Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment

Abstract

1. Introduction

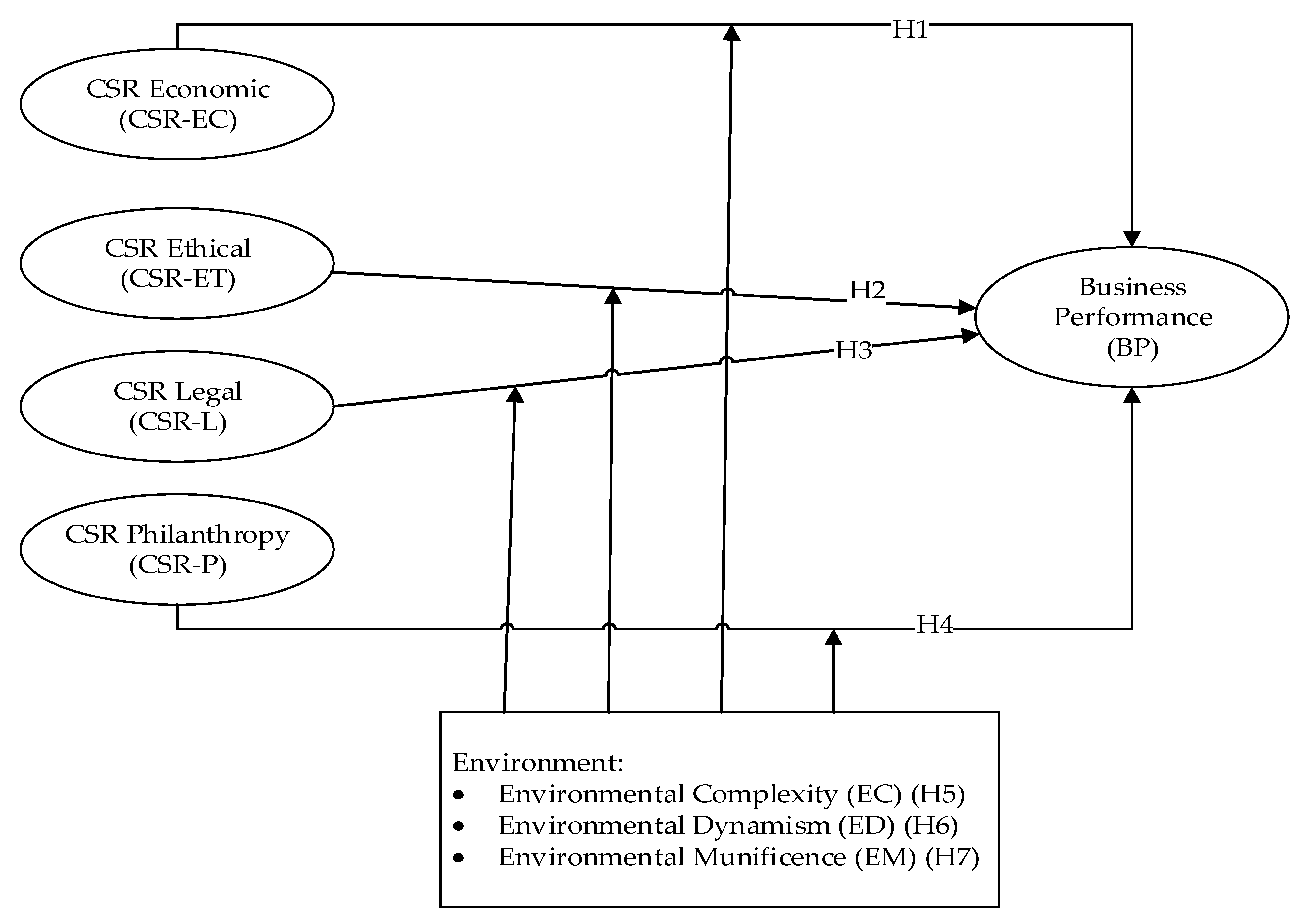

2. Literature Review and Hypotheses Development

2.1. Corporate Social Responsibility (CSR) and Firm Performance

2.2. Environment as Moderator

3. Methodology

3.1. Sampling Design and Procedures

3.2. Measurement Instrument

4. Data Analysis and Results

4.1. Data Analysis

4.2. Assessment of Common Method Bias

4.3. Measurement Model Evaluation

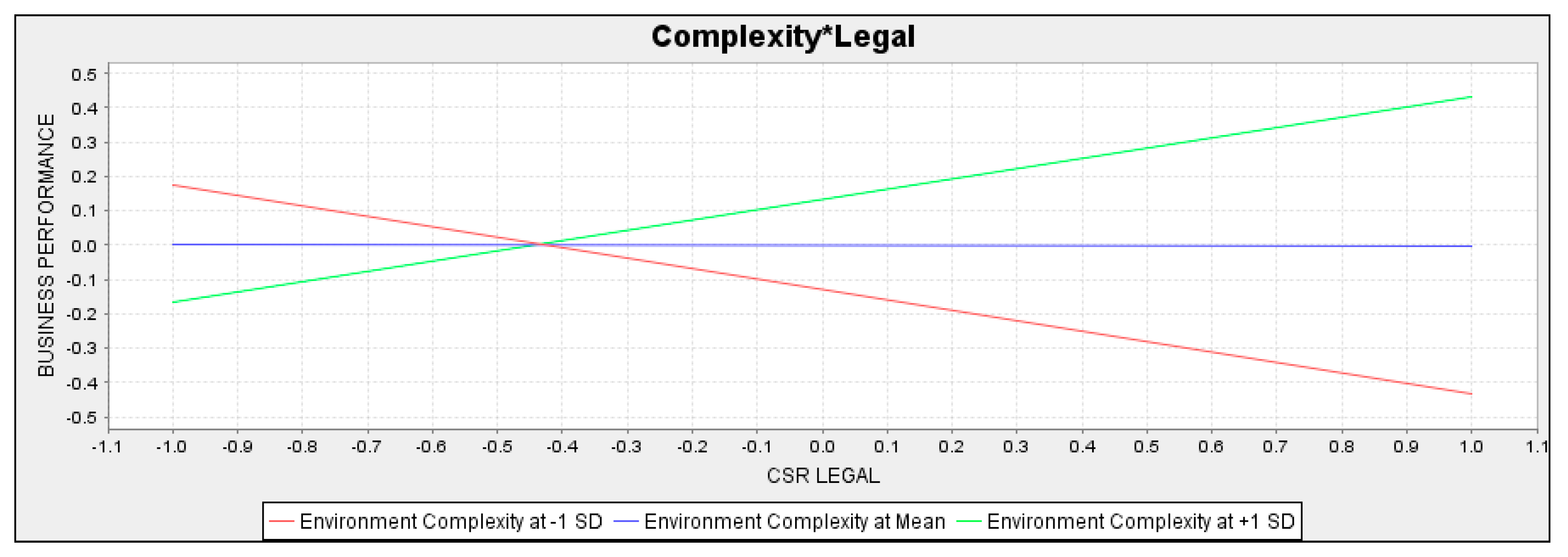

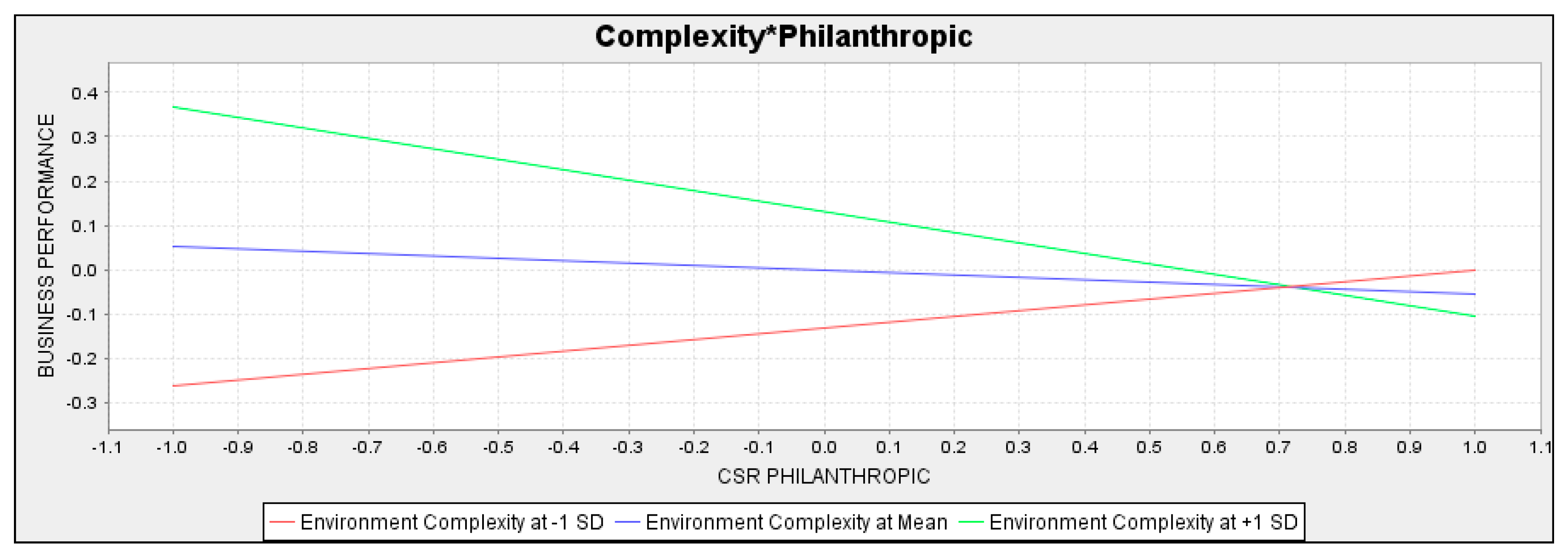

4.4. Structural Model Evaluation

5. Discussion and Conclusions

5.1. Theoretical Implication

5.2. Managerial Contribution

6. Limitations and Future Research Suggestions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Al Mahi, A.S.M.M.; Sim, C.S.; Hassan, A.F. Religiosity and Demand for Takaful (Islamic Insurance): A Preliminary Investigation. Int. J. Appl. Bus. Econ. Res. 2017, 15, 485–499. [Google Scholar]

- Bhatty, A. The Growing Importance of Takaful Insurance. In Proceedings of the Asia Regional Seminar, Kuala Lumpur, Malaysia, 23–24 September 2010. [Google Scholar]

- Haron, S.; Azmi, N.W. Islamic Finance Banking System; McGraw-Hill: The Synergy, Singapore, 2009. [Google Scholar]

- Abu-Hussin, M.F.; Muhamad, N.H.N.; Hussin, M.Y.M. Takaful (Islamic Insurance) Industry in Malaysia and the Arab Gulf States: Challenges and Future Direction. Asian Soc. Sci. 2014, 10, 26–34. [Google Scholar] [CrossRef]

- Halim, N. The Takaful & re-Takaful Industry: An Overview. Available online: https://www.islamicfinancenews.com/supplements/the-takaful-and-re-takaful-industry (accessed on 30 May 2012).

- The Star. 2020. Available online: https://www.thestar.com.my/business/business-news/2020/05/05/takaful-market-grows-despite-covid-19-malaysia-praised (accessed on 5 May 2020).

- Yaacob, Y.; Azmi, I.A.G. Entrepreneur’s social responsibilities from Islamic perspective: A Study of Muslim Entrepreneurs in Malaysia. Procedia Soc. Behav. Sci. 2012, 58, 1131–1138. [Google Scholar] [CrossRef]

- El-Tahir, H. The Way Forward for Takaful Spotlight on Growth, Investment and Regulation in Key Markets; Deloitte & Touche (ME): Kuala Lumpur, Malaysia, 2014. [Google Scholar]

- Sharif, K. Development, Growth and Challenges of Takaful in Malaysia. Available online: https://www.islamicfinancenews.com/development-growth-and-challenges-of-takaful-in-malaysia.html (accessed on 12 May 2012).

- Ho, C.C.; Huang, C.; Ou, C.Y. Analysis of the factors influencing sustainable development in the insurance industry. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 391–410. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Joyner, B.E.; Payne, D.; Raiborn, C.A. Building values, business ethics and corporate social responsibility into the developing organization. J. Dev. Entrep. 2002, 7, 113–131. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Organ. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Schneider, A.; Meins, E. Two dimensions of corporate sustainability assessment: Towards a comprehensive framework. Bus. Strateg. Environ. 2013, 21, 211–222. [Google Scholar] [CrossRef]

- Wagner, M.; Blom, J. The reciprocal and non-linear relationship of sustainability and financial performance. Bus. Ethics Eur. Rev. 2011, 20, 418–432. [Google Scholar] [CrossRef]

- Gunawan, J.; Permatasari, P.; Tilt, C. Sustainable development goal disclosures: Do they support responsible consumption and production? J. Clean. Prod. 2020, 246, 118989. [Google Scholar] [CrossRef]

- Scott, M.P. Insurers’ impacts remain uncovered. Environ. Financ. 2003, 17, 22. [Google Scholar]

- Ullah, M.S.; Muttakin, M.B.; Khan, A. Corporate governance and corporate social responsibility disclosures in insurance companies. Int. J. Acc. Inf. Manag. 2019, 27, 284–300. [Google Scholar] [CrossRef]

- Farooq, S.U.; Chaudhry, T.; Alam, F.-E.; Ahmad, G. An analytical study of the potential of Takaful companies. Eur. J. Econ. Financ. Adm. Sci. 2010, 20, 54–75. [Google Scholar]

- Wu, S.I.; Wang, W.H. Impact of CSR perception on brand image, brand attitude and buying willingness: A study of a global café. Int. J. Mark. Stud. 2014, 6, 43–56. [Google Scholar] [CrossRef]

- Yadav, R.K.; Jain, R.; Singh, S. An overview of Corporate Social Responsibility (CSR) in insurance sector with special reference to Reliance Life Insurance. World Sci. News 2016, 2, 196–223. [Google Scholar]

- Hwang, J.; Kim, J.J.; Lee, S. The importance of philanthropic corporate social responsibility and its impact on attitude and behavioral intentions: The moderating role of the barista disability status. Sustainability 2020, 12, 6235. [Google Scholar] [CrossRef]

- Collier, J.; Esteban, R. Corporate social responsibility and employee commitment. Bus. Ethics Eur. Rev. 2007, 16, 19–33. [Google Scholar] [CrossRef]

- Ahmad, M.F.; Samsi, S.Z.M.; Rasit, R.M.; Yunus, N.; Rahim, N.R.A. Corporate social responsibility for Takaful industry’s branding image. J. Pengur. (UKM J. Manag.) 2016, 46, 15–124. [Google Scholar] [CrossRef][Green Version]

- Manokaran, K.; Ramakrishnan, S.; Hishan, S.; Soehod, K. The impact of corporate social responsibility on financial performance: Evidence from Insurance firms. Manag. Sci. Lett. 2018, 8, 913–932. [Google Scholar] [CrossRef]

- Jain, T.; Jamali, D. Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corp. Gov. Int. Rev. 2016, 243, 253–273. [Google Scholar] [CrossRef]

- Miller, S.R.; Eden, L.; Li, D. CSR reputation and firm performance: A dynamic approach. J. Bus. Ethics 2020, 163, 619–636. [Google Scholar] [CrossRef]

- Kong, Y.; Antwi-Adjei, A.; Bawuah, J. A systematic review of the business case for corporate social responsibility and firm performance. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 444–454. [Google Scholar] [CrossRef]

- Bai, X.; Chang, J. Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment. Asia Pac. J. Manag. 2015, 2, 505–530. [Google Scholar] [CrossRef]

- Prescott, J.E. Environments as moderators of the relationship between strategy and performance. Acad. Manag. J. 1986, 29, 329–346. [Google Scholar]

- Nazri, M.A.; Omar, N.A. Corporate Social Responsibility and Takaful Agency’s Business Performance in Malaysia: A Critical Review. In Proceedings of the 2nd Global Conference on Economics and Management Sciences 2016, Langkawi, Malaysia, 28–29 November 2016. [Google Scholar]

- Bowen, H.R.; Johnson, F.E. Social Responsibilities of the Businessman; New York Harper: New York, NY, USA, 1953. [Google Scholar]

- Brown, T.J.; Dacin, P.A. The company and the product: Corporate associations and consumer product responses. J. Mark. 1997, 61, 68–84. [Google Scholar] [CrossRef]

- Freeman, I.; Hasnaoui, A. The meaning of corporate social responsibility: The vision of four nations. J. Bus. Ethics 2011, 100, 419–443. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business is to Increase its Profits. In Corporate Ethics and Corporate Governance; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Lantos, G.P. The ethicality of altruistic corporate social responsibility. J. Consum. Mark. 2002, 19, 205–232. [Google Scholar] [CrossRef]

- Deegan, C. The legitimising effect of social and environmental disclosures–a theoretical foundation. Acc. Audit. Acc. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Yen, G.F.; Yang, H.T. Does consumer empathy influence consumer responses to strategic corporate social responsibility? The dual mediation of moral identity. Sustainability 2018, 10, 1812. [Google Scholar] [CrossRef]

- Valmohammadi, C. Impact of corporate social responsibility practices on organizational performance: An ISO 26000 perspective. Soc. Responsib. J. 2014, 10, 455–479. [Google Scholar] [CrossRef]

- Wang, S.; Huang, W.; Gao, Y.; Ansett, S.; Xu, S. Can socially responsible leaders drive Chinese firm performance? Leadersh. Organ. Dev. J. 2015, 10, 2403. [Google Scholar] [CrossRef]

- Richard, P.J.; Devinney, T.M.; Yip, G.S.; Johnson, G. Measuring organizational performance: Towards methodological best practice. J. Manag. 2009, 35, 718–804. [Google Scholar] [CrossRef]

- Kuei, C.H.; Madu, C.N.; Lin, C. The relationship between supply chain quality management practices and organizational performance. Int. J. Qual. Reliab. Manag. 2001, 18, 864–872. [Google Scholar] [CrossRef]

- Venkatraman, N.; Ramanujam, V. Measurement of business performance in strategy research: A comparison of approaches. Acad. Manag. Rev. 1986, 11, 801–814. [Google Scholar] [CrossRef]

- Griffin, M.A.; Neal, A.; Parker, S.K. A new model of work role performance: Positive behavior in uncertain and interdependent contexts. Acad. Manag. J. 2007, 50, 327–347. [Google Scholar] [CrossRef]

- Kim, J.S.; Milliman, J.; Lucas, A. Effects of CSR on employee retention via identification and quality-of-work-life. Int. J. Contemp. Hosp. Manag. 2020, 32, 1163–1179. [Google Scholar] [CrossRef]

- Enquist, B.; Johnson, M.; Skålén, P. Adoption of corporate social responsibility–incorporating a stakeholder perspective. Qual. Res. Acc. Manag. 2006, 3, 188–207. [Google Scholar] [CrossRef]

- Jamali, D. A stakeholder approach to corporate social responsibility: A fresh perspective into theory and practice. J. Bus. Ethics 2008, 82, 213–231. [Google Scholar] [CrossRef]

- Novak, M. Business as a Calling: Work and the Examined Life; The Free Press: New York, NY, USA, 1996. [Google Scholar]

- Maon, F.; Lindgreen, A.; Swaen, V. Designing and implementing corporate social responsibility: An integrative framework grounded in theory and practice. J. Bus. Ethics 2009, 87, 71–89. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Korschun, D.; Sen, S. Strengthening stakeholder–company relationships through mutually beneficial corporate social responsibility initiatives. J. Bus. Ethics 2009, 2, 257–272. [Google Scholar] [CrossRef]

- Maignan, I.; Ferrell, O. Corporate social responsibility and marketing: An integrative framework. J. Acad. Mark. Sci. 2004, 32, 3–19. [Google Scholar] [CrossRef]

- Lee, Y.-K.; Lee, K.H.; Li, D.-X. The impact of CSR on relationship quality and relationship outcomes: A perspective of service employees. Int. J. Hosp. Manag. 2012, 31, 745–756. [Google Scholar] [CrossRef]

- Xu, X.; Zeng, S.; Chen, H. Signaling good by doing good: How does environmental corporate social responsibility affect international expansion? Bus. Strateg. Environ. 2018, 27, 946–959. [Google Scholar] [CrossRef]

- Van Beurden, P.; Gössling, T. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407–424. [Google Scholar] [CrossRef]

- Gossling, T.; Vocht, C. Social Role Conceptions and CSR Policy Success. J. Bus. Ethics 2007, 47, 363–372. [Google Scholar] [CrossRef]

- Lankoski, L. Corporate responsibility activities and economic performance: A theory of why and how they are connected. Bus. Strateg. Environ. 2008, 17, 536–547. [Google Scholar] [CrossRef]

- Freeman, R.E. The Politics of Stakeholder Theory: Some Future Directions. Bus. Ethics Q. 1994, 4, 409–421. [Google Scholar] [CrossRef]

- Mazzi, A.; Toniolo, S.; Manzardo, A.; Ren, J.; Scipioni, A. Exploring the Direction on the Environmental and Business Performance Relationship at the Firm Level. Lessons from a Literature Review. Sustainability 2016, 8, 1200. [Google Scholar] [CrossRef]

- Roman, R.M.; Hayibor, S.; Agle, R.B. The Relation between Social and Financial Performance: Repainting a Portrait. Bus. Soc. 1999, 38, 109–125. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives. Bus. Adm. Sci. Quart. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Rutledge, R.W.; Karim, K.E.; Aleksanyan, M.; Wu, C. An examination of the relationship between corporate social responsibility and financial performance: The case of Chinese state-owned enterprises. Accounting for the Environment: More Talk and Little Progress. Adv. Environ. Acc. Manag. 2014, 5, 1–22. [Google Scholar]

- Molina-Azorín, J.F.; Claver-Cortés, E.; López-Gamero, M.D.; Tarí, J.J. Green management and financial performance: A literature review. Manag. Decis. 2009, 47, 1080–1100. [Google Scholar] [CrossRef]

- Chand, M.; Fraser, S. The relationship between corporate social performance and corporate financial performance: Industry type as a boundary condition. Bus. Rev. 2006, 5, 240–245. [Google Scholar]

- Wang, C.-H.; Chen, K.-Y.; Chen, S.-C. Total quality management, market orientation and hotel performance: The moderating effects of external environmental factors. Int. J. Hosp. Manag. 2012, 31, 119–129. [Google Scholar] [CrossRef]

- May, R.C.; Stewart, W.H., Jr.; Sweo, R. Environmental scanning behavior in a transitional economy: Evidence from Russia. Acad. Manag. J. 2000, 43, 403–427. [Google Scholar]

- Bourgeois, L.J., III. Strategy and environment: A conceptual integration. Acad. Manag. Rev. 1980, 5, 25–39. [Google Scholar] [CrossRef]

- Castrogiovanni, J.G. Environmental munificence: A theoretical assessment. Acad. Manag. Rev. 1991, 16, 542–565. [Google Scholar] [CrossRef]

- Dess, G.G.; Beard, D.W. Dimensions of organizational task environments. Adm. Sci. Q. 1984, 29, 52–73. [Google Scholar] [CrossRef]

- Fuentes-Fuentes, M.M.; Albacete-Sáez, C.A.; Lloréns-Montes, F.J. The impact of environmental characteristics on TQM principles and organizational performance. Omega 2004, 32, 425–442. [Google Scholar] [CrossRef]

- Zahra, S.A. Predictors and financial outcomes of corporate entrepreneurship: An exploratory study. J. Bus. Ventur. 1991, 6, 259–285. [Google Scholar] [CrossRef]

- Slater, S.F.; Narver, J.C. Does competitive environment moderate the market orientation-performance relationship? J. Mark. 1994, 58, 46–55. [Google Scholar] [CrossRef]

- Duncan, R.B. Characteristics of organizational environments and perceived environmental uncertainty. Adm. Sci. Q. 1972, 17, 52–73. [Google Scholar] [CrossRef]

- Khandwalla, P. The Design of Organizations; Harcourt Brace Jovanovich: New York, NY, USA, 1977. [Google Scholar]

- Sharfman, M.; Dean, J.W. Conceptualizing and measuring the organizational environment: A multidimensional approach. J. Manag. 1991, 17, 681–700. [Google Scholar] [CrossRef]

- Goll, I.; Rasheed, A.A. The moderating effect of environmental munificence and dynamism on the relationship between discretionary social responsibility and firm performance. J. Bus. Ethics 2004, 49, 41–54. [Google Scholar] [CrossRef]

- Annuar, H.A. Al-Wakalah and customers’ preferences toward it: A case study of two takaful companies in Malaysia. Am. J. Islamic Soc. Sci. 2004, 1, 28–49. [Google Scholar] [CrossRef]

- Ramakrishnan, S.; Alsahliy, D.K.; Hishan, S.S.; Keong, L.B.; Vaicondam, Y. Corporate responsibility of the listed Malaysian insurance companies. Adv. Sci. Lett. 2017, 23, 9279–9281. [Google Scholar] [CrossRef]

- Muwazir, M.R.; Muhamad, R.; Noordin, K. Corporate social responsibility disclosure: A Tawhidic approach. J. Syariah 2006, 14, 125–142. [Google Scholar]

- Churchill, G.A. Marketing Research: Methodological Foundations, 5th ed.; The Dryden Press: London, UK, 1995. [Google Scholar]

- Gounaris, S.P.; Avlonitis, G.J. Market orientation development: A comparison of industrial vs consumer goods companies. J. Bus. Ind. Mark. 2001, 16, 354–381. [Google Scholar] [CrossRef]

- Osuagwu, L. Market orientation in Nigerian companies. Mark. Intell. Plan. 2006, 24, 608–631. [Google Scholar] [CrossRef]

- MacKenzie, S.B.; Podsakoff, P.M. Common method bias in marketing: Causes, mechanisms, and procedural remedies. J. Retail. 2012, 88, 542–555. [Google Scholar] [CrossRef]

- Hooi, L.W.; Ngui, K.S. Enhancing organizational performance of Malaysian SMEs. Int. J. Manpow. 2014, 35, 973–995. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Podsakoff, N.P. Sources of method bias in social science research and recommendations on how to control it. Annu. Rev. Psychol. 2012, 63, 539–569. [Google Scholar] [CrossRef] [PubMed]

- Gu, F.F.; Hung, K.; Tse, D.K. When does Guanxi matter? Issues of capitalization and its dark sides. J. Mark. 2008, 72, 12–28. [Google Scholar] [CrossRef]

- Carroll, A.B. Carroll’s pyramid of CSR: Taking another look. Int. J. Corp. Soc. Responsib. 2016, 1, 1–8. [Google Scholar] [CrossRef]

- Ramayah, T.; Samat, N.; Lo, M.C. Market orientation, service quality and organizational performance in service organizations in Malaysia. Asia Pac. J. Bus. Adm. 2011, 8, 8–27. [Google Scholar] [CrossRef]

- Wong, K.K. Partial least squares structural equation modeling (PLS-SEM) techniques using smartPLS. Mark. Bull. 2013, 24, 1–32. [Google Scholar]

- Vinzi, V.E.; Trinchera, L.; Amato, S. PLS Path Modeling: From Foundations to Recent Developments and Open Issues for Model Assessment and Improvement. In Handbook of Partial Least Squares. Springer Handbooks of Computational Statistics; Esposito Vinzi, V., Chin, W., Henseler, J., Wang, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2010. [Google Scholar] [CrossRef]

- Jorge, M.L.; Madueno, J.H.; Martínez-Martínez, D.; Sancho, M.P.L. Competitiveness and environmental performance in Spanish small and medium enterprises: Is there a direct link? J. Clean. Prod. 2015, 101, 26–37. [Google Scholar] [CrossRef]

- Sarstedt, M.; Cheah, J.H. Partial least squares structural equation modeling using SmartPLS: A software review. J. Mark. Anal. 2019, 7, 196–202. [Google Scholar] [CrossRef]

- Hair Jr, J.F.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Kline, R.B. Principles and Practice of Structural Equation Modeling; Guilford Publications: New York, NY, USA, 2015. [Google Scholar]

- Bhattacherjee, A. Social Science Research: Principles, Methods, And Practices, 2nd ed.; University of South Florida: Tampa, FL, USA, 2012. [Google Scholar]

- Raut, R.D.; Mangla, S.K.; Narwane, V.S.; Gardas, B.B.; Priyadarshinee, P.; Narkhede, B.E. Linking big data analytics and operational sustainability practices for sustainable business management. J. Clean. Prod. 2019, 224, 10–24. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural Equation Models with Unobservable Variables and Measurement Error. Algebra and Statistics; SAGE Publications: Los Angeles, CA, USA, 1981. [Google Scholar]

- Venkatesh, V.; Chan, F.K.; Thong, J.Y. Designing e-government services: Key service attributes and citizens’ preference structures. J. Oper. Manag. 2012, 30, 116–133. [Google Scholar] [CrossRef]

- Wan, S.; Liu, Z. Institutional background, company value and social responsibility cost: The evidence from listed companies of CSI300 index. Nankai Bus. Rev. 2013, 16, 110–121. [Google Scholar]

- Maignan, I.; Ferrell, O.; Ferrell, L. A stakeholder model for implementing social responsibility in marketing. Eur. J. Mark. 2005, 39, 956–977. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Latent Variable | Std. Loading | CR | AVE |

|---|---|---|---|

| Business Performance (BP) | 0.919 | 0.654 | |

| BP2 | 0.823 | ||

| BP3 | 0.845 | ||

| BP4 | 0.795 | ||

| BP5 | 0.757 | ||

| BP6 | 0.781 | ||

| BP7 | 0.848 | ||

| CSR Economic (CSR-EC) | 0.924 | 0.803 | |

| CSR-EC1 | 0.865 | ||

| CSR-EC2 | 0.916 | ||

| CSR-EC3 | 0.906 | ||

| CSR Ethic (CSR-ET) | 0.816 | 0.527 | |

| CSR-ET1 | 0.763 | ||

| CSR-ET2 | 0.686 | ||

| CSR-ET3 | 0.801 | ||

| CSR-ET4 | 0.644 | ||

| CSR Legal (CSR-L) | 0.916 | 0.730 | |

| CSR-L1 | 0.852 | ||

| CSR-L2 | 0.869 | ||

| CSR-L3 | 0.847 | ||

| CSR-L4 | 0.850 | ||

| CSR Philanthropic (CSR-P) | 0.796 | 0.566 | |

| CSR-P1 | 0.682 | ||

| CSR-P2 | 0.781 | ||

| CSR-P3 | 0.789 | ||

| Environment Complexity (EC) | 0.917 | 0.691 | |

| EC1 | 0.818 | ||

| EC2 | 0.889 | ||

| EC3 | 0.901 | ||

| EC4 | 0.852 | ||

| EC5 | 0.679 | ||

| Environment Dynamism (ED) | 0.835 | 0.560 | |

| ED1 | 0.719 | ||

| ED2 | 0.750 | ||

| ED3 | 0.688 | ||

| ED4 | 0.828 | ||

| Environment Munificence (EM) | 0.872 | 0.587 | |

| EM1 | 0.768 | ||

| EM2 | 0.909 | ||

| EM3 | 0.915 | ||

| EM4 | 0.645 | ||

| EM5 | 0.517 |

| Variables | BP | CSR-EC | CSR-ET | CSR-L | CSR-P | EC | ED | EM | |

|---|---|---|---|---|---|---|---|---|---|

| Business Performance (BP) | 0.809 | ||||||||

| CSR Economic (CSR-EC) | 0.538 | 0.896 | |||||||

| CSR Ethics (CSR-ET) | 0.534 | 0.606 | 0.726 | ||||||

| CSR Legal (CSR-L) | 0.467 | 0.767 | 0.580 | 0.855 | |||||

| CSR Philanthropic (CSR-P) | 0.498 | 0.575 | 0.657 | 0.461 | 0.752 | ||||

| Environment Complexity (EC) | 0.541 | 0.545 | 0.515 | 0.663 | 0.472 | 0.831 | |||

| Environment Dynamism (ED) | 0.566 | 0.487 | 0.492 | 0.494 | 0.539 | 0.666 | 0.748 | ||

| Environment Munificence (EM) | 0.423 | 0.409 | 0.531 | 0.483 | 0.411 | 0.673 | 0.476 | 0.766 | |

| Hypothesis | Relationship | Std Beta | Std Error | t-Values | p Values | Decision | R2 | f2 |

|---|---|---|---|---|---|---|---|---|

| H1 | CSR-EC -> BP | 0.251 ** | 0.100 | 2.502 | 0.006 | Supported | 0.456 | 0.040 |

| H2 | CSR-ET -> BP | 0.186 ** | 0.071 | 2.610 | 0.005 | Supported | 0.027 | |

| H3 | CSR-L -> BP | −0.107 | 0.094 | 1.141 | 0.127 | Not Supported | 0.007 | |

| H4 | CSR-P -> BP | 0.057 | 0.071 | 0.803 | 0.211 | Not Supported | 0.003 | |

| ED -> BP | 0.249 *** | 0.084 | 2.980 | 0.001 | - | |||

| EM -> BP | 0.011 | 0.069 | 0.154 | 0.439 | - | |||

| EC -> BP | 0.180 ** | 0.105 | 1.707 | 0.044 | - |

| Hypothesis | Moderating Effect (Environment) | |||

|---|---|---|---|---|

| Model 1 (Dynamism) | Model 2 (Complexity) | Model 3 (Munificence) | ||

| Specific Effects | ||||

| CSR-EC -> BP | 0.281 ** | 0.208 ** | 0.262 ** | |

| CSR-ET -> BP | 0.134 * | 0.246 ** | 0.214 ** | |

| CSR-L -> BP | −0.155* | −0.002 | −0.111 | |

| CSR-P -> BP | 0.152* | −0.053 | 0.023 | |

| Moderating Effects | ||||

| H5 | CSR-EC * EC | −0.019 | ||

| CSR-ET * EC | −0.029 | |||

| CSR-L * EC | 0.301 * | |||

| CSR-P * EC | −0.182 * | |||

| H6 | CSR-EC * ED | 0.135 | ||

| CSR-ET * ED | −0.136 | |||

| CSR-L * ED | −0.139 | |||

| CSR-P * ED | 0.125 | |||

| H7 | CSR-EC * EM | −0.046 | ||

| CSR-ET * EM | 0.051 | |||

| CSR-L * EM | 0.130 | |||

| CSR-P * EM | −0.035 | |||

| R2 | 0.482 | 0.464 | 0.490 | |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nazri, M.A.; Omar, N.A.; Aman, A.; Ayob, A.H.; Ramli, N.A. Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment. Sustainability 2020, 12, 8291. https://doi.org/10.3390/su12208291

Nazri MA, Omar NA, Aman A, Ayob AH, Ramli NA. Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment. Sustainability. 2020; 12(20):8291. https://doi.org/10.3390/su12208291

Chicago/Turabian StyleNazri, Muhamad Azrin, Nor Asiah Omar, Aini Aman, Abu Hanifah Ayob, and Nur Ainna Ramli. 2020. "Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment" Sustainability 12, no. 20: 8291. https://doi.org/10.3390/su12208291

APA StyleNazri, M. A., Omar, N. A., Aman, A., Ayob, A. H., & Ramli, N. A. (2020). Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment. Sustainability, 12(20), 8291. https://doi.org/10.3390/su12208291