Estimated Profitability of Thoroughbred Yearlings Sold in Auctions in the United States, 2001–2018

Abstract

1. Introduction

1.1. Background

1.2. Related Literature

2. Data and Empirical Methods

2.1. Data

2.2. Empirical Methods

3. Results

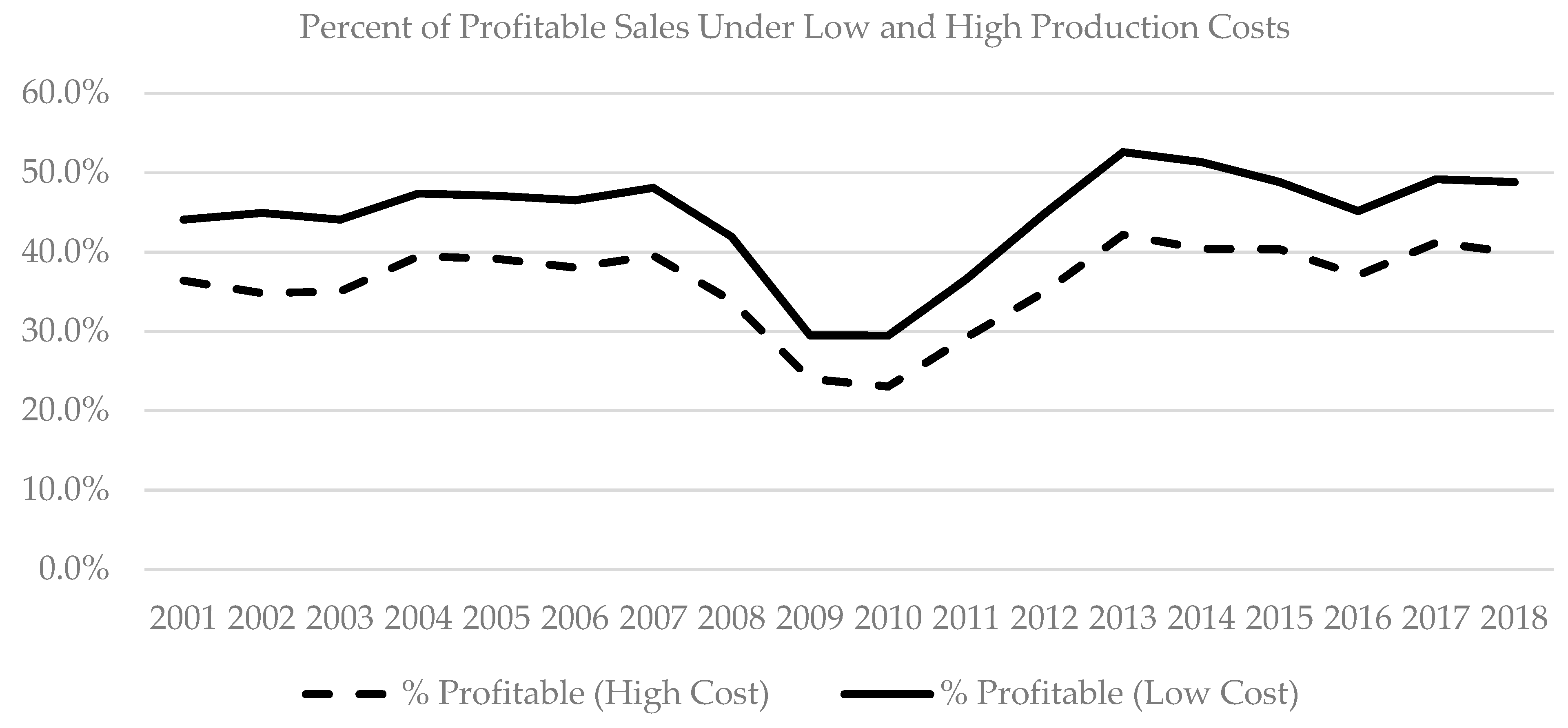

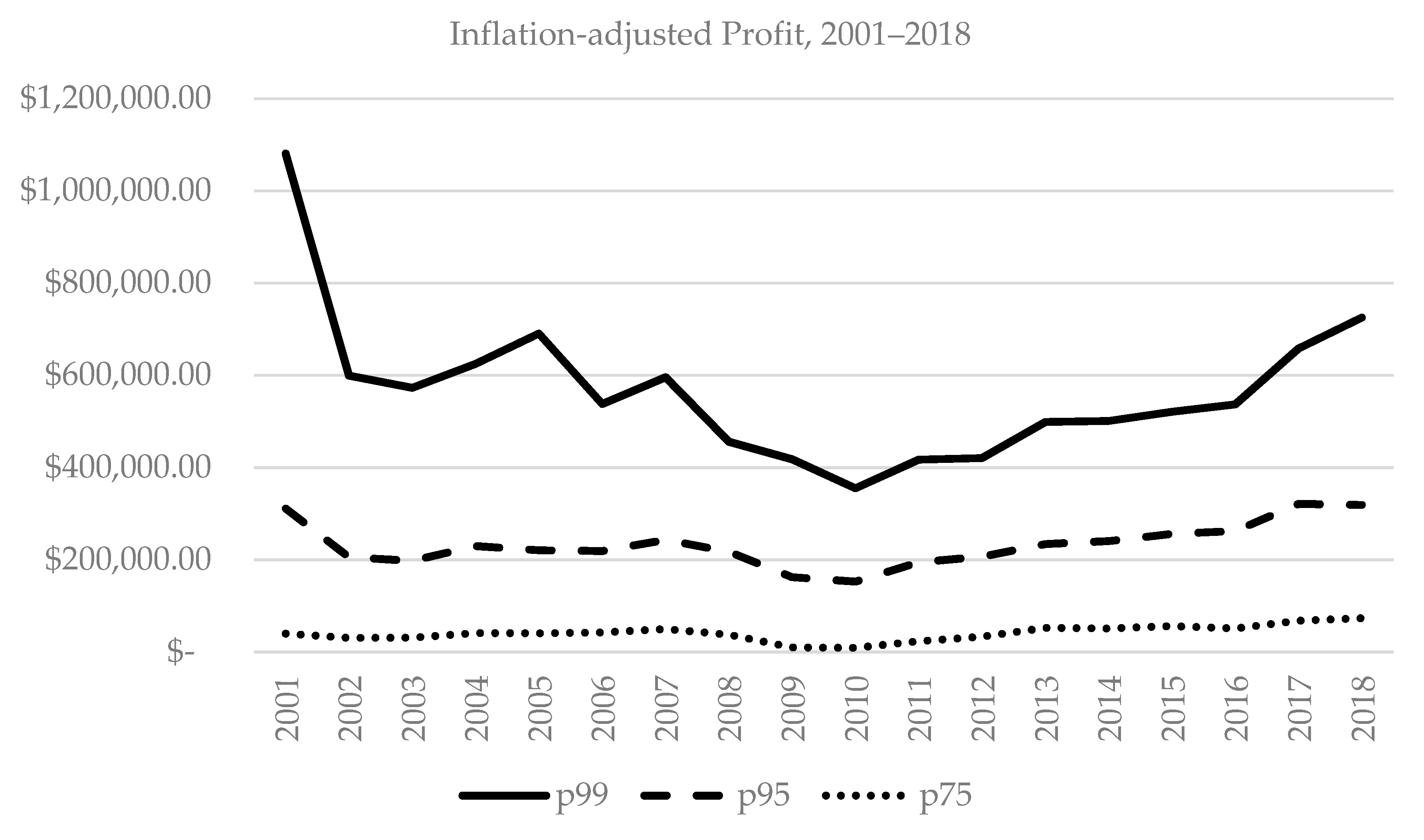

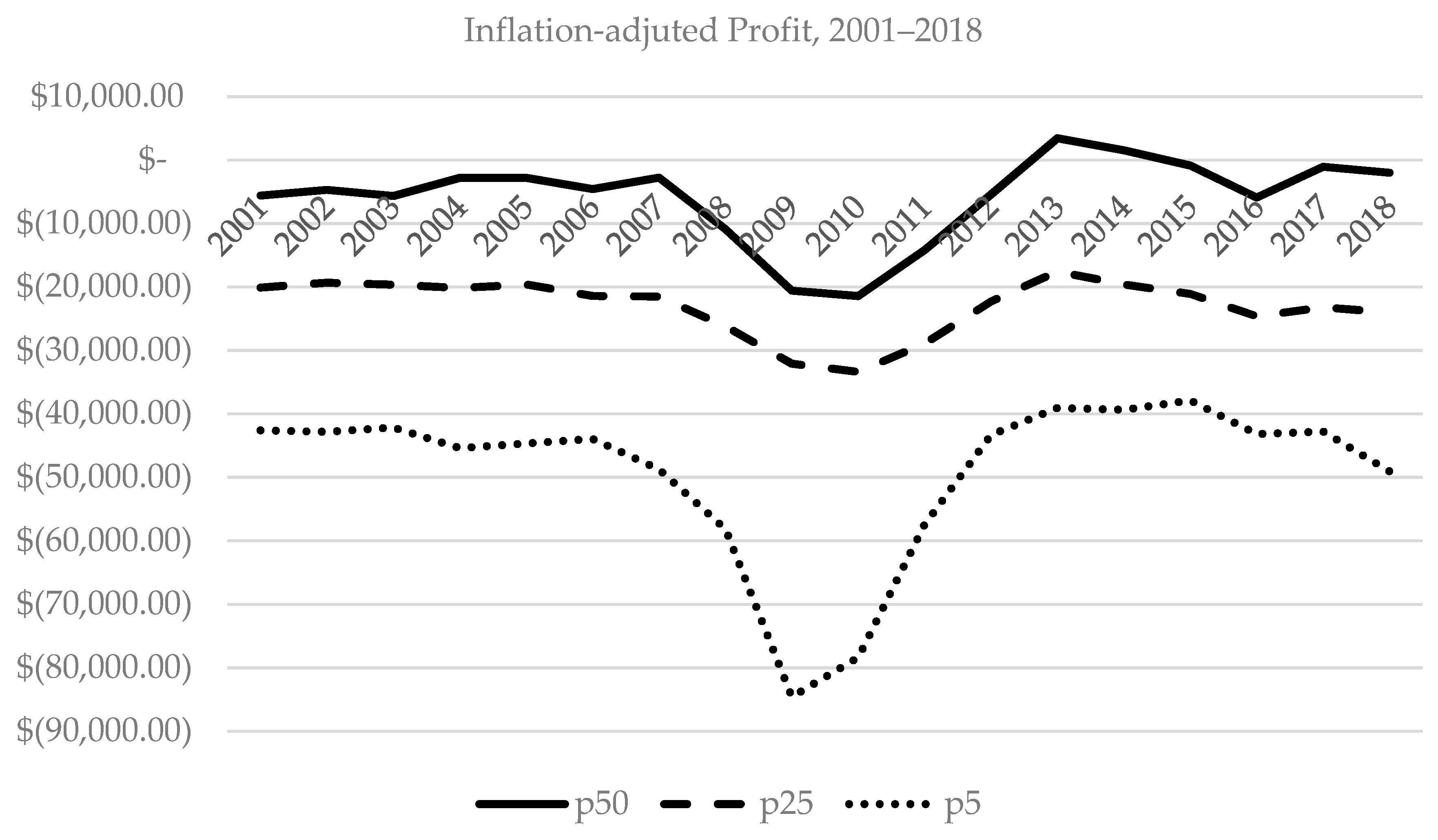

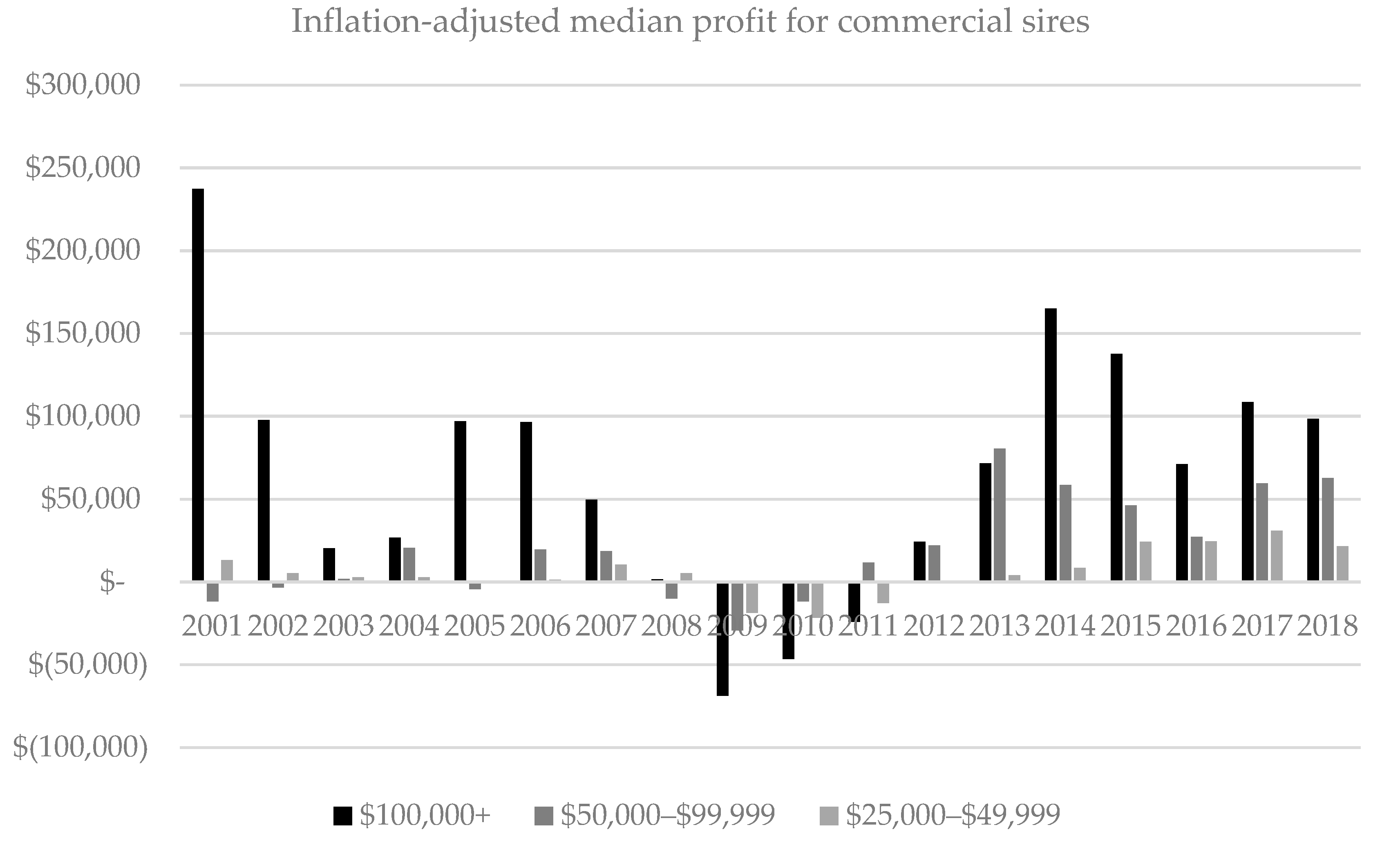

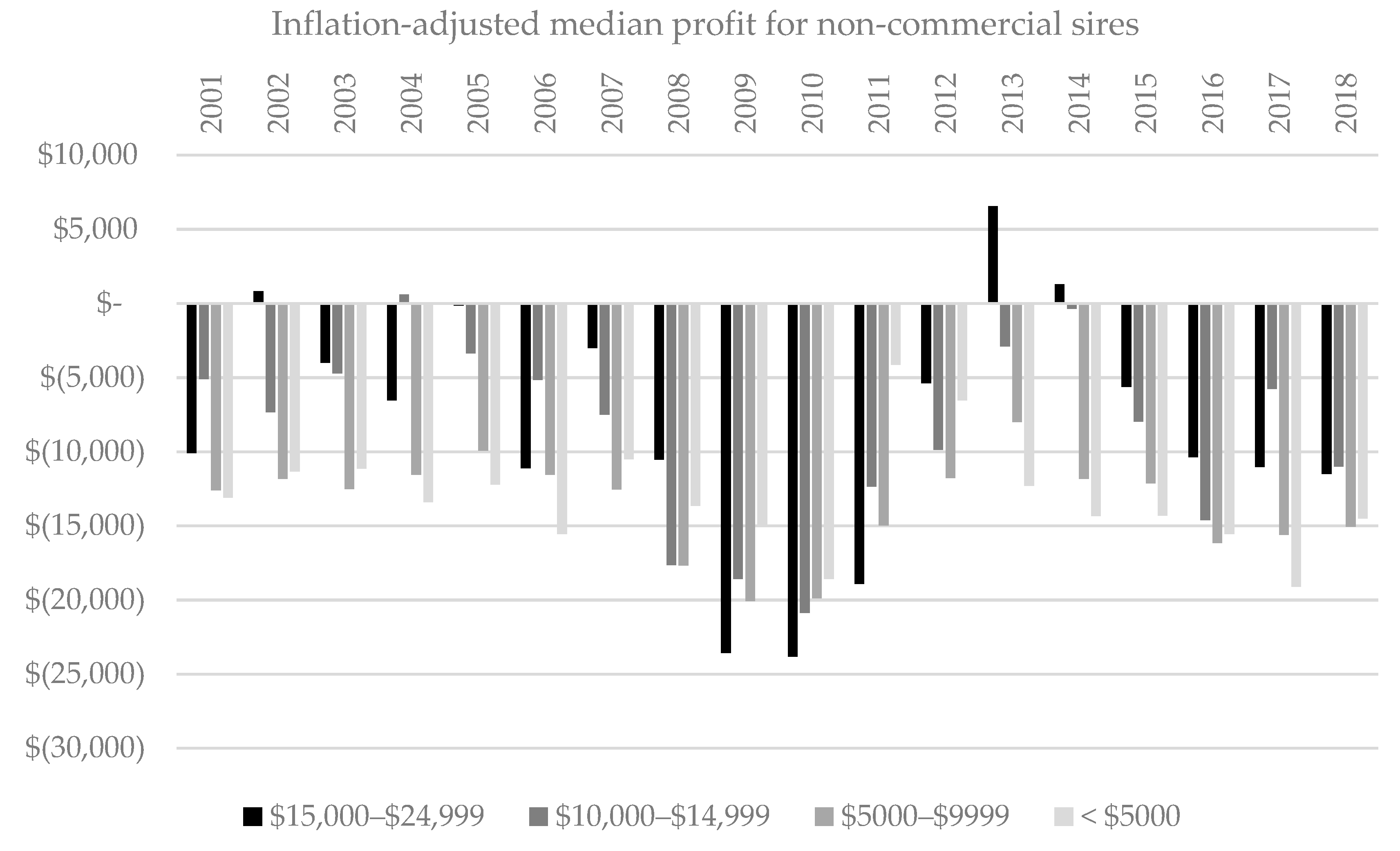

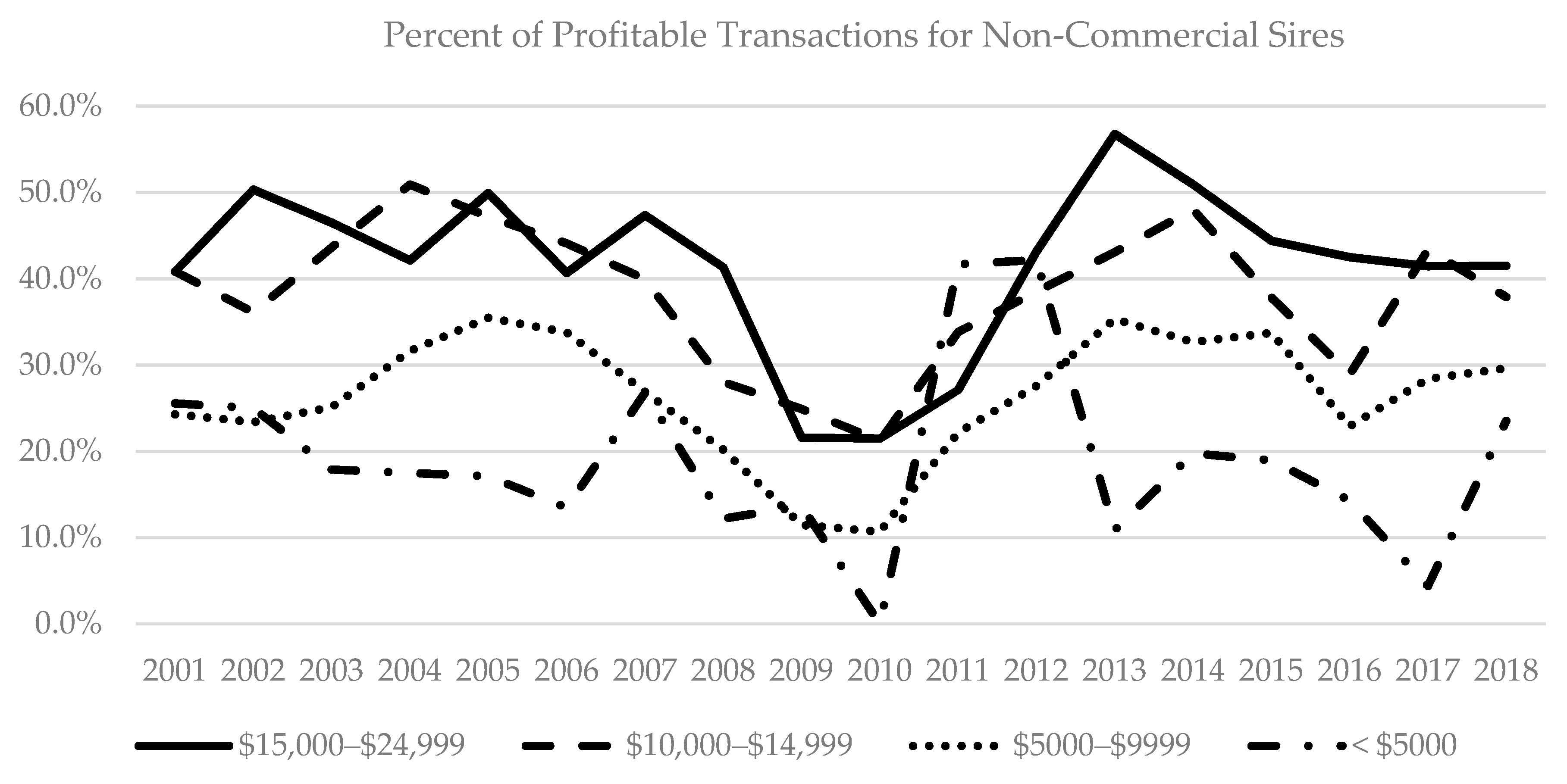

3.1. Trends in Sales Prices and Profitability, 2001–2018

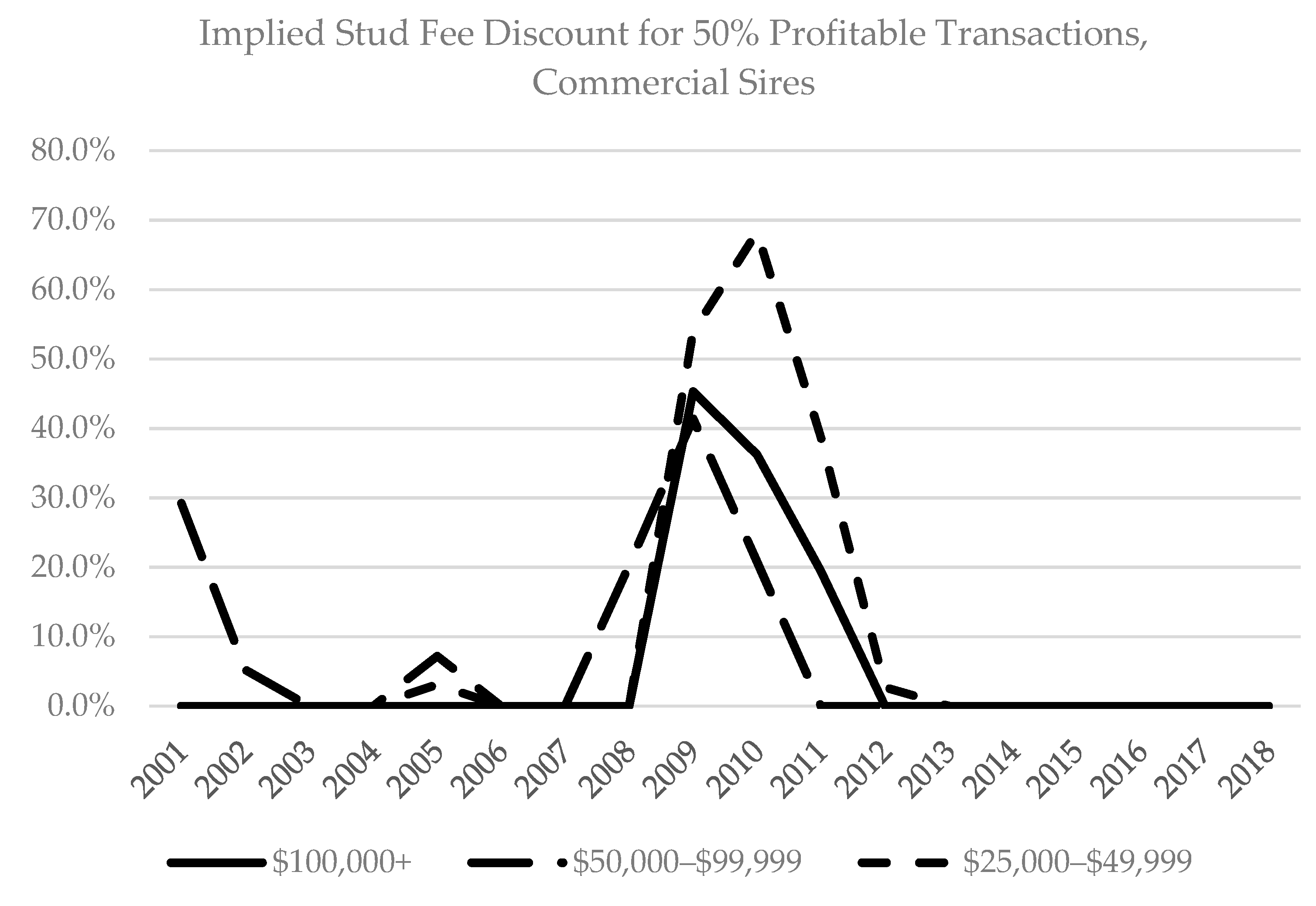

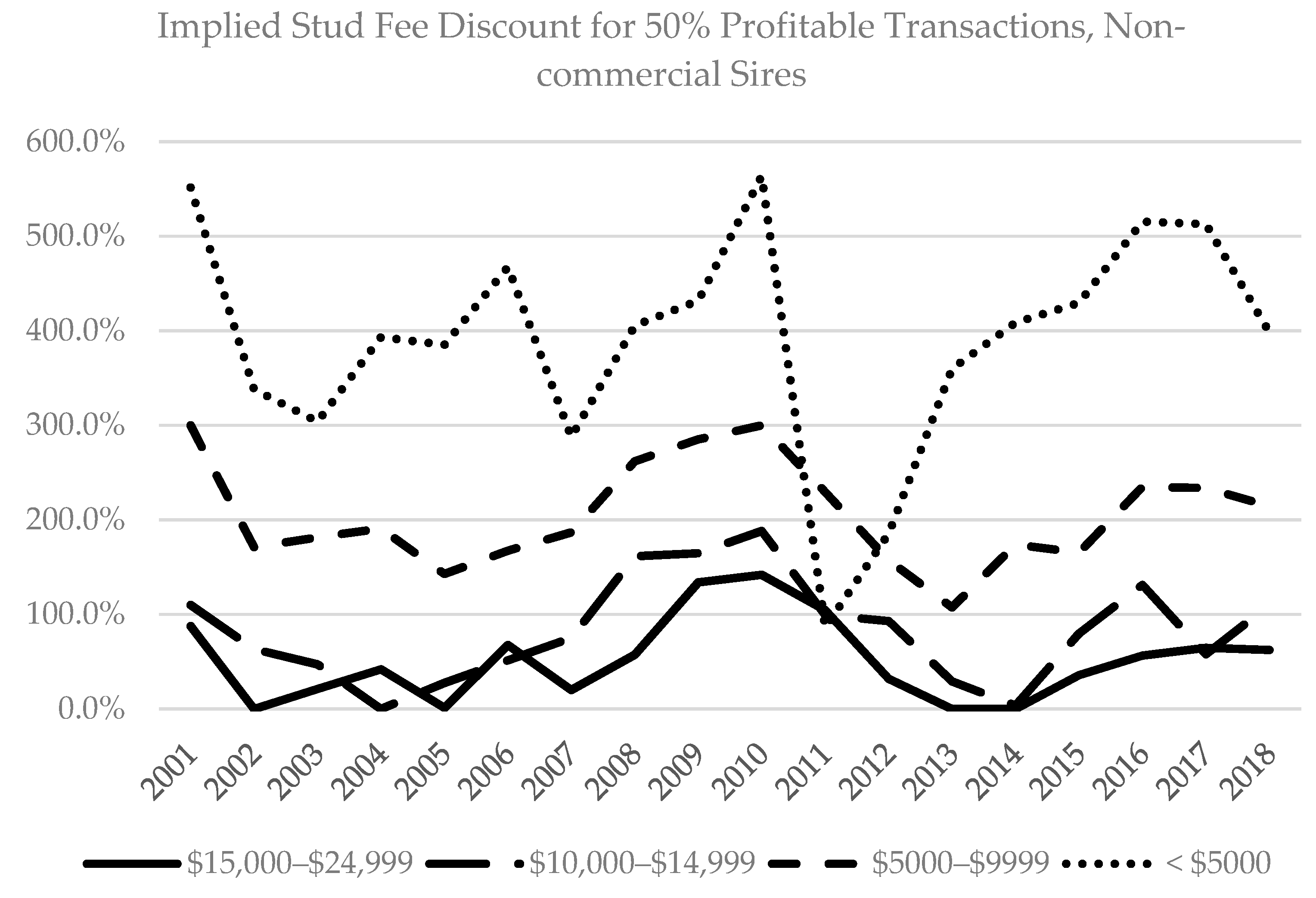

3.2. Implied Stud Fee Discount

4. Discussion

Author Contributions

Funding

Conflicts of Interest

References and Notes

- The Contribution of Thoroughbred Breeding to the UK Economy and Factors Impacting the Industry’s Supply Chain. Thoroughbred Breeders’ Assocation: Great Britain, UK, 2018. Available online: https://www.thetba.co.uk/wp-content/uploads/2018/09/TBA-Economic-Impact-Study-2018.pdf (accessed on 26 December 2019).

- 2019 Fact Book; The Jockey Club: Lexington, KY, USA, 2019. Available online: http://www.jockeyclub.com/Default.asp?section=Resources&area=11 (accessed on 26 December 2019).

- 2018 Auctions Digest; Blood-Horse, LLC: Lexington, KY, USA, 2018; p. 56.

- 2012 Auctions Digest; Blood-Horse LLC: Lexington, KY, USA, 2012; p. 1.

- 2010 Auctions Digest; Blood-Horse LLC: Lexington, KY, USA, 2010; p. 3877.

- Keeneland Sales Summaries. 2019. Available online: http://flex.keeneland.com/summaries/summaries.html (accessed on 26 December 2019).

- Fasig-Tipton Results Archive. 2019. Available online: http://www.fasigtipton.com/results/2019 (accessed on 26 December 2019).

- Nutt, P.; Clark, M.; Graycarek, R.; Hall, C.T.; Roenker, J. The Kentucky Thoroughbred Breeding Industry and State Programs that Assist the Equine Industry; Legislative Research Commission: Frankfort, KY, USA, 2011. [Google Scholar]

- Neibergs, J.S.; Vinzant, P.L. Maximum-Likelihood Estimates of Racehorse Earnings and Profitability. J. Agribus. 1999, 17, 37–48. [Google Scholar]

- Bosh, K.A.; Powell, D.; Neibergs, J.S.; Shelton, B.; Zent, W. Impact of reproductive efficiency over time and mare financial value on economic returns among Thoroughbred mares in central Kentucky. Equine Vet. J. 2009, 41, 889–894. [Google Scholar] [CrossRef] [PubMed]

- Gamrat, F.A.; Sauer, R.D. The utility of sport and returns to ownership: Evidence from the thoroughbred market. J. Sports Econ. 2000, 1, 219–235. [Google Scholar] [CrossRef]

- Consumer Price Index—All Urban Consumers, 2001–2018. 2019. Available online: http://data.bls.gov (accessed on 28 October 2019).

- Karungu, P.; Reed, M.; Tvedt, D. Macroeconomic Factors and the Thoroughbred Industry. J. Agric. Appl. Econ. 1993, 25, 165–173. [Google Scholar] [CrossRef][Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sale Year | Keeneland | Fasig-Tipton | Total |

|---|---|---|---|

| 2001 | 2666 | -- | 2666 |

| 2002 | 2788 | -- | 2788 |

| 2003 | 2899 | 922 | 3821 |

| 2004 | 3302 | 743 | 4045 |

| 2005 | 3443 | 1263 | 4706 |

| 2006 | 3494 | 1193 | 4687 |

| 2007 | 3776 | 1309 | 5085 |

| 2008 | 3591 | 1418 | 5009 |

| 2009 | 3102 | 1293 | 4395 |

| 2010 | 3040 | 1358 | 4398 |

| 2011 | 2901 | 1185 | 4086 |

| 2012 | 2499 | 1390 | 3889 |

| 2013 | 2729 | 1208 | 3937 |

| 2014 | 2798 | 1309 | 4107 |

| 2015 | 2724 | 1542 | 4266 |

| 2016 | 2775 | 1435 | 4210 |

| 2017 | 2538 | 1604 | 4142 |

| 2018 | 2900 | 1652 | 4552 |

| Total | 53,965 | 20,824 | 74,789 |

| High Production Costs | Low Production Costs | |||||

|---|---|---|---|---|---|---|

| Sale Year | Nominal Profit | Inflation-Adjusted Profit (2018 Dollars) | % Profitable | Nominal Profit | Inflation-Adjusted Profit (2018 Dollars) | % Profitable |

| 2001 | $45,621.80 | $64,684.55 | 36.4% | $56,201.25 | $79,684.55 | 44.1% |

| 2002 | $21,189.90 | $29,576.34 | 34.8% | $31,936.61 | $44,576.34 | 44.9% |

| 2003 | $17,786.06 | $24,272.17 | 35.0% | $28,777.69 | $39,272.16 | 44.1% |

| 2004 | $25,650.47 | $34,096.52 | 39.5% | $36,934.82 | $49,096.52 | 47.4% |

| 2005 | $29,300.73 | $37,672.37 | 39.1% | $40,967.40 | $52,672.37 | 47.1% |

| 2006 | $28,301.17 | $35,250.12 | 38.0% | $40,344.19 | $50,250.13 | 46.5% |

| 2007 | $26,324.90 | $31,887.04 | 39.6% | $38,708.41 | $46,887.03 | 48.1% |

| 2008 | $9623.41 | $11,223.59 | 33.9% | $22,484.82 | $26,223.59 | 41.9% |

| 2009 | $(8965.57) | $(10,495.35) | 24.0% | $3848.06 | $4504.65 | 29.5% |

| 2010 | $(11,904.63) | $(13,705.88) | 23.1% | $1124.04 | $1294.11 | 29.5% |

| 2011 | $3323.97 | $3711.20 | 29.3% | $16,758.85 | $18,711.19 | 36.6% |

| 2012 | $12,627.91 | $13,810.40 | 35.0% | $26,343.56 | $28,810.40 | 44.9% |

| 2013 | $27,598.60 | $29,742.53 | 42.2% | $41,517.35 | $44,742.52 | 52.6% |

| 2014 | $25,144.80 | $26,674.52 | 40.4% | $39,284.58 | $41,674.52 | 51.3% |

| 2015 | $26,897.26 | $28,497.48 | 40.4% | $41,054.96 | $43,497.47 | 48.8% |

| 2016 | $23,330.58 | $24,409.62 | 37.1% | $37,667.50 | $39,409.62 | 45.2% |

| 2017 | $35,596.53 | $36,467.93 | 41.2% | $50,238.11 | $51,467.93 | 49.2% |

| 2018 | $36,732.77 | $36,732.77 | 39.9% | $51,732.77 | $51,732.77 | 48.8% |

| Total | $20,263.61 | 36.1% | $33,219.45 | 44.4% | ||

| Stud Fee Category | % Profitable | n | % of Total |

|---|---|---|---|

| $100,000+ | 57.6% | 5125 | 6.9% |

| $50,000–$99,999 | 57.0% | 8021 | 10.7% |

| $25,000–$49,999 | 51.7% | 20,906 | 28.0% |

| $15,000–$24,999 | 41.7% | 16,623 | 22.2% |

| $10,000–$14,999 | 38.2% | 12,658 | 16.9% |

| $5000–$9999 | 28.1% | 10,314 | 13.8% |

| Less than $5000 | 19.7% | 1142 | 1.5% |

| Total | 44.4% | 74,789 | 100% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bryant, J.; Stowe, C.J. Estimated Profitability of Thoroughbred Yearlings Sold in Auctions in the United States, 2001–2018. Sustainability 2020, 12, 463. https://doi.org/10.3390/su12020463

Bryant J, Stowe CJ. Estimated Profitability of Thoroughbred Yearlings Sold in Auctions in the United States, 2001–2018. Sustainability. 2020; 12(2):463. https://doi.org/10.3390/su12020463

Chicago/Turabian StyleBryant, Jenna, and C. Jill Stowe. 2020. "Estimated Profitability of Thoroughbred Yearlings Sold in Auctions in the United States, 2001–2018" Sustainability 12, no. 2: 463. https://doi.org/10.3390/su12020463

APA StyleBryant, J., & Stowe, C. J. (2020). Estimated Profitability of Thoroughbred Yearlings Sold in Auctions in the United States, 2001–2018. Sustainability, 12(2), 463. https://doi.org/10.3390/su12020463