Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinese Private Firms

Abstract

1. Introduction

2. Literature Review

3. Theory and Hypotheses

3.1. Political Ties and Private Firms’ Over-Investment in CSR

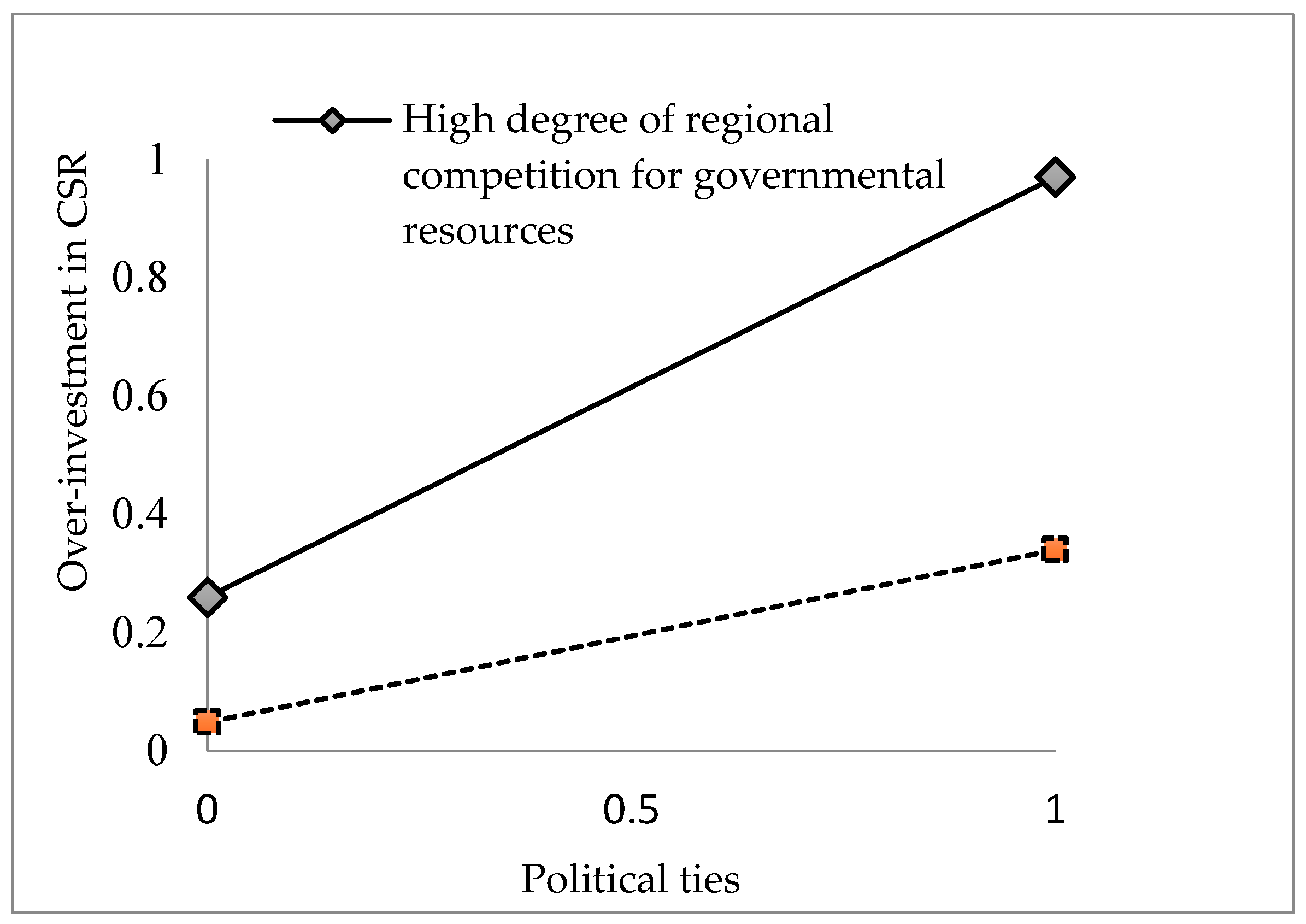

3.2. The Moderating Effect of Regional Competition for Governmental Resources

4. Methods

4.1. Data and Sample

4.2. Measures

5. Results

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CSR investments | 0.17 | 0.00 | 1 | |||||||||||

| CSR over-investment | 0.42 | 0.49 | 0.29 | 1 | ||||||||||

| Political ties | 0.47 | 0.50 | −0.11 | 0.14 | 1 | |||||||||

| Regional competition for government resources | 9.84 | 2.67 | −0.09 | 0.11 | 0.02 | 1 | ||||||||

| Firm age | 7.39 | 4.75 | −0.07 | 0.04 | 0.25 | 0.12 | 1 | |||||||

| Firm size | 6.67 | 2.18 | −0.44 | 0.24 | 0.40 | 0.23 | 0.23 | 1 | ||||||

| New product number | 0.66 | 1.16 | −0.06 | 0.08 | 0.20 | 0.13 | 0.15 | 0.32 | 1 | |||||

| Brand number | 0.19 | 0.42 | −0.06 | 0.06 | 0.24 | 0.01 | 0.16 | 0.26 | 0.36 | 1 | ||||

| Overseas investment ratio | 0.00 | 0.05 | 0.01 | 0.01 | 0.02 | −0.00 | 0.00 | −0.01 | 0.02 | 0.01 | 1 | |||

| Overseas sales ratio | 0.05 | 0.02 | −0.06 | 0.06 | 0.07 | 0.17 | 0.07 | 0.21 | 0.25 | 0.08 | 0.04 | 1 | ||

| R&D intensity | 0.02 | 0.13 | 0.11 | 0.00 | −0.01 | −0.02 | −0.00 | −0.08 | 0.12 | 0.03 | 0.01 | 0.03 | 1 | |

| Advertisement intensity | 0.01 | 0.12 | 0.32 | −0.02 | −0.02 | −0.03 | −0.03 | −0.13 | 0.01 | 0.00 | 0.00 | −0.02 | 0.21 | 1 |

| ROS | 4.57 | 0.13 | −0.19 | 0.02 | 0.02 | 0.01 | 0.02 | 0.04 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 |

| Leverage ratio | 1.04 | 4.67 | −0.04 | 0.02 | 0.04 | −0.01 | 0.02 | 0.11 | 0.04 | 0.06 | −0.01 | 0.03 | −0.00 | −0.01 |

| Donation history | 0.99 | 0.08 | 0.11 | −0.02 | 0.05 | 0.02 | 0.03 | 0.11 | 0.07 | 0.06 | 0.01 | 0.04 | 0.02 | 0.02 |

| Quality certificate | 0.46 | 0.50 | −0.10 | 0.06 | 0.26 | 0.10 | 0.18 | 0.43 | 0.35 | 0.34 | 0.03 | 0.15 | 0.03 | −0.03 |

| ROE | 0.73 | 0.08 | −0.08 | 0.08 | 0.04 | 0.03 | 0.04 | 0.13 | 0.07 | 0.05 | 0.00 | 0.01 | 0.06 | −0.01 |

| Income | 8.25 | 0.23 | −0.09 | 0.14 | 0.17 | 0.05 | 0.09 | 0.33 | 0.19 | 0.18 | −0.00 | 0.04 | 0.08 | −0.02 |

| Managerial discretion | 0.33 | 0.47 | 0.06 | 0.01 | −0.12 | 0.02 | 0.01 | −0.24 | −0.12 | −0.08 | −0.03 | −0.04 | −0.03 | −0.02 |

| Entrepreneur duality | 1.09 | 0.29 | 0.04 | −0.00 | −0.12 | −0.06 | −0.07 | −0.07 | −0.02 | −0.02 | 0.03 | −0.04 | −0.02 | 0.03 |

| Entrepreneur age | 47.19 | 70.37 | −0.02 | −0.03 | −0.02 | −0.02 | 0.02 | 0.02 | 0.01 | 0.00 | −0.01 | −0.00 | −0.00 | −0.01 |

| Entrepreneur education | 3.03 | 1.19 | 0.02 | −0.10 | −0.14 | 0.09 | 0.05 | −0.18 | −0.14 | −0.11 | −0.03 | −0.01 | −0.04 | 0.00 |

| Entrepreneur gender | 1.15 | 0.36 | 0.00 | −0.05 | −0.10 | −0.07 | −0.07 | −0.13 | −0.08 | −0.03 | 0.03 | −0.04 | 0.02 | 0.02 |

| 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | ||||

| ROS | 1 | |||||||||||||

| Leverage ratio | 0.00 | 1 | ||||||||||||

| Donation history | 0.00 | 0.02 | 1 | |||||||||||

| Quality certificate | 0.02 | 0.07 | 0.08 | 1 | ||||||||||

| ROE | 0.02 | 0.30 | 0.02 | 0.08 | 1 | |||||||||

| Income | 0.02 | 0.02 | 0.02 | 0.19 | 0.25 | 1 | ||||||||

| Managerial discretion | 0.01 | −0.03 | −0.01 | −0.13 | −0.03 | −0.09 | 1 | |||||||

| Entrepreneur duality | 0.01 | −0.02 | −0.05 | −0.06 | 0.02 | −0.0 | −0.10 | 1 | ||||||

| Entrepreneur age | 0.00 | −0.01 | −0.01 | 0.01 | −0.01 | 0.01 | −0.02 | 0.00 | 1 | |||||

| Entrepreneur education | 0.00 | 0.02 | −0.01 | −0.11 | −0.04 | −0.10 | 0.19 | −0.06 | 0.03 | 1 | ||||

| Entrepreneur gender | 0.01 | −0.02 | −0.02 | −0.10 | −0.01 | −0.04 | 0.01 | 0.07 | 0.00 | −0.01 | 1 |

| DV = Over-Investment in CSR | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Control variable | |||

| Regional competition for governmental resources | 0.027 *** | 0.030 *** | 0.029 *** |

| (0.010) | (0.010) | (0.011) | |

| Firm age | −0.007 | −0.010 ** | −0.010 ** |

| (0.005) | (0.005) | (0.005) | |

| Firm size | 0.141 *** | 0.127 *** | 0.130 *** |

| (0.037) | (0.040) | (0.040) | |

| New product number | 0.008 | 0.009 | 0.005 |

| (0.030) | (0.030) | (0.030) | |

| Brand number | 0.009 | −0.014 | −0.011 |

| (0.060) | (0.058) | (0.057) | |

| Overseas investment ratio | 0.496 | 0.452 | 0.495 |

| (0.534) | (0.516) | (0.526) | |

| Overseas sales ratio | −0.054 | −0.051 | −0.065 |

| (0.121) | (0.124) | (0.122) | |

| R&D intensity | 0.016 | 0.016 | 0.002 |

| (0.333) | (0.336) | (0.334) | |

| Advertisement intensity | 0.261 | 0.243 | 0.238 |

| (0.195) | (0.192) | (0.193) | |

| ROS | 0.118 | 0.116 | 0.118 |

| (0.098) | (0.099) | (0.097) | |

| Leverage ratio | −0.003 | −0.003 | −0.003 |

| (0.004) | (0.004) | (0.004) | |

| Donation history | −0.614 ** | −0.635 ** | −0.649 ** |

| (0.295) | (0.300) | (0.304) | |

| Quality certificate | −0.171 *** | −0.180 *** | −0.186 *** |

| (0.066) | (0.064) | (0.064) | |

| ROE | 0.618 | 0.634 | 0.675 |

| (0.638) | (0.658) | (0.655) | |

| Net income | 0.338 | 0.327 | 0.326 |

| (0.284) | (0.285) | (0.283) | |

| Managerial discretion | 0.219 *** | 0.229 *** | 0.231 *** |

| (0.077) | (0.076) | (0.077) | |

| Entrepreneur’s duality | 0.004 | 0.026 | 0.023 |

| (0.113) | (0.117) | (0.117) | |

| Entrepreneur’s age | −0.001 *** | −0.001 *** | −0.001 *** |

| (0.000) | (0.000) | (0.000) | |

| Entrepreneur’s education | −0.079 *** | −0.074 *** | −0.074 *** |

| (0.019) | (0.019) | (0.019) | |

| Entrepreneur’s gender | −0.070 | −0.060 | −0.059 |

| (0.098) | (0.098) | (0.098) | |

| Independent variable | |||

| Political ties | 0.197 *** | 0.185 ** | |

| (0.074) | (0.088) | ||

| Interaction term | |||

| Political ties × competition for governmental resources | 0.044 ** | ||

| (0.020) | |||

| Industry dummies | Included | Included | Included |

| Log likelihood | −1479.816 *** | −1474.748 *** | −1472.454 *** |

| N | 2304 | 2304 | 2304 |

References

- Lin, K.J.; Tan, J.; Zhao, L.; Karim, K. In the name of charity: Political connections and strategic corporate social responsibility in a transition economy. J. Corp. Financ. 2015, 32, 327–346. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Jamali, D.; Mirshak, R. Corporate social responsibility (CSR): Theory and practice in a developing country context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Benlemlih, M.; Bitar, M. Corporate social responsibility and investment efficiency. J. Bus. Ethics 2018, 148, 647–671. [Google Scholar] [CrossRef]

- Becchetti, L.; Ciciretti, R.; Hasan, I. Corporate social responsibility, stakeholder risk, and idiosyncratic volatility. J. Corp. Financ. 2015, 35, 297–309. [Google Scholar] [CrossRef]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate social responsibility and firm risk: Theory and empirical evidence. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manage. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Lys, T.; Naughton, J.P.; Wang, C. Signaling through corporate accountability reporting. J. Account. Econ. 2015, 60, 56–72. [Google Scholar] [CrossRef]

- Utz, S. Over-investment or risk mitigation? Corporate social responsibility in Asia-Pacific, Europe, Japan, and the United States. Rev. Financ. Econ. 2018, 36, 167–193. [Google Scholar] [CrossRef]

- Bhandari, A.; Javakhadze, D. Corporate social responsibility and capital allocation efficiency. J. Corp. Financ. 2017, 43, 354–377. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility a review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar]

- Blau, P.M. Justice in social exchange. Sociol. Inq. 1964, 34, 193–206. [Google Scholar] [CrossRef]

- Cropanzano, R.; Mitchell, M.S. Social exchange theory: An interdisciplinary review. J. Manag. 2015, 31, 874–900. [Google Scholar] [CrossRef]

- Yin, J.; Singhapakdi, A.; Du, Y. Causes and moderators of corporate social responsibility in China: The influence of personal values and institutional logics. Asian. Bus. Manag. 2016, 15, 226–254. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Eden, L.; Lau, C.M.; Wright, M. Strategy in emerging economies. Acad. Manag. J. 2000, 43, 249–267. [Google Scholar]

- Li, H.; Zhang, Y. The role of managers political networking and functional experience in new venture performance: Evidence from Chinas transition economy. Strateg. Manag. J. 2007, 28, 791–804. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and intrinsic drivers of corporate social performance: Evidence from foreign and domestic firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Rupp, D.E. An employee-centered model of organizational justice and social responsibility. Organ. Psychol. Rev. 2011, 1, 72–94. [Google Scholar]

- Rupp, D.E.; Ganapathi, J.; Aguilera, R.V.; Williams, C.A. Employee reactions to corporate social responsibility: An organizational justice framework. J. Organ. Behav. 2006, 27, 537–543. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Sharma, S. Managerial interpretations and organizational context as predictors of corporate choice of environmental strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar]

- Marcus, A.A.; Anderson, M.H. A general dynamic capability: Does it propagate business and social competencies in the retail food industry? J. Manag. Stud. 2006, 43, 19–46. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- den Hond, F.; de Bakker, F.G.A. Ideologically motivated activism: How activist groups influence corporate social change activities. Acad. Manag. Rev. 2007, 32, 901–924. [Google Scholar] [CrossRef]

- Hillman, A.J.; Withers, M.C.; Collins, B.J. Resource dependence theory: A review. J. Manag. 2009, 35, 1404–1427. [Google Scholar] [CrossRef]

- Tokoro, N. Stakeholders and corporate social responsibility (CSR): A new perspective on the structure of relationships. Asian Bus. Manag. 2007, 6, 143–162. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate social responsibility, ownership structure, and political interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Xin, K.K.; Pearce, J.L. Guanxi: Connections as substitutes for formal institutional support. Acad. Manag. J. 1996, 39, 1641–1658. [Google Scholar]

- Okhmatovskiy, I. Performance implications of ties to the government and SOEs: A political embeddedness perspective. J. Manag. Stud. 2010, 47, 1020–1047. [Google Scholar] [CrossRef]

- Peng, M.W.; Luo, Y. Managerial ties and firm performance in a transition economy: The nature of a micro-macro link. Acad. Manag. J. 2000, 43, 486–501. [Google Scholar]

- Shleifer, A.; Vishny, R.W. Politicians and firms. Q. J. Econ. 1994, 109, 995–1025. [Google Scholar] [CrossRef]

- See, G. Harmonious Society and Chinese CSR: Is There Really a Link? J. Bus. Ethics 2009, 89, 1–22. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ Sci. 2013, 25, 127–148. [Google Scholar] [CrossRef]

- Park, S.H.; Luo, Y. Guanxi and organizational dynamics: Organizational networking in Chinese firms. Strateg. Manag. J. 2001, 22, 455–477. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. Index of Marketization of China; Economic Science Press: Beijing, China, 2007. [Google Scholar]

- Cui, G.; Liu, Q. Regional market segments of China: Opportunities and barriers in a big emerging market. J. Consum. Mark. 2003, 17, 55–72. [Google Scholar] [CrossRef]

- Boisot, M.; Child, J. From fiefs to clans and network capitalism: Explaining China’s emerging economic order. Adm. Sci. Q. 1996, 41, 600–628. [Google Scholar] [CrossRef]

- Gao, Y.; Hafsi, T.; He, X. Business owners’ achieved social status and corporate philanthropy: Evidence from Chinese private small-and medium-sized enterprises. J. Manag. Organ. 2017, 23, 277–296. [Google Scholar] [CrossRef]

- Zhang, Y.; Liu, C.; Wang, T. Direct or indirect? The impact of political connections on export mode of Chinese private enterprises. China Econ. Rev. 2020, 61, 1–16. [Google Scholar] [CrossRef]

- Fabrizi, M.; Mallin, C.; Michelon, G. The role of CEO’s personal incentives in driving Corporate Social Responsibility. J. Bus. Ethics 2014, 124, 311–326. [Google Scholar] [CrossRef]

- Arya, B.; Zhang, G. Institutional reforms and investor reactions to CSR announcements: Evidence from an emerging economy. J. Manag. Stud. 2009, 46, 1089–1112. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C.B. The debate over doing good: Corporate social performance, strategic marketing levers, and firm-idiosyncratic risk. J. Mark. 2009, 73, 198–213. [Google Scholar] [CrossRef]

- Berens, G.; Van Riel, C.B.; Van Bruggen, G.H. Corporate associations and consumer product responses: The moderating role of corporate brand dominance. J. Mark. 2005, 69, 35–48. [Google Scholar] [CrossRef]

- Arnaud, S.; Wasieleski, D.M. Corporate humanistic responsibility: Social performance through managerial discretion of the HRM. J. Bus. Ethics 2014, 120, 313–334. [Google Scholar] [CrossRef]

- Orlitzky, M.; Benjamin, J.D. Corporate social performance and firm risk: A meta-analytic review. Bus. Soc. 2001, 40, 369–396. [Google Scholar] [CrossRef]

- Smith, S.M.; Alcorn, D.S. Cause marketing: A new direction in the marketing of corporate responsibility. J. Consum. Mark. 1991, 8, 19–35. [Google Scholar] [CrossRef]

- Wang, S.; Gao, Y.; Hodgkinson, G.P.; Rousseau, D.M.; Flood, P.C. Opening the black box of CSR decision making: A policy-capturing study of charitable donation decisions in China. J. Bus. Ethics 2015, 128, 665–683. [Google Scholar] [CrossRef]

- Liu, X.; Garcia, P.; Vredenburg, H. CSR adoption strategies of Chinese state oil companies: Effects of global competition and cooperation. Soc. Resp. J. 2014, 10, 38–52. [Google Scholar] [CrossRef]

- Hammond, S.A.; Slocum, J.W., Jr. The impact of prior firm financial performance on subsequent corporate reputation. J. Bus. Ethics 1996, 15, 159–165. [Google Scholar] [CrossRef]

- Graafland, J.; Van de Ven, B.; Stoffele, N. Strategies and instruments for organising CSR by small and large businesses in the Netherlands. J. Bus. Ethics 2003, 47, 45–60. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Karpoff, J.M.; Lott, J.R., Jr.; Wehrly, E.W. The reputational penalties for environmental violations: Empirical evidence. J. Law Econ. 2005, 48, 653–675. [Google Scholar] [CrossRef]

- Baltagi, B.H.; Chang, Y.-J. Incomplete panels: A comparative study of alternative estimators for the unbalanced one-way error component regression model. J. Econ. 1994, 62, 67–89. [Google Scholar] [CrossRef]

- Singer, J.D. Using SAS PROC MIXED to fit multilevel models, hierarchical models, and individual growth models. J. Educ. Behav. Stat. 1998, 23, 323–355. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G. Multiple Regression: Testing and Interpreting Interactions; Sage Publications: Thousand Oaks, CA, USA, 1991. [Google Scholar]

- Orlitzky, M. Corporate social responsibility, noise, and stock market volatility. Acad. Manag. Perspect. 2013, 27, 238–254. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Zhao, X.; Murrell, A.J. Revisiting the corporate social performance-financial performance link: A replication of Waddock and Graves. Strateg. Manag. J. 2016, 37, 2378–2388. [Google Scholar] [CrossRef]

- Zhao, X.; Wu, C.; Chen, C.C.; Zhou, Z. The influence of corporate social responsibility on incumbent employees: A meta-analytic investigation of the mediating and moderating mechanisms. J. Manag. 2020. [Google Scholar] [CrossRef]

| Variable | Measurement |

|---|---|

| Independent variable and moderator | |

| Political ties | Coded as “1” if an entrepreneur is a member of the CPPCC or a delegate of the PC, and as “0” otherwise |

| Regional competition for governmental resources | The index of the development of non-state sectors in China, a major sub-category in marketization index [40] |

| Dependent variable | |

| CSR investments | The ratio of the total amount of firm investment in environment, employee welfare, and local community to total sales in 2007 |

| Over-investments in CSR | Coded as “1” if the residual of the first-stage regression is greater than zero, and as “0” otherwise. |

| Control variable | |

| Firm age | 2007 minus the year of firm’s establishment |

| Firm size | Nature log of firm’s sales in 2007 |

| New product number | Nature log of total number of new products |

| Brand number | Nature log of total number of famous trademarks officially certificated by the State Administration for Industry and Commerce of China |

| Overseas investment ratio | The ratio of overseas investment to total sales in 2007 |

| Overseas sales ratio | The ratio of overseas sales to total sales in 2007 |

| R&D intensity | The ratio of R&D expenditures to total sales in 2007 |

| Advertisement intensity | The ratio of advertisement expenditure to total sales in 2007 |

| ROS | The ratio of net income to total sales |

| Leverage ratio | The ratio of debt to total asset |

| Donation history | Whether a firm had previously made charitable donations |

| Quality certificate | Whether a firm had acquired quality certificate (e.g., ISO 9000) |

| ROE | The ratio of net income to total equity |

| Net income | Net income in 2007 |

| Managerial discretion | Whether an entrepreneur has discretion in firm’s decision making |

| Entrepreneur duality | Whether the roles of CEO and chairperson were held simultaneously |

| Entrepreneur age | 2007 minus entrepreneur’s year of birth |

| Entrepreneur education | The conferring of credentials. Code entrepreneur education as 1–6 which correspond to six different levels of conferring of credentials (from primary school to graduate degree) |

| Entrepreneur gender | Male or female |

| Industry dummies | A set of industry dummies used to control for industry-fixed effects |

| DV = CSR Investments | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| Firm age | 0.001 | −0.003 *** | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Firm size | −0.072 *** | −0.080 *** | −0.070 *** | |

| (0.003) | (0.003) | (0.003) | ||

| New product number | 0.008 * | −0.004 | 0.012 ** | 0.007 |

| (0.005) | (0.005) | (0.005) | (0.005) | |

| Brand number | 0.015 | −0.009 | 0.020 | 0.009 |

| (0.012) | (0.014) | (0.013) | (0.012) | |

| Overseas investment ratio | 0.073 | 0.190 * | 0.067 | 0.085 |

| (0.095) | (0.109) | (0.103) | (0.096) | |

| Overseas sales ratio | 0.051 ** | −0.049 * | 0.054 * | 0.043 * |

| (0.026) | (0.030) | (0.028) | (0.026) | |

| R&D intensity | 0.160 *** | 0.271 *** | 0.217 *** | 0.160 *** |

| (0.037) | (0.042) | (0.040) | (0.037) | |

| Advertisement intensity | 0.795 *** | 0.940 *** | 0.808 *** | |

| (0.038) | (0.043) | (0.039) | ||

| ROS | −0.493 *** | −0.526 *** | −0.485 *** | −0.495 *** |

| (0.036) | (0.041) | (0.039) | (0.036) | |

| Leverage ratio | 0.002 | −0.000 | 0.002 | 0.002 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Donation history | 0.295 *** | 0.213 *** | 0.317 *** | 0.308 *** |

| (0.054) | (0.062) | (0.059) | (0.054) | |

| Quality certificate | 0.043 *** | −0.032 *** | 0.043 *** | 0.054 *** |

| (0.011) | (0.012) | (0.012) | (0.011) | |

| ROE | −0.167 *** | −0.221 *** | −0.168 | −0.172 *** |

| (0.061) | (0.070) | (0.067) | (0.062) | |

| Net income | 0.059 *** | −0.069 *** | 0.062 *** | 0.070 *** |

| (0.021) | (0.024) | (0.023) | (0.022) | |

| Managerial discretion | −0.040 *** | 0.016 | −0.051 *** | −0.040 *** |

| (0.010) | (0.011) | (0.011) | (0.010) | |

| Industry dummies | Included | Included | Included | Not Included |

| R2 | 0.449 | 0.280 | 0.348 | 0.429 |

| N | 2365 | 2365 | 2365 | 2379 |

| DV = Over-Investment in CSR | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Control variable | |||

| Regional competition for governmental resources | 0.025 * | 0.025 ** | 0.023 * |

| (0.013) | (0.012) | (0.013) | |

| Firm age | −0.008 * | −0.010 ** | −0.010 ** |

| (0.005) | (0.005) | (0.005) | |

| Firm size | 0.147 *** | 0.139 *** | 0.142 *** |

| (0.041) | (0.042) | (0.042) | |

| New product number | −0.007 | −0.006 | −0.009 |

| (0.032) | (0.032) | (0.031) | |

| Brand number | −0.026 | −0.037 | −0.034 |

| (0.052) | (0.054) | (0.053) | |

| Overseas investment ratio | 0.542 | 0.494 | 0.528 |

| (0.566) | (0.546) | (0.551) | |

| Overseas sales ratio | −0.120 | −0.116 | −0.128 |

| (0.125) | (0.126) | (0.124) | |

| R&D intensity | −0.001 | −0.001 | −0.015 |

| (0.334) | (0.339) | (0.337) | |

| Advertisement intensity | 0.315 | 0.304 | 0.298 |

| (0.215) | (0.213) | (0.213) | |

| ROS | 0.131 | 0.128 | 0.128 |

| (0.099) | (0.101) | (0.101) | |

| Leverage ratio | −0.004 | −0.004 | −0.004 |

| (0.004) | (0.003) | (0.003) | |

| Donation history | −0.692 ** | −0.699 ** | −0.708 ** |

| (0.306) | (0.303) | (0.306) | |

| Quality certificate | −0.205 *** | −0.207 *** | −0.211 *** |

| (0.066) | (0.066) | (0.065) | |

| ROE | 0.641 | 0.651 | 0.692 |

| (0.683) | (0.693) | (0.691) | |

| Net income | 0.348 | 0.343 | 0.342 |

| (0.300) | (0.301) | (0.299) | |

| Managerial discretion | 0.232 *** | 0.235 *** | 0.236 *** |

| (0.079) | (0.078) | (0.078) | |

| Entrepreneur duality | 0.010 | 0.021 | 0.017 |

| (0.104) | (0.104) | (0.104) | |

| Entrepreneur age | −0.001 *** | −0.001 *** | −0.001 *** |

| (0.000) | (0.000) | (0.000) | |

| Entrepreneur education | −0.085 *** | −0.084 *** | −0.084 *** |

| (0.023) | (0.022) | (0.022) | |

| Entrepreneur gender | −0.080 | −0.078 | −0.077 |

| (0.103) | (0.101) | (0.100) | |

| Independent variable | |||

| Political ties | 0.188 ** | 0.192 ** | |

| (0.074) | (0.083) | ||

| Interaction term | |||

| Political ties × regional competition for governmental resources | 0.046 * | ||

| (0.025) | |||

| Industry dummies | Included | Included | Included |

| Log likelihood | −1462.056 *** | −1459.354 *** | −1457.517 *** |

| N | 2304 | 2304 | 2304 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xiong, C.; Zhang, K.; Zhao, X. Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinese Private Firms. Sustainability 2020, 12, 7203. https://doi.org/10.3390/su12177203

Xiong C, Zhang K, Zhao X. Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinese Private Firms. Sustainability. 2020; 12(17):7203. https://doi.org/10.3390/su12177203

Chicago/Turabian StyleXiong, Chan, Ke Zhang, and Xiaoping Zhao. 2020. "Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinese Private Firms" Sustainability 12, no. 17: 7203. https://doi.org/10.3390/su12177203

APA StyleXiong, C., Zhang, K., & Zhao, X. (2020). Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinese Private Firms. Sustainability, 12(17), 7203. https://doi.org/10.3390/su12177203