Proposal for a Maturity Model in Sustainability in the Supply Chain

,

,  ,

,  , ,

, ,

Abstract

1. Introduction

- Environmental management throughout the supply chain process.

- Achieving the objectives of profit and market share, while decreasing the risks and environmental impacts.

- Management of purchases, materials, and production directed towards the reduction of environmental impacts.

- Use of reverse logistics.

- Integrating environmental thinking into SCM, including product design, supply and material selection, manufacturing processes, delivery of the final product to consumers, as well as managing the end of the product’s life after its useful life.

2. Theoretical Framework

2.1. Sustainability: Definition and Relevance for Organizations

2.2. Maturity Model Concept

2.3. Supply Chain Performance Measurement Systems: Relevant Concepts, Aspects and the Relationship with Maturity Models

2.3.1. Concepts

- Measures of performance, and support infrastructure.

- Functions of performance measurement systems: measuring performance, managing strategy, exercising communication, influencing behavior, and providing learning and improvement.

- Processes of performance measurement systems: selection and development of measures; data collection and manipulation; information management; performance assessment and review of the system.

2.3.2. Relationship between Maturity Models and Supply Chain Performance Measurement Systems

2.3.3. Performance Measurement Systems and their Maturity

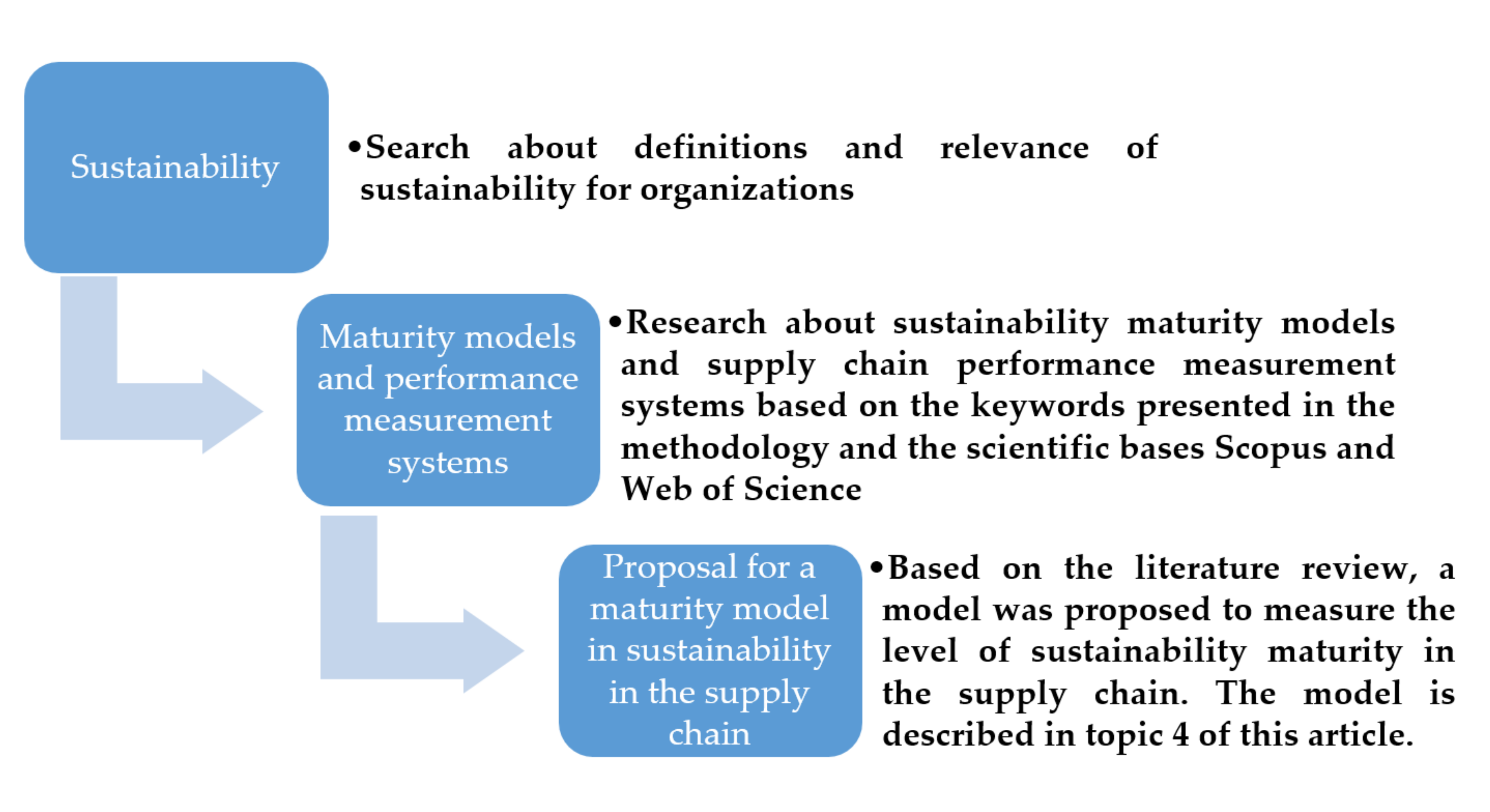

3. Methodology

4. Proposal for a Maturity Model in Sustainability in the Supply Chain

4.1. Identification of the Limitations of Sustainability Models in the Supply Chain

4.2. Construction of the Basic Theoretical Model

4.2.1. Description of the Subdimensions of the Environmental Dimension

- Emissions to the atmosphere, water, and soil: emissions to the atmosphere, water, and soil due to corporate activities [13].

- Hazardous waste: hazardous waste and waste due to business activities [13].

- Waste minimization: global product lifecycle/example management service system integrated with business strategy [15].

- “Carbon punch”: evidence of reconfiguration of operations to minimize the “carbon footprint” [15].

- The product portfolio subdimension is composed of four characteristic elements: resources (materials, energy, and recycling); Life Cycle Assessment Process (LCA); remanufacturing and material and parts selection. The characteristic elements are described below:

- Resources (materials, energy, and recycling): use of renewable and nonrenewable resources and energy through the company, including recycled resources [13].

- LCA: evaluation of whether the life cycle assists in the decision-making process of designers and in their cost and degree of efficiency. It also considers: selection of a sustainable production process; alternatives by designing teams aiming to reduce environmental impacts during the use of the product or service by the customer; and whether the evaluation of products are designed to facilitate disassembly, recycling, and reuse at the end of life [14].

- Remanufacturing: evaluation of loss of production materials due to defective products and shavings; use of some procedure to reduce the use of materials and standardized procedure that supports the environmentally correct use of resources. Considers the creation of production and packaging waste in the company. It also evaluates the use of long air in the production process; the amount of compressed air consumption, liquid infrastructure and compressor technology; identification and rapid correction of vulnerabilities and periodic review of the compressed air network to detect vulnerabilities and leaks [17].

- Material and parts selection: reduction of environmental impact through material selection [14].

- The tools subdimension is composed of one characteristic element: lean and green practices. The characteristic element is described below:

- Lean and green practices: use of lean tools (5S; Andon; Just in Time, Kanban; Poka-Yoke; Single Minute Exchange of Die (SMED); and Total Productive Maintenance (TPM) to reduce environmental impact [18].

4.2.2. Description of the Subdimensions of the Social Dimension

- Motivation and encouragement: active involvement and exemplary management function in sustainability issues for employees. Awareness of the need’s demands, and motivation factors of employees to implement sustainability in a sufficiently conscious way in the organization. Management support to act in a sustainable manner and the development of incentive and reward systems [13].

- Health and safety: safety and assurance so that there are no health and safety risks when working within/for the organization. No negative impact on the physical health of employees at any time. Operation of programs to prevent employees from preventing hazards and generally staying healthy [13].

- Ergonomics and safety: describe the way physiology takes care of body functions. It involves how a person interacts with their immediate work area and how people react to environmental conditions. With regard to safety, the organization must ensure the physical integrity of workers in the execution of their activities [13].

- Development of human capital: development of human capital for sustainability-related issues through specific programs such as continuing education, mentoring or training. A broad cross-cutting education in order to become aware of the different challenges and issues of corporate sustainability [8,13].

- The external subdimension is composed of three characteristic elements: ethical behavior and human rights, no controversial activity, and corporate citizenship. The characteristic elements are described below:

- Ethical behavior and human rights: ethical behavior in relation to sustainability, basic assumptions and principles relating to cooperation in the organization and behavior towards (external) stakeholders. In relation to sustainability, the important elements are a culture of respect, fair rules and behavior within an organization and an equitable distribution of wealth and results, consideration of the ideals and needs of stakeholders. No harm to employees, or with regard to their religious convictions, sex, nationality, color, disability, or age [13].

- No controversial activity: lack of participation in organizations that are mostly defined as unsustainable. Absence of use or sale of assets and own assets for unsustainable activities [13].

- Corporate citizenship: be a good corporate citizen on a national level, conservation of subsidiaries in the country and establishment of economic power of a country, as well as an increase in the lifestyle of society. Support for stakeholders and their issues at regional level; participation or creation of sustainability-related activities for the local community. Guidance on future generations without exploring the present (or nature) [13].

- The social risk subdimension is composed of one characteristic element: sustainability risk analysis. The characteristic element is described below:

- Sustainability risk analysis: risk analysis in supply chains. Cost and implementation risks arising from the application of sustainability practices are fully assessed with partners. Risk assessment is for both environmental and social aspects. With regard to environmental risks, the company must evaluate the impacts of the production process on the community [8,16].

4.2.3. Description of the Subdimensions of the Economic Dimension

- Return and investment in sustainability: return and investment made in order to leverage issues involving sustainability [19].

- Management of the distribution of economic value: there is a broader scope of spending from supply chain suppliers (include fair trade throughout the chain) [1].

- The return and investment subdimension is composed of two characteristic elements: return and investment in sustainability; management of the distribution of economic value. The characteristic elements are described below:

- Inventory: costs related to the calculation of materials in stock and related to the remanufacturing process [17].

- Scrap and rework: costs related to materials that cannot be used in the production process and the activities that need to be performed again, depending on if the product does not present the parameters and characteristics defined in the project design [17].

- Organization of production: costs related to the internal organization of the plant to achieve sustainability [17].

- The analysis and results subdimension are composed of one characteristic element: financial results associated with sustainability efforts. The characteristic element is described below:

- Financial results associated with sustainability efforts: evaluation of the means used by the organization to determine the efforts directed towards sustainability. In addition, there is an assessment of the impact of expenditure on sustainability [19].

4.2.4. Description of the Subdimensions of the Cross Dimension

- Information systems: the sustainability practices of the information system are used in an integrated manner. For this, the organization is fully committed to sustainability and is oriented towards the continuous improvement of green IT practices implemented through detailed performance reports, exhaustive use of sustainability metrics, and management of the innovation process in sustainability [20,21].

- Sustainable innovation: sustainable innovation implies that it occurs regularly and systematically for the company’s efforts, that is, it is purposely incorporated into the business culture and contributes to the financial stability of the organization. In addition, the organization should promote the integration of network knowledge with sustainable lean practices and total quality of global industry standard. The organization should aim to lead the sector in sustainable technologies and disruptive sustainable innovation [15,19]. The result of sustainable innovation is the generation of a differentiated product in all elements of sustainability. Design priority for sustainability in all new disruptive technologies. Industry Leader [15].

- Purchase: considers sustainability in procurement and the supply chain. Relationship with suppliers focused on sustainability. Whether the acquisition strategy is reviewed regularly, examined externally, and directly linked to the program and environmental management system of organizations. In this case, a detailed review is carried out to determine future priorities and a new strategy is developed beyond this framework [13,22].

- Sustainability risk analysis for supply: best practices shared with other organizations and key sustainability performance indicators agreed with key suppliers [22].

- Supplier commitment program: suppliers recognized as essential for the implementation of the sustainable supply strategy of organizations and best practices shared with partner organizations. There are measures used to guide the organizational sustainable development strategy. Progress formally measured with partner organizations. The presence of independent audit reports available in the public domain and the simple measures based on the performance of all aspects of the level of leadership are put into practice and delivered [22].

- The strategic subdimension is composed of five characteristic elements: corporate governance; strategic and business vision; management of the portfolio of projects and programs; positioning and strategic marketing; collaboration. The characteristic elements are described below:

- Corporate governance: transparency in all its activities to improve the relationship with its stakeholders [13].

- Management of the portfolio of projects and programs: integrated value chain plus external benchmarking [15].

- Positioning and strategic marketing: leadership strategy in the customer-centric sector and supported by a sustainable product service system [15].

- Collaboration: good cooperation and active collaboration with various trading partners. Work on common programs and networks on innovative products and technologies. Exchange of information and knowledge [13].

- The stakeholder subdimension is composed of one characteristic element: management of the relationship of suppliers, customers, and society. The characteristic element is described below:

- Management of the relationship of suppliers, customers, and society: the relationship management scheme goes beyond upstream and downstream partners to include managing the impact of operations on communities [1].

- The stakeholder subdimension is composed of six characteristic elements: knowledge management; processes; sustainability reports; global sustainability standards; sustainability benchmarking and sustainability training. The characteristic elements are described below:

- Knowledge management: activities and approaches to maintain knowledge related to sustainability in the organization. Methods to plan, develop, organize, maintain, transfer, apply, and measure specific knowledge and improve the organizational knowledge base. Knowledge management is institutionalized throughout the organization for the dissemination of issues involving sustainability. Checks organizational processes are improved based on formal evaluation procedures that consider aspects of sustainability [13,23,24].

- Processes: clear processes and roles are defined so that business activities are conducted efficiently and that each employee knows what the organization expects from it. Adapting process management to sustainability needs to systematically implement corporate sustainability. Integration of sustainability in everyday business life [13].

- Sustainability reports: considers the presence of sustainability in the company’s reports, whether in a separate sustainability report or integrated into the corporate report. The formulation of performance indicators in the three dimensions and some metrics on the activities of supply chain suppliers [1,13]. Collection of internal and external data. Data is collected from most members of the supply chain. Data on environmental and social aspects are collected [8].

- Global sustainability standards: participation in all items of Global Reporting Initiative (GRI), Carbon Disclosure Project (CDP), ISO 14000, and ISO 26000, United Nations Global Compact. Commitment to sustainability standards. Creative development of new sustainable capacities [25].

- Sustainability benchmarking: internal and external benchmarking. The comparison is made between multiple organizational units over time and between members of the supply chain. The scope of benchmarking is both for environmental and social aspects [8].

- Sustainability training: training of internal and business partners. Training given to internal managers, supervisors and business partners involved in sustainability practices. Training focuses on environmental and social aspects [8].

4.2.5. Description of the Level of Nonexistent Maturity

Environmental Risk

- The company is unaware of emission laws and regulations for air, water, and soil and does not present specific targets to reduce these emissions [13].

- The company is unaware of laws and regulations regarding hazardous waste and does not present specific targets for the issue of hazardous waste [13].

- The company is totally indifferent and does not take any specific action to minimize waste generation [15].

- For the “carbon footprint”, initial/unstrategy sensitization [15].

- The company is unaware of the laws and regulations related to biodiversity [13].

Product Portfolio

- For the use of resources are not considered any criteria [13].

- There is no LCA in relation to the products marketed by the company [14].

- The company does not take any specific action in relation to remanufacturing [17].

- Design teams’ design does not consider material selection as an alternative to reduce environmental impacts [14].

Tools

- The company does not adopt any lean tool (5S; Andon, Just in Time, Kanban; Poka-Yoke; SMED, and TPM to reduce environmental impacts) [18].

Internal

- The motivation of employees to achieve sustainability objectives has no impact under it [13].

- Health and safety are not considered in the company [13].

- The work environment does not consider environmental impacts that may negatively influence people’s performance. With regard to security, the organization does not invest in actions that aim to preserve the physical integrity of its employees. Workplace design does not positively influence the ergonomics, attitudes, motivation, and behavior of staff [13].

- In relation to sustainability, no general and specific measures for the development of human capital are defined [13].

External

Social Risk

- No sustainability risk analysis [8].

Return and Investment

- Innovation is irregular and generally activity-based, with little or no formal process guidance. It is generally regarded as a necessity and rarely or never directed towards forecasting [19].

- Information not available regarding the management of economic value distribution [1].

- There is no control in relation to remanufacturing-related inventory [17].

- There is no control regarding scrap/rework related to remanufacturing [17].

- The company does not invest in the plant’s internal physical arrangement to achieve sustainability [17].

- The company does not consider the possibility of financial reports focused on sustainability-oriented efforts [19].

Remanufacturing

Analysis and Results

- The company does not consider the possibility of financial reports focused on sustainability-oriented efforts [19].

Innovation and Technology

Supply

Strategic

- The company is unaware of the concept of corporate governance [13].

- Internal business plan in relation to strategic and business vision [15].

- Based on internal knowledge regarding the management of the portfolio of projects and programs [15].

- Basic reports of corporate social responsibility not highlighted in the marketing literature [15].

- The company does not take any action in relation to the collaboration process [13].

Stakeholders

- Information not available for managing the relationship of suppliers, customers, and society [1].

Knowledge and Performance

- With regard to knowledge management, there is an incipient increase in awareness of the benefits for business improvement [23].

- The company does not adopt the perspective of the vision of processes in its management [13].

- No sustainability-related report [8].

- No participation in global sustainability standards [25].

- Sem Benchmarking [8].

- No sustainability training [8].

4.2.6. Description of the Level of Conscious Maturity

Environmental Risk

- The company is aware of the existence of emission laws and regulations for air, water, and soil. However, it does not have specific targets for reducing these emissions [13].

- The company is aware of the existence of laws and regulations regarding hazardous waste. However, it does not present specific targets for the issue of hazardous waste [13].

- The company recognizes the relevance but does not take any specific action to minimize waste generation [15].

- For the “carbon footprint”, the complete measurement of the “carbon footprint” occurs for high volume/high environmental impact products through carbon [15].

- The company is aware of the laws and regulations relating to biodiversity but is not in compliance with them. The most relevant impacts on biodiversity are not yet identified and considered [13].

Product Portfolio

- For the use of resources, only economic and technical criteria are considered [13].

- The company is structuring forms, still in the initial stages, of construction of the LCA [14].

- For remanufacturing, manufacturing processes are considered during the project and design teams reduce the impact of products by choosing a more sustainable production process. Design teams’ design still does not seek to minimize the impact of the product or service while it is in use by the customer. Design teams’ design still does not consider what will happen to the product at the end of its useful life and the products are not yet designed to facilitate disassembly, recycling, and end-of-life reuse [17].

- Design teams’ design considers material selection as an alternative to reducing environmental impact. However, these alternatives are not implemented [14].

Tools

- The company adopts one of the lean tools (5S; Andon, Just in Time, Kanban; Poka-Yoke; SMED and is unaware of the concept of TPM for reducing environmental impacts) [18].

Internal

- The motivation of employees to achieve sustainability objectives is not focused or has a dysfunctional impact on sustainability [13].

- Health and safety are respected to the extent of the legal obligation [13].

- The work environment considers some environmental impacts that may negatively influence people’s performance. With regard to safety, the organization invests seasonally in actions that aim to preserve the physical integrity of its employees. Workplace design does not positively influence the ergonomics, attitudes, motivation, and behavior of staff [13].

- Regarding sustainability, the company is still structuring some general measures for the development of human capital [13].

External

Social Risk

- Risk analysis in preparation for internal sustainability practices. The implications of cost and implementation risks in selected organizational units are evaluated. Objective of the risk analysis: one aspect of TBL [8].

Return and Investment

Remanufacturing

- The remanufacturing inventory process exists, but is not sufficiently transparent [17].

- The remanufacturing-related scrap/rework control process exists, but is not sufficiently transparent [17].

- The company prepares a plan for the realization of investments in internal physical arrangement of the plant to achieve sustainability [17].

Analysis and Results

- The company is evaluating the possibility of building reports to determine the efforts directed towards sustainability.

Innovation and Technology

Supply

Strategic

- Corporate governance is focused on a mandatory structure [13].

- Business planning process in force for medium-term objectives in relation to strategic and business vision [15].

- Independent portfolio management in all business units in relation to project and program portfolio management [15].

- Repeated/consistent reports between business units with alignment with strategy and vision [15].

- The company is not an active partner in network diagrams [13].

Stakeholders

- For management of the relationship of suppliers, customers, and society, a relationship of seller and traditional buyer, without any evaluation of suppliers or development program [1].

Knowledge and Performance

- Development of knowledge management strategy and definition of work. Characterized by knowledge management structure, need for resources, barriers, and risks [23].

- Absence of sustainability issues in the definition of processes [13].

- Internal reports are under construction [8].

- Internal structuring to enable participation in one of the global sustainability standards (GRI, CDP, ISO 14000 and ISO 26000, United Nations Global Compact) [25].

- Start of implementation of internal benchmarking [8].

- Under construction, training aimed at sustainability [8].

4.2.7. Description of Intermediate Maturity Level

Environmental Risk

- The company follows some laws and regulations relating to emissions to air, water, and soil. However, it is still structuring specific targets to reduce these emissions [13].

- The company follows some laws and regulations regarding hazardous waste. However, it is still structuring specific targets for the issue of hazardous waste [13].

- The company irregularly adopts some specific actions to minimize waste generation [15].

- With regard to the “carbon footprint”, the evaluation of manufacturing sites from switching to renewable sources/implementation of the smart grid [15].

- Compliance with biodiversity laws and regulations. The most relevant impacts on biodiversity are identified and considered [13].

Product Portfolio

- For the use of resources, economic and technical criteria are considered and/or partially the environmental/social criteria. Resource efficiency is measured for some business processes [13].

- LCA data are incorporated into the decision-making by the design teams, but the LCA process is not yet well established [14].

- For remanufacturing, manufacturing processes are considered during the project and design teams reduce the impact of products by choosing a more sustainable production process. Design teams seek to minimize the impact of the product or service while in use by the customer. Design teams design still do not consider what will happen to the product at the end of its useful life and the products are not yet designed to facilitate disassembly, recycling, and end-of-life reuse [17].

- Design teams’ design implement consistent alternatives to reduce the environmental impact of products through material selection. However, the cost is still high for the company [14].

Tools

- The company adopts three of the lean tools (5S; Andon, Just in Time, Kanban; Poka-Yoke; SMED and is in the initial phase of application of the concept of TPM for reducing environmental impacts) [18].

Internal

- In several areas of the organization, measures are defined to encourage motivation for sustainability [13].

- Health and safety are respected to the extent of the legal obligation. Health and safety measures are established when dangerous situations or specific accidents occur. The deployment is more reactive than systematically planned [13].

- The work environment considers some environmental impacts that may negatively influence people’s performance. With regard to security, the organization invests irregularly in actions that aim to preserve the physical integrity of its employees. Workplace design essentially influences staff ergonomics [13].

- Some general measures for the development of human capital are defined in relation to sustainability [13].

External

- Human rights are respected. The main rules of behavior within the organization are challenged [13].

- The company declares to be aware to those who sell its products [13].

- Certain corporate citizenship projects are initiated or supported (mainly in monetary terms). Rarely presents a relationship between projects and the corporate business [13].

Social Risk

- Risk analysis for internal sustainability practices. The implications of cost and implementation risks in selected organizational units are evaluated. Risk analysis: environmental [8].

Return and Investment

- Innovation processes are well documented, and innovation is expected to be effectively realized. Supply chain members are selected in part based on their ability to accelerate or contribute to innovation efforts. Innovation is seen as an element to the contribution of the financial health of companies and overcome the perception of being cost neutral to be based on opportunities [19].

- Awards and rewards awarded to employees [1].

Remanufacturing

- Existence of indicators for processes implementation of isolated optimization methods in relation to inventory for remanufacturing [17].

- Existence of indicators for processes implementation of isolated optimization methods in relation to scrap and rework for remanufacturing [17].

- The company makes sporadic investments in the factory’s internal physical arrangement to achieve sustainability [17].

Analysis and Results

- The company is in the reporting phase for the investigation of efforts directed to sustainability [19].

Innovation and Technology

- Green IT practices are clearly defined, established, and managed in different business areas, contributing to sustainability in and through IT [21].

- The company is between an initial and intermediate phase of incorporating systematic and reapplicable innovation processes (innovation projects intentionally linked to the strategy and opportunities of corporate social and environmental responsibility). Some projects will be cost-based, others cost-neutral, and other revenue generators expected to have balanced overall financial performance [19].

Supply

- Transform sustainable supply policy into a strategy that addresses risk, process integration, marketing, supplier engagement, review, and measurement process. Strategy approved by the strategic level [22].

- All contracts are assessed for general sustainability risks and management actions and risks managed throughout all phases of the supply process are identified [22].

- Program oriented to the involvement of suppliers, promoting continuous improvement of sustainability. There is a two-way communication between the buyer and the supplier with incentives [22].

Strategic

- The company is focused on mandatory and voluntary corporate governance structures [13].

- Long-term strategic plan linked to the defined needs of the client, conducted by the focal company, with results communicated to the network between companies in relation to strategic and business vision [15].

- Regarding the management of the portfolio of projects and programs, linked through the strategic marketing function, but without interdependencies. Value chains of the mapped and understood program(s); internal benchmarking; integration of customers and feedback on supplier quality [15].

- Corporate social responsibility reports incorporating all elements of the TBL and limited in relation to the dimensions of sustainability (energy efficiency and effectiveness; use of resources; minimization of waste; “carbon footprint”). Some integration with customer specifications [15].

- Communication and collaboration with the most relevant business partners (supplier, customer) [13].

Stakeholders

- For the management of the relationship of suppliers, customers, and society, an active program of evaluation and development of suppliers upstream and downstream [1] is in place.

Knowledge and Performance

- Increased visibility of initiatives and leadership in knowledge management. Characterized by a structured approach to implement and modify management directed to barriers and risks [23].

- The most relevant sustainability issues are respected in the relevant business processes [13].

- Limited internal reports. The reports are only for top management. The scope of the report: only one aspect of the TBL [8].

- Participation in three items related to global sustainability standards (GRI, CDP, ISO 14000 and ISO 26000, United Nations Global Compact) [25].

- Limited internal benchmarking. Comparison of environmental performance with the goal set by top management. The scope of benchmarking is only for a single aspect of the TBL [8].

- Limited internal training. Training given to the main business managers to generate awareness about sustainability. Training focused on one aspect of TBL [8].

4.2.8. Description of the Advanced Maturity Level

Environmental Risk

- The company complies with emission laws and regulations for air, water, and soil. In addition, it presents specific and conservative emission reduction targets [13].

- The company operates and complies with laws and regulations regarding hazardous waste. In addition, it presents specific and conservative targets for the issue of hazardous waste [13].

- The company regularly adopts some specific actions to minimize waste generation [15].

- For the “carbon footprint”, map the network to the coverage area based on the configuration of operations [15].

- Biodiversity and organizational impact on it in strategy, policy, and processes are considered [13].

Product Portfolio

- For the use of resources economic, technical and/ or environmental/social criteria are considered. Resource efficiency is measured for business processes; targets are set for resource management. The principles of sustainability are partially considered [13].

- LCA data is incorporated into decision-making by design teams and the LCA process is efficient and well established. However, LCA still has a high cost for the company [14].

- For remanufacturing, manufacturing processes are considered during the project and design teams reduce the impact of products by choosing a more sustainable production process. Design teams seek to minimize the impact of the product or service while in use by the customer. Design teams’ design considers what will happen to the product at the end of its useful life and the products are not yet designed to facilitate disassembly, recycling, and end-of-life reuse [17].

- Design teams’ design has consistent alternatives to reducing the environmental impact of products through material selection. However, it still adopts the financial cost as the main criterion for the selection of material [14].

Tools

- The company adopts five of the lean tools (5S; Andon, Just in Time, Kanban; Poka-Yoke; SMED and is in the final phase of application of the concept of TPM for reducing environmental impacts) [18].

Internal

- In most areas of the organization, measures are defined to encourage motivation for sustainability. Top management has an exemplary sustainability role [13].

- Health and safety are systematically planned and implemented in most areas of the company. Activities are defined to avoid long-term health and safety risks [13].

- The work environment considers all environmental impacts that may negatively influence people’s performance. With regard to security, the organization regularly invests in actions that aim to preserve the physical integrity of its employees. Workplace design essentially influences staff ergonomics [13].

- Some specific measures for the development of human capital are defined in relation to sustainability [13].

External

- There is the definition of corporate codes and guidelines on the (internal) behavior of the entire organization [13].

- The organization knows whom it sells its products to and establishes measures to reduce controversial activities [13].

- Corporate citizenship is systematically planned and conducted (monetary and nonmonetary commitment). There is a link between the projects and the corporate business [13].

Social Risk

- Rigorous analysis of internal sustainability practices. Risks of costs and implementation of changes arising from changes introduced in the structure and organizational processes evaluated internally. Risk assessment: environmental [8].

Return and Investment

Remanufacturing

Analysis and Results

- The company has some reports to determine the efforts directed to sustainability. In addition, there is an assessment of the impact of expenditure on sustainability [19].

Innovation and Technology

- Green IT within organizations is properly managed and governed, performing the monitoring, evaluation and measurement of green IT practices implemented, through a set of sustainability metrics established for this purpose [21].

- The implications of sustainability are an important and thoughtful consideration in most innovation efforts. Sustainability-based innovation efforts cover most business domains and are well understood with financial performance. Some innovations for sustainability processes and results are benchmarking of quality and considered as good practices by nature [19].

Supply

- Review and strengthen the sustainable supply strategy, recognizing in particular the potential of new technologies. Try to link the strategy to environmental management programs and systems and include it in the company’s overall strategy [22].

- Detailed sustainability risks assessed for high impact contracts and implemented sustainability governance contracts/projects. [22].

- Sustainability audits and supply chain improvement programs in place. Key suppliers oriented to intensive development. Achievements are formally recorded [22].

Strategic

- The company is focused on mandatory and voluntary corporate governance structures. Other measures aimed at ensuring corporate transparency [13].

- Implementation of external benchmarking in internally driven goals in relation to strategic and business vision [15]. Sustainability in the process of insertion in the mission and vision of the organization; the concept of TBL begins to achieve profound relevance for the result and sustainability measures and metrics are reported regularly and consistently [14].

- Limited understanding of the overlapping of elements of the value chain between project portfolios in relation to project and program portfolio management [15].

- Fully managed positioning with clear plan to achieve the best supply of product service systems in the sector [15].

- Communication and collaboration with stakeholders on sustainability issues [13].

Stakeholders

- To manage the relationship of suppliers, customers, and society, upstream and downstream partners are tracked and/or trained in occupational health and safety, child labor and/or human rights programs [1].

Knowledge and Performance

- Improvement of the performance of activities related to knowledge management. Characterized by an increase in emphasis on the specific use of qualitative and quantitative methods to measure and monitor the performance of knowledge management and justify knowledge management initiatives [23].

- Relevant sustainability issues are respected in business and support processes [13].

- Broader internal reports. Both for top management and for all management layers. Increased transparency in reports. Scope of reports: environmental and social [8].

- Participation in all items of GRI, CDP, ISO 14000 and ISO 26000, United Nations Global Compact [25].

- Strict internal benchmarking. The comparison is made between several organizational units over time and in relation to the goals established by the high management level. The scope of benchmarking refers to environmental and social aspects [8].

- Broader internal training. Training (environmental and social) given to leading business managers and supervisory staff to develop awareness of sustainability about making information-based and sustainable decisions [8].

4.2.9. Description of the Level of Sustainable Maturity

Environmental Risk

- The company complies with emission laws and regulations for air, water, and soil (e.g., evaluation of the best techniques). Ambitious emission reduction targets are set [13].

- The company operates and complies with laws and regulations regarding hazardous waste. Ambitious targets are set for the issue of hazardous waste [13].

- For waste minimization, the Global Product Lifecycle/Example Management Service System integrated with the business strategy [15].

- Evidence of reconfiguration of operations to minimize the “carbon footprint” [15].

- Notable activities and approaches are implemented in order to reduce the organizational impact on biodiversity [13].

Product Portfolio

- For the use of resources a combination of economic, technical, environmental, and social criteria is considered. Resource efficiency is controlled for all processes. The long-term resource management strategy is aligned with the principles of sustainability [13].

- LCA data are incorporated into the decision-making by the design teams and the LCA process is well established, efficient, and inexpensive [14].

- For remanufacturing, manufacturing processes are considered during the project and design teams reduce the impact of products by choosing a more sustainable production process. Design teams seek to minimize the impact of the product or service while in use by the customer. Design teams’ design considers what will happen to the product at the end of its useful life and the products are designed to facilitate disassembly, recycling, and end-of-life reuse [17].

- Design teams’ design has consistent alternatives to reducing the environmental impact of products through material selection. The company adopts both the financial and environmental cost as well as criteria for the selection of materials [14].

Tools

- The company adopts all lean tools (5S; Andon, Just in Time, Kanban; Poka-Yoke; SMED and fully applies the concept of TPM for reducing environmental impacts) [18].

Internal

- Senior management has an exemplary role when it comes to sustainability issues. Employees are efficiently supported by appropriate incentives and motivations (monetary and nonmonetary). Because of this, the principles of sustainability are internalized and change behavior [13].

- The health and safety approach supports organizational goals toward sustainability. It is systematically planned and deployed throughout the enterprise. Activities are defined to avoid long-term health and safety risks and are consequently improved [13].

- The work environment considers all environmental impacts that may negatively influence people’s performance. With regard to security, the organization regularly invests in actions that aim to preserve the physical integrity of its employees. Workplace design positively influences the ergonomics, attitudes, motivation, and behavior of staff [13].

- Various education programs and measures are offered. Every employee is trained in sustainability issues [13].

External

- The organization is known as a noncontroversial operating company. It shows credibility in that it offers and follows possibilities to avoid the negative use of its products, based on the requirements of stakeholders [13].

- Corporate citizenship is systematically planned and conducted (monetary and nonmonetary commitment) and focused on long-term commitment. Most employees are integrated into the process. There is a link between the organization’s projects and the corporate business [13].

Social Risk

- Risk analysis in supply chains. Cost and implementation risks arising from the application of sustainability practices are fully assessed with partners. Risk assessment is directed to environmental aspects [8].

Return and Investment

- Revenue related to innovation is of strategic importance to the company and significantly guides reinvestment (with quantifiable expected return) in the research and development strategy. Most innovation efforts are based on previously established planning, with many projects based on long-term trends and opportunities. The innovation, research, and development strategy is directly linked to the economic aspects of sustainability [19].

- There is a broader scope of spending on supply chain suppliers (including fair trade throughout the chain) [1].

Remanufacturing

- Implementation of advanced optimization methods in operator/worker management and include the optimization of processes in daily work for the issue of inventory in remanufacturing [17].

- Implementation of advanced optimization methods in operator/worker management and include the optimization of processes in daily work for the issue of scrap/rework in remanufacturing [17].

- The company makes regular investments and presents a specific budget for the internal physical arrangement of the plant with the objective of achieving sustainability [17].

Analysis and Results

- The company has specific reports for the investigation of efforts directed to sustainability. In addition, there is an assessment of the impact of expenditure on sustainability [19].

Innovation and Technology

- The organization is fully committed to sustainability and is oriented towards the continuous improvement of green IT practices implemented through detailed performance reports, exhaustive use of sustainability metrics and management of the sustainability innovation process [21].

- All innovation efforts explicitly incorporate sustainability considerations. The supplier selection process includes evaluating their ability to collaborate on sustainability issues related to efforts for business innovation through the TBL. The company is an industry leader in sustainability innovation efforts and results [19].

Supply

- The strategy is regularly reviewed, examined externally and directly linked to the program and environmental management system of organizations. A detailed review is carried out to determine future priorities and a new strategy beyond this framework is developed [22].

- Best practices shared with other organizations and key sustainability performance indicators agreed with key suppliers [22].

- Suppliers recognized as essential for the implementation of the sustainable supply strategy of organizations. Best practices shared with other/peer organizations [22].

Strategic

- The company is focused on mandatory and voluntary corporate governance structures. Other measures aimed at ensuring corporate transparency. Proactive commitment to the strictest rules [13].

- Implementation of goals and results defined by the client in relation to strategic and business vision [15]. Sustainability fits into the organization’s mission and vision; the concept of TBL has deep relevance to the result and sustainability measures and metrics are reported regularly and consistently [14].

- Integrated value chain with external benchmarking in relation to project and program portfolio management [15].

- Leadership strategy in the customer-centric sector and supported by a sustainable product service system [15].

- Communication and collaboration with stakeholders. The company has a leading role and proactivity in creating these sustainability-related networks [13].

Stakeholders

- To manage the relationship of suppliers, customers, and society, the relationship management scheme goes beyond upstream and downstream partners to include the management of the impact of operations on communities [1].

Knowledge and Performance

- Sustain the performance of activities related to knowledge management. The expectation regarding knowledge management is to compose the normal routine, disseminated within the organization, as well as to be an integral part of organizational culture, employee behavior, business processes, and product development [23].

- Sustainability issues are respected in business and support processes in a sufficiently efficient manner. Roles and responsibilities are defined [13].

- Internal and external reports. External reporting may involve reporting to regulators and the general public. Scope of reports: environmental and social [8].

- Participation in all items of GRI, CDP, ISO 14000 and ISO 26000, United Nations Global Compact. Commitment to sustainability standards. Creative development of new sustainable capacities [25].

- Internal and external benchmarking. The comparison is made between multiple organizational units over time and between members of the supply chain. The scope of benchmarking is both for environmental and social aspects [8].

- Training of internal and business partners. Training given to internal managers, supervisors, and business partners involved in sustainability practices. Training focuses on environmental and social aspects [8].

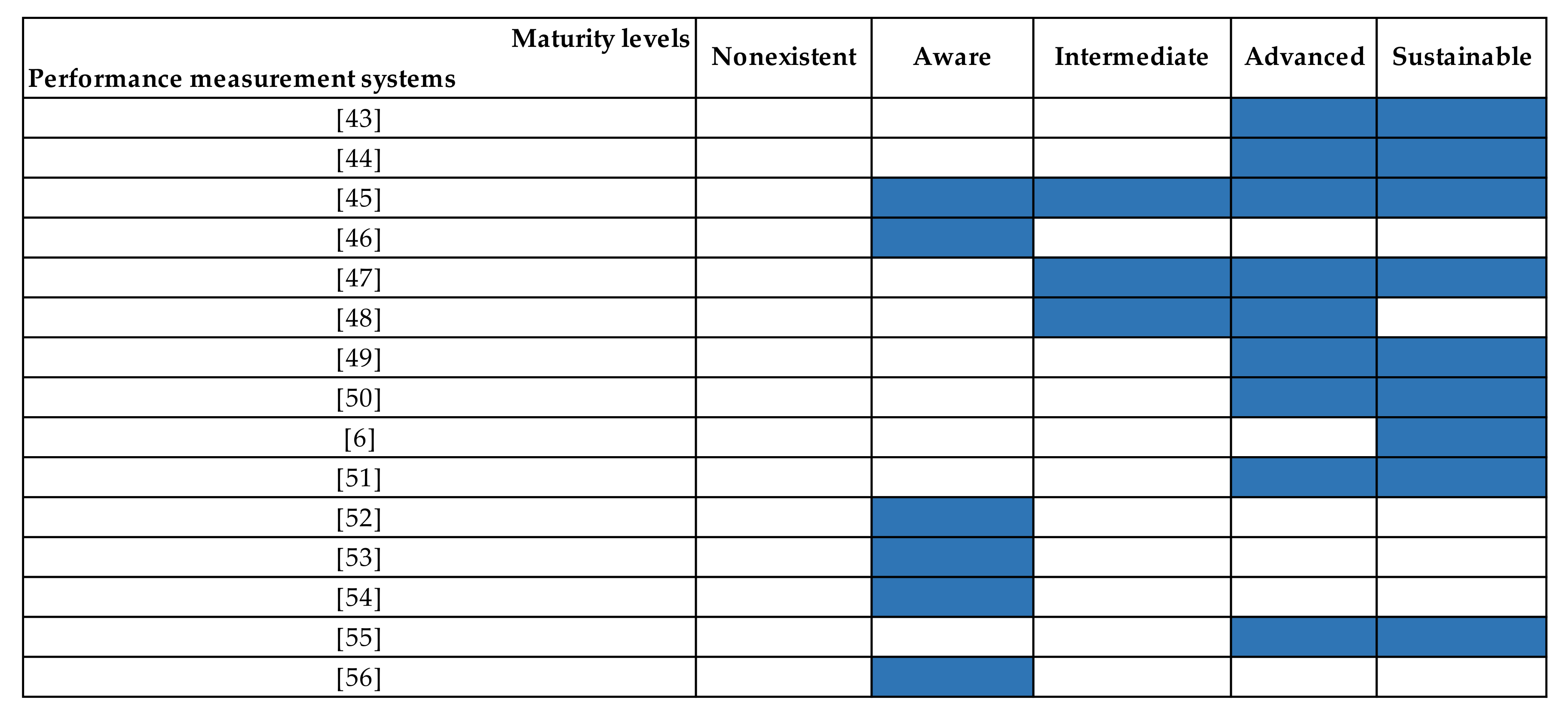

4.3. Classification of Performance Measurement Systems at Maturity Level in the Basic Theoretical Model

4.4. Proposed Theoretical Model

4.5. Discussion and General Considerations about the Model

- Compliance with laws and regulations concerning emissions to air, water, and soil, with specific targets for these issues. In addition, you should consider compliance with laws and regulations concerning hazardous waste (e.g., assessment of best techniques).

- Minimization of hazardous waste.

- Risks of cost and implementation of sustainable practices with the entire supply chain.

- “Carbon footprint”.

- Biodiversity.

- Use of resources (materials, energy, and recycling) and selection of parts/materials considered specific criteria.

- LCA is incorporated in its development. In this case, it is relevant to consider aspects of remanufacturing.

- Use of tools linked to the lean concept to reduce environmental impacts.

- The strategic level of organizations has an exemplary function with regard to sustainability issues and the incentives and motivations (monetary and nonmonetary) are appropriate.

- The health and safety approach supports organizational goals towards sustainability.

- Environmental impacts that negatively influence employee performance.

- Specific programs for training employees in issues involving sustainability.

- Definition of corporate codes and guidelines on (internal) behavior throughout the organization.

- The company demonstrates credibility to the extent that it offers and follows possibilities of avoiding the negative use of its products, based on the requirements of the interested parties.

- Corporate citizenship is systematically planned and conducted (monetary and nonmonetary commitment) and focused on long-term commitment.

- Analysis of cost risks and implementation of sustainable practices with the entire supply chain.

- Innovation-related revenue is of strategic importance to the company and significantly guides reinvestment (with quantifiable expected returns) in the strategy of research and development. Most innovation efforts are based on pre-established planning, with many projects based on long-term trends and opportunities.

- Evaluation of supply chain supplier spending, with the inclusion of fair trade throughout the chain.

- Evaluation if the organization maintains a permanent control of parts and materials used for the remanufacturing process.

- Cost evaluation for materials that will no longer be reused and activities that need to be performed again.

- Costs related to the internal physical arrangement of the plant to achieve sustainability.

- Evaluation of the existence of specific reports for the measurement of efforts towards sustainability.

- Assessment of whether the company is oriented toward green IT practices.

- Sustainable innovation is widespread throughout the company, partners and supply chain relationships. The result of sustainable innovation is linked to the supply of a sustainable product in all its aspects.

- Environmental criteria for the purchasing process.

- Focus on sustainability in the relationship with suppliers.

- Procurement strategy regularly reviewed and linked to the company’s environmental system.

- Evaluation of the sharing of best practices with other organizations and key performance indicators agreed with suppliers.

- The organization rewards suppliers recognized as essential for the implementation of the sustainable sourcing strategy.

- Evaluation of mandatory and voluntary corporate governance structures.

- Sustainability fits the mission and vision of the company

- Integration of the value chain.

- Implements external benchmarking.

- Industry leadership strategy that is customer focused and based on a sustainable product service system.

- Communication and collaboration with stakeholders.

- Proactive trend monitoring and behavior.

- Relationship goes beyond upstream and downstream supply chain partners to include managing the impact of operations on communities.

- Customer needs addressed by the design team.

- In the company–client relationship, value is added for both parties.

- Systematic and comprehensive activities for knowledge management related to sustainability.

- Sustainability issues present in business and support processes.

- Defined roles and responsibilities.

- Corporate communication in relation to sustainability issues.

- Collection of internal and external data. Data is collected from most members of the supply chain.

- Participation in all GRI, CDP, ISO 14000 and ISO 26000 items, United Nations Global Compact.

- External and internal benchmarking, involving environmental and social issues.

- Training given to internal managers, supervisors and business partners involved in sustainability practices.

- The organization presents five perspectives for its performance measurement system: internal performance within units (e.g., materials management, production, distribution), external performance among the different units of the company; external performance of the whole company in relation to customers; supplier performance in relation to the company and relationship between logistics performance and the performance of the whole company.

- The performance measurement system focuses on four basic processes: planning (demand/supply planning and plan infrastructure), supply (sourcing/acquisition of materials), do (production execution) and deliver (demand management, order management, warehouse management, transportation management, facility management, and delivery infrastructure).

- The performance measurement system operates from four perspectives: financial, customer, business process (internal and external), and learning and growth, focused on the supply chain.

- The performance measurement system operates from four perspectives focused on sustainability issues: financial (examples: revenues from “green” products and avoiding costs with environmental actions), customer (examples: functional eco-efficiency of the product and green products), business process (examples: greenhouse gas emissions, energy consumption, and accidents and spills) and learning/growth (examples: community complaints, functions with environmental responsibilities, and emergency response programs).

- The performance measurement system merges two concepts: BSC and SCOR. In this case, four basic processes and four perspectives for the supply chain are considered.

- The level of maturity in sustainability in the supply chain will be evaluated based on the topics presented above. These items represent an essential roadmap for the application of the proposed model. Another important point is the scope of the items considered in terms of sustainability.

5. Conclusions and Recommendations

Author Contributions

Funding

Conflicts of Interest

References

- Okongwu, U.; Morimoto, R.; Lauras, M. The maturity of supply chain sustainability disclosure from a continuous improvement perspective. Int. J. Prod. Perform. Manag. 2013, 62, 827–855. [Google Scholar] [CrossRef]

- Lopes, L.J.; Pires, S.R.I. Green supply chain management in the automotive industry: A study in Brazil. Bus. Strat. Environ. 2020, 29, 2755–2769. [Google Scholar] [CrossRef]

- Council of Supply Chain Management Professionals (CSCMP). Available online: http://cscmp.org/ (accessed on 26 May 2020).

- Bertaglia, P.R. Logística e Gerenciamento da Cadeia de Abastecimento, 2nd ed.; Saraiva: São Paulo, Brazil, 2009; pp. 32–33. [Google Scholar]

- Govindan, K.; Soleimani, H.; Kannan, D. Reverse logistics and closed-loop supply chain: A comprehensive review to explore the future. Eur. J. Oper. Res. 2015, 240, 603–626. [Google Scholar] [CrossRef]

- Hervani, A.A.; Helms, M.M.; Sarkis, J. Performance measurement for green supply chain management. Benchmarking: Int. J. 2005, 12, 330–353. [Google Scholar] [CrossRef]

- Uygun, Ö.; Dede, A. Performance evaluation of green supply chain management using integrated fuzzy multi-criteria decision making techniques. Comput. Ind. Eng. 2016, 102, 502–511. [Google Scholar] [CrossRef]

- Kurnia, S.; Rahim, M.M.; Samson, D.; Prakash, S. Sustainable supply chain management capability maturity: Framework development and initial evaluation. In Proceedings of the European Conference on Information Systems (ECIS), Tel Aviv, Israel, 9–11 June 2014. [Google Scholar]

- Kumar, R.; Chandrakar, R. Overview of green supply chain management: Operation and environmental impact at different stages of the supply chain. Int. J. Eng. Adv. Technol. 2012, 1, 1–6. [Google Scholar]

- Correia, E.; Carvalho, H.; Azevedo, S.G.; Govindan, K. Maturity Models in Supply Chain Sustainability: A Systematic Literature Review. Sustainability 2017, 9, 64. [Google Scholar] [CrossRef]

- Roy, V.; Schoenherr, T.; Charan, P. The thematic landscape of literature in sustainable supply chain management (SSCM). Int. J. Oper. Prod. Manag. 2018, 38, 1091–1124. [Google Scholar] [CrossRef]

- Elkington, J. Enter the triple bottom line. In The Triple Bottom Line: Does It All Add Up? Henriques, A., Richardson, J., Eds.; Earthscan: London, UK, 2004. [Google Scholar]

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Hynds, E.J.; Brandt, V.; Burek, S.; Knox, P.; Parker, J.P.; Zietlow, M.; Schwartz, L.; Taylor, J.; Jäger, W. A Maturity Model for Sustainability in New Product Development. Res. Manag. 2014, 57, 50–57. [Google Scholar] [CrossRef]

- Srai, J.S.; Alinaghian, L.S.; Kirkwood, D.A. Understanding sustainable supply network capabilities of multinationals: A capability maturity model approach. Proc. Inst. Mech. Eng. Part B J. Eng. Manuf. 2013, 227, 595–615. [Google Scholar] [CrossRef]

- Rudnicka, A. How to manage sustainable supply chain? The issue of maturity. LogForum 2016, 12, 203–211. [Google Scholar] [CrossRef]

- Golinska, P.; Kuebler, F. The Method for Assessment of the Sustainability Maturity in Remanufacturing Companies. Procedia CIRP 2014, 15, 201–206. [Google Scholar] [CrossRef]

- Verrier, B.; Rose, B.; Caillaud, E. Lean and Green strategy: The Lean and Green House and maturity deployment model. J. Clean. Prod. 2016, 116, 150–156. [Google Scholar] [CrossRef]

- Edgeman, R.; Eskildsen, J. Modeling and Assessing Sustainable Enterprise Excellence. Bus. Strat. Environ. 2014, 23, 173–187. [Google Scholar] [CrossRef]

- Standing, C.; Jackson, P. An approach to sustainability for information systems. J. Syst. Inf. Technol. 2007, 9, 167–176. [Google Scholar] [CrossRef]

- Patón-Romero, J.D.; Baldassarre, M.T.; Rodriguez, M.; Piattini, M. Maturity model based on CMMI for governance and management of Green IT. IET Softw. 2019, 13, 555–563. [Google Scholar] [CrossRef]

- Tchokogué, A.; Nollet, J.; Merminod, N.; Paché, G.; Goupil, V. Is Supply’s Actual Contribution to Sustainable Development Strategic and Operational? Bus. Strategy Environ. 2018, 27, 336–358. [Google Scholar] [CrossRef]

- Robinson, H.; Anumba, C.; Carrillo, P.; Al-Ghassani, A. STEPS: A knowledge management maturity roadmap for corporate sustainability. Bus. Process. Manag. J. 2006, 12, 793–808. [Google Scholar] [CrossRef]

- Batista, L.; Dora, M.; Toth, J.; Molnár, A.; Malekpoor, H.; Kumari, S. Knowledge management for food supply chain synergies – a maturity level analysis of SME companies. Prod. Plan. Control. 2019, 30, 995–1004. [Google Scholar] [CrossRef]

- Babin, R.; Nicholson, B. How green is my outsourcer? Measuring sustainability in global IT outsourcing. Strat. Outsourcing: Int. J. 2011, 4, 47–66. [Google Scholar] [CrossRef]

- Gong, R.; Xue, J.; Zhao, L.; Zolotova, O.; Ji, X.; Xu, Y. A Bibliometric Analysis of Green Supply Chain Management Based on the Web of Science (WOS) Platform. Sustain. 2019, 11, 3459. [Google Scholar] [CrossRef]

- Zimon, D.; Tyan, J.; Sroufe, R. drivers of sustainable supply chain management: Practices to alignment with un sustainable development goals. Int. J. Qual. Res. 2020, 14, 219–236. [Google Scholar] [CrossRef]

- Zimon, D.; Tyan, J.; Sroufe, R. Implementing Sustainable Supply Chain Management: Reactive, Cooperative, and Dynamic Models. Sustainability 2019, 11, 7227. [Google Scholar] [CrossRef]

- Ahi, P.; Searcy, C. A comparative literature analysis of definitions for green and sustainable supply chain management. J. Clean. Prod. 2013, 52, 329–341. [Google Scholar] [CrossRef]

- Reefke, H.; Ahmed, M.D.; Sundaram, D. Sustainable Supply Chain Management—Decision Making and Support: The SSCM Maturity Model and System. Glob. Bus. Rev. 2014, 15, 1–12. [Google Scholar] [CrossRef]

- Estampe, D.; Lamouri, S.; Paris, J.-L.; Brahim-Djelloul, S. A framework for analysing supply chain performance evaluation models. Int. J. Prod. Econ. 2013, 142, 247–258. [Google Scholar] [CrossRef]

- Kovacheva, T.; Todorov, N. Optimizing software development process: A case study for integrated Agile-CMMI process model. In Proceedings of the 2011 IEEE EUROCON—International Conference on Computer as a Tool, Lisbon, Portugal, 27–29 April 2011; pp. 1–2. [Google Scholar]

- Pigosso, D.C.A.; Rozenfeld, H.; McAloone, T.C. Ecodesign maturity model: A management framework to support ecodesign implementation into manufacturing companies. J. Clean. Prod. 2013, 59, 160–173. [Google Scholar] [CrossRef]

- Aboelmaged, M.G. Linking operations performance to knowledge management capability: The mediating role of innovation performance. Prod. Plan. Control. 2014, 25, 44–58. [Google Scholar] [CrossRef]

- Bititci, U.S.; Garengo, P.; Ates, A.; Nudurupati, S.S. Value of maturity models in performance measurement. Int. J. Prod. Res. 2015, 53, 3062–3085. [Google Scholar] [CrossRef]

- Gouvinhas, R.P.; Reyes, T.; Naveiro, R.M.; Perry, N.; Filho, E.R. A proposed framework of sustainable self-evaluation maturity within companies: An exploratory study. Int. J. Interact. Des. Manuf. (IJIDeM) 2016, 10, 319–327. [Google Scholar] [CrossRef]

- Machado, C.G.; De Lima, E.P.; Da Costa, S.E.G.; Angelis, J.J.; Mattioda, R.A. Framing maturity based on sustainable operations management principles. Int. J. Prod. Econ. 2017, 190, 3–21. [Google Scholar] [CrossRef]

- Bastas, A.; Liyanage, K. Setting a framework for organisational sustainable development. Sustain. Prod. Consum. 2019, 20, 207–229. [Google Scholar] [CrossRef]

- Neely, A. The performance measurement revolution: Why now and what next? Int. J. Oper. Prod. Manag. 1999, 19, 205–228. [Google Scholar] [CrossRef]

- Bourne, M.; Neely, A.; Mills, J.; Platts, K. Implementing performance measurement systems: A literature review. Int. J. Bus. Perform. Manag. 2003, 5, 1–24. [Google Scholar] [CrossRef]

- Franco-Santos, M.; Kennerley, M.; Micheli, P.; Martinez, V.; Mason, S.; Marr, B.; Gray, D.; Neely, A. Towards a definition of a business performance measurement system. Int. J. Oper. Prod. Manag. 2007, 27, 784–801. [Google Scholar] [CrossRef]

- Hald, K.S.; Mouritsen, J. The evolution of performance measurement systems in a supply chain: A longitudinal case study on the role of interorganisational factors. Int. J. Prod. Econ. 2018, 205, 256–271. [Google Scholar] [CrossRef]

- Andersson, P.; Aronsson, H.; Storhagen, N.G. Measuring logistics performance. Eng. Costs Prod. Econ. 1989, 17, 253–262. [Google Scholar] [CrossRef]

- Stewart, G. Supply-chain operations reference model (SCOR): The first cross-industry framework for integrated supply-chain management. Logist. Inf. Manag. 1997, 10, 62–67. [Google Scholar] [CrossRef]

- Van Hoek, R.I. “Measuring the unmeasurable”—Measuring and improving performance in the supply chain. Supply Chain Manag. Int. J. 1998, 3, 187–192. [Google Scholar] [CrossRef]

- Beamon, B.M. Measuring supply chain performance. Int. J. Oper. Prod. Manag. 1999, 19, 275–292. [Google Scholar] [CrossRef]

- Holmberg, S. A systems perspective on supply chain measurements. Int. J. Phys. Distrib. Logist. Manag. 2000, 30, 847–868. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Patel, C.; Tirtiroglu, E. Performance measures and metrics in a supply chain environment. Int. J. Oper. Prod. Manag. 2001, 21, 71–87. [Google Scholar] [CrossRef]

- Park, J.H.; Lee, J.K.; Yoo, J.S. A framework for designing the balanced supply chain scorecard. Eur. J. Inf. Syst. 2005, 14, 335–346. [Google Scholar] [CrossRef]

- Bhagwat, R.; Sharma, M.K. Performance measurement of supply chain management: A balanced scorecard approach. Comput. Ind. Eng. 2007, 53, 43–62. [Google Scholar] [CrossRef]

- Thakkar, J.; Kanda, A.; Deshmukh, S. Supply chain performance measurement framework for small and medium scale enterprises. Benchmarking Int. J. 2009, 16, 702–723. [Google Scholar] [CrossRef]

- Hofmann, E.; Locker, A. Value-based performance measurement in supply chains: A case study from the packaging industry. Prod. Plan. Control. 2009, 20, 68–81. [Google Scholar] [CrossRef]

- Luzzini, D.; Caniato, F.; Spina, G. Designing vendor evaluation systems: An empirical analysis. J. Purch. Supply Manag. 2014, 20, 113–129. [Google Scholar] [CrossRef]

- Sillanpää, I. Empirical study of measuring supply chain performance. Benchmarking Int. J. 2015, 22, 290–308. [Google Scholar] [CrossRef]

- Laihonen, H.; Pekkola, S. Impacts of using a performance measurement system in supply chain management: A case study. Int. J. Prod. Res. 2016, 54, 5607–5617. [Google Scholar] [CrossRef]

- Jääskeläinen, A.; Thitz, O. Prerequisites for performance measurement supporting purchaser-supplier collaboration. Benchmark. Int. J. 2018, 25, 120–137. [Google Scholar] [CrossRef]

- Frederico, G.F.; Martins, R.A. Modelo para alinhamento entre a maturidade dos sistemas de medição de desempenho e a maturidade da gestão da cadeia de suprimentos. Gest. Prod. 2012, 19, 857–871. [Google Scholar] [CrossRef]

- Neto, M.S.; Pires, S.R.I. Medição de desempenho em cadeias de suprimentos: Um estudo na indústria automobilística. Gest. Prod. 2012, 19, 733–746. [Google Scholar] [CrossRef][Green Version]

- Morgan, C. Structure, speed and salience: Performance measurement in the supply chain. Bus. Process. Manag. J. 2004, 10, 522–536. [Google Scholar] [CrossRef]

- Lockamy, A., III; McCormack, K. Linking SCOR planning practices to supply chain performance. Int. J. Oper. Prod. Manag. 2004, 24, 1192–1218. [Google Scholar] [CrossRef]

- Ayers, J.B.; Malmberg, D.M. Supply chain systems: Are you ready? Infor. Strategy Exec. J. 2002, 19, 18–27. [Google Scholar]

- Bell, E.; Bryman, A.; Harley, B. Business Research Methods, 5th ed.; Oxford University Press: New York, NY, USA, 2018; pp. 20–25. [Google Scholar]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Briner, R.B.; Denyer, D. Handbook of Evidence-Based Management: Companies, Classrooms and Research Systematic Review and Evidence Synthesis as a Practice and Scholarship Tool, 1st ed.; Oxford University Press: New York, NY, USA, 2012; pp. 112–129. [Google Scholar]

- Rousseau, D.M.; Manning, J.; Denyer, D. Evidence in management and organizational science: Assembling the field’s full weight of scientific knowledge through syntheses. Acad. Manag. Ann. 2008, 2, 475–515. [Google Scholar] [CrossRef]

- Yatskovskaya, E.; Srai, J.S.; Kumar, M. Integrated Supply Network Maturity Model: Water Scarcity Perspective. Sustainability 2018, 10, 896. [Google Scholar] [CrossRef]

- Rauch, E.; Unterhofer, M.; Rojas, R.A.; Gualtieri, L.; Woschank, M.; Matt, D.T. A Maturity Level-Based Assessment Tool to Enhance the Implementation of Industry 4.0 in Small and Medium-Sized Enterprises. Sustainability 2020, 12, 3559. [Google Scholar] [CrossRef]

- Xavier, A.; Reyes, T.; Aoussat, A.; Luiz, L.; De Souza, L.M. Eco-Innovation Maturity Model: A Framework to Support the Evolution of Eco-Innovation Integration in Companies. Sustainability 2020, 12, 3773. [Google Scholar] [CrossRef]

- Yang, J.Y.; Roh, T. Open for Green Innovation: From the Perspective of Green Process and Green Consumer Innovation. Sustainability 2019, 11, 3234. [Google Scholar] [CrossRef]

- Aarstad, J.; Jakobsen, S.-E. Norwegian Firms’ Green and New Industry Strategies: A Dual Challenge. Sustainability 2020, 12, 361. [Google Scholar] [CrossRef]

- Kusi-Sarpong, S.; Gupta, H.; Sarkis, J. A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 2019, 57, 1990–2008. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainable supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Authors | Description of the Model |

|---|---|

| [23] | Establishes five levels of maturity of knowledge management, and the high level of maturity is directly related to the ability to implement the principles of sustainability. |

| [20] | Integrates sustainability with the systems area and is based on Control Objectives for Information and related Technology (COBIT) concepts; presents six levels of maturity. |

| [13] | Presents three relevant dimensions in relation to sustainability and four levels of maturity. |

| [25] | Focuses on the sustainability of providers offering Information Technology (IT) at the global level; represents a robust way to identify, classify, and evaluate the sustainability capacity of these providers. |

| [33] | Aggregates some practices that integrate the environmental eco-design process in the development of related products and processes. |

| [15] | Adopts a network and a Triple Bottom Line (TBL) perspective that allows for a systematic analysis and evaluation of practices that support sustainable operations; considers five capacity groups and five maturity levels. |

| [1] | Aims to improve knowledge about the maturity levels achieved by organizations by communicating sustainability initiatives to companies that might or might not be involved in the supply chain. |

| [14] | Focuses on the development of new products. |

| [8] | Focuses on evaluating capabilities to implement sustainable supply chain practices; identifies four categories of organizations that differ in the status of their respective maturity levels in Sustainable Supply Chain Management (SSCM) capabilities. |

| [17] | Focuses on the sustainability of remanufacturing for companies using the TBL approach. The goal of the maturity model is to identify the potential for optimizing resource utilization. |

| [30] | Presents six maturity levels, and for each of the levels a description, goals and requirements are provided. |

| [19] | Proposes a system of sustainable business excellence that emphasizes the financial stability of the company while addressing social and environmental challenges. The model considers six elements, called ‘compass dimensions’ (from strategy and governance to the results of human capital), and five levels of maturity. |

| [16] | Presents six drivers: knowledge; impact; social risk; environmental risk; cooperation, and communication; includes five levels of maturity. |

| [18] | Establishes an important relationship between lean waste and associated green impacts and presents five maturity levels. |

| [36] | Structured based on six levels of maturity, namely: completely immature companies; immature enterprises; companies at initial maturity; mature enterprises; mature/education enterprises and integrated enterprises. |

| [37] | Establishes management principles for the maturity framework based on sustainable operations. |

| [22] | Assesses the level of sustainable management of the supply process within an organization; addresses the question of how sustainable purchasing practices are effectively used as a leverage effect for sustainable development; includes five phases and five management dimensions. |

| [21] | Is based on the Capability Maturity Model Integration (CMMI) through which you want organizations to gradually implement and improve, through different levels of maturity, governance and green IT management. |

| [24] | Uses as reference the CMMI model and the maturity levels specified by [32]; considers five levels of maturity that include the interorganizational relationship of the supply chain and the relevant societal aspects. |

| [38] | Aims to perform the organizational integration of sustainability outlined in the concepts of TBL through quality management and supply chain. |

| Authors | Main Features |

|---|---|

| [43] | Balances financial measurement methods and projected physical measurements (productivity, lead times, quality, customer service, turnover rates, etc.) |

| [44] | Integrates internal and external improvement based on supply chain compression into four areas: planning, supplying, making/assembling, and delivering. |

| [45] | Establishes the evolution of the cost-effectiveness (basic) level performance measurement system for integration (integration of the performance measurement system, considering the supply chain as a whole). |

| [46] | Presents the three elements that should be present in a performance measurement system: resource measures (R), output measures (O), and flexibility measures (F). |

| [47] | Adopts a systemic perspective to explain the challenges and opportunities related to the application of supply chain metrics. |

| [48] | Aligns financial and nonfinancial metrics with the four areas of the supply chain, namely: planning, supplying, making/assembling, and delivering. |

| [49] | Merges Balanced Scored Card (BSC)-related concepts and supply and chain management produced the Balanced Supply Chain Scorecard (BSCS). |

| [50] | Develops a BSC for Supply Chain Management (SCM) and illustrates the ways BSC was developed and applied in small and medium-sized enterprises. Structured in four perspectives: financial; performance for the customer; innovation/learning; and performance for the internal business perspective. |

| [51] | Develops a system and performance measurement based on BSC and Supply Chain Operations Reference (SCOR) for the case of small and medium enterprises. |

| [52] | Analyzes the development of a value-based performance measurement concept in supply chains by means of a case study of the packaging industry. |

| [53] | Considers three components of the model related to the supplier evaluation system, namely: strategic alignment, configuration process and execution. |

| [54] | Creates and verifies a supply chain measurement framework for the manufacturing industry. The aforementioned measurement structure is linked to four indicators: order book analysis; profitability; time; and management analysis. |

| [55] | It examines how the use of a new performance measurement system influences the SCM and what kind of impacts the new system has on supply chain performance. The impacts of a performance measurement system under the supply chain can be categorized as: (1) impacts on people’s behavior; (2) impacts on organizational capabilities; and (3) impacts on performance. |

| [56] | Explores the prerequisites for the performance measurement system to support buyer-vendor relationships and value co-creation. For this, some prerequisites must be met: the non-financial perspective of the measurement and the nonstandard nature of the measurement. |

| Models | Limitations Identified |

|---|---|

| [23] | Focus on only one aspect of the supply chain (knowledge management) and the model does not clarify how alternatives could be prioritized for permanence or elevation of the level of maturity. |

| [20] | Emphasis on only one aspect of the supply chain (information systems), low level of detail of the characteristic elements of the model, absence of a method for prioritizing clear actions for permanence or elevation of the level of maturity and the lack of a practical application to prove or adjust the premises of the model. |

| [13] | Generic approach to economic sustainability, with the insertion of a series of elements that do not present a clear relationship with the economic dimension of the TBL. In addition, this model uses the analytical research method [10]. In this case, there was no finding or adjustment of its theoretical postulates. Another important point is that the model does not elucidate the means for permanence or elevation of the maturity level. |

| [25] | Focus on one aspect of the supply chain (assessing IT vendor capacity at the global level) and the model does not clarify how alternatives could be prioritized for permanence or elevation of maturity level. |

| [33] | The model is concentrated in only one aspect of the supply chain (eco-design) and the absence of a method for identifying the order of priorities of the actions to be performed for permanence or elevation of the level and maturity. |

| [15] | Absence of direct relationship of the characteristic elements of the model with the dimensions determined in the TBL concept. Remembering that this concept is truly relevant for the understanding of organizational sustainability. Another relevant point is that the model does not establish a method to list the alternatives to be prioritized for the permanence or elevation of the maturity level. |

| [1] | Focus on only one aspect of the supply chain (investigating the maturity levels achieved by organizations in reporting their supply chain sustainability initiatives) and the absence of a method to determine which aspects should be prioritized for the permanence or elevation of the maturity level. |

| [30] | The model does not clearly present its characteristic elements. In addition, this model uses the analytical research method [10]. In this case, there was no proof or adjustment of its theoretical premises. Another significant aspect is the absence of a method for prioritizing clear actions for permanence or elevation of the maturity level. |