1. Introduction

As a part of the shift of technology in the financial business, mobile financial services have been exploring at an accelerate speed [

1]. Innovations and technological expansion have emerged with significant advantages to the recent commercial market. Over the past few years, businesses have been redirecting their goals to making information system technology an essential part of their processes [

2]. Therefore, more and more literature is diverted to the IS-related field [

3]. The investigation of some existing studies which recommend integrating various theoretical models to understand the IT adoption has stressed that a comprehensive analysis in the context is required [

2,

4]. From these perspectives, an increasing number of researchers are focused on mobile financial services (MFS) considered as the development of the information system (IS) domain [

5,

6,

7,

8].

MFS refers to any financial transaction remotely conducted by the application of a mobile phone (e.g., smartphone or tablet) and mobile software (e.g., apps programs) either through banking service or network provider service [

9,

10]. MFS providers allow their consumers the flexibility to access their financial services (access information inquiry, bill payment, and money transfers) anywhere and anytime via a mobile phone, to support and improve service relationships by investing lots of resources using wireless Internet technology [

11].

The studies of MFS that emphasized on electronic money transfer include three major mobile technologies-related fields of study, primarily mobile banking services (MB), mobile payment services (MP), and mobile money transfer (MMT) services [

10]. MB remains part of the latest in a sequence of new mobile technological wonders [

12]. Therefore, an expectation toward it should be for a significant impact on the market [

13]. Payment today has now progressed to mobile devices (m-devices) identified as mobile financial services, particularly mobile payments [

14]. Mobile money has appeared as a significant innovation with a potential expansion to financial inclusion in developing countries in various ways [

15]. It is, therefore, growing access to financial services for a large number of people, who are entirely disregarded by banks because of longer travel distances or insufficient funds to fulfill the minimum deposit recommended for opening account in a bank [

16,

17], low-income population in developing countries [

18], insofar, as it has several advantages [

15,

19,

20]. In addition to the advantages granted to certain persons and companies, there are also advantages at the national economy level, primarily in emerging economies such as Hungary. The use of increasingly more accommodating tools may incentivize the suppressed use of cash, parallel to which, the countability of economic performance with statistical instruments continues to improve; meanwhile tax payment discipline also improves and the total social cost of payments decreases, etc., that is, overall the economy begins to whiten, leading to improved competitiveness [

21].

While tremendous benefits are associated with adopting MFS as opposed to traditional payment methods, such as physical exchange notes, cheques, coins [

18], the adoption rate is far from full utilization in many developing countries. This is characteristically the situation of West African Countries and particularly Togo. Given the statistical information on the Statista Portal (2016), the population using smartphones worldwide is predicted to be over five billion marks in 2019. Approximately 67% of the Togolese population subscribed to the mobile phone in 2015, while users of mobile Internet doubled between 2014 and 2015. However, the percentage rate of users of banking services is less than 15% [

22] and, the rate of consumer acceptance of mobile banking remains trivial (around 1%) when considering the expectation [

23]. It is, therefore, leading to deduct that mobile money services should fill this lacuna by providing significant input to increase the acceptance of MFS. This hope is far from being the case. The experiences of more developed countries also suggest the same, not technological limitations were the primary obstacle of the extension of the innovative payment solutions [

24]. Therefore, the motives for the successful evolution or not together with the causes and motives for mobile money adoption, remain not understood sufficiently, which infers that the technology has not been extensively adopted. These trends reveal partial knowledge regarding the motivators and inhibitors that impact the acceptance of this mobile service [

25].

Understanding why it is worth to select to use MFS can help in strategy development and allow businesses to effectively communicate benefits to their customers [

26,

27]. Mobile financial service operators might increase their attractiveness and competitiveness if they were able to enhance their strategies to satisfy the demand of their consumers. Therefore, there is a necessity of understanding the various requirements of MFS users and the comparative weight of each factor or criteria that could affect the demand of consumers. One possible motive for the existence of a gap between these could be the perception of risk that limits consumers’ capability to make informed decisions to partake the benefit of MFS technology in Togo [

28]. This is particularly true for emerging nations, mainly in an unstable country where the consideration of the loss of privacy in the security system and the associated risk played a crucial part in adopting IT [

29]. Moreover, the studies in the past revealed that once there are risk issue concerns, the demand for trust becomes a necessity, since trust and risk are interrelated facets [

28,

30]. Not only the developing countries facing the issue of e-business but also the reflection of the online risk has called for a considerable attention among the developed countries like Hungary, particularly in 2014 when the case of fraud risk in electronic payment transactions ascended in Hungary (the case was discussed in the work of Kovács and David in detail [

31]).

Driven by studies toward the multiple scopes for risk and trust and the central research on trust in contrast to risk in novel information technology perspective [

32], we suppose that initiating research into novel IT artifacts such as this research could enlighten how trust and perceived risk could influence the ultimate adoption of novel technologies in developing countries.

The goal of this study is to disclose mechanisms related to behavior associated with MFS adoption and sustainable development when decision-making involves multiple criteria issues. One main research question is to understand how multi-dimensional trust and multi-faceted perceived risk perceptions affect a new emerging information technology such as MFS adoption at the individual level in an unstable country. Our approach differs from most prior studies that assess trust and risk perception of individual behavior. Indeed, most of the research that investigated the acceptance and application of communicative IT has been done within stable, capitalist, and highly-developed communities. Moreover, the majority of research undertakes that individuals have freedom of speech, and safety of their lives, basic protection and business offered by the government. However, little has been known regarding the adoption of IT in emerging and dynamic societies [

33,

34]. Therefore, we explore the fundamental trust and risk allied with MFS technology usage in high poverty.

The majority of prior research typically tests trust as a single construct [

35,

36,

37] or investigates trust constructs and risk dimensions disjointedly [

27,

38]. In other words, how to effectively assess trust and risk concerns concurrently remains a black box. Drawing on research in information technology [

39,

40], we stress that multi-dimensional trust and perceived risk concepts may jointly play an integral part in individual behavior with regard to adopting a novel MFS, and it is of paramount importance for this to be investigated, particularly in developing countries such as Togo.

Furthermore, a plethora of research has been done in order to fully understand the factors that affect MFS adoption and its significance. However, most prior studies in this perspective have emphasized the general factors regarding the adoption of MFS, using explanatory statistical analysis as the research method [

41,

42]. The beta coefficients gained in multiple regression techniques can be considered as the relative weights of the constructs, however, their values are obtained indirectly via the testing result. Additionally, a negative value of beta can be found, making it quite complex for the justification of the importance of the resultant value [

43]. Making decisions has continually been an essential activity in day to day life. Therefore, using services such as MFS necessitates a careful decision from an individual so that he/she would not regret his/her decision, ever since decision-making has emerged as a mathematical science today [

44]. From there, multiple criteria decision-making (MCDM) techniques constitute a critical framework through which companies focus on which strategy to implement to meet the needs of consumers, to acquire the appropriate income, and to prosper in the competitive milieu [

45].

In order to advance current IS researches, Esearch and Koppius [

46] stressed that there is a necessity to integrate decision modeling methods in IS research to generate data estimates as well as methods for assessing the analytical power of the result. Therefore, applying a combined analytic method stressed how integrating two or multiple data analysis techniques in either methodology or investigation can patronize the confidence and validity in the resulting outcome [

15,

47]. Additionally, most managers make strategic decisions based on a single goal or dimension, but strategic planning is impacted by many different factors and regarded from several perspectives [

48]. As the traditional notion of strategic planning lacks multidimensional prominence, this paper integrates the structural equation modeling and technique for order preference by similarity to ideal solution (SEM-TOPSIS) method to construct the relationships between decision factors for MFS adoption, while classifying the alternative of MFS. It is a unique decision support technique grounded in structural modeling.

The primary objectives of this research are: To explore the influential antecedent of trust and risk perception at the multidimensional level regarding MFS adoption in Togo; to propose and validate model MFS acceptance using an SEM technique by employing data collected through experts of MFS and MFS experienced users; to develop an SEM-TOPSIS-based model for multi-criteria decision-making by selecting the appropriate MFS type for MFS, grounded in experts’ view, and by prioritizing the operative trust-risk factors while exposing the veiled relationship among the factors that influence customers in the MFS. The present study has the following contributions.

Primarily, a growing number of recent studies link the multiple criteria decision-making (MCDM) techniques to financial decision making [

49]. In the majority of cases, the traditional model of MCDM considers the criteria (factors) are independently and hierarchically organized. Nevertheless, problems are often organized by interdependent criteria and dimensions and might even reveal feedback-like effects [

50]. TOPSIS is one of the most extensively adopted decision methodologies in technology, engineering, management, science, and business. TOPSIS approaches, as part of MCDM, have an impact on improving the quality of decisions by generating the development more efficient, rational, and explicit. However, previous works have not sufficiently kept pace. Thus, we believe that there is a necessity for the methodical integration of SEM-TOPSIS to merge a recent study performed in this field of study. This study incorporates a complex multi-criteria decision-making problem by assessing types of multidimensional trust and risk in MFS that have rarely been investigated and touched in past studies. As such, a literature review is conducted, and then SEM analysis is used to construct a hierarchical structure for trust and risk factors, which includes a total of ten sub-factors. According to the identified criteria and sub-criteria and by considering relationships among them, TOPSIS is adopted for selecting the appropriate types of MFS, based on the critical factors that influence customers’ trust and risk. Hence, the study contributes by proposing a solution that could effectively enhance trust and mitigation-perceived risk measures through a multi-level approach considered as a new added concept to planning strategy from the MFS perspective.

Second, one of the contributions of this research is based on the comparison of the results of both TOPSIS and analytical hierarchical process (AHP) technique, for a given model, to inspect if there are, indeed, noteworthy differences. The result of AHP is derived from the earlier work of Gbongli [

10] in which the SEM-AHP technique has been applied for assessing the issues of risk and trust using the specified population. Similarly, the main work is derived from previous work in which SEM-TOPSIS has been extensively adopted on the equal given population [

51]. As a result, this study shows that both approaches achieved comparable results and were well consistent and, in general, agreed with each other. In other words, both methods classify mobile money services as the most important MFS used, followed by mobile payment as the second and mobile banking as the last. However, the TOPSIS method is better suited to the problem of MFS selection for this study area since AHP requires a long process of pairwise comparison, and the requirement of the consistency ratio should also be considered in the process. The paper provides a detailed methodology application that could provide very useful insights for managers and researchers for their specific application.

The remainder of this paper is structured as follows. In

Section 2, we offer a succinct overview of the literature and theory review. For

Section 3, we present the theoretical framework. In

Section 4, the description of the research methodology and the procedure of this research are presented.

Section 5 provides findings based on the research objectives. We conclude the work with discussions of the findings, implications, limitations, and future study suggestions.

6. Discussion

New technology adoptions are impacted mainly by many factors, which may vary from technology concerns to the trust dimension, the perception of risk facets, and the behavior of users, to mention a few. The intricacy and significance related to the effort in elucidating the motives or reasons for users’ adoption or rejection of new IT have led to the development of various concepts. Furthermore, there are a plethora of studies on the influence of trust and perceived risk with their determinant toward the adoption decision in an online environment.

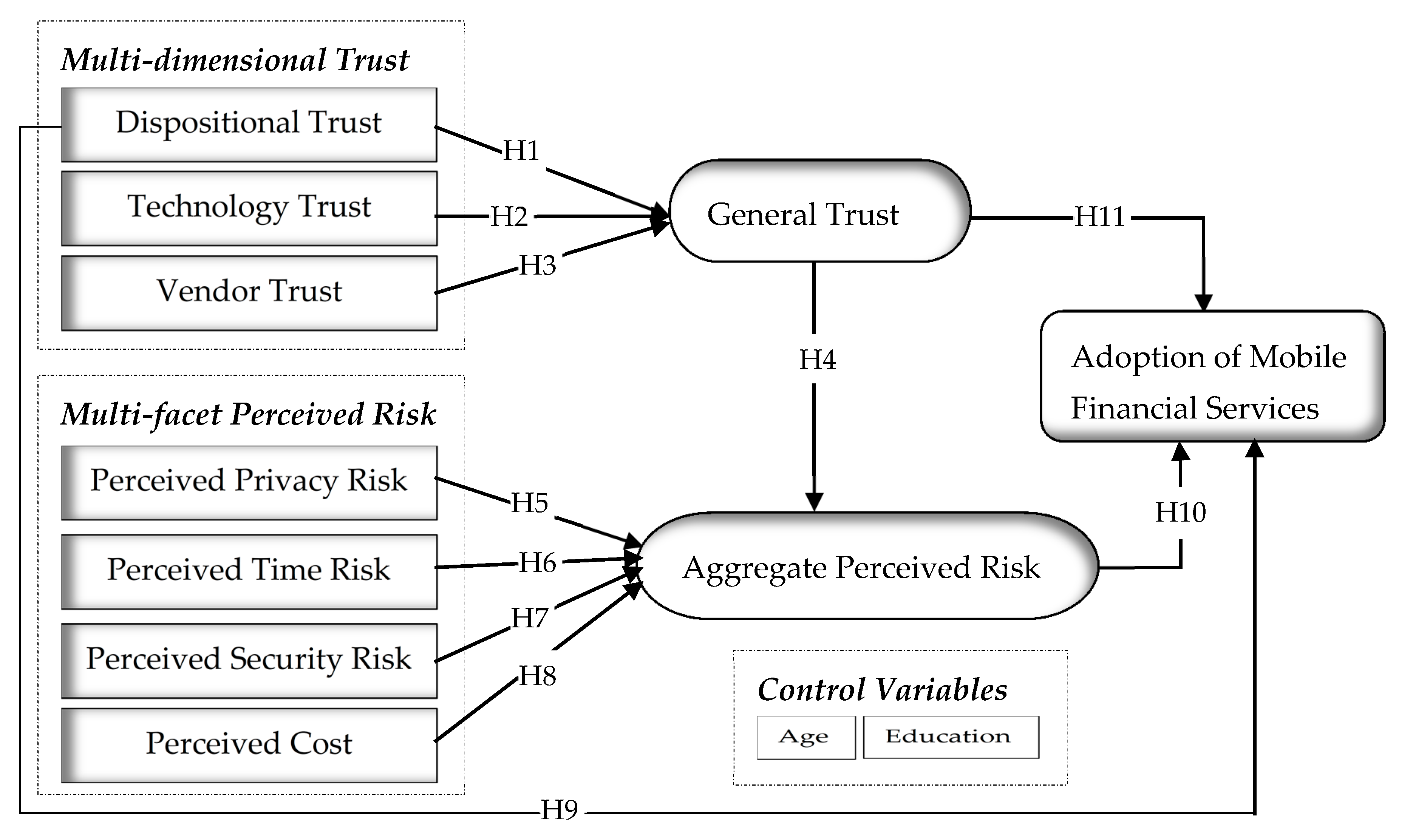

Conversely to prior research works, this study scrutinizes the influence of critical variables such as multi-dimensional trust and perceived risk facets on the consumers’ adoption behavior of MFS and incorporates each of them into the MFS alternative decision-making scenario. Some postulations were made toward the possible relationship among the factors. The findings are yet to be probed purposively to draw an important conclusion and implication. The result of the MFS structural model analysis regarded as a final model after validation is summarized and portrayed in

Figure 2. To be specific, the discussion section is scheduled to be under two sections. The first section will be made with SEM methodology grounded on hypotheses results, which are comprised of three sets. First set: hypotheses associated with trust; second set: hypotheses associated with perceived risk; and third set: hypotheses associated with MFS adoption constructs. The last section of the discussion is booked for a succinct analysis of TOPSIS output obtained via the SEM-TOPSIS hybrid technique.

It should be mentioned that all hypotheses were tested when controlling for age and education. The reason for controlling variables is to support mitigating the unrelated effect. Moreover, its use contributes to improving the robustness and validity of the outcome. In terms of relationships, the study account for the

p-value column allied with each variable where the related

p-value of less than 0.05 indicates a significant relation associated. The results of the entire tested eleven hypotheses were statistically significant except for the relationship between perceived time risk (PTimeR) and perceived risk (PRisk, i.e., H6 as displayed from

Figure 2).

The first set of hypotheses is related to trust, which was scrutinized by H1–H3. Empirical evidence is found to accept hypothesis H1 (β = 0.207,

p < 0.001), which refers to the positive effect the disposition to trust has on general trust in MFS. Payne and Clark [

190] showed that the general disposition to trust exerts substantial control on the trust among senior managers in an industrial context. Moreover, consumers’ disposition to trust has been revealed to maintain a strong influence on their trust in an e-vendor. Although most of the previous studies did not plainly define the direction of the impact, the present study ratifies that disposition to trust and trust are positively related in MFS. Such information comes to back the knowledge that consumers who unveil a greater disposition to trust will more willingly trust the e-vendor [

137] compared to those who will require more info [

191]. However, our results are contradicted by earlier e-services [

110], particularly in mobile banking. The reason might be that when consumers are to encounter a choice within MFS perspectives (mobile banking, mobile payment, mobile money), their trust disposition significantly affects the general trust more or less that of the single type of MFS. As a result, companies dealing with MFS should be aware of this critical effect and prepare for any competitive advantage strategies in the marketplace.

H2 (β = 0.222,

p < 0.001) tested the effect of trust in technology on trust in general, and the findings stressed that technology trust has a strong positive impact on trust. Given technological trust as a sole antecedent of trust whereby the object upon which the trust remained imparted when referring to the inert technology [

192], then, our empirical results are in line with previous findings in the context of mobile banking [

110]. Furthermore, previous works [

193] implicitly incorporated the concept of trust technology to trust with its importance being emphasized as a facilitator of e-commerce adoption.

Trust in the vendor was also found to have a positive influence on general trust, which supports H3 (β = 0.251,

p < 0.001). The results of this research are reliable with the previous finding in which vendor trust has been defined as multi-dimensional and influential levers that the vendors could employ to build consumer trust [

113]. Vendor trust remains so vital to promoting trust in changing a potential consumer from a curious viewer to one that will be ready to perform MFS. Thoughtful discerning of the essence and antecedents of consumer trust in MFS can support e-vendors with a set of controllable, strategic levers to develop such trust, which will encourage greater MFS acceptance and usage.

As a result, lack of consumer trust (trust disposition, technology trust, and vendor trust) in the overall online environment has been, and persists in being, a hamper to IS adoption [

194] and thus to MFS. All these could serve as a clue to the concept that the consumers’ espousal of MFS may be shaped accordingly.

The second set of hypotheses is associated with perceived risk. From this part, perceived risk has five antecedents, such as H4 and H5–H8. The investigation of the relationship between trust and perceived risk has been one of the main issues in the development of IS [

195]. Our result shows that general trust has a negative influence on perceived risk, which supports H4 (β = −0.070,

p < 0.05). The literature offers supportive studies on the import of this relationship [

8,

195]. Various researchers have also contributed to the belief that trust mitigates consumers’ perceived risk [

196,

197,

198] as well as affecting perceived benefit in e-commerce [

199]. Lots of incentives that increase trust are similar incentives that reduce perceived risk. This result clarifies to some extent, the doubt related to the direction of the causality between trust and risk, which were found deficient from the past literature [

121]. From H5–H8, the empirical study found to patronize all the hypotheses at a different level of

p-value mention that each dimension of perceived risk has a positive influence on the overall perceived risk except H6 (see

Figure 2). At that point, the moderate to weak positive relationships between the perceived risk (aggregate) and the risk component offers further reinforcement that risk can be researched as a multidimensional phenomenon [

200]. These results are also consistent with the work of Featherman and Pavlou [

127], which validated a majority of these antecedents as a risk dimension; therefore, being the influential element of the aggregated risk. Again, the outcomes reveal the multidimensional nature of perceived risk in information technology, mainly MFS. Boksberger et al. [

201] are supporters of these findings in the area of air travel. Again, the results show that perceived privacy risk H5 (β = 0.309,

p < 0.001) is indeed the predominant perceived risk dimension for the partakers of MFS, shadowed by the perceived cost H8 (β = 0.146,

p < 0.001) and perceived security risk H7 (β = 0.142,

p < 0.001). Moreover, this study confirms the positive effect of the perceived cost on the consumers’ perceived risk, such as that the lower the cost, the more minor the perception of risk and the more the likelihood of MFS adoption. As such, the involvement aspect of the risk [

202] is importantly observed when the price or cost is high, and the consumers risk losing money.

This research reveals no statistical evidence to support the hypothesis H6 (β = 0.032,

p < 0.342) that perceived time risk has a positive influence on the aggregate perceived. Although H6 is rejected; the expected direction of the relationship is kept just so that the

p-value is not statistically significant at 0.05. However, our findings are controverted by prior online payment research that has indicated a positive relationship between time risk and perceived risk [

203]. It has stressed that consumers lack patience in waiting a long time because they are always delighted in pursuing new things [

203]. Then, a longer waiting time for service delivery would deter the desire, impact their buying disposition or decision to adopt as well. In the view of this current study, the perceived risk dimension, such as perceived time risk, does not appear to impact the specific information technology acceptance, at least for the Togolese MFS investigated in this research. The reason may be related to the participants’ (user and potential user) MFS experience. Since quite many of them lack experience in MFS, they might not be conscious regarding the real time needed for a service to be completed. This implies that the effect of time risk perceived is worthy of further development in future researches and MFS companies are encouraged to continue easing the transaction process of MFS in terms of time spent.

The third set of hypotheses is associated with the adoption of MFS. Among them, the hypothesis associated with the positive relationship that the dispositional trust has with MFS adoption was supported by the test result; hence, H9 (β = 0.355,

p < 0.001) is accepted (

Figure 2). This infers that when increasing the level of trust disposition, individuals tend to adopt MFS technologies without necessarily cogitating on the general trust. The finding is consistent with e-commerce adoption for SMEs [

204]. Moreover, the scholars reported that indicators for the dispositional trust should be incorporated into empirical studies either as a moderating variable or as a precursor of trusting beliefs, intentions, and behaviors [

205]. Being an antecedent of trust, a disposition to trust remains one of the most operative elements required during the launch phases of a relationship when parties are generally unacquainted with each other [

206]. Given that MFS is still in the early stages of adoption in Togo, services providers are recommended to promote the variable that could increase the consumer’s dispositional trust.

From

Figure 3, perceived risk significantly negates the adoption and usage of MFS, rendering the support of H10 (β = −0.097,

p < 0.022). It is so crucial to signpost the feasibility of this outcome to be enlightened by the theory of consumer behavior [

116] allied with risk perception. The importance of perceived risk in the study also confirms previous studies that demonstrate that consumers’ perceived risk is more efficacious at clarifying purchasing or adoption behavior inasmuch as consumers are more recurrently driven to avert mistakes than to capitalize on utility in purchasing [

207]. This output is also coherent with a recent report on mobile payment adoption, which underlines rapid technology innovation while stressing the importance of perceived risk in the form of security [

208,

209].

Last but not least, the study entails and accepts the hypothesis H11 (β = 0.108,

p < 0.008) in which general trust has a positive influence on MFS adoption. Generally, trust remains a vital factor in various economic and social relations involving uncertainty and reliance [

210,

211], particularly those regarding important decisions [

212] and new technologies [

198] as an MFS perspective. Accordingly, our findings are sustained via the idea that trust in business rests on the pertinent and crucial stimulus of behavior in general [

213,

214,

215], and the facilitator factors for MFS adoption and usage in particular.

Under this set, it can then be deduced that both improving trust and decreasing risk continue to raise the likelihood level of consumers’ engagement in MFS transaction. Companies are required to take the necessary precaution to balance the trade-off.

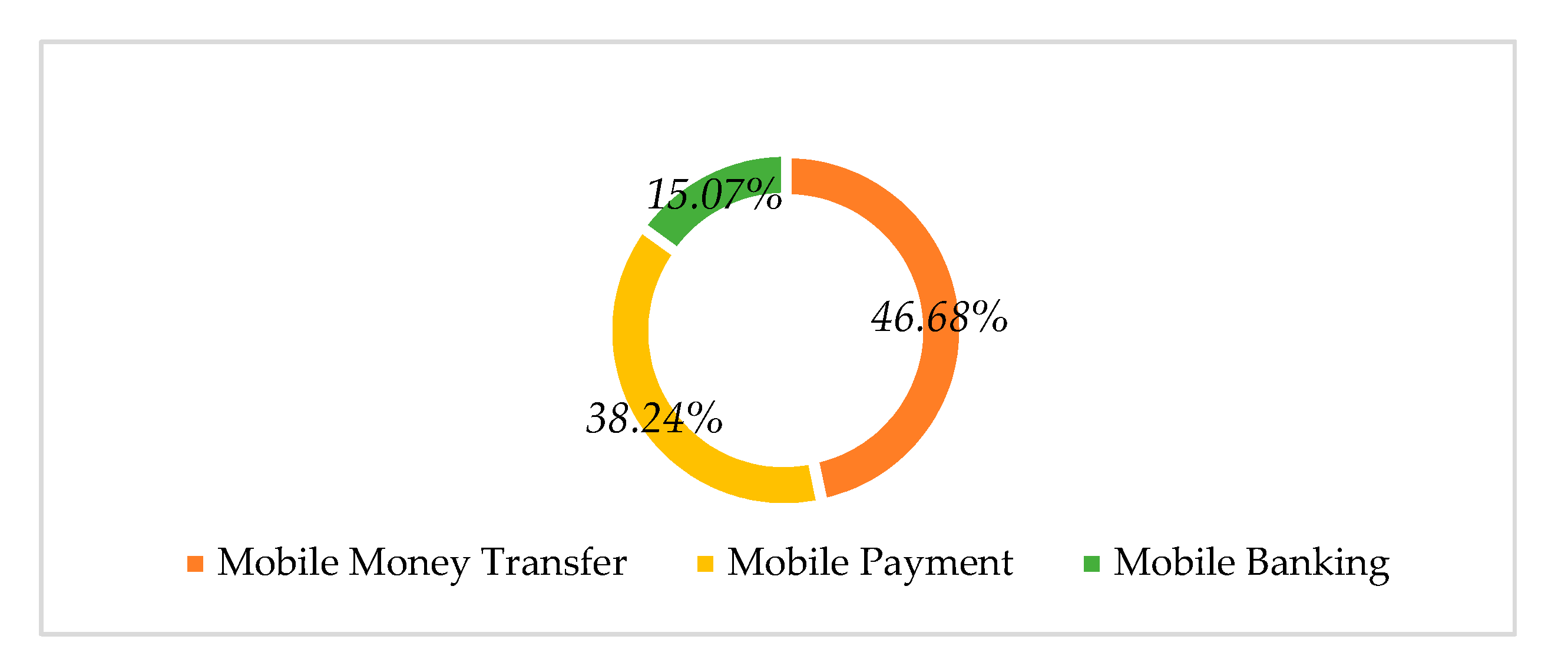

SEM-TOPSIS: It is noteworthy to recall that the second section of discussion concerns the output of MFS alternatives computation. The overall result from the TOPSIS technique shows the preference of each alternative regarding the various sub-criteria. The relative closeness

results obtained satisfies the sine qua non-condition, i.e.,

. Furthermore, TOPSIS technique is grounded on the principle that the higher the value of

, the high the rank order, and consequently, the more the chosen alternatives are favored over others. The final result reveals that mobile money transfer (MMT) is the most preferable MFS to adopt and use with

tantamount to 0.7454 signifying 46.68% compared to the last two remainings. Mobile payment (MP) with 0.6106 (38.24%) was found to be the second MFS alternative used, whereas mobile banking (MB) adoption with 0.2407 (15.07%) is considered minor. This finding is relatively supported by the prior study on mobile banking and mobile payment, where 82% of participants under 35 years old have made mobile payments as compared to 79% who used mobile banking [

216]. A similar past study has further shown that mobile payment usage among USA millennials was higher than that of mobile banking generally. The likely motive of the MFS preference acknowledged in this study can be explained based on the significant issues of concern toward perceived privacy risk. Using mobile money transfer or mobile payment service does not necessarily involve consumers’ personal information or an account that needs to be connected to a bank account. By that, lots of end-users would rather opt for mobile money transfer and mobile payment than for mobile banking accordingly.

Table 7 below compares the outputs of TOPSIS and AHP and reveals the same results for the choice of the alternative ranking of mobile financial services (MFS). It was found that the outcomes were well consistent and, in general, agreed with each other. Based on the results of the ranking of the two techniques, mobile money transfer (MMT) was chosen as the most appropriate among the mobile financial services followed by mobile payment and mobile banking. However, there are slight differences found in the percentage of coefficient distribution among the classification of their alternatives. For instance, AHP reveals that MFS consumers have a high preference in using mobile money services (i.e., the difference in the percentage of coefficient: 13.32%) as compared to TOPSIS results. Contrarily, the TOPSIS result shows that consumers are more interested in using mobile payment when considering the difference in percentage sharing between the two techniques (i.e., the difference in the percentage of coefficient: 13.75%).

However, the results regarding the difference in percentage distribution of coefficient between TOPSIS and AHP in terms of mobile banking selection remain trivial. These results stressed that MFS consumers would not prefer using mobile banking if they have a choice between the proposed mobile financial services (MFS).

The difference between the finding of TOPSIS and AHP in the choice of MFS depends on their strengths and weaknesses, which are thoroughly pronounced in the literature [

161,

217]. For instance, the core advantages of AHP over TOPSIS can be attributed to its intuitive appeal to decision-makers, and its ability to check inconsistencies. Furthermore, decision-makers find the pairwise comparison system of data input convenient and straightforward. However, the application of AHP leads to the decision problem being decomposed into numerous subsystems, which require a considerable number of pairwise comparisons to be completed. Therefore, it is a complex and time-consuming implementation. In the situation of TOPSIS, the non-linear relations between one-dimensional scores and distance ratios lead to the consideration of both negative and positive ideal solutions. Also, in the TOPSIS framework, we can use variables with different units of measurement. It is very simple and easy to implement so that it is adopted when the user prefers a simpler weighting approach. However, TOPSIS, in its standard and original form, is deterministic and does not embrace uncertainty in the calculations associated with final weightings.

{kind=link}

{kind=link}

{kind=link}