 | Average plant availability factor by energy source and regulatory regime. | ||

| 201-2 | Financial implications and other risks and opportunities for the organization’s activities due to climate change. | ||

| 13.3 Improve education, awareness-raising, and human and institutional capacity on climate change mitigation, adaptation, impact reduction, and early warning. | 404-4 | Training and education. Climate change and renewable energy awareness-raising activities. | |

| General Objectives | Specific Objectives | |

|---|---|---|

| Section 1. Corporate governance | O.1. Evaluate corporate governance | O.1.1. Evaluate the cooperatives’ commitment to CSR culture and management. |

| Section 2. Policies and strategies | O.1.2. Identify and evaluate the use of CSR and PR management policies, procedures, and standards. | |

| Section 3. Stakeholders engagement | O.2. Evaluate strategic CSR management | O.2.1. Evaluate the level of CSR development with stakeholders (consubstantial, contextual, and contractual levels). |

| Section 4. Processes | O.2.2. Evaluate the inclusion of stakeholder expectations in the definition of key processes. | |

| Section 5. Commitments and partnerships | O.3. Measure degree of knowledge and contribution to targets of SDG 7 and SDG 13 | O.3.1. Identify the commitment and partnerships with stakeholders arising from CSR policies in the five phases of the value curve. |

| O.3.2. Identify the links between CSR policy development and SDG 7 and SDG 13. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Campillo-Alhama, C.; Igual-Antón, D. Corporate Social Responsibility Strategies in Spanish Electric Cooperatives. Analysis of Stakeholder Engagement. Sustainability 2021, 13, 6810. https://doi.org/10.3390/su13126810

Campillo-Alhama C, Igual-Antón D. Corporate Social Responsibility Strategies in Spanish Electric Cooperatives. Analysis of Stakeholder Engagement. Sustainability. 2021; 13(12):6810. https://doi.org/10.3390/su13126810

Chicago/Turabian StyleCampillo-Alhama, Concepción, and Diego Igual-Antón. 2021. "Corporate Social Responsibility Strategies in Spanish Electric Cooperatives. Analysis of Stakeholder Engagement" Sustainability 13, no. 12: 6810. https://doi.org/10.3390/su13126810

APA StyleCampillo-Alhama, C., & Igual-Antón, D. (2021). Corporate Social Responsibility Strategies in Spanish Electric Cooperatives. Analysis of Stakeholder Engagement. Sustainability, 13(12), 6810. https://doi.org/10.3390/su13126810