The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

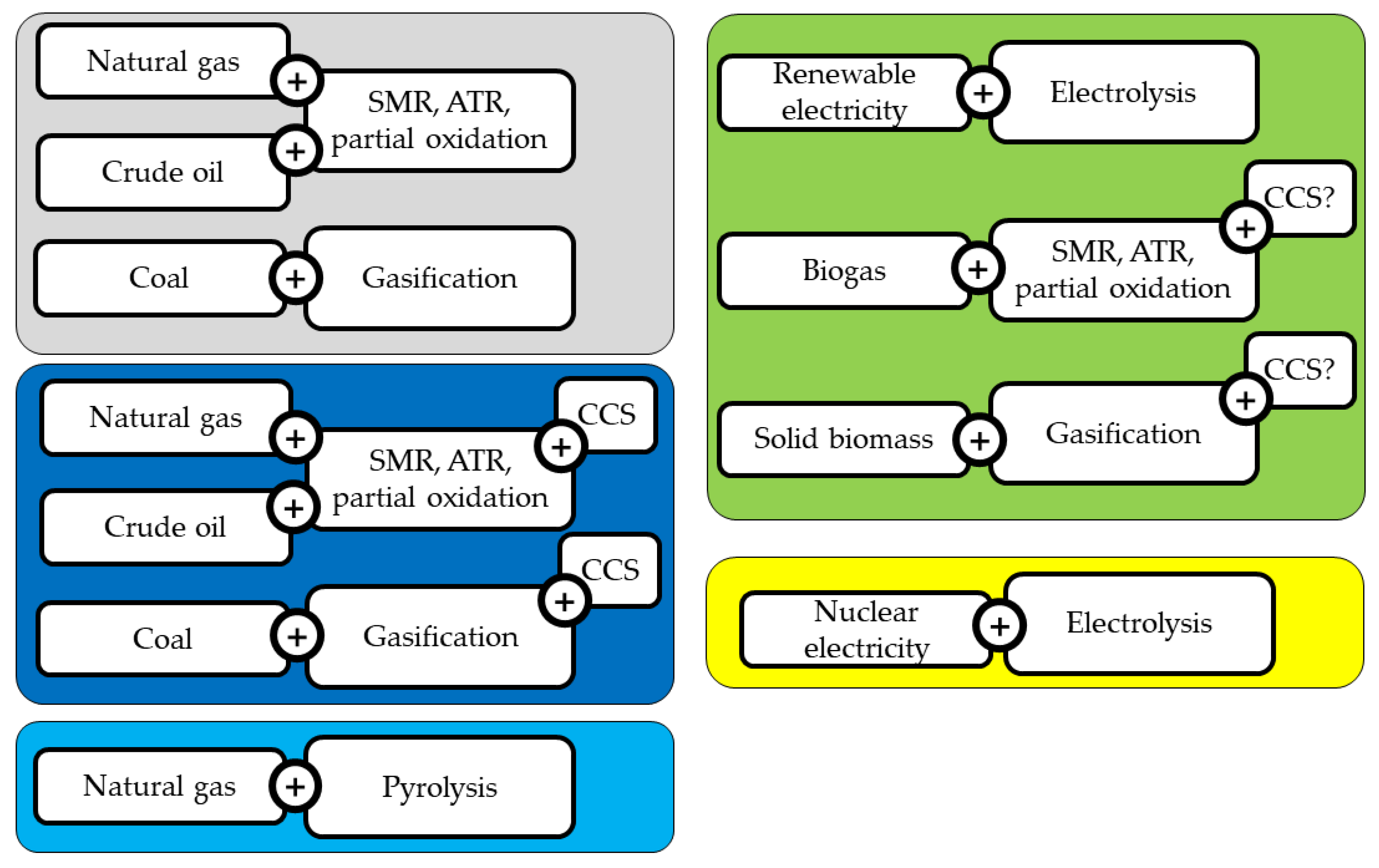

- grey (or brown/black) hydrogen, produced by fossil fuels (mostly natural gas and coal), and causing the emission of carbon dioxide in the process;

- blue hydrogen, through the combination of grey hydrogen and carbon capture and storage (CCS), to avoid most of the GHG emissions of the process;

- turquoise hydrogen, via the pyrolysis of a fossil fuel, where the by-product is solid carbon;

- green hydrogen, when produced by electrolyzers supplied by renewable electricity (and in some cases through other pathways based on bioenergy, such as biomethane reforming or solid biomass gasification);

- yellow (or purple) hydrogen, when produced by electrolyzers supplied by electricity from nuclear power plants.

2. Technological Aspects

2.1. Hydrogen Generation

2.1.1. Green Hydrogen

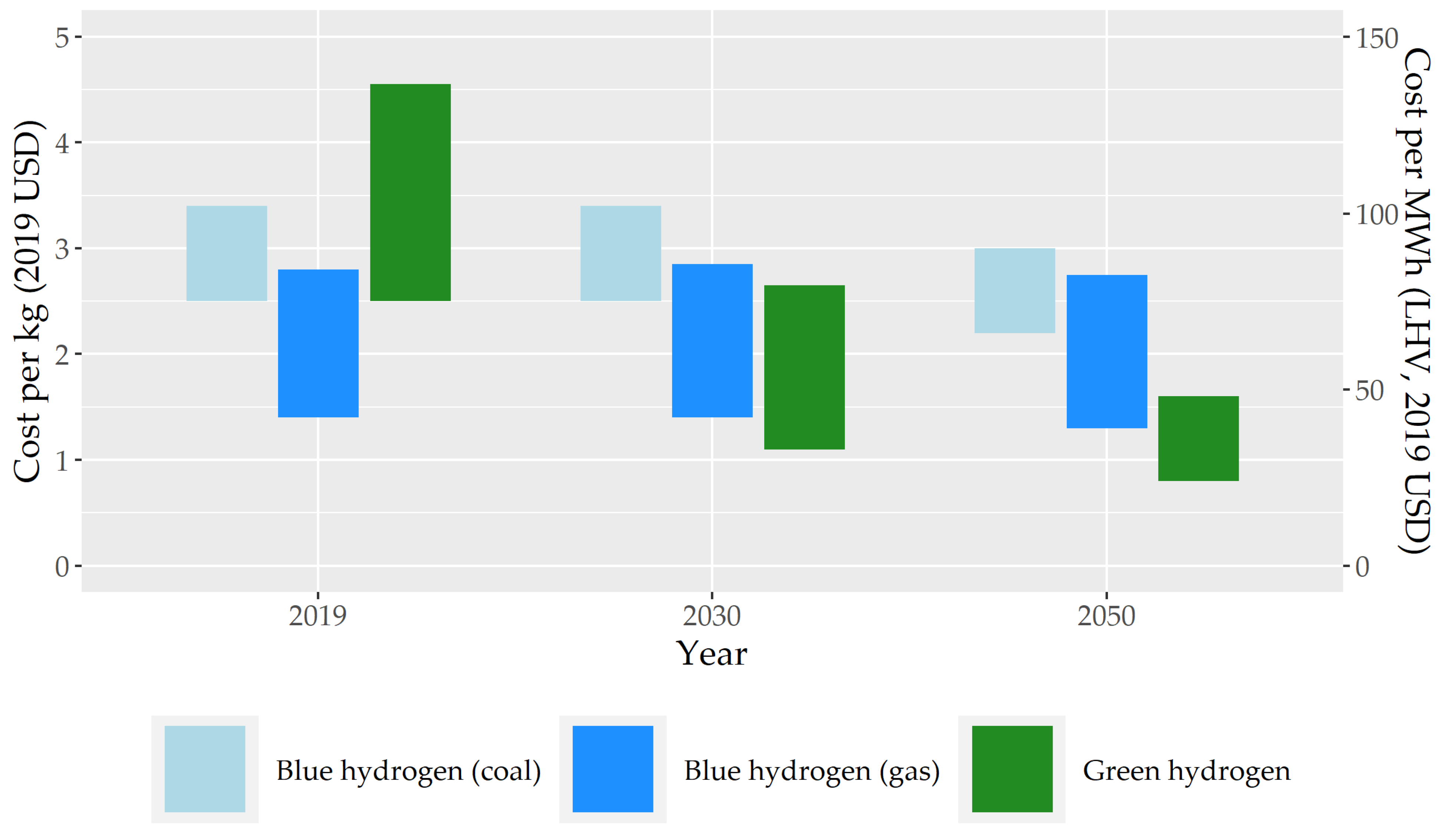

2.1.2. Blue Hydrogen

2.2. Hydrogen Transportation and Storage

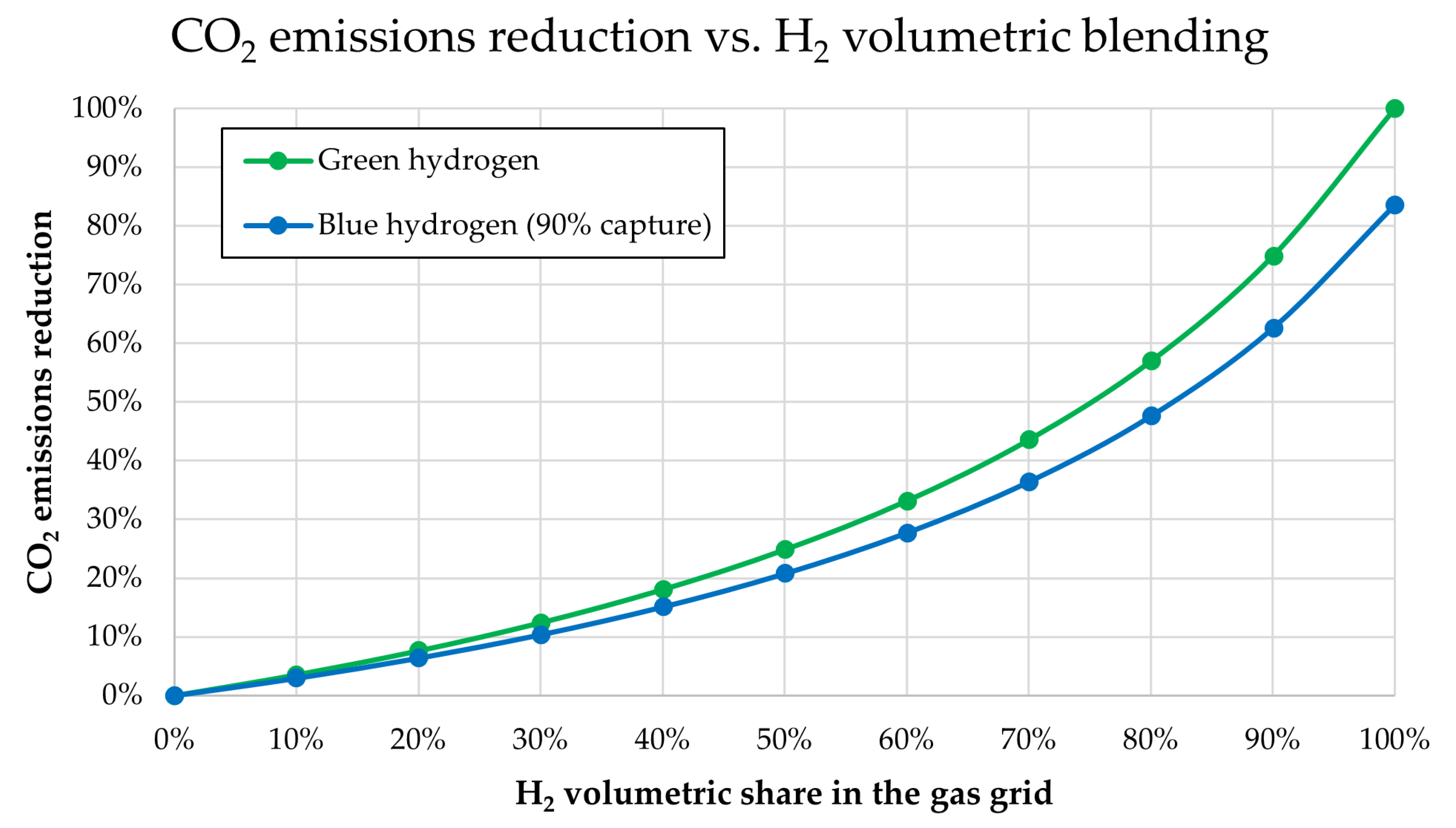

2.2.1. Hydrogen Blending in Natural Gas Grids

2.2.2. Long-Distance Transport

2.2.3. Hydrogen Distribution

2.2.4. Storage

2.3. Hydrogen Demand

2.3.1. Industry

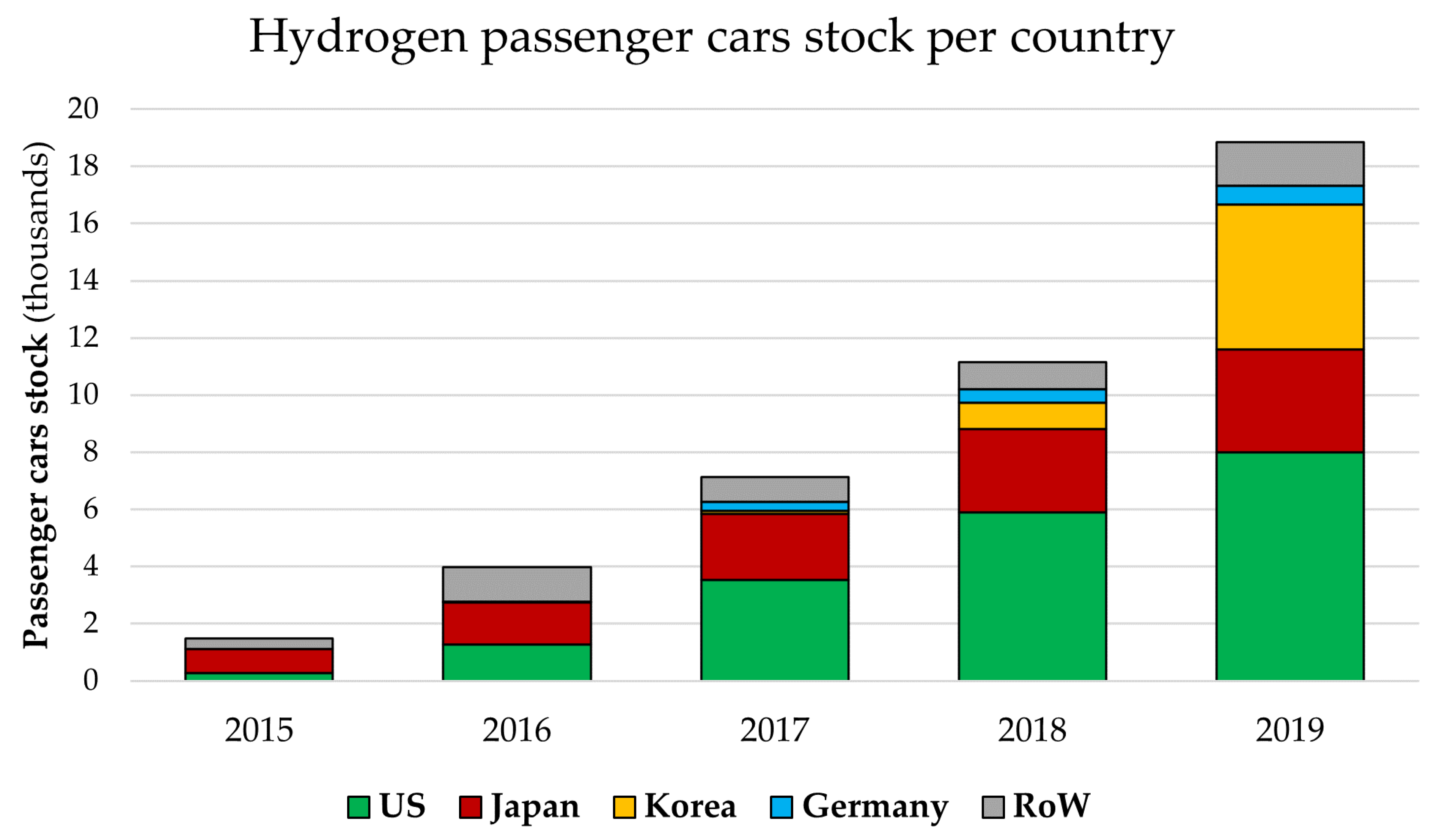

2.3.2. Transport

2.3.3. Buildings

2.3.4. Power Generation

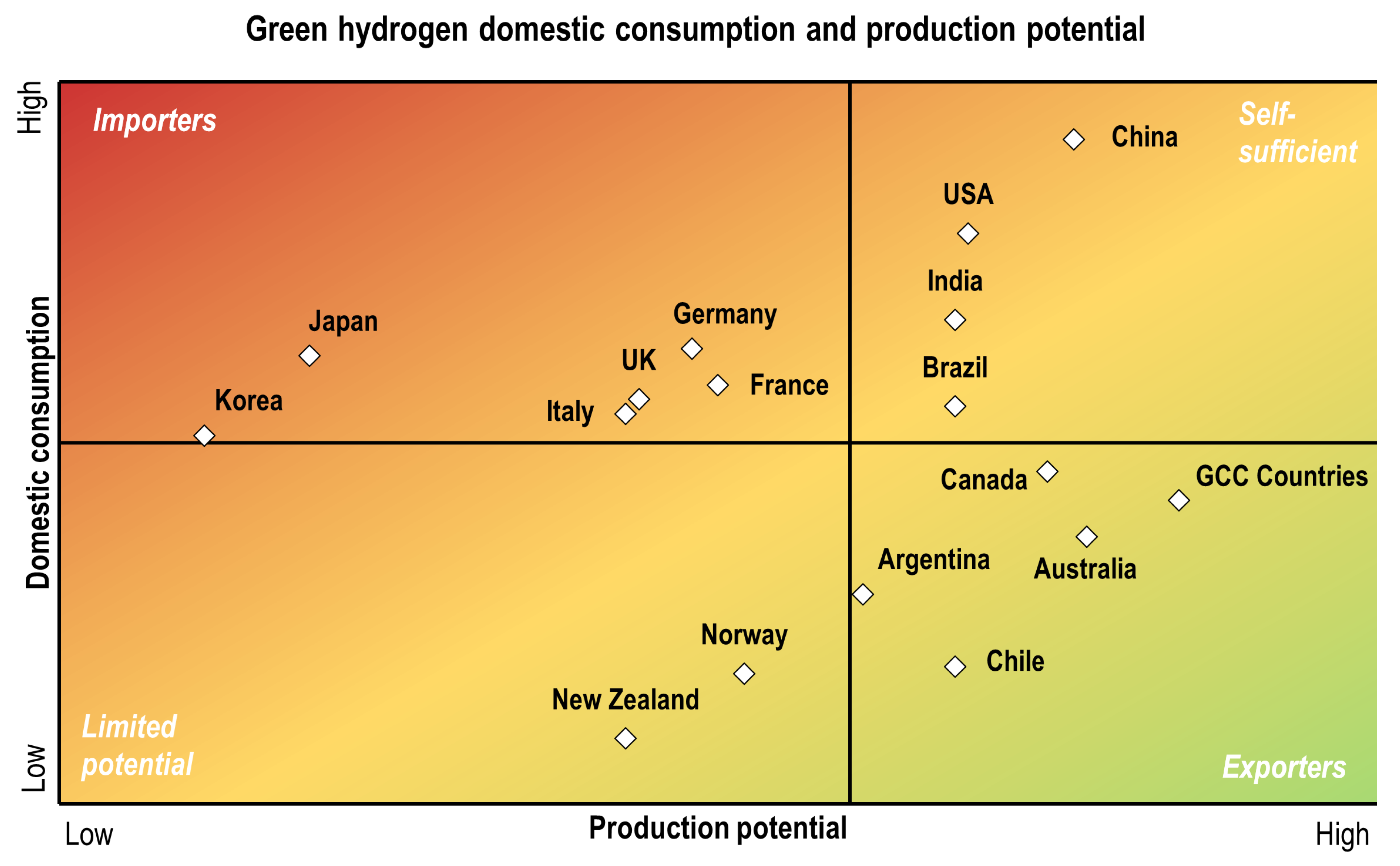

3. Geopolitical Aspects

3.1. National Strategies

3.2. The Role of Private Companies

3.3. International Agreements

4. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| ATR | Autothermal reforming |

| BNEF | Bloomberg New Energy Finance |

| CHP | Combined heat and power |

| DRI | Direct reduction of iron |

| EVs | Electric vehicles |

| GHG | Greenhouse gas |

| IEA | International Energy Agency |

| IRENA | International Renewable Energy Agency |

| LHV | Lower heating value |

| LNG | Liquefied natural gas |

| LOHC | Liquid organic hydrogen carriers |

| PEM | Proton exchange membrane |

| PV | Photovoltaic |

| RES | Renewable energy sources |

| SMR | Steam methane reforming |

| TRL | Technology readiness level |

References

- Chaube, A.; Chapman, A.; Shigetomi, Y.; Huff, K.; Stubbins, J. The Role of Hydrogen in Achieving Long Term Japanese Energy System Goals. Energies 2020, 13, 4539. [Google Scholar] [CrossRef]

- German Federal Government—Federal Ministry for Economic Affairs and Energy. The National Hydrogen Strategy. 2020. Available online: https://www.bmwi.de/Redaktion/EN/Publikationen/Energie/the-national-hydrogen-strategy.pdf (accessed on 18 December 2020).

- Australian Government. Australia’s National Hydrogen Strategy. 2019. Available online: https://www.industry.gov.au/data-and-publications/australias-national-hydrogen-strategy (accessed on 18 December 2020).

- EU Commission. A Hydrogen Strategy for a Climate Neutral Europe. 2020. Available online: https://ec.europa.eu/commission/presscorner/detail/en/FS_20_1296 (accessed on 18 December 2020).

- IEA. The Future of Hydrogen. 2019. Available online: https://www.iea.org/reports/the-future-of-hydrogen (accessed on 10 December 2020).

- Bloomberg. Bloomberg: A Three-Part Series on Hydrogen Energy. 2020. Available online: https://www.bloomberg.com/graphics/2020-opinion-hydrogen-green-energy-revolution-challenges-risks-advantages/oil.html (accessed on 11 December 2020).

- Rifkin, J. The Hydrogen Economy; Tarcher-Putnam: New York, NY, USA, 2002. [Google Scholar]

- IRENA. Hydrogen: A Renewable Energy Perspective. 2019. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Sep/IRENA_Hydrogen_2019.pdf (accessed on 18 December 2020).

- Newborough, M.; Cooley, G. Developments in the global hydrogen market: The spectrum of hydrogen colours. Fuel Cells Bull. 2020, 2020, 16–22. [Google Scholar] [CrossRef]

- Ivanenko, A. A Look At The Colors Of Hydrogen That Could Power Our Future. Forbes. 2020. Available online: https://www.forbes.com/sites/forbestechcouncil/2020/08/31/a-look-at-the-colors-of-hydrogen-that-could-power-our-future/?sh=3edf9d6e5e91 (accessed on 30 December 2020).

- Scita, R.; Raimondi, P.P.; Noussan, M. Green Hydrogen: The Holy Grail of Decarbonisation? An Analysis of the Technical and Geopolitical Impilcations of the Future Hydrogen Economy; FEEM Nota di Lavoro; Fondazione Eni Enrico Mattei: Milano, Italy, 2020; Volume 2020. [Google Scholar]

- Van de Graaf, T.; Overland, I.; Scholten, D.; Westphal, K. The new oil? The geopolitics and international governance of hydrogen. Energy Res. Soc. Sci. 2020, 70, 101667. [Google Scholar] [CrossRef]

- Dickel, R. Blue Hydrogen as an Enabler of Green Hydrogen: The Case of Germany; OIES Paper; The Oxford Institute for Energy Studies: Oxford, UK, 2020. [Google Scholar]

- BloombergNEF. Hydrogen Economy Outlook. 2020. Available online: https://data.bloomberglp.com/professional/sites/24/BNEF-Hydrogen-Economy-Outlook-Key-Messages-30-Mar-2020.pdf (accessed on 18 December 2020).

- El-Emam, R.S.; Ozcan, H.; Zamfirescu, C. Updates on promising thermochemical cycles for clean hydrogen production using nuclear energy. J. Clean. Prod. 2020, 262, 121424. [Google Scholar] [CrossRef]

- Pinsky, R.; Sabharwall, P.; Hartvigsen, J.; O’Brien, J. Comparative review of hydrogen production technologies for nuclear hybrid energy systems. Prog. Nucl. Energy 2020, 123, 103317. [Google Scholar] [CrossRef]

- Ping, Z.; Laijun, W.; Songzhe, C.; Jingming, X. Progress of nuclear hydrogen production through the iodine–sulfur process in China. Renew. Sustain. Energy Rev. 2018, 81, 1802–1812. [Google Scholar] [CrossRef]

- Zhiznin, S.; Timokhov, V.; Gusev, A. Economic aspects of nuclear and hydrogen energy in the world and Russia. Int. J. Hydrog. Energy 2020, 45, 31353–31366. [Google Scholar] [CrossRef]

- Bhandari, R.; Trudewind, C.A.; Zapp, P. Life cycle assessment of hydrogen production via electrolysis—A review. J. Clean. Prod. 2014, 85, 151–163. [Google Scholar] [CrossRef]

- IRENA. Hydrogen from Renewable Power—Technology Outlook for the Energy Transition. 2018. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2018/Sep/IRENA_Hydrogen_from_renewable_power_2018.pdf (accessed on 10 December 2020).

- IEA. Global Electrolysis Capacity Becoming Operational Annually, 2014–2023, Historical And Announced. 2020. Available online: https://www.iea.org/data-and-statistics/charts/global-electrolysis-capacity-becoming-operational-annually-2014-2023-historical-and-announced (accessed on 10 December 2020).

- Thomas, D. Renewable Hydrogen—The Missing Link between the Power, Gas, Industry and Transport Sectors. 2018. Available online: https://hydrogeneurope.eu/sites/default/files/2018-06/2018-06_Hydrogenics_Company%20presentation.compressed.pdf (accessed on 10 December 2020).

- Al-Qahtani, A.; Parkinson, B.; Hellgardt, K.; Shah, N.; Guillen-Gosalbez, G. Uncovering the true cost of hydrogen production routes using life cycle monetisation. Appl. Energy 2021, 281, 115958. [Google Scholar] [CrossRef]

- d’Amore Domenech, R.; Santiago, Ó.; Leo, T.J. Multicriteria analysis of seawater electrolysis technologies for green hydrogen production at sea. Renew. Sustain. Energy Rev. 2020, 133, 110166. [Google Scholar] [CrossRef]

- Cloete, S.; Ruhnau, O.; Hirth, L. On capital utilization in the hydrogen economy: The quest to minimize idle capacity in renewables-rich energy systems. Int. J. Hydrog. Energy 2020, 46, 169–188. [Google Scholar] [CrossRef]

- Rabiee, A.; Keane, A.; Soroudi, A. Technical barriers for harnessing the green hydrogen: A power system perspective. Renew. Energy 2021, 163, 1580–1587. [Google Scholar] [CrossRef]

- Proost, J. Critical assessment of the production scale required for fossil parity of green electrolytic hydrogen. Int. J. Hydrog. Energy 2020, 45, 17067–17075. [Google Scholar] [CrossRef]

- Armijo, J.; Philibert, C. Flexible production of green hydrogen and ammonia from variable solar and wind energy: Case study of Chile and Argentina. Int. J. Hydrog. Energy 2020, 45, 1541–1558. [Google Scholar] [CrossRef]

- The Royal Society. Options foR Producing Low-Carbon Hydrogen at Scale. 2018. Available online: https://royalsociety.org/~/media/policy/projects/hydrogen-production/energy-briefing-green-hydrogen.pdf (accessed on 10 December 2020).

- CertifHy. CertifHy-SD Hydrogen Criteria. 2019. Available online: https://www.certifhy.eu/images/media/files/CertifHy_2_deliverables/CertifHy_H2-criteria-definition_V1-1_2019-03-13_clean_endorsed.pdf (accessed on 18 December 2020).

- Philibert, C. Methane Splitting and Turquoise Ammonia. 2020. Available online: https://www.ammoniaenergy.org/articles/methane-splitting-and-turquoise-ammonia/ (accessed on 10 December 2020).

- Fuel Cells Bulletin. German, French TSOs in MOU on transport, blending of hydrogen in natural gas networks. Fuel Cells Bull. 2020, 2020, 10. [Google Scholar] [CrossRef]

- Pellegrini, M.; Guzzini, A.; Saccani, C. A Preliminary Assessment of the Potential of Low Percentage Green Hydrogen Blending in the Italian Natural Gas Network. Energies 2020, 13, 5570. [Google Scholar] [CrossRef]

- Ekhtiari, A.; Flynn, D.; Syron, E. Investigation of the Multi-Point Injection of Green Hydrogen from Curtailed Renewable Power into a Gas Network. Energies 2020, 13, 6047. [Google Scholar] [CrossRef]

- Cerniauskas, S.; Jose Chavez Junco, A.; Grube, T.; Robinius, M.; Stolten, D. Options of natural gas pipeline reassignment for hydrogen: Cost assessment for a Germany case study. Int. J. Hydrog. Energy 2020, 45, 12095–12107. [Google Scholar] [CrossRef]

- Nguyen, T.T.; Park, J.S.; Kim, W.S.; Nahm, S.H.; Beak, U.B. Environment hydrogen embrittlement of pipeline steel X70 under various gas mixture conditions with in situ small punch tests. Mater. Sci. Eng. A 2020, 781, 139114. [Google Scholar] [CrossRef]

- Wulf, C.; Reuß, M.; Grube, T.; Zapp, P.; Robinius, M.; Hake, J.F.; Stolten, D. Life Cycle Assessment of hydrogen transport and distribution options. J. Clean. Prod. 2018, 199, 431–443. [Google Scholar] [CrossRef]

- Ishimoto, Y.; Voldsund, M.; Nekså, P.; Roussanaly, S.; Berstad, D.; Gardarsdottir, S.O. Large-scale production and transport of hydrogen from Norway to Europe and Japan: Value chain analysis and comparison of liquid hydrogen and ammonia as energy carriers. Int. J. Hydrog. Energy 2020, 45, 32865–32883. [Google Scholar] [CrossRef]

- Boretti, A. Production of hydrogen for export from wind and solar energy, natural gas, and coal in Australia. Int. J. Hydrog. Energy 2020, 45, 3899–3904. [Google Scholar] [CrossRef]

- Gallardo, F.I.; Monforti Ferrario, A.; Lamagna, M.; Bocci, E.; Astiaso Garcia, D.; Baeza-Jeria, T.E. A Techno-Economic Analysis of solar hydrogen production by electrolysis in the north of Chile and the case of exportation from Atacama Desert to Japan. Int. J. Hydrog. Energy 2020, in press. [Google Scholar] [CrossRef]

- Heuser, P.M.; Ryberg, D.S.; Grube, T.; Robinius, M.; Stolten, D. Techno-economic analysis of a potential energy trading link between Patagonia and Japan based on CO2 free hydrogen. Int. J. Hydrog. Energy 2019, 44, 12733–12747. [Google Scholar] [CrossRef]

- Ash, N.; Scarbrough, T. Sailing on Solar: Could Green Ammonia Decarbonise International Shipping? Environmental Defense Fund: London, UK, 2019. [Google Scholar]

- Miyaoka, H.; Miyaoka, H.; Ichikawa, T.; Ichikawa, T.; Kojima, Y. Highly purified hydrogen production from ammonia for PEM fuel cell. Int. J. Hydrog. Energy 2018, 43, 14486–14492. [Google Scholar] [CrossRef]

- Reuß, M.; Grube, T.; Robinius, M.; Stolten, D. A hydrogen supply chain with spatial resolution: Comparative analysis of infrastructure technologies in Germany. Appl. Energy 2019, 247, 438–453. [Google Scholar] [CrossRef]

- Tlili, O.; Mansilla, C.; Linen, J.; Reuß, M.; Grube, T.; Robinius, M.; André, J.; Perez, Y.; Le Duigou, A.; Stolten, D. Geospatial modelling of the hydrogen infrastructure in France in order to identify the most suited supply chains. Int. J. Hydrog. Energy 2020, 45, 3053–3072. [Google Scholar] [CrossRef]

- Lahnaoui, A.; Wulf, C.; Heinrichs, H.; Dalmazzone, D. Optimizing hydrogen transportation system for mobility via compressed hydrogen trucks. Int. J. Hydrog. Energy 2019, 44, 19302–19312. [Google Scholar] [CrossRef]

- Moradi, R.; Groth, K.M. Hydrogen storage and delivery: Review of the state of the art technologies and risk and reliability analysis. Int. J. Hydrog. Energy 2019, 44, 12254–12269. [Google Scholar] [CrossRef]

- Bracha, M.; Lorenz, G.; Patzelt, A.; Wanner, M. Large-scale hydrogen liquefaction in Germany. Int. J. Hydrog. Energy 1994, 19, 53–59. [Google Scholar] [CrossRef]

- Wijayanta, A.T.; Oda, T.; Purnomo, C.W.; Kashiwagi, T.; Aziz, M. Liquid hydrogen, methylcyclohexane, and ammonia as potential hydrogen storage: Comparison review. Int. J. Hydrog. Energy 2019, 44, 15026–15044. [Google Scholar] [CrossRef]

- Aakko-Saksa, P.T.; Cook, C.; Kiviaho, J.; Repo, T. Liquid organic hydrogen carriers for transportation and storing of renewable energy—Review and discussion. J. Power Sources 2018, 396, 803–823. [Google Scholar] [CrossRef]

- Brey, J. Use of hydrogen as a seasonal energy storage system to manage renewable power deployment in Spain by 2030. Int. J. Hydrog. Energy 2020, in press. [Google Scholar] [CrossRef]

- Reuß, M.; Grube, T.; Robinius, M.; Preuster, P.; Wasserscheid, P.; Stolten, D. Seasonal storage and alternative carriers: A flexible hydrogen supply chain model. Appl. Energy 2017, 200, 290–302. [Google Scholar] [CrossRef]

- Zivar, D.; Kumar, S.; Foroozesh, J. Underground hydrogen storage: A comprehensive review. Int. J. Hydrog. Energy 2020, in press. [Google Scholar] [CrossRef]

- Caglayan, D.G.; Weber, N.; Heinrichs, H.U.; Linßen, J.; Robinius, M.; Kukla, P.A.; Stolten, D. Technical potential of salt caverns for hydrogen storage in Europe. Int. J. Hydrog. Energy 2020, 45, 6793–6805. [Google Scholar] [CrossRef]

- Tarkowski, R. Perspectives of using the geological subsurface for hydrogen storage in Poland. Int. J. Hydrog. Energy 2017, 42, 347–355. [Google Scholar] [CrossRef]

- Bai, M.; Song, K.; Sun, Y.; He, M.; Li, Y.; Sun, J. An overview of hydrogen underground storage technology and prospects in China. J. Pet. Sci. Eng. 2014, 124, 132–136. [Google Scholar] [CrossRef]

- Lemieux, A.; Shkarupin, A.; Sharp, K. Geologic feasibility of underground hydrogen storage in Canada. Int. J. Hydrog. Energy 2020, 45, 32243–32259. [Google Scholar] [CrossRef]

- Hirscher, M.; Yartys, V.A.; Baricco, M.; Bellosta von Colbe, J.; Blanchard, D.; Bowman, R.C.; Broom, D.P.; Buckley, C.E.; Chang, F.; Chen, P.; et al. Materials for hydrogen-based energy storage—past, recent progress and future outlook. J. Alloy. Compd. 2020, 827, 153548. [Google Scholar] [CrossRef]

- Crow, J.M. Hydrogen storage gets real. Chemistry World. 2019. Available online: https://www.chemistryworld.com/features/hydrogen-storage-gets-real/3010794.article (accessed on 18 December 2020).

- Collins, L. World First for Solid-State Green Hydrogen at Hybrid Solar Project. 2020. Available online: https://www.rechargenews.com/transition/world-first-for-solid-state-green-hydrogen-at-hybrid-solar-project/2-1-771319 (accessed on 18 December 2020).

- Plug Power. Fuel Cells Products for Material Handling Equipment. 2020. Available online: https://www.plugpower.com/fuel-cell-power/gendrive/ (accessed on 18 December 2020).

- Kakoulaki, G.; Kougias, I.; Taylor, N.; Dolci, F.; Moya, J.; Jäger-Waldau, A. Green hydrogen in Europe—A regional assessment: Substituting existing production with electrolysis powered by renewables. Energy Convers. Manag. 2020, 113649, in press. [Google Scholar] [CrossRef]

- Bhaskar, A.; Assadi, M.; Nikpey Somehsaraei, H. Decarbonization of the Iron and Steel Industry with Direct Reduction of Iron Ore with Green Hydrogen. Energies 2020, 13, 758. [Google Scholar] [CrossRef]

- IEA. Global EV Outlook 2020. 2020. Available online: https://www.iea.org/reports/global-ev-outlook-2020 (accessed on 10 December 2020).

- IEA. Global EV Outlook 2019. 2019. Available online: https://www.iea.org/reports/global-ev-outlook-2019 (accessed on 10 December 2020).

- TCP, I.A. 2019 Survey on the Number of Fuel Cell Vehicles, Hydrogen Refueling Stations and Targets. 2019. Available online: https://www.ieafuelcell.com/fileadmin/publications/2019-04_AFC_TCP_survey_status_FCEV_2018.pdf (accessed on 10 December 2020).

- Wanitschke, A.; Hoffmann, S. Are battery electric vehicles the future? An uncertainty comparison with hydrogen and combustion engines. Environ. Innov. Soc. Transit. 2020, 35, 509–523. [Google Scholar] [CrossRef]

- FuelCellsWorks. 600 HYPE Hydrogen Taxis Planned in Paris for the End of 2020. 2020. Available online: https://fuelcellsworks.com/news/thursday-throwback-spotlight-600-hype-hydrogen-taxis-planned-in-paris-for-the-end-of-2020/ (accessed on 10 December 2020).

- Hall, M. Plans for 50,000 Hydrogen-Powered Taxis in Paris. 2020. Available online: https://www.pv-magazine.com/2020/11/12/plans-for-50000-hydrogen-powered-taxis-in-paris/ (accessed on 10 December 2020).

- Bae, S.; Lee, E.; Han, J. Multi-Period Planning of Hydrogen Supply Network for Refuelling Hydrogen Fuel Cell Vehicles in Urban Areas. Sustainability 2020, 12, 4114. [Google Scholar] [CrossRef]

- Grüger, F.; Dylewski, L.; Robinius, M.; Stolten, D. Carsharing with fuel cell vehicles: Sizing hydrogen refueling stations based on refueling behavior. Appl. Energy 2018, 228, 1540–1549. [Google Scholar] [CrossRef]

- Lee, D.Y.; Elgowainy, A.; Kotz, A.; Vijayagopal, R.; Marcinkoski, J. Life-cycle implications of hydrogen fuel cell electric vehicle technology for medium- and heavy-duty trucks. J. Power Sources 2018, 393, 217–229. [Google Scholar] [CrossRef]

- El Hannach, M.; Ahmadi, P.; Guzman, L.; Pickup, S.; Kjeang, E. Life cycle assessment of hydrogen and diesel dual-fuel class 8 heavy duty trucks. Int. J. Hydrog. Energy 2019, 44, 8575–8584. [Google Scholar] [CrossRef]

- Mulholland, E.; Teter, J.; Cazzola, P.; McDonald, Z.; Ó Gallachóir, B.P. The long haul towards decarbonising road freight—A global assessment to 2050. Appl. Energy 2018, 216, 678–693. [Google Scholar] [CrossRef]

- Connolly, D. Economic viability of electric roads compared to oil and batteries for all forms of road transport. Energy Strategy Rev. 2017, 18, 235–249. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. ASKO puts four Scania hydrogen fuel cell electric trucks into service in Norway. Fuel Cells Bull. 2020, 2020, 1. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. H2-Share starts demo of hydrogen powered truck in Netherlands. Fuel Cells Bull. 2020, 2020, 4. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. Clean Logistics JV converts diesel trucks to hydrogen-hybrid. Fuel Cells Bull. 2019, 2019, 4–5. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. Air Liquide, Rotterdam link to foster hydrogen trucks, infrastructure. Fuel Cells Bull. 2020, 2020, 4. [Google Scholar] [CrossRef]

- Lao, J.; Song, H.; Wang, C.; Zhou, Y.; Wang, J. Reducing atmospheric pollutant and greenhouse gas emissions of heavy duty trucks by substituting diesel with hydrogen in Beijing-Tianjin-Hebei-Shandong region, China. Int. J. Hydrog. Energy 2020. [Google Scholar] [CrossRef]

- Kast, J.; Morrison, G.; Gangloff, J.J.; Vijayagopal, R.; Marcinkoski, J. Designing hydrogen fuel cell electric trucks in a diverse medium and heavy duty market. Res. Transp. Econ. 2018, 70, 139–147. [Google Scholar] [CrossRef]

- Tyrol, H.S. The CHIC Project. 2020. Available online: https://www.h2-suedtirol.com/en/projects/chic/ (accessed on 6 December 2020).

- Loría, L.E.; Watson, V.; Kiso, T.; Phimister, E. Investigating users’ preferences for Low Emission Buses: Experiences from Europe’s largest hydrogen bus fleet. J. Choice Model. 2019, 32, 100169. [Google Scholar] [CrossRef]

- Hua, T.; Ahluwalia, R.; Eudy, L.; Singer, G.; Jermer, B.; Asselin-Miller, N.; Wessel, S.; Patterson, T.; Marcinkoski, J. Status of hydrogen fuel cell electric buses worldwide. J. Power Sources 2014, 269, 975–993. [Google Scholar] [CrossRef]

- Lozanovski, A.; Whitehouse, N.; Ko, N.; Whitehouse, S. Sustainability Assessment of Fuel Cell Buses in Public Transport. Sustainability 2018, 10, 1480. [Google Scholar] [CrossRef]

- Lee, D.Y.; Elgowainy, A.; Vijayagopal, R. Well-to-wheel environmental implications of fuel economy targets for hydrogen fuel cell electric buses in the United States. Energy Policy 2019, 128, 565–583. [Google Scholar] [CrossRef]

- Piraino, F.; Genovese, M.; Fragiacomo, P. Towards a new mobility concept for regional trains and hydrogen infrastructure. Energy Convers. Manag. 2020, Article in press, 113650. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. Hydrogen station for Hesse passenger trains. Fuel Cells Bull. 2020, 2020, 9. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. Alstom, Eversholt Rail invest another £1m in Breeze hydrogen train. Fuel Cells Bull. 2020, 2020, 5. [Google Scholar] [CrossRef]

- Fuel Cells Bulletin. Alstom, Snam develop hydrogen trains in Italy. Fuel Cells Bull. 2020, 2020, 4. [Google Scholar]

- Bicer, Y.; Dincer, I. Environmental impact categories of hydrogen and ammonia driven transoceanic maritime vehicles: A comparative evaluation. Int. J. Hydrog. Energy 2018, 43, 4583–4596. [Google Scholar] [CrossRef]

- Baroutaji, A.; Wilberforce, T.; Ramadan, M.; Olabi, A.G. Comprehensive investigation on hydrogen and fuel cell technology in the aviation and aerospace sectors. Renew. Sustain. Energy Rev. 2019, 106, 31–40. [Google Scholar] [CrossRef]

- Airbus. Airbus ZEROe Project. 2020. Available online: https://www.airbus.com/newsroom/stories/these-new-Airbus-concept-aircraft-have-one-thing-in-common.html (accessed on 6 December 2020).

- Lo Basso, G.; Nastasi, B.; Astiaso Garcia, D.; Cumo, F. How to handle the Hydrogen enriched Natural Gas blends in combustion efficiency measurement procedure of conventional and condensing boilers. Energy 2017, 123, 615–636. [Google Scholar] [CrossRef]

- Schiro, F.; Stoppato, A.; Benato, A. Modelling and analyzing the impact of hydrogen enriched natural gas on domestic gas boilers in a decarbonization perspective. Carbon Resour. Convers. 2020, 3, 122–129. [Google Scholar] [CrossRef]

- Wahl, J.; Kallo, J. Quantitative valuation of hydrogen blending in European gas grids and its impact on the combustion process of large-bore gas engines. Int. J. Hydrog. Energy 2020, 45, 32534–32546. [Google Scholar] [CrossRef]

- Meziane, S.; Bentebbiche, A. Numerical study of blended fuel natural gas-hydrogen combustion in rich/quench/lean combustor of a micro gas turbine. Int. J. Hydrog. Energy 2019, 44, 15610–15621. [Google Scholar] [CrossRef]

- H21. H21 Project. 2016. Available online: https://www.h21.green/ (accessed on 6 December 2020).

- Hy4Heat. Hy4Heat Project. 2018. Available online: https://www.hy4heat.info/ (accessed on 6 December 2020).

- Worcester-Bosch. Hydrogen-Fired Boiler. 2020. Available online: https://www.worcester-bosch.co.uk/hydrogen (accessed on 6 December 2020).

- SNG. H100 Fife Project. 2020. Available online: https://www.sgn.co.uk/H100Fife (accessed on 6 December 2020).

- Taanman, M.; de Groot, A.; Kemp, R.; Verspagen, B. Diffusion paths for micro cogeneration using hydrogen in the Netherlands. J. Clean. Prod. 2008, 16, S124–S132. [Google Scholar] [CrossRef]

- Lokar, J.; Virtič, P. The potential for integration of hydrogen for complete energy self-sufficiency in residential buildings with photovoltaic and battery storage systems. Int. J. Hydrog. Energy 2020, 45, 34566–34578. [Google Scholar] [CrossRef]

- McPherson, M.; Johnson, N.; Strubegger, M. The role of electricity storage and hydrogen technologies in enabling global low-carbon energy transitions. Appl. Energy 2018, 216, 649–661. [Google Scholar] [CrossRef]

- Ozawa, A.; Kudoh, Y.; Kitagawa, N.; Muramatsu, R. Life cycle CO2 emissions from power generation using hydrogen energy carriers. Int. J. Hydrog. Energy 2019, 44, 11219–11232. [Google Scholar] [CrossRef]

- Matsuo, Y.; Endo, S.; Nagatomi, Y.; Shibata, Y.; Komiyama, R.; Fujii, Y. A quantitative analysis of Japan’s optimal power generation mix in 2050 and the role of CO2-free hydrogen. Energy 2018, 165, 1200–1219. [Google Scholar] [CrossRef]

- Shulga, R.; Putilova, I.; Smirnova, T.; Ivanova, N. Safe and waste-free technologies using hydrogen electric power generation. Int. J. Hydrog. Energy 2020, 45, 34037–34047. [Google Scholar] [CrossRef]

- Kafetzis, A.; Ziogou, C.; Panopoulos, K.; Papadopoulou, S.; Seferlis, P.; Voutetakis, S. Energy management strategies based on hybrid automata for islanded microgrids with renewable sources, batteries and hydrogen. Renew. Sustain. Energy Rev. 2020, 134, 110118. [Google Scholar] [CrossRef]

- Kalamaras, E.; Belekoukia, M.; Lin, Z.; Xu, B.; Wang, H.; Xuan, J. Techno-economic Assessment of a Hybrid Off-grid DC System for Combined Heat and Power Generation in Remote Islands. Energy Procedia 2019, 158, 6315–6320. [Google Scholar] [CrossRef]

- Gracia, L.; Casero, P.; Bourasseau, C.; Chabert, A. Use of Hydrogen in Off-Grid Locations, a Techno-Economic Assessment. Energies 2018, 11, 3141. [Google Scholar] [CrossRef]

- Pflugmann, F.; Blasio, N.D. Geopolitical and Market Implications of Renewable Hydrogen. New Dependencies in a Low-Carbon Energy World. 2020. Harvard Belfer Center for Science and International Affairs, Report, March 2020. Available online: https://www.belfercenter.org/sites/default/files/files/publication/Geopolitical%20and%20Market%20Implications%20of%20Renewable%20Hydrogen.pdf (accessed on 18 December 2020).

- IRENA. Green Hydrogen: A Guide to Policy Making. 2020. International Renewable Energy Agency, Abu Dhabi, November 2020. Available online: https://www.irena.org/publications/2020/Nov/Green-hydrogen (accessed on 18 December 2020).

- Hikima, K.; Tsujimoto, M.; Takeuchi, M.; Kajikawa, Y. Transition Analysis of Budgetary Allocation for Projects on Hydrogen-Related Technologies in Japan. Sustainability 2020, 12, 8546. [Google Scholar] [CrossRef]

- Meng, X.; Gu, A.; Wu, X.; Zhou, L.; Zhou, J.; Liu, B.; Mao, Z. Status quo of China hydrogen strategy in the field of transportation and international comparisons. Int. J. Hydrog. Energy 2020, in press. [Google Scholar] [CrossRef]

- SPGLOBAL. How Hydrogen Can Fuel The Energy Transition. 2020. Available online: https://www.spglobal.com/ratings/en/research/articles/201119-how-hydrogen-can-fuel-the-energy-transition-11740867 (accessed on 18 December 2020).

- Kan, S. South Korea’s Hydrogen Strategy and Industrial Perspectives. 2020. Available online: https://www.ifri.org/sites/default/files/atoms/files/sichao_kan_hydrogen_korea_2020_1.pdf (accessed on 18 December 2020).

- Rystad Energy. Hydrogen Wars: Governments Race to Boost Green Hydrogen Production; Rystad Energy: Oslo, Norway, 2020. [Google Scholar]

- Hartley, P.G.; Au, V. Towards a Large-Scale Hydrogen Industry for Australia. Engineering 2020, 6, 1346–1348. [Google Scholar] [CrossRef]

- Council, T.A. The ACWA Power—Air Products Joint Venture for gReen Hydrogen: A New Saudi Energy Policy? 2020. Atlantic Council, 24 July 2020. Available online: https://www.atlanticcouncil.org/blogs/energysource/the-acwa-power-air-products-joint-venture-for-green-hydrogen-a-new-saudi-energy-policy/ (accessed on 18 December 2020).

- SPGLOBAL. UAE Investing in Green and Blue Hydrogen Projects as Part of Clean Energy Move: Official. 2020. Available online: https://www.spglobal.com/platts/en/market-insights/latest-news/electric-power/101920-uae-investing-in-green-and-blue-hydrogen-projects-as-part-of-clean-energy-move-official (accessed on 18 December 2020).

- Smith, M. Morocco aims for global green hydrogen role. Hydrogen Economist. 2020. Available online: https://pemedianetwork.com/hydrogen-economist/articles/green-hydrogen/2020/morocco-aims-for-global-green-hydrogen-role (accessed on 18 December 2020).

- Ishikawa, Y. Russia plans to export hydrogen to Asia in green shift. Asia Nikkei. 2020. Available online: https://asia.nikkei.com/Editor-s-Picks/Interview/Russia-plans-to-export-hydrogen-to-Asia-in-green-shift#:~:text=Russia%20produces%20hydrogen%20now%20for,increase%20it%20tenfold%20by%202035 (accessed on 18 December 2020).

- Strategy&. The Dawn of Green Hydrogen—Maintaining the GCC’s Edge in a Decarbonized World. 2020. Available online: https://www.strategyand.pwc.com/m1/en/reports/2020/the-dawn-of-green-hydrogen/the-dawn-of-green-hydrogen.pdf (accessed on 11 December 2020).

- European Hydrogen Backbone Initiative. European Hydrogen Backbone. 2020. Available online: https://gasforclimate2050.eu/sdm_downloads/european-hydrogen-backbone/ (accessed on 18 December 2020).

- Franke, A.; Baratti, G. Green Hydrogen: A Guide to Policy Making. 2020. S&P Global Platts, 9 December 2020. Available online: https://www.spglobal.com/platts/en/market-insights/latest-news/metals/120920-european-groups-join-hydrogen-project-targeting-2kg-production (accessed on 18 December 2020).

- Ratcliffe, V. Saudi Arabia Sends Blue Ammonia to Japan in World-First Shipment. 2020. Available online: https://www.bloomberg.com/news/articles/2020-09-27/saudi-arabia-sends-blue-ammonia-to-japan-in-world-first-shipment (accessed on 11 December 2020).

- Velazquez Abad, A.; Dodds, P.E. Green hydrogen characterisation initiatives: Definitions, standards, guarantees of origin, and challenges. Energy Policy 2020, 138, 111300. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Noussan, M.; Raimondi, P.P.; Scita, R.; Hafner, M. The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective. Sustainability 2021, 13, 298. https://doi.org/10.3390/su13010298

Noussan M, Raimondi PP, Scita R, Hafner M. The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective. Sustainability. 2021; 13(1):298. https://doi.org/10.3390/su13010298

Chicago/Turabian StyleNoussan, Michel, Pier Paolo Raimondi, Rossana Scita, and Manfred Hafner. 2021. "The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective" Sustainability 13, no. 1: 298. https://doi.org/10.3390/su13010298

APA StyleNoussan, M., Raimondi, P. P., Scita, R., & Hafner, M. (2021). The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective. Sustainability, 13(1), 298. https://doi.org/10.3390/su13010298