1. Introduction

Achieving financial sustainability is a basic goal for everyone and it has become a shared concern globally due to increasing life expectancy. Low financial sustainability may refer to individuals with low financial wealth, as well as investors with a lack of financial literacy. Especially for individuals with limited wealth, financial sustainability after retirement is a real concern because of uncertainty in pension plans arising from relatively early retirement age and change in the demographic structure (see, for example, [

1,

2]). One form of attaining financial independence is through investment in financial assets. Even though high-net-worth individuals can easily receive professional management services, that is not the case for most individuals, which leads to poor risk management that can have a direct impact on their lifestyle after retirement. Regarding low financial sustainability due to financial illiteracy, investment in funds (e.g., mutual funds) are often recommended. Even though funds provide exposure to stock markets, sectors or countries, understanding detailed fund structure and selecting appropriate funds may be more difficult than choosing among familiar companies for investors without much experience [

3].

Without professional advice, the investment behavior of individuals is known to be highly influenced by familiarity, which leads to concentrated investments that are not diversified. Diversifying investments is one of the fundamental approaches for reducing risk and the power of diversification shows that even the risk of an equally-weighted portfolio decreases with a larger number of assets. Diversification is particularly important for individual investors who are not-so-rich, because drawdowns are much more critical compared to high-net-worth individuals or institutional investors [

4].

Therefore, it is critical to analyze whether it is possible to form well-diversified portfolios with a small portfolio size. In this study, we investigate the relationship between portfolio size and risk, but we focus on an alternative measure of portfolio size: the total amount of investment (i.e., portfolio budget). The number of securities in a given portfolio may represent the size of the portfolio to some degree, but we believe that the total nominal amount of investment is more suitable for analyzing the viability of small account diversification and more representative of individuals’ financial strength. Another key contribution of our formulation is computing the optimal allocation in terms of the number of shares (quantity) instead of portfolio weights. This properly enforces budget restrictions by incorporating asset price (e.g., limitations on investing in stocks trading at high prices).

In our analysis, diversification benefit is examined through efficient portfolios in the mean-variance framework. That is, instead of analyzing the average performance of randomly constructed portfolios as in most of the previous studies, we study the maximum level of risk diversification of constrained mean-variance efficient portfolios since the mean-variance framework exploits risk diversification by incorporating correlations between asset returns. This is especially important because mean-variance analysis is the fundamental approach in portfolio allocation [

5] as well as automated investment management for individual investors [

6].

The remainder of the paper is organized as follows. The literature review is included in

Section 2.

Section 3 introduces our proposed formulation for constructing optimal portfolios with budget constraints.

Section 4 presents the empirical results on the effect of portfolio size. Further discussion on investment with small accounts is included in

Section 5, and

Section 6 concludes the paper.

2. Literature Review

While the notion of diversification often expressed as ‘don’t put all your eggs in one basket’ predates modern portfolio theory, Markowitz [

7] pioneered portfolio optimization through his mean-variance model, which presented a theory for analyzing the effects of diversification when risks are correlated and provided a framework for measuring the benefits of diversification [

8]. The mean-variance model computes portfolio risk using the variance of returns and portfolio variance can be reduced by investing in multiple assets with low correlation.

The mean-variance framework has since led to numerous extensions as well as applications in practice [

9]. Konno and Yamazaki [

10] propose mean-absolute deviation portfolio optimization that can be formulated as a linear program. Other measures of risk, such as lower semi-absolute deviation [

11] and conditional value-at-risk [

12], are also suggested. As for improving practicality, constraints for the tracking error of portfolios are incorporated by Jorion [

13] and cardinality constraints using regularization are studied in Brodie et al. [

14]. Moreover, robust portfolio models are introduced to reduce the sensitivity of mean-variance portfolios [

15].

Generally, theories and formulations on portfolio optimization can be applied at the individual asset level or asset-class level and the models are not restricted to specific investor types. Nonetheless, achieving diversification through portfolio optimization has been primarily adopted by asset managers and not average individual investors. Individuals are observed to invest in assets with high familiarity. More specifically, Kenneth and Poterba [

16] investigate domestic ownership of the world’s five largest stock markets and find that individual investors lack international diversification. Furthermore, individuals show strong interest in domestic firms that are located nearby [

17,

18,

19]. For average individuals, familiarity often leads to investment in few numbers of stocks and this causes major concern due to lack of risk diversification. Goetzmann and Kumar [

20] find that U.S. individual investors held four stocks on average during the 1991 to 1996 period, and Polkovnichenko [

21] reveals that many individuals that invest directly in stocks hold only one or two stocks based on the Survey of Consumer Finances data during the 1983 to 2001 period.

These observations clearly show how individuals hold under-diversified portfolios and the diversification levels of concentrated portfolios have been observed by several studies. These studies focus on the effect of portfolio size on reducing investment risk through diversification, where most studies observe the number of securities in a portfolio as a representation of portfolio size. Evans and Archer [

22] state that one can achieve a diversified portfolio with only ten stocks. Fisher and Lorie [

23] find that investment in eight stocks demonstrates most of the benefits of investing in a larger number of stocks. On the other hand, Elton and Gruber [

24] argue that the decrease in risk from adding stocks beyond 15 appears to be significant. In addition, at least 30 stocks are suggested by Statman [

25], over 300 stocks are observed by Statman [

26], and a minimum of 20 stocks are recommended by Chong and Phillips [

27] for forming a well-diversified portfolio. These findings are not converging towards a certain number but rather reveal the difficulty in observing a definitive relationship between the number of stocks and diversification. The main contribution of our study is that we analyze the relationship between portfolio size and risk where portfolio size is measured as the total investment amount.

Recently, automated services commonly referred to as robo-advisors began also serving investors with small accounts for providing investment diversification. Goal-based management for individuals is also popular, which refers to portfolio models that address multiple investment objectives of individuals [

28,

29]. As these services are mostly based on quantitative approaches [

6,

30], it is essential to investigate if it is theoretically possible to gain diversification effects with small investment amount.

3. Quantity-Based Optimal Mean-Variance Portfolio with Limited Size

The construction of an optimal mean-variance portfolio with a limited investment amount is based on the traditional mean-variance model of Markowitz [

7]. The traditional mean-variance formulation finds the portfolio with minimum variance while having expected return above a required level. Since long-term investments often avoid short positions, we focus on the formulation with no-shorting constraints expressed by the non-negativity restrictions on weights,

| |

| s.t. | 1Tw = 1 |

| | wTμ ≥ μ0 |

| | w ≥ 0 |

where

| n ∈ ℤ≥0 | :number of candidate securities, |

| w ∈ ℝn | :portfolio weight vector, |

| μ ∈ ℝn | :mean return vector of n securities, |

| Σ ∈ ℝ n × n | :covariance matrix of n securities, |

| μ0 ∈ ℝ | :minimum required expected return, |

| 1 ∈ ℝn | :vector of ones. |

While the above formulation finds the optimal allocation as portfolio weights that sum to one, we reformulate the problem so the optimal allocation is expressed as the number of shares to hold for each security. Thus, purchasing a fraction of a share is not allowed and investors can buy securities only in a non-negative integer number of shares. While this constraint is not necessary in all investment situations, it is a better reflection of reality for investors with small investment amounts. With a specified investment budget

, the portfolio weight

can be rewritten as

where

| :quantity vector, |

| :price vector, |

| :budget, |

and the notation

denotes the Hadamard product (or element-wise product). By substituting the expression for portfolio weight

w, the original Markowitz problem with no-shorting constraints can now be expressed as the following,

The above formulation given by (1) finds the optimal allocation in terms of the quantity of each security to purchase when there exists an overall budget on the investment. Since it finds a portfolio with minimum risk for a given level of expected return, the resulting allocation is an efficient portfolio within the mean-variance framework. Therefore, the proposed formulation given by (1) captures the budget constraint of individual investors and the composition of the optimal portfolio will reveal the relationship between portfolio size and risk diversification. In other words, diversification levels can be observed for various investment amounts to analyze the necessary budget size for achieving diversification benefits. Optimal mean-variance portfolios constructed from formulation (1) are further analyzed in the following section.

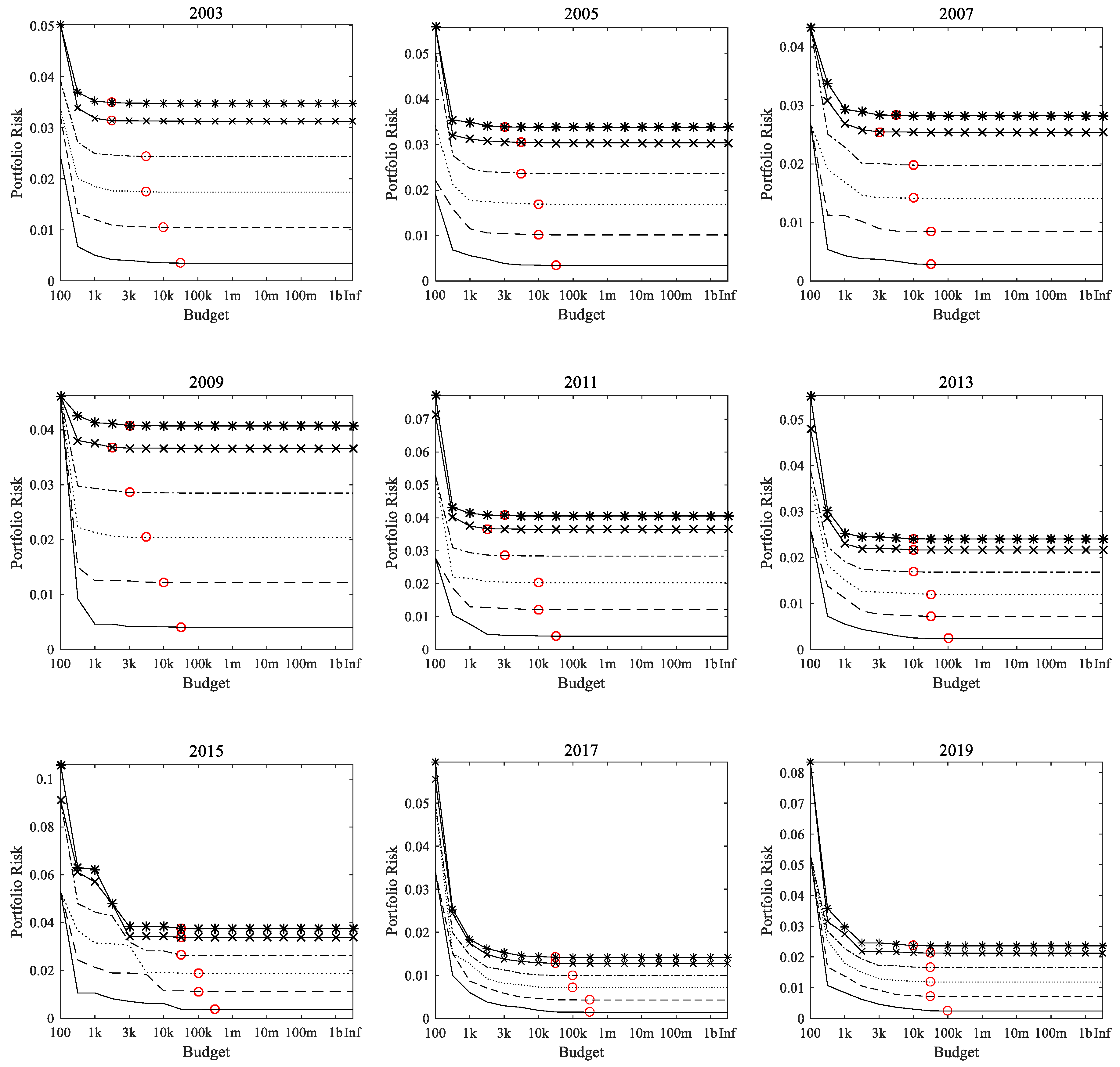

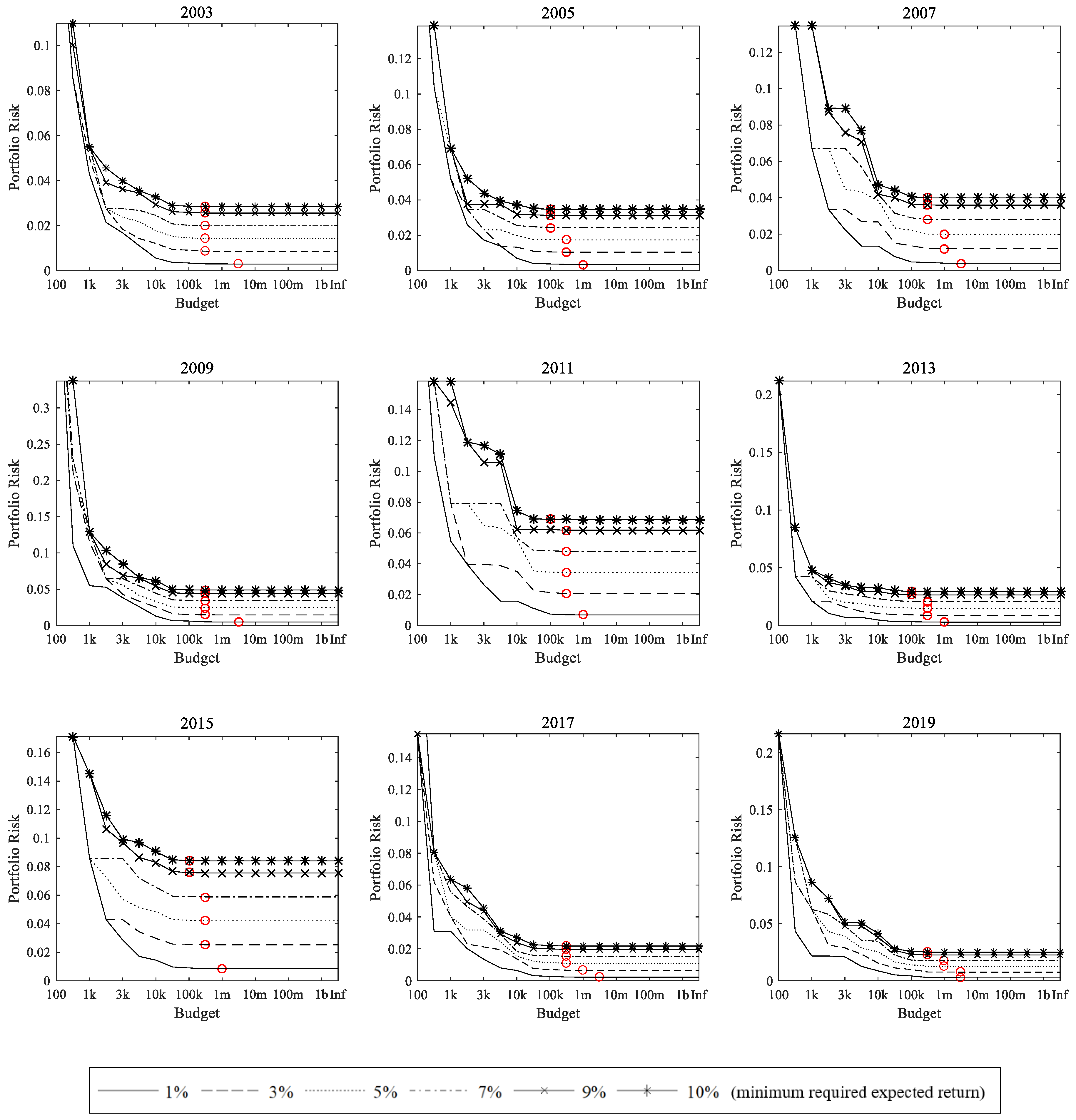

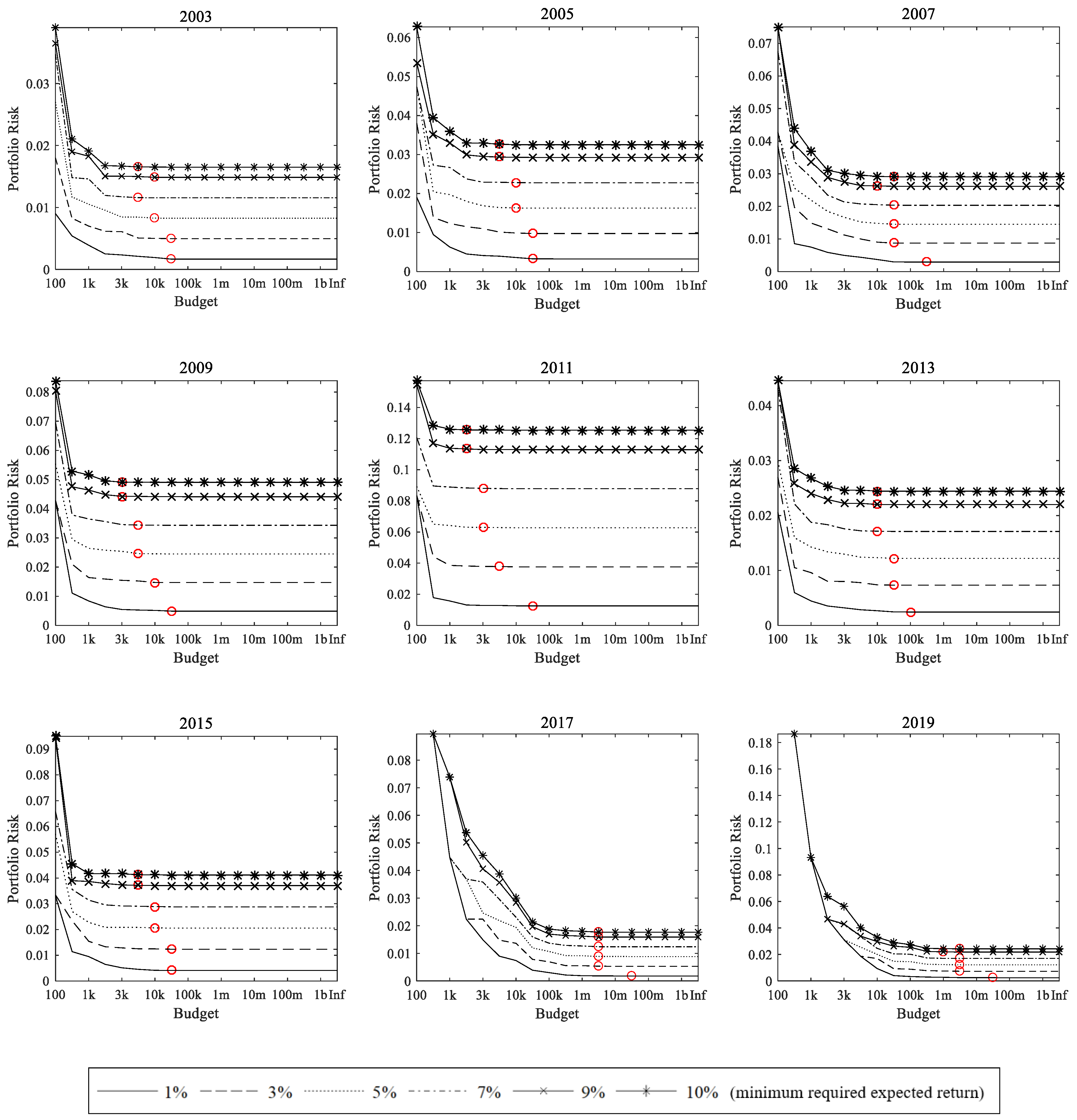

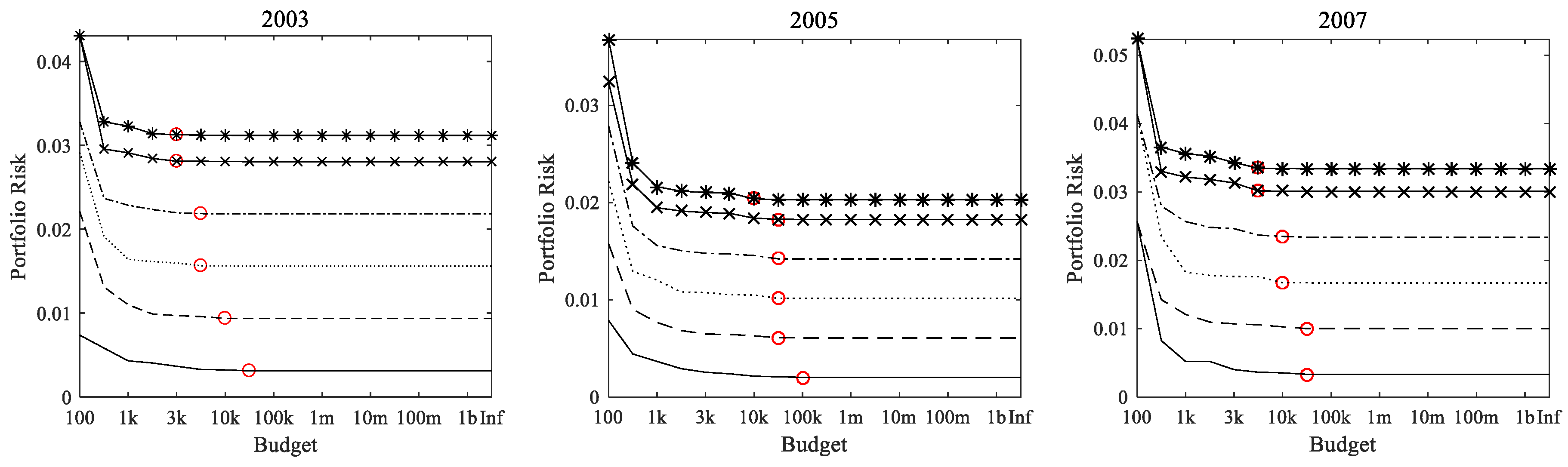

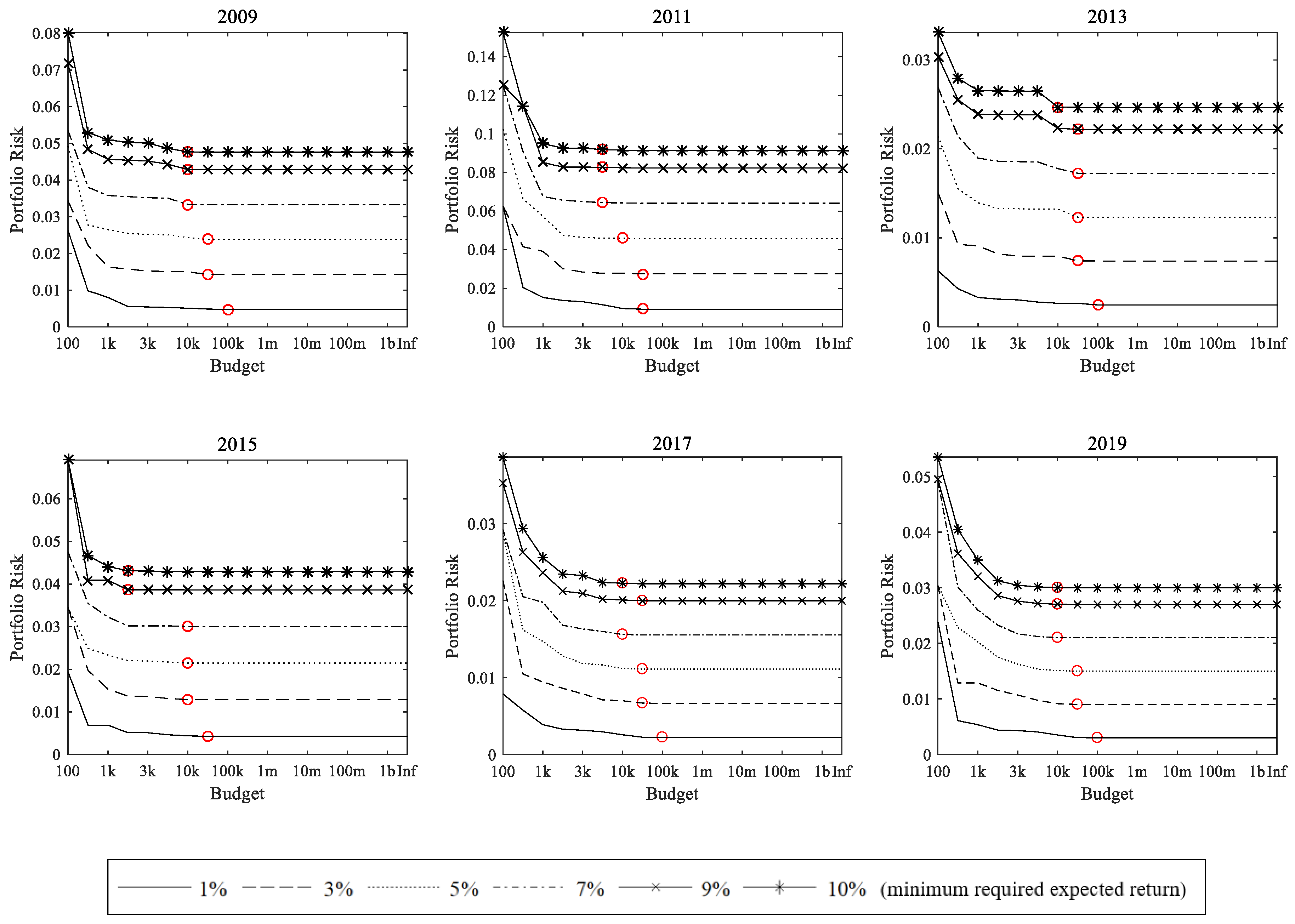

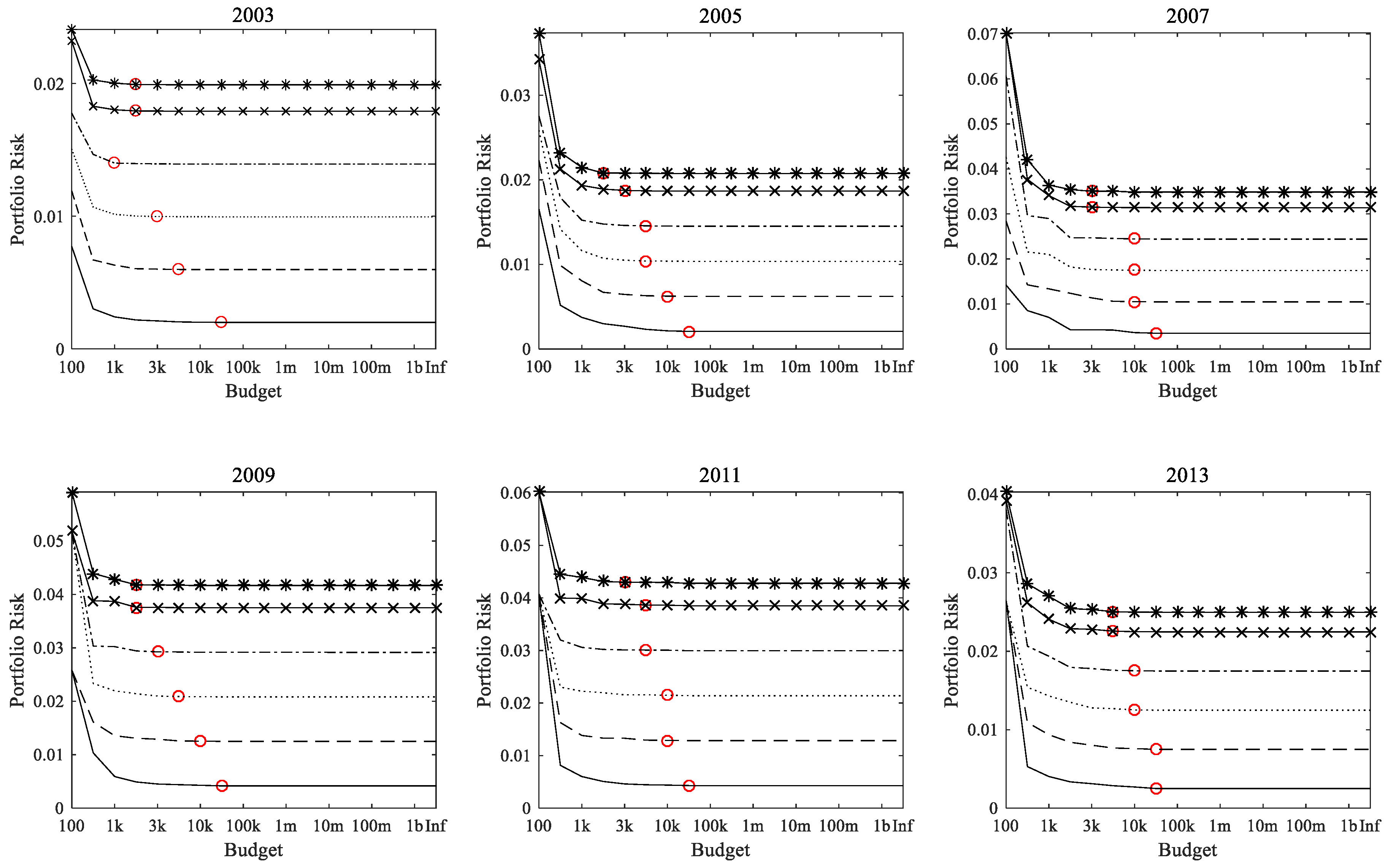

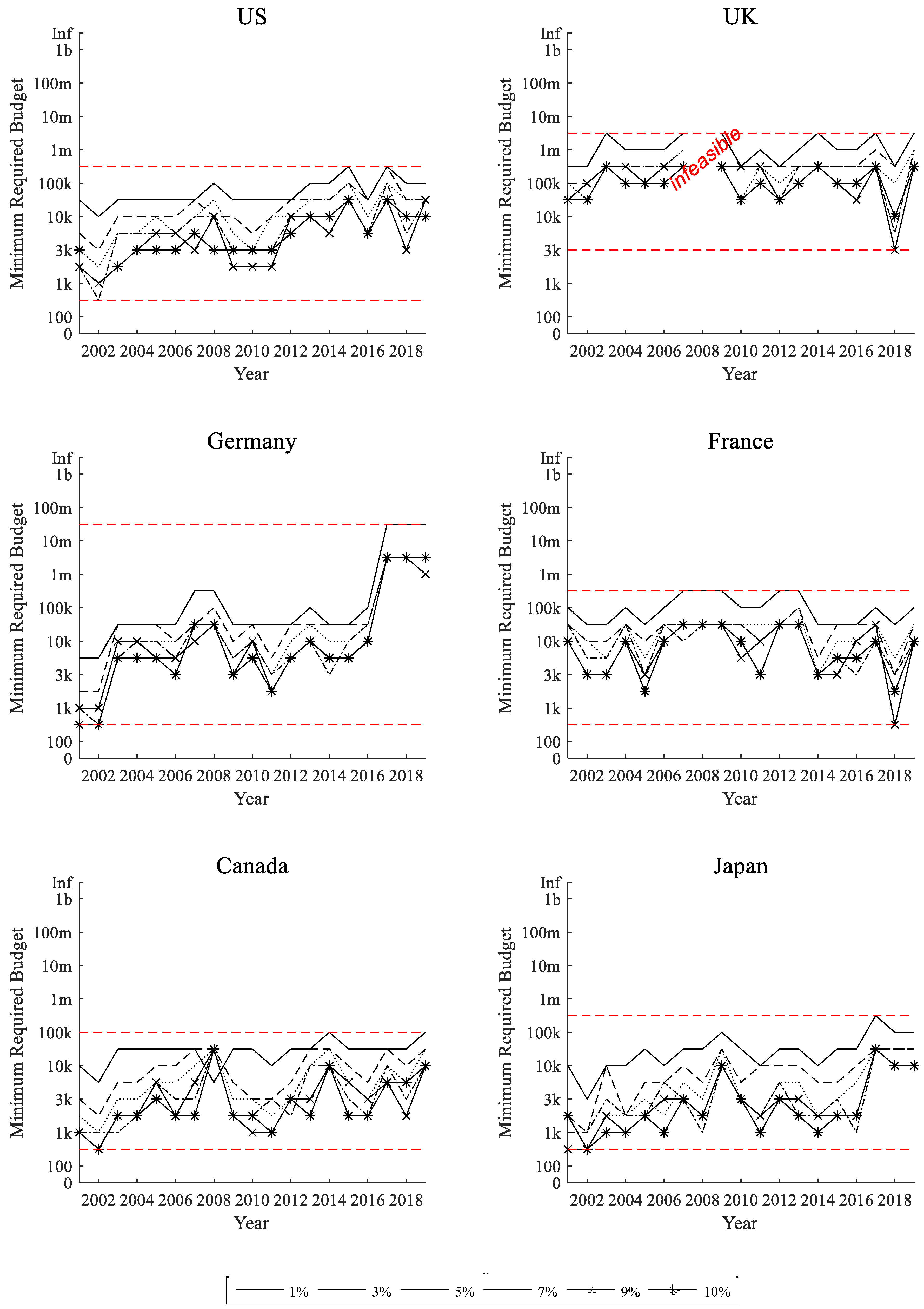

We note that the formulation given by (1) is a mixed-integer quadratic programming problem, which is a complex problem for finding the global optimum, and CPLEX solver is used for optimization. As the variance of budgeted portfolios gradually decreases towards the variance of the mean-variance portfolio without budget constraints as presented in

Figure 1,

Figure 2,

Figure 3,

Figure 4,

Figure 5 and

Figure 6, this pattern shows that the CPLEX solver finds portfolios close to the optimal solution (see

Figure 2,

Figure 3,

Figure 4,

Figure 5 and

Figure 6).

4. Empirical Analysis on the Impact of Portfolio Size

The main objective of portfolio diversification is to diversify risk and hence reduce the overall risk of a portfolio. Therefore, we examine the risk of a portfolio as measured by the variance of returns. Furthermore, to see the impact of investment budget on portfolio risk, we solve the problem given by (1) repeatedly with various levels of minimum required expected annual returns,

and various levels of budget,

Here, the highest level of budget is classed as having an infinite budget and this problem becomes the same as solving the original mean-variance model without budget constraints. The classical Markowitz model allows fractional allocations and fractions become viable allocation amounts when multiplied by an infinitely large budget.

The analysis is based on the stock markets of six developed countries: US, UK, Germany, France, Canada, and Japan. For each country, we select 50 stocks each year with the largest market capitalizations at the beginning of the year among the constituents of the country’s most representative stock market index. Our focus on forming portfolios with the largest individual stocks reflects the general behavior of average investors of investing in familiar companies. We note that extending the candidate stocks will help with achieving risk diversification, especially with a small budget. This will be further discussed in

Section 5.

Table 1 lists the market indices that are used in our analysis. Weekly price data are retrieved from Datastream and all values are converted to US dollars for ease of comparison using weekly foreign exchange rates data (USD/GBP, USD/EUR, USD/JPY). The empirical analysis is performed on an annual basis from 2001 to 2019.

Figure 1,

Figure 2,

Figure 3,

Figure 4,

Figure 5 and

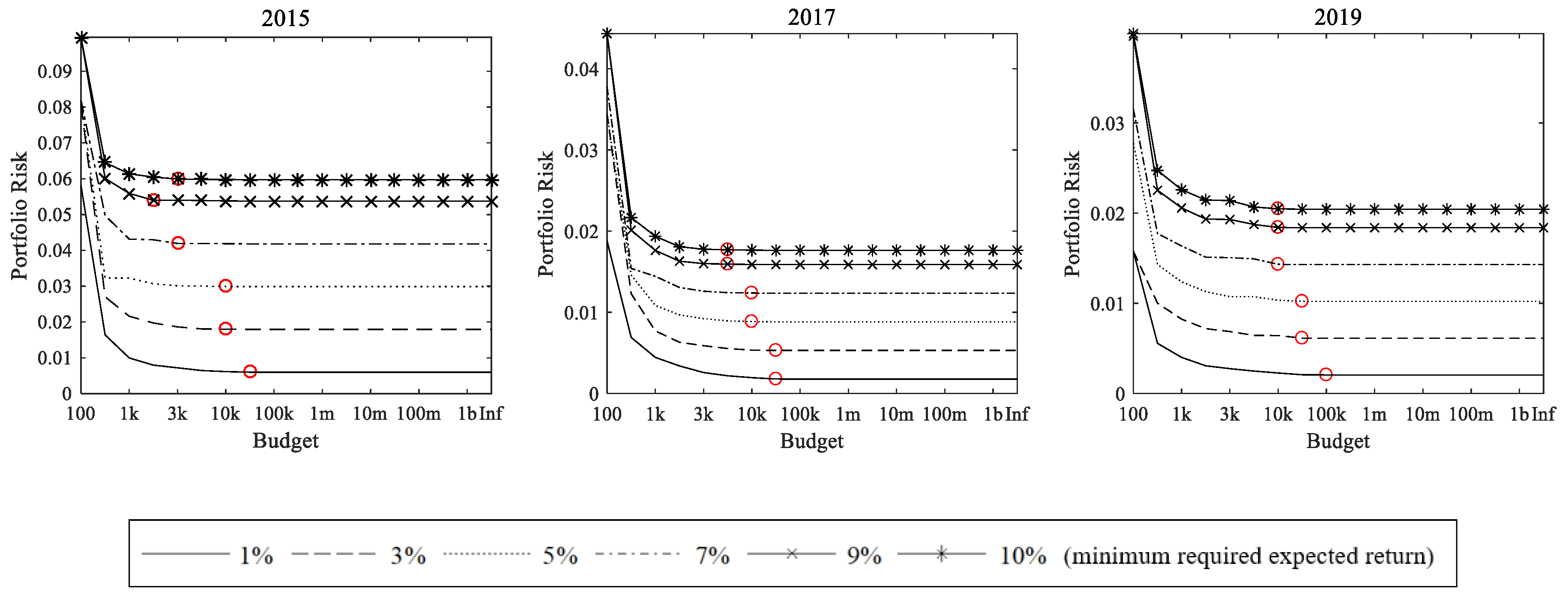

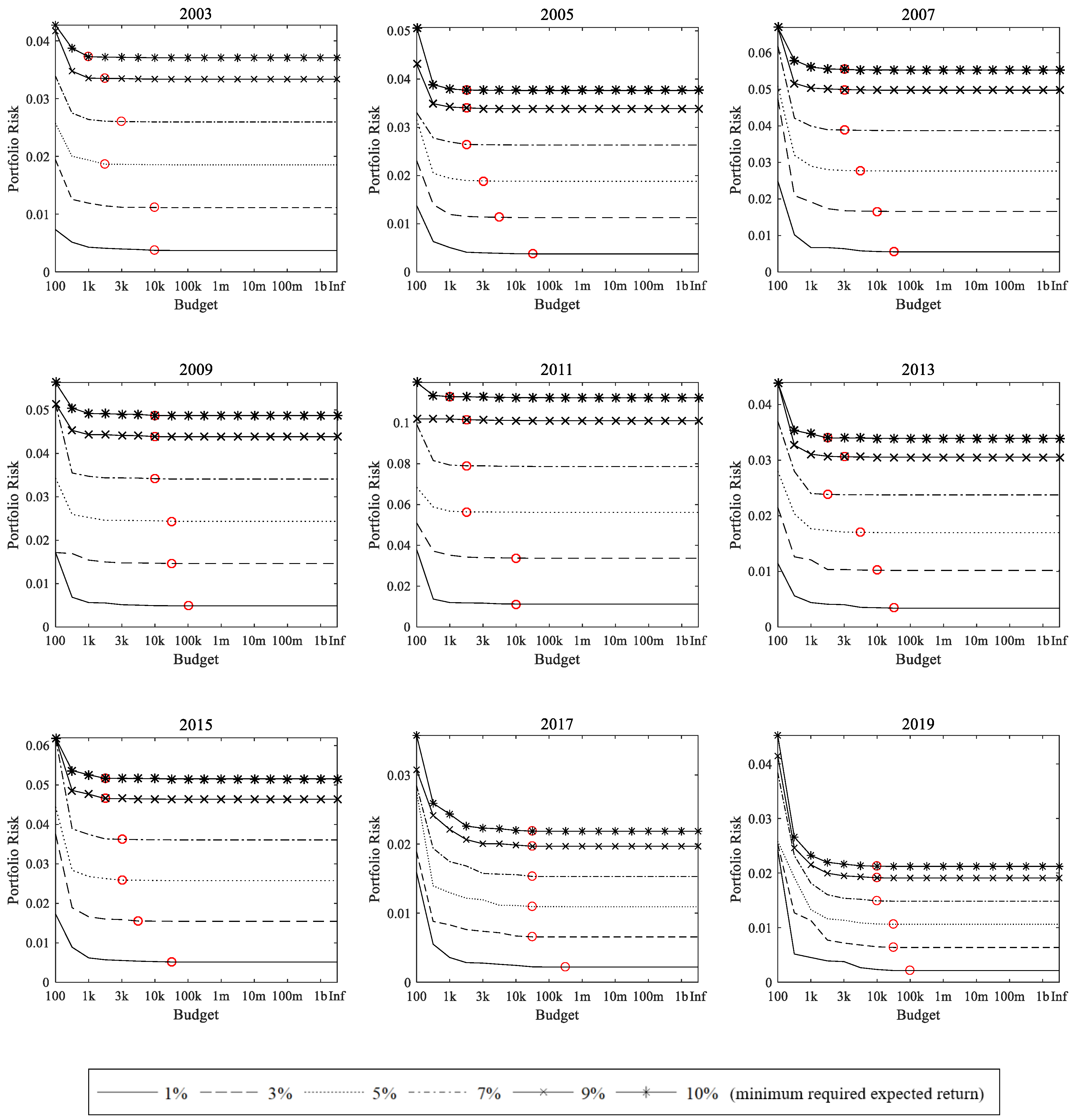

Figure 6 present our results on the standard deviation of portfolio returns that invest in stocks of the six countries, for various levels of budget. The minimum required budget necessary for constructing fully risk-diversified portfolios are marked with empty circles, where fully risk-diversified portfolios are classified as portfolios with less than one percent difference in portfolio variance, which is the objective value of the portfolio problem, compared to the optimal mean-variance portfolio without budget constraints. The optimal portfolio with no size constraint is the reference point because it is considered the maximally risk-diversified portfolio for a given level of required return. While results for odd years are only shown in these figures, findings for even years are similar to that of adjacent years, and a summary of the entire period is presented in

Figure 7 and

Figure 8. Achieving positive expected returns was impossible during 2008 in UK and these cases are denoted as “infeasible” in our results.

The results reveal three significant findings. First, it is very clear from

Figure 1,

Figure 2,

Figure 3,

Figure 4,

Figure 5 and

Figure 6 that having a larger portfolio does not help in reducing risk through diversification after a certain point. This is clearly evident in all six countries. Additionally, it is interesting to note that more money is necessary for constructing fully risk-diversified portfolios when the required return is smaller. This is likely because the optimization problems are tightly constrained when the required returns are large so that these problems do not have much opportunity to explore different solutions to reduce risk through diversification. On the other hand, less constrained problems are able to consider more candidates to reduce risk because they do not have to match large returns.

Second, it is possible for an average investor to form fully risk-diversified portfolios. The minimum required budgets for achieving full risk diversification with different minimum required returns are summarized in

Figure 7. Diversification is most expensive in the United Kingdom where a balance above

$50,000 is necessary to achieve full risk diversification. However, in the United States, Germany, and France, fully risk-diversified portfolios can be constructed with

$2000 to

$500,000, and only

$1000 to

$100,000 in Canada and Japan. While results are dependent on the minimum required return and the country, almost all risk reduction is achieved with a portfolio size between

$10,000 and

$100,000.

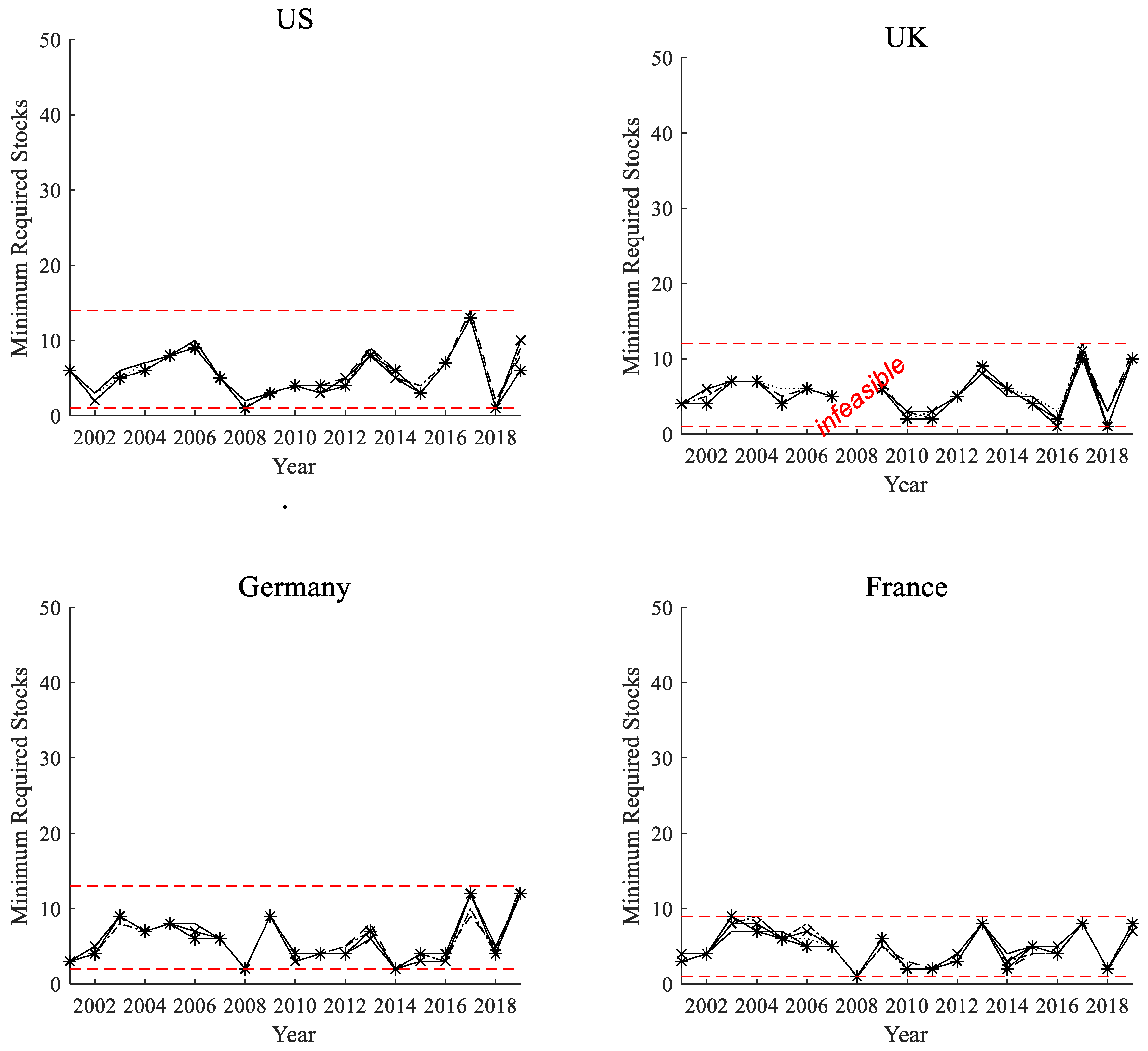

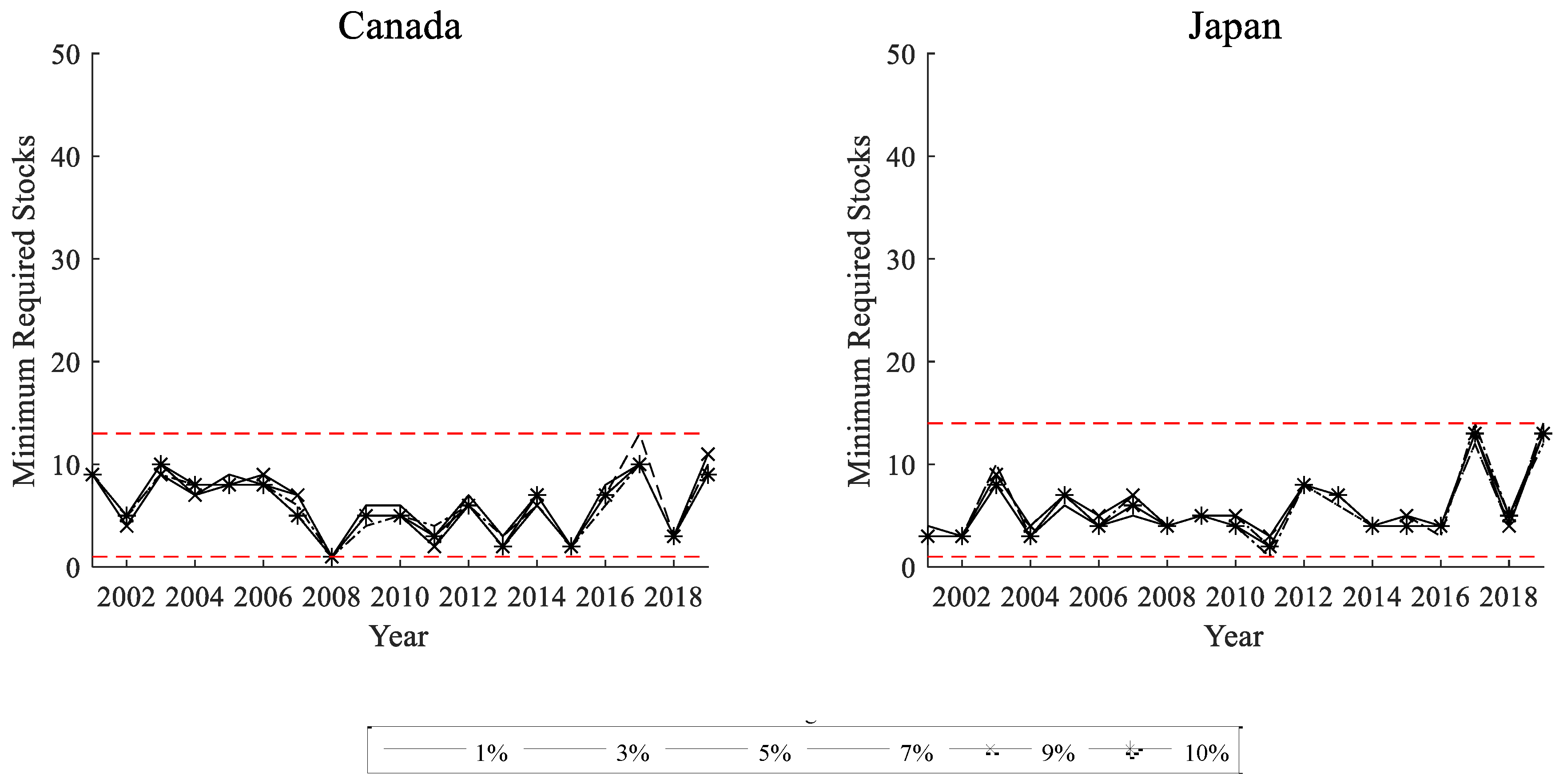

Third, individual investors can achieve diversification benefits by investing in only a small number of stocks. In order to further validate the practicality of managing a small portfolio, we compare the number of securities that form optimal portfolios for various portfolio sizes.

Figure 8, which shows the number of candidate assets in optimal portfolios at different levels of budget, exhibits that the required number of individual stocks in an optimal portfolio each year varies between one and 16. Although there appears to be some variability, the overall number of candidate assets required for forming a diversified portfolio is confirmed to be relatively small.

5. Further Discussion

5.1. Discussion on Required Budget

As presented in

Section 4, our results show that it is possible to explore full risk diversification with as low as

$1000 or

$2000 in some cases. Even though other cases require a larger budget, it will be easier to achieve larger diversification effects with a low budget in practice. The analysis in this study uses the largest 50 stocks in each market for forming risk-diversified portfolios. Since the problem restricts the choice of assets to only 50 stocks, it will be much more advantageous to consider more stocks especially under a tight budget because stocks trading at high price are out of reach. For example, an individual with a

$1000 budget cannot purchase stocks trading above

$1000 (e.g., Amazon, WA, USA) and can only purchase three shares of stocks trading around

$300 (e.g., Apple, CA, USA). Moreover, firms with large market capitalization tend to trade at a relatively higher price (e.g., five largest firms in the US all trade at above

$100), and thus, our test settings make it more difficult to achieve diversification. Nonetheless, the choice of using the largest 50 stocks is a reasonable representation of individual behavior because most individuals invest in companies they are familiar with [

31,

32].

In

Section 4, the necessary budget for achieving full risk diversification was measured with a threshold of at most 1% difference in portfolio variance with the no-budget optimal portfolio. As shown in panel B of

Table 2, if the threshold is increased to 5% or 10%, the required budget decreases and most cases achieves diversification with less than

$10,000. More importantly, optimal portfolios with thresholds of 5% or 10% show a trivial increase in portfolio risk. Panel A of

Table 2 shows that a 5% threshold results in less than a 1% point increase in portfolio risk, which is not a noteworthy rise that can be discarded even by investment managers. Thus, well-diversified portfolios can be formed with a smaller budget than our results in

Section 4 with a slightly relaxed threshold on complete risk diversification.

According to the 2013 Survey of Consumer Finances (SCF) reported by the Federal Reserve, a typical U.S. household in 2013 held

$294,300 in stocks, with the median being

$27,000 (see Bricker et al. [

33] for details on the 2013 SCF). Therefore, it will be possible for an average investor to construct a well-diversified portfolio (if not a fully risk-diversified one), by forming optimal mean-variance portfolios. Finally, the effect of transaction cost will be minimal in our case because the number of assets in a portfolio is small and frequent rebalancing is not necessary.

5.2. Discussion on Investing in Stocks

As mentioned in the introduction, the low financial sustainability addressed in this study includes both low financial wealth and lack of financial literacy. For these individuals, managing risk through efficient diversification is critical but challenging. Receiving professional wealth management service is out of reach due to limited wealth, and exploiting advanced investment models is overwhelming due to limited experience in financial management. Thus, investment in funds is often advised. While investment in funds is indeed a good guideline in general, funds also present concerns. The after-fee efficiency of funds is sometimes questioned [

3], and the consistent skill of funds is debatable [

34,

35,

36]. More importantly, finding the ideal fund or a group of funds is just as complex as forming a portfolio of stocks, especially when the candidate funds include actively managed funds.

Therefore, average individuals have largely two possible options. The first approach is passive investment in index funds or exchange-traded funds (ETFs), which provides exposure to overall market movements with relatively low fees. The second option is to invest in a number of familiar stocks so that the investor has enough information on the chosen stocks and also has the opportunity to achieve diversification by investing in several stocks.

As for the first approach, we note that it is also possible to form a portfolio of passive funds. However, the flexibility in choosing individual stocks provides more efficiency in diversifying risk for investments with specific levels of target return. In

Table 3, we demonstrate risk levels of portfolios composed of S&P 500 index and US Treasury bond ETFs with the same target returns from our analyses in

Section 4. Here, data for iShares from Datastream are used, which is one of the most popular families of ETFs. The two instruments are iShares Core S&P 500 ETF and iShares Short Treasury Bond ETF.

The annualized mean and standard deviation of returns are presented along with the risk levels of portfolios with infinite budget for the years between 2008 to 2019. From these results, indices are shown to have reasonable levels of risk due to their diversified exposure in the market. Nonetheless, it is generally possible to form more efficient portfolios by optimizing stock selection even with a small budget as we have summarized in

Figure 1. In

Table 3, infeasibility in achieving target returns are left blank such as the case for 2008 when the mean return for S&P 500 was negative. Even though the efficiency of portfolios in individual stocks is observed for in-sample comparisons, it provides insight into achieving risk diversification and supports the contribution of analyzing diversification through investment in stocks for average individuals.

In summary, investment in funds is recommended for individuals with limited financial wealth or financial literacy. However, selecting a fund with strong after-fee performance requires experience and skill. More importantly, forming portfolios of index-based funds with specific levels of return or risk is challenging. As the main objective of this study is to analyze the risk diversification levels for various target return levels, the focus is on the second approach by investigating the possibility of achieving risk diversification through investment in a small number of individual stocks.

6. Conclusions

We discuss the viability of small account diversification for individual investors with a relatively smaller level of wealth than investors—often classified as high-net-worth individuals. In order to reflect on the more practical situation for small investors, we focus on the amount of investment for examining diversification benefits, instead of the popular choice of using the number of securities in a portfolio. Furthermore, we analyze optimal mean-variance portfolios, rather than evaluating random portfolios to compute the average portfolio risk, where the optimal allocation is computed in terms of the number of shares to incorporate the price of assets.

Our results demonstrate that it is possible for individuals with low financial sustainability to invest in well-diversified portfolios, if not fully risk-diversified ones. We find in the stock markets of six countries that an investment amount around $10,000–100,000 is enough for constructing fully risk-diversified portfolios, which suggests that a substantial investment is not necessary for gaining complete diversification benefits. We also find that it is possible to form well-diversified portfolios with less than $10,000, which is much less than the average amount invested in stocks in the U.S., according to the Federal Reserve. Even with the use of a restricted set of assets and a tight limit on diversification, our findings show that forming a well-diversified portfolio within the mean-variance framework is achievable for average individuals.

Finally, since the proposed quantity-based portfolio formulation with a budget constraint can be applied to any set of candidate assets, it can be used to form and analyze portfolios in certain sectors or industries. This may provide further details on how average individual investors can achieve risk diversification.

Author Contributions

Conceptualization: Y.L., W.C.K. and J.H.K.; Methodology: Y.L., W.C.K. and J.H.K.; Writing—original draft: Y.L., W.C.K. and J.H.K.; Writing—review & editing: Y.L. and J.H.K. All authors have read and agreed to the published version of the manuscript

Funding

This research was supported by Basic Science Research Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Science, ICT & Future Planning (NRF-2018R1C1B6004271) and the New Faculty Fund (1.180089.01) of UNIST (Ulsan National Institute of Science and Technology).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fehr, H.; Kallweit, M.; Kindermann, F. Pension reform with variable retirement age: A simulation analysis for Germany. J. Pension Econ. Financ. 2012, 11, 389–417. [Google Scholar] [CrossRef]

- Wang, H.; Huang, J.; Yang, Q. Assessing the Financial Sustainability of the Pension Plan in China: The Role of Fertility Policy Adjustment and Retirement Delay. Sustainability 2019, 11, 883. [Google Scholar] [CrossRef]

- Lee, Y.; Kwon, D.-G.; Kim, W.C.; Fabozzi, F.J. An alternative approach for portfolio performance evaluation: Enabling fund evaluation relative to peer group via Malkiel’s monkey. Appl. Econ. 2018, 50, 4318–4327. [Google Scholar] [CrossRef]

- Fowler, G.B.; De Vassal, V. Holistic Asset Allocation for Private Individuals. J. Wealth Manag. 2006, 9, 18–30. [Google Scholar] [CrossRef]

- Kolm, P.N.; Tütüncü, R.; Fabozzi, F.J. 60 Years of portfolio optimization: Practical challenges and current trends. Eur. J. Oper. Res. 2014, 234, 356–371. [Google Scholar] [CrossRef]

- Beketov, M.; Lehmann, K.; Wittke, M. Robo Advisors: Quantitative methods inside the robots. J. Asset Manag. 2018, 19, 363–370. [Google Scholar] [CrossRef]

- Markowitz, H.M. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Markowitz, H.M. The Early History of Portfolio Theory: 1600–1960. Financ. Anal. J. 1999, 55, 5–16. [Google Scholar] [CrossRef]

- Fabozzi, F.J.; Gupta, F.; Markowitz, H.M. The Legacy of Modern Portfolio Theory. J. Invest. 2002, 11, 7–22. [Google Scholar] [CrossRef]

- Konno, H.; Yamazaki, H. Mean-Absolute Deviation Portfolio Optimization Model and Its Applications to Tokyo Stock Market. Manag. Sci. 1991, 37, 519–531. [Google Scholar] [CrossRef]

- Konno, H.; Koshizuka, T. Mean-absolute deviation model. IIE Trans. 2005, 37, 893–900. [Google Scholar] [CrossRef]

- Rockafellar, R.T.; Uryasev, S. Optimization of conditional value-at-risk. J. Risk 2000, 2, 21–41. [Google Scholar] [CrossRef]

- Jorion, P. Portfolio Optimization with Tracking-Error Constraints. Financ. Anal. J. 2003, 59, 70–82. [Google Scholar] [CrossRef]

- Brodie, J.; Daubechies, I.; De Mol, C.; Giannone, D.; Loris, I. Sparse and stable Markowitz portfolios. Proc. Natl. Acad. Sci. USA 2009, 106, 12267–12272. [Google Scholar] [CrossRef]

- Fabozzi, F.J.; Kolm, P.N.; Pachamanova, D.A.; Focardi, S.M. Robust Portfolio Optimization and Management; John Wiley & Sons: New York, NY, USA, 2007. [Google Scholar]

- French, K.; Poterba, J. Investor Diversification and International Equity Markets. JSTOR 1991, 81, 222–226. [Google Scholar] [CrossRef]

- Coval, J.D.; Moskowitz, T.J. Home Bias at Home: Local Equity Preference in Domestic Portfolios. J. Finance 1999, 54, 2045–2073. [Google Scholar] [CrossRef]

- Grinblatt, M.; Keloharju, M.M. How Distance, Language, and Culture Influence Stockholdings and Trades. J. Financ. 2001, 56, 1053–1073. [Google Scholar] [CrossRef]

- Ivković, Z.; Weisbenner, S. Local Does as Local Is: Information Content of the Geography of Individual Investors’ Common Stock Investments. J. Financ. 2005, 60, 267–306. [Google Scholar] [CrossRef]

- Goetzmann, W.N.; Kumar, A. Equity Portfolio Diversification. Rev. Financ. 2008, 12, 433–463. [Google Scholar] [CrossRef]

- Polkovnichenko, V. Household Portfolio Diversification: A Case for Rank-Dependent Preferences. Rev. Financ. Stud. 2005, 18, 1467–1502. [Google Scholar] [CrossRef]

- Evans, J.L.; Archer, S.H. Diversification and the reduction of dispersion: An empirical analysis. J. Financ. 1968, 23, 761–767. [Google Scholar]

- Fisher, L.; Lorie, J.H. Some Studies of Variability of Returns on Investments in Common Stocks. J. Bus. 1970, 43, 99. [Google Scholar] [CrossRef]

- Elton, E.J.; Gruber, M.J. Risk Reduction and Portfolio Size: An Analytical Solution. J. Bus. 1977, 50, 415. [Google Scholar] [CrossRef]

- Statman, M. How Many Stocks Make a Diversified Portfolio? J. Financ. Quant. Anal. 1987, 22, 353. [Google Scholar] [CrossRef]

- Statman, M. The Diversification Puzzle. Financ. Anal. J. 2004, 60, 44–53. [Google Scholar] [CrossRef]

- Chong, J.; Phillips, G.M. Portfolio Size Revisited. J. Wealth Manag. 2013, 15, 49–60. [Google Scholar] [CrossRef]

- Li, Z.; Li, X.; Hui, Y.; Wong, W.-K. Maslow Portfolio Selection for Individuals with Low Financial Sustainability. Sustainability 2018, 10, 1128. [Google Scholar] [CrossRef]

- Chhabra, A.B. Beyond Markowitz: A comprehensive wealth allocation framework for individual investors. J. Wealth Manag. 2005, 7, 8–34. [Google Scholar] [CrossRef]

- Ahn, W.; Lee, H.S.; Ryou, H.; Oh, K.J. Asset Allocation Model for a Robo-Advisor Using the Financial Market Instability Index and Genetic Algorithms. Sustainability 2020, 12, 849. [Google Scholar] [CrossRef]

- Brown, J.R.; Ivković, Z.; Smith, P.A.; Weisbenner, S. Neighbors Matter: Causal Community Effects and Stock Market Participation. J. Financ. 2008, 63, 1509–1531. [Google Scholar] [CrossRef]

- Engelberg, J.E.; Parsons, C.A. The Causal Impact of Media in Financial Markets. J. Financ. 2011, 66, 67–97. [Google Scholar] [CrossRef]

- Bricker, J.; Dettling, L.J.; Henriques, A.; Hsu, J.W.; Moore, K.B.; Sabelhaus, J.; Thompson, J.; Windle, R.A. Changes in U.S. family finances from 2010 to 2013: Evidences from the survey of consumer finances. Fed. Res. Bull. 2014, 100, 1–41. [Google Scholar]

- Barras, L.; Scaillet, O.; Wermers, R. False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas. J. Financ. 2010, 65, 179–216. [Google Scholar] [CrossRef]

- Cuthbertson, K.; Nitzsche, D.; O’Sullivan, N. UK mutual fund performance: Skill or luck? J. Empir. Financ. 2008, 15, 613–634. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Luck versus Skill in the Cross-Section of Mutual Fund Returns. J. Financ. 2010, 65, 1915–1947. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}