Predicting the Insolvency of SMEs Using Technological Feasibility Assessment Information and Data Mining Techniques

Abstract

:1. Introduction

2. Literature Review

2.1. Policy Funds

2.2. Research on Predicting Company Insolvency

3. Research Method

3.1. Research Framework

3.2. Data

3.3. Target Variable

3.4. Independent Variable

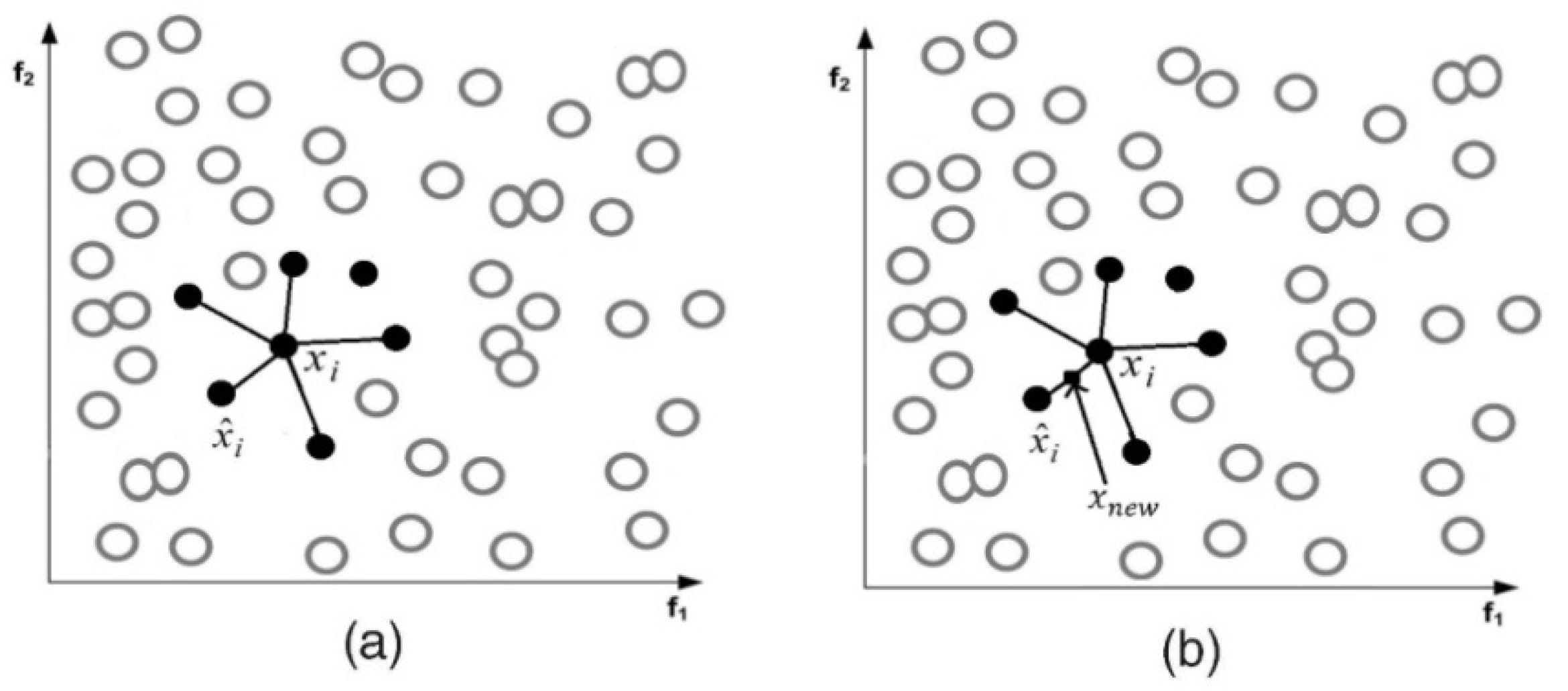

3.5. Feature Selection

4. Experimental Results

4.1. Evaluation of Prediction Models

4.2. Insolvency Rules of SMEs

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Linna, T. Insolvency proceedings from a sustainability perspective. Int. Insolv. Rev. 2019, 28, 210–232. [Google Scholar]

- Beaver, W.H. Financial ratios as predictors of failure. J. Account. Res. 1966, 4, 71–111. [Google Scholar]

- Altman, E.I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar]

- Kim, K.H. A Detailed Analysis of Start-Up Support Companies; Korea Institute of Startup & Entrepreneurship Development: Daejeon, Korea, 2019; pp. 67–95. [Google Scholar]

- Giacosa, E.; Mazzoleni, A. A decision model for the suitable financing for small and medium enterprises. Int. J. Manag. Financ. Account. 2016, 8, 39–74. [Google Scholar]

- Cho, Y.S. Major Issues and Policy Tasks of SME Policy Fund; ISSUE PAPER 2008-232; KIET: Seoul, Korea, 2008. [Google Scholar]

- Kim, H.O.; Yoon, B.S. The Current State of Policy Fund Support: Differentiation Measures of Small and Medium Business Corporation (SBC). J. Decis. Sci. 2015, 23, 113–133. [Google Scholar]

- Kim, J.K. Improvement of Financing in Policy Fund; Korea Development Institute: Seoul, Korea, 1993; pp. 113–176. [Google Scholar]

- Lim, H.J. A study on the effect of Macroeconomic variables on credit guarantee performance. J. SME Financ. 2009, Autumn, 39–67. [Google Scholar]

- Lee, J.S.; Kim, J.J. A Study on the Effective Combining Technology and Credit Appraisal Information in the Innovation Financing Market. J. Digit. Converg. 2017, 15, 199–208. [Google Scholar]

- Lim, H.J. Firm Characteristics and Default Predictability: Relationship-Banking, Age and Size. Korean Econ. Anal. 2016, 22, 81–142. [Google Scholar]

- Kim, T.H.; Han, B.H. Association between Technology Evaluation Grades and Financial Performance for Small and Medium-Sized Enterprises. Korean J. Bus. Adm. 2009, 22, 2789–2808. [Google Scholar]

- Kolte, A.; Capasso, A.; Rossi, M. Critical analysis of failure of Kingfisher Airlines. Int. J. Manag. Financ. Account. 2018, 10, 391–409. [Google Scholar]

- Ohlson, J.A. Financial ratios and the probabilistic prediction of bankruptcy. J. Account. Res. 1980, 18, 109–131. [Google Scholar]

- Altman, E.I.; Sabato, G. Modelling credit risk for SMEs: Evidence from the U.S. market. Abacus 2007, 43, 332–357. [Google Scholar]

- Podviezko, A.; Kurschus, R.; Lapinskiene, G. Eliciting weights of significance of criteria for a monitoring model of performance of SMEs for successful insolvency administrator’s intervention. Sustainability 2019, 11, 5667. [Google Scholar]

- Meyer, P.A.; Pifer, H.W. Prediction of bank failures. J. Financ. 1970, 25, 853–868. [Google Scholar]

- Dimitras, A.I.; Zanakis, S.H.; Zopounidis, C. A survey of business failures with an emphasis on prediction methods and industrial applications. Eur. J. Oper. Res. 1996, 90, 487–513. [Google Scholar]

- Abbasi, A.; Albrecht, C.; Vance, A.; Hansen, J. Metafraud: A meta-learning framework for detecting financial fraud. MIS Q. 2012, 36, 1293–1327. [Google Scholar]

- Chuang, C.L. Application of hybrid case-based reasoning for enhanced performance in bankruptcy prediction. Inf. Sci. 2013, 236, 174–185. [Google Scholar]

- Kim, R.H.; Yoo, D.H.; Kim, G.W. Development of Prediction Model of Financial Distress and Improvement of Prediction Performance Using Data Mining Techniques. Inf. Syst. Rev. 2016, 18, 173–198. [Google Scholar]

- Bae, J.K. An Integrated Approach to Predict Company Bankruptcy with Voting Algorithms and Neural Networks. J. Corp. Innov. 2010, 3, 79–101. [Google Scholar]

- Wang, G.; Ma, J.; Yang, S. An improved boosting based on feature selection for corporate bankruptcy prediction. Expert Syst. Appl. 2014, 41, 2353–2361. [Google Scholar]

- Choi, J.W.; Han, H.S.; Lee, M.Y.; Ahn, J.M. The Prediction of Company Bankruptcy Using Text-mining Methodology. Product. Rev. 2015, 29, 201–228. [Google Scholar]

- Lee, J.S.; Han, J.H. Usability test of non-financial information in bankruptcy prediction using artificial neural network—The case of small and medium-sized firms. J. Intell. Inf. Syst. 1995, 1, 123–134. [Google Scholar]

- Cultrera, L.; Brédart, X. Bankruptcy prediction: The case of Belgian SMEs. Rev. Account. Financ. 2016, 15, 101–119. [Google Scholar]

- Lugovskaya, L. Predicting default of Russian SMEs on the basis of financial and non-financial variables. J. Financ. Serv. Mark. 2010, 14, 301–313. [Google Scholar]

- Pervan, I.; Kuvek, T. The relative importance of financial ratios and nonfinancial variables in predicting of insolvency. Croat. Oper. Res. Rev. 2013, 4, 187–197. [Google Scholar]

- Shin, D.R. A Study on the Usefulness of Productivity Indicators in Company Financial Distress Prediction. Product. Rev. 2006, 20, 1–24. [Google Scholar]

- Jo, N.O.; Shin, K.S. Bankruptcy Prediction Modeling Using Qualitative Information Based on Big Data Analytics. J. Intell. Inf. Syst. 2016, 22, 33–56. [Google Scholar]

- Bărbuță-Mișu, N.; Madaleno, M. Assessment of bankruptcy risk of large companies: European countries evolution analysis. J. Risk Financ. Manag. 2020, 13, 58. [Google Scholar]

- Pompe, P.P.; Bilderbeek, J. The prediction of bankruptcy of small-and medium-sized industrial firms. J. Bus. Ventur. 2005, 20, 847–868. [Google Scholar]

- Makropoulos, A.; Weir, C.; Zhang, X. An analysis of the determinants of failure processes in UK SMEs. J. Small Bus. Enterp. Dev. 2020, 27, 405–426. [Google Scholar]

- Mayr, S.; Mitter, C.; Kücher, A.; Duller, C. Entrepreneur characteristics and differences in reasons for business failure: Evidence from bankrupt Austrian SMEs. J. Small Bus. Entrep. 2020, in press. [Google Scholar]

- Akbar, M.; Akbar, A.; Maresova, P.; Yang, M.; Arshad, H.M. Unraveling the Bankruptcy Risk‒Return Paradox across the Corporate Life Cycle. Sustainability 2020, 12, 3547. [Google Scholar]

- Sánchez-Lasheras, F.; de Andrés, J.; Lorca, P.; de Cos Juez, F.J. A hybrid device for the solution of sampling bias problems in the forecasting of firms’ bankruptcy. Expert Syst. Appl. 2012, 39, 7512–7523. [Google Scholar]

- Ok, J.K.; Kim, K.J. Integrated Company Bankruptcy Prediction Model Using Genetic Algorithms. J. Intell. Inf. Syst. 2009, 15, 99–120. [Google Scholar]

- Svabova, L.; Michalkova, L.; Durica, M.; Nica, E. Business Failure Prediction for Slovak Small and Medium-Sized Companies. Sustainability 2020, 12, 4572. [Google Scholar]

- Ahmeti, L.; Zubanovic, A. The Predictive Power of Financial Ratios on Bankruptcy: A Quantitative Study of Non-Listed Limited Liability SMEs Companies in Sweden. Master’s Thesis, Jönköping University, Jönköping, Sweden, 30 May 2020. [Google Scholar]

- Kim, M.J. Ensemble Learning for Solving Data Imbalance in Bankruptcy Prediction. J. Intell. Inf. Syst. 2009, 15, 1–15. [Google Scholar]

- Zhou, B.; Zhang, X.; Zhang, S.; Li, Z.; Liu, X. Analysis of Factors Affecting Real-Time Ridesharing Vehicle Crash Severity. Sustainability 2019, 11, 3334. [Google Scholar]

- Chawla, N.V.; Bowyer, K.W.; Hall, L.O.; Kegelmeyer, W.P. SMOTE: Synthetic minority over-sampling technique. J. Artif. Intell. Res. 2002, 16, 321–357. [Google Scholar]

- He, H.; Garcia, E.A. Learning from imbalanced data. IEEE Trans. Knowl. Data Eng. 2009, 21, 1263–1284. [Google Scholar]

- Dash, M.; Liu, H. Feature selection for classification. Intell. Data Anal. 1997, 1, 131–156. [Google Scholar]

- Wi, P.R. Changes in SBC’s SME Policy Fund Support and Its Implications (2001–2012). Econ. Reform Rep. 2014, 1, 1–29. [Google Scholar]

- Witten, I.H.; Frank, E. Data mining: Practical machine learning tools and techniques with Java implementations. ACM Sigmod Rec. 2002, 31, 76–77. [Google Scholar]

- Kalkhouran, A.A.; Nedaei, B.H.; Rasid, S.Z.A. An exploratory investigation of an integrated model of costing practices in small and medium-sized enterprises. Int. J. Manag. Financ. Account. 2017, 9, 338–360. [Google Scholar]

- Bogliacino, F.; Pianta, M. The Pavitt Taxonomy, revisited: Patterns of innovation in manufacturing and services. Econ. Polit. 2016, 33, 153–180. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Number of Features | Method | Data Type | Number of Companies | Accuracy (%) | |

|---|---|---|---|---|---|---|

| Insolvency | Healthy | |||||

| [2] | 6 | Univariate Analysis | Finance | 79 | 79 | 78–87 |

| [3] | 5 | Multiple Discriminant Analysis | Finance | 33 | 33 | 74–95 |

| [14] | 9 | Logit Model | Finance | 105 | 2058 | 92.84–96.12 |

| [20] | 26 | Case-based Reasoning | Finance | 42 | 279 | 96.90 |

| [22] | 11 | Artificial Neural Network | Finance | 944 | 944 | 80.89 |

| [23] | 24 | FS-Boosting | Finance | 66 | 66 | 86.79 |

| [32] | 45 | Multiple Discriminant Analysis, Neural Network | Finance | 1500 | 1500 | 72–79 |

| [36] | 5 | Artificial Neural Network, Multivariate Adaptive Regression Splines | Finance | 256 | 63,107 | 89.58 |

| [37] | 16 | Genetic Algorithm | Finance | 1570 | 1570 | 77.3–82.5 |

| [38] | 11 | Logistic Regression Discriminant Analysis | Finance | 8220 | 67,432 | 90.4–93.8 |

| [39] | 11 | Logistic Regression | Finance | 46 | 46 | 82.6 |

| [24] | 7 | Decision Tree | Non-Finance | 177 | 160 | 56.2–83.1 |

| [19] | 12 | Stacking | Finance, Non-Finance | 815 | 8191 | 93.10 |

| [25] | 9 | Artificial Neural Network | Finance, Non-Finance | 20 | 221 | 75 |

| [26] | 16 | Logistic Regression | Finance, Non-Finance | 3576 | 3576 | 83 |

| [27] | 25 | Linear Discriminant Analysis | Finance, Non-Finance | 584 | 8393 | 79 |

| [28] | 7 | Logistic Regression | Finance, Non-Finance | 127 | 698 | 88.1 |

| [29] | 4 | Logistic Regression | Finance, Non-Finance | 112 | 112 | 74.1–79 |

| Type | Initial Collected Data | Over-Sampling Data | ||||

|---|---|---|---|---|---|---|

| Healthy | Insolvency | Sum | Healthy | Insolvency | Sum | |

| Fewer than three years | 1171 | 618 | 1789 | 1171 | 1171 | 2342 |

| More than three years | 2018 | 549 | 2569 | 2018 | 2018 | 4036 |

| Sum | 3189 | 1167 | 4358 | 3189 | 3189 | 6378 |

| No | Features | Definition | Category |

|---|---|---|---|

| 1 | KA1 | Business management ability | Management ability |

| 2 | KA2 | Management stability | |

| 3 | KA3 | Internal control | |

| 4 | KA4 | Labor relations | |

| 5 | KA5 | Appropriateness of financing plan | |

| 6 | KA6 | Financing ability | |

| 7 | KB10 | Credit status | |

| 8 | KC17 | Business propulsion | |

| 9 | KC18 | CEO’s reliability | |

| 10 | KC19 | CEO’s professionalism | |

| 11 | K-Score | Sum of management ability assessment | |

| 12 | SA2 | Transaction stability | Business feasibility |

| 13 | SA9 | Sales management | |

| 14 | SB11 | Sales growth | |

| 15 | SB12 | Future profitability | |

| 16 | SC16 | Market entry/expansion possibility | |

| 17 | SC18 | Market position | |

| 18 | SC22 | Product competitiveness | |

| 19 | SD23 | Competitive strength | |

| 20 | SD24 | Market growth | |

| 21 | SD25 | Market environment | |

| 22 | S-Score | Sum of business feasibility assessment | |

| 23 | TA2 | Technology development manpower | Technical ability |

| 24 | TA3 | Technology development environment | |

| 25 | TA7 | R&D investment | |

| 26 | TG24 | Process improvement | |

| 27 | TG26 | Production efficiency | |

| 28 | TG28 | Facility adequacy | |

| 29 | TG32 | Quality and process improvement | |

| 30 | TG33 | Quality innovation | |

| 31 | TO67 | Technology development performance | |

| 32 | TO68 | Technical application capacity | |

| 33 | TO69 | Possibility of technology expansion | |

| 34 | TO72 | Core technology superiority/discrimination | |

| 35 | T-Score | Sum of technical assessment | |

| 36 | Total Score | Total score | Other |

| 37 | Usage | Usage of loan (working or facility capital) |

| Algorithm | Accuracy (%) | ||

|---|---|---|---|

| Fewer Than Three Years | More Than Three Years | ||

| Single | Logistic Regression | 59.3 | 62.8 |

| Decision Tree | 68.1 | 80.6 | |

| Artificial Neural Network | 61.4 | 70.1 | |

| Ensemble | Boosting (Logistic Regression) | 59.3 | 62.8 |

| Boosting (Decision Tree) | 69.1 | 82.7 | |

| Boosting (Artificial Neural Network) | 63.8 | 76.3 | |

| Category | Features | Definition | Max Points |

|---|---|---|---|

| Management ability | KA6 | Financing ability | 5 |

| KC18 | CEO’s reliability | 7 | |

| KC19 | CEO’s professionalism | 5 | |

| Business feasibility | SA2 | Transaction stability | 6 |

| SA9 | Sales management | 4 | |

| SB12 | Future profitability | 5 | |

| SC16 | Market entry/expansion possibility | 4 | |

| Technical ability | TO72 | Core technology superiority/discrimination | 7 |

| Other | Usage | Usage of loan (working or facility capital) | - |

| Rule | Description | Target Variable | Prediction | Probability (%) | |

|---|---|---|---|---|---|

| True | False | ||||

| 1 | (KA6 > 2.4) and (3 < SB12 <= 4) | Insolvency | 77 | 0 | 100 |

| 2 | (KA6 > 2.4), (SB12 <= 3), and (4.2 < KC18 <= 5.5) | Insolvency | 32 | 0 | 100 |

| 3 | (KA6 > 2.4), (SB12 <= 3), (KC18 <= 4.2), (SA9 <= 3.2), (3.6 < SA2 <= 4.8), and (Usage = “Working capital”) | Insolvency | 20 | 0 | 100 |

| 4 | (1.6 < KA6 <= 2.4) | Insolvency | 118 | 1 | 99 |

| 5 | (KA6 <= 1.6), (KC18 <= 5.5), and (KC19 <= 4) | Insolvency | 20 | 2 | 91 |

| 6 | (KA6 > 2.4), (SB12 > 4), (SC16 > 3.6), and (TO72 > 4.8) | Insolvency | 24 | 6 | 80 |

| Category | Features | Definition | Max Points |

|---|---|---|---|

| Management ability | KA3 | Internal control | 4 |

| KA6 | Financing ability | 5 | |

| KB10 | Credit status | 5 | |

| KC17 | Business propulsion | 3 | |

| Business feasibility | SC18 | Market position | 4 |

| SD23 | Competitive strength | 3 | |

| SD25 | Market environment | 3 |

| Rule | Description | Target Variable | Predict | Probability (%) | |

|---|---|---|---|---|---|

| True | False | ||||

| 7 | (3 < KB10 <= 4) | Insolvency | 250 | 0 | 100 |

| 8 | (KB10 <= 3), (3 < KA6 <= 4), (SD23 <= 1.8), and (1.8 < SD25 <= 2.4) | Insolvency | 232 | 0 | 100 |

| 9 | (KB10 <= 3) and (2 < KA6 <= 3) | Insolvency | 185 | 0 | 100 |

| 10 | (KB10 <= 3), (3 < KA6 <= 4), and (1.8 < SD23 <= 2.4) | Insolvency | 130 | 0 | 100 |

| 11 | (KB10 <= 3), (3 < KA6 <= 4), (SD23 <= 1.8), (SD25 <= 1.8), (KA3 > 2.4), (SC18 <= 2.4), and (1.8 < KC17 <= 2.4) | Insolvency | 76 | 0 | 100 |

| 12 | (KB10 <= 3), (3 < KA6 <= 4), (SD23 <= 1.8), (SD25 <= 1.8), (KA3 > 2.4), and (2.4 < SC18 <= 3.2) | Insolvency | 54 | 0 | 100 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.; Choi, K.; Yoo, D. Predicting the Insolvency of SMEs Using Technological Feasibility Assessment Information and Data Mining Techniques. Sustainability 2020, 12, 9790. https://doi.org/10.3390/su12239790

Lee S, Choi K, Yoo D. Predicting the Insolvency of SMEs Using Technological Feasibility Assessment Information and Data Mining Techniques. Sustainability. 2020; 12(23):9790. https://doi.org/10.3390/su12239790

Chicago/Turabian StyleLee, Sanghoon, Keunho Choi, and Donghee Yoo. 2020. "Predicting the Insolvency of SMEs Using Technological Feasibility Assessment Information and Data Mining Techniques" Sustainability 12, no. 23: 9790. https://doi.org/10.3390/su12239790

APA StyleLee, S., Choi, K., & Yoo, D. (2020). Predicting the Insolvency of SMEs Using Technological Feasibility Assessment Information and Data Mining Techniques. Sustainability, 12(23), 9790. https://doi.org/10.3390/su12239790