Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment

Abstract

1. Introduction

2. Theory and Hypotheses

2.1. CSR

2.2. Corporate Performance Measurement

2.3. CSR and Corporate Performance in the Banking Industry

2.4. CSR and Customer’s Brand Trust

2.5. CSR and Customer’s Brand Loyalty

2.6. CSR and Customer’s Perception of Service Quality

2.7. CSR and Customer Satisfaction

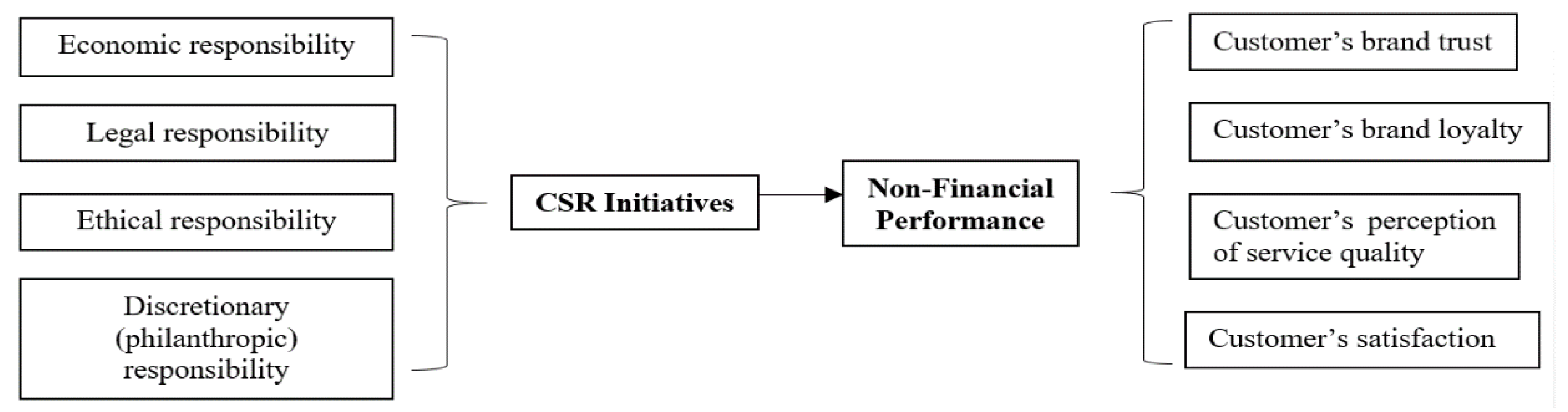

3. Research Model

Measurement of Constructs

- for firm i in year t, for firm i in year t,

- for firm i in year t, for firm i in year t, is a dummy that represents the year of information of firm i, and is the error term for firm i in year t.

4. Empirical Results

4.1. CSR and Financial Performance

4.2. CSR and Non-Financial Performance

4.2.1. Demographical Analysis

4.2.2. Descriptive Statistics and Exploratory Factor Analysis

4.2.3. Reliability Analysis

4.2.4. Regression Analysis

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Maignan, I.; Ferrer, O. Corporate social responsibility and marketing: An integrative framework. J. Acad. Mark. Sci. 2004, 32, 3–19. [Google Scholar] [CrossRef]

- Khan, I.; Kasliwal, N.; Joshi, M. Corporate social responsibility and consumer behavior: A review to establish a conceptual model. Int. J. Emerg. Res. Manag. Technol. 2017, 6, 142–148. [Google Scholar] [CrossRef]

- Tran, Q.; Le, T.; Huynh, L. Perception of bank customers towards banking corporate social responsibility in Vietnam. Int. Res. J. Financ. Econ. 2017, 161, 81–95. [Google Scholar]

- Chatterjee, C.; Lefcovitch, A. Corporate social responsibility and banks. Amic. Curiae. 2009, 78, 24–28. [Google Scholar] [CrossRef]

- Brown, T.; Dacin, P. The company and the product: Corporate associations and consumer product responses. J. Mark. 1997, 61, 68–85. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C. Corporate social responsibility, customer satisfaction, and market value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Li, F.; Minor, D.; Wang, J.; Yu, C. A learning curve of the market: Chasing alpha of socially responsible firms. J. Econ. Dyn. Control 2019. [Google Scholar] [CrossRef]

- Barriga Yumiguano, G.E.; González, M.G.; Torres, Y.A.; Zurita, E.G.; Pinilla Rodríguez, D.E. Desarrollo financiero y crecimiento económico en el Ecuador: 2000–2017. Rev. Espac. 2018, 39, 25–34. [Google Scholar]

- Freire, C.; Govea, K.; Hurtado, G. Incidencia de la responsabilidad social empresarial en la rentabilidad económica de empresas ecuatorianas. Rev. Espac. 2018, 39, 7–17. [Google Scholar]

- Bowen, H. Social responsibilities of the businessmen; Harper Brother: New York, NY, USA, 1953. [Google Scholar]

- Carroll, A. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Sethi, S. Dimensions of corporate social performance: An analytical framework. Calif. Manag. Rev. 1975, 17, 58–64. [Google Scholar] [CrossRef]

- Porter, M.; Kramer, M. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–90. [Google Scholar] [PubMed]

- Melo, T.; Garrido-Morgado, A. Corporate reputation: A combination of social responsibility and industry. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 11–31. [Google Scholar] [CrossRef]

- Nagler, J. Entrepreneurs: The world needs you. Thunderbird Int. Bus. Rev. 2012, 54, 3–5. [Google Scholar] [CrossRef]

- Hansen, S.; Dunford, B.; Boss, A.; Angermerier, I. Corporate social responsibility and the benefits of employee trust: A cross-disciplinary perspective. J. Bus. Ethics. 2011, 102, 29–45. [Google Scholar] [CrossRef]

- Arikan, E.; Güner, S. The impact of corporate social responsibility, service quality and customer-company identification on customers. Procedia Soc. Behav. Sci. 2013, 99, 304–313. [Google Scholar] [CrossRef]

- Valentine, S.; Fleischman, G. Ethics programs, perceived corporate social responsibility and job satisfaction. J. Bus. Ethics. 2008, 77, 159–172. [Google Scholar] [CrossRef]

- Carvalho, S.; Sen, S.; Mota, M.R.L. Consumer reactions to CSR: A Brazilian perspective. J. Bus. Ethics 2010, 91, 291–310. [Google Scholar] [CrossRef]

- He, H.; Li, Y. CSR and service brand: The mediating effect of brand identification and moderating effect of service quality. J. Bus. Ethics 2011, 100, 673–688. [Google Scholar] [CrossRef]

- Lee, E.; Park, S.; Rapert, M.; Newman, C. Does perceived consumer fit matter in corporate social responsibility issues. J. Bus. Res. 2012, 65, 1558–1564. [Google Scholar] [CrossRef]

- Marin, L.; Ruiz, S.; Rubio, A. The role of identify salience in the effects of corporate social responsibility on consumer behavior. J. Bus. Res. 2009, 84, 65–78. [Google Scholar]

- Stanaland, A.; Lwin, M.; Murphy, P. Consumer perceptions of the antecedents and consequences of corporate social responsibility. J. Bus. Ethics 2011, 102, 47–55. [Google Scholar] [CrossRef]

- Dunbar, C.; Li, Z.; Shi, Y. Corporate social responsibility and CEO risk-taking incentives. J. Corp. Financ. 2019. [Google Scholar] [CrossRef]

- Searcy, C. Corporate sustainability performance measurement systems: A review and research agenda. J. Bus. Ethics 2012, 107, 239–253. [Google Scholar] [CrossRef]

- Atkinson, G. Measuring corporate sustainability. J. Environ. Plan. Manag. 2000, 43, 235–252. [Google Scholar] [CrossRef]

- Alrubaiee, L. Exploring the relationship between ethical sales behavior, relationship quality, and customer loyalty. Int. J. Mark. Stud. 2012, 4, 7–25. [Google Scholar] [CrossRef][Green Version]

- Liu, T.; Wu, L. Customer retention and cross-buying in the banking industry: An integration of service attributes, satisfaction, and trust. J. Financ. Serv. Mark. 2007, 12, 132–145. [Google Scholar] [CrossRef]

- Roy, S.; Shekhar, V. Dimensional hierarchy of trustworthiness of financial service providers. Int. J. Bank Mark. 2010, 28, 47–64. [Google Scholar] [CrossRef]

- Matute-Vallejo, J.; Bravo, R.; Pina, J. The influence of corporate social responsibility and price fairness on customer behavior: Evidence from the financial sector. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 317–331. [Google Scholar] [CrossRef]

- McDonald, L.; Rundle-Thiele, S. Corporate social responsibility and bank customer satisfaction: A research agenda. Int. J. Bank Mark. 2008, 26, 170–182. [Google Scholar] [CrossRef]

- Decker, S.; Sale, C. An analysis of corporate social responsibility, trust and reputation in the banking profession. In Professionals’ Perspectives of Corporate Social Responsibility; Springer: Berlin, Germany, 2009; pp. 135–156. [Google Scholar]

- Spence, A. Competitive and optimal responses to signals: An analysis of efficiency and distribution. J. Econ. Theory 1974, 7, 296–332. [Google Scholar] [CrossRef]

- Yoon, Y.; Gurhan-Canli, Z.; Schwarz, N. The effect of corporate social responsibility (CSR) activities on companies with bad reputations. J. Consum. Psychol. 2006, 16, 377–390. [Google Scholar] [CrossRef]

- Frank, R.; Massy, W.; Lodahl, T. Purchasing behavior and personal attributes. J. Advert. Res. 1969, 9, 15–24. [Google Scholar]

- Bartol, K.; Martin, D. Management; McGraw-Hill Company: New York, NY, USA, 1994. [Google Scholar]

- Chiou, J.; Droge, C. Service quality, trust, specific asset investment, and expertise: Direct and indirect effects in satisfaction-loyalty framework. J. Acad. Mark. Sci. 2006, 34, 613–627. [Google Scholar] [CrossRef]

- Reichheld, F. The Loyalty Effect: The Hidden Force behind Growth, Profits, and Lasting Value; Harvard Business School Press: Boston, MA, USA, 1996. [Google Scholar]

- Aaker, D. Managing Brand Equity: Capitalizing in the Value of a Brand Name; The Free Press: New York, NY, USA, 1991. [Google Scholar]

- Fornell, C.; Wernerfelt, B. Defensive marketing strategy by customer complaInt. management: A theoretical analysis. J. Mark. Res. 1987, 24, 337–346. [Google Scholar] [CrossRef]

- Dick, A.; Basu, K. Customer loyalty: Toward an integrated conceptual framework. J. Acad. Mark. Sci. 1994, 22, 99–113. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.; Berry, L. SERVQUAL: A multi-item scale for measuring consumer perceptions of service quality. J. Retail. 1988, 64, 12–40. [Google Scholar]

- Zeithaml, V.; Berry, L.; Parasuraman, A. The behavioral consequences of service quality. J. Mark. 1996, 60, 31–46. [Google Scholar] [CrossRef]

- Mohr, L.; Webb, D. The effects of corporate social responsibility and price on consumer responses. J. Consum. Aff. 2005, 39, 121–147. [Google Scholar] [CrossRef]

- Boshoff, C.; Gray, B. The relationship between service quality, customer satisfaction and buying intentions in the private hospital industry. South Afr. J. Bus. Manag. 2004, 35, 27–37. [Google Scholar] [CrossRef]

- Chung, K.-H.; Yu, J.-E.; Choi, M.-G.; Shin, J.-I. The effects of CSR on customer satisfaction and loyalty in China: The moderating role of corporate image. J. Econ. Bus. Manag. 2015, 3, 542–547. [Google Scholar] [CrossRef]

- Carroll, A.; Shabana, K. The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Anderson, R.; Srinivasan, S. E-satisfaction and e-loyalty: A contingency framework. Psychol. Mark. 2003, 20, 123–138. [Google Scholar] [CrossRef]

- Cowart, K.; Fox, G.; Wilson, A. A structural look at consumer innovativeness and self-congruence in new product purchase. Psychol. Mark. 2008, 25, 1111–1130. [Google Scholar] [CrossRef]

- Ishaq, M. Perceived value, service quality, corporate image and customer loyalty: Empirical assessment from Pakistan. Serbian J. Manag. 2012, 7, 25–36. [Google Scholar] [CrossRef]

- Kaur, H.; Soch, H. Validating antecedents of customer loyalty for Indian cell phone users. Vikalpa. 2012, 37, 47–61. [Google Scholar] [CrossRef]

- Lee, Y.; Lee, C.; Lee, S.; Babin, B. Festivalscapes and patrons’ emotions, satisfaction, and loyalty. J. Bus. Res. 2008, 61, 56–64. [Google Scholar] [CrossRef]

- Lin, C. Webcasting adoption: Technology fluidity, user innovativeness, and media substitution. J. Broadcast. Electron. Media. 2004, 48, 446–465. [Google Scholar] [CrossRef]

- Li, F. Endogeneity in CEO power: A survey and experiment. Investig. Anal. J. 2016, 45, 149–162. [Google Scholar] [CrossRef]

- Tulcanaza-Prieto, A.; Koo, J.; Lee, Y. Does cost stickiness affect capital structure? Evidence from Korea. Korean J. Manag. Account. Res. 2019, 19, 27–57. [Google Scholar] [CrossRef]

- Ecuadorian Superintendence of Banks. Managerial Report from Monthly Financial Newsletters. Available online: http://estadisticas.superbancos.gob.ec/portalestadistico/portalestudios/?page_id=415 (accessed on 10 May 2019).

- Chen, E.; Dixon, W. Estimates of Parameters of a Censored Regression Sample. J. Am. Stat. Assoc. 1972, 67, 664–671. [Google Scholar] [CrossRef]

- Wu, M.W.; Shen, C.H. Corporate social responsibility in the banking industry: Motives and financial performance. J. Bank Financ. 2013, 37, 3529–3547. [Google Scholar] [CrossRef]

- Djalilov, K.; Vasylieva, T.; Lyeonov, S.; Lasukova, A. Corporate social responsibility and bank performance in transition countries. Corp. Ownersh. Control. 2015, 13, 879–888. [Google Scholar] [CrossRef]

- Ashraf, M.; Khan, B.; Tariq, R. Corporate social responsibility impact on financial performance of bank’s: Evidence from Asian countries. Int. J. Acad. Res. Bus. Soc. Sci. 2017, 7, 618–632. [Google Scholar]

- Fayad, A.; Ayoub, R.; Ayoub, M. Causal relationship between CSR and FB in banks. Arab. Econ. Bus. J. 2017, 12, 93–98. [Google Scholar] [CrossRef]

- Hair, J.; Black, W.; Babin, B.; Anderson, R. Multivariate Data Analysis, 7th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Chin, W. The partial least squares. approach to structural equation modeling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Lawrence Erlbaum Associates: London, UK, 1998; pp. 295–336. [Google Scholar]

- Baron, R.; Kenny, D. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Daub, C.; Ergenzinger, R. Enabling sustainable management through a new multi-disciplinary concept of customer satisfaction. J. Mark. 2005, 39, 998–1012. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Constructs | Items | Label | Related Literature |

|---|---|---|---|

| Demographic information | Gender, age, occupation, level of education, and banking entity. | Nominal scale | |

| CSR knowledge | Are you familiarized with the definition of CSR? | CSR1, CSR2 [32,47], CSR3 | |

| Customer’s brand trust (TRU) | In general, I trust my bank. | Tru1 | [2,33,34] |

| My bank is an honest entity and treats me fairly and justly. | Tru2 | ||

| I believe faithfully in the financial and service information provided by my bank. | Tru3 | ||

| When I have a problem with the bank, its staff responds with sufficient consideration and clarifies my doubts. | Tru4 | ||

| Customer’s brand loyalty (LOY) | I am a loyal customer of my bank. | Loy1 | [48,49,50] |

| When I have the possibility, I manifest attributes (positive things) of my bank. | Loy2 | ||

| I will recommend my bank to other people. | Loy3 | ||

| I will continue to do more business with my bank in the future. | Loy4 | ||

| Customer’s perception of service quality (QUA) | My bank provides caring and individualized attention to customers. | Qua1 | [17,42,50] |

| The workers of my bank treat me with courtesy. | Qua2 | ||

| My bank call center provides efficient and effective answers to any problem. | Qua3 | ||

| My bank provides me with good quality financial services fast. | Qua4 | ||

| Customer satisfaction (SAT) | Overall, my feeling with this bank is satisfactory. | Sat1 | [48,51,52] |

| My bank is one of the best five entities in the entire national financial system. | Sat2 | ||

| I would choose this bank again. | Sat3 | ||

| Overall, I am satisfied with the CSR activities of my bank. | Sat4 | ||

| Economic responsibility (ECO) | My bank has a strong competitive position in the Ecuadorian financial market. | Eco1 | [46,47,53] |

| My bank promotes financial innovation through the inclusion of fresh financial products and services. | Eco2 | ||

| Investments and deposits in my banking institution are profitable to me (payment of interest and financial costs according to the law). | Eco3 | ||

| My bank quickly incorporates new technologies (mobile application, instant messaging, cash management, data encryption) into the financial service compared to other national banking entities. | Eco4 | ||

| Legal responsibility (LEG) | My bank promotes policies and executes controls to avoid money laundering (request of origin and destination of funds when a certain amount is exceeded in transactions). | Leg1 | [46,47] |

| My bank keeps the secrecy of my financial information (confidentiality—it does not reveal my personal financial information). | Leg2 | ||

| My bank obeys and respects national laws and regulations. | Leg3 | ||

| My bank meets minimal legal requirements related to financial services. | Leg4 | ||

| Ethical responsibility (ETH) | My bank owns and executes ethical standards within the business of financial intermediation (i.e., does not encourage over-indebtedness, transparent information, fair, and equal treatment). | Eth1 | [46,47] |

| My bank operates with transparency, providing full and accurate information when I require it. | Eth2 | ||

| My bank has been involved in scandals regarding financial mismanagement and/or legal problems. | Eth3 | ||

| My bank has mission, vision, and institutional values and they have been socialized with me. | Eth4 | ||

| Philanthropic (discretionary) responsibility (PHI) | My bank promotes financial inclusion for vulnerable groups. | Phi1 | [46,47] |

| My bank participates in charitable activities and combines them with its commercial activities. | Phi2 | ||

| My perception of the degree of education and specialization of the staff of my bank is high (i.e., the staff of my bank is continuously trained in financial, legal, and customer service issues). | Phi3 | ||

| I have observed/heard that my bank helps communities in need (i.e., disadvantaged people, disaster relief, anti-drug plans, and educational scholarship). | Phi4 | ||

| Variables | Model 1—Equation (1) | Model 2—Equation (2) | ||

|---|---|---|---|---|

| ROA | ROE | ROA | ROE | |

| Education | 0.0003 *** | 0.0016 *** | ||

| (2.706) | (4.537) | |||

| Housing | 0.0042 ** | 0.0096 | ||

| (2.018) | (1.646) | |||

| Microenterprise | 0.0003 *** | 0.0007 *** | ||

| (2.631) | (2.592) | |||

| CSR Initiatives | 0.0001 ** | 0.0005 *** | ||

| (2.257) | (3.364) | |||

| Size | 0.0038 *** | 0.0196 *** | 0.0036 *** | 0.0193 *** |

| (9.852) | (18.519) | (9.620) | (18.313) | |

| Intercept | 0.0677 *** | 0.3224 *** | 0.0654 *** | 0.3163 *** |

| (9.166) | (15.706) | (8.917) | (15.468) | |

| Year-fixed effects | Yes | Yes | Yes | Yes |

| Adjusted R-Square | 0.148 | 0.367 | 0.140 | 0.356 |

| F-Statistics | 18.950 *** | 63.526 *** | 26.883 *** | 91.028 *** |

| Durbin-Watson | 1.617 | 1.557 | 1.623 | 1.560 |

| N | 304 | |||

| Constructs | Label | Mean | Std. Deviation | Variance | Composite Mean | Factor Loadings |

|---|---|---|---|---|---|---|

| Customer’s brand trust (TRU) | Tru1 | 3.912 | 0.911 | 0.829 | 3.825 | 0.773 |

| Tru2 | 3.737 | 0.998 | 0.997 | 0.798 | ||

| Tru3 | 3.825 | 0.955 | 0.912 | 0.752 | ||

| Customer’s brand loyalty (LOY) | Loy1 | 4.000 | 0.975 | 0.952 | 3.962 | 0.734 |

| Loy2 | 3.719 | 1.078 | 1.163 | 0.786 | ||

| Loy3 | 3.851 | 0.973 | 0.947 | 0.742 | ||

| Loy4 | 4.276 | 0.767 | 0.589 | 0.701 | ||

| Customer’s perception of service quality (QUA) | Qua1 | 3.860 | 1.057 | 1.117 | 3.885 | 0.663 |

| Qua2 | 4.149 | 0.903 | 0.815 | 0.775 | ||

| Qua3 | 3.702 | 1.164 | 1.356 | 0.702 | ||

| Qua4 | 3.829 | 1.012 | 1.023 | 0.757 | ||

| Customer satisfaction (SAT) | Sat1 | 3.974 | 0.839 | 0.704 | 3.798 | 0.683 |

| Sat2 | 3.820 | 1.032 | 1.064 | 0.784 | ||

| Sat3 | 3.930 | 1.009 | 1.017 | 0.758 | ||

| Sat4 | 3.469 | 1.112 | 1.237 | 0.740 | ||

| Economic responsibility (ECO) | Eco2 | 4.048 | 0.901 | 0.813 | 3.537 | 0.765 |

| Eco3 | 3.026 | 1.330 | 1.770 | 0.704 | ||

| Legal responsibility (LEG) | Leg2 | 3.689 | 1.229 | 1.511 | 4.026 | 0.664 |

| Leg3 | 4.096 | 0.966 | 0.933 | 0.731 | ||

| Leg4 | 4.294 | 0.838 | 0.702 | 0.786 | ||

| Ethical responsibility (ETH) | Eth2 | 3.855 | 1.087 | 1.182 | 3.803 | 0.752 |

| Eth4 | 3.750 | 1.200 | 1.439 | 0.777 | ||

| Philanthropic (discretionary) responsibility (PHI) | Phi1 | 3.259 | 1.134 | 1.285 | 3.165 | 0.822 |

| Phi2 | 3.263 | 1.165 | 1.358 | 0.802 | ||

| Phi4 | 2.974 | 1.283 | 1.647 | 0.852 |

| Var. | Items | CA | CR | AVE | Correlations | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Tru | Loy | Qua | Sat | Eco | Leg | Eth | Phi | |||||

| Tru | 3 | 0.859 | 0.818 | 0.600 | (0.775) | |||||||

| Loy | 4 | 0.748 | 0.830 | 0.550 | 0.622 *** | (0.741) | ||||||

| Qua | 4 | 0.794 | 0.816 | 0.526 | 0.591 *** | 0.572 *** | (0.726) | |||||

| Sat | 4 | 0.819 | 0.830 | 0.551 | 0.604 *** | 0.692 *** | 0.632 *** | (0.742) | ||||

| Eco | 2 | 0.715 | 0.701 | 0.541 | 0.643 *** | 0.615 *** | 0.567 *** | 0.668 *** | (0.735) | |||

| Leg | 3 | 0.762 | 0.772 | 0.531 | 0.537 *** | 0.503 *** | 0.559 *** | 0.596 *** | 0.405 *** | (0.729) | ||

| Eth | 2 | 0.793 | 0.738 | 0.585 | 0.616 *** | 0.536 *** | 0.613 *** | 0.657 *** | 0.557 *** | 0.558 *** | (0.765) | |

| Phi | 3 | 0.840 | 0.865 | 0.682 | 0.532 *** | 0.409 *** | 0.460 *** | 0.569 *** | 0.602 *** | 0.409 *** | 0.648 *** | (0.826) |

| Hypothesis | Prop Effect | Adj. R2 | Durbin Watson | F | Constant | β | Test Results |

|---|---|---|---|---|---|---|---|

| H1a. CSR→ NFCP | + | 0.657 | 2.054 | 435.891 *** | 1.233 *** (9.5553) | 0.725 *** (20.878) | Supported |

| H1b. ECO→ NFCP | + | 0.515 | 1.946 | 242.029 *** | 2.069 *** (17.256) | 0.508 *** (15.557) | Supported |

| H1c. LEG→ NFCP | + | 0.399 | 2.030 | 151.904 *** | 1.774 *** (10.221) | 0.520 *** (12.325) | Supported |

| H1d. ETH→ NFCP | + | 0.488 | 2.007 | 217.721 *** | 1.967 *** (14.809) | 0.500 *** (14.755) | Supported |

| H1e. PHI→ NFCP | + | 0.323 | 1.812 | 109.270 *** | 2.667 *** (22.080) | 0.379 *** (10.453) | Supported |

| H2. CSR→ TRU | + | 0.518 | 2.200 | 245.210 *** | 0.965 *** (5.167) | 0.787 *** (15.659) | Supported |

| H3. CSR→ LOY | + | 0.403 | 1.966 | 154.193 *** | 1.805 *** (10.163) | 0.594 *** (12.417) | Supported |

| H4. CSR→ QUA | + | 0.458 | 2.008 | 192.529 *** | 1.285 *** (6.706) | 0.716 *** (13.875) | Supported |

| H5. CSR→ SAT | + | 0.592 | 1.985 | 330.706 *** | 0.876 *** (5.333) | 0.804 *** (18.185) | Supported |

| Variable | Proposed Effect | NFCP Model | Testing Hypothesis |

|---|---|---|---|

| ECO | + | 0.310 *** (9.200) | Supported |

| LEG | + | 0.240 *** (6.635) | Supported |

| ETH | + | 0.211 *** (5.505) | Supported |

| PHI | + | 0.103 *** (3.077) | Supported |

| Constant | 1.010 *** (7.623) | ||

| Adj. R2 | 0.701 | ||

| Durbin Watson | 2.144 | ||

| F-statistics | 133.746 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tulcanaza-Prieto, A.B.; Shin, H.; Lee, Y.; Lee, C.W. Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment. Sustainability 2020, 12, 1621. https://doi.org/10.3390/su12041621

Tulcanaza-Prieto AB, Shin H, Lee Y, Lee CW. Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment. Sustainability. 2020; 12(4):1621. https://doi.org/10.3390/su12041621

Chicago/Turabian StyleTulcanaza-Prieto, Ana Belen, HoKyun Shin, Younghwan Lee, and Chang Won Lee. 2020. "Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment" Sustainability 12, no. 4: 1621. https://doi.org/10.3390/su12041621

APA StyleTulcanaza-Prieto, A. B., Shin, H., Lee, Y., & Lee, C. W. (2020). Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment. Sustainability, 12(4), 1621. https://doi.org/10.3390/su12041621