3.3. Variables and Data

The study was designed in two stages:

Stage 1: An exploratory study was carried out to know the characteristics of the clients of the MFIs included in the sample. The instrument used in this investigation was a structured questionnaire-type survey.

Stage 2: In this stage of the study, it was determined if there are significant differences in mean between the punctuality of the payments of women and men according to the variables which could affect it: Age, ethnicity, educational level, marital status, amount, term, and purpose of the microcredit.

In summary, the purpose was to determine if the punctuality of the payments is due to some characteristic of women or men, or of the microcredits granted.

Table 1 summarizes the variables analyzed in this study by specifying their type. The way of obtaining the data will be described and justified in

Section 3.4 (Methodology).

3.3.1. Stage 1

In this stage, the CEOs of the MFIs involved in the study were asked to provide quantitative information about the characteristics that better describe women and men served by their organizations. In our opinion, taking into account the final objective of this paper, age, ethnicity, level of education, and marital status are the basic personal traits when analyzing the behavior of individuals who face the repayment of a loan, specifically a microcredit. This idea is confirmed by the usual “credit score” applied by banks when analyzing the solvency and credit worthiness of a potential client.

Each CEO was required to assess the degree of belonging of his/her (male or female) “standard client” to the characteristics and modalities displayed in

Table 2. To do this, they used a Likert scale from 1 to 5 (1: “Not important”, 2: “Scarcely important”, 3: “Moderately important”, 4: “Important”, and 5: “Most important”). For example,

Table 2 exhibits the response of a specific CEO about the age of his/her male “standard client”.

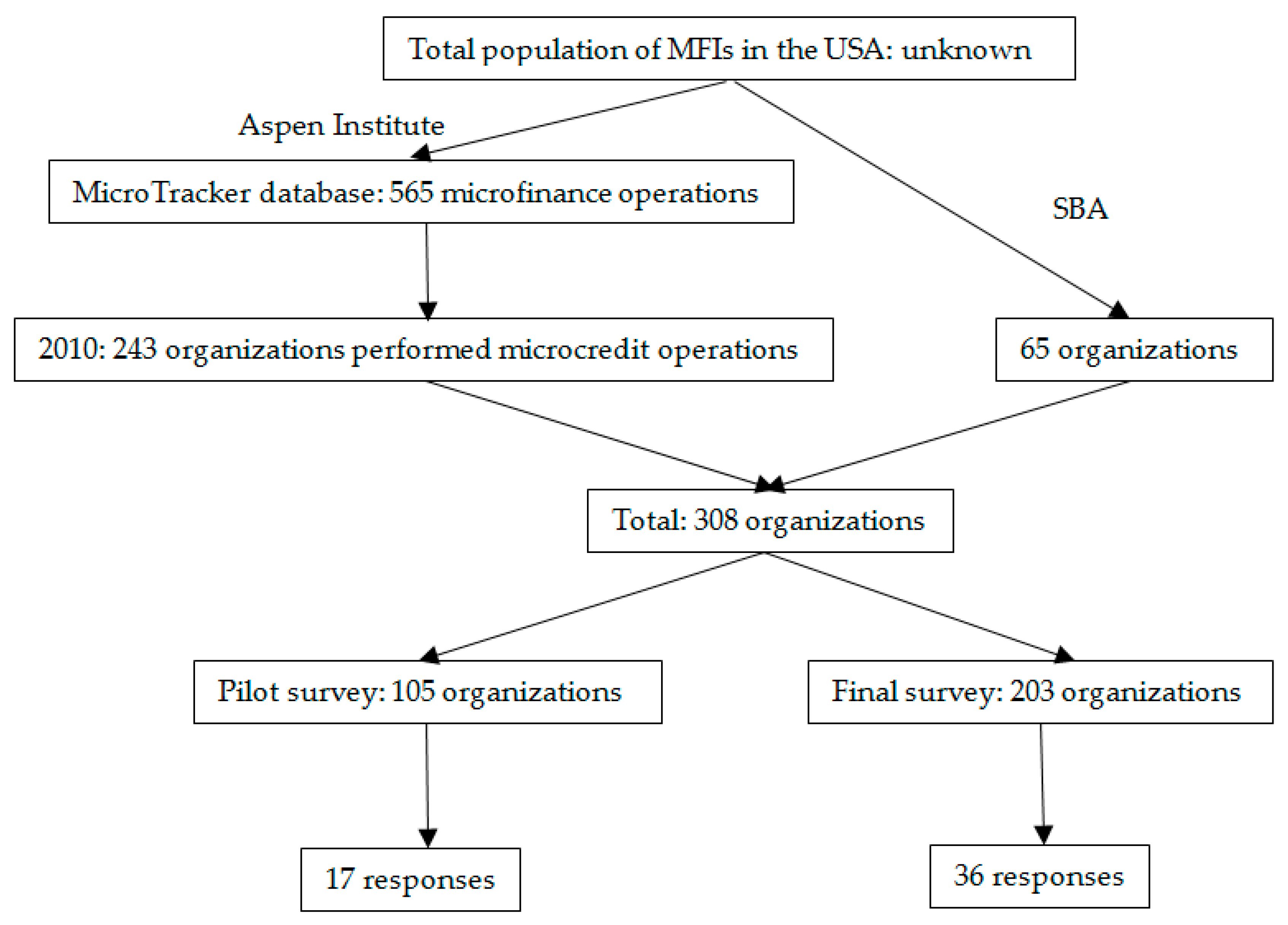

This means that a ratio of 3 to 8 (= 3 + 4 + 1) clients are between 18 and 25 years, a ratio of 4 to 8 are between 26 and 45 years, and that a ratio of 1 to 8 are older than 45 years. This interpretation can be extended to the rest of the characteristics, modalities, and sex. Finally, although the survey was responded to by 36 MFIs, some of them provided incomplete information for some modalities. This is the reason whereby the number,

n, of valid responses by modality and sex is lower than 36. The specific number of valid responses, as well as the mean and the standard deviation, by modality and sex are displayed in

Table 3.

3.3.2. Stage 2

In this second stage, the executives of the MFIs were asked for their opinions about the punctuality of men and women with respect to the following independent variables: Age, ethnicity, educational level, marital status, amount, term, and purpose of the microcredit.

Firstly, the punctuality was measured by the microcredit portfolio at risk of more than 30 days (PAR 30) of MFIs in USA at the date of their last fiscal year (2017). The PAR 30 is a known term used in the industry to measure the portfolio at risk. This is calculated by dividing the total dollar amount of loans which are overdue or with payment in arrears over thirty days by the total loan portfolio.

Secondly, experts responded to the survey by pointing out how independent variables affect PAR 30 depending on the sex. As in stage 1, each CEO was required to assess the degree of influence of the characteristics of his/her (male or female) “standard client” on the microcredit repayment. To do this, they answered on a Likert scale from one to six: 1: “Totally disagree”, 2: “Disagree”, 3: “Somewhat disagree”, 4: “Somewhat agree”, 5: “Agree”, and 6: “Totally agree”. In the beginning, the independent variables could or could not affect payment behavior depending on the sex of clients [

38]. For the sake of clarity, take into account that CEOs or portfolio managers in MFIs are responsible for keeping the payments in arrears under control for MFI sustainability; their professional experience and the appreciation of the situation of their MFI is the way to obtain the information needed for the study through the survey. In other words, the opinions and the beliefs of MFI managers about the personal traits of their clients is the “only truth” they are willing to take into account when giving a microcredit.

The specific number of valid responses, as well as the mean and the standard deviation, by characteristic and sex are displayed in

Table 4.

3.4. Methodology

As indicated, this paper focuses on data obtained from managers because managers perceive the most important determinants of repayment. In effect, the manager’s opinion plays a very significant role in planning and making decisions of the companies and the way in which forthcoming algorithms should be developed, due to the fact that managers provide us with plenty of information coming from their daily business lives.

The following paragraphs justify the chosen methodology as the only way to obtain the information necessary to implement the empirical analysis.

First, take into account that MFIs are required to contribute actual information on their clients. Each manager, apart from the information on PAR 30, has to look for the information of the actual characteristics of all his/her clients. If the number of clients of a specific MFI is high, it is possible that this manager has to select a sample of their clients.

Second, when providing managers’ perceptions about these characteristics, the number of valid responses was 36. Consequently, in the case of requiring actual information, we foresee that the number of valid responses could be insignificant because managers are not willing to lose time to respond to questionnaires.

This paper focuses on data obtained from managers. More specifically, it is assumed that the opinions and beliefs of MFI managers about the personal traits of their clients are considered as if they were the “only truth” that they are willing to take into account when giving a credit.

Therefore, our research is based on how the involved MFI managers perceive the most important determinants of loan repayment, providing us with quantitative information about the characteristics that better describe women and men served by their organization, such as the punctuality of men and women with respect to the following independent variables: Age, ethnicity, educational level, marital status, amount, term, and purpose of the microcredits.

Although perception is a cognitive process [

39], some authors provide some evidence on the critical role of managerial perception in both organizational decision-making and strategy formulation processes by providing some evidence on the significant influence that research from a managerial perception perspective has had on the understanding of how strategy forms in the organizations [

40]. The main contribution of this effort is the elaboration of various ways in which managerial perceptions influence strategy development processes beyond only implementation [

40].

As a relevant reflection, the article proves that the levels of perception that managers have about the conditions and characteristics of the organizational environment should contribute to the formation of their vision about the way strategies should be designed and appropriately implemented to adapt to the requirements of the specific environment; in our research, the microcredit policies in relation to women in the USA.

Many have been written about the accuracy of managers’ perceptions. In this way, Reference [

41] discusses an odyssey into the study of managerial perceptions spanning two decades and two empirical studies. It depicts the evolution of research questions, samples, study designs, problems with such research, and inferences drawn. It also identifies some errors which tend to be especially large and suggests some corrective actions.

As a matter of fact, using algorithms could be considered as a more precise tool than managers opinions. The fact that these decisions are made by algorithms rather than by people may influence perceptions of the decisions that are made, regardless of the qualities of the actual decision outcomes [

42].

In favor of our idea of the importance of the manager’s point of view, some academic research [

43] and results reinforce the argument that the general public does not fully trust algorithms or find it fair to use algorithms for decisions involving subjective judgments of human workers.

Further research needs to be done in order to understand what contributes to the perception that certain tasks can be done well uniquely by humans. People’s attitudes toward and perceptions of technologies have changed throughout history; some technologies originally considered to be socially awkward, rude, or unacceptable were eventually adopted as perceptions changed, or designs were improved to better fit human conceptions.

Crawford and Calo [

44] referred to a critical perspective on current trends in algorithms and artificial intelligence in industry. They argued that people fear that artificial intelligence is taking over human jobs, when, in fact, the problem is that industries often incorporate technology whose performance and effectiveness are not yet proven, without careful validation and reflection.

A lot of managers make decisions and analyze decision problems on the basis of their own intuition and creativity rather than on rational thinking [

42].

Some authors point out that their findings indicate that the financial information used in operational management is highly rated by managers when they focus on managers’ perceptions of the management accounting information systems in transition countries [

45].

Thus, managers’ opinions and perceptions play a very significant role in planning and making decisions of the companies, whilst providing us with plenty of information coming from their daily business lives.

Historically, the results obtained by [

46] show that decision-makers and users do not have much time for a thorough analysis and consultation of the results with researchers or other employees in the company.

In consequence, as Tversky and Kahneman proved a long time ago, human judgments which accompany decisions are frequently subject to systematic biases [

47].

On the other hand, a

t-test was conducted to specifically investigate if, in the USA, there are differences in microcredit repayment behavior between women and men. In order to analyze the significance of the difference between the means obtained by women and men in the responses to the survey, we will perform the

t-test [

48,

49]. In effect, to know if the variables “age”, “ethnicity”, “educational level”, “marital status”, “amount of the microcredit”, “term of the microcredit”, and “purpose of the microcredit” are affected by the sex of respondents, we will calculate the

t of the two samples (women and men), first to analyze if there are significant differences between the traits of the clients of the surveyed MFIs by sex, and then to analyze the perceived punctuality in microcredit repayment by clients.

For this purpose, the following two null hypotheses will be tested: (1) There is no significant difference in the averages of the traits of clients, and (2) there is no significant difference in perceived punctuality of microcredit repayment by clients. To do this, we first need to determine the standard error of the difference between the two means, which is also called the margin of error of the

t-test:

Second, we have to determine the ratio of the difference of the means to the margin of error, that is to say, the experimental value:

Third, the number of degrees of freedom is the total sample size minus two:

which is used in significance testing. Fourth, we determine the theoretical (critical) value

t at the 5% significance level and

degree of freedom. If

, the null hypotheses cannot be rejected and the difference of the means is due to randomness.

{kind=link}