Evaluating the Performance of the Government Venture Capital Guiding Fund Using the Intuitionistic Fuzzy Analytic Hierarchy Process

Abstract

1. Introduction

2. Literature Review

2.1. The Performance Evaluation of the GVC

2.2. The Performance Evaluation Methods of the GVC

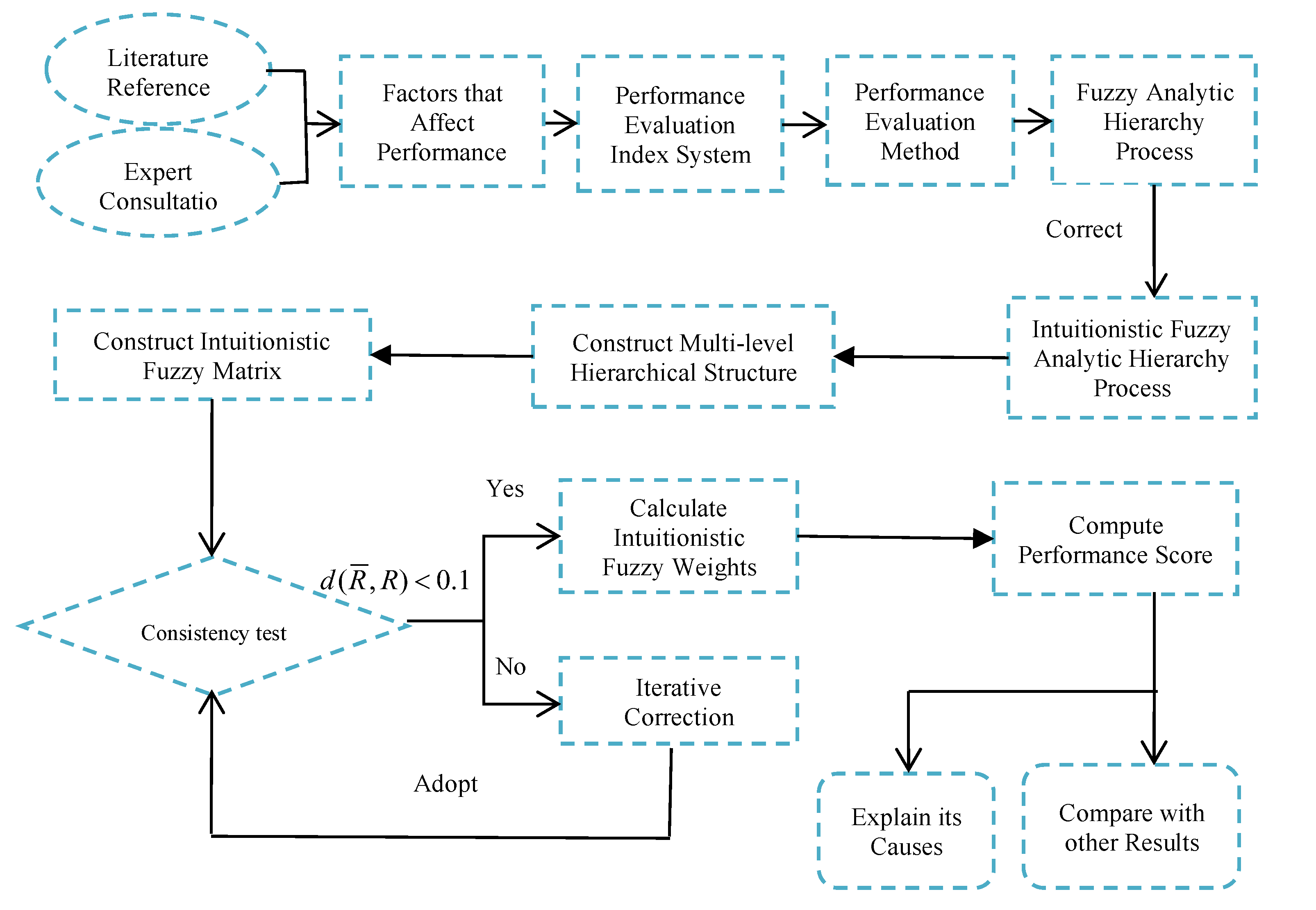

3. Research Design

3.1. Objectives and Contents of Performance Evaluation of the GVCGF

3.2. Procedure of Performance Evaluation of the GVCGF

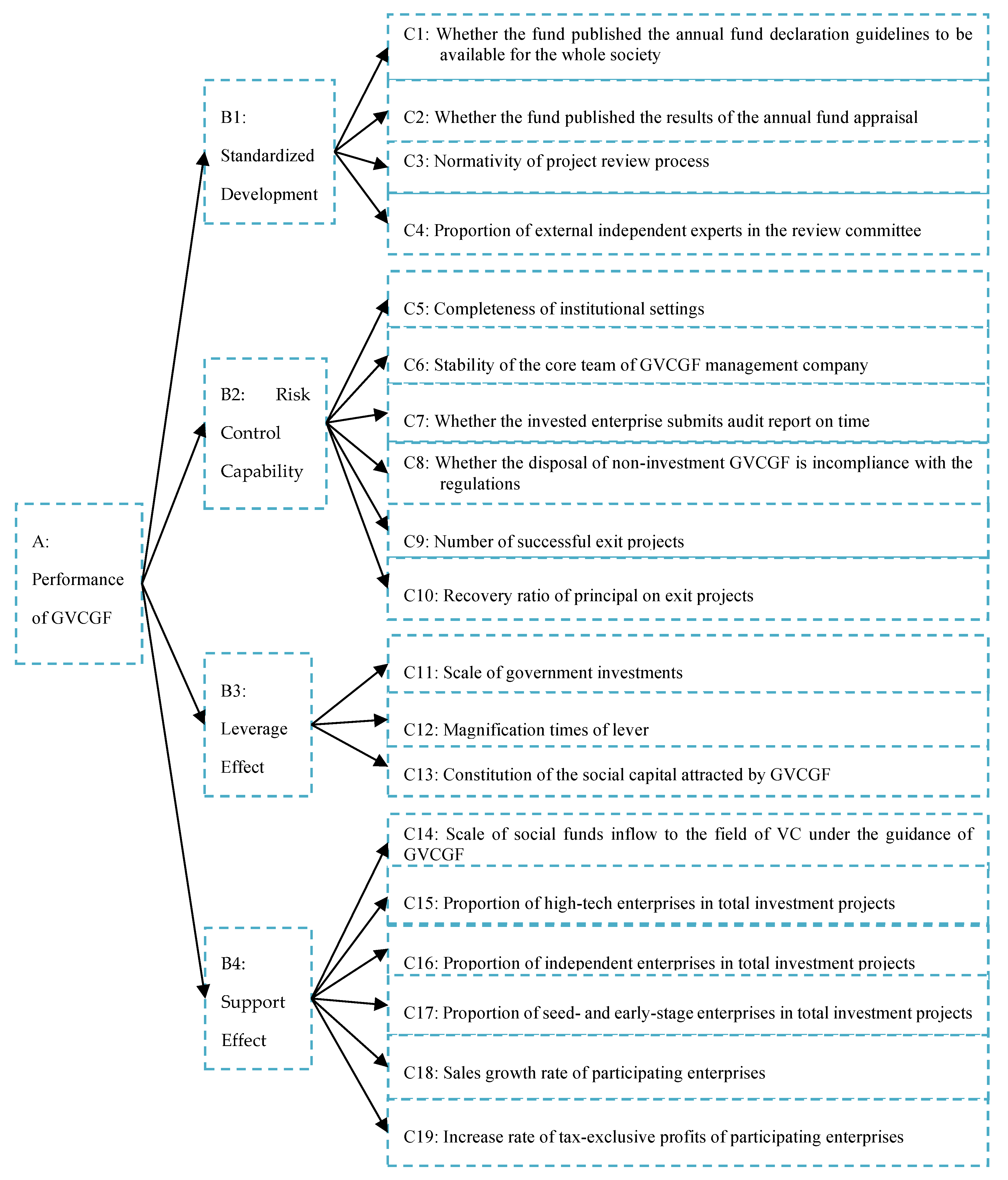

3.3. Construction of the Index System for Performance Evaluation of the GVCGF

3.4. The IFAHP for Performance Evaluation of the GVCGF

3.5. Judgement Criteria for the Development Performance of the GVCGF

4. Application of the Performance Evaluation Model

4.1. Performance Evaluation Process of the GVCGF in Ningbo, China

4.2. Analysis of Performance Evaluation Results

4.3. Comparison with the Results Obtained by AHP Methods

5. Conclusions and Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Category | Indicator | Reference | a1 (0.1) | a2 (0.4) | a3 (0.7) | a4 (0.9) | Score | Retain |

|---|---|---|---|---|---|---|---|---|

| Standardized development | Whether the fund published the annual fund declaration guidelines to be available for the whole society | [53] | 0 | 1 | 2 | 7 | 0.81 | Yes |

| Whether the fund published the results of the annual fund appraisal | [53] | 0 | 0 | 2 | 8 | 0.86 | Yes | |

| Quality of information provided on official websites | [53] | 2 | 3 | 3 | 2 | 0.53 | No | |

| Normativity of the project review process | [53] | 0 | 2 | 4 | 4 | 0.72 | Yes | |

| Normative selection of cooperative VC enterprises | [53] | 0 | 3 | 4 | 3 | 0.67 | No | |

| Office capacity of the GVCGF Board | [27] | 0 | 4 | 3 | 3 | 0.64 | No | |

| Proportion of external independent experts on the review committee | [53] | 0 | 2 | 4 | 4 | 0.72 | Yes | |

| Professional evaluation ability of the GVCGF expert appraisers | [80] | 0 | 3 | 3 | 4 | 0.69 | No | |

| Risk control capability | Whether the record information is complete | [53] | 1 | 3 | 4 | 2 | 0.59 | No |

| Effectiveness of internal control mechanism | [53] | 0 | 3 | 5 | 2 | 0.65 | No | |

| Completeness of institutional settings | [80] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Stability of the core team of the GVCGF management company | [49] | 0 | 2 | 5 | 3 | 0.70 | Yes | |

| Whether the invested enterprise submits audit report on time | [53] | 0 | 2 | 4 | 4 | 0.72 | Yes | |

| Whether the disposal of non-investment GVCGF is incompliance with the regulations | [53] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Number of exit projects | [28] | 3 | 2 | 3 | 2 | 0.50 | No | |

| Number of successful exit projects | [42] | 0 | 1 | 5 | 4 | 0.75 | Yes | |

| Recovery ratio of principal on exit projects | [18,42] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Leverage effect | Scale of government investments | [16] | 0 | 2 | 4 | 4 | 0.72 | Yes |

| Growth rate of the GVCGF | [16] | 2 | 3 | 3 | 2 | 0.53 | No | |

| Magnification times of lever | [26] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Rate of the GVCGF in place | [80] | 3 | 2 | 2 | 3 | 0.52 | No | |

| Investment structure of the GVCGF | [81] | 1 | 2 | 4 | 3 | 0.64 | No | |

| Constitution of the social capital attracted by the GVCGF | [80] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Support effect | Whether the fund investment in the related industry is supported and encouraged by the government | [80] | 2 | 2 | 4 | 2 | 0.56 | No |

| Scale of social funds inflow to the field of VC under the guidance of the GVCGF | [16] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Growth rate of social funds inflow to the field of VC under the guidance of the GVCGF | [80] | 1 | 2 | 4 | 3 | 0.64 | No | |

| Proportion of high-tech enterprises in total investment projects | [18,28] | 0 | 1 | 4 | 5 | 0.77 | Yes | |

| Proportion of local enterprises in total investment projects | [38] | 1 | 3 | 4 | 2 | 0.59 | No | |

| Proportion of independent enterprises in total investment projects | [35] | 0 | 2 | 4 | 5 | 0.81 | Yes | |

| Proportion of small and medium-sized enterprises in total investment projects | [80] | 2 | 2 | 4 | 2 | 0.56 | No | |

| Proportion of seed- and early-stage enterprises in total investment projects | [19] | 0 | 2 | 3 | 5 | 0.74 | Yes | |

| Employment growth rate of participating enterprises | [31] | 1 | 2 | 4 | 3 | 0.64 | No | |

| Sales growth rate of participating enterprises | [28] | 0 | 2 | 4 | 4 | 0.72 | Yes | |

| Number of successful R&D projects of participating enterprises | [35] | 2 | 2 | 3 | 3 | 0.58 | No | |

| Increase rate of tax-exclusive profits of participating enterprises | [49] | 0 | 2 | 5 | 3 | 0.70 | Yes |

Appendix B

| Indicators Name | Definition | Type |

|---|---|---|

| C1: Whether the fund published the annual fund declaration guidelines to be available to the whole society | Published = 1, unpublished = 0 | Dum |

| C2: Whether the fund published the results of the annual fund appraisal | Published = 1, unpublished = 0 | Dum |

| C3: Normativity of project review process | Non-normative = 0, relatively normative = 1, normative = 3, very normative = 5 | Qua |

| C4: Proportion of external independent experts on the review committee | Number of external independent experts/Total number of review committees | Con |

| C5: Completeness of institutional settings | Incomplete = 0, relatively complete = 1, complete = 3, very complete = 5 | Qua |

| C6: Stability of the core team of the GVCGF management company | Instability = 0, relatively stable = 1, stable = 3, very stable = 5 | Qua |

| C7: Whether the invested enterprise submits audit report on time | Delivery on time = 1, delivery not on time = 0 | Dum |

| C8: Whether the disposal of non-investment the GVCGF is incompliance with the regulations | Compliance = 1, non-compliance = 0 | Dum |

| C9: Number of successful exit projects | Number of successful exit projects/Total exit projects | Con |

| C10: Recovery ratio of principal on exit projects | Principal/Input number of exit projects | Con |

| C11: Scale of government investments | Government input amount | Con |

| C12: Magnification times of lever | Government funds/Social funds | Con |

| C13: Constitution of the social capital attracted by the GVCGF | The sum of private capital/Social capital | Con |

| C14: Scale of social funds inflow to the field of VC under the guidance of the GVCGF | The amount of social capital entering entrepreneurial enterprises | Con |

| C15: Proportion of high-tech enterprises in total investment projects | High-tech enterprises/Total invested enterprises | Con |

| C16: Proportion of independent enterprises in total investment projects | Independent enterprises/Total invested enterprises | Con |

| C17: Proportion of seed- and early-stage enterprises in total investment projects | Seed- and early-stage enterprises/Total invested enterprises | Con |

| C18: Sales growth rate of participating enterprises | Current sales increase/Previous sales of invested enterprises | Con |

| C19: Net profit growth rate of participating enterprises | Net profit growth rate = (net profit for the current year-net profit for the previous year)/net profit for the previous year × 100% | Con |

Appendix C. The Analytic Hierarchy Process to Calculate the Weight

| Scale | Meaning |

|---|---|

| 1 | Element i and element j are equally important |

| 3 | Element i is slightly more important than element j |

| 5 | Element i is significantly more important than element j |

| 7 | Element i is strongly more important than element j |

| 9 | Element i is extremely more important than element j |

| 2,4,6,8 | The intermediate values of the above adjacent judgments |

| Reciprocal | If is the importance ratio of the element to the element j, then is the importance ratio of the element j to the element i. That is to say, |

| Matrix Order | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| RI | 0 | 0 | 0.52 | 0.89 | 1.12 | 1.26 | 1.36 | 1.41 |

| The judgment matrix of criterion layers A–B | |||||||

| A | B2 | B3 | B4 | B1 | Wi | ||

| B1 | 2.000 | 0.500 | 0.250 | 1.000 | - | ||

| B2 | 1.000 | 0.333 | 0.250 | 0.500 | - | ||

| B3 | 3.000 | 1.000 | 0.333 | 5.000 | - | ||

| B4 | 4.000 | 3.000 | 1.000 | 4.000 | - | ||

| Consistency check CR = 0.1070 > 0.1 | |||||||

| The judgment matrix of criterion layers A–B * | |||||||

| A | B2 | B3 | B4 | B1 | Wi | ||

| B1 | 2.000 | 0.500 | 0.250 | 1.000 | 0.143 | ||

| B2 | 1.000 | 0.333 | 0.250 | 0.500 | 0.093 | ||

| B3 | 3.000 | 1.000 | 0.333 | 2.000 | 0.239 | ||

| B4 | 4.000 | 3.000 | 1.000 | 4.000 | 0.525 | ||

| Consistency check CR = 0.0329 < 0.1; λmax = 4.0878 | |||||||

| The judgment matrix of index layers B1–C | |||||||

| B1 | C11 | C12 | C13 | C14 | Wi | ||

| C1 | 1.000 | 1.000 | 1.000 | 1.000 | 0.242 | ||

| C2 | 1.000 | 1.000 | 3.000 | 1.000 | 0.338 | ||

| C3 | 1.000 | 0.333 | 1.000 | 1.000 | 0.192 | ||

| C4 | 1.000 | 1.000 | 1.000 | 1.000 | 0.229 | ||

| Consistency check CR = 0.0687 < 0.1 λmax = 4.1223 | |||||||

| The judgment matrix of index layers B2–C | |||||||

| B2 | C21 | C22 | C23 | C24 | C25 | C26 | Wi |

| C5 | 1.000 | 1.000 | 2.000 | 1.000 | 1.000 | 1.000 | 0.172 |

| C6 | 1.000 | 1.000 | 1.000 | 2.000 | 0.500 | 0.500 | 0.151 |

| C7 | 0.500 | 1.000 | 1.000 | 1.000 | 0.333 | 0.333 | 0.099 |

| C8 | 1.000 | 0.500 | 1.000 | 1.000 | 2.000 | 1.000 | 0.174 |

| C9 | 1.000 | 2.000 | 3.000 | 0.500 | 1.000 | 1.000 | 0.196 |

| C10 | 1.000 | 2.000 | 3.000 | 1.000 | 1.000 | 1.000 | 0.209 |

| Consistency check CR = 0.0714 < 0.1; λmax = 0.4499 | |||||||

| The judgment matrix of index layers B3–C | |||||||

| B3 | C31 | C32 | C33 | Wi | |||

| C11 | 1.000 | 0.500 | 1.000 | 0.250 | |||

| C12 | 2.000 | 1.000 | 2.000 | 0.500 | |||

| C13 | 1.000 | 0.500 | 1.000 | 0.250 | |||

| Consistency check CR = 0.0000 < 0.1; λmax = 3.0000 | |||||||

| The judgment matrix of index layers B4–C | |||||||

| B4 | C41 | C42 | C43 | C44 | C45 | C46 | Wi |

| C14 | 1.000 | 3.000 | 3.000 | 3.000 | 1.000 | 1.000 | 0.266 |

| C15 | 0.333 | 1.000 | 1.000 | 1.000 | 0.500 | 0.500 | 0.101 |

| C16 | 0.333 | 1.000 | 1.000 | 1.000 | 0.500 | 0.500 | 0.101 |

| C17 | 0.333 | 1.000 | 1.000 | 1.000 | 0.500 | 0.500 | 0.101 |

| C18 | 1.000 | 2.000 | 2.000 | 2.000 | 1.000 | 1.000 | 0.216 |

| C19 | 1.000 | 2.000 | 2.000 | 2.000 | 1.000 | 1.000 | 0.216 |

| Consistency check CR = 0.0044 < 0.1; λmax = 6.0275 | |||||||

References

- Ning, Y.; Xu, G.; Long, Z. What Drives the Venture Capital Investments in China? Chin. Manag. Stud. 2019, 13, 574–602. [Google Scholar] [CrossRef]

- Bernstein, S.; Giroud, X.; Townsend, R.R. The Impact of Venture Capital Monitoring. J. Financ. 2016, 71, 1591–1622. [Google Scholar] [CrossRef]

- Croce, A.; Martí, J.; Murtinu, S. The Impact of Venture Capital on the Productivity Growth of European Entrepreneurial Firms: ‘Screening’ or ‘Value Added’ Effect? J. Bus. Ventur. 2013, 28, 489–510. [Google Scholar] [CrossRef]

- Gompers, P.; Lerner, J. The Venture Capital Cycle; MIT Press: Cambridge, UK, 1999. [Google Scholar]

- Gompers, P.; Lerner, J. The Venture Capital Revolution. J. Econ. Perspect. 2001, 15, 145–168. [Google Scholar] [CrossRef]

- Gompers, P.; Lerner, J. Short-Term America Revisited? Boom and Bust in the Venture Capital Industry and the Impact on Innovation. Innov. Policy Econ. 2003, 3, 1–27. [Google Scholar] [CrossRef]

- Gompers, P.A.; Lerner, J. The Venture Capital Cycle, 2nd ed.; MIT Press: Cambridge, UK, 2004. [Google Scholar]

- Gompers, P.; Kovner, A.; Lerner, J.; Scharfstein, D. Venture Capital Investment Cycles: The Impact of Public Markets. J. Financ. Econ. 2008, 87, 1–23. [Google Scholar] [CrossRef]

- Groh, A.P.; Von Liechtenstein, H. The First Step of the Capital Flow from Institutions to Entrepreneurs: The Criteria for Sorting Venture Capital Funds. Eur. Financ. Manag. 2001, 17, 532–559. [Google Scholar] [CrossRef]

- Groh, A.P.; von Liechtenstein, H.; Lieser, K. The European Venture Capital and Private Equity Country Attractiveness Indices. J. Corp. Financ. 2010, 16, 205–224. [Google Scholar] [CrossRef]

- Keuschnigg, C. Venture Capital Backed Growth. J. Econ. Growth 2004, 9, 239–261. [Google Scholar] [CrossRef]

- Li, X.; Tan, H.H.; Wilson, C.; Wu, Z. When Should Venture Capitalists Exit Their Investee Companies? Int. J. Manag. Financ. 2013, 9, 351–364. [Google Scholar] [CrossRef]

- Nahata, R. Venture Capital Reputation and Investment Performance. J. Financ. Econ. 2008, 90, 127–151. [Google Scholar] [CrossRef]

- Nahata, R.; Hazarika, S.; Tandon, K. Success in Global Venture Capital Investing: Do Institutional and Cultural Differences Matter? J. Financ. Quant. Anal. 2014, 49, 1039–1070. [Google Scholar] [CrossRef]

- Xue, J.; Klein, P.G. Regional Determinants of Technology Entrepreneurship. Int. J. Entrep. Ventur. 2010, 1, 291–308. [Google Scholar] [CrossRef]

- Brander, J.A.; Du, Q.; Hellmann, T. The Effects of Government-Sponsored Venture Capital: International Evidence. Rev. Financ. 2015, 19, 571–618. [Google Scholar] [CrossRef]

- Martin, S.; Scott, J.T. The Nature of Innovation Market Failure and The Design of Public Support for Private Innovation. Res. Policy 2000, 29, 437–447. [Google Scholar] [CrossRef]

- Cumming, D. Government policy towards entrepreneurial finance: Innovation investment funds. J. Bus. Ventur. 2007, 22, 193–235. [Google Scholar] [CrossRef]

- Cumming, D.J.; Grilli, L.; Murtinu, S. Governmental and Independent Venture Capital Investments in Europe: A Firm-Level Performance Analysis. J. Corp. Financ. 2017, 42, 439–459. [Google Scholar] [CrossRef]

- Lerner, J. The Government as Venture Capitalist: The Long-Run Effects of the SBIR Program. J. Bus. 1999, 72, 285–318. [Google Scholar] [CrossRef]

- Munari, F.; Toschi, L. Assessing the Impact of Public Venture Capital Programmes in the United Kingdom: Do Regional Characteristics Matter? J. Bus. Ventur. 2015, 30, 205–226. [Google Scholar] [CrossRef]

- Lin, L. Engineering a Venture Capital Market: Lessons from China. Columbia J. Asian Law 2017, 30, 160–220. [Google Scholar]

- Wang, J.; Wang, J.; Ni, H.; He, S. How Government Venture Capital Guiding Funds Work in Financing High-Tech Start-Ups in China: A ‘Strategic Exchange’ Perspective. Strateg. Chang. 2013, 22, 417–429. [Google Scholar] [CrossRef]

- Murray, G.; Maula, M.V.J. Finnish Industry Investment Ltd.: An International Evaluation; Ministry of Trade and Industry Publication: Helsinki, Finland, 2003; pp. 53–61.

- Bertoni, F.; Tykvová, T. Does Governmental Venture Capital Spur Invention and Innovation? Evidence from Young European Biotech Companies. Res. Policy 2015, 44, 925–935. [Google Scholar] [CrossRef]

- Leleux, B.; Surlemont, B. Public Versus Private Venture Capital: Seeding or Crowding Out? APan-European Analysis. J. Bus. Ventur. 2003, 18, 81–104. [Google Scholar] [CrossRef]

- Cumming, D.; Macintosh, J. Crowding Out Private Equity: Canadian Evidence. J. Bus. Ventur. 2006, 21, 569–609. [Google Scholar] [CrossRef]

- Colombo, M.G.; Cumming, D.J.; Vismara, S. Governmental Venture Capital for Innovative Young Firms. J. Technol. Transfer. 2016, 41, 10–24. [Google Scholar] [CrossRef]

- Rin, M.D.; Nicodano, G.; Sembenelli, A. Public Policy and the Creation of Active Venture Capital Markets. J. Public Econ. 2006, 90, 1699–1723. [Google Scholar] [CrossRef]

- Faccio, M.; Masulis, R.W.; Mcconnell, J.J. Political Connections and Corporate Bailouts. J. Financ. 2006, 61, 2597–2635. [Google Scholar] [CrossRef]

- Grilli, L.; Murtinu, S. Government, Venture Capital and the Growth of European High-Tech Entrepreneurial Firms. Res. Policy 2014, 43, 1523–1543. [Google Scholar] [CrossRef]

- Sohn, D.W.; Kim, H.J.; Hur, W. Effect of Venture Capital and Government Support on the Performance of Venture Firms in Korea. Asian J. Technol. Innov. 2012, 20, 309–322. [Google Scholar] [CrossRef]

- Alperovych, Y.; Hübner, G.; Lobet, F. How Does Governmental Versus Private Venture Capital Backing Affect A Firm’s Efficiency? Evidence from Belgium. J. Bus. Ventur. 2015, 30, 508–525. [Google Scholar] [CrossRef]

- Audretsch, D.B.; Link, A.N.; Scott, J.T. Public/Private Technology Partnerships: Evaluating SBIR-supported Research. Res. Policy 2002, 31, 145–158. [Google Scholar] [CrossRef]

- Bertoni, F.; Tykvová, T. Which Form of Venture Capital Is Most Supportive of Innovation; ZEW Discussion Paper No.12-018; Mannheim, German. 2012. Available online: https://www.zew.de/publikationen/which-form-of-venture-capital-is-most-supportive-of-innovation/ (accessed on 8 July 2020).

- Buzzacchi, L.; Scellato, G.; Ughetto, E. The Investment Strategies ofPublicly Sponsored Venture Capital Funds. J. Bank. Financ. 2013, 37, 707–716. [Google Scholar] [CrossRef]

- Cumming, D. Public Economics Gone Wild: Lessons from Venture Capital. Int. Rev. Financ. Anal. 2014, 36, 251–260. [Google Scholar] [CrossRef]

- Cumming, D.; Johan, S. Pre-Seed Government Venture Capital Funds. J. Int. Entrep. 2009, 7, 26–56. [Google Scholar] [CrossRef]

- Islam, M.; Fremeth, A.; Marcus, A. SignalingbyEarly Stage Start-Ups: Us Government Research Grants and Venture Capital Funding. J. Bus. Ventur. 2018, 33, 35–51. [Google Scholar] [CrossRef]

- Lim, S.; Kim, Y. How to Design Public Venture Capital Funds: Empirical Evidence from South Korea. J. Small Bus. Manag. 2015, 53, 843–867. [Google Scholar] [CrossRef]

- Pierrakis, Y.; Saridakis, G. Do Publicly Backed Venture Capital Investments Promote Innovation? Differences between Privately and Publicly Backed Funds in the UK Venture Capital Market. J. Bus. Ventur. Insights 2017, 7, 55–64. [Google Scholar] [CrossRef]

- Zhang, Y.; Mayes, D.G. The Performance of Governmental Venture Capital Firms: A Life Cycle Perspective and Evidence from China. Pac. Basin Financ. J. 2018, 48, 162–185. [Google Scholar] [CrossRef]

- Abdullah, L.; Najib, L. Sustainable Energy Planning Decision Using the Intuitionistic Fuzzy Analytic Hierarchy Process: Choosing Energy Technology in Malaysia. Int. J. Sustain. Energy 2016, 35, 360–377. [Google Scholar] [CrossRef]

- Afful-Dadzie, E.; Afful-Dadzie, A. A Decision Making Model for Selecting Start-Up Businesses in a Government Venture Capital Scheme. Manag. Decis. 2016, 54, 714–734. [Google Scholar] [CrossRef]

- Afful-Dadzie, E.; Afful-Dadzie, A.; Oplatkova, Z.K. Assessing Commercial Viability of Technology Start-Up Businesses in a Government Venture Capital under Intuitionistic Fuzzy Environment. Int. J. Fuzzy Syst. 2017, 19, 400–413. [Google Scholar] [CrossRef]

- Cumming, D.; Li, D. Public Policy, Entrepreneurship, and Venture Capital in the United States. J. Corp. Financ. 2013, 23, 345–367. [Google Scholar] [CrossRef]

- Karsai, J. Government venture capital in Central and Eastern Europe. Ventur. Cap. Int. J. Entrep. Financ. 2018, 20, 73–102. [Google Scholar] [CrossRef]

- Murray, G.C. A Policy Responseto Regional Disparitiesin the Supply of Risk Capital to New Technology-based Firms in the European Union: The European Seed Capital and Scheme. Reg. Stud. 1998, 32, 405–419. [Google Scholar] [CrossRef]

- Nightingale, P.; Murray, G.; Cowling, M.; Baden-Fuller, C.; Mason, C.; Siepel, J.; Hopkins, M.; Dannreuther, C. From Funding Gaps to Thin Markets: UK Government Support for Early-Stage Venture Capital; NESTA Research Report; London, UK. 2009. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1478902 (accessed on 8 July 2020).

- Guerini, M.; Quas, A. Governmental Venture Capital in Europe: Screening and Certification. J. Bus. Ventur. 2016, 31, 175–195. [Google Scholar] [CrossRef]

- Bertoni, F.; Colombo, M.G.; Quas, A. The Role of Governmental Venture Capital in the Venture Capital Ecosystem: An Organizational Ecology Perspective. Entrep. Theory Pract. 2019, 43, 611–628. [Google Scholar] [CrossRef]

- Zhang, Y. Gain or Pain? New Evidence on Mixed Syndication between Governmental and Private Venture Capital Firms in China. Small Bus. Econ. 2018, 51, 995–1031. [Google Scholar] [CrossRef]

- Chen, Y. Establishment of the Target Evaluation System of Venture Capital Guidance Fund: Taking Hangzhou as an Example. Master’s Thesis, Zhejiang Gongshang University, Hangzhou, China, 2014. [Google Scholar]

- Xiang, Y. The Research on the Performance Evaluation of Government Venture Capital Guiding Fund-Take the Instance of Hangzhou and Ningbo. Master’s Thesis, Zhejiang University, Hangzhou, China, 2018. [Google Scholar]

- Saaty, T.L. A Scaling Method for Priorities in Hierarchical Structures. J. Math. Psychol. 1977, 15, 234–281. [Google Scholar] [CrossRef]

- Laarhoven, P.J.M.V.; Pedrycz, W. A fuzzy Extension of Saaty’s Priority Theory. Fuzzy Sets Syst. 1983, 11, 229–241. [Google Scholar] [CrossRef]

- Buckley, J.J. Fuzzy hierarchical analysis. Fuzzy Sets Syst. 1985, 17, 233–247. [Google Scholar] [CrossRef]

- Atanassov, K.T. Intuitionistc Fuzzy Sets. Fuzzy Sets Syst. 1986, 20, 87–96. [Google Scholar] [CrossRef]

- Atanassov, K.T. More on Intuitionistic Fuzzy Sets. Fuzzy Sets Syst. 1989, 33, 37–45. [Google Scholar] [CrossRef]

- Atanassov, K.T. Intuitionistic Fuzzy Sets Theory and Applications; Physica-Verlag: Heidelberg, Germany; New York, NY, USA, 1999. [Google Scholar]

- Zadeh, L.A. Fuzzy Sets. Inf. Control 1965, 8, 338–353. [Google Scholar] [CrossRef]

- Xu, Z.; Liao, H. Intuitionistic Fuzzy Analytic Hierarchy Process. IEEE Trans. Fuzzy Syst. 2014, 22, 749–761. [Google Scholar] [CrossRef]

- Kaur, P. Selection of Vendor Based on Intuitionistic Fuzzy Analytical Hierarchy Process. Adv. Oper. Res. 2014, 2014, 1–10. [Google Scholar] [CrossRef]

- Nguyen, H. An Application of Intuitionistic Fuzzy Analytic Hierarchy Process in Ship System Risk Estimation. J. KONES Powertrain Transp. 2016, 23, 365–372. [Google Scholar]

- Wang, J.; Sun, Y. The Intuitionistic Fuzzy Sets in Evaluation of Risks in Projects of Energy Management Contrac. Syst. Eng. Procedia 2012, 3, 30–35. [Google Scholar] [CrossRef]

- Sadiq, R.; Tesfamariam, S. Environmental Decision-Making under Uncertainty Using Intuitionistic Fuzzy Analytic Hierarchy Process (IF-AHP). Stoch. Environ. Res. Risk Assess. 2009, 23, 75–91. [Google Scholar] [CrossRef]

- Wang, Y.; Xu, Z. Evaluation of the Human Settlement in Lhasa with Intuitionistic Fuzzy Analytic Hierarchy Process. Int. J. Fuzzy Syst. 2018, 20, 29–44. [Google Scholar] [CrossRef]

- Jaafar, S.; Abdullah, L.; Taib, I. Intuitionistic Fuzzy Analytic Hierarchy Process Approach in Ranking of Human Capital Indicators. J. Appl. Sci. 2013, 13, 423–429. [Google Scholar]

- Weng, Y.J.; Deng, Q.Z.; Du, L. Systematic Analysis of the Factors Influencing the Size of Local Government Administrative Establishment from the Perspective of Complex System: Based on Dematel-ISM Integration Method. Math. Pract. Theory 2015, 45, 110–119. [Google Scholar]

- Xu, Z.; Cai, X. Intuitionistic Fuzzy Information Aggregation. In Intuitionistic Fuzzy Information Aggregation; Springer: Berlin, Germany, 2012. [Google Scholar]

- Szmidt, E.; Kacprzyk, J. Distances between Intuitionistic Fuzzy Sets. Fuzzy Sets Syst. 2000, 114, 505–518. [Google Scholar] [CrossRef]

- Xu, Z. Intuitionistic Fuzzy Aggregation Operators. IEEE Trans. Fuzzy Syst. 2007, 15, 1179–1187. [Google Scholar]

- Gao, H.Y.; Wang, C.; Ha, M.H. Intuitive Fuzzy Analytic Hierarchy Process. J. Hebei Univ. Eng. (Nat. Sci. Ed.) 2011, 28, 101–105. [Google Scholar]

- Cerioli, A.; Zani, S.A. Fuzzy Approach on Measurement of Poverty. In Income and Wealth Distribution and Inequality and Poverty: Studies in Contemporary Economics; Dagum, C., Zenga, M., Eds.; Springer: Berlin, Germany, 1990. [Google Scholar]

- Aloini, D.; Dulmin, R.; Mininno, V. A Peer IF-Topsis Based Decision Support System for Packaging Machine Selection. Expert Syst. Appl. 2014, 41, 2157–2165. [Google Scholar] [CrossRef]

- Torra, V. Hesitant Fuzzy Sets. Int. J. Intell. Syst. 2010, 25, 525–539. [Google Scholar] [CrossRef]

- Liao, H.; Xu, Z. A Vikor-Based Method for Hesitant Fuzzy Multi-Criteria Decision Making. Fuzzy Optim. Decis. Mak. 2013, 12, 373–392. [Google Scholar] [CrossRef]

- Rodriguez, R.M.; Martinez, L.; Herrera, F. Hesitant Fuzzy Linguistic Term Sets for Decision Making. IEEE Trans. Fuzzy Syst. 2012, 20, 109–119. [Google Scholar] [CrossRef]

- Liao, C.H.; Xu, Z.S. Hesitant Fuzzy Decision Making Methodologies and Applications; Springer: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Campbell, T.; Ulrich, B.; Alexandre, B. Evaluation of EIF Funding of Venture Capital Fund-EIB/ETF Mandate; European Investment Bank Evaluation Report; Luxembourg. 2007. Available online: https://www.eib.org/attachments/ev/ev_eif_funding_of_venture_capital_funds_en.pdf (accessed on 8 July 2020).

- Bartzokas, A.; Mani, S. (Eds.) Financial Systems, Corporate Investment in Innovation, and Venture Capital; Edward Elgar Publishing: Cheltenham, UK, 2004. [Google Scholar]

| Linguistic Terms | Intuitionistic Fuzzy Number |

|---|---|

| Extremely important | (0.90,0.10,0.00) |

| Very important | (0.80,0.15,0.05) |

| Medium importance | (0.70,0.20,0.10) |

| Slightly important | (0.60,0.25,0.15) |

| Equally important | (0.50,0.50,0.00) |

| Level | Level I | Level II | Level III | Level IV |

|---|---|---|---|---|

| Interval | [0, 0.25) | [0.25, 0.50) | [0.50, 0.75) | [0.75, 1.00] |

| Characteristics of Performance | Very low | Low | Relatively High | Very high |

| Weight of Criterion Layer B | Weight of Index Layer C | Comprehensive Weights |

|---|---|---|

| (0.117, 0.828) | (0.200, 0.743) | (0.023, 0.956) |

| (0.245, 0.709) | (0.029, 0.950) | |

| (0.256, 0.678) | (0.030, 0.944) | |

| (0.189, 0.746) | (0.022, 0.956) | |

| (0.153, 0.795) | (0.095, 0.833) | (0.015, 0.966) |

| (0.158, 0.762) | (0.024, 0.951) | |

| (0.087, 0.845) | (0.013, 0.968) | |

| (0.126, 0.794) | (0.019, 0.958) | |

| (0.154, 0.764) | (0.023, 0.952) | |

| (0.175, 0.744) | (0.027, 0.947) | |

| (0.289, 0.639) | (0.226, 0.675) | (0.065, 0.883) |

| (0.371, 0.520) | (0.107, 0.827) | |

| (0.257, 0.633) | (0.074, 0.868) | |

| (0.319, 0.599) | (0.192, 0.731) | (0.061, 0.892) |

| (0.110, 0.849) | (0.035, 0.940) | |

| (0.110, 0.848) | (0.035, 0.939) | |

| (0.111, 0.845) | (0.035, 0.938) | |

| (0.157, 0.772) | (0.050, 0.909) | |

| (0.163, 0.767) | (0.052, 0.906) |

| Method: Intuitionistic Fuzzy Analytic Hierarchy Process | Method: Analytic Hierarchy Process | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| B | C | Z1 | W1 | Z2 | W2 | Z2 × W2 | W3 | Z1 × W3 | Z1 | W1 | Z2 | W2 | Z2 × W2 | W3 | Z1 × W3 |

| B1 | C1 | 0.780 | 0.229 | 0.707 | 0.153 | 0.108 | 0.033 | 0.026 | 0.780 | 0.242 | 0.700 | 0.143 | 0.100 | 0.023 | 0.018 |

| C2 | 0.720 | 0.262 | 0.038 | 0.027 | 0.720 | 0.338 | 0.027 | 0.019 | |||||||

| C3 | 0.800 | 0.285 | 0.042 | 0.034 | 0.800 | 0.192 | 0.029 | 0.024 | |||||||

| C4 | 0.500 | 0.224 | 0.033 | 0.017 | 0.500 | 0.229 | 0.023 | 0.012 | |||||||

| B2 | C5 | 0.780 | 0.134 | 0.639 | 0.183 | 0.117 | 0.026 | 0.020 | 0.780 | 0.172 | 0.634 | 0.093 | 0.059 | 0.016 | 0.013 |

| C6 | 0.780 | 0.189 | 0.037 | 0.029 | 0.780 | 0.151 | 0.023 | 0.018 | |||||||

| C7 | 0.740 | 0.124 | 0.024 | 0.018 | 0.740 | 0.099 | 0.015 | 0.011 | |||||||

| C8 | 0.800 | 0.164 | 0.032 | 0.026 | 0.800 | 0.174 | 0.020 | 0.016 | |||||||

| C9 | 0.333 | 0.187 | 0.036 | 0.012 | 0.333 | 0.196 | 0.023 | 0.008 | |||||||

| C10 | 0.500 | 0.203 | 0.039 | 0.020 | 0.500 | 0.209 | 0.025 | 0.012 | |||||||

| B3 | C11 | 0.380 | 0.279 | 0.548 | 0.316 | 0.173 | 0.086 | 0.033 | 0.380 | 0.25 | 0.562 | 0.239 | 0.134 | 0.048 | 0.018 |

| C12 | 0.654 | 0.409 | 0.125 | 0.082 | 0.654 | 0.5 | 0.070 | 0.046 | |||||||

| C13 | 0.560 | 0.312 | 0.096 | 0.054 | 0.560 | 0.25 | 0.054 | 0.030 | |||||||

| B4 | C14 | 0.571 | 0.223 | 0.567 | 0.348 | 0.197 | 0.079 | 0.045 | 0.571 | 0.266 | 0.582 | 0.525 | 0.306 | 0.046 | 0.026 |

| C15 | 0.506 | 0.129 | 0.045 | 0.023 | 0.506 | 0.101 | 0.026 | 0.013 | |||||||

| C16 | 0.449 | 0.13 | 0.046 | 0.021 | 0.449 | 0.101 | 0.027 | 0.012 | |||||||

| C17 | 0.452 | 0.132 | 0.046 | 0.021 | 0.452 | 0.101 | 0.027 | 0.012 | |||||||

| C18 | 0.667 | 0.190 | 0.068 | 0.045 | 0.667 | 0.216 | 0.040 | 0.026 | |||||||

| C19 | 0.667 | 0.195 | 0.069 | 0.046 | 0.667 | 0.216 | 0.040 | 0.027 | |||||||

| A | 0.596 | 0.596 | 0.599 | 0.599 | |||||||||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, J.; Yu, L.; Gupta, R. Evaluating the Performance of the Government Venture Capital Guiding Fund Using the Intuitionistic Fuzzy Analytic Hierarchy Process. Sustainability 2020, 12, 6908. https://doi.org/10.3390/su12176908

Xu J, Yu L, Gupta R. Evaluating the Performance of the Government Venture Capital Guiding Fund Using the Intuitionistic Fuzzy Analytic Hierarchy Process. Sustainability. 2020; 12(17):6908. https://doi.org/10.3390/su12176908

Chicago/Turabian StyleXu, Jianjun, Lijie Yu, and Rakesh Gupta. 2020. "Evaluating the Performance of the Government Venture Capital Guiding Fund Using the Intuitionistic Fuzzy Analytic Hierarchy Process" Sustainability 12, no. 17: 6908. https://doi.org/10.3390/su12176908

APA StyleXu, J., Yu, L., & Gupta, R. (2020). Evaluating the Performance of the Government Venture Capital Guiding Fund Using the Intuitionistic Fuzzy Analytic Hierarchy Process. Sustainability, 12(17), 6908. https://doi.org/10.3390/su12176908