1. Introduction

This paper draws a causal relation between CEO compensation structure and firm corporate social responsibility (CSR). To draw our conclusions, we examine the sensitivity of CEO pay to both stock return volatility (vega) and stock returns (delta) using panel data spanning 1995–2013. CEO compensation has a profound influence on firm outcomes such as financial performance and investment and policy decisions; however, its effects on firm social performance are underexplored. The scarce literature examining the link between executive compensation and CSR has focused solely on the instruments of compensation as opposed to the underlying pay sensitivities that those instruments produce. Some use a lagged measure of long-term executive pay [

1] or the percentage of salary from bonus and stock options [

2]. McGuire et al. [

3] use salary, bonus, and long-term incentives, while Deckop et al. [

4] use percentage of short-term pay vs. long-term-pay to link CEO compensation with CSR levels. Although these studies address how CEO pay motivates CSR participation, they fail to address the reasons behind these investments. By using pay sensitivities, we can understand the underlying motivations behind CSR investment from the CEO’s perspective, not just whether the investment is made. Higher vega incentivizes CEOs to pursue policies that will increase stock price volatility, whereas higher delta motivates the CEO to increase the stock price. Understanding how CEOs respond to incentives related to CSR is crucial to designing compensation policies that not only maximize shareholder value but also promote corporate citizenship in operating environments that are increasingly impacted by societal perceptions.

Employing fixed effects models and controlling for firm size, risk level, and industry, we find that CSR standing is significantly positively related to measures of vega but not significantly related to measures of delta. This suggests that CEOs view CSR investing as a risky policy, similar to what the previous literature concludes about R&D spending [

5], financial leverage, and concentrated product lines [

6,

7,

8]. That is, CEOs generally perceive CSR projects as riskier than the average projects they are running. It is plausible that CSR investments are usually for new innovative projects and, more importantly, impose enormous uncertainty to stock performance and shareholder value. Delta has no significant effect on CSR levels, which suggests that a CEO’s decisions on CSR are independent of their pay sensitivity to the underlying stock price. Our findings indicate that stock option compensation significantly increases the likelihood of CSR initiatives, but only to the extent that the CEO’s pay sensitivity to the underlying volatility of the stock price is increased. This paper links the existing CEO compensation literature with the CSR literature in a way that has not previously been explored.

In an ideal world, CEO and shareholder interests would perfectly align. Every decision a CEO makes would maximize shareholder value. However, managers solve their own maximization problem with the goal of increasing their own utility; this is known as the agency problem [

9,

10]. Corporate governance policies aim to ensure that managers act in a manner consistent with shareholder value maximization, and part of this goal is achieved through compensation policy [

9,

10]. An optimal compensation contract is one that promotes the managerial decision making that maximizes shareholder value. This involves exposing the CEO to varying risk/reward incentive combinations via cash, stock, and options payments in an effort to mitigate the agency problem [

11]. Jenson and Murphy [

12] argue that CEO pay should be substantially linked to shareholder welfare. This idea gained significant traction throughout the 1990s, and Hall and Liebman [

13,

14] document a dramatic increase in equity-based CEO compensation throughout this period. CEO compensation includes three components: cash, stock, and options. According to optimal contracting theory, when company boards determine CEO compensation, they target a compensation mix that they believe will maximize shareholder value by reducing agency costs [

15]. This raises the question: how do CEOs respond to varying risk/reward combinations across compensation packages?

Naturally, CEO pay relating to the present cash component of compensation is independent of future stock price movements. However, equity-based compensation exhibits varying return characteristics depending on the instruments used. Stock-based compensation will move linearly with the stock price, resulting in a delta of 1; however, the sensitivity of options compensation depends entirely on the structure of the contracts. Given that CEOs are risk-averse and almost always highly exposed to firm specific risk, it is not enough to simply structure compensation policy to mimic the pay sensitivity of the shareholder. Even if managers are incentivized to take actions that increase shareholder wealth, they may still choose suboptimal policies that reduce personal portfolio risk [

16]. Therefore, we need to understand the risks that the CEO faces, and how these risks influence decision making.

There is extensive literature examining the effect of delta and vega on CEO decision making [

6,

7,

11]; however, the effect of delta and vega on CSR levels has not previously been explored. This shareholder value-maximization problem is further complicated by the issue of whether CSR is indeed a value-enhancing investment opportunity for a given firm. There is much debate surrounding this question in the existing literature [

17,

18,

19,

20]. Although it is beyond the scope of this paper to answer this question definitively, we contribute to the existing literature by identifying vega as an avenue that shareholders can use to encourage CEOs to alter CSR standings.

The remainder of this paper is organized as follows. In the following section, we review relevant literature and develop hypotheses.

Section 3 introduces our data sample, and

Section 4 presents empirical findings and discussion.

Section 5 concludes.

2. Literature Review and Hypothesis Development

This section serves as a review of existing literature relating to the topics of both CEO compensation and corporate social responsibility. We will begin by surveying the existing literature regarding CEO compensation, followed by the CSR literature, and conclude with a brief discussion of how we plan to link these literatures in a unique way to gain insight into how CEOs alter CSR levels in response to compensation incentives.

As a means to mitigate costs arising from agency concerns, Jensen and Murphy [

12] argue that CEO compensation should be substantially linked to shareholder value. They argue that since managerial actions and investment opportunities are not perfectly observable to shareholders, equity-based compensation encourages managerial actions that increase shareholder wealth. In accordance with this assertion, throughout the 1990s, there was a dramatic increase in both stock option compensation [

21,

22] and the sensitivity of CEO pay to the firm’s stock price [

14,

23]. Perry and Zenner [

22] raise the question of whether the increase in executive pay performance sensitivity is excessive, in that during bull markets (such as that of the 1990s), CEOs may be extracting excess rents from shareholders. This idea is built upon that by Bebchuk et al. [

15], where the issue of CEO power is explored as a rationale for puzzling compensation practices, such as the lack of controls to filter out general market/sector factors influencing the share price when designing equity-based compensation packages. Bebchuk et al. [

15] explore the idea that company boards are constrained when setting CEO compensation by CEO power. The argument is that powerful CEOs wield a degree of influence over the board and can use this influence to alter their own compensation structure, thereby extracting rents from shareholders. The CEO power approach to analyzing CEO compensation contracts contrasts the previous optimal contracting literature and has opened new avenues of study.

Much of the literature agrees that linking CEO compensation to shareholder wealth can reduce agency costs in many circumstances if implemented effectively. However, given the concerns surrounding imperfect information, ex-post contract enforcement feasibility, and the heterogeneity of both shareholders and CEOs, determining the appropriate compensation mix to maximize shareholder value is a contentious issue. A large problem with the idea of simply linking CEO compensation to shareholder wealth is that risk-averse CEOs are overly exposed to firm-specific risk because of equity-based compensation. This is a contrast to diversified shareholders who are owners of many firms and whose net worth is less sensitive to changes in the price of a given firm. Smith and Stulz [

16] build on Ross [

24] to demonstrate how risk-averse CEOs can be influenced to forgo positive NPV (net present value) projects when their total pay is linked to firm value. One solution to this problem is to mitigate the concavity of the utility of expected pay by using convex incentive schemes involving stock options. Guay [

11] finds that providing managers with convex incentive schemes encourages managers to invest in risk-increasing, positive NPV projects. However, the question of how much convexity to provide to a given manager remains elusive. Indeed, Ross [

25] proves that there exists no incentive schedule that renders all expected utility maximizers less risk averse.

There is a host of literature that details the responses of CEOs to the incentives created by options within a compensation structure. Defusco et al. [

26] find that firms that approved executive stock options plans between 1978 and 1988 exhibited increased stock return variance. Ju et al. [

27] show that usage of call options can induce either too much or too little risk-taking behavior. Jolls [

28] shows that CEOs that are compensated with options are more likely to engage in stock repurchases rather than dividend issuance. Knopf et al. [

8] show that the use of derivatives for hedging purposes within firms is negatively related to vega and positively related to delta. Ryan and Wiggins [

5] find that stock option grants coincide with increases in R&D spending. The most intriguing findings are provided by Cohen et al. [

6]. The authors augment the Hall–Liebman [

13] database on executive options holdings and value the holdings using the Black–Scholes [

29] method. They then compute the elasticity of CEO pay to changes in firm price volatility and find that executives respond to the incentives provided by options compensation. The authors further speculate, however, that as vega increases, CEOs may undertake negative NPV projects if they increase firm volatility. This is a key finding related to our paper because it raises the question of what CEOs may do in the face of uncertainty surrounding the profitability of investment projects.

Despite the extensive agreement in the literature that CEOs respond to the incentives created by compensation structure, there is often debate concerning the significance, magnitude and direction of various effects. There is a body of literature that takes advantage of the closed form solution of the Black–Scholes option-pricing model to take derivatives of option prices with respect to the underlying price (delta) and volatility (vega) [

7,

30,

31,

32]. However, how delta and vega fit into a given model has been interpreted in a wide variety of ways. Some studies try to use firm characteristics to estimate delta as a dependent variable [

30,

31], while others use delta as an independent variable [

32]. Many studies omit vega altogether, partly because vega is difficult to compute and it is easier to find proxies for delta, such as number of options held, options granted, or the value of options at a point in time. To a large extent, this problem was remedied by Core and Guay [

30] who developed a method to increase the accuracy of delta and vega estimates. Following this innovation, Coles et al. [

7] reasoned that both vega and delta should be treated as independent variables that are chosen exogenously by shareholders to promote desired decision making in CEOs. They used the method of Core and Guay [

30] to determine that higher vega results in the implementation of riskier firm policies, including higher R&D spending, less CAPEX, more concentrated product lines, and higher leverage. They also find that delta is generally inversely related to vega for these measures. From an optimal contracting perspective, the key point is that delta aligns the direction of managerial pay changes with that of the shareholders, while vega can be used to mitigate risk aversion.

All the above studies lead to a natural question: how is CSR as an investment perceived by CEOs? In order to answer this question, we need to obtain both an understanding of what CSR is and how to quantify it. Tsoutsoura [

33] defines CSR as “a comprehensive set of policies, practices, and programs that are integrated into business operations, supply chains, and decision-making processes throughout the company and usually includes issues related to business ethics, community investment, environmental concerns, governance, human rights, the marketplace as well as the workplace”. However, the question of how to quantify CSR has been approached from multiple angles. Some studies use subjective measures such as surveys [

34,

35,

36], while others use Fortune rankings [

17,

37,

38]. Waddock and Graves [

39] recognized the need for a more objective way to quantify CSR. They made use of the Kinder Lydenberg Domini (KLD) corporate social performance (CSP) rating system, which draws upon a combination of financial statements, press articles, academic journals, and government reports to assess CSP along eight dimensions. The advantage of this approach is that KLD is an independent ratings service (since acquired by MSCI) that applies objective criteria consistently across time. Using this improved method, Waddock and Graves [

39] find that CSP is initially driven by slackness in the budget constraints of firms that have high financial performance, but that CSP itself also creates positive financial performance. These findings concur with the positive relationship between firm performance and CSP found in the past [

17,

40,

41]. However, it contrasted with both the negative relation hypothesized by Friedman [

42] and the findings of a neutral relation by Ullmann [

43]. Therefore, we have the alternative hypotheses based on the literature:

Hypothesis 1a (H1a). CEOs with higher pay-performance sensitivity improve CSR if they view CSR as value enhancing.

Hypothesis 1b (H1b). CEOs with higher pay-performance sensitivity decrease CSR if they view CSR as value damaging.

Hypothesis 2a (H2a). CEOs with higher pay-risk sensitivity improve CSR if they view CSR as risk enhancing.

Hypothesis 2b (H2b). CEOs with higher pay-risk sensitivity decrease CSR if they view CSR as risk reducing.

CSR affects firms through other avenues besides accounting profitability. Gregory et al. [

44] look at the risk-reducing effects of CSR, and Albuquerque et al. [

45] examine how CSR diversifies risk within firms. The relationship between CSR and better access to financing, along with lower financing costs, is also explored [

46,

47,

48]. Attig et al. [

49] find that CSR leads to higher credit ratings. Servaes and Tamayo [

50] consider how CSR raises firm value through increased customer awareness. The effects of CSR on corporate governance, firm value, and as a method of resolving conflicts between stakeholders is explored by Jo and Harjoto [

51]. Jo and Harjoto [

52] look at the causal effect of CSR on corporate governance. Hong et al. [

53] and Ikram et al. [

54] use hand collected compensation data to show that giving executives direct incentives related to CSR is effective at increasing CSP.

There is a wide body of literature indicating that CSR affects firms through a variety of channels. Part of this literature seeks to determine how executive compensation affects CSR [

53,

54]; however, this is performed by examining explicit incentives provided to executives. Our paper uses a new method to explore the relationship between CSR and compensation. Previous studies have focused on whether CEO compensation influences CSR ratings. Using pay sensitivities, we address the actual mechanism through which CEOs make their decision. We use the method of Coles et al. [

7] to determine CEO delta and vega and then formulate a fixed effects model to estimate their effect on firm CSR ratings. As opposed to examining how CEOs respond to direct incentives, this approach examines how CEOs perceive CSR investment opportunities independent of other incentive frameworks.

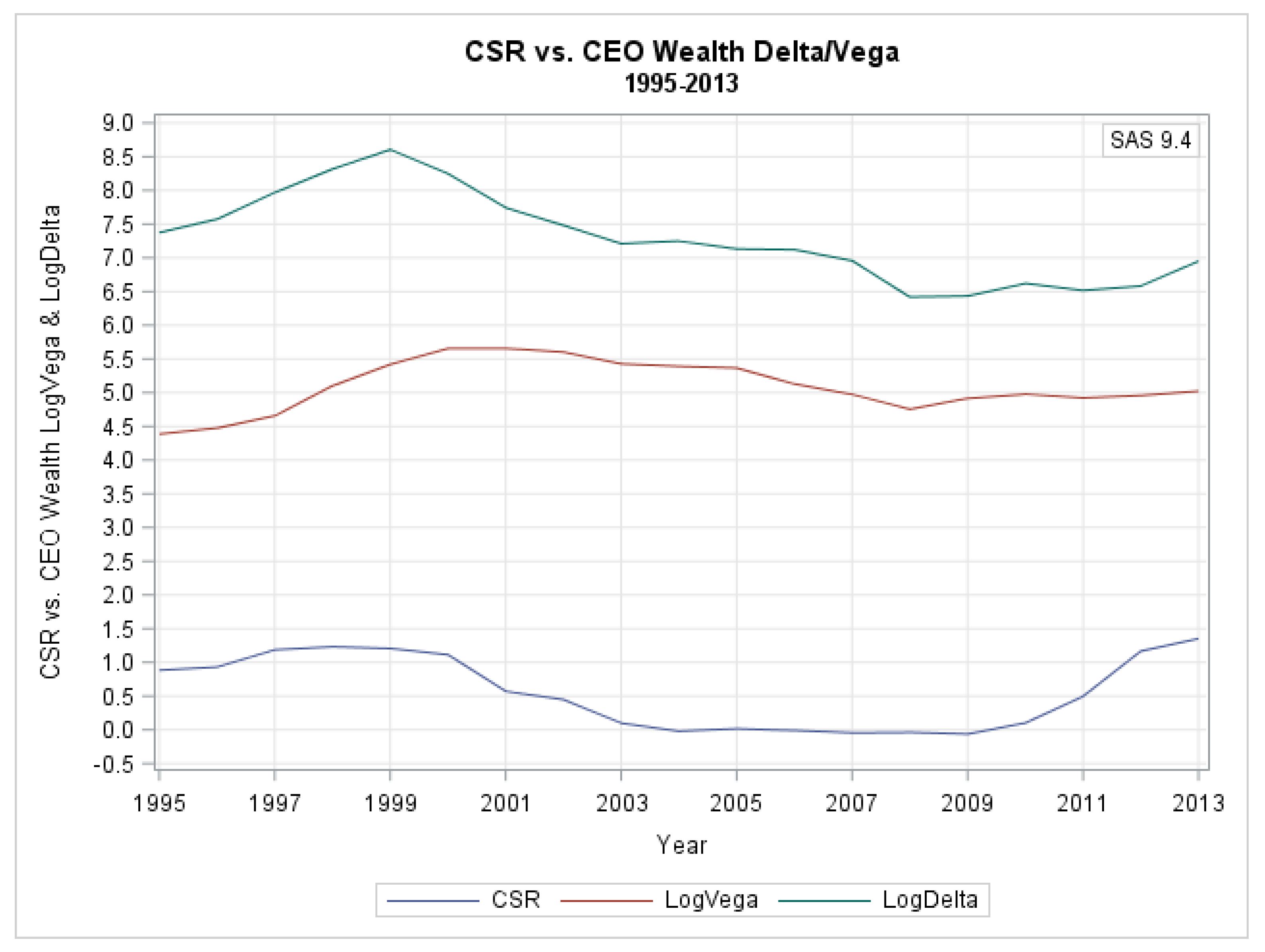

3. Data

We created a panel dataset spanning 1995–2013 using firm fundamental data, executive compensation data, CSR ratings, and CEO pay sensitivity data. The firm fundamentals data were obtained using the Standard and Poor’s COMPUSTAT North America database which covers all public firms listed in the U.S. across all industries. This database contains detailed, up-to-date firm fundamentals information for North American securities. The database uses SEC (the U.S. Securities and Exchange Commission) filings to track firm balance sheet, income statement, and cash flow statement entries on an annual, quarterly, and year-to-date basis. We used firms’ unique identifier (GVKEY) to follow changes in firm fundamentals through time. We gather measures of Total Debt (DT), Total Assets (AT), Research and Development Expense (XRD), Total Sales (REVT), and Industry SIC Code (SIC). We then computed the variables Debt-to-Assets (DTA), LogAssets, LogSales, and LogR&D. These variables were later used as controls for firm size, firm risk, and industry when we constructed our model. For example, we used total sales and total assets as proxies for firm size in accordance with Tsoutsoura [

33]; we controlled for R&D expenses following McWilliams and Siegel [

55].

We obtained executive compensation data from the Standard and Poor’s EXECUCOMP database. This database provides detailed compensation data for the highest paid executives at over 3462 firms that are part of the S&P 1500 index or were once part of the index and whose securities remain publicly traded. This database allows us to separate annual CEO compensation into its cash, stock, and options components. The data start in 1992, but the post-1994 data contain a much larger number of firms due to expansion of the database’s mandate. The database also provides each executive with a permanent ID (EXECID), as well as each firm/executive combination with a unique identifier during their tenure (CO_PER_ROL). Data are reported on a fiscal year basis and contain information on cash awards, vested/unvested stock and options awards, deferred compensation, and pension awards. For a given year, a firm’s CEO can be identified using the CEOANN flag variable.

CSR data were obtained using the MSCI ESG Stats Data Set. This is the same Kinder, Lydenberg, and Domini (KLD) data used in the previous literature [

33,

39,

56,

57], but the dataset is now managed by MSCI, who acquired KLD in 2010. The KLD data are collected by a global team of over 140 research analysts. They assess how well companies manage environmental, social, and governance (ESG) risks using macro data, company disclosures, government databases, news articles, and NGO data. Each company is then assigned a positive or negative indicator for ESG performance, and firms are invited to verify the findings. The dataset contains yearly ESG indicators for over 2600 firms. For the purposes of constructing the CSR rating, an ESG strength was assigned a score of +1, while a concern was given a score of −1. We used six different ESG strength/concern criteria in our analysis: company, diversity, employee, environmental, human rights, and product. We excluded the corporate governance category, following the literature. In our research setting, corporate governance measures may well be the determinants of CEO incentives, which defeats our attempt to study how incentives lead to social performance. We then summed the total strengths and concerns for firms to obtain our CSR rating variable.

Since Waddock and Graves [

39], KLD data as a measure of corporate social responsibility have become increasingly popular [

33]. Tsoutsoura [

33] measures CSR using both the KLD ratings data for S&P 500 companies and the Domini 400 Social index (DSI 400). She follows the method of McWilliams and Siegel [

55] by creating a dummy variable for CSP that is equal to 1 if a firm is included in the DSI 400 and 0 otherwise. She also uses COMPUSTAT to find measures of firm performance through accounting measures such as return on assets (ROA), return on equity (ROE), and return on sales (ROS). She then creates a panel dataset spanning 1996–2000 and adds control variables to account for firm risk, size, and industry. Previous studies [

17,

39,

41] find that CSR is positively related to firm profitability.

Data on CEO pay sensitivity to the underlying stock price (delta) and stock volatility (vega) are obtained via the Core et al. [

30] and Coles et al. [

7] datasets. The authors use EXECUCOMP data to determine the number of vested and unvested stock and options holdings of each executive, as well as the expiration dates of the options. They then use the closed form solution of the Black–Sholes option-pricing model to compute delta and vega estimates for each individual CEO. We merged this CEO pay sensitivity data with our COMPUSTAT, EXECUCOMP, and KLD data using YEAR and GVKEY variables. This gave us a dataset that provides a complete picture of CEO pay sensitivity, firm characteristics, and CSR ratings over time.

5. Conclusions

We developed a model to estimate CSR ratings as a function of CEO pay sensitivity to delta and vega. We used panel data spanning 1995–2013 to construct yearly firm CSR ratings and estimates of CEO pay sensitivity to firm stock price (delta) and volatility (vega). This was the longest sample period we were able to collect. The nineteen years were long enough for the statistically significant tests we conducted. In addition, to capture macro shocks in the sample period, we controlled for year fixed effects. We found that CSR ratings increased as CEOs were exposed to higher levels of vega, but not delta. This leads us to conclude that CEOs make CSR related decisions independent of their pay sensitivity to the underlying stock price, but that CEOs view CSR projects as a way of promoting stock volatility. Given that we should expect CSR ratings to have a positive relationship with delta if it is viewed as a value-enhancing policy, these results suggest that CEOs may be pursuing CSR projects simply to increase their own compensation through vega by increasing stock price volatility.

When interpreting these results, it is imperative not to infer conclusions regarding the actual effect of CSR on firm value. Our analysis only indicates how CEOs perceive CSR standings, not the actual effect these investments have on a firm’s financial performance. CEO actions are not always value maximizing from the shareholder’s perspective. Sometimes, this manifests itself through agency problems, but sometimes it is because CEOs do not have the necessary information to make ex-post value-maximizing decisions. The effects of CSR on financial performance are a major source of debate in the literature. Therefore, it is reasonable to assume that CEOs may also be unsure of how to make value-maximizing CSR investments. If we infer that CEOs are acting in the best interest of shareholders, then a decision made independently of delta could be consistent with the neutral present value proposition from Ullmann [

43]. However, it could also be reconciled with the viewpoint that CSR increases financial performance [

17,

40,

41], since it could be argued that CEOs implement CSR measures when there is a clear benefit to the firm, regardless of delta exposure.

Most importantly, our findings on the relation between CEOs’ pay sensitivity to vega and CSR ratings indicate that CEOs make CSR investments to increase firm risk, which would be inconsistent with [

45,

49]. One plausible explanation is that CEOs may simply view CSR as a way of increasing stock price volatility without having adverse effects on operational risk. For example, this could be achieved if many market participants have diverging views on the correct valuation methods to apply to CSR projects. Under these assumptions, a situation could be constructed where the expectation of the stock price remains unchanged with an increase in CSR standing while volatility of the stock price increases. Another potential explanation is that CEOs with higher vega exposure choose riskier CSR projects than other CEOs. Further research needs to be performed in this area in order to properly identify the source of this relationship. These findings have implications for both the executive compensation literature and the CSR literature. By understanding how CEOs respond to various compensation incentives, we can begin to formulate better compensation structures that minimize agency costs and simultaneously maximize shareholder and stakeholder value.

To better address the omitted variable bias that likely exists in this paper and any studies alike, future research should focus on better empirical proxies and theoretical frameworks for managerial risk aversion and talent. Empiricists should collect more detailed information, for instance, on CEOs’ background and personal experience. For theorists, it is important to model other forces aside from those in the agency framework. Developing new theories of how managerial attributes affect firm policy and outcomes and the contractual structure of managerial compensation can contribute to our understanding of the relationships between executive compensation and CSR.

{kind=link}