Research on Pharmaceutical Product Life Cycle Patterns for Sustainable Growth

, ,

, ,

Abstract

1. Introduction

2. Materials and Methods

2.1. Data

2.2. Analysis

2.2.1. Changes in Top-Selling Drug Therapeutic Area, Drug Modality, and Geographic Strategy

2.2.2. Investigation of Blockbuster Life Cycle Patterns

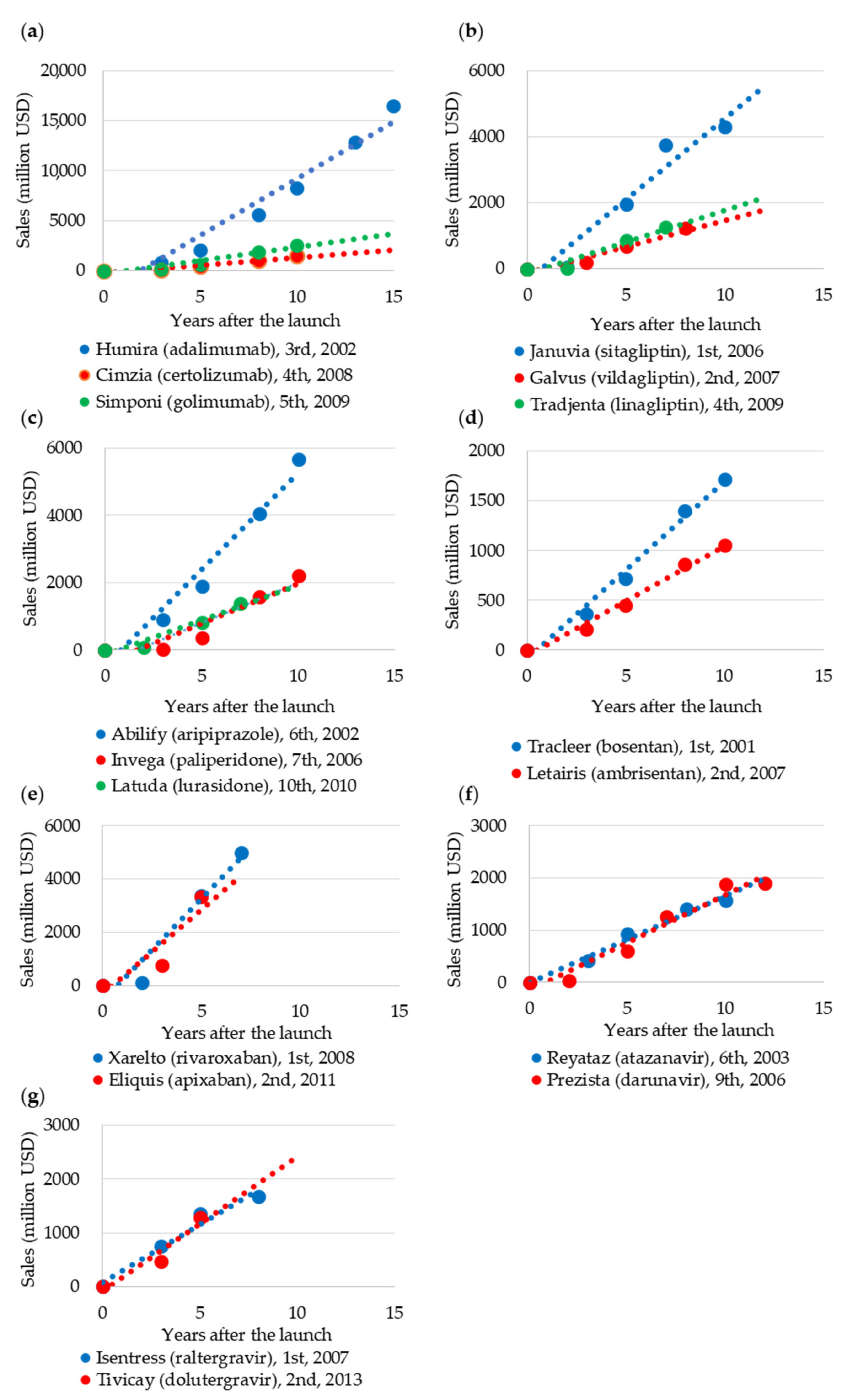

2.2.3. Blockbuster Life Cycle Patterns: Case Study

3. Results

3.1. Changes in Top-Selling Drug Therapeutic Area, Modality, and Geographic Strategy

3.2. Blockbuster Product Life Cycle Patterns

3.3. Case Study of Blockbuster Product Life Cycle Patterns

4. Discussion and Implications

5. Conclusions, Limitations, and Future Directions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- DiMasia, J.A.; Grabowski, H.G. The cost of biopharmaceutical R&D: Is biotech different? Manag. Decis. Econ. 2007, 28, 469–479. [Google Scholar]

- Paul, S.M.; Mytelka, D.S.; Dunwiddle, C.T.; Persinger, C.C.; Munos, B.H.; Lindborg, S.R.; Schach t, A.L. How to improve R&D productivity: The pharmaceutical industry’s grand challenge. Nat. Rev. Drug Discov. 2010, 9, 203–214. [Google Scholar] [PubMed]

- Farrell, D. Beyond offshoring: Assess your company’s global potential. Harv. Bus. Rev. 2004, 82, 82–90. [Google Scholar] [PubMed]

- Glickman, S.W.; McHutchison, J.G.; Peterson, E.D.; Cairns, C.B.; Harrington, R.A.; Califf, R.M.; Schulman, K.A. Ethical and scientific implications of the globalization of clinical research. N. Engl. J. Med. 2009, 360, 816–823. [Google Scholar] [CrossRef]

- Jeong, S.; Sohn, M.; Kim, J.H.; Ko, M.; Seo, H.; Song, Y.K.; Choi, B.; Han, N.; Na, H.S.; Lee, J.G.; et al. Current globalization of drug interventional clinical trials: Characteristics and associated factors, 2011–2013. Trials 2017, 18, 288. [Google Scholar] [CrossRef]

- Moorkens, E.; Meuwissen, N.; Huys, I.; Declerck, P.; Vulto, A.G.; Simoens, S. The market of biopharmaceutical medicines: A snapshot of a diverse industrial landscape. Front. Pharm. 2017, 8, 314. [Google Scholar] [CrossRef]

- Pharmaceuticals and Medical Devices Agency. Annual Reports. Available online: https://www.pmda.go.jp/english/about-pmda/annual-reports/0001.html (accessed on 25 August 2020).

- Slywotzky, A.J. The Art of Profitability; Warner Business Books: New York, NY, USA, 2002. [Google Scholar]

- Cutler, D. The demise of the blockbuster? New Engl. J. Med. 2007, 356, 1292–1293. [Google Scholar] [CrossRef]

- Nickisch, K.; Greuel, J.; Bode-Greuel, K. How can pharmaceutical and biotechnology companies maintain a high profitability? J. Commer. Biotechnol. 2009, 15, 309–323. [Google Scholar] [CrossRef]

- Montalban, M.; Sakinç, M.E. Financialization and productive models in the pharmaceutical industry. Ind. Corp. Chang. 2013, 22, 981–1030. [Google Scholar] [CrossRef]

- Anusha, K.; Krishna, P.; Kumar, V.P. Pharmaceutical product management. Pharma Innov. J. 2017, 6, 112–114. [Google Scholar]

- Vockley, J.G.; Niederhuber, J.E. Diagnosis and treatment of cancer using genomics. Br. Med. J. 2015, 350. Available online: www.jstor.org/stable/26520084 (accessed on 26 September 2020). [CrossRef]

- Friedman, A.A.; Letai, A.; Fisher, D.E.; Flaherty, K.T. Precision medicine for cancer with next-generation functional diagnostics. Nat. Rev. Cancer 2015, 15, 747–756. [Google Scholar] [CrossRef] [PubMed]

- Bentley, A.R.; Callier, S.; Rotimi, C.N. Diversity and inclusion in genomic research: Why the uneven progress? J. Community Genet. 2017, 8, 255–266. [Google Scholar] [CrossRef] [PubMed]

- Exchange Rates. Available online: http://data.imf.org/?sk=4C514D48-B6BA-49ED-8AB9-52B0C1A0179B&sId=1409151240976 (accessed on 27 September 2018).

- Rugman, A.M.; Verbeke, A. A perspective of regional and global strategies of multinational enterprises. J. Int. Bus. Stud. 2004, 35, 3–18. [Google Scholar] [CrossRef]

- Ohmae, K. Triad Power: The Coming Shape of Global Competition; The Free Press: New York, NY, USA, 1985. [Google Scholar]

- Gautam, A.; Pan, X. The changing model of big pharma: Impact of key trends. Drug Discov. Today 2016, 21, 379–384. [Google Scholar] [CrossRef]

- Teramae, F.; Makino, T.; Lim, Y.; Sengoku, S.; Kodama, K. International strategy for sustainable growth in multinational pharmaceutical companies. Sustainability 2020, 12, 867. [Google Scholar] [CrossRef]

- KEGG DRUG Database. Available online: https://www.kegg.jp/kegg/drug/drug_ja.html (accessed on 26 August 2020).

- Anderson, C.R.; Zeithaml, C.P. Stage of the product life cycle, business strategy, and business performance. Acad. Manag. J. 1984, 27, 5–24. [Google Scholar]

- Lehner, F. Software life cycle management based on a phase distinction method. Microproc. Microprogr. 1991, 32, 603–608. [Google Scholar] [CrossRef]

- Witte, R.S.; Witte, J.S. Statistics, 11th ed.; Wiley: Hoboken, NJ, USA, 2017. [Google Scholar]

- Schulze, U.; Ringel, M. What matters most in commercial success: First-in-class or best-in-class? Nat. Rev. Drug Discov. 2013, 12, 419–420. [Google Scholar] [CrossRef]

- Lieberman, M.B.; Montgomery, D.B. Conundra and progress: Research on entry order and performance. Long Range Plan. 2013, 46, 312–324. [Google Scholar] [CrossRef]

- Zachary, M.A.; Gianiodis, P.T.; Payne, G.T.; Markman, G.D. Entry timing: Enduring lessons and future directions. J. Manag. 2015, 41, 1388–1415. [Google Scholar] [CrossRef]

- Gudiksen, M.; Fleming, E.; Furstenthal, L.; Ma, P. What drives success for specialty pharmaceuticals? Nat. Rev. Drug Discov. 2009, 7, 563–567. [Google Scholar] [CrossRef] [PubMed]

- Lambkin, M. Order of entry and performance in new markets. Strat. Manag. J. 1988, 9, 127–140. [Google Scholar] [CrossRef]

- Lilien, G.; Yoon, E. The timing of competitive market entry. Manag. Sci. 1990, 36, 568–585. [Google Scholar] [CrossRef]

- Lambkin, M. Pioneering new markets: A comparison of market share winners and losers. Int. J. Res. Mark. 1992, 9, 5–22. [Google Scholar] [CrossRef]

- Gurumurthy, K.; Robinson, W.T.; Urban, G.L. Order of market entry: Established empirical generalizations, emerging empirical generalizations, and future research. Mark. Sci. 1995, 14, 212–221. [Google Scholar]

- Jensen, R. Innovative leadership: First mover advantages in new product adoption. Econ. Theory 2003, 21, 97–116. [Google Scholar] [CrossRef]

- Ouma, P.; Kilika, J.M. Innovation strategies, first mover advantage and performance in context of the microfinance sector: A review of literature. Int. J. Bus. Manag. 2018, 13, 195–209. [Google Scholar] [CrossRef]

- Rau, R. Adalimumab (a fully human anti- tumour necrosis factor alpha monoclonal antibody) in the treatment of active rheumatoid arthritis: The initial results of five trials. Ann. Rheum. Dis. 2002, 61, 70–73. [Google Scholar] [CrossRef]

- Goel, N.; Stephens, S. Certolizumab pegol. Mabs 2010, 2, 137–147. [Google Scholar] [CrossRef] [PubMed]

- Mazumdar, S.; Greenwald, D. Golimumab. Mabs 2009, 1, 422–431. [Google Scholar] [CrossRef]

- Evering, T.H.; Markowitz, M. Raltegravir (MK-0518): An integrase inhibitor for the treatment of HIV-1. Drugs Today 2007, 43, 865–877. [Google Scholar]

- Walmsley, S.L.; Antela, A.; Clumeck, N.; Duiculescu, D.; Eberhard, A.; Gutiérrez, F.; Hocqueloux, L.; Maggiolo, F.; Sandkovsky, U.; Granier, C.; et al. Dolutegravir plus abacavir-lamivudine for the treatment of HIV-1 infection. N. Engl. J. Med. 2013, 369, 1807–1818. [Google Scholar] [CrossRef]

- Balfour, J.A.B.; Plosker, G.L. Rosiglitazone. Drugs 1999, 57, 921–930. [Google Scholar] [CrossRef] [PubMed]

- Gillies, P.S.; Dunn, C.J. Pioglatizone. Drugs 2000, 60, 333–343. [Google Scholar] [CrossRef] [PubMed]

- Plourde, P.V.; Dyroff, M.; Dowsett, M.; Demers, L.; Yates, R.; Webster, A. ARIMIDEX: A new oral, once-a-day aromatase inhibitor. J. Steroid Biochem. Mol. Biol. 1995, 53, 175–179. [Google Scholar] [CrossRef]

- Trunet, P.F.; Bhatnagar, A.S.; Chaudri, H.A.; Hornberger, U. Letrozole (CGS 20267), a new oral aromatase inhibitor for the treatment of Advanced breast cancer in postmenopausal patients. Acta Oncol. 1996, 35, 15–18. [Google Scholar] [CrossRef] [PubMed]

- Booth, B.; Zemmel, R. Prospects for productivity. Nat. Rev. Drug Discov. 2004, 3, 451–456. [Google Scholar] [CrossRef]

- Kessel, M. The problems with today’s pharmaceutical business–an outsider’s view. Nat. Biotechnol. 2011, 29, 27–33. [Google Scholar] [CrossRef]

- Schuhmacher, A.; Germann, P.G.; Trill, H.; Gassmann, O. Models for open innovation in the pharmaceutical industry. Drug Discov. Today 2013, 18, 1133–1137. [Google Scholar] [CrossRef]

- Mazzola, E.; Bruccoleri, M.; Perrone, G. Open innovation and firms’ performance: State of the art and empirical evidences from the bio-pharmaceutical industry. Int. J. Technol. Manag. 2016, 70, 109–134. [Google Scholar] [CrossRef]

- Olk, P.; West, J. The relationship of industry structure to open innovation: Cooperative value creation in pharmaceutical consortia. RD Manag. 2020, 50, 116–135. [Google Scholar] [CrossRef]

- Attwood, M.M.; Rask-Andersen, M.; Schiöth, H.B. Orphan drugs and their impact on pharmaceutical development. Trends Pharm. Sci. 2018, 39, 525–535. [Google Scholar] [CrossRef]

- Kempf, L.; Goldsmith, J.C.; Temple, R. Challenges of developing and conducting clinical trials in rare disorders. Am. J. Med. Genet. 2018, 176, 773–783. [Google Scholar] [CrossRef]

- Hay, M.; Thomas, D.W.; Craighead, J.L.; Economides, C.; Rosenthal, J. Clinical development success rates for investigational drugs. Nat. Biotechnol. 2014, 32, 40–51. [Google Scholar] [CrossRef] [PubMed]

- Kola, I.; Landis, J. Can the pharmaceutical industry reduce attrition rates? Nat. Rev. 2004, 3, 711–715. [Google Scholar] [CrossRef]

- DiMasi, J.A.; Feldman, L.; Seckler, A.; Wilson, A. Trends in risks and associated with new drug development: Success rates for investigational drugs. Clin. Pharm. 2010, 87, 272–277. [Google Scholar] [CrossRef]

- Shukla, A.A.; Wolfe, L.S.; Mostafa, S.S.; Norman, C. Evolving trends in mAb production processes. Bioeng. Transl. Med. 2017, 2, 58–69. [Google Scholar] [CrossRef]

- Roque, A.C.A.; Lowe, C.R.; Taipa, M.Â. Antibodies and genetically engineered related molecules: Production and purification. Biotechnol. Progr. 2004, 20, 639–654. [Google Scholar] [CrossRef]

- Kleinman, M. Pharma Shifts Focus From Small Molecules to Biologics. PearlIRB 2012. Available online: https://www.pearlirb.com/pharma-shifts-focus-from-small-molecules-to-biologics/ (accessed on 6 October 2020).

- Teece, D.J. A dynamic capabilities-based entrepreneurial theory of the multinational enterprise. J. Int. Bus. Stud. 2014, 45, 8–37. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Therapeutic Areas/ Modalities | Cardio-Vascular Diseases | Infectious Diseases | Cancers | Endocrine and Metabolic Diseases | Central Nervous System Diseases | Immune System Diseases | Others | Total | |

|---|---|---|---|---|---|---|---|---|---|

| Small molecules | 2011 | 9 (17.6%) | 2 (3.9%) | 3 (5.9%) | 2 (3.9%) | 9 (17.6%) | 0 (0.0%) | 8 (15.7%) | 33 (64.7%) |

| 2017 | 4 (6.6%) | 5 (8.2%) | 7 (11.5%) | 2 (3.3%) | 3 (4.9%) | 0 (0.0%) | 8 (13.1%) | 29 (47.5%) | |

| Antibodies | 2011 | 0 (0.0%) | 0 (0.0%) | 3 (5.9%) | 0 (0.0%) | 0 (0.0%) | 2 (3.9%) | 1 (2.0%) | 6 (11.8%) |

| 2017 | 0 (0.0%) | 0 (0.0%) | 6 (9.8%) | 0 (0.0%) | 0 (0.0%) | 5 (8.2%) | 4 (6.6%) | 15 (24.6%) | |

| Hormones, proteins, and peptides | 2011 | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 3 (5.9%) | 0 (0.0%) | 1 (2.0%) | 5 (9.8%) | 9 (17.6%) |

| 2017 | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 6 (9.8%) | 0 (0.0%) | 2 (3.3%) | 6 (9.8%) | 14 (23.0%) | |

| Others | 2011 | 1 (2.0%) | 1 (2.0%) | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 1 (2.0%) | 3 (5.9%) |

| 2017 | 0 (0.0%) | 2 (3.3%) | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 0 (0.0%) | 1 (1.6%) | 3 (4.9%) | |

| Total | 2011 | 10 (19.6%) | 3 (5.9%) | 6 (11.8%) | 5 (9.8%) | 9 (17.6%) | 3 (5.9%) | 15 (29.4%) | 51 (100.0%) |

| 2017 | 4 (6.6%) | 7 (11.5%) | 13 (21.3%) | 8 (13.1%) | 3 (4.9%) | 7 (11.5%) | 19 (31.1%) | 61 (100.0%) |

| Internationalization | Global | Bi-Regional | Home Region-Oriented | Host Region-Oriented | Unknown | Total | |

|---|---|---|---|---|---|---|---|

| Drugs | 2011 | 5 (23.8%) | 2 (9.5%) | 10 (47.6%) | 4 (19.0%) | 30 | 51 |

| 2017 | 4 (8.2%) | 1 (2.0%) | 31 (63.3%) | 13 (26.5%) | 12 | 61 |

| Therapeutic Areas | Introduction and Growth | Maturity (Peak) | Decline | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Average Million USD/y (SD) | n | p | Average Million USD (SD) | n | p | Average Million USD/y (SD) | n | p | |

| Cardio-vascular diseases | +302.386 (211.750) | 20 | 0.752 | 3239.620 (2766.851) | 28 | 0.065 | −348.361 (419.697) | 28 | 0.040 |

| Infectious diseases | +455.033 (678.060) | 28 | 2005.968 (1907.527) | 23 | −346.970 (648.543) | 23 | |||

| Cancers | +325.549 (233.024) | 28 | 2372.785 (1864.003) | 21 | −166.948 (153.257) | 21 | |||

| Endocrine and metabolic diseases | +300.789 (155.375) | 10 | 3216.716 (2105.874) | 10 | −233.867 (354.692) | 10 | |||

| Central nervous system diseases | +239.942 (145.033) | 22 | 2573.470 (1415.890) | 29 | −295.959 (243.229) | 29 | |||

| Modalities | Introduction and Growth | Maturity (Peak) | Decline | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Average Million USD/y (SD) | n | p | Average Million USD (SD) | n | p | Average Million USD/y (SD) | n | p | |

| Small molecules | +330.110 (393.848) | 103 | 0.001 | 2578.793 (2007.308) | 122 | 0.204 | −291.860 (385.537) | 122 | 0.018 |

| Antibodies | +374.857 (258.018) | 20 | 4631.614 (3180.532) | 7 | −200.940 (177.354) | 7 | |||

| Hormones, proteins, and peptides | +212.266 (200.791) | 30 | 2359.080 (1706.421) | 26 | −159.113 (207.098) | 26 | |||

| Modalities | Introduction and Growth | Decline | ||||

|---|---|---|---|---|---|---|

| Small Molecules | Antibodies | Hormones, Proteins, and Peptides | Small Molecules | Antibodies | Hormones, Proteins, and Peptides | |

| Small molecules | - | = (p = 0.291) | > (p < 0.05) | - | = (p = 1.000) | > (p < 0.05) |

| Antibodies | = (p = 0.291) | - | > (p < 0.01) | = (p = 1.000) | - | = (p = 1.000) |

| Hormones, proteins, and peptides | < (p < 0.05) | < (p < 0.01) | - | < (p < 0.05) | = (p = 1.000) | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Teramae, F.; Makino, T.; Sengoku, S.; Lim, Y.; Natori, T.; Kodama, K. Research on Pharmaceutical Product Life Cycle Patterns for Sustainable Growth. Sustainability 2020, 12, 8938. https://doi.org/10.3390/su12218938

Teramae F, Makino T, Sengoku S, Lim Y, Natori T, Kodama K. Research on Pharmaceutical Product Life Cycle Patterns for Sustainable Growth. Sustainability. 2020; 12(21):8938. https://doi.org/10.3390/su12218938

Chicago/Turabian StyleTeramae, Fumio, Tomohiro Makino, Shintaro Sengoku, Yeongjoo Lim, Takashi Natori, and Kota Kodama. 2020. "Research on Pharmaceutical Product Life Cycle Patterns for Sustainable Growth" Sustainability 12, no. 21: 8938. https://doi.org/10.3390/su12218938

APA StyleTeramae, F., Makino, T., Sengoku, S., Lim, Y., Natori, T., & Kodama, K. (2020). Research on Pharmaceutical Product Life Cycle Patterns for Sustainable Growth. Sustainability, 12(21), 8938. https://doi.org/10.3390/su12218938