Approaching Monetary Integration in the Context of the Imperative to Ensure the Sustainable Growth in the EU

Abstract

1. Introduction

- What are the factors through which European monetary integration influences economic growth?

- Which of these factors have a greater impact on economic growth?

- What is the (positive or negative) impact of European bank integration on growth?

2. Theoretical Background

2.1. Monetary Integration and Monetary Policy

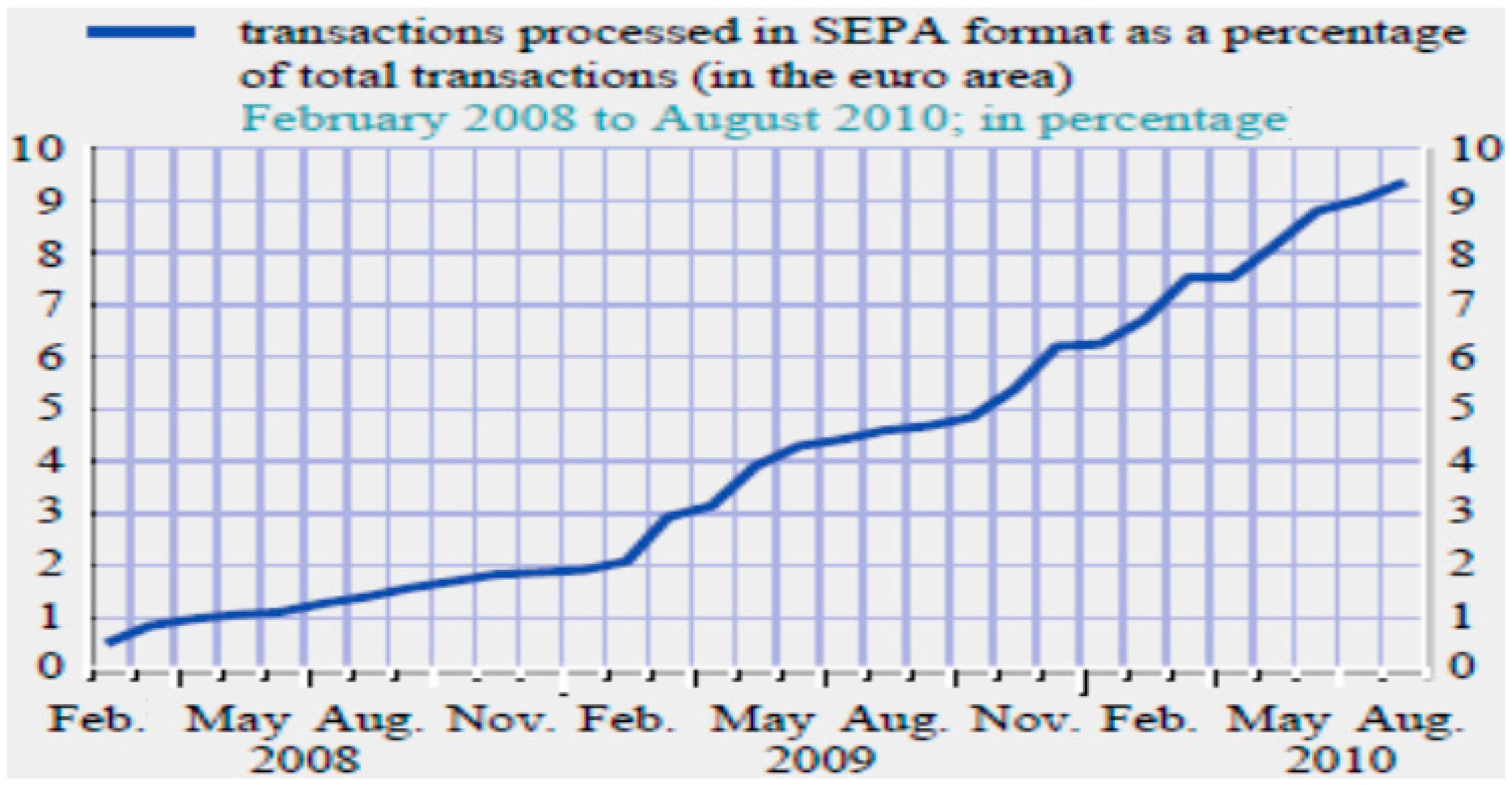

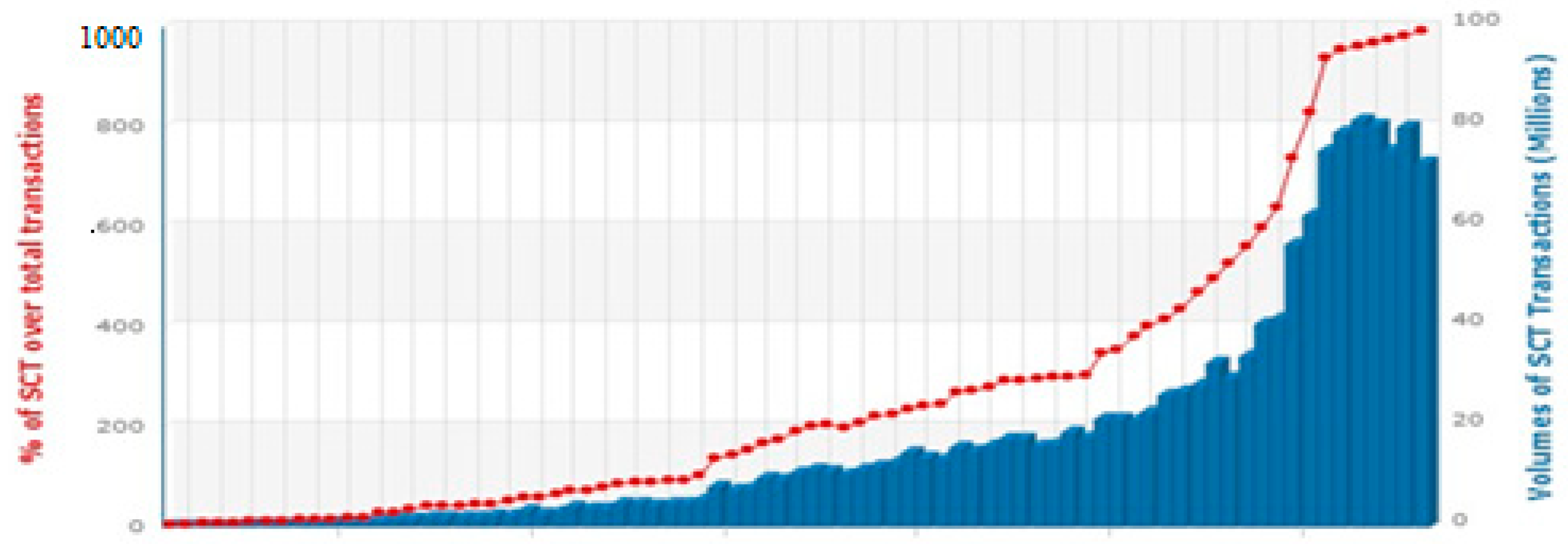

2.2. Cross-Border Payments

3. Data and Methodology

4. Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Cham, T. Does monetary integration lead to an increase in FDI flows? An empirical investigation from the West African Monetary Zone (WAMZ). BorsaIstanb. Rev. 2016, 16, 9–20. [Google Scholar] [CrossRef]

- Todorov, I. The Monetary Integration of the New Member States before the Euro Area Debt Crisis. Manag. Glob. Transit. 2013, 11, 375–390. [Google Scholar]

- Smitha, T.H. Impact of Monetary Policy on Indian Economy in the Post-Reform Period. Ph.D. Thesis, Department of Applied Economics, Cochin University of Science and Technology, Kochi, India, 2010. Available online: https://dyuthi.cusat.ac.in/jspui/bitstream/purl/2159/3/Dyuthi-T0517.pdf (accessed on 25 July 2020).

- Auray, S.; Eyquem, A.; Poutineau, J.-C. The welfare gains of trade integration in the european monetary union. Macroecon. Dyn. 2010, 14, 645–676. [Google Scholar] [CrossRef][Green Version]

- Chen, M.; Wu, J.; Jeon, B.N.; Wang, R. Monetary policy and bank risk-taking: Evidence from emerging economies. Emerg. Mark. Rev. 2017, 31, 116–140. [Google Scholar] [CrossRef]

- Artis, M.; Zhang, W. International Business Cycles and the ERM: Is There a European Business Cycle? Int. J. Financ. Econ. 1997, 2, 1–16. [Google Scholar] [CrossRef]

- Artis, M. Should the UK Join Emu? Natl. Inst. Econ. Rev. 2000, 171, 70–81. [Google Scholar] [CrossRef]

- Micossi, S. The Monetary Policy of the European Central Bank (2002–2015); Centre for European Policy Studies: Manchester, UK, 2015. [Google Scholar]

- Uxo, J. Is the end of fiscal austerity feasible in Spain? An alternative plan to the current Stability Programme (2015–2018). Camb. J. Econ. 2017, 41, 999–1020. [Google Scholar] [CrossRef]

- Altavilla, C.; Pagano, M.; Simonelli, S. Bank Exposures and Sovereign Stress Transmission. Rev. Financ. 2017, 21, 2103–2139. [Google Scholar] [CrossRef]

- Wyplosz, C. The Eurozone Crisis: A Near-Perfect Case of Mismanagement. Available online: https://link.springer.com/chapter/10.1007/978-3-319-63706-8_2 (accessed on 27 August 2020).

- De Grauwe, P. Economics of the Monetary Union, 13th ed.; Oxford University Press: New York, NY, USA, 2020. [Google Scholar]

- Tomann, H. Monetary Integration in Europe; Springer Science and Business Media: Berlin, Germany, 2017. [Google Scholar]

- Kalemli-Ozcan, S.; Manganelli, S.; Papaioannou, E.; Peydro, J.S. Financial Integration and Risk Sharing: The Role of the Monetary Union. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.492.3198&rep=rep1&type=pdf (accessed on 23 July 2020).

- Kalemli-Ozcan, S.; Papaioannou, E.; Peydró, J.-L. What Lies Beneath the Euro’s Effect on Financial Integration: Currency Risk, Legal Harmonization, or Trade? J. Int. Econ. 2010, 81, 75–88. [Google Scholar] [CrossRef]

- European Central Bank. The Single Euro Payments Area (SEPA)—An Integrated Retail Payment Market. Available online: https://www.ecb.europa.eu/pub/pdf/other/sepa_brochure_2009en.pdf (accessed on 21 July 2020).

- European Central Bank. Single Euro Payments Area—Seventh Progress Report beyond Theory and Practice. Available online: https://www.ecb.europa.eu/pub/pdf/other/singleeuropaymentsarea201010en.pdf19 (accessed on 22 July 2020).

- European Central Bank. Euro Area Markets for Banks’ Long-Term Debt Financing Instruments: Recent Developments, State of Integration and Implications for Monetary Policy Transmission. Available online: https://www.ecb.europa.eu/pub/pdf/other/art2_mb201111en_pp73-90en.pdf (accessed on 22 July 2020).

- Todorović, V.; Sedlarevic, L.; Tomic, N.; Violeta, T.; Lazar, S.; Nenad, T. Impact of the single euro payment area on performance of banking sector. Industrija 2017, 45, 23–44. [Google Scholar] [CrossRef]

- Mare, C.; Litan, C. Perspectives on Euro introduction in the Romanian economy. Balt. J. Econ. 2012, 12, 23–40. [Google Scholar] [CrossRef]

- Barrel, R.; Gottschalk, S.; Holland, D.; Khoman, E.; Liadze, I.; Pomerantz, O. The Impact of EMU on Growth and Unemployment. Eur. Com. Econ. Pap. 2008, 318, 35. [Google Scholar]

- Mongelli, F.P. European Economic and Monetary Integration, and the Optimum Currency Area Theory. Eur. Com. Econ. Pap. 2008, 302, 44. [Google Scholar]

- Bagnai, A.; Ospina, C.A.M. Monetary integration vs. real disintegration: Single currency and productivity divergence in the euro area. J. Econ. Policy Reform 2017, 21, 353–367. [Google Scholar] [CrossRef]

- Nchake, M.A.; Edwards, L.; Rankin, N. Closer monetary union and product market integration in emerging economies: Evidence from the Common Monetary Area in Southern Africa. Int. Rev. Econ. Financ. 2018, 54, 154–164. [Google Scholar] [CrossRef]

- Quah, C.-H.; Crowley, P.M. Monetary Integration in East Asia: A Hierarchical Clustering Approach. Int. Financ. 2010, 13, 283–309. [Google Scholar] [CrossRef]

- Walti, S. Stock Market Synchronization and Monetary Integration. A Publication of the National Centre of Competence in Research (NCCR) Supported by the Swiss National Science Foundation. NCCR. 2006. Available online: https://www.tcd.ie/Economics/staff/waltis/papers/eurofin.pdf (accessed on 23 July 2020).

- Almunia, J. Monetary and Economic Integration—The EU Experience. European Commissioner for Economic and Monetary Affairs. 2006. Speech 06(529). Available online: https://ec.europa.eu/commission/presscorner/detail/en/SPEECH_06_529 (accessed on 20 July 2020).

- Kenen, P.B.; Meade, E.E. Monetary Integration in East Asia. Available online: https://www.frbsf.org/economic-research/files/Kenen.pdf (accessed on 23 July 2020).

- Saqib, N.; Aggarwal, P. Impact of Fiscal and Monetary Policyon Economic Growth in an Emerging Economy. Int. J. Appl. Bus. Econ. Res. 2017, 15, 457–462. [Google Scholar]

- Candelon, B.; Muysken, J.; Vermeulen, R. Fiscal policy and monetary integration in Europe: An update. Oxf. Econ. Pap. 2009, 62, 323–349. [Google Scholar] [CrossRef]

- Ramos, S.C. A Structural Analysis of the European Monetary Union and its Effect on Greece in Light of the European Financial Crisis. Master’s Thesis, Claremont McKenna College, Claremont, CA, USA, 2011. Available online: https://scholarship.claremont.edu/cmc_theses/239 (accessed on 23 July 2020).

- Barro, R.J. Economic Growth; MIT Press Cambridge: Cambridge, MA, USA, 2004. [Google Scholar]

- Campos, N.F.; Macchiarelli, C. Symmetry and Convergence in Monetary Unions. Available online: https://www.lse.ac.uk/european-institute/Assets/Documents/LEQS-Discussion-Papers/LEQSPaper131.pdf (accessed on 27 August 2020).

- Ioannatos, P.E. Has the Euro Promoted Eurozone’s Growth? J. Econ. Integr. 2018, 33, 1388–1411. [Google Scholar] [CrossRef]

- Schmiedel, H. The Economic Impact of the Single Euro. ECB Occasional 2007. Paper Series No. 71. Available online: https://www.ecb.europa.eu//pub/pdf/scpops/ecbocp71.pdf (accessed on 22 July 2020).

- Dingela, S.; Khobai, H. Dynamic Impact of Money Supply on Economic Growth in South Africa. In An ARDL Approach; MPRA Paper: Munchen, Germany, 2017. [Google Scholar]

- Shafiei, E. International Trade and Its Impact on Economic Growth. Available online: http://www.ijirset.com/upload/2014/march/52_Effect.pdf (accessed on 23 July 2020).

- Ivanović, V.; Stanišić, N. Monetary freedom and economic growth in New European Union Member States. Econ. Res. Ekon. Istraživanja 2017, 30, 453–463. [Google Scholar] [CrossRef]

- Bukowski, S.I. The Maastricht Convergence Criteria and Economic Growth in the EMU. Available online: http://www.ec.unipg.it/DEFS/uploads/quad24.pdf (accessed on 25 July 2020).

- Del Hoyo, J.L.D.; Dorrucci, E.; Heinz, F.F.; Muzikarova, S. Real convergence in the euro area: A long-term perspective. Available online: https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op203.en.pdf (accessed on 22 July 2020).

- Drastichová, M. The relations of real and nominal convergence in the EU with impacts on the euro area participation. Ekon. Rev. Cent. Eur. Rev. Econ. Issues 2012, 15, 107–122. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Benefits (According to the Openness of the Economy) | Costs |

|---|---|

| The reduction of transaction costs | Inflation and seigniorage tax aren’t available for the national governments |

| The markets are more transparent (indirect influence) | The abandonment of the exchange rate policy needed for balance the intra-union asymmetrical shocks |

| The reduction of price discrimination | According to the wage and price rigidity, the countries are “different” |

| The decrese of monetary investment risks | |

| Growth effects |

| Variables | Obs. | Average | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| TFP | 392 | 1.08 | 0.50 | 0.2 | 4.85 |

| MS | 391 | 4.23 | 0.63 | 2.21 | 5.98 |

| TRADE | 392 | 4.66 | 0.46 | 3.86 | 5.94 |

| MONFR | 392 | 81.03 | 4.17 | 67 | 90.1 |

| UNEM | 392 | 8.94 | 4.22 | 3.7 | 24.9 |

| BDEF | 392 | −2.67 | 3.35 | −13.8 | 5 |

| PSP | 392 | 44.60 | 7.17 | 17.07 | 58.1 |

| GRS | 391 | 21.75 | 5.70 | 7.98 | 36.73 |

| CONCPI | 392 | 0.74 | 0.80 | 0.01 | 4.68 |

| CONEXR | 392 | 10.98 | 25.51 | 1.45 | 157.03 |

| CONINT | 392 | 0.89 | 0.88 | 0.02 | 5.40 |

| GDP | 392 | 9.89 | 0.68 | 8.16 | 11.39 |

| SCT | 383 | 20.35 | 2.99 | 10.89 | 27.85 |

| SDD | 383 | 16.46 | 3.14 | 7.52 | 23.01 |

| SC | 383 | 16.30 | 2.87 | 8.96 | 21.70 |

| CRHO | 385 | 9.46 | 2.34 | 3.33 | 13.24 |

| Independent Variables | Dependent Variable-GDP | Dependent Variable-TFP | ||||||

|---|---|---|---|---|---|---|---|---|

| OLS with Years Dummy | Fixed Effects | OLS with Years Dummy | Fixed Effects | |||||

| Country FE; Year FE; Year FE (2) | Country FE; Year FE; Year FE (2) | |||||||

| CONCPI | 0.07 ** | 0.035 *** | 0.01 ** | 0.02 *** | 0.02 | 0.04 * | 0.04 | 0.02 * |

| (0.02) | (0.007) | (0.006) | (0.006) | (0.03) | (0.04) | (0.04) | (0.04) | |

| CONEXR | 0.005 *** | 0.0001 | 0.006 *** | 0.003 * | 0.001 * | 0.004 | 0.002 * | 0.001 *** |

| (0.001) | (0.002) | (0.001) | (0.001) | (0.001) | (0.01) | (0.01) | (0.01) | |

| SCT | 0.05 *** | 0.009 * | 0.003 | 0.001 | 0.005 | 0.04 | 0.04 * | 0.04 |

| (0.009) | (0.005) | (0.003) | (0.003) | (0.01) | (0.02) | (0.02) | (0.02) | |

| SDD | 0.05 *** | −0.002 | 0.0006 | 0.001 | 0.009 | 0.03 * | 0.03 * | 0.04 |

| (0.009) | (0.002) | (0.002) | (0.002) | (0.01) | (0.01) | (0.01) | (0.02) | |

| SC | 0.01 ** | 0.07 *** | 0.02 *** | 0.01 *** | 0.001 | 0.06 * | 0.04 | 0.05 * |

| (0.009) | (0.008) | (0.007) | (0.006) | (0.01) | (0.04) | (0.04) | (0.05) | |

| MS | 0.15 *** | 0.01 * | 0.02 ** | 0.02 ** | 0.05 | 0.02 *** | 0.05 | 0.16 * |

| (0.03) | (0.01) | (0.01) | (0.01) | (0.04) | (0.06) | (0.06) | (0.09) | |

| TRADE | 0.46 *** | 0.66 *** | 0.03 | 0.16 ** | 0.15 ** | 0.96 *** | 0.78 * | 0.72 |

| (0.05) | (0.06) | (0.07) | (0.06) | (0.07) | (0.32) | (0.47) | (0.53) | |

| MONFR | 0.02 *** | 0.002 * | 0.001 | 0.002 * | 0.02 *** | 0.03 *** | 0.03 *** | 0.02 *** |

| (0.006) | (0.001) | (0.001) | (0.001) | (0.008) | (0.008) | (0.009) | (0.01) | |

| UNEM | −0.03 *** | −0.02 *** | −0.01 *** | −0.017 *** | −0.01 ** | −0.03 *** | −0.03 *** | −0.02 ** |

| (0.006) | (0.002) | (0.001) | (0.001) | (0.006) | (0.1);(0.01);(0.01);(0.01) | |||

| CONINT | 0.08 *** | 0.01 * | 0.006 ** | 0.015 *** | 0.072 ** | 0.12 *** | 0.014 *** | 0.05 *** |

| (0.02) | (0.007) | (0.006) | (0.005) | (0.03) | (0.04) | (0.04) | (0.04) | |

| BDEF | 0.0003 | −0.007 | −0.007 ** | −0.004 ** | −0.02 ** | −0.02 ** | −0.03 * | −0.03 * |

| (0.008) | (0.002) | (0.002) | (0.002) | (0.01) | (0.01) | (0.01) | (0.01) | |

| PSP | 0.02 *** | 0.006 *** | 0.0006 | 0.0007 | −0.01 *** | −0.01 | −0.01 ** | −0.006 |

| (0.003) | (0.001) | (0.001) | (0.001) | (0.004) | (0.009) | (0.009) | (0.01) | |

| GRS | 0.005 | 0.008 *** | 0.01 *** | 0.009 *** | 0.01 * | 0.01 | 0.01 | 0.03 *** |

| (0.004) | (0.001) | (0.001) | (0.001) | (0.005) | (0.009) | (0.009) | (0.01) | |

| CRHO | 0.10 *** | 0.007 | 0.016 *** | 0.019 *** | 0.04 ** | 0.06 * | 0.07 ** | 0.07 ** |

| (0.012) | (0.006) | (0.005) | (0.004) | (0.01) | (0.03) | (0.03) | (0.03) | |

| Cons | 2.94 *** | 5.52 *** | 9.38 *** | 9.12 *** | 0.59 *** | 6.18 *** | 4.2 *** | 3.71 *** |

| (0.66) | (0.32) | (0.37) | (0.33) | (0.85) | (1.66) | (1.40) | (1.76) | |

| R squared | 0.72 | 0.66 | 0.81 | 0.81 | 0.23 | 0.20 | 0.31 | 0.36 |

| F statistic | 33.65 *** | 46.93 *** | 52 *** | 50.89 *** | 3.97 *** | 5.06 ***.4.24 ***.4.30 ***.0.30 *** | ||

| Obs. | 392 | 392 | 392 | 365 | 392 | 392 | 392 | 365 |

| Independent Variables | Dependent Variable-GDP | Dependent Variable-TFP | ||||||

|---|---|---|---|---|---|---|---|---|

| OLS with Years Dummy | Fixed Effects | OLS with Years Dummy | Fixed Effects | |||||

| Country FE Year FE Year FE (2) | Country FE Year FE Year FE (2) | |||||||

| CONCPI | 0.014 | 0.0003 * | 0.02 ** | 0.015 ** | 0.03 | 0.12 ** | 0.14 ** | 0.04 |

| (0.024) | (0.009) | (0.009) | (0.007) | (0.04) | (0.05) | (0.06) | (0.07) | |

| CONEXR | 3.04 *** | 0.03 *** | 1.17 *** | 0.75 *** | 0.02 | 0.001 | 0.28 * | 1.65 *** |

| (1.00) | (0.008) | (0.31) | (0.26) | (1.04) | (0.04) | (0.24) | (0.50) | |

| SCT | 0.007 ** | 0.001 | 0.002 | 0.02 | 0.03 ** | 0.06 ** | 0.06 ** | 0.06 * |

| (0.01) | (0.005) | (0.004) | (0.003) | (0.01) | (0.02) | (0.02) | (0.03) | |

| SDD | 0.015 ** | 0.001 * | 0.003 | 0.02 ** | 0.01 | 0.05 ** | 0.05 ** | 0.05 * |

| (0.009) | (0.003) | (0.003) | (0.002) | (0.01) | (0.02) | (0.02) | (0.02) | |

| SC | 0.05 *** | 0.08 *** | 0.044 *** | 0.03 *** | 0.01 | 0.08 ** | 0.04 ** | 0.12 *** |

| (0.01) | (0.01) | (0.011) | (0.009) | (0.01) | (0.07) | (0.07) | (0.09) | |

| MS | 0.10 *** | 0.01 | 0.03 *** | 0.02 ** | 0.09 *** | 0.22 *** | 0.24 *** | 0.25 ** |

| (0.02) | (0.01) | (0.01) | (0.01) | (0.03) | (0.07) | (0.07) | (0.10) | |

| TRADE | 0.40 *** | 0.62 *** | 0.10 * | 0.27 *** | 0.07 | 0.83 ** | 0.47 * | 0.10 |

| (0.04) | (0.07) | (0.08) | (0.07) | (0.06) | (0.42) | (0.59) | (0.06) | |

| MONFR | 0.011 ** | 0.007 *** | 0.004 ** | 0.005 *** | 0.014 * | 0.01 | 0.02 | 0.01 |

| (0.006) | (0.002) | (0.001) | (0.001) | (0.008) | (0.01) | (0.01) | (0.01) | |

| UNEM | −0.03 *** | −0.02 *** | −0.019 *** | −0.01 *** | −0.009 *** | −0.02 ** | −0.1 ** | −0.01 ** |

| (0.005) | (0.002) | (0.001) | (0.001) | (0.007) | (0.01) | (0.01) | (0.01) | |

| CONINT | 0.002 * | 0.01 ** | 0.004 | 0.01 ** | 0.02 *** | 0.09 ** | 0.08 * | 0.05 ** |

| (0.01) | (0.007) | (0.003) | (0.005) | (0.02) | (0.04) | (0.04) | (0.03) | |

| BDEF | 0.006 * | −0.01 *** | −0.009 *** | −0.005 ** | −0.01 | −0.03 ** | −0.03 * | −0.03 |

| (0.007) | (0.002) | (0.002) | (0.002) | (0.01) | (0.01) | (0.01) | 0.02 | |

| PSP | 0.01 *** | 0.002 | −0.002 * | −0.001 | −0.009 * | −0.01 | −0.01 * | −0.01 |

| (0.003) | (0.001) | (0.001) | (0.001) | (0.004) | (0.01) | (0.01) | (0.01) | |

| GRS | 0.010 *** | 0.005 *** | 0.009 *** | 0.008 *** | 0.009 * | 0.02 * | 0.02 ** | 0.04 *** |

| (0.003) | (0.001) | (0.001) | (0.001) | (0.005) | (0.01) | (0.01) | (0.01) | |

| CRHO | 0.16 *** | 0.002 | 0.07 * | 0.01 * | 0.009 | 0.12 ** | 0.13 ** | 0.11 ** |

| (0.01) | (0.008) | (0.007) | (0.006) | (0.01) | (0.04) | (0.05) | (0.06) | |

| Cons | 14.2 *** | 6.21 *** | 1.79 *** | 4.11 *** | 1.45 *** | 3.06 *** | 0.96 *** | 10.66 ** |

| (1.36) | (0.39) | (0.61) | (1.67) | (0.84) | (1.22) | (1.21) | (1.97) | |

| R squared | 0.81 | 0.71; 0.83; 0.85; 0.85 | 0.30 | 0.30 | 0.33 | 0.36 | ||

| F statistic | 36.93 *** | 39.01 *** | 37.96 *** | 41.76 *** | 2.90 *** | 3.93 *** | 3.10 *** | 2.52 *** |

| Obs. | 252 | 252 | 252 | 231 | 252 | 252 | 252 | 231 |

| Independent Variables | Dependent Variable-GDP | Dependent Variable-TFP | ||||||

|---|---|---|---|---|---|---|---|---|

| OLS with Years Dummy | Fixed Effects | OLS with Years Dummy | Fixed Effects | |||||

| Country FE, Year FE, Year FE (2) | Country FE, Year FE, Year FE (2) | |||||||

| CONCPI | −0.0007 | −0.05 *** | 0.01 | −0.014 * | 0.01 | −0.09 | −0.13 ** | −0.08 |

| (0.036) | (0.01) | (0.014) | (0.007) | (0.06) | (0.06) | (0.06) | (0.008) | |

| CONEXR | −0.004 | −0.004 ** | −0.008 *** | −0.78 *** | 0.0006 | 0.09 | −0.32 | 0.008 |

| (0.001) | (0.002) | (0.001) | (0.26) | (0.002) | (0.009) | (0.04) | (0.001) | |

| SCT | 0.02 | 0.02 ** | 0.01 * | −0.002 * | 0.04 | −0.01 | −0.06 ** | 0.08 |

| (0.01) | (0.01) | (0.009) | (0.003) | (0.02) | (0.006) | (0.02) | (0.07) | |

| SDD | 0.06 *** | 0.008 | 0.006 | 0.0005 | −0.06 *** | 0.07 | 0.05 ** | −0.004 |

| (0.01) | (0.006) | (0.005) | (0.002) | (0.029) | (0.003) | (0.02) | (0.02) | |

| SC | 0.04 | 0.03 *** | 0.01 | 0.03 * | 0.01 | −0.02 | 0.04 | 0.04 |

| (0.01) | (0.01) | (0.008) | (0.009) | (0.002) | (0.004) | (0.007) | (0.006) | |

| MS | 0.55 *** | 0.13 *** | 0.10 *** | −0.02 ** | 0.37 *** | 1.34 *** | −0.24 *** | −0.62 |

| (0.07) | (0.04) | (0.03) | (0.01) | (0.14) | (0.19) | (0.07) | (0.08) | |

| TRADE | −0.47 *** | 0.41 *** | −0.41 ** | −0.26 | 0.15 | −0.63 | 0.51 | 2.37 *** |

| (0.14) | (0.10) | (0.11) | (0.07) | (0.02) | (0.51) | (0.05) | (0.99) | |

| MONFR | −0.1 | −0.004 | 0.002 | −0.005 * | 0.04 ** | 0.020 ** | 0.02 | 0.05 * |

| (0.008) | (0.002) | (0.002) | (0.001) | (0.011) | (0.01) | (0.01) | (0.012) | |

| UNEM | −0.05 *** | −0.02 *** | −0.02 *** | −0.011 *** | −0.02 ** | −0.04 *** | −0.01 *** | −0.03 * |

| (0.009) | (0.004) | (0.003) | (0.001) | (0.01) | (0.02) | (0.01) | (0.03) | |

| CONINT | −0.03 ** | −0.021 | −0.02 *** | −0.01 ** | −0.29 ** | −0.18 ** | −0.09 | 0.19 |

| (0.004) | (0.01) | (0.013) | (0.005) | (0.08) | (0.09) | (0.04) | (0.13) | |

| BDEF | 0.032 *** | −0.03 | −0.0005 | −0.005 ** | −0.02 | 0.03 | −0.03 * | −0.02 |

| (0.010) | (0.005) | (0.004) | (0.002) | (0.002) | (0.02) | (0.01) | (0.003) | |

| PSP | 0.04 *** | 0.009 *** | 0.004 | 0.001 | −0.011 | −0.09 | −0.01 | −0.009 |

| (0.005) | (0.003) | (0.002) | (0.001) | (0.010) | (0.01) | (0.010) | (0.002) | |

| GRS | 0.05 *** | 0.01 ** | 0.013 *** | 0.008 | −0.02 * | −0.03 | 0.02 * | −0.027 |

| (0.007) | (0.004) | (0.003) | (0.001) | (0.017) | (0.02) | (0.014) | (0.02) | |

| CRHO | 0.05 ** | −0.018 ** | −0.02 *** | −0.016 ** | −0.07 * | 0.01 | −0.13 *** | −0.01 |

| (0.01) | (0.008) | (0.006) | (0.006) | (0.03) | (0.003) | (0.05) | (0.005) | |

| Cons | 5.11 *** | 5.84 *** | 10.01 *** | 3.94 *** | 3.29 *** | 3.26 *** | 1.09 *** | 4.83 *** |

| (0.92) | (0.59) | (0.58) | (1.70) | (1.68) | (0.88) | (1.13) | (1.45) | |

| R squared | 0.94 | 0.80 | 0.91 | 0.85 | 0.57 | 0.54 | 0.63 | 0.54 |

| F statistic | 64.92 *** | 30.88 *** | 37.21 *** | 41.86 *** | 5 *** | 8.82 *** | 27.45 *** | 18.75 *** |

| Obs. | 140 | 140 | 140 | 128 | 140 | 140 | 140 | 128 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bostan, I.; Oprea, O.-R.; Stoica, O. Approaching Monetary Integration in the Context of the Imperative to Ensure the Sustainable Growth in the EU. Sustainability 2020, 12, 7065. https://doi.org/10.3390/su12177065

Bostan I, Oprea O-R, Stoica O. Approaching Monetary Integration in the Context of the Imperative to Ensure the Sustainable Growth in the EU. Sustainability. 2020; 12(17):7065. https://doi.org/10.3390/su12177065

Chicago/Turabian StyleBostan, Ionel, Otilia-Roxana Oprea, and Ovidiu Stoica. 2020. "Approaching Monetary Integration in the Context of the Imperative to Ensure the Sustainable Growth in the EU" Sustainability 12, no. 17: 7065. https://doi.org/10.3390/su12177065

APA StyleBostan, I., Oprea, O.-R., & Stoica, O. (2020). Approaching Monetary Integration in the Context of the Imperative to Ensure the Sustainable Growth in the EU. Sustainability, 12(17), 7065. https://doi.org/10.3390/su12177065