The Influence of the CEO on Auditor Choice in Private Firms: An Interplay of Willingness and Ability

Abstract

1. Introduction

2. Theory and Hypotheses

2.1. Auditor Choice and Agency Conflicts

2.2. Willingness of Management to Influence Auditor Choice

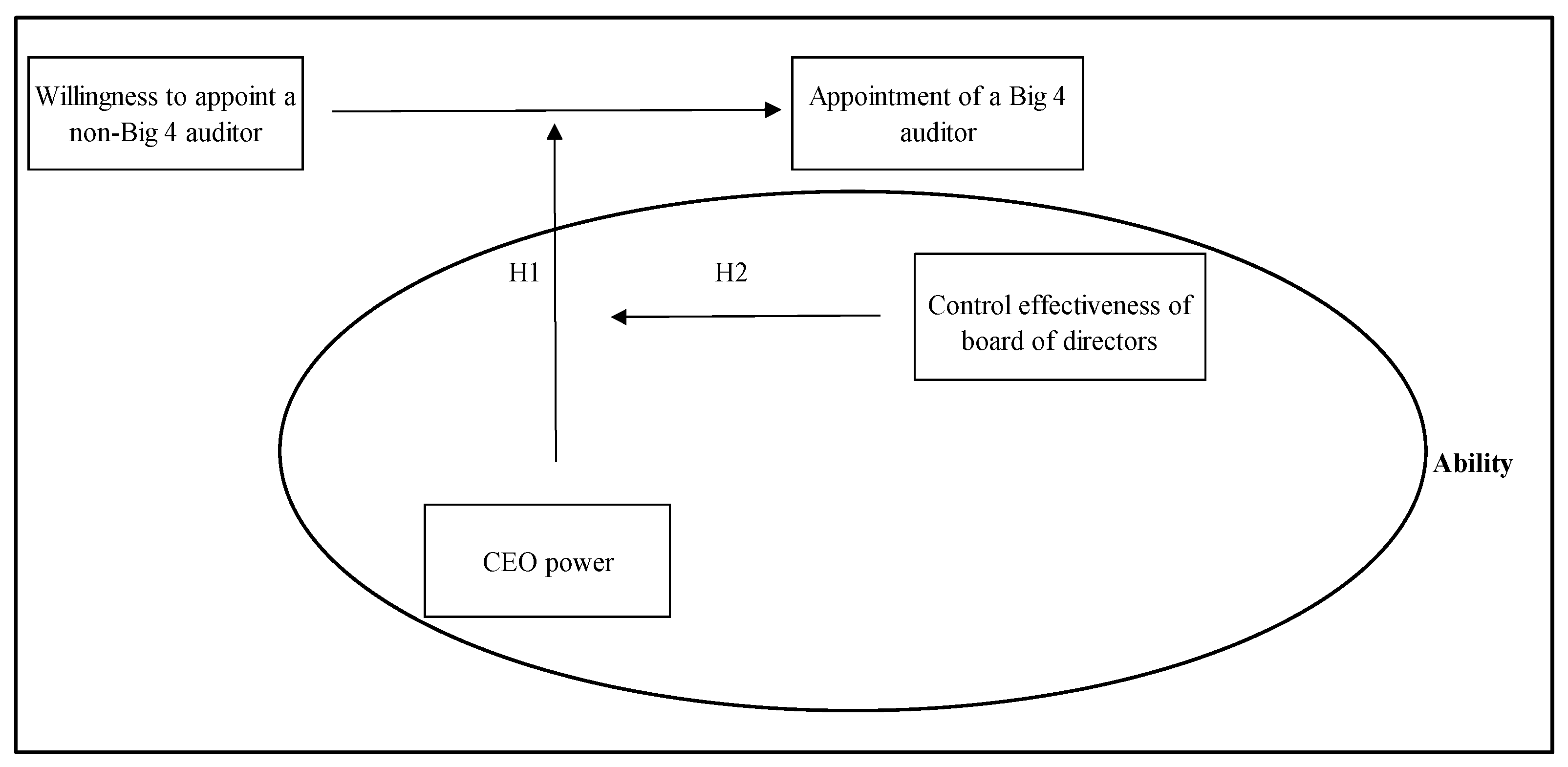

2.3. Management Influence: A Combination of Willingness and Ability

2.3.1. Ability: Managerial Power

2.3.2. Ability: A Combination of CEO Power and the Board of Directors

3. Data and Methodology

3.1. Sample

3.2. Variables

3.2.1. Dependent Variable

3.2.2. Explanatory Variables

3.2.3. Control Variables

3.2.4. Model

4. Results

4.1. Descriptive Statistics and Correlations

4.2. Regression Results

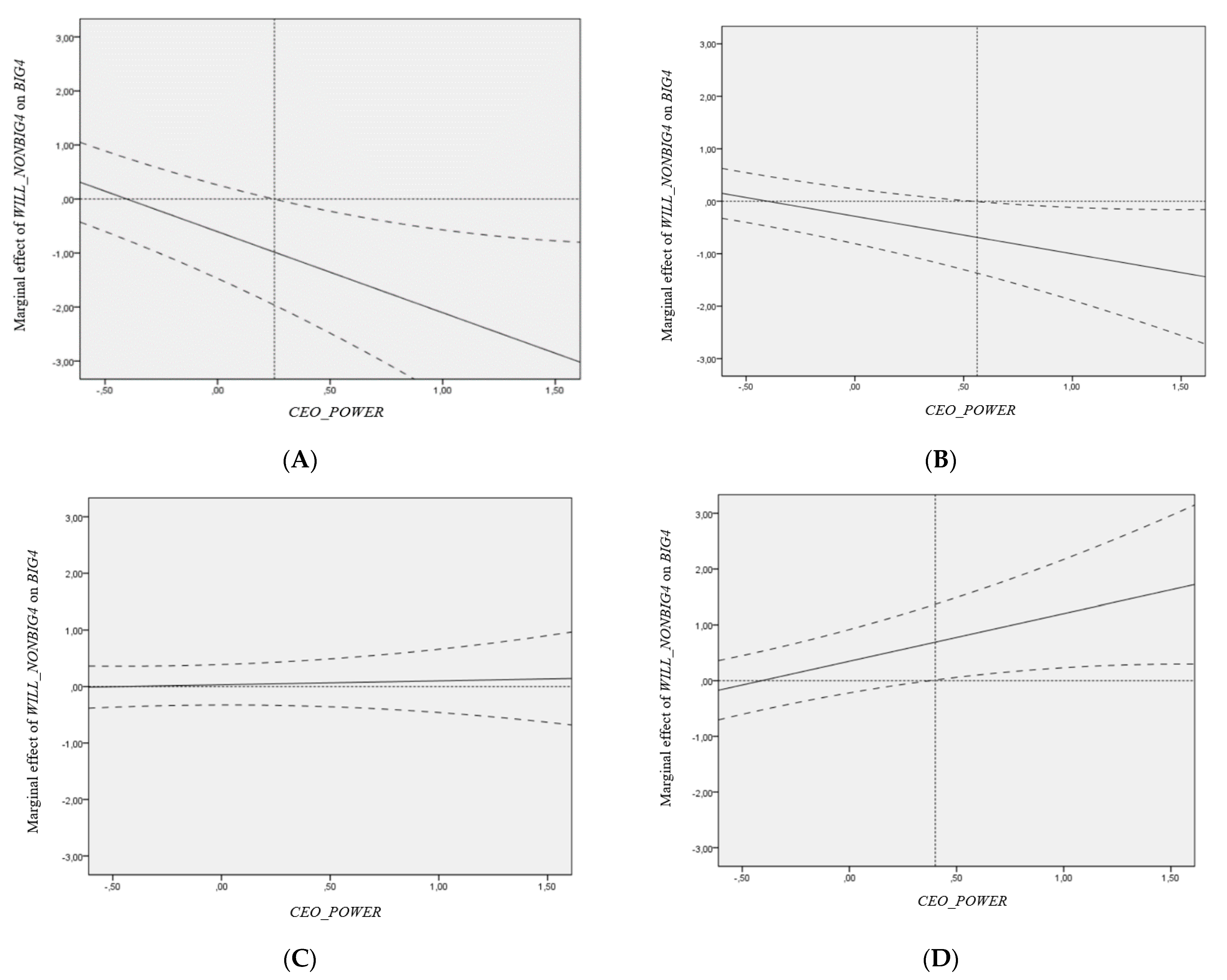

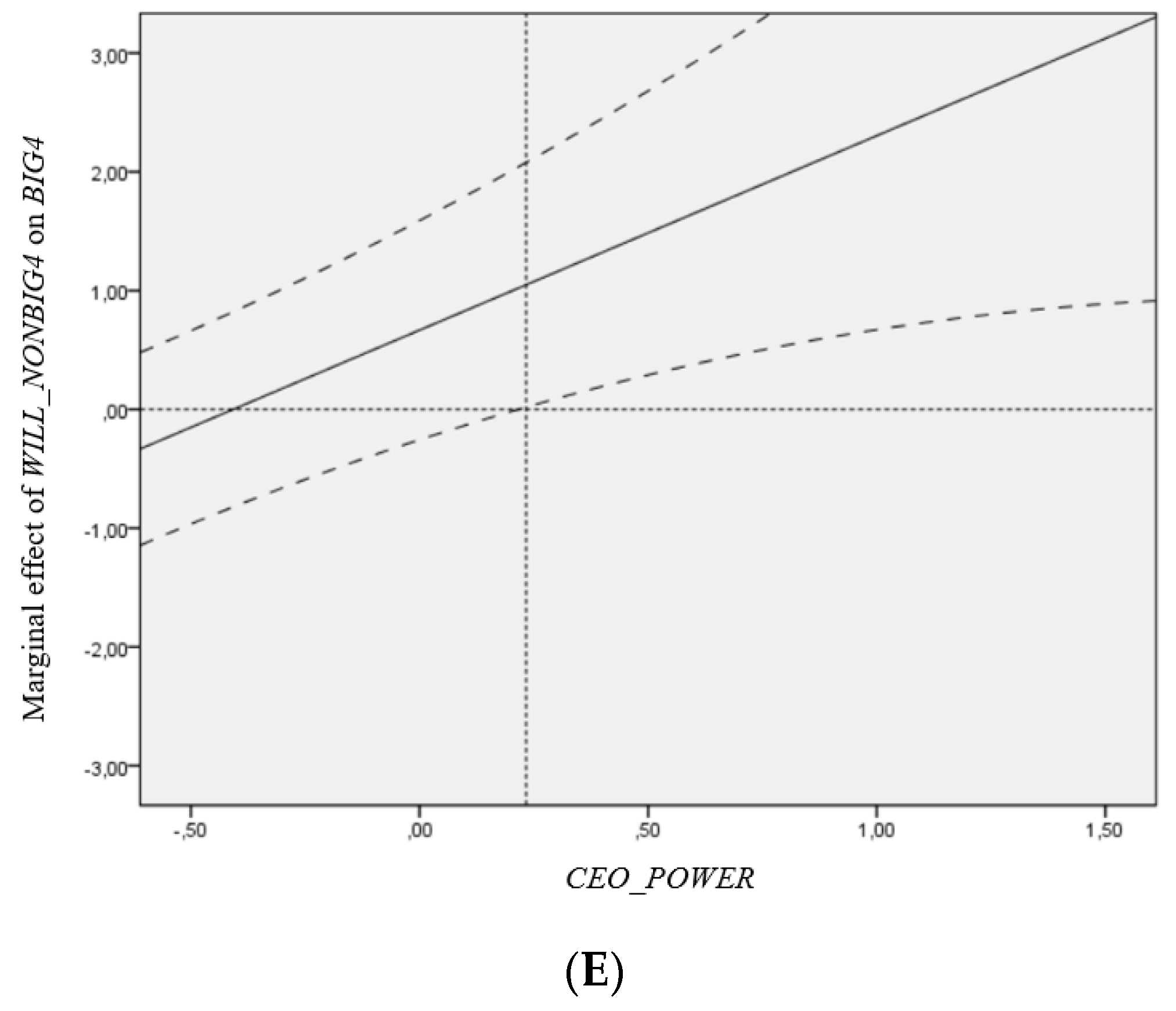

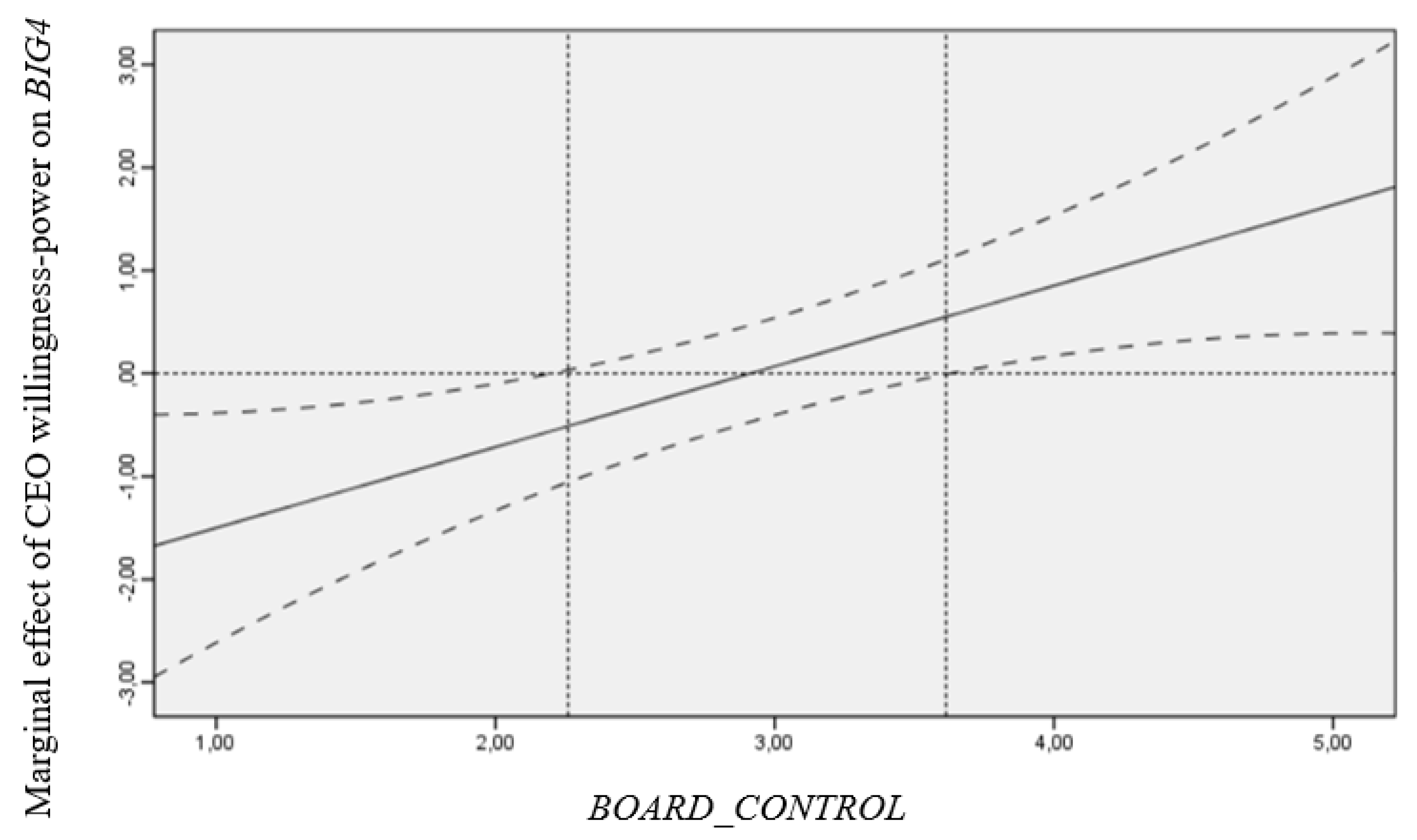

4.3. Graphical Interpretation

4.4. Robustness Analyses

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

- An external audit increases the quality of the financial statements of our company. (R)

- An external audit has a positive influence on the financial performance of our company. (R)

- An external audit strengthens the corporate governance of our company. (R)

- An external audit provides us with useful advice. (R)

- An external audit improves the efficiency and reliability of our business processes/internal control. (R)

- I consider an external audit as a waste of time.

- An external audit reassures me about the financial reporting of our results. (R)

- An external audit provides no added value to an external accountant.

- An external audit increases my personal credibility towards the board of directors and the shareholders. (R)

- The board is actively involved in monitoring that all internal behaviors are adequately controlled

- The board is actively involved in defining behavioral guidelines for divisional and functional managers

- The board is actively involved in supervising the CEO

- The board controls that the activities are well organized

- The board develops plan and budgets

- The board is kept informed on the financial position of the company

- The board actively monitors and evaluates strategic decisions

References

- Bar-Yosef, S.; D’Augusta, C.; Prencipe, A. Accounting research on private firms: State of the art and future directions. Int. J. Account. 2019, 54, 1950007. [Google Scholar] [CrossRef]

- DeFond, M.L. The Association between changes in client firm agency costs and auditor switching. Audit. J. Pract. Theory 1992, 11, 16–31. [Google Scholar]

- Knechel, W.R.; Niemi, L.; Sundgren, S. Determinants of auditor choice: Evidence from a small client market. Int. J. Audit. 2008, 12, 65–88. [Google Scholar] [CrossRef]

- Niskanen, M.; Karjalainen, J.; Niskanen, J. Demand for audit quality in private firms: Evidence on ownership effects. Int. J. Audit. 2011, 15, 43–65. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- DeAngelo, L.E. Auditor size and audit quality. J. Account. Econ. 1981, 3, 183–199. [Google Scholar] [CrossRef]

- Cohen, J.; Krishnamoorthy, G.; Wright, A. Corporate governance in the post-sarbanes-oxley era: Auditors’ experiences. Contemp. Account. Res. 2010, 27, 751–786. [Google Scholar] [CrossRef]

- Fleischer, R.; Goettsche, M. Size effects and audit pricing: Evidence from Germany. J. Int. Account. Audit. Tax. 2012, 21, 156–168. [Google Scholar] [CrossRef]

- Karjalainen, J. Audit quality and cost of debt capital for private firms: Evidence from finland. Int. J. Audit. 2011, 15, 88–108. [Google Scholar] [CrossRef]

- Fiegener, M.K.; Brown, B.M.; Dreux, D.R.; Dennis, W.J. The adoption of outside boards by small private US firms. Entrep. Reg. Dev. 2000, 12, 291–309. [Google Scholar] [CrossRef]

- Lennox, C. Management ownership and audit firm size. Contemp. Account. Res. 2005, 22, 205–227. [Google Scholar] [CrossRef]

- Carcello, J.V.; Hermanson, D.R.; Ye, Z. Corporate governance research in accounting and auditing: Insights, practice implications, and future research directions. Audit. J. Pract. Theory 2011, 30, 1–31. [Google Scholar] [CrossRef]

- Cohen, J.; Krishnamoorthy, G.; Wright, A. The corporate governance mosaic and financial reporting quality. J. Account. Lit. 2004, 23, 87–152. [Google Scholar]

- Corten, M.; Steijvers, T.; Lybaert, N. The influence of the CEO’s value perception towards auditing on audit demand in private firms. Account. Financ. 2019, 59, 2307–2343. [Google Scholar] [CrossRef]

- Collis, J.; Jarvis, R.; Skerratt, L. The demand for the audit in small companies in the UK. Account. Bus. Res. (Wolters Kluwer UK) 2004, 34, 87–100. [Google Scholar] [CrossRef]

- Niemi, L.; Kinnunen, J.; Ojala, H.; Troberg, P. Drivers of voluntary audit in Finland: To be or not to be audited? Account. Bus. Res. 2012, 42, 169–196. [Google Scholar] [CrossRef]

- De Massis, A.; Kotlar, J.; Chua, J.H.; Chrisman, J.J. Ability and willingness as sufficiency conditions for family-oriented particularistic behavior: Implications for theory and empirical studies. J. Small Bus. Manag. 2014, 52, 344–364. [Google Scholar] [CrossRef]

- Pathan, S. Strong boards, CEO power and bank risk-taking. J. Bank. Financ. 2009, 33, 1340–1350. [Google Scholar] [CrossRef]

- Finkelstein, S. Power in top management teams: Dimensions, measurement, and validation. Acad. Manag. J. 1992, 35, 505–538. [Google Scholar]

- Zahra, S.A.; Pearce, J.A. Boards of directors and corporate financial performance: A review and integrative model. J. Manag. 1989, 15, 291–334. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–326. [Google Scholar] [CrossRef]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach; The Guilford Press: New York, NY, USA, 2013. [Google Scholar]

- Piot, C.; Janin, R. External auditors, audit committees and earnings management in France. Eur. Account. Rev. 2007, 16, 429–454. [Google Scholar] [CrossRef]

- Becker, C.L.; Defond, M.L.; Jiambalvo, J.; Subramanyam, K.R. The effect of audit quality on earnings management. Contemp. Account. Res. 1998, 15, 1–24. [Google Scholar] [CrossRef]

- Lennox, C.; Pittman, J.A. Big five audits and accounting fraud. Contemp. Account. Res. 2010, 27, 209–247. [Google Scholar] [CrossRef]

- Francis, J.R.; Maydew, E.L.; Sparks, H.C. The role of big 6 auditors in the credible reporting of accruals. Audit. J. Pract. Theory 1999, 18, 17. [Google Scholar] [CrossRef]

- Gul, F.A. Audit prices, product differentiation and economic equilibrium. Audit. J. Pract. Theory 1999, 18, 90–100. [Google Scholar] [CrossRef]

- Hope, O.-K.; Langli, J.C.; Thomas, W.B. Agency conflicts and auditing in private firms. Account. Organ. Soc. 2012, 37, 500–517. [Google Scholar] [CrossRef]

- Dedman, E.; Kausar, A.; Lennox, C. The demand for audit in private firms: Recent large-sample evidence from the UK. Eur. Account. Rev. 2014, 23, 1–23. [Google Scholar] [CrossRef]

- Gibbins, M.; Salterio, S.; Webb, A. Evidence about auditor-client management negotiation concerning client’s financial reporting. J. Account. Res. 2001, 39, 535–563. [Google Scholar] [CrossRef]

- Daily, C.M.; Johnson, J.L. Sources of CEO power and firm financial performance: A longitudinal assessment. J. Manag. 1997, 23, 97. [Google Scholar] [CrossRef]

- Francis, J.; Huang, A.H.; Rajgopal, S.; Zang, A.Y. CEO reputation and earnings quality. Contemp. Account. Res. 2008, 25, 109–147. [Google Scholar] [CrossRef]

- Lennox, C. Audit quality and executive officers’ affiliations with CPA firms. J. Account. Econ. 2005, 39, 201–231. [Google Scholar] [CrossRef]

- Cohen, J.; Krisnamoorthy, G.; Wright, A.M. Corporate governance and the audit process. Contemp. Account. Res. 2002, 19, 573–594. [Google Scholar] [CrossRef]

- Ali, C.B.; Teulon, F. CEO monitoring and board effectiveness: Resolving the CEO compensation issue. Manag. Int. 2017, 21, 123. [Google Scholar]

- Van den Heuvel, J.; Van Gils, A.; Voordeckers, W. Board roles in small and medium-sized family businesses: Performance and importance. Corp. Gov. Int. Rev. 2006, 14, 467–485. [Google Scholar] [CrossRef]

- Francis, J.R. What do we know about audit quality? Br. Account. Rev. 2004, 36, 345–368. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis, 6th ed.; Pearson Education: Upper Saddle River, NJ, USA, 2006. [Google Scholar]

- Lewellyn, K.B.; Muller-Kahle, M.I. CEO power and risk taking: Evidence from the subprime lending industry. Corp. Gov. Int. Rev. 2012, 20, 289–307. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R. Financial performance of founder-managed versus professionally managed small corporations. J. Small Bus. Manag. 1992, 30, 25–34. [Google Scholar]

- Beasley, M.S.; Petroni, K.R. Board independence and audit-firm type. Audit. J. Pract. Theory 2001, 20, 97. [Google Scholar] [CrossRef]

- Ireland, J.C.; Lennox, C.S. The large audit firm fee premium: A case of selectivity bias? J. Account. Audit. Financ. 2002, 17, 73–91. [Google Scholar] [CrossRef]

- Minichilli, A.; Zattoni, A.; Zona, F. Making boards effective: An empirical examination of board task performance. Br. J. Manag. 2009, 20, 55–74. [Google Scholar] [CrossRef]

- Finkelstein, S.; Mooney, A.C. Not the usual suspects: How to use board process to make boards better. Acad. Manag. Exec. 2003, 17, 101–113. [Google Scholar] [CrossRef]

- Gabrielsson, J.; Winlund, H. Boards of directors in small and medium-sized industrial firms: Examining the effects of the board’s working style on board task performance. Entrep. Reg. Dev. 2000, 12, 311–330. [Google Scholar] [CrossRef]

- Minichilli, A.; Zattoni, A.; Nielsen, S.; Huse, M. Board task performance: An exploration of micro- and macro-level determinants of board effectiveness. J. Organ. Behav. 2012, 33, 193–215. [Google Scholar] [CrossRef]

- O’Sullivan, N. The impact of board composition and ownership on audit quality: Evidence from large UK companies. Br. Account. Rev. 2000, 32, 397–414. [Google Scholar] [CrossRef]

- Reed, B.J.; Trombley, M.A.; Dhaliwal, D.S. Demand for audit quality: The case of laventhol and horwath’s auditees. J. Account. Audit. Financ. 2000, 15, 183–198. [Google Scholar] [CrossRef]

- Niskanen, M.; Karjalainen, J.; Niskanen, J. The role of auditing in small, private family firms: Is it about quality and credibility? Fam. Bus. Rev. 2010, 23, 230–245. [Google Scholar] [CrossRef]

- Hay, D.C.; Knechel, W.R.; Wong, N. Audit fees: A meta-analysis of the effect of supply and demand attributes. Contemp. Account. Res. 2006, 23, 141–191. [Google Scholar] [CrossRef]

- Park, J.-H.; Kim, C.; Chang, Y.K.; Lee, D.-H.; Sung, Y.-D. CEO hubris and firm performance: Exploring the moderating roles of CEO power and board vigilance. J. Bus. Ethics 2018, 147, 919–933. [Google Scholar] [CrossRef]

- Finkelstein, S.; D’Aveni, R.A. Ceo duality as a double-edged sword: How boards of directors balance entrenchment avoidance and unity of command. Acad. Manag. J. 1994, 37, 1079–1108. [Google Scholar]

- Westphal, J.D. Collaboration in the boardroom: Behavioral and performance consequences of CEO-boards social ties. Acad. Manag. J. 1999, 42, 7–24. [Google Scholar]

- Craswell, A.T.; Francis, J.R.; Taylor, S.L. Auditor brand name reputations and industry specializations. J. Account. Econ. 1995, 20, 297–322. [Google Scholar] [CrossRef]

- Francis, J.R.; Yu, M.D. Big 4 office size and audit quality. Account. Rev. 2009, 84, 1521–1552. [Google Scholar] [CrossRef]

- Boone, J.P.; Khurana, I.K.; Raman, K.K. Do the big 4 and the Second-tier firms provide audits of similar quality? J. Account. Public Policy 2010, 29, 330–352. [Google Scholar] [CrossRef]

- Francis, J.R.; Khurana, I.K.; Martin, X.; Pereira, R. The relative importance of firm incentives versus country factors in the demand for assurance services by private entities. Contemp. Account. Res. 2011, 28, 487–516. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dependent variable | |

| BIG4 | A dummy variable coded 1 if the firm appointed a Big Four auditor and 0 if it appointed a non-Big Four auditor |

| Explanatory variables | |

| WILL_NONBIG4 | The average score on the perceived value of external auditing. This has been measured negatively: the higher the score, the more negative the perception (i.e., the higher the willingness to appoint a non-Big Four auditor) |

| CEO_POWER | A variable including two standardized items: whether the CEO is the founder and his/her shareholdings |

| BOARD_CONTROL | The average score on the board control tasks, where a higher score means a stronger control role of the board of directors |

| Control variables | |

| DISPERSION | The natural logarithm of one plus the number of shareholders |

| LEVERAGE | The ratio of total debt to total assets |

| SIZE | The natural logarithm of total assets |

| ROA | The ratio of annual net income to total assets indicated as a percentage |

| SUBSIDIARY | A dummy variable coded 1 if the firm is part of a group as a subsidiary |

| PRODUCTION | A dummy variable that controls for industry |

| CONSTRUCTION | A dummy variable that controls for industry |

| TRADE | A dummy variable that controls for industry |

| SERVICES | A dummy variable that controls for industry |

| Continuous Variables | Min. | Max. | Mean | s.d. |

|---|---|---|---|---|

| WILL_NONBIG4 | 1 | 5 | 2.66 | 0.95 |

| CEO_POWER | −0.60 | 2.22 | 0.05 | 0.85 |

| BOARD_CONTROL | 1 | 5 | 2.86 | 0.98 |

| DISPERSION | 0.69 | 3.47 | 1.27 | 0.52 |

| LEVERAGE | 0 | 0.99 | 0.63 | 0.22 |

| SIZE | 6.92 | 14.44 | 9.50 | 1.09 |

| ROA | −68.37 | 58.08 | 6.41 | 10.38 |

| Dichotomous Variables | Sum | Proportion | ||

| BIG4 | 103 | 0.33 | ||

| SUBSIDIARY | 147 | 0.47 | ||

| PRODUCTION | 106 | 0.34 | ||

| CONSTRUCTION | 40 | 0.12 | ||

| TRADE | 107 | 0.34 | ||

| SERVICES | 63 | 0.20 |

| BIG4 | WILL_ NONBIG4 | CEO_ POWER | BOARD_ CONTROL | DISPERSION | LEVERAGE | SIZE | ROA | SUBSIDIARY | |

|---|---|---|---|---|---|---|---|---|---|

| BIG4 | 1 | −0.092 | −0.372 ** | 0.024 | −0.218 ** | −0.062 | 0.195 ** | 0.017 | 0.380 ** |

| WILL_NONBIG4 | −0.101 | 1 | 0.097 | −0.129 * | 0.027 | −0.006 | −0.185 ** | −0.110 | −0.075 |

| CEO_POWER | −0.294 ** | 0.094 | 1 | 0.051 | 0.242 ** | 0.021 | −0.267 ** | −0.044 | −0.498 ** |

| BOARD_CONTROL | 0.015 | −0.133 * | 0.050 | 1 | 0.059 | 0.094 | −0.008 | 0.033 | −0.030 |

| DISPERSION | −0.158 ** | −0.015 | 0.060 | 0.013 | 1 | −0.094 | −0.041 | 0.068 | −0.386 ** |

| LEV | −0.058 | −0.042 | 0.035 | 0.116 * | −0.045 | 1 | −0.067 | −0.230 ** | 0.006 |

| SIZE | 0.254 ** | −0.193 ** | −0.224 ** | 0.015 | −0.056 | −0.060 | 1 | 0.013 | 0.057 |

| ROA | −0.002 | −0.048 | −0.038 | 0.068 | 0.050 | −0.039 | −0.094 | 1 | 0.044 |

| SUBSIDIARY | 0.380 ** | −0.093 | −0.370 ** | −0.032 | −0.335 ** | −0.003 | 0.055 | 0.046 | 1 |

| Model | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| Dependent variable: | BIG4 | BIG4 | BIG4 | BIG4 |

| Explanatory variables: | ||||

| WILL_NONBIG4 | −0.0552 (0.1527) | −0.0446 (0.1562) | −0.9087 * (0.5590) | |

| CEO_POWER | −0.4065 (0.5833) | 6.3122 *** (2.0633) | ||

| BOARD_CONTROL | −0.8067 (0.5134) | |||

| Interaction terms: | ||||

| WILL_NONBIG4 × CEO_POWER | −0.0497 (0.2073) | −2.2740 *** (0.8064) | ||

| WILL_NONBIG4 × BOARD_CONTROL | 0.3118 * (0.1818) | |||

| CEO_POWER × BOARD_CONTROL | −2.4209 *** (0.7299) | |||

| WILL_NONBIG4 × CEO_POWER × BOARD_CONTROL | 0.7833 *** (0.2684) | |||

| Control variables: | ||||

| DISPERSION | −0.1280 (0.2390) | −0.1305 (0.2924) | −0.1790 (0.2992) | −0.2465 (0.3088) |

| LEVERAGE | −0.6540 (0.6280) | −0.6639 (0.6293) | −0.6709 (0.6378) | −0.6596 (0.6615) |

| SIZE | 0.5140 *** (0.1280) | 0.5055 *** (0.1301) | 0.4491 *** (0.1327) | 0.4776 *** (0.1386) |

| ROA | 0.0013 (0.0125) | 0.0010 (0.0126) | 0.0007 (0.0126) | 0.0003 (0.0130) |

| SUBSIDIARY | 1.7974 *** (0.3094) | 1.7897 *** (0.3101) | 1.5430 *** (0.3283) | 1.5656 *** (0.3443) |

| PRODUCTION | 0.2106 (0.3732) | 0.2192 (0.3741) | 0.1957 (0.3785) | 0.4072 (0.3967) |

| CONSTRUCTION | −0.4115 (0.5009) | −0.4120 (0.5014) | −0.4358 (0.5148) | −0.3796 (0.5248) |

| TRADE | −0.8799 ** (0.3894) | −0.8649** (0.3916) | −0.9392** (0.3981) | −0.8143 ** (0.4118) |

| Intercept | −5.8302 *** (1.4430) | −5.5950 *** (1.5790) | −4.8958 *** (1.6109) | −3.0897 (2.1741) |

| Chi-square | 78.771 *** | 78.902 *** | 86.381 *** | 99.535 *** |

| Nagelkerke R² | 0.322 | 0.308 | 0.334 | 0.377 |

| Model | 5 | 6 |

|---|---|---|

| Dependent variable: | BIG4 | BIG4 |

| Explanatory variables: | ||

| WILL_NONBIG4 | −0.7027 * (0.4209) | 0.1260 (0.5607) |

| CEO_POWER | 5.5391 *** (1.7007) | 3.9192 * (2.0169) |

| BOARD_CONTROL | −0.6702 (0.4421) | 0.4077 (0.4652) |

| Interaction terms: | ||

| WILL_NONBIG4 × CEO_POWER | −1.7718 *** (0.6250) | −1.7148 ** (0.8069) |

| WILL_NONBIG4 × BOARD_CONTROL | 0.2366 * (0.1374) | −0.0719 (0.1666) |

| CEO_POWER × BOARD_CONTROL | −2.2950 *** (0.6395) | −1.3972 ** (0.6171) |

| WILL_NONBIG4 × CEO_POWER × BOARD_CONTROL | 0.6211 *** (0.1989) | 0.5331 ** (0.2387) |

| Control variables: | ||

| DISPERSION | −0.2409 (0.3307) | −0.1428 (0.3122) |

| LEVERAGE | −0.4589 (0.7143) | −0.9932 (0.6841) |

| SIZE | 0.4667 *** (0.1521) | 0.4901 *** (0.1437) |

| ROA | −0.0009 (0.0135) | 0.0039 (0.0132) |

| SUBSIDIARY | 1.6596 *** (0.3690) | 1.6743 *** (0.3512) |

| PRODUCTION | 0.2605 (0.4200) | 0.3076 (0.3996) |

| CONSTRUCTION | −0.4976 (0.5771) | −0.2876 (0.5360) |

| TRADE | −0.7734 * (0.4435) | −0.9245 ** (0.4255) |

| Intercept | −3.6114 * (2.0548) | −6.5045 *** (2.2710) |

| Chi-square | 103.999 *** | 100.447 *** |

| Nagelkerke R² | 0.422 | 0.388 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Corten, M.; Steijvers, T.; Lybaert, N.; Coeckelbergs, C. The Influence of the CEO on Auditor Choice in Private Firms: An Interplay of Willingness and Ability. Sustainability 2021, 13, 6710. https://doi.org/10.3390/su13126710

Corten M, Steijvers T, Lybaert N, Coeckelbergs C. The Influence of the CEO on Auditor Choice in Private Firms: An Interplay of Willingness and Ability. Sustainability. 2021; 13(12):6710. https://doi.org/10.3390/su13126710

Chicago/Turabian StyleCorten, Maarten, Tensie Steijvers, Nadine Lybaert, and Céline Coeckelbergs. 2021. "The Influence of the CEO on Auditor Choice in Private Firms: An Interplay of Willingness and Ability" Sustainability 13, no. 12: 6710. https://doi.org/10.3390/su13126710

APA StyleCorten, M., Steijvers, T., Lybaert, N., & Coeckelbergs, C. (2021). The Influence of the CEO on Auditor Choice in Private Firms: An Interplay of Willingness and Ability. Sustainability, 13(12), 6710. https://doi.org/10.3390/su13126710