The general model we use is as follows:

where

Tobin’s Q represents firm value, computed annually,

X is an explanatory variable representing board characteristics, and

A is the control for firm accounting information.

T is the total number of years in the sample period. We consider firm and year fixed effects throughout our analyses in this study.

5.1. Gaussian Copula Marginal Regression Results

We first consider a regression model incorporating all of the eight board characteristics (board size, independent directors, director age, family directors (1/0), outside CEO directors, directors with financial expertise, female directors, foreign directors) with controls for firm characteristics.

Based on the Akaike information criterion (AIC), we select an optimal error correlation matrix model of ARMA (1, 1) for four different combinations of p and q: (0, 0), (0, 1), (1, 0), and (1, 1).

Table 2 shows the result of the ARMA model selection and presents the GCMR model estimation of Tobin’s Q (c_q) with eight board characteristics and controls for firms with an error dependence structure of ARMA (1, 1).

Among the 13 board and firm characteristics, most variables, except independent directors (v_outsiderpct) and directors with financial expertise (v_financialoutpct), have a statistically significant association with firm value, or Tobin’s Q (c_q). We observe that board size (v_bsize), director age (v_age), foreign directors (v_foreignpct), log(Sales) (c_lnsale), firm age (c_firmage), and business segments (c_segment_bus) have a statistically significant negative association with firm value at the 1% level. Family directors (1/0) (v_relativeflag) and female directors (v_femalepct) are negatively related to firm value at the 10% significance level. Outside CEO directors (v_ceodirector), capital expenditure to sales (c_capx_sale), and ROA (c_fichroa) are positively associated with firm value at the 1% significance level.

Thus, after considering eight widely used board characteristics, we do not find much evidence that independent directors and directors with financial expertise affect firm value. However, we do confirm that an increase in board size decreases firm value, which is consistent with Eisenberg et al. [

1] and Yermack [

3]. We also observe that having outside CEO directors helps increase firm value, which is consistent with Faleye [

8]. In addition, on average, having older directors, higher proportions of foreign directors, larger fractions of female directors, and directors with a family member who is a CEO of a company are likely to decrease the firm value.

After observing the overall effect of board/director characteristics on firm value, we analyze causal relationships among firm value, board characteristics, and firm characteristics using various statistical methods.

5.2. Structural Equation Modeling Results

In this section, we examine how board and firm characteristics (including firm value) are associated with each other. We consider all 14 of the variables (eight board variables and six firm variables) in the analysis.

We perform PCA and map all 14 of the variables onto a two-dimensional PCA plot (see

Figure 1). After examining

Figure 1 more closely, we split the variables into two groups based on the first principal component. Factor 1 contains variables on the right side of the domain: Female directors (v_femalepct), independent directors (v_outsiderpct), log(Sales) (c_lnsale), firm age (c_firmage), director age (v_age), foreign directors (v_foreignpct), board size (v_bsize), and business segments (c_segment_bus). These variables characterize large and experienced companies. We categorize all such variables as Factor 1. Factor 2 includes variables on the left side of the domain: Firm value, or Tobin’s Q (c_q), ROA (c_fichroa), outside CEO directors (v_ceodirector), and capital expenditures to sales (c_capx_sale). We categorize these variables, which characterize high-performance companies, as Factor 2.

Next, we incorporate Factors 1 and 2 into SEM. These two factors are used as latent variable models.

Table 3 shows the performance results of SEM. The

p-values of both the estimator model and test baseline model are less than 0, confirming the validity of our model.

Table 3 reports the comparative fit index (CFI), the Tucker–Lewis index (TLI), AIC, Bayesian information criterion (BIC), the root mean square error of approximation (RMSEA), and the standardized root mean square residual (SRMR) of the model.

Table 4 presents latent variable model estimations for Factors 1 and 2. Parameter estimates, standard errors, and Z-values for statistical significance of the parameters are reported.

The Z-values of all parameters in

Table 4, Panel A are larger than 2; thus, the association is statistically significant for all eight firm and board variables in the Factor 1 category. All firm and board characteristics have estimates larger than 0.1, and firm age (c_firmage), director age (v_age), and log (Sales) (c_lnsale) are the top three characteristics explaining for Factor 1. Variables in Factor 1 have traits of large seasoned companies. Thus, firms that are more seasoned in age and have larger sales with relatively older directors do play an important role.

Table 4, Panel B shows the latent modeling result for Factor 2. Similarly to Factor 1 in

Table 4, Panel A, we find that all four firm and board variables are representatives of Factor 2. The top three characteristics are Tobin’s Q (c_q), ROA (c_fichroa), and outside CEO directors (v_ceodirector). These variables are traits of high-performance companies. Thus, we conclude that independent directors with outside CEO positions (v_ceodirector) play a significant role in high-performance companies.

5.3. Factor Analysis Results

We cluster firm and board characteristics are into three factors, instead of two factors, based on their covariance. In this process, a characteristic or a variable is used to explain the factor with the largest factor loading. For example, log (Sales) explains Factor 3 because its factor loading (0.6) is the largest in Factor 3. Factor 1 is explained by four variables: Firm age (c_firmage), independent directors (v_outsiderpct), director age (v_age), and outside CEO directors (v_ceodirector). Factor 2 contains two variables: ROA (c_fichroa) and Tobin’s Q (c_q). Factor 3 includes two variables—log (Sales) (c_lnsale) and board size (v_bsize)—for its descriptions. Among the 14 variables, eight are used to explain three factors; the remaining six (family, female, and foreign directors, directors with financial expertise, capital expenditures to sales, and business segments) are not selected.

Factor 1 characterizes seasoned or experienced firms, which are likely to be listed earlier, have larger sales, have a higher proportion of independent directors, have directors who are aged, and have fewer directors with CEO positions in other companies. Factor 2 captures firm value and firm performance. Factor 3 characterizes large firms, as they tend to have higher sales and larger boards.

The factor analysis separates our variables in a more interpretable way compared to SEM in

Section 5.2, such that Factor 1 and Factor 3 capture how board characteristics and firm characteristics are related to each other, whereas Factor 2 explains firm performance through ROA and Tobin’s Q.

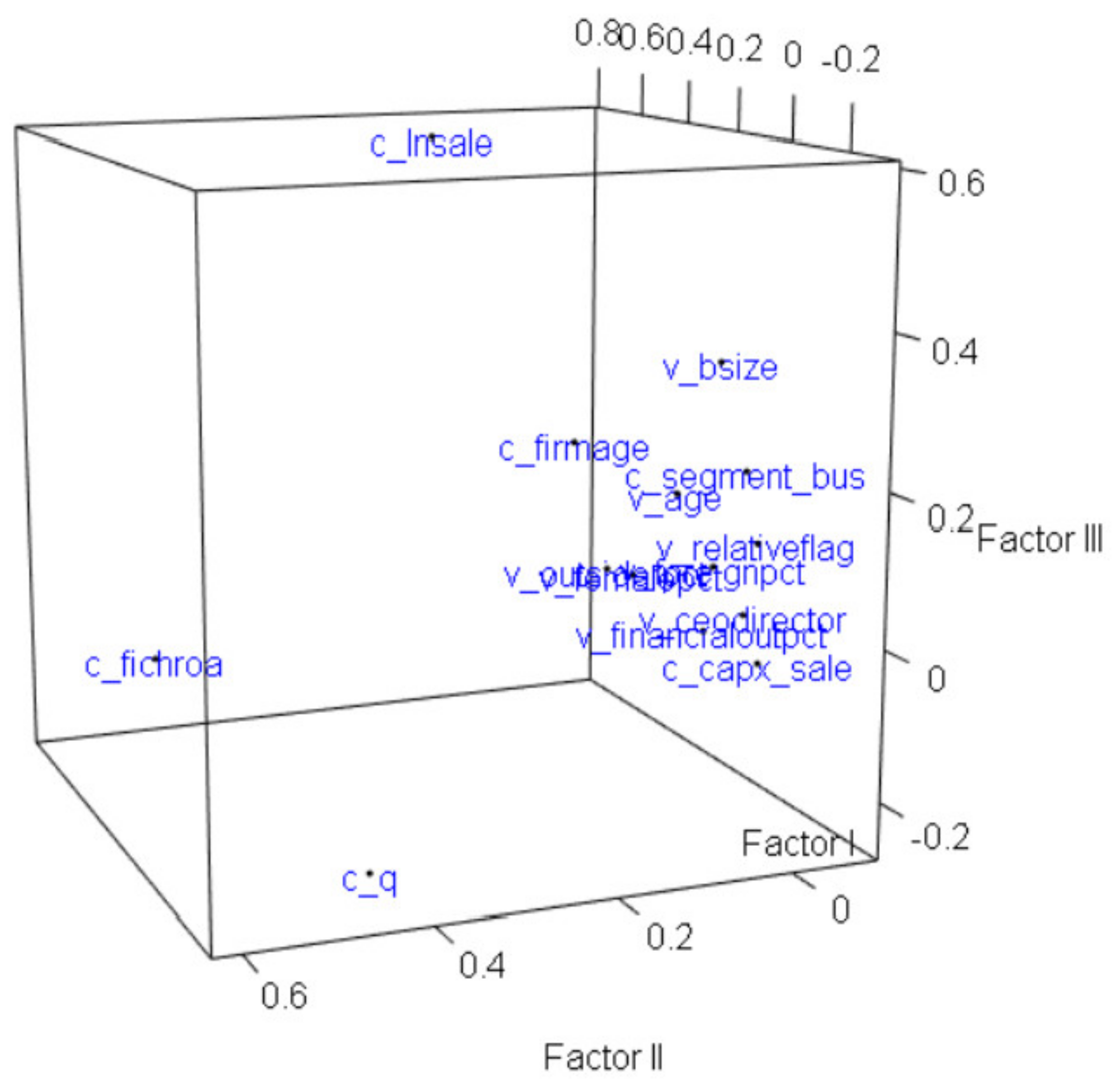

Figure 2 shows a three-dimensional visualization of the association of the 14 board and firm variables based on the three factors.

Table 5 represents factor loadings of firm and board characteristics. We observe that the loadings for Factors 1 and 2 tend to have the opposite signs, especially for board-level variables. This implies that most of the board-level variables, except outside CEO directors and female directors, are negatively associated with the factor representing firm performance and firm value.

We move on to the graphical approach by constructing a DAG to examine causal inferences among firm value, board variables, and firm characteristics.

5.4. Graphical Model Results: DAG with GCMR

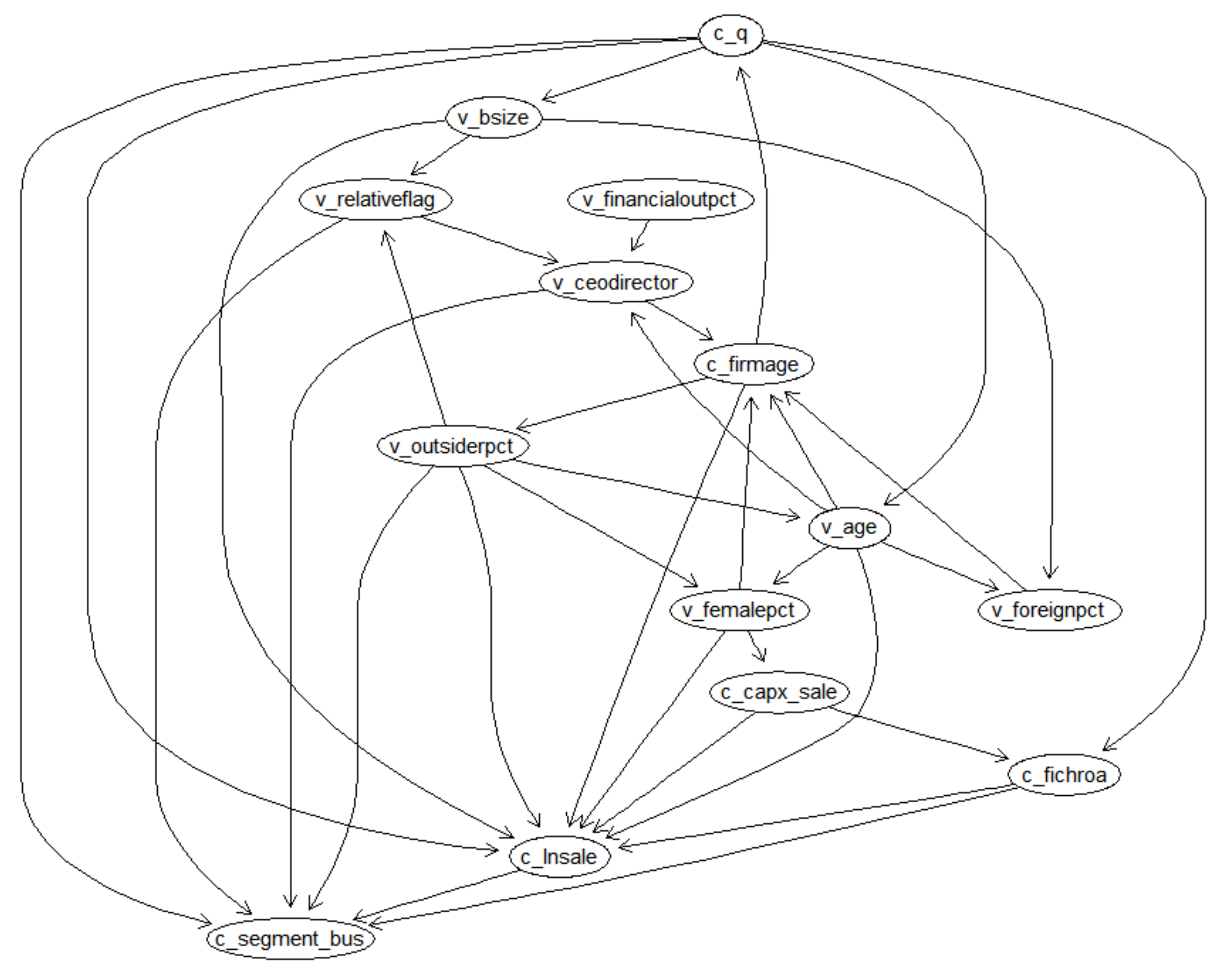

To further investigate the relationships among the eight board and six firm characteristics, including firm value, we construct a DAG.

Figure 3 plots the DAG of the 14 variables. The explanatory variable is located at the origin and the dependent variable at the point of the arrows.

From

Figure 3, we select three terminal nodes: Business segments (c_segment_bus), log (Sales) (c_lnsale), and firm age (c_firmage). We then construct three GCMR models by defining the terminal node as the response variable and the nodes with directed edges, each of which represents a direct cause, as predictor variables.

First, in Model 1, we construct a GCMR model where the business segment (c_segment_bus) is the dependent variable and Tobin’s Q (c_q), family directors (1/0) (v_relativeflag), outside CEO directors (v_ceodirector), independent directors (v_outsiderpct), log (Sales) (c_lnsale), and ROA (c_fichroa) are explanatory variables.

Table 6 shows the result of selecting p and q for an optimal ARMA model based on AIC criteria among four different combinations of p and q: (0, 0), (0, 1), (1, 0), and (1, 1). Both ARMA (0, 1) and ARMA (1, 0) turn out to be the best models with minimum AIC values.

Table 6 also presents the estimation results of the GCMR model of business segments (c_segment_bus) as a dependent variable with ARMA (0, 1) and ARMA (1, 0) error dependence structures. In both models, all variables—Tobin’s Q (c_q), family directors (1/0) (v_relativeflag), outside-CEO directors (v_ceodirector), independent directors (v_outsiderpct), log (Sales) (c_lnsale), and ROA (c_fichroa)—remain statistically significant at the 5% level. Tobin’s Q (c_q) and ROA (c_fichroa) are negatively related to business segments (c_segment_bus), and the other four variables are positively related to business segments (c_segment_bus). The sigma dispersion parameter is statistically significant at the 5% significance level. From

Table 6, we observe a reverse-causal relationship for Tobin’s Q and business segments. Firms with larger firm value and ROA tend to have lower numbers of business segments. We also find that firms with greater fractions of independent directors, larger sales, greater proportions of outside CEO directors, and directors whose relatives are CEOs of the same company are likely to have a larger number of business segments on average.

In Model 2, we construct a GCMR model where log (Sales) (c_lnsale) is the dependent variable and Tobin’s Q (c_q), board size (v_bsize), independent directors (outsiderpct), firm age (v_firmage), female directors (v_femalepct), capital expenditures to sales (c_capx_sale), director age (v_age), and ROA (c_fichroa) are explanatory variables.

where

Independent Directors and

Female Directors represent proportions of outside directors and female directors, respectively.

Table 7 shows the results of selecting p and q for an optimal ARMA model based on AIC criteria for four different combinations of p and q: (0, 0), (0, 1), (1, 0), and (1, 1). ARMA (1, 1) is selected as the best model with the minimum AIC value.

Table 7 also presents the estimation results of the GCMR model of log (Sales) (c_lnsale) as a dependent variable with an error dependence structure of ARMA (1, 1). All variables—Tobin’s Q (c_q), board size (v_bsize), independent directors (outsiderpct), firm age (v_firmage), female directors (v_femalepct), capital expenditures to sales (c_capx_sale), director age (v_age), and ROA (c_fichroa)—remain statistically significant at the 5% level. Tobin’s Q (c_q) and capital expenditures to sales (c_capx_sale) are negatively related and the other six variables are positively related to log (Sales) (c_lnsale). The sigma dispersion parameter is statistically significant at the 5% significance level. Firms are likely to have lower sales for those with larger firm value and capital expenditures to sales, on average. Firms tend to have larger sales on average as they are listed earlier and have larger ROA. Also, a company with more directors, more fractions of outsiders and female directors, and older directors has larger sales on average.

In Model 3, we construct a GCMR model where firm age (c_firmage) is the dependent variable and outside-CEO directors (v_ceodirector), female directors (v_femalepct), director age (v_age), and foreign directors (v_foreignpct) are explanatory variables.

where

Outside CEO, Female, and

Foreign Directors represent the proportions of the respective directors.

Table 8 shows the result of selecting p and q for an optimal ARMA model based on AIC criteria among four different combinations of p and q: (0, 0), (0, 1), (1, 0), and (1, 1). ARMA (1, 1) is selected as the best model with the minimum AIC value.

Table 8 also presents the estimation results of the GCMR model of firm age (c_firmage) as a dependent variable with the ARMA (1, 1) error dependence structure. All variables—outside CEO directors (v_ceodirector), female directors (v_femalepct), director age (v_age), and foreign directors (v_foreignpct)—remain statistically significant at the 5% level. The outside CEO directors (v_ceodirector) variable is negatively related and the other three variables are positively related to firm age (c_firmage). The sigma dispersion parameter is statistically significant at the 5% significance level. An average firm tends to be listed earlier if the company has lower proportions of outside CEO directors, greater fractions of female and foreign directors, and directors who are aged.

{kind=link}

{kind=link}

{kind=link}