1. Introduction

The energy transition is one of the greatest political challenges of our time. The challenges not only lie in the technical implementation of the energy system transformation, but also in the carbon lock-in effects that come with the transformation of the energy system [

1,

2]. One aspect that has a strong impact on political decision-makers as well as on public acceptance are societal implications that result from the energy transition. Uncertainty about these implications may well be one of the greatest barriers to the rigorous realization of the energy transition in most countries. In this context, one of the most pressing issues is the change in industrial structures and employment that accompanies a change in technology. The discussion of the impact of new technologies on employment has been on the economic agenda ever since David Ricardo wrote [

3] his famous chapter “On Machinery” in the third edition of his Principles of Political Economy and Taxation in 1821. Therefore, the successful establishment of new industries in the technologies that are the drivers of the energy transition is of particular importance for political decision-makers [

4].

In order to monitor and assess the development of the renewable energy (RES) industry economic indicators like domestic demand and employment are essential. However, RES technologies as evolving cross-sectional technologies are not represented in official classifications of goods and industries so that no immediate information on the RES-sector employment can be found in official statistics. Therefore, gross employment effects must be derived by formal quantitative estimation methods.

A number of methods have been used so far in different countries and regions to determine gross employment in RES-technologies [

5,

6,

7,

8,

9]. Most of these approaches differ significantly in many ways. Cameron and Zwaan [

10], as well as Barros et al. [

11] give a good overview of the research that has been carried out regarding gross employment of RES-technologies. Aldieri et al. [

12] offers a recent overview of the wind energy sector. Furthermore, a classification conducted by Breitschopf et al. [

13] identifies three main approaches: (a) the employment factor approach, (b) the supply chain analysis and (c) the input–output modeling approach that help to improve the interpretation and comparison of RES-employment related work.

This paper aims to contribute to the scientific discourse on the effects of the energy transition in several ways. It will show four different methods using an input–output modeling approach that were applied to estimate the development of gross employment of the RES-industry in Germany between 2000 and 2018. The technology specific IO-vectors that were created from two of these approaches will be provided in the

supplementary material for further discussion and use in the research community. The vectors for the production and installation of RES technologies in Germany are based on primary data from company surveys. The vectors for the operation and maintenance of RES plants in Germany are based on questionnaire-based interviews with experts from companies active in the respective markets.

This paper focuses on the development of gross employment (direct and indirect employment), which reflects the employment attributable to the activities of the built-up and operation of renewable energy plants. Employment has been chosen as the main indicator representing economic activity connected to the built-up of the RES industry in Germany mainly for two reasons: (1) The total input requirements for labor calculated with the input–output approach encompass all stages of the value-added chain. (2) Employment is easier to comprehend and to communicate than other economic indicators like e.g., gross production or gross value added. Focusing on gross employment has some merits but also important drawbacks. Gross employment gives a broad picture of economic resources committed to facilitate the built-up of RES industry and to put it in perspective to other economic activities and the economy as a whole. With this it allows for the monitoring of the development of the RES industry due to the expansion of renewable energy technologies in a country. However, this approach neglects possible negative employment effects that are relevant from an economy-wide point of view, such as the budget or substitution effect. Therefore, this approach cannot inform about the overall economy-wide economic effects of the built-up of RES-industries. The balance of the economy-wide effects (positive and negative), generally called net effects, are essential to assess the advantageousness of economic policy measures e.g., the policy measures to foster the diffusion of RES technologies in Germany. This important strand of analysis is not addressed in this study. However, it should be noted, that the methods and results presented regarding gross employment form an indispensable set of information for studies on net employment effects (e.g., technology-specific IO-vectors). Based on the generated data set presented in this study, net employment effects have been analyzed in a series of studies [

14,

15,

16,

17,

18,

19]. The results hint to small, but under most assumptions, positive net employment effects induced by the expansion of RES-technologies in Germany.

Next to the methodological input, this study provides detailed insights into the developments of different RES-sectors in Germany and the role of different areas of business activity. It contributes a set of economic indicators over a period of almost 20 years for the RES-industry in Germany, starting from the status of infant industry to a mature, consolidating industry that can be used for further analysis (detailed data-sheets are provided in the

supplementary material). The overall comparability of the gross employment figures between years is provided by adjustments to the IO-vectors for each year according to the official input-tables for Germany.

Altogether, this study aims to shed insights in the determination of gross employment effects of RES in Germany in order to improve the understanding and transparency of figures communicated by the German government. In addition, it aims to improve the discrepancy that most literature on RES-employment has not been published in peer-reviewed journals [

10] and therefore often does not contribute to the global academic discourse. The hope is that a better understanding of German employment figures will improve the comparison done in other publications, such as IRENA [

20] as well as EurObserv’ER [

21]. The overall intention is to provide data-driven, methodologically sound input for the political debate on economic implications of the support of new technologies over a comparably long period of investigation.

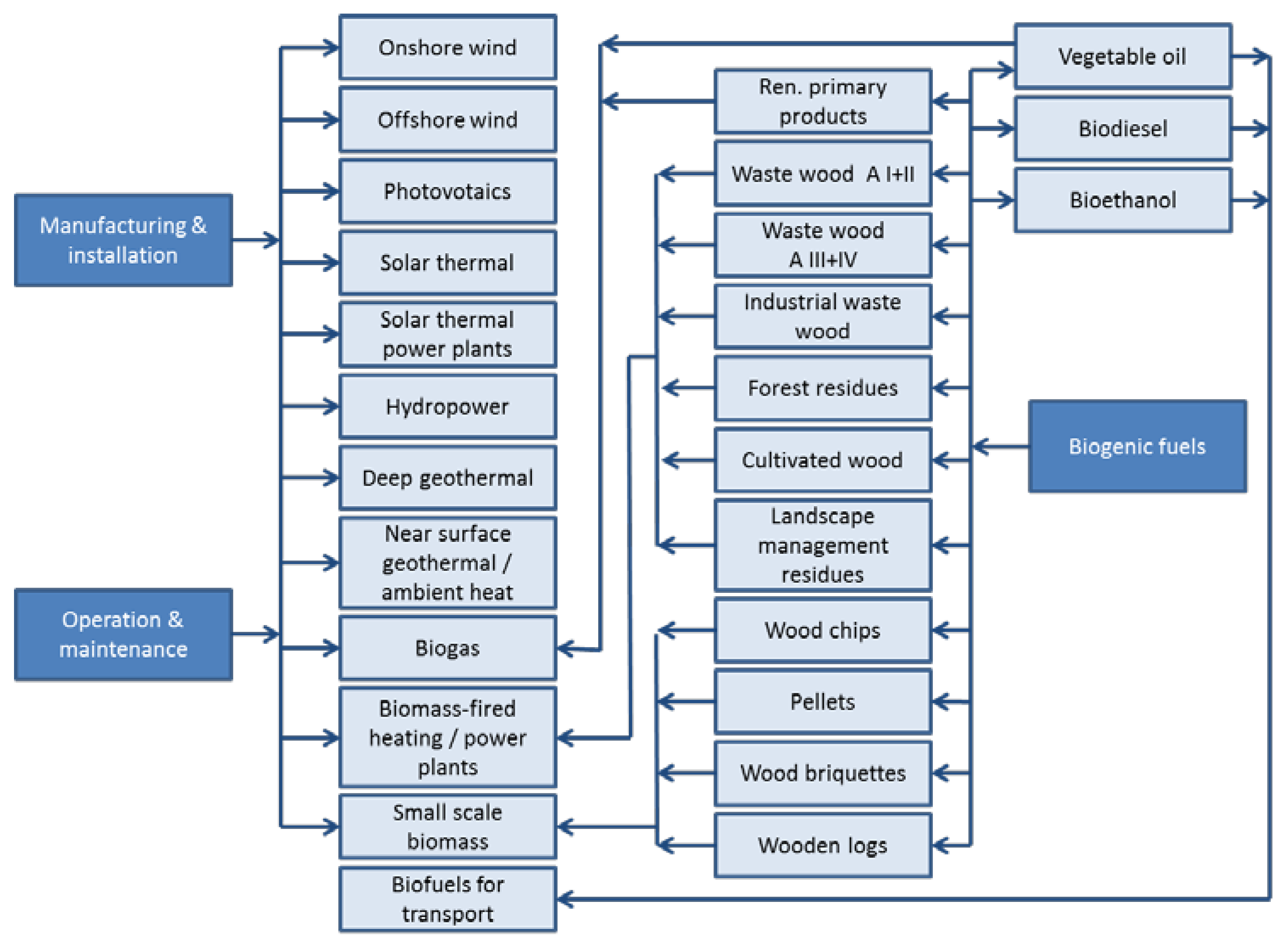

Three different areas of entrepreneurial activity will be taken into consideration—the manufacturing and installation of new RES-capacities, the operation and maintenance of existing RES-capacities, as well as the provision of biogenic fuels for stationary plants and the transport sector. Regarding the technological differentiation of RES-plants, 12 different sectors have been taken into consideration; eight power technology sectors, three heat technology sectors and one transport sector (see

Figure 1). The sectors that cover the eight power technologies also include combined heat and power technologies (wind onshore, wind offshore, photovoltaics, solar thermal power plants, hydropower, deep geothermal, biogas including installations for the use of liquid biomass, biomass-fired heating/power plants). The only sector that also includes pure heat technologies is the one for biomass-fired heating/power plants. The reason for this aggregation lies in the structure of the industry. The differentiation of this sector was not feasible as the companies providing the technologies are the same. However, three more technologies that are only used for heating purposes could be distinguished from their respective counterparts for electricity generation—solar thermal, near surface geothermal/ambient heat and small-scale biomass. For all these 11 sectors, manufacturing and installation are considered. In addition, operation and maintenance have been taken into account for 10 out of the 11 sectors. As solar thermal power plants are not built in Germany, due to the low solar irradiation, operation and maintenance are not relevant for this sector in Germany. The provision of biogenic fuels for the operation of biomass applications has also been taken into consideration for a wide range of different biomass fractions. Renewable primary products like corn are taken into consideration as input for biogas plants. Vegetable oil is used in installations for the use of liquid biomass. Different kinds of waste wood, forest residues, cultivated wood, and landscape management residues are taken into consideration for biomass-fired heating/power plants. Wood chips, pellets, wood briquettes and wooden logs have been considered for the use in small scale biomass technologies. Besides the 11 power and heat technology sectors one sector is specifically aimed at the transport sector—biofuels for transport. This sector only covers the provision of biogenic fuels and includes vegetable oil, biodiesel and bioethanol.

Section 2 describes the methodology as well as the data used to determine the employment in the various RES-sectors. In

Section 3 the time series of employment, as well as other economic indicators, will be presented. In addition, some background information will be provided that explains the developments. The discussion in

Section 4 will provide a summary of the methodological conclusions as well as conclusions on the development of the RES-industry in Germany.

3. Results

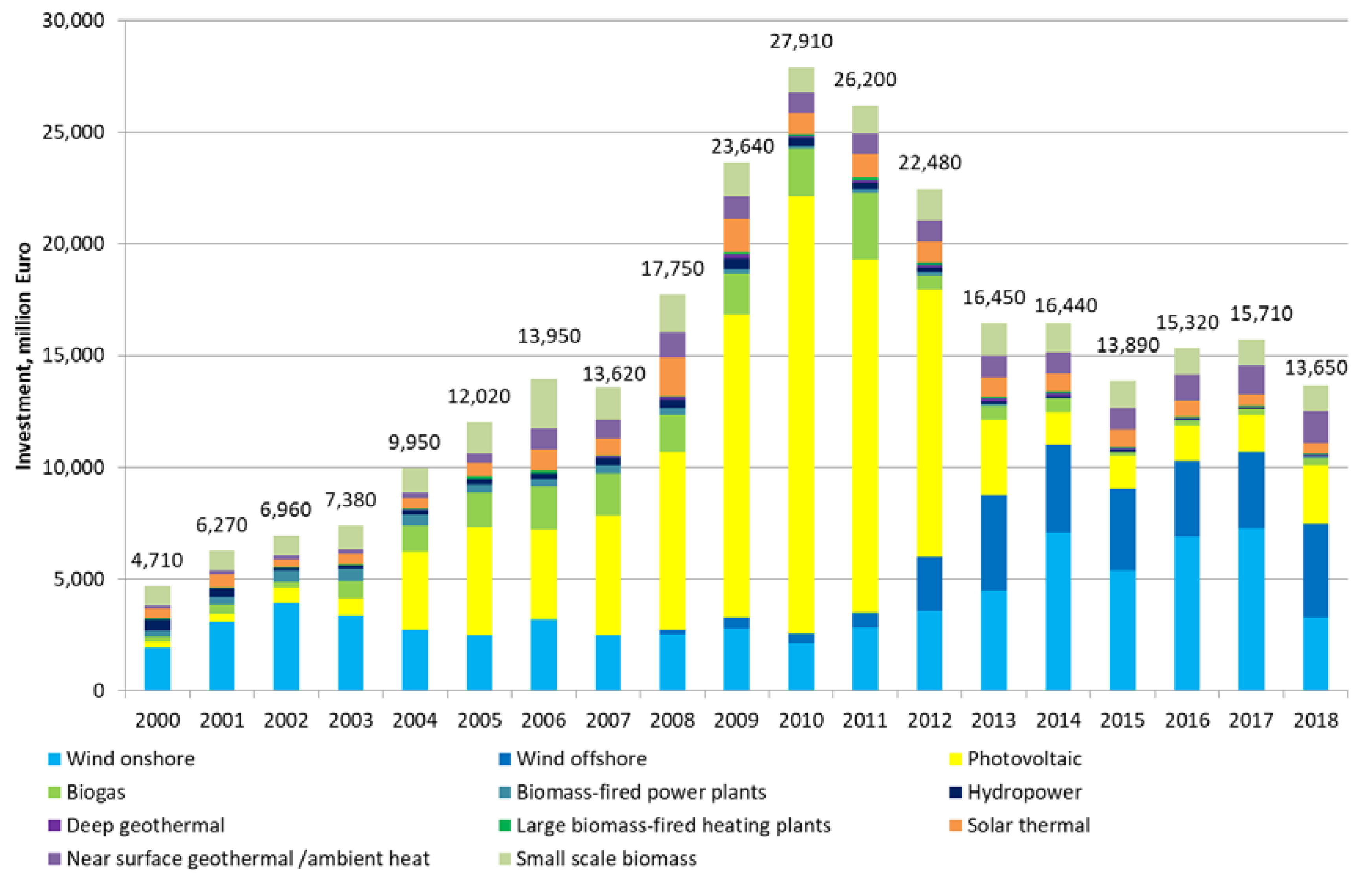

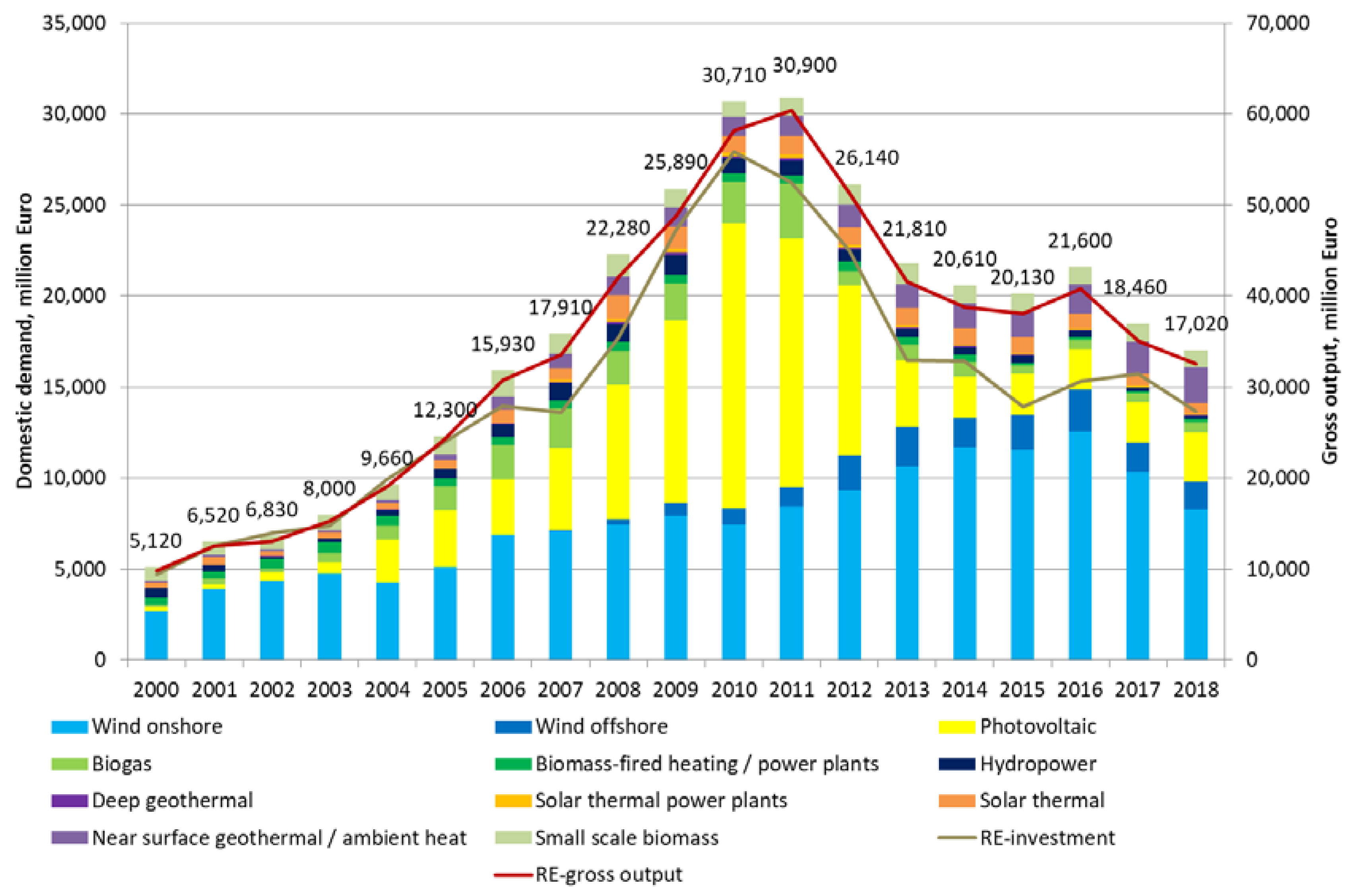

The development of RES-technologies in Germany can be observed from the investment undertaken (see

Figure 4). These investments were strongly driven by market-pull instruments [

44,

45]. Especially the Renewable Energy Sources Act (EEG) for RES-power generation systems that was introduced in 2000 as well as its predecessor the “Stromeinspeisegesetz” from 1991 had a strong effect on the German RES-market development. More than 81% of the investments in RES-technologies between 2000 and 2018 were in electricity generation technologies, most of which were within the scope of the EEG. Only about 19% of the investment could be allocated to technologies exclusively used for heating. The ones that were eligible under a promotion scheme were primarily supported via the Market Incentive Program, which facilitates investments via state subsidies. As this program is dependent on the national budget, this support mechanism has proven to be not as stable as the EEG, which is paid by a levy from the electricity customers.

This instability was experienced in May 2010 when an unexpected budget freeze was imposed on the Market Incentive Program. However, this budget freeze was maintained for less than two and a half months, the investment momentum in the heating sector was slowed down with a lasting effect. As a result, some manufacturers of RES-heating systems have tried to become independent of government market support schemes in order to achieve a more stable development in demand.

In the field of RES-power generation plants, the EEG has been a comparatively reliable support framework for many years. However, this legal framework has also led to a number of uncertainties, which are reflected in the development of RES-investment. Over the course of time, it has repeatedly been possible to observe an increase or decrease in investment activity triggered by changes in support under one of the seven amendments of the EEG. One example is the biogas sector. The prospect of an improvement in support conditions in mid-2008 led to a postponement of investments in this sector. In 2011, on the other hand, investments were brought forward, as deterioration in support conditions was to be expected. Another example is the PV sector. Even though PV would be expected to have the highest installation rates during the summer due to weather conditions, its yearly peak was found to be in December shortly before the digression of the feed-in tariffs [

46]. Therefore, it can be said that investments in a market backed by support instruments present the industry with the challenge of dealing with constantly changing market conditions and developments.

Altogether more than 284 billion euros was invested in RES-technologies in Germany in the period between 2000 and 2018. The major amount went into photovoltaics as well as wind energy technologies, which accounted for a share of 35% each (approx. Euro 100 billion).

Yearly investments in RES-technologies in Germany increased continuously in the period from 2000 to 2010 with the exception of 2007. The main driver for the sharp increase in investments was photovoltaics (PV), which nearly quadrupled its investment volume. Between 2011 and 2013, there was a significant reduction in investments, again primarily related to the PV-sector. In 2011 and 2012, this development was exclusively attributable to the sharp decline in this technology’s specific investment costs, while installations remained at an all-time high of about 7–8 GW. In contrast, just under one-third of the installed capacity of the previous year was added in 2013. A similar course of investment activities, albeit at a much lower level, could be observed in the biogas sector during this period. However, the significant increase in investment in the offshore wind sector prevented the decline in total investment between 2012 and 2013 from being even more dramatic. Overall, investments have been comparatively stable since 2013 at a level between 14 and 16 billion euros.

The domestic demand for RES-plants and components in Germany derived from investments and foreign trade is shown in

Figure 5. All-in-all, just under 338 billion euros could be determined for the years 2000 to 2018. The largest share of domestic demand with about euros 161 billion (48%) was provided by the wind sector, followed by the PV-sector with 86 billion euros (25%).

Starting from around 5 billion euros in 2000, domestic demand for RES-installations rose to just under 31 billion euros in 2010 and 2011. The decline, mainly induced by the developments in the PV-industry between 2011 and 2013, resulted in a domestic demand of around 21 billion euros annually between 2013 and 2016. In 2017/2018, there was a further decline in domestic demand to around euros 17 billion euros.

Gross output, which is determined via the IO-framework, was almost twice as high as domestic demand over the whole time period under consideration.

Comparing

Figure 4 and

Figure 5, a difference in the technological representation becomes apparent. The sectors of biomass-fired power plants and large biomass-fired heating plants that are individually represented in

Figure 4 are combined into one sector in

Figure 5. As mentioned before, this is due to the industrial structure of this technology, which does not allow a differentiation between the electricity and heat sector. In addition, the sector of solar thermal power plants appears in

Figure 5, which is not taken into consideration in

Figure 4 since there are no investments in this technology in Germany.

Comparing the development of domestic demand and the development of investments in renewable energy plants in Germany, the overall development pattern appears to be quite similar. Differences are mainly based on shifts between domestic and foreign demand. While investments declined slightly between 2006 and 2007, companies were able to realize further growth in exports, which led to an increase in domestic demand in 2007. Exports were still able to offset the decline in investments in 2011, whereas from 2012 onwards, a consolidation took place, which affected the PV and biogas sectors in particular. Investments in Germany rose from 2016 to 2017, while domestic demand declined. This development is attributable to a significant decline in exports in 2017, which could not be offset by the increase in investments.

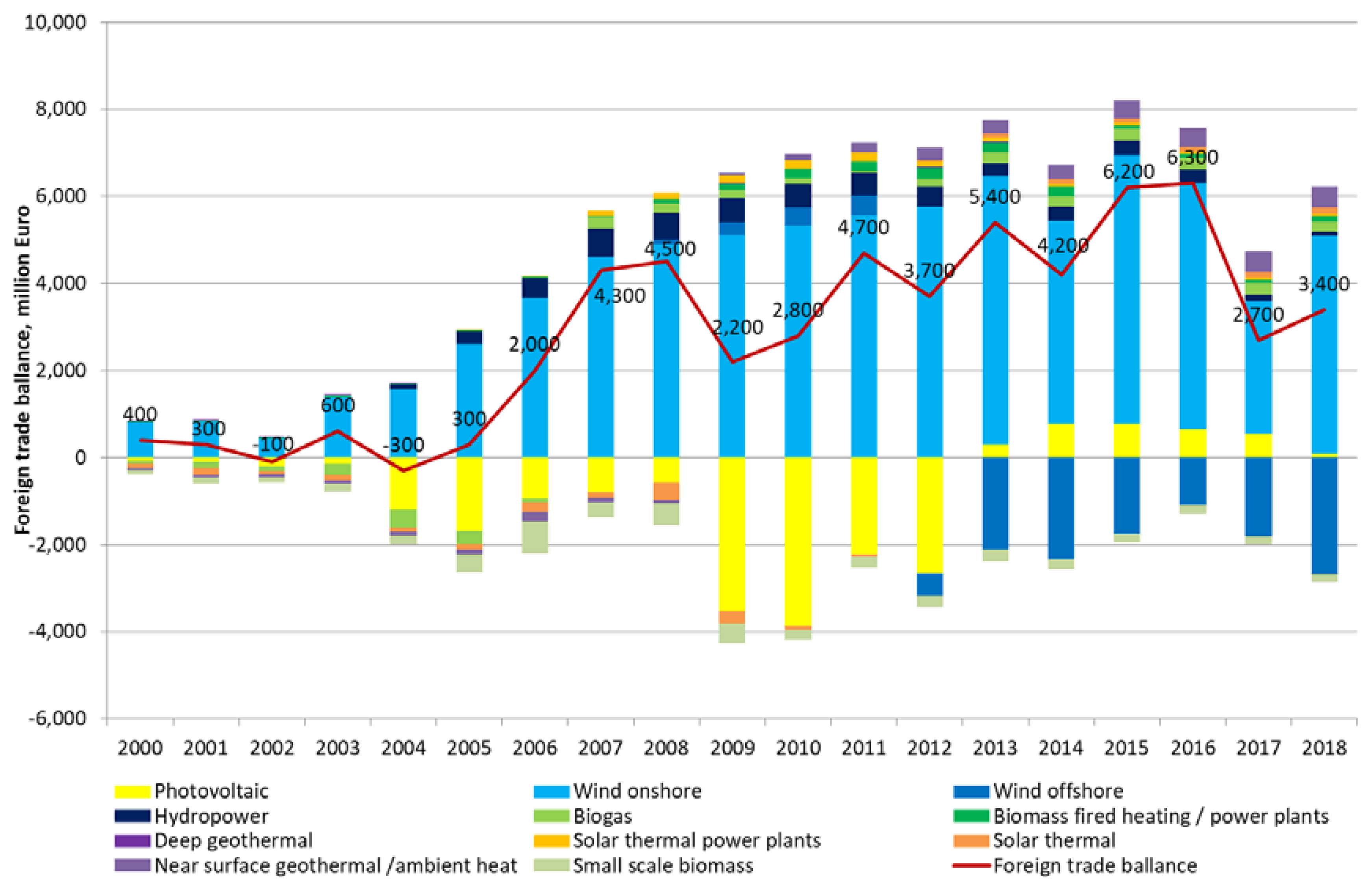

A closer look at foreign trade shows that there were more exports in the period under review than direct imports of RES-systems on the German market (see

Figure 6). Overall, foreign trade surplus totaled to around 53.5 billion euros in the period between 2000 and 2018. It also becomes clear that the annual surplus has risen over time to a high of over 6 billion euros per year, whereas at the beginning of the period (2002 and 2004), it was hardly relevant, if not negative.

It should also be noted that the foreign trade figures shown here only include imports of end products, whereas on the export side, intermediate products are included as well. However, imports of intermediate products are considered within the IO-framework and are therefore taken into account in the determination of employment.

The technology-specific illustration in

Figure 6 shows which technologies had positive and negative foreign trade balances over time. In the PV-sector, the trade balance from 2000 to 2012 was consistently negative, which shows that Germany did not have sufficient production capacity to meet domestic demand. The sharp decline in the yearly installed capacity in the period between 2012 and 2014 led to a foreign trade surplus in recent years. This surplus was mainly driven by the strong position of German inverter manufacturers whereas many PV module manufacturers were forced to leave the market.

In addition to the PV sector, there are a number of other RES-sectors with trade deficits. Particularly striking is the deficit in offshore wind energy, which is influenced in particular by the strong market position of Siemens with its production facilities in Denmark. The trade deficits in various heating technologies can be partly explained by the historically strong role of other countries in this segment, such as Austria.

Over time, trade surpluses were achieved in almost all sectors in Germany, again not taking imports of intermediate products into consideration. The only ones that continue to have negative trade surpluses are the offshore wind and small-scale biomass sector.

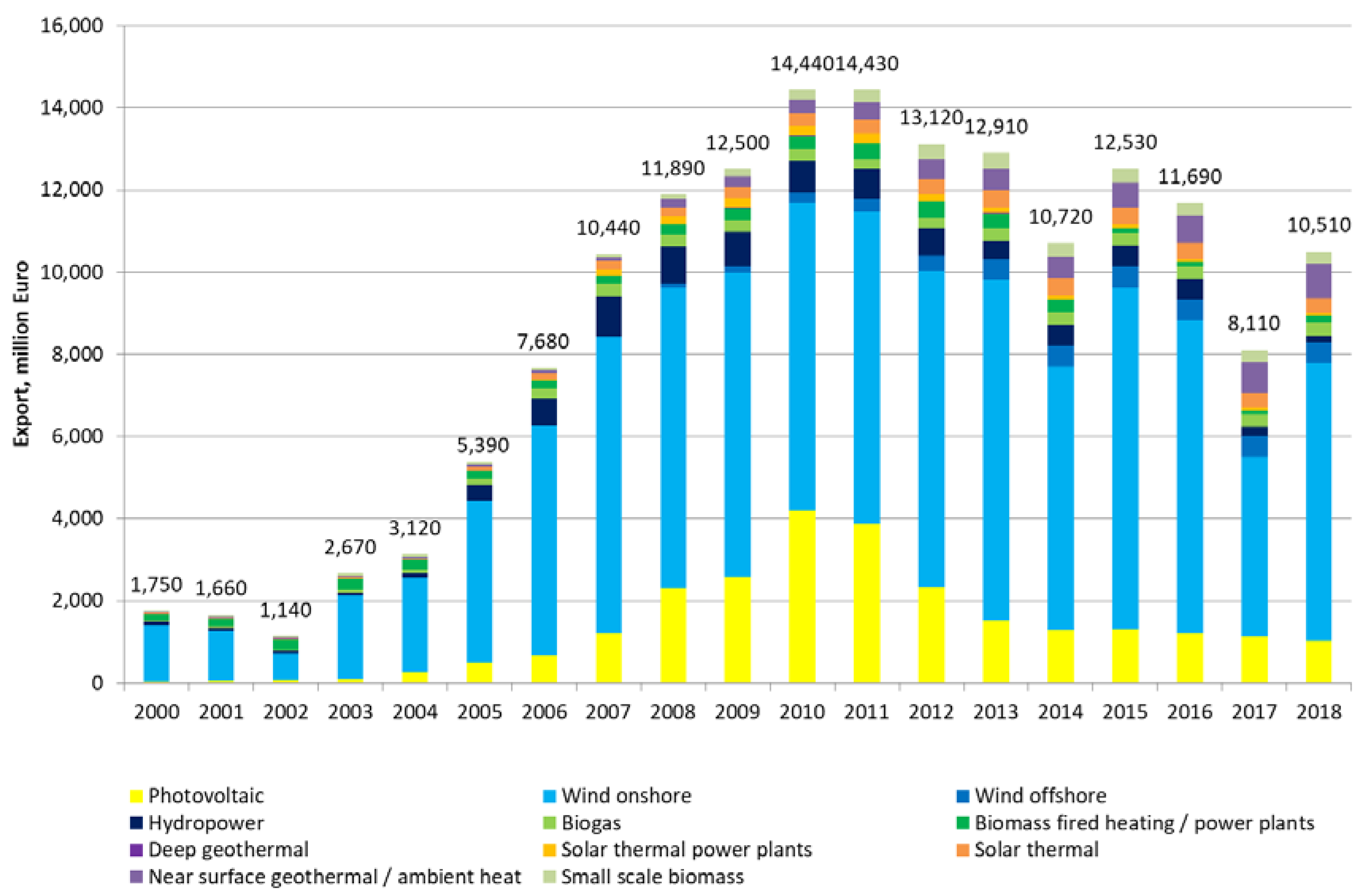

In terms of exports, the onshore wind energy sector stands out (see

Figure 7). The decline in exports in 2014 has to be seen in context with the development of domestic investments. In 2014, investments in onshore wind capacities in Germany increased significantly compared to the previous year. Therefore, it can be assumed that exports declined in order to serve the domestic market. The development over the next two years suggests that wind production capacities in Germany were expanded. In 2017, German exports in the wind energy sector fell significantly by 43% [

32]. At first glance, this export trend appears to be surprising. According to international statistics, the worldwide development in the construction of wind turbines was slightly declining in 2017, but the development in Europe was clearly positive [

47]. However, a closer analysis of the foreign trade statistics reveals that German companies have played a relatively small role in the largest growth market of 2017, the United Kingdom. On the other hand, other markets, in which German companies have been very successful in prior years, experienced a significant market downturn in 2017. The most important example in this context is Turkey.

The decline in exports in the PV-sector since 2012 has two reasons. First, it is attributable to the consolidation of the German PV industry, and second, it reflects the decline in the European PV market.

A steady increase in exports can be observed in most other RES-sectors. It clearly shows the economic development of this infant industry. Initially, strongly focused on the domestic market, it has diversified its markets over time with various export strategies. This also becomes evident in an analysis of the results of the company surveys. In the course of time, an increasing share of companies declared to export its products. At the same time, the average export quota rose in all RES-sectors. In addition, the number of companies establishing production sites in other countries also increased over time.

Overall, exports of RES-plants and components rose from a level below 2 billion euros in the period from 2000 to 2003 to a peak at around 14 billion euros in 2010 and 2011.

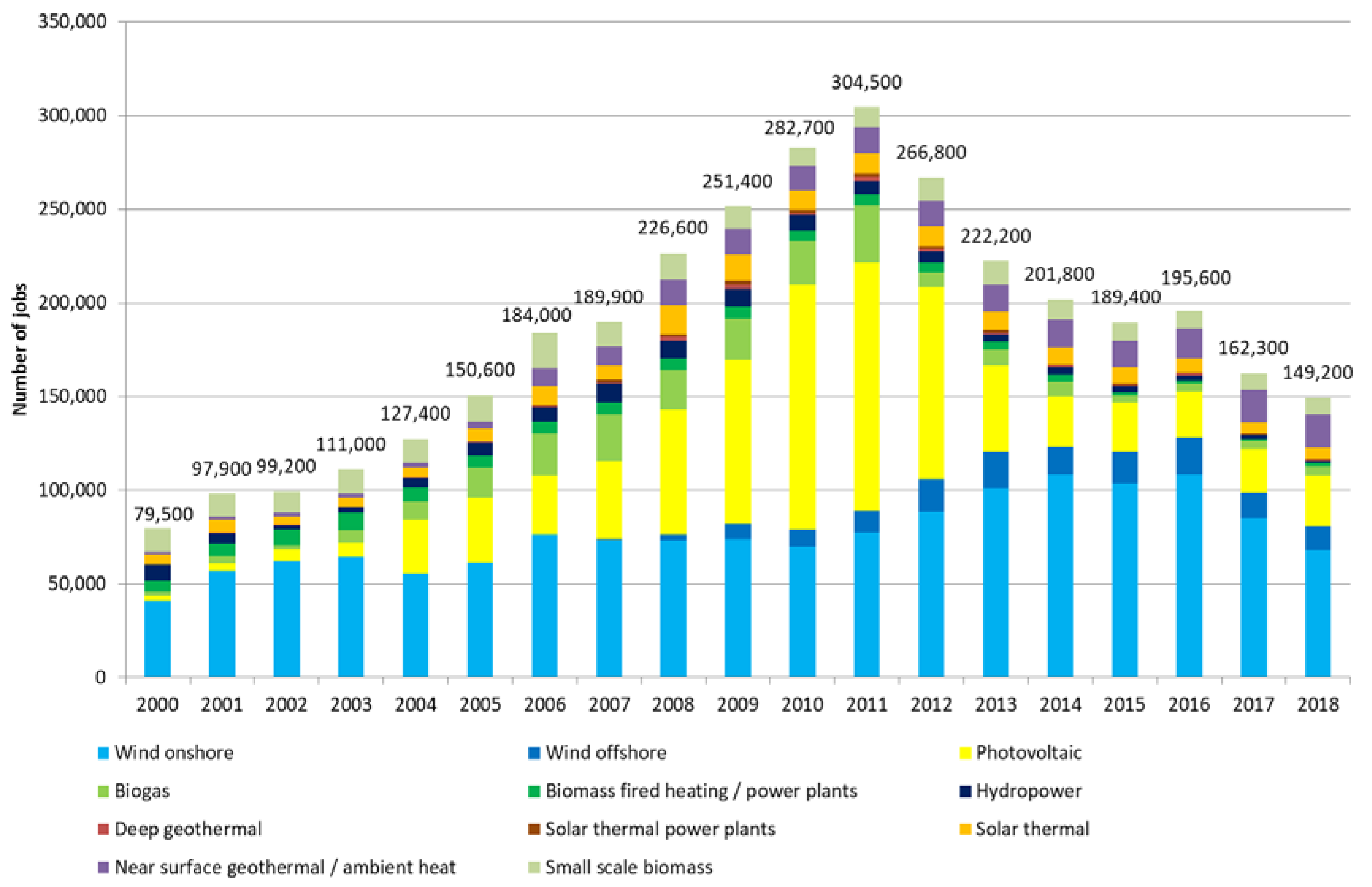

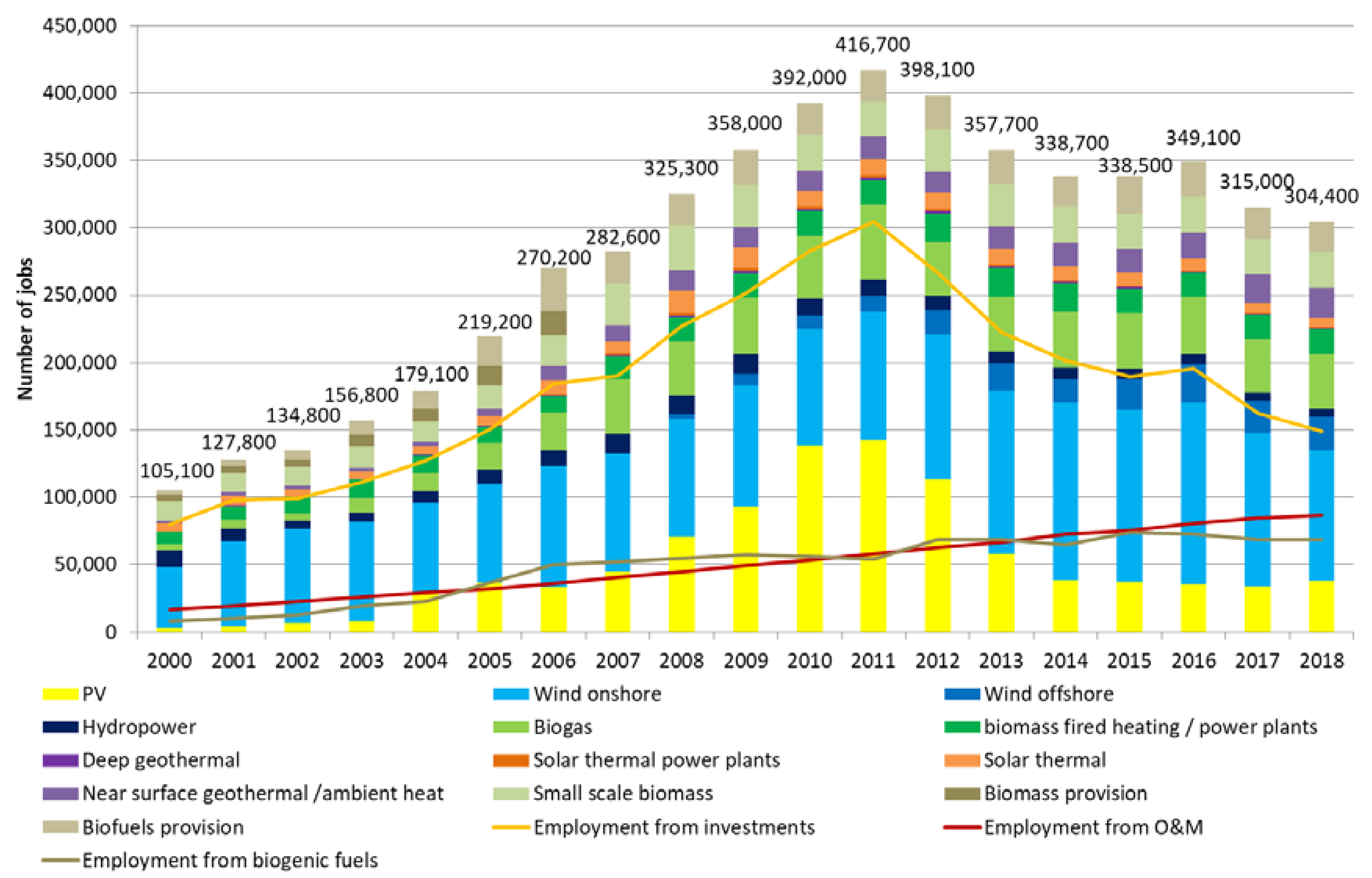

The employment resulting from investments in installations for the use of renewable energies in Germany and abroad is displayed in

Figure 8. Starting from around 79,500 jobs in 2000, employment rose to 304,500 in 2011. In the following three years, employment fell by around one third. In 2016 there was a slight increase, followed by yet another decline. In 2018 about 149,200 jobs were determined in the context of investments in RES-technologies.

A comparison of the development of employment with the development of domestic demand reveals a difference in the development of both indicators, which requires a more detailed explanation. The significant increase in employment between 2010 and 2011 was accompanied by only a slight improvement in domestic demand. This discrepancy can be attributed to specific developments in the PV-sector that were previously mentioned. In Germany, PV system prices were on average 24% lower in 2011 than in the previous year and domestic demand in this sector declined by about 13%. In contrast, newly installed capacity in Germany rose by another 470 MW compared with the previous year (+6%), as did the production of modules, cells and inverters [

41]. Furthermore, an analysis of corporate communications revealed that there were no significant reductions in the number of employees in 2011. It was therefore assumed that the decline in domestic demand was not fully reflected in employment in 2011. Instead, it had a significant impact on company results [

29]. In 2012, this development led to a consolidation of the German PV industry, as many companies were unable to adequately meet the further strong decline in prices.

The increase in employment in 2011 is therefore primarily attributable to the fact that employment in photovoltaics rose slightly despite declining gross production. In addition, many other sectors, such as onshore and offshore wind energy, biogas and all heating technologies, also reported growth. The year 2012 was then marked by massive reductions in employment in the PV sector and the biogas sector. In the PV sector, this development was further reinforced in 2013 by the strong decline of domestically installed capacities by 68% compared to the previous year.

Looking at the development of the RES-sector as a whole, another important aspect becomes apparent. Operation and maintenance (O&M), as well as the provision of biomass and biogenic fuels have had a stabilizing effect on the employment in the RES-sector (see

Figure 9).

Employment in operation and maintenance is not as much influenced by annual fluctuations in the addition of new capacities as the manufacturing and installation of RES-plants. Only its development is directly linked to the net additions of RES-capacities, while the majority of the economic basis remains stable over time. However, once again, it should be pointed out that employment in the O&M sector has also shown increases in labor productivity, which are taken into account.

With regard to the provision of biogenic fuels, there are some more uncertainties than in the area of O&M. Due to existing installation, the demand for biomass products is relatively stable which is a major advantage over the plant manufacturing sector. However, many biomass products are subject to an international market, which may affect the development of employment in this area due to exports and imports. Overall, it can be assumed that the employment development in this sector will be more even than in the business area of investments.

Employment resulting from O&M and the provision of biogenic fuels has been less relevant in the past. However, these areas are gaining importance and employed just over half of the people in the RES-industry in Germany in 2018. Nevertheless, the main driver of the development so far has been the investment in new RES-installations. The fluctuations in the development of the overall RES-employment are almost exclusively attributable to them.

4. Discussion

Data regarding the development of new technologies and their industries cannot be found in official statistics. Therefore, approaches are needed to derive a reasonable estimate of economic indicators in order to assess the development of those emerging industries.

A methodological approach that allows for the determination of direct and indirect employment uses country-specific input–output tables. The work presented in this study shows that there are many different possibilities to apply the input–output (IO) modeling approach. Four different methods were chosen here to determine gross employment for the renewable energy (RES) industry in Germany. The approaches differ significantly in their complexity and the associated data and information requirements.

- (1)

The most complex approach described in this study involves the development of specific IO-vectors based on company surveys. This approach is particularly appropriate when an industry is characterized by newly created enterprises that play only a minor role in the relevant IO-vectors of the conventional classification. With regard to the required business surveys, however, it must be taken into account that a high degree of transparency and effort is required from companies to obtain adequate data on the flow of intermediate goods. Therefore, this approach should be based on a clear benefit and support of the industry under investigation.

- (2)

A less elaborate way to extend an IO-table with a new vector was chosen for the operation and maintenance of RES-plants. The new IO-vectors were derived by a recombination of existing IO-vectors taking into account the specific costs structure of the service under investigation. This approach follows the assumption that the intermediate goods and services purchased by the new sector do not differ significantly from the representation of the relevant IO-vectors in the conventional classification. The quality and reliability of results can be improved when questionnaire-based interviews with relevant actors and experts are used in the data generation process.

- (3)

The third approach using the IO-table without actively extending it is closely related to the second method. It recombines existing IO-vectors by taking the specific costs structures into consideration. The main difference is that no new vector is created, but the domestic demand of the good under consideration is divided between the different vectors. This approach was taken for the provision of biogenic fuels. This approach is particularly useful when there is no further use for a new vector and a variety of different goods are to be considered.

- (4)

The simplest approach to estimate employment in a sector using the IO approach is to apply domestic demand directly to an existing IO-vector. This was done in the case of the provision of biomass in the early years of the time under investigation. However, the labor coefficient was rescaled by a factor for the sector “Products of agriculture, hunting and related services”, as the production of “energy plants” requires less labor input than the average product portfolio of agricultural products.

All of the approaches described using the IO-methodology, require detailed data from other sources. Even the simplest approach was in need of information regarding labor intensity from detailed agricultural statistics in Germany. The availability of this detailed information is, therefore, crucial in order to apply the IO-methodology to specific technologies and their industries.

Overall, it can, therefore, be concluded that there can be considerable methodological differences in the determination of economic indicators using the IO-approach. Therefore, different studies using the IO-methodology for the same country or region may vary significantly. This may also be true for two studies using the same approach based on different data sources.

Moreover, the data required for the different IO-approaches is very country-specific, as are the IO-tables. The transferability to other countries as well as the comparability of results from studies of different countries is therefore limited.

Another aspect is the development stage of the industry under consideration. Results have shown that labor intensity and its development strongly depends on the development phase in which an industry is at the time of the analysis. This can vary considerably from one country to another. Another aspect is the possibility of unexpected labor productivity developments. In the case of the drastic price adjustments of PV modules, for example, there was a temporary decline in labor productivity in Germany. The results of these short-term, special circumstances do not apply to other phases and industries, which once again makes transferability of results a challenge.

5. Conclusions

The results of the determination of the development of gross employment in the RES-industry in Germany show the relevance of different areas of business activity. It particularly shows the importance of investments and installations on gross employment in the early years of the development and the growing relevance of operation and maintenance as well as the provision of biogenic fuels in the later stages of the energy transition.

For the overall development of the German RES-industry, the wind onshore and PV industries have both played the most important role. At the same time, the two sectors have shown very different developments.

The wind energy industry has experienced a relatively reliable domestic market that did not show any radical developments in the time under consideration. The major share of onshore wind installations in Germany was provided by wind companies with production sites in Germany. Over the course of time, the German wind industry managed to develop a strong export orientation, which helped to overcome fluctuations in domestic demand.

On the other hand, the German PV-sector has experienced a substantial expansion, driven by domestic demand that was followed by a consolidation within a few years. Imports of PV-cells and–modules were necessary at all times to meet domestic demand. Moreover, the German PV sector’s overall trade balance has been negative over a large part of the time span considered here. Exports were also used as a stabilizing factor by the PV-industry. However, the German PV-sector did not develop the same export orientation as the wind sector. One possible explanation is the strong expansion of domestic demand. Another reason may have been the low volume of other markets in the early years of our investigation period. Between 2002 and 2010, the German PV market accounted for a share of the global expansion, ranging from 30% to 68% annually.

However, these differences only provide first insights into the developments of these RES-sectors in Germany. Further research into these industries on a global level is needed to gain a better understanding of the role of national and international markets.

This study shows that the expansion of RES-technologies in Germany was accompanied by a substantial buildup of an evolving industry that supplies investment goods, which were used for the installation of domestic and foreign RES facilities. Domestic installations paved the way for increasing demand for employment in operation and maintenance as well as the provision of biofuels.

It is widely discussed that gross employment effects are not sufficient to describe the overall employment effects of RES-expansion as other effects such as budget or substitution effects are not taken into account (see also [

15,

17,

48]). The authors of this study are in total agreement with those arguments. Therefore, no statement can be made about the positive or negative effects of the transition towards the use of RES in Germany based directly on this publication. However, as argued in the introduction to this study, we still believe that analyzing gross employment effects has merits in and of itself as it gives a comprehensive picture of the economic relevance of the evolving RES industry in Germany. In addition, we would argue that the research presented generates valuable information for investigation of net effects of the RES expansion as is demonstrated in studies based on our data set [

14,

15,

16,

17,

18,

19].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}